By RoboForex Analytical Department

The EUR/USD pair tumbled to 1.1569 on Friday, propelling the US dollar to a two-month high. The rally comes as investors retreat from both the euro and the yen, which have lost their appeal.

The yen has depreciated roughly 4.0% against the dollar since Sanae Takaichi won the race to become Japan’s next prime minister. Markets are anticipating an expansion of fiscal stimulus and a continuation of accommodative monetary policy under the new leadership.

Meanwhile, the euro has weakened by approximately 1.5%, pressured by political instability in France. President Emmanuel Macron is now seeking his sixth prime minister in just two years, creating significant uncertainty.

In the United States, the government shutdown has entered its ninth day. This has delayed the release of key macroeconomic data, leaving markets without crucial information to assess the Federal Reserve’s policy outlook.

Market pricing currently indicates a 95% probability of a 0.25 percentage point interest rate cut in October. However, the likelihood of a subsequent easing in December has fallen to 80%, down from 90% a week ago.

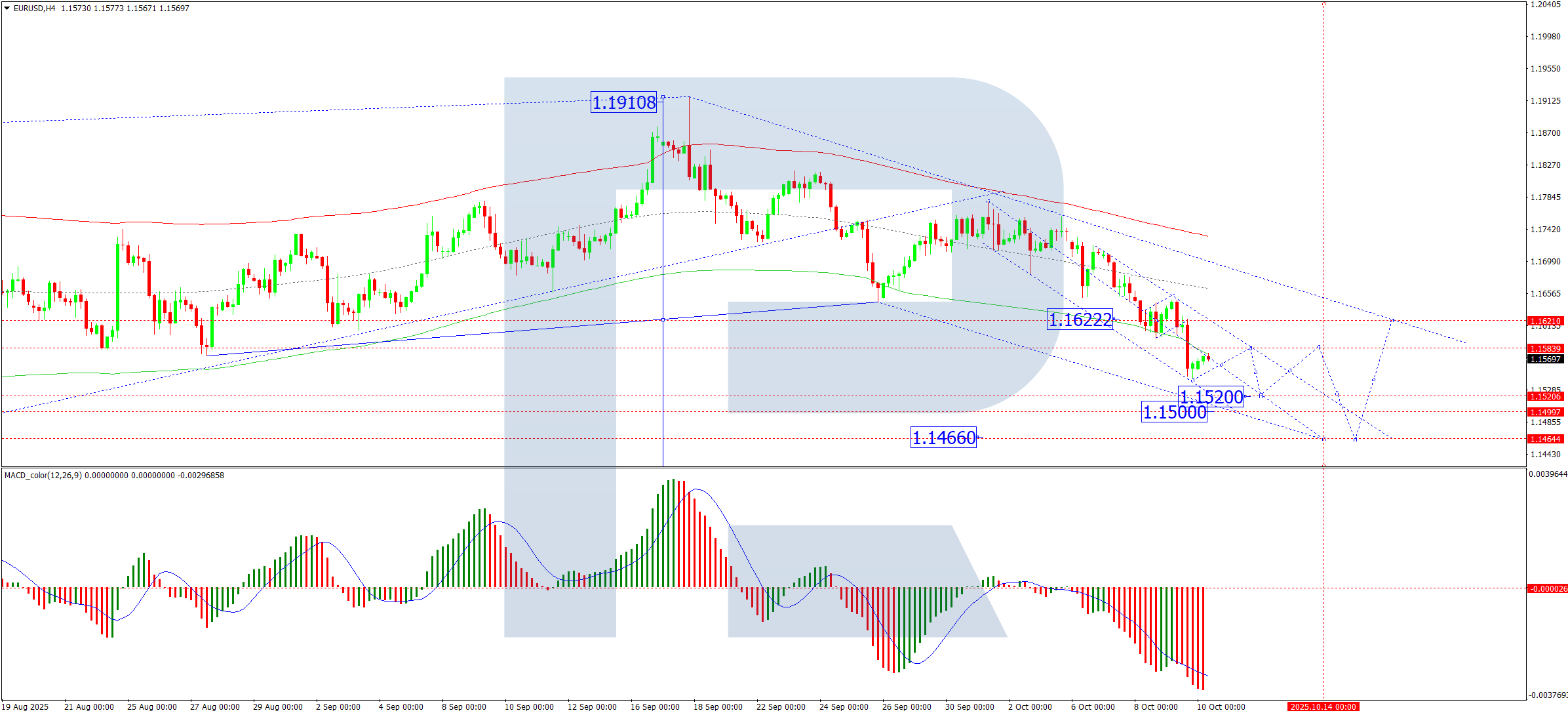

Technical Analysis: EUR/USD

H4 Chart:

The pair completed a downward wave to 1.1622 and subsequently formed a consolidation range around this level. Today’s downward breakout from this range has completed a further decline to 1.1542. A corrective pullback to 1.1584 is now possible. Following this, a decline towards 1.1520 is expected, with the potential to extend the downtrend to 1.1500. This bearish scenario is technically confirmed by the MACD indicator, whose signal line is below zero and pointing firmly downward.

H1 Chart:

A decline to 1.1640 was followed by the formation of a consolidation range below this level. The subsequent downward movement culminated in a wave reaching 1.1542. A short-term correction to 1.1580 is possible today. Upon its completion, a further decline to 1.1520 is anticipated, with the local target for the downward wave structure seen at 1.1500. Technically, this outlook is supported by the Stochastic oscillator, with its signal line below 80 and pointing sharply downward towards 20.

Conclusion

The EUR/USD is firmly on the back foot, driven by a stronger US dollar and distinct weaknesses in both the euro and yen. The technical structure is overwhelmingly bearish, pointing towards a continued decline with key targets at 1.1520 and 1.1500.

Disclaimer:

Any forecasts contained herein are based on the author’s particular opinion. This analysis may not be treated as trading advice. RoboForex bears no responsibility for trading results based on trading recommendations and reviews contained herein.