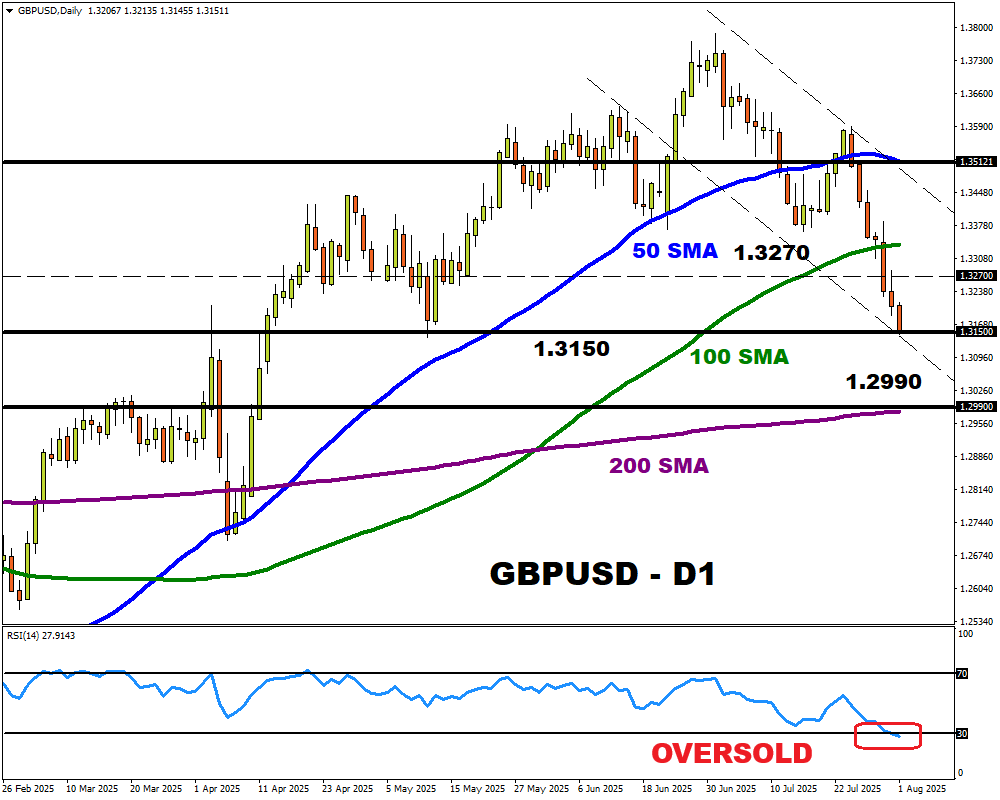

By JustMarkets

As of Tuesday’s close, the Dow Jones Index (US30) declined by 0.14%. The S&P 500 Index (US500) fell by 0.49%, and the tech-heavy Nasdaq (US100) ended lower by 0.65%. The US stocks closed lower on Tuesday as investors grappled with disappointing economic data, escalating trade tensions, and mixed corporate earnings. Stagflation concerns resurfaced after the ISM Services Index showed activity stalled in July. Meanwhile, President Trump’s threats to impose steep tariffs of up to 250% on pharmaceutical imports, along with potential tariffs on semiconductors, heightened market anxiety amid ongoing trade uncertainty with India, Switzerland, and China. On the earnings front, Palantir rose by 7.8% after raising its revenue expectations, while Pfizer gained 5.2% following a strong quarterly report.

In June 2025, Canada’s trade deficit widened to CAD 5.9 billion (seasonally adjusted), up from the revised figure of CAD 5.5 billion in the previous month. Imports increased by 1.4% from a six-month low to CAD 67.6 billion, marking the first increase in four months. Exports to the US, subject to sectoral and country-specific tariffs, rose 3.1% from the previous month but remained 12.5% lower year-over-year.

European stock markets mostly rose yesterday. Germany’s DAX (DE40) gained 0.37%, France’s CAC 40 (FR40) closed down 0.14%, Spain’s IBEX35 (ES35) rose by 0.15%, and the UK’s FTSE 100 (UK100) closed up 0.16%. The DAX in Frankfurt gave up early gains and closed 0.4% higher on Tuesday as investors continued to monitor earnings season and trade developments, with US tariffs set to take effect on August 7. Under the US-EU deal, most EU exporters will face a unified 15% US tariff — half the 30% Trump had previously threatened. In return, the EU pledged to lower its own tariffs on certain goods and boost energy imports from the US by $750 billion over the remaining three and a half years of Trump’s presidency. However, Trump warned he could impose 35% tariffs on the EU if Brussels fails to meet its $600 billion investment commitment in US infrastructure.

WTI crude oil prices rose above $65 per barrel on Wednesday, snapping a four-day losing streak and rebounding from a five-week low amid supply disruption concerns. Investors assessed potential supply interruptions, as India may reduce imports of Russian oil in response to President Trump’s tariff threats over continued purchases. Trump warned of raising tariffs on Indian goods within 24 hours to pressure Russian President Vladimir Putin to end the war in Ukraine. Additional support for bulls came from API data showing a 4.2 million barrel drop in US crude inventories last week, exceeding market expectations of a 1.8 million barrel decline and signaling stronger-than-expected demand.

Silver held near $37.8 per ounce on Wednesday after rising for three straight sessions, supported by growing expectations of Federal Reserve rate cuts. The latest ISM Services PMI for July pointed to sluggish growth, a decline in employment, and persistent price pressures, reinforcing signs of labor market cooling after last week’s weaker-than-expected payroll report. Markets are now pricing in two Fed rate cuts by year-end, with the first potentially in September.

Asian markets mostly rose yesterday. Japan’s Nikkei 225 (JP225) gained 0.64%, China’s FTSE China A50 (CHA50) increased by 0.94%, Hong Kong’s Hang Seng (HK50) rose by 0.68%, and Australia’s ASX 200 (AU200) posted a strong performance, up 1.23%.

The Reserve Bank of India (RBI), at its August meeting, held the key repo rate steady at 5.50%, maintaining a neutral stance after cutting the rate by 50 basis points in June, more than usual and in line with expectations. The rate remains at its lowest level since August 2022. The decision came amid easing inflation and the recent US announcement of 25% tariffs on Indian imports. On the economic outlook, the RBI maintained its GDP growth expectations at 6.5% for the 2025/26 fiscal year and 6.6% for the following year. Meanwhile, inflation expectations were revised downward to 3.1% from 3.7%, remaining within the RBI’s target range of 2-6%.

Vietnam’s annual inflation rate fell to 3.19% in July 2025 from 3.57% in June, marking the lowest level in three months. Meanwhile, core inflation, excluding volatile items, slowed to 3.30% in July from 3.46% in June, also a three-month low. On a monthly basis, consumer prices rose by 0.11%, down from a 0.48% increase in the previous period.

In June 2025, the unemployment rate in New Zealand rose to 5.2%, which is slightly higher than the previous figure of 5.1% and in line with market expectations. The number of unemployed increased to 158,000 people compared to 156,000 in March, representing an annual increase of 16,000 people, or 11.1%. This data indicates growing slack in the labor market, putting pressure on policymakers as economic dynamics continue to weaken.

S&P 500 (US500) 6,299.19 −30.75 (−0.49%)

Dow Jones (US30) 44,111.74 −61.90 (−0.14%)

DAX (DE40) 23,846.07 +88.38 (+0.37%)

FTSE 100 (UK100) 9,142.73 +14.43 (+0.16%)

USD Index 98.76 −0.03 (−0.03%)

News feed for: 2025.08.06

- New Zealand Unemployment Rate (q/q) at 01:45 (GMT+3);

- Japan Average Cash Earnings (y/y) at 02:30 (GMT+3);

- Eurozone Retail Sales (m/m) at 12:00 (GMT+3);

- US Crude Oil Reserves (w/w) at 17:30 (GMT+3).

By JustMarkets

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

Trees like these in Boston can help keep neighborhoods cooler on hot days.

Trees like these in Boston can help keep neighborhoods cooler on hot days.