With the possibility of a Fed pivot looming, expert Clive Maund touches on his views of the precious metals sector and why he believes you should invest in it sooner rather than later.

On the 1-year chart for gold shown below, we can see precisely why it has been in a quite severe downtrend from its peak last March. It is because the dollar and interest rates, shown at the top and bottom of the chart, have been in strong uptrends during this period.

A very important point to note is that while gold has dropped about $400 from its March peak, in real terms, this decline is much more serious because of the robust inflation during this period.

So if the Fed does pivot soon, that is to say, it stops raising rates and starts lowering them, or other Central Banks start raising rates, thus reducing the dollar’s appeal.

It will mean a reversal to the downside in the dollar and to the upside in gold and commodities and risk-on assets generally, and as we saw on Friday 21st, even talk of a pivot is enough to generate a recovery.

Gold

A very important point to note is that while gold has dropped about $400 from its March peak, in real terms, this decline is much more serious because of the robust inflation during this period.

So when you talk about $1600 gold now, it means that in, say, 2019 prices, it’s probably about $1200. This gives us more of an idea about how undervalued gold and especially silver are now. Before leaving this chart, observe that gold may be making a Double Bottom here with its September lows.

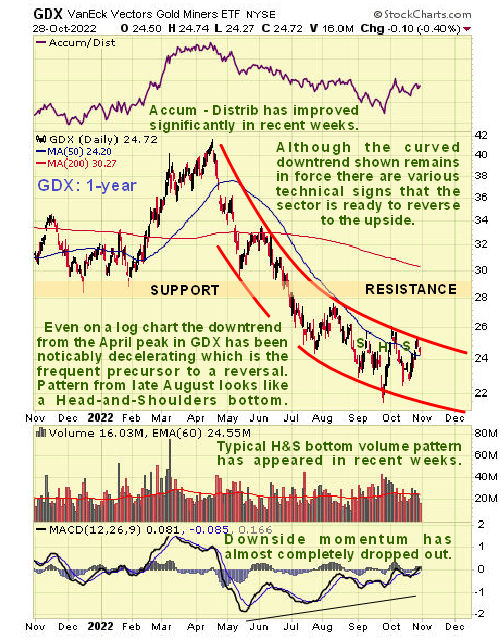

The next chart, the 1-year chart for PM sector proxy GDX, is most interesting as it makes plain that, even on a log chart as this is, the downtrend in the sector from its April highs has been decelerating steadily to the point that the MACD indicator has recovered back almost to the zero line.

If this interpretation is correct, then we are at a point of huge opportunity to buy the sector before it breaks out.

This is the sort of behavior that usually precedes a reversal to the upside, so it is not surprising to see that a small Head-and-Shoulders appears to be completed within the downtrend channel, whose validity is endorsed by the bullish volume pattern that has accompanied it, with strong volume on the rise to form the right side of the Head of the pattern and again on the rise late last week as it completes what is believed to be the Right Shoulder of the pattern.

If this interpretation is correct, then we are at a point of huge opportunity to buy the sector before it breaks out.

In the context of the foregoing, it’s useful for us to consider the extent to which the PM sector has markedly underperformed even the frail stock market in recent months.

Silver is regarded as probably the most undervalued asset in the world.

On the 1-year chart for GDX over the S&P500 index, we can see that it has seriously underperformed due, of course, to the strong rise in the dollar and interest rates.

This is important because it means that the PM sector is even better value here compared to the broad market.

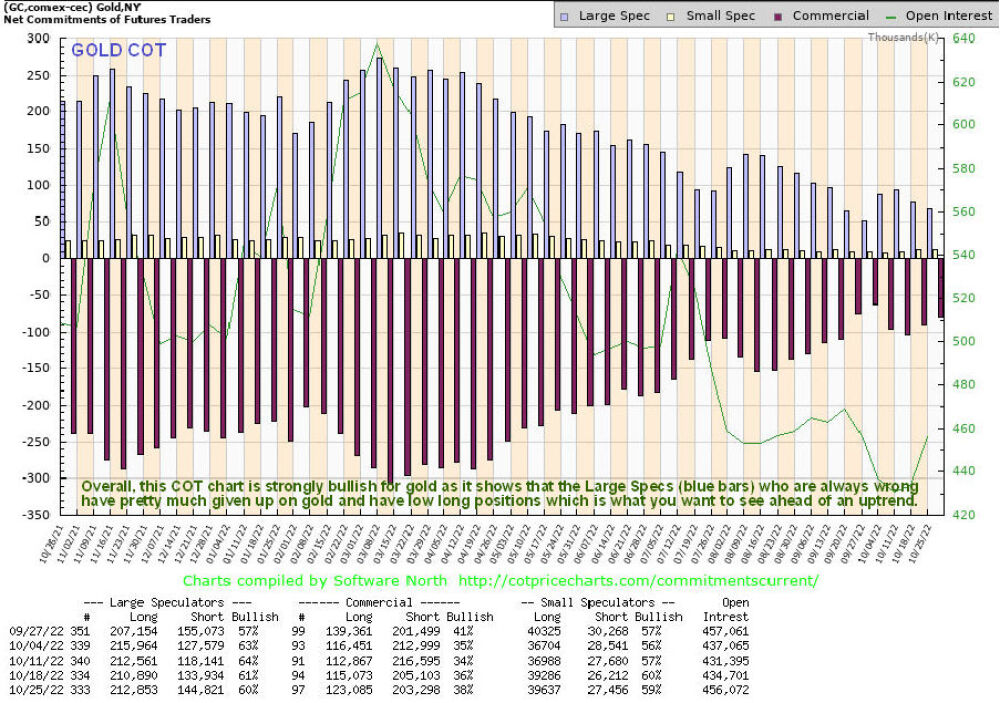

Alright, so if we are at or close to a bottom in gold and the PM sector, then we would expect to see the normally wrong Large Specs having Little interest in gold, and that is exactly what we see on the latest COT chart for gold, which shows that they have pretty much given up on it.

This COT chart alone augurs well for a new bull market phase in gold . . .

Silver

What about silver?

On its 1-year chart, we can see that it has dropped back from its March highs for the same reasons that gold has, the strong uptrends in the dollar, and interest rates.

This is looking like a great place to load up on the better gold and silver stocks.

However, since July, a potential base pattern has been building out that is now starting to look like a completing Triple Bottom, and with the steadily uptrending momentum (MACD) now about to swing positive, the outlook is brightening and the strong volume on the rally out of the low in the middle of the month, better seen on a 6-month chart, looks like the beginnings of a rally up towards the resistance at the upper boundary of the pattern.

Silver is regarded as probably the most undervalued asset in the world, and in the dark times that we are headed towards, physical silver is probably the best asset to have in your possession, along with some firearms to make sure that it stays in your possession.

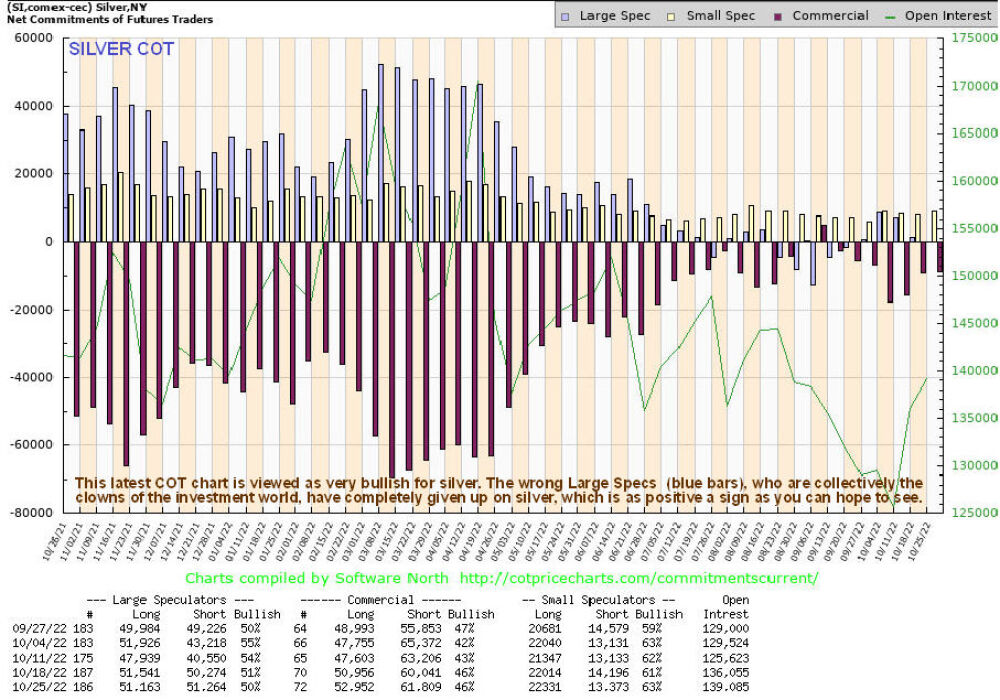

If silver is close to an optimum point to buy, then we would expect to see the dumb Large Specs having no interest in it all, and that is exactly what we see on silver’s latest COT chart, which shows the Large Specs net long positions to be virtually non-existent . . .

It’s useful here to take a quick look at the 5-year chart for the dollar index because, on this chart, we see that it has gone parabolic in recent months, and it’s possible that it just topped out.

Two possible reasons for it to turn and break down that have already been mentioned are a “Fed pivot” and other countries or trading blocs, such as the European Union, following the Fed’s lead and raising rates too.

The U.S. Dollar and British Pound

Just for laughs, let’s take a quick look at the 5-year chart for the British Pound.

It shows that it has been terribly weak, dropping an incredible 40% in less than 18 months . . .

For U.S. readers who’ve always wanted to see the sights in Britain, and have the time and money, now is a good time to vacation there while the exchange rate is good before the Winter.

If you want ideas on what to visit, I can give you a list as long as your arm.

The Risk of a Market Crash

Finally, what about the ongoing risk of an all-out market crash? Would that not drag gold and silver, and PM stocks down even further?

Well, it could, although it may not because, this time, there will be no hiding place for investors in the Treasury market, which is already on the rocks.

So with this option closed off, funk money will probably flee into gold and silver instead. This time round is very different in that the powers that be fully intend to destroy the world economy kill off most of the population, and turn the survivors into cyborg-like slaves, and have made their intentions very clear to anyone with more than a few functioning brain cells.

This would best be achieved by a state of hyperinflation, Venezuela style, that would render the population destitute and totally at the mercy of the State (except for some preppers, who will probably be identified and rounded up anyway).

Following this logic, they will continue to create money to defer the debt market collapse for as long as possible, and the hyperinflation that will result, which we are already close to, must mean an exponential rise in the price of hard assets like gold and silver, with physical being very highly prized and hard to obtain.

The charts that we have reviewed in this update strongly suggest that, whatever the broad market does from here, the PM sector has bottomed out and is going to rally soon. An important article posted by Adam Hamilton a couple of days ago, Gold Stocks’ Winter Rally 7, strongly supports this contention.

Although long, this common sense article presents reasoned arguments based on his many years of experience with this sector and should thus be taken seriously.

Conclusion — This is looking like a great place to load up on the better gold and silver stocks.

CliveMaund.com Disclosures

The above represents the opinion and analysis of Mr. Maund, based on data available to him, at the time of writing. Mr. Maund’s opinions are his own, and are not a recommendation or an offer to buy or sell securities. Mr. Maund is an independent analyst who receives no compensation of any kind from any groups, individuals or corporations mentioned in his reports. As trading and investing in any financial markets may involve serious risk of loss, Mr. Maund recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction and do your own due diligence and research when making any kind of a transaction with financial ramifications. Although a qualified and experienced stock market analyst, Clive Maund is not a Registered Securities Advisor. Therefore Mr. Maund’s opinions on the market and stocks can only be construed as a solicitation to buy and sell securities when they are subject to the prior approval and endorsement of a Registered Securities Advisor operating in accordance with the appropriate regulations in your area of jurisdiction.

Disclosures: 1) Statements and opinions expressed are the opinions of Clive Maund and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. The author was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

An uneasy calm settled across financial markets ahead of the Federal Reserve’s policy meeting this evening. Equities struggled for direction; the dollar index remained static while gold prices were little changed.

Sentiment in general remains shaky and fragile thanks to concerns over slowing global growth with investors adopting a guarded approach ahead of what could be a volatile event. Markets widely expect the Federal Reserve to raise interest rates by 75bp in November but much attention will be directed towards the press conference which could offer fresh clues into monetary policy.

Our focus this afternoon will be directed toward the global equity arena, especially US indices which remain highly reactive to Fed rate hike expectations.

S&P 500 tangled between MA’s

After failing to secure a daily close above the 100-day SMA, the S&P 500 has the potential to trade lower if the 50-day SMA is breached. A strong breakdown below 3810 could trigger a selloff towards 3760 and 3700, respectively. Should 3810 prove to be reliable support, prices could rebound towards 3945 and 4000. It is worth keeping in mind that the short-term outlook will be influenced by the Fed meeting this evening and the US jobs report on Friday.

Nasdaq trapped below 11650?

It looks like the Nasdaq could gearing up for a selloff. After failing to break above the 11650 resistances, prices have tumbled with bears eyeing the 11037 supports. The Fed rate decision and press conference may influence the Nasdaq’s short-term outlook. Technical levels to watch out for are 11037 and 10716. Given how prices are trading below the 50, 100, and 200 Simple Moving Average – bears still have some power. A strong break under 10716 could signal a selloff towards 10436.

FTSE100 lingers below resistance

Since punching above the 7200-resistance level, prices have struggled to push higher as the 100-day Simple Moving Average offered another line of resistance. Although the FTSE100 has staged a rebound from the 6705 regions, prices still remain in a bearish channel. Should 7200 prove to be a tough nut to crack for bulls, prices could sink back towards 7000. Alternatively, a strong breakout above 7200 may open the doors towards 7340 – a level where the 200-day SMA resides.

EURO STOXX 50 breakout or fakeout?

This index remains in an uptrend on the daily charts as there have been consistently higher highs and higher lows. Prices are trading above the 50 and 100-day SMA but below the 200-day which could offer strong resistance. If bulls lose momentum and secure a solid daily close below 3650, this may trigger a selloff back towards 3550 – a level just above the 100-day SMA. Alternatively, a strong daily close above the 3685 regions could inject bulls with enough confidence to push above the 200-day SMA. Such a development may result in an incline towards 3700, 3770, and 3820, respectively.

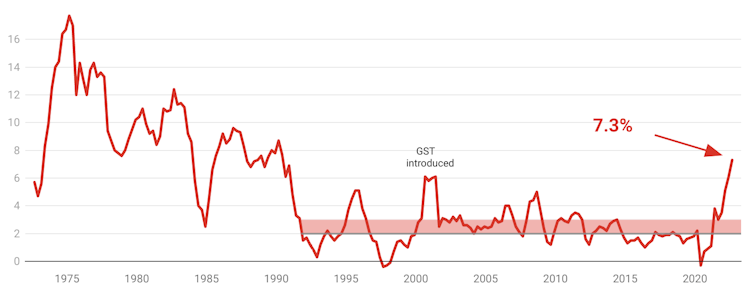

Pushing up interest rates isn’t something the Reserve Bank does lightly.

But what’s worrying the Reserve Bank – and why it increased interest rates for a record seventh consecutive month on Melbourne Cup Tuesday – is that inflation seems to become completely detached from the bank’s target band.

That target band of 2-3% was introduced in the early 1990s, at a time when that’s where inflation was. With one brief exception during the introduction of the goods and services tax, at the start of the 2000s, inflation has never since been far away from the band – until now.

The jump in inflation from 6.1% to 7.3%, revealed last Wednesday, made it clear that, even after six consecutive interest rate hikes, inflation was further away from the Bank’s target band than it had ever been.

Inflation breaks free of the target band

Annual increases in the consumer price index. The RBA’s 2-3% inflation target band was adopted in the early 1990s. ABS

When the Reserve Bank began hiking its so-called cash rate during the May election campaign, the National Australia Bank’s standard variable mortgage rate was 3.45%. It’s now 5.95% and about to go to 6.2%.

For a borrower with a $500,000 mortgage, the increase in payments amounts to $800 per month. For a borrower on a fixed-rate loan of 2% that’s about to expire, the burden will be even greater.

So the Reserve Bank wants to be sure the jump in inflation to 7.3% is real.

How the cost of buying a home skews inflation

The first thing to say is that 7.3% is almost the real thing, but not quite.

The Bureau of Statistics collects information on millions of prices per week, at times by going into stores in eight cities and noting down what’s on price tags, at times by direct feeds from supermarkets, petrol stations and electricity suppliers, and at times by “scraping” prices quoted on the web for home deliveries.

The bureau categorises the things it prices as either essential or non-essential (its words are “non-discretionary” and “discretionary”).

It’s found that the prices of essential items (those we generally have to buy) climbed by more than 7.3% in the year to September – by an extraordinary 8.4% – whereas the prices of things we generally don’t need climbed 5.5%.

For obvious reasons, food is among the bureau’s list of essential or “non-discretionary” items. Food prices continue to be pushed up by floods and labour shortages.

But what many people don’t realise is that also among that list of supposedly “non-discertionary” items is one type of purchase people don’t make often – and which some of Australians will never make.

Buying a home is so expensive compared to the other things we buy (such as bread and milk) that it accounts for almost 9% of the consumer price index.

Worse still, being classified as essential, it makes up almost 15% of the “essentials” index, even though for most of us in any given year buying a home is optional.

In most years, this anomaly doesn’t matter much. The price of a new home (what’s priced is only the construction of the home, not the land) climbs pretty much in line with everything else.

But building material shortages, COVID-induced labour shortages, and an explosion in demand for building fed by the government’s HomeBuilder grant have pushed up the price of new dwellings by an astonishing 20.7% in the past year. That’s enough to add an awful lot to the reported rate of inflation.

The real cost of living is probably up 6%

A rough calculation suggests Australia’s inflation rate would be 6%, instead of 7.3%, if the price of new homes didn’t have such an outsized influence.

We will know more by mid-Wednesday. The bureau actually produces separate living cost indexes a week after the consumer price index that substitute mortgage payments for the cost of home-building.

Lately these indexes have been pointing to increases one to two percentage points below the official rate of inflation.

Accurately measuring rent rises

Another peculiarity is that the rent increases recorded in the consumer price index are so far below those we keep hearing about.

The bureau says in the year to September, average capital city rents climbed just 2.8%, compared to the figures of 10%, and in some suburbs, 20%, quoted by real estate analysts.

In part, this is because the bureau only reports capital city rents. But more importantly it is because it does its job better than real estate analysts.

It collects data on not only the rents that are advertised (these are climbing strongly), but also on the hundreds of thousands of rents paid by continuing renters, which either aren’t climbing at all or aren’t climbing as strongly.

The water in the tub represents all rents being paid by households, while the water entering the tub from the tap represents new rental agreements. The consumer price index is measuring the overall temperature of the bathtub whereas an advertised rents series measures the temperature of the water flowing into the tub.

Worse news ahead

Perhaps surprisingly, the bureau finds the average retail price of electricity only climbed 3.2% in the year to September, and the price of gas by only 16.6%, much less than the 56% and 44% mentioned in last week’s federal budget.

But the budget numbers were predictions of what’ll happen over the next two years unless the government provides relief. The bureau was telling us what has happened.

Which is why the Reserve Bank is worried. While gas and electricity prices will subside eventually, inflation is likely to climb even higher before it falls – the bank says to around 8%.

The way back to the target band of 2-3% is anything but clear. That means for homebuyers, there’s no relief in sight just yet.

The war against inflation remains fierce and relentless.

Central banks across the world are on the offensive, unleashing aggressive rate hikes despite the growing risks of collateral damage to their respective economies.

Last week, the Bank of Canada (BoC) announced a smaller-than-expected hike of 50bp as recession fears intensified. However, the European Central Bank (ECB) hiked rates by 75 basis points for the second consecutive time thanks to soaring inflation in the Euro Area.

Over the next few days, the Federal Reserve is poised to raise rates by 75 basis points for the fourth consecutive time while the Bank of England could finally join the jumbo hike club!

Before we take a deep dive into what to expect from the BoE on Thursday, it’s safe to say that the past few weeks have been wild for not only the UK economy but Pound. A toxic combination of political drama and central bank intervention sent the GBPUSD on a chaotic roller-coaster ride.

After making a swift recovery in recent days, the GBPUSD is trading back above 1.15 for the first time in 6 weeks. This move has been the product of dollar weakness and improving sentiment toward the UK economy after Rishi Sunak became Prime Minister. The currency pair will most likely be influenced by the Fed rate decision on Wednesday and the BoE meeting on Thursday.

The low down…

The Bank of England remains in a tricky position as it potentially delivers what would be the biggest UK rate hike in 33 years.

Sentiment towards the UK economy is fragile due to fears that the country is probably already in a recession while the recent political drama over ex-Prime Minister Liz Truss’s controversial mini-budget has left a bitter aftertaste. With inflation through the roof at 10.1%, expectations remain elevated over the Bank of England joining the heavy hitters by unleashing a 75bp monetary policy bazooka. However, recent economic data including retail sales, monthly GDP, and manufacturing data among many others have shown signs of a slowing economy.

At the peak of the political crisis when the pound tumbled to an all-time low, markets were pricing in a gargantuan 200 basis point hike in November. But with some normality returning to UK markets and sterling staging a strong recovery, BoE rate hike expectations have cooled.

Although according to Bloomberg, traders have fully priced in a 75bp rate hike at the BoE’s November meeting – expectations can differ from reality.

Other things to watch out for…

Mid-week, the Federal Reserve is expected to raise interest rates by 75 basis points. Given how such a move has already been priced, much attention will be on the press conference for clues on future monetary policy. Should the central bank strike a cautious tone with doves entering the scene, this could weaken the dollar as aggressive rate hike bets cool. A weaker dollar may push the GBPUSD higher ahead of the BoE meeting on Thursday 3rd November.

Possible outcomes of BoE meeting

BoE hikes rates by 75-basis points. This decision could inject some life into pound bulls but gains may be limited if the central bank signals that this is a “one-off” move. Expect the pound to weaken eventually as expectations rise over the BoE adopting a less aggressive approach towards rates beyond November and 2023.

BoE hikes rate by 50-basis points. This decision could be based on the gloomy macroeconomic decisions and fears of the UK already entering a recession. Such a move could trigger a pound selloff as the BoE rejects the 75bp club membership.

Unlikely outcomes of BoE meeting

BoE hikes rates by 100 basis points. Given how UK inflation remains at a 40-year high, the central bank decides to go full-auto to contain rising prices. Pound is likely to rally aggressively following such a move but the upside may be capped by recession fears.

GBPUSD to breakout or breakdown?

The next few days could be volatile for the GBPUSD thanks to the Fed & BoE policy meetings.

Fundamentally, the GBPUSD remains bearish but the technicals could be singing a different tune. Prices are trading above 1.1500 due to the recent weakness in the USD as traders bet over the Fed slowing the pace of rate hikes. Should 1.1500 prove to be reliable support a move back towards 1.1750 and 1.1850 could be on the cards. If bears succeed in dragging the GBPUSD back under 1.1500, the first point of interest can be found at 1.1400 where the 50-day SMA resides. Below this point, prices could sink towards 1.1200 and 1.0925.

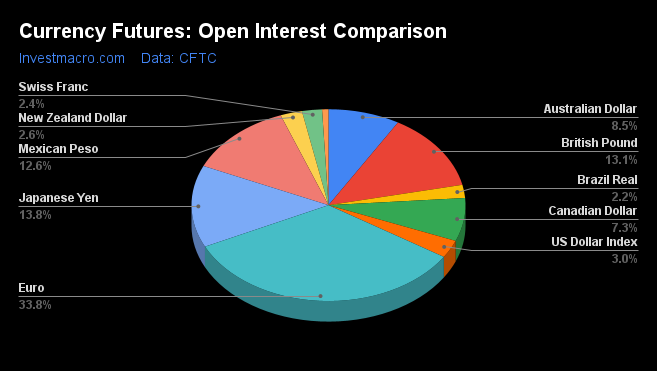

Here are the latest charts and statistics for the Commitment of Traders (COT) data published by the Commodities Futures Trading Commission (CFTC).

The latest COT data is updated through Tuesday October 25th and shows a quick view of how large market participants (for-profit speculators and commercial traders) were positioned in the futures markets. All currency positions are in direct relation to the US dollar where, for example, a bet for the euro is a bet that the euro will rise versus the dollar while a bet against the euro will be a bet that the euro will decline versus the dollar.

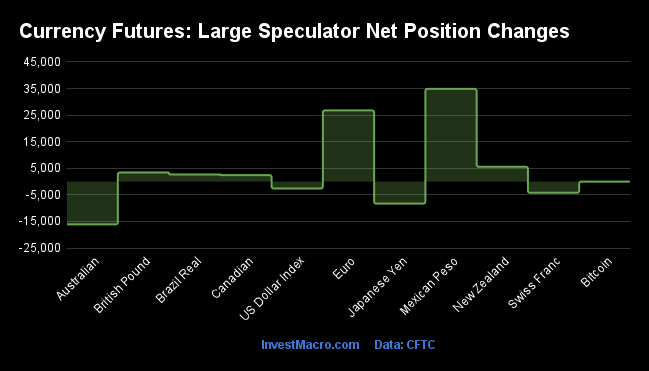

Weekly Speculator Changes led by Mexican Peso & Euro

The COT currency market speculator bets were mostly higher this week as seven out of the eleven currency markets we cover had higher positioning while the other four markets had lower speculator contracts.

Leading the gains for the currency markets was the Mexican peso (34,868 contracts) with the Euro (26,759 contracts), the New Zealand dollar (5,561 contracts), the British pound sterling (3,406 contracts), the Brazilian real (2,681 contracts), the Canadian dollar (2,418 contracts) and Bitcoin (1 contracts) also showing positive weeks.

The currencies leading the declines in speculator bets this week were the Australian dollar (-16,087 contracts) with the Japanese yen (-8,282 contracts), the Swiss franc (-4,214 contracts) and the US Dollar Index (-2,592 contracts) also registering lower bets on the week.

Highlighting the COT currency positioning this week is the further push higher for the Euro speculators. The large speculator position in Euro futures jumped again this week and is higher for the seventh time in the past eight weeks. This week’s rise by over +26,000 contracts follows a gain by over +10,000 contracts last week. The past eight-week gains for Euro speculator bets now stands at +122,585 contracts and the current bullish position (+74,909 contracts currently) is at the most bullish level in 68-weeks, dating back to July 6th of 2021.

The strong bullishness in the Euro is despite the Euro price remaining at parity against the US Dollar (near 20-year lows). The European Central Bank raised their interest rate by 75 basis points on Thursday to try and offset high inflation in the Eurozone and brought the interest rate differential with the US Dollar a little narrower. Going forward, this divergence in the speculator positioning and the weak Euro price brings up some interesting questions. Does the sharply improving speculator sentiment foreshadow an improvement in the Euro price or will it set up a short squeeze with prices going lower if the speculators throw in the towel and bail out of their bullish bets?

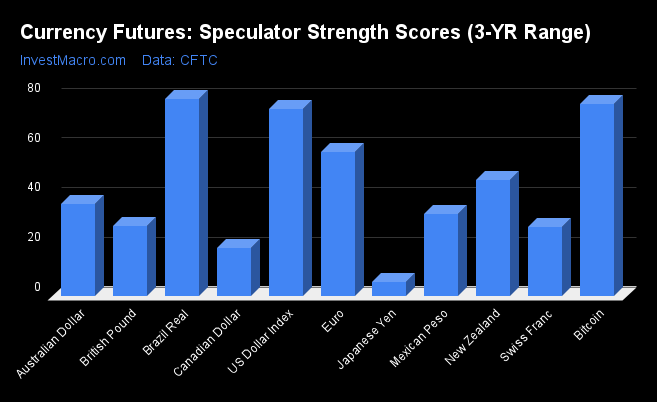

Brazilian Real, Bitcoin and US Dollar Index lead Strength Scores

Strength Scores (a normalized measure of Speculator positions over a 3-Year range, from 0 to 100 where above 80 is extreme bullish and below 20 is extreme bearish) showed that Brazilian Real (79.1 percent), Bitcoin (77.3 percent) and the US Dollar Index (75.1 percent) lead the currency markets near the top of their respective ranges. The EuroFX (58.0 percent) comes in as the next highest in the currency markets in strength scores and above the 50 percent level.

On the downside, the Japanese Yen (5.7 percent) comes in at the lowest strength level currently and is in an extreme bearish position below 20 percent.

Strength Statistics: US Dollar Index (75.1 percent) vs US Dollar Index previous week (79.5 percent) EuroFX (58.0 percent) vs EuroFX previous week (49.8 percent) British Pound Sterling (28.0 percent) vs British Pound Sterling previous week (25.0 percent) Japanese Yen (5.7 percent) vs Japanese Yen previous week (10.8 percent) Swiss Franc (27.8 percent) vs Swiss Franc previous week (38.5 percent) Canadian Dollar (19.0 percent) vs Canadian Dollar previous week (16.3 percent) Australian Dollar (37.1 percent) vs Australian Dollar previous week (52.1 percent) New Zealand Dollar (46.5 percent) vs New Zealand Dollar previous week (36.6 percent) Mexican Peso (32.7 percent) vs Mexican Peso previous week (17.8 percent) Brazilian Real (79.1 percent) vs Brazilian Real previous week (76.4 percent) Bitcoin (77.3 percent) vs Bitcoin previous week (77.3 percent)

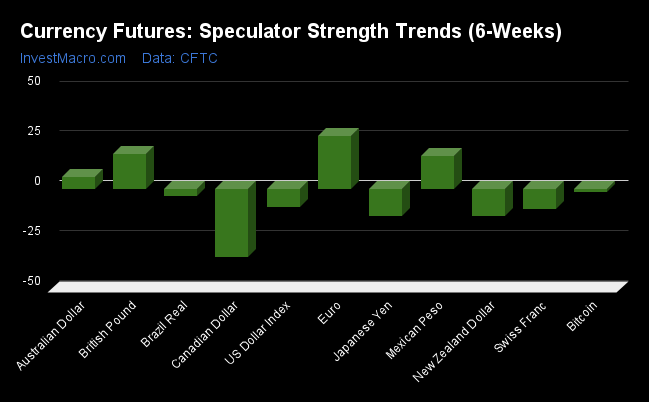

Euro leads the Strength Trends

Strength Score Trends (or move index, calculates the 6-week changes in strength scores) show that the EuroFX (26.6 percent) leads the past six weeks trends for the currency markets this week. The British Pound Sterling (17.4 percent), the Mexican Peso (16.2 percent) and the Australian Dollar (5.9 percent) fill out the other positive movers in the latest trends data.

The Canadian Dollar (-34.3 percent) leads the downside trend scores currently while the next market with lower trend scores were the New Zealand Dollar (-13.5 percent), Japanese Yen (-13.5 percent) and the Swiss Franc (-10.1 percent).

Strength Trend Statistics: US Dollar Index (-9.3 percent) vs US Dollar Index previous week (-5.7 percent) EuroFX (26.6 percent) vs EuroFX previous week (25.9 percent) British Pound Sterling (17.4 percent) vs British Pound Sterling previous week (-0.7 percent) Japanese Yen (-13.5 percent) vs Japanese Yen previous week (-22.3 percent) Swiss Franc (-10.1 percent) vs Swiss Franc previous week (-7.7 percent) Canadian Dollar (-34.3 percent) vs Canadian Dollar previous week (-43.2 percent) Australian Dollar (5.9 percent) vs Australian Dollar previous week (19.6 percent) New Zealand Dollar (-13.5 percent) vs New Zealand Dollar previous week (-28.0 percent) Mexican Peso (16.2 percent) vs Mexican Peso previous week (3.1 percent) Brazilian Real (-3.7 percent) vs Brazilian Real previous week (-4.3 percent) Bitcoin (-1.8 percent) vs Bitcoin previous week (-22.7 percent)

Individual COT Forex Markets:

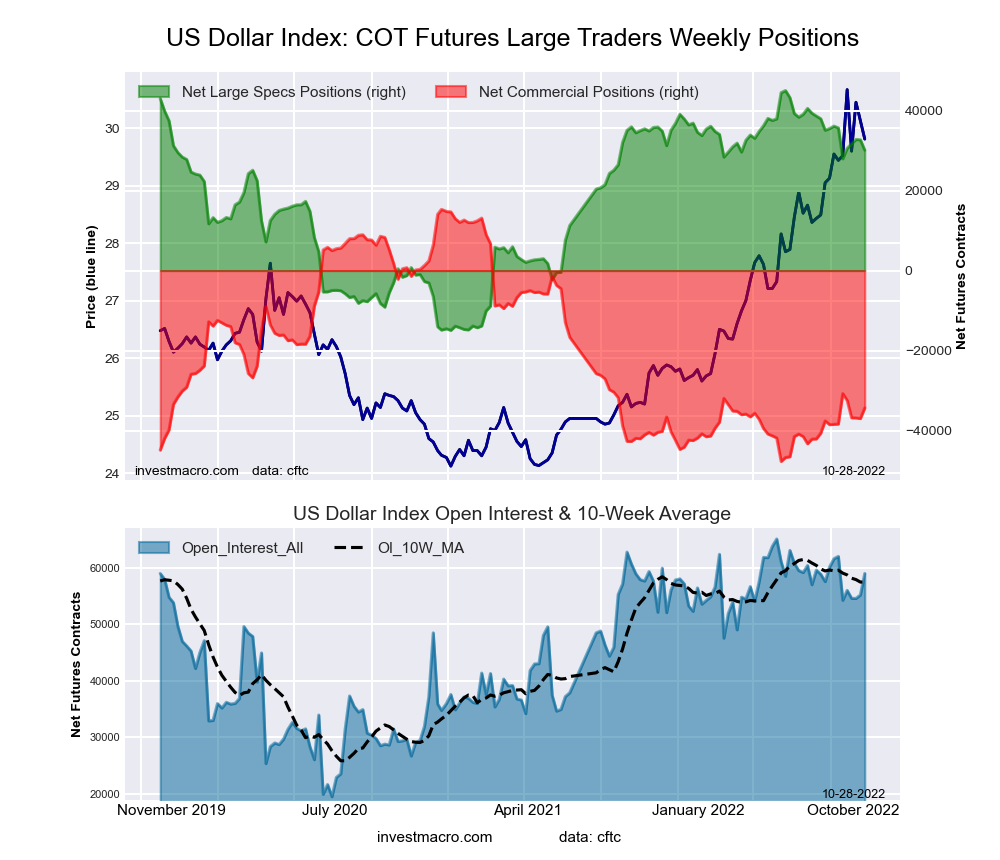

US Dollar Index Futures:

The US Dollar Index large speculator standing this week equaled a net position of 30,098 contracts in the data reported through Tuesday. This was a weekly lowering of -2,592 contracts from the previous week which had a total of 32,690 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 75.1 percent. The commercials are Bearish with a score of 21.2 percent and the small traders (not shown in chart) are Bullish with a score of 63.1 percent.

US DOLLAR INDEX Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

76.2

9.5

11.7

– Percent of Open Interest Shorts:

25.2

67.6

4.5

– Net Position:

30,098

-34,360

4,262

– Gross Longs:

44,998

5,587

6,921

– Gross Shorts:

14,900

39,947

2,659

– Long to Short Ratio:

3.0 to 1

0.1 to 1

2.6 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

75.1

21.2

63.1

– Strength Index Reading (3 Year Range):

Bullish

Bearish

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-9.3

6.4

17.0

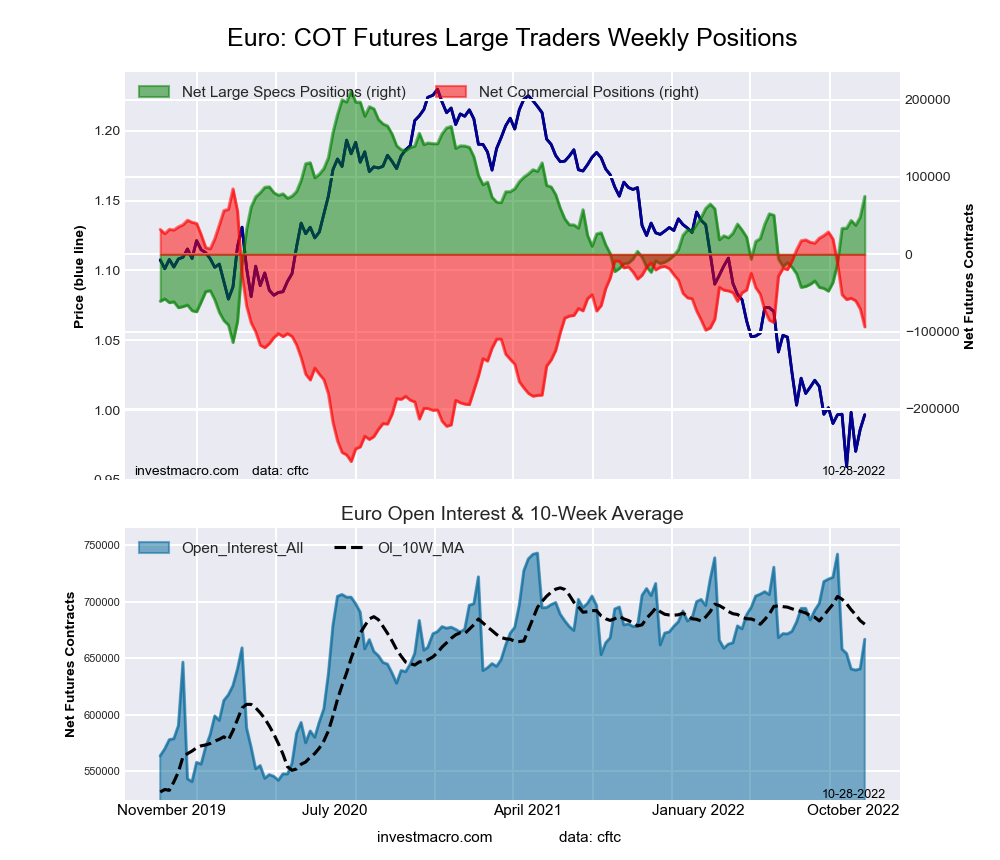

Euro Currency Futures:

The Euro Currency large speculator standing this week equaled a net position of 74,909 contracts in the data reported through Tuesday. This was a weekly increase of 26,759 contracts from the previous week which had a total of 48,150 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 58.0 percent. The commercials are Bearish with a score of 49.4 percent and the small traders (not shown in chart) are Bearish-Extreme with a score of 9.2 percent.

EURO Currency Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

34.0

52.0

11.4

– Percent of Open Interest Shorts:

22.8

66.1

8.5

– Net Position:

74,909

-93,832

18,923

– Gross Longs:

226,734

346,949

75,890

– Gross Shorts:

151,825

440,781

56,967

– Long to Short Ratio:

1.5 to 1

0.8 to 1

1.3 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

58.0

49.4

9.2

– Strength Index Reading (3 Year Range):

Bullish

Bearish

Bearish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

26.6

-23.4

-6.9

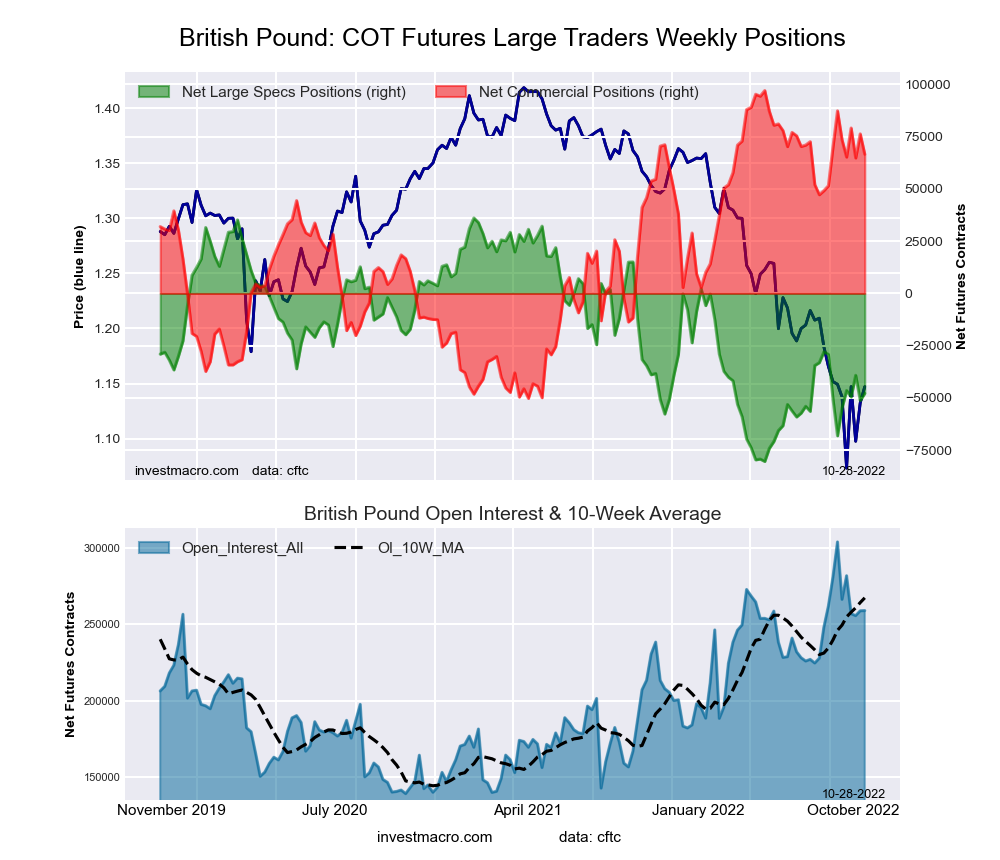

British Pound Sterling Futures:

The British Pound Sterling large speculator standing this week equaled a net position of -47,805 contracts in the data reported through Tuesday. This was a weekly boost of 3,406 contracts from the previous week which had a total of -51,211 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 28.0 percent. The commercials are Bullish with a score of 79.3 percent and the small traders (not shown in chart) are Bearish with a score of 21.2 percent.

BRITISH POUND Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

16.8

73.0

8.1

– Percent of Open Interest Shorts:

35.3

47.3

15.4

– Net Position:

-47,805

66,560

-18,755

– Gross Longs:

43,511

189,146

21,012

– Gross Shorts:

91,316

122,586

39,767

– Long to Short Ratio:

0.5 to 1

1.5 to 1

0.5 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

28.0

79.3

21.2

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

17.4

-14.1

0.9

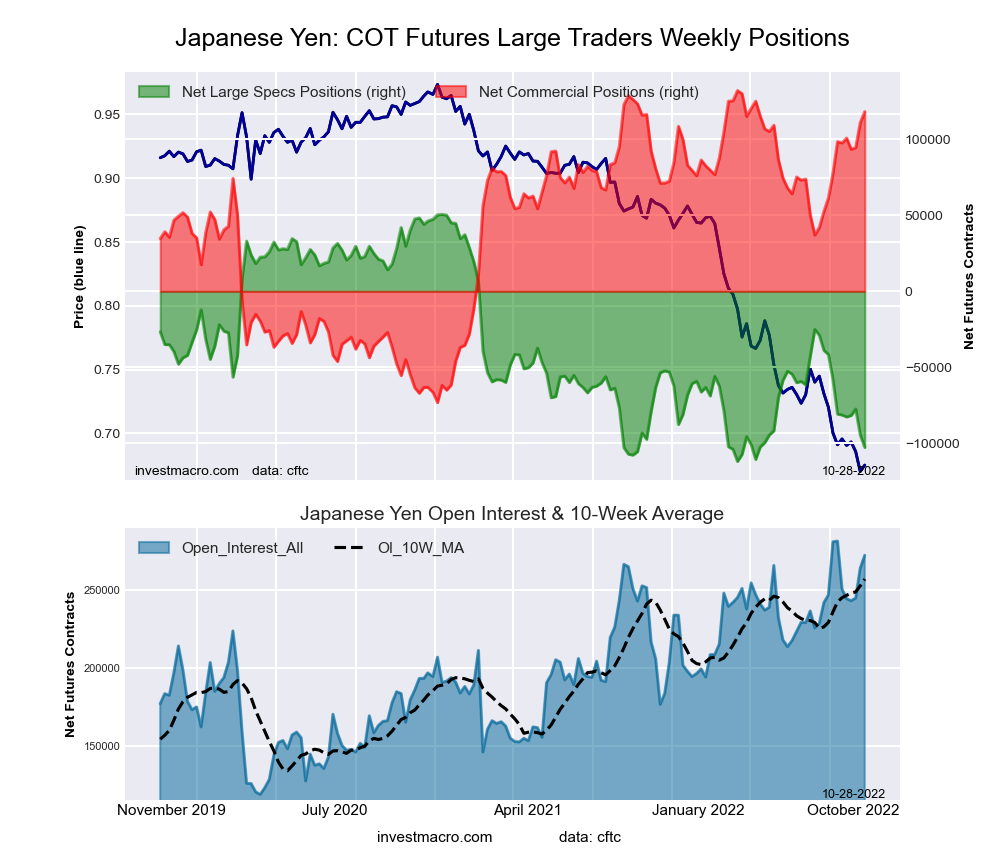

Japanese Yen Futures:

The Japanese Yen large speculator standing this week equaled a net position of -102,618 contracts in the data reported through Tuesday. This was a weekly decline of -8,282 contracts from the previous week which had a total of -94,336 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 5.7 percent. The commercials are Bullish-Extreme with a score of 93.3 percent and the small traders (not shown in chart) are Bearish with a score of 22.0 percent.

JAPANESE YEN Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

13.8

75.2

9.4

– Percent of Open Interest Shorts:

51.4

31.9

15.0

– Net Position:

-102,618

118,082

-15,464

– Gross Longs:

37,579

205,120

25,555

– Gross Shorts:

140,197

87,038

41,019

– Long to Short Ratio:

0.3 to 1

2.4 to 1

0.6 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

5.7

93.3

22.0

– Strength Index Reading (3 Year Range):

Bearish-Extreme

Bullish-Extreme

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-13.5

9.6

4.4

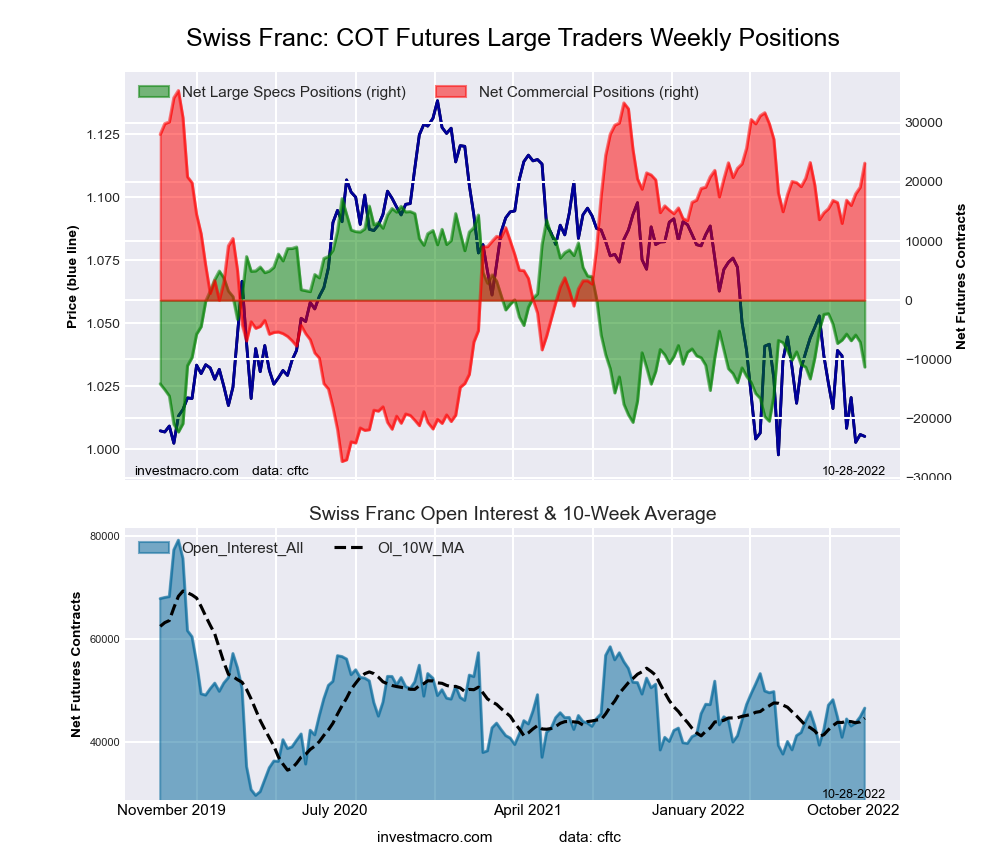

Swiss Franc Futures:

The Swiss Franc large speculator standing this week equaled a net position of -11,300 contracts in the data reported through Tuesday. This was a weekly reduction of -4,214 contracts from the previous week which had a total of -7,086 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 27.8 percent. The commercials are Bullish-Extreme with a score of 80.4 percent and the small traders (not shown in chart) are Bearish-Extreme with a score of 17.4 percent.

SWISS FRANC Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

11.9

68.3

19.5

– Percent of Open Interest Shorts:

36.1

18.6

45.0

– Net Position:

-11,300

23,161

-11,861

– Gross Longs:

5,538

31,843

9,097

– Gross Shorts:

16,838

8,682

20,958

– Long to Short Ratio:

0.3 to 1

3.7 to 1

0.4 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

27.8

80.4

17.4

– Strength Index Reading (3 Year Range):

Bearish

Bullish-Extreme

Bearish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-10.1

10.6

-9.0

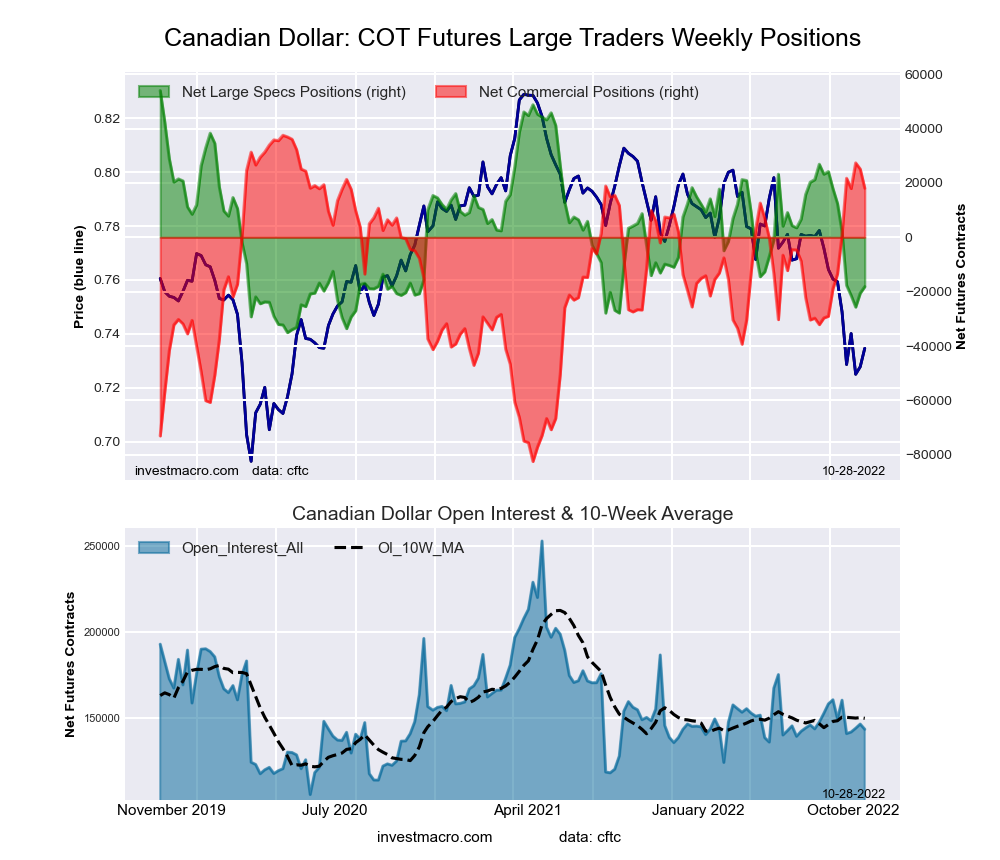

Canadian Dollar Futures:

The Canadian Dollar large speculator standing this week equaled a net position of -18,155 contracts in the data reported through Tuesday. This was a weekly gain of 2,418 contracts from the previous week which had a total of -20,573 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 19.0 percent. The commercials are Bullish-Extreme with a score of 83.8 percent and the small traders (not shown in chart) are Bearish with a score of 30.3 percent.

CANADIAN DOLLAR Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

24.8

51.6

21.7

– Percent of Open Interest Shorts:

37.5

39.1

21.6

– Net Position:

-18,155

18,053

102

– Gross Longs:

35,607

74,064

31,123

– Gross Shorts:

53,762

56,011

31,021

– Long to Short Ratio:

0.7 to 1

1.3 to 1

1.0 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

19.0

83.8

30.3

– Strength Index Reading (3 Year Range):

Bearish-Extreme

Bullish-Extreme

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-34.3

26.3

-1.9

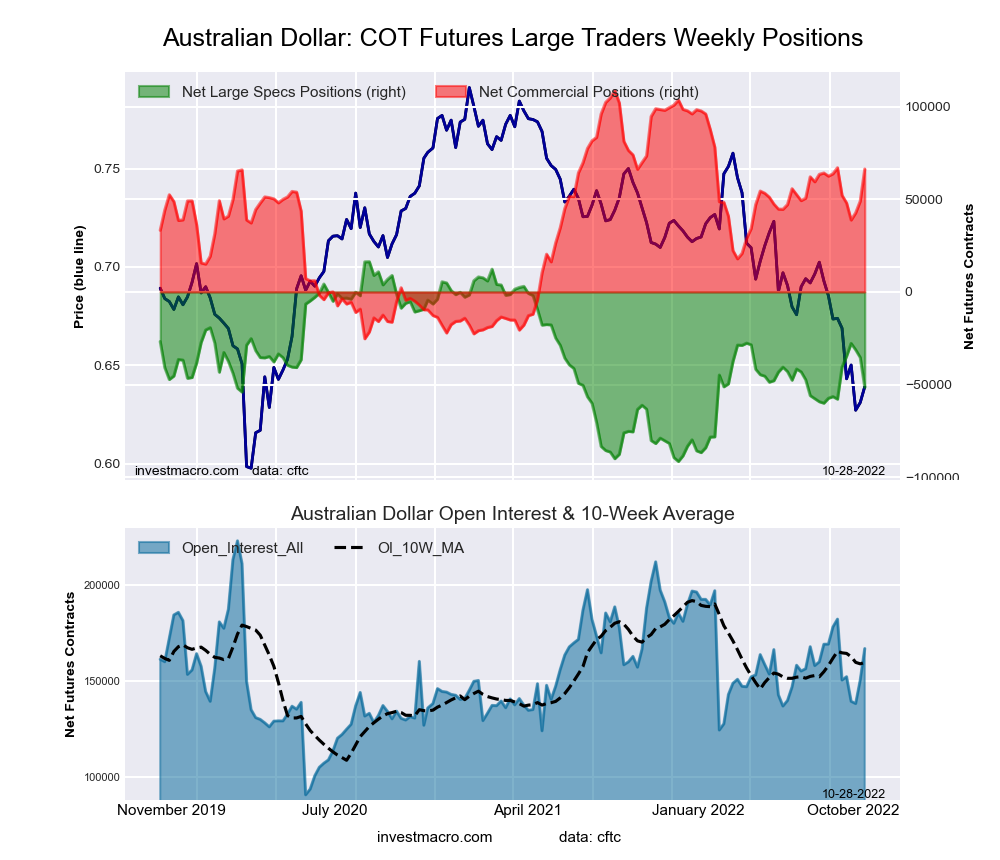

Australian Dollar Futures:

The Australian Dollar large speculator standing this week equaled a net position of -51,446 contracts in the data reported through Tuesday. This was a weekly decrease of -16,087 contracts from the previous week which had a total of -35,359 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 37.1 percent. The commercials are Bullish with a score of 68.4 percent and the small traders (not shown in chart) are Bearish-Extreme with a score of 16.2 percent.

AUSTRALIAN DOLLAR Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

19.3

69.1

9.0

– Percent of Open Interest Shorts:

50.1

29.4

17.9

– Net Position:

-51,446

66,319

-14,873

– Gross Longs:

32,159

115,337

15,022

– Gross Shorts:

83,605

49,018

29,895

– Long to Short Ratio:

0.4 to 1

2.4 to 1

0.5 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

37.1

68.4

16.2

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bearish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

5.9

-0.5

-13.9

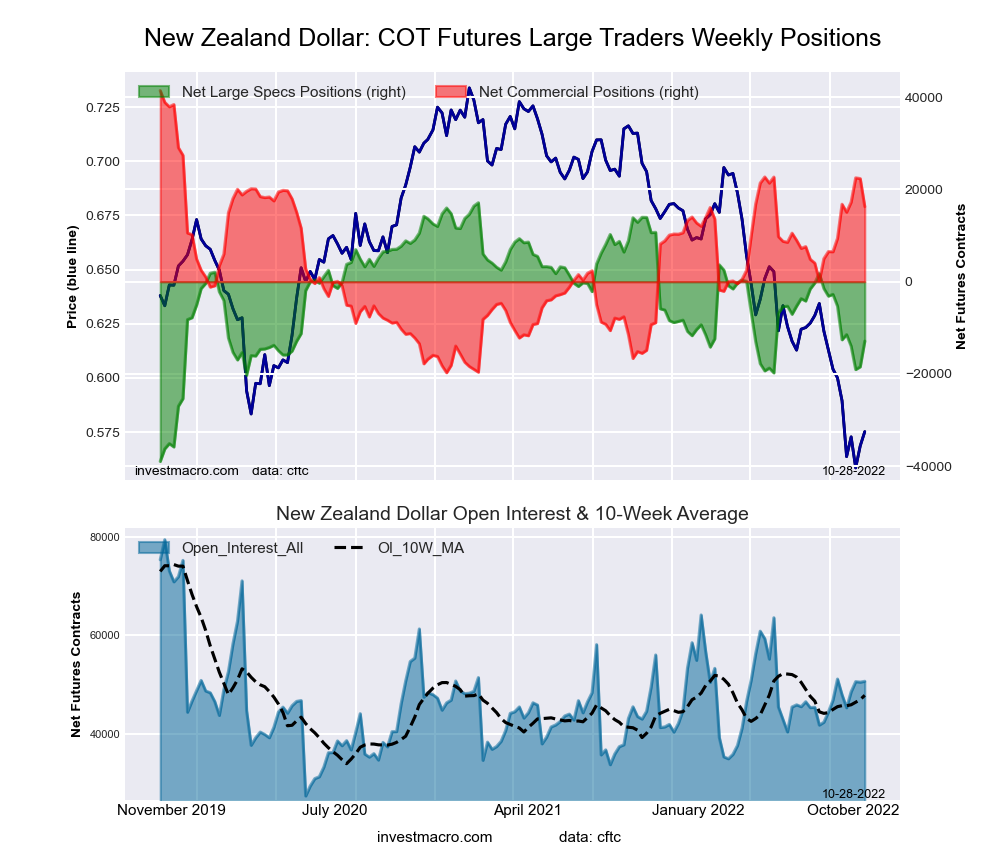

New Zealand Dollar Futures:

The New Zealand Dollar large speculator standing this week equaled a net position of -12,884 contracts in the data reported through Tuesday. This was a weekly increase of 5,561 contracts from the previous week which had a total of -18,445 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 46.5 percent. The commercials are Bullish with a score of 58.9 percent and the small traders (not shown in chart) are Bearish-Extreme with a score of 12.5 percent.

NEW ZEALAND DOLLAR Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

30.9

62.4

5.9

– Percent of Open Interest Shorts:

56.3

30.2

12.6

– Net Position:

-12,884

16,289

-3,405

– Gross Longs:

15,639

31,568

2,983

– Gross Shorts:

28,523

15,279

6,388

– Long to Short Ratio:

0.5 to 1

2.1 to 1

0.5 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

46.5

58.9

12.5

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bearish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-13.5

11.2

8.1

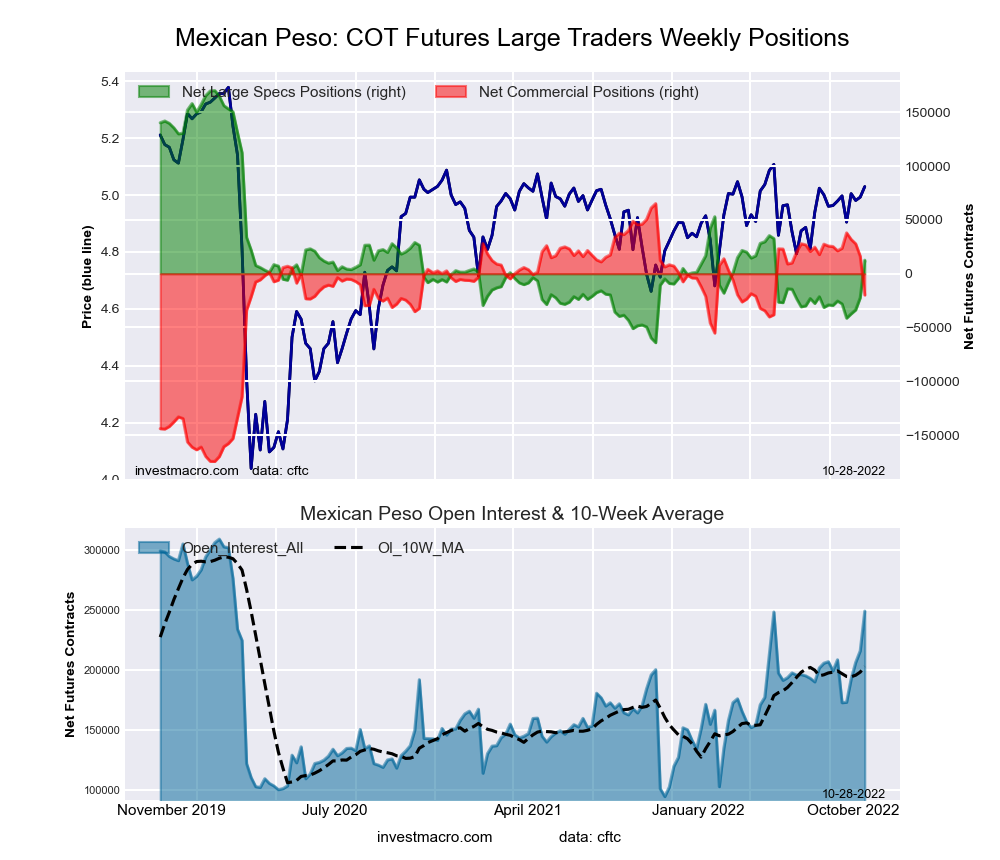

Mexican Peso Futures:

The Mexican Peso large speculator standing this week equaled a net position of 12,574 contracts in the data reported through Tuesday. This was a weekly gain of 34,868 contracts from the previous week which had a total of -22,294 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 32.7 percent. The commercials are Bullish with a score of 64.5 percent and the small traders (not shown in chart) are Bullish with a score of 73.7 percent.

MEXICAN PESO Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

64.9

31.6

3.4

– Percent of Open Interest Shorts:

59.9

39.6

0.5

– Net Position:

12,574

-19,809

7,235

– Gross Longs:

161,558

78,742

8,379

– Gross Shorts:

148,984

98,551

1,144

– Long to Short Ratio:

1.1 to 1

0.8 to 1

7.3 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

32.7

64.5

73.7

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

16.2

-17.2

13.5

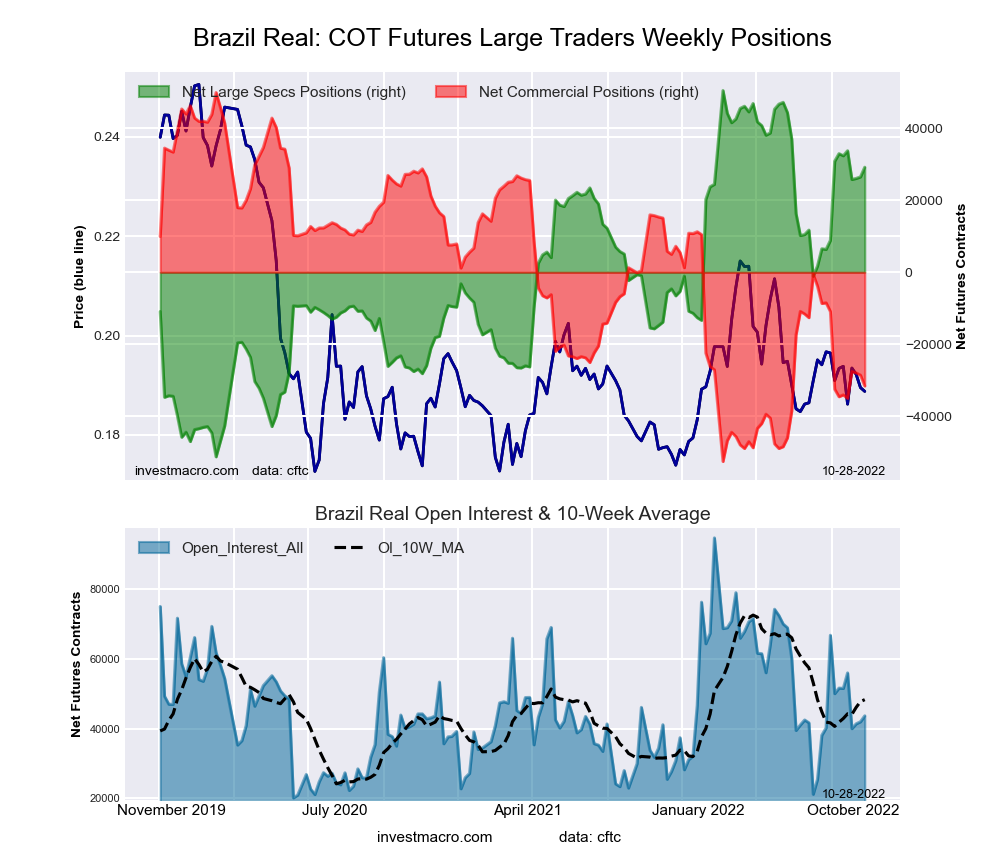

Brazilian Real Futures:

The Brazilian Real large speculator standing this week equaled a net position of 29,179 contracts in the data reported through Tuesday. This was a weekly advance of 2,681 contracts from the previous week which had a total of 26,498 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 79.1 percent. The commercials are Bearish with a score of 20.5 percent and the small traders (not shown in chart) are Bullish-Extreme with a score of 93.0 percent.

BRAZIL REAL Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

72.9

16.1

8.6

– Percent of Open Interest Shorts:

6.1

88.5

3.1

– Net Position:

29,179

-31,590

2,411

– Gross Longs:

31,835

7,041

3,746

– Gross Shorts:

2,656

38,631

1,335

– Long to Short Ratio:

12.0 to 1

0.2 to 1

2.8 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

79.1

20.5

93.0

– Strength Index Reading (3 Year Range):

Bullish

Bearish

Bullish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-3.7

2.9

9.2

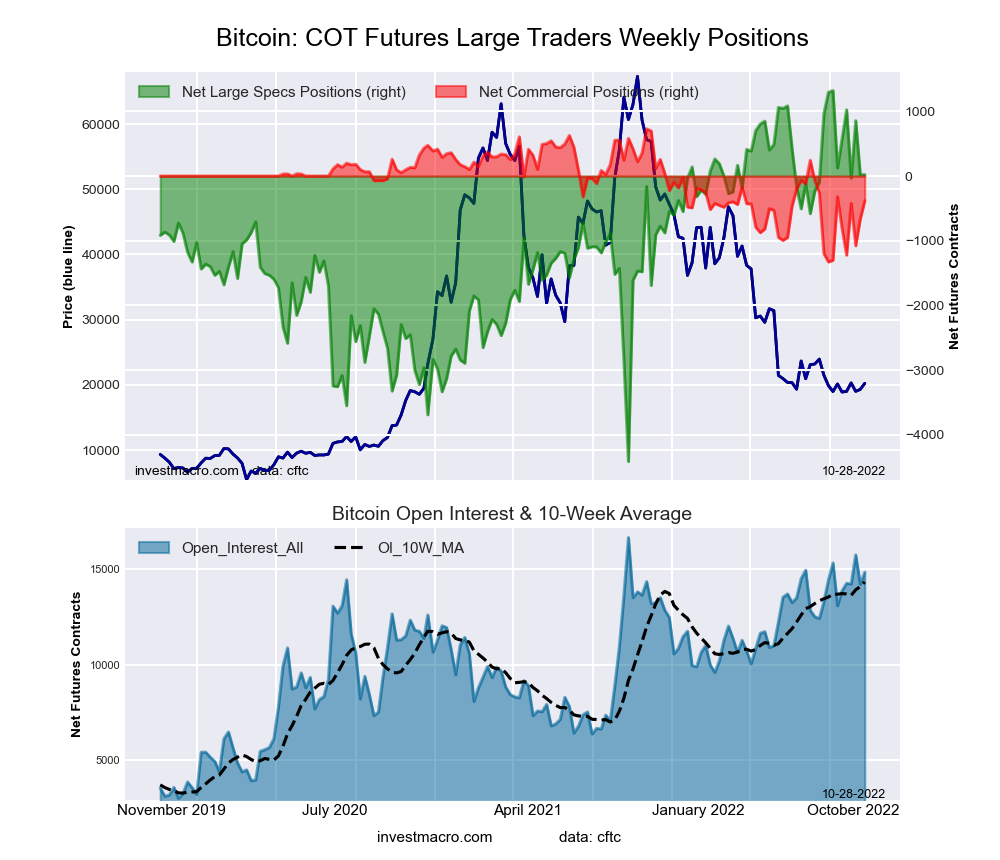

Bitcoin Futures:

The Bitcoin large speculator standing this week equaled a net position of 23 contracts in the data reported through Tuesday. This was a weekly advance of 1 contracts from the previous week which had a total of 22 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 77.3 percent. The commercials are Bearish with a score of 46.1 percent and the small traders (not shown in chart) are Bearish with a score of 21.1 percent.

BITCOIN Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

74.6

4.0

7.9

– Percent of Open Interest Shorts:

74.5

6.6

5.5

– Net Position:

23

-380

357

– Gross Longs:

11,084

601

1,176

– Gross Shorts:

11,061

981

819

– Long to Short Ratio:

1.0 to 1

0.6 to 1

1.4 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

77.3

46.1

21.1

– Strength Index Reading (3 Year Range):

Bullish

Bearish

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-1.8

-2.9

3.7

Article By InvestMacro – Receive our weekly COT Newsletter

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators) as well as their open interest (contracts open in the market at time of reporting). See CFTC criteria here.

Here are the latest charts and statistics for the Commitment of Traders (COT) data published by the Commodities Futures Trading Commission (CFTC).

The latest COT data is updated through Tuesday October 25th and shows a quick view of how large traders (for-profit speculators and commercial entities) were positioned in the futures markets.

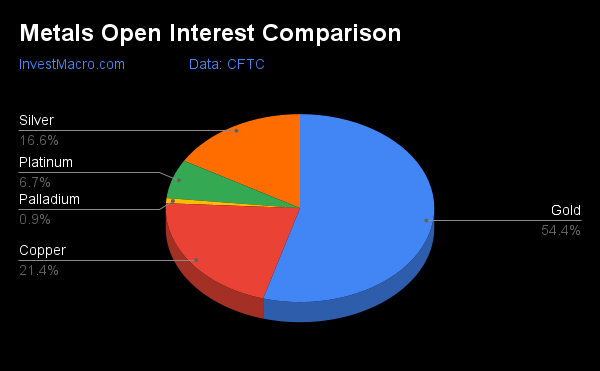

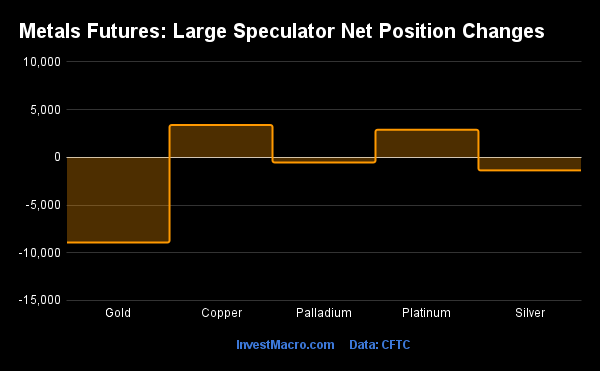

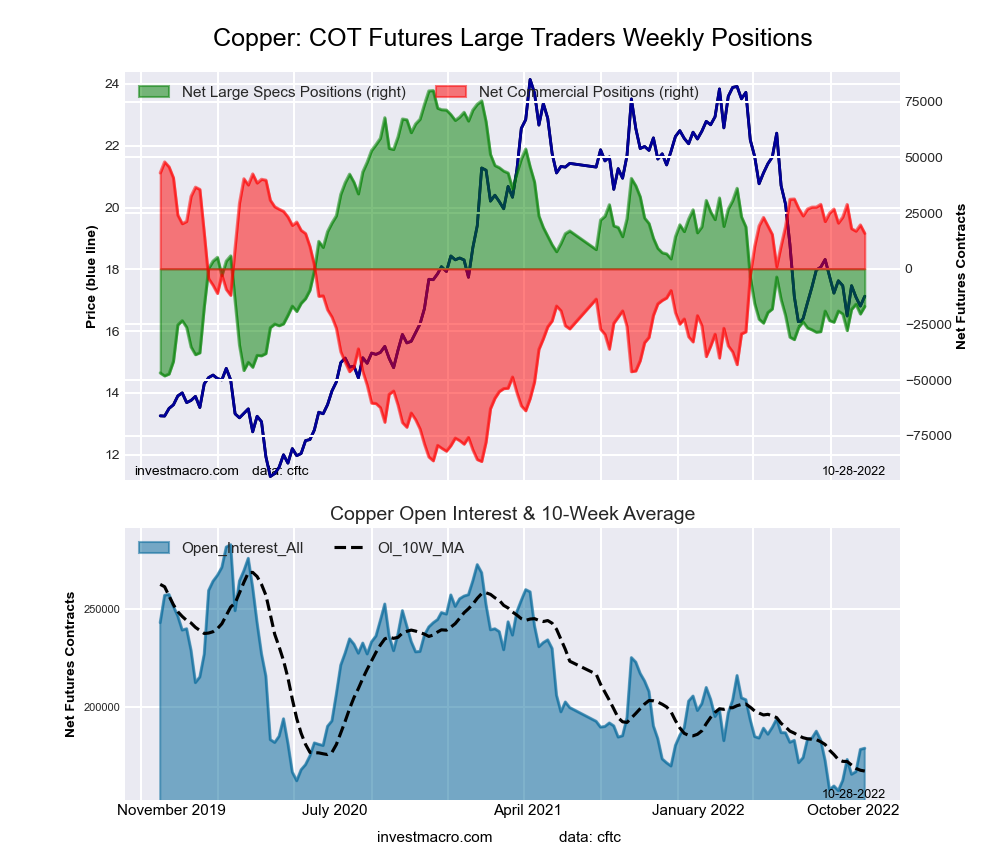

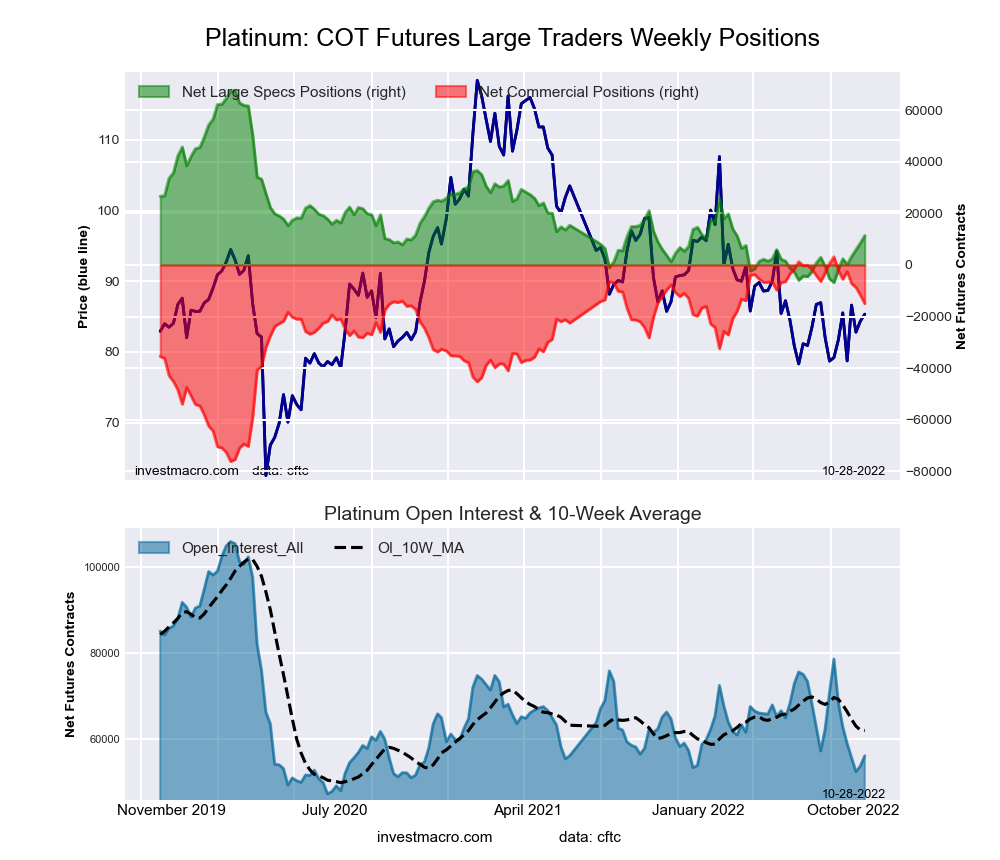

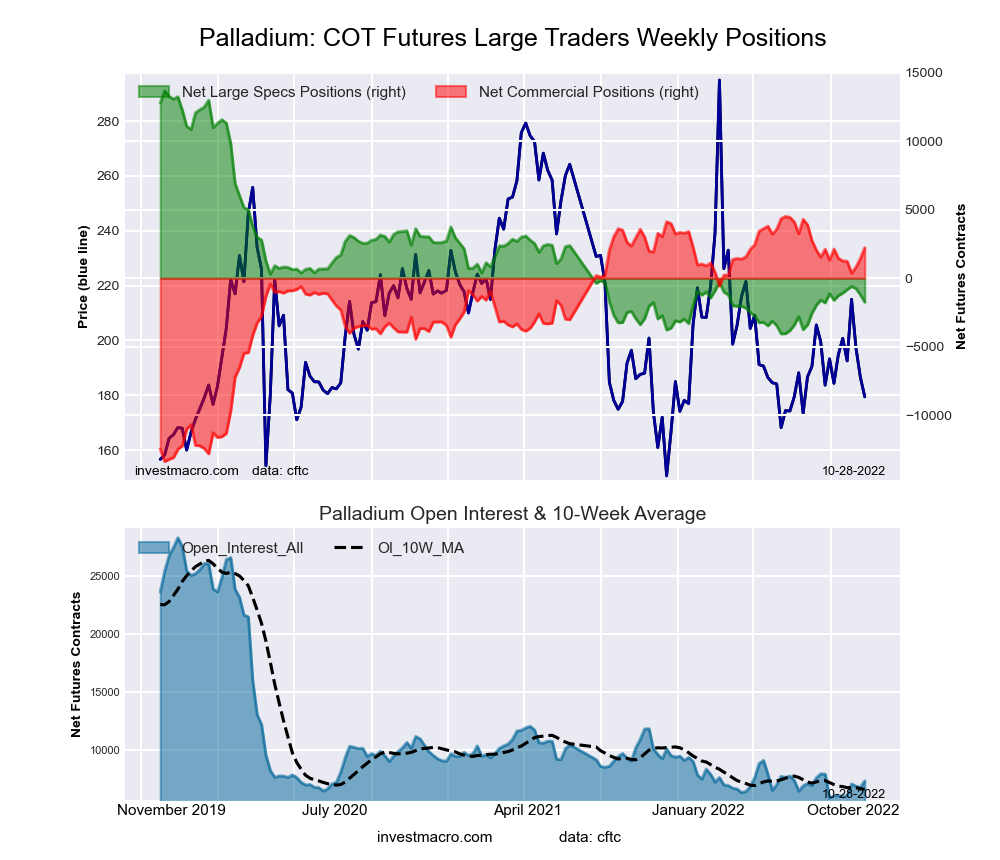

Copper and Platinum lead Weekly Speculator Changes

The COTprecious metals speculator bets were lower this week as two out of the five metals markets we cover had higher positioning this week while three markets had lower contracts.

Leading the gains for the precious metals markets was Copper (3,383 contracts) with Platinum (2,887 contracts) also showing a positive week.

The metals markets leading the declines in speculator bets this week was Gold (-8,924 contracts) with Silver (-1,368 contracts) and Palladium (-536 contracts) also registering lower bets on the week.

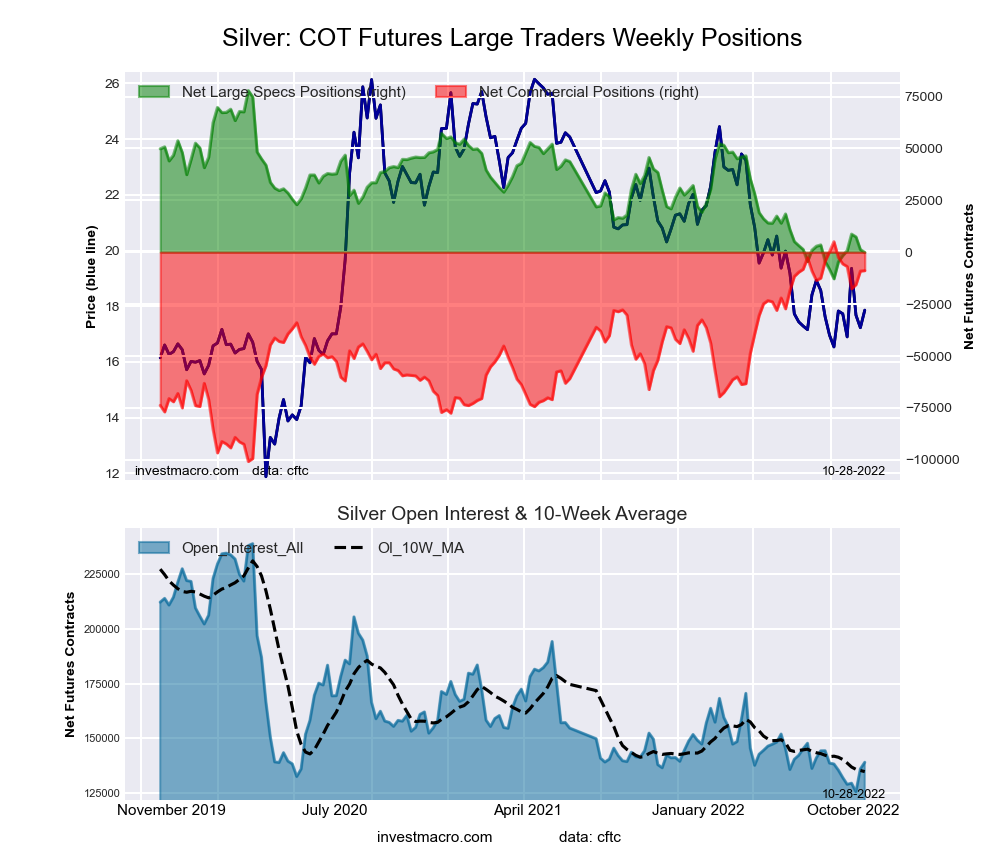

Highlighting the COT metals data this week is the decline in the speculators positions for Silver. The large speculators dropped their Silver bets for the third straight week following gains in the previous four weeks. This has brought the overall net position back into a small bearish standing this week (-101 contracts) for the first time in the past five weeks. Previously, the Silver net positioning had spent five weeks from August 23rd to September 20th in bearish territory before seeing speculator positions improve and regain their bullishness on September 27th.

The Silver price, like the other precious metals, remains under pressure and saw a small decline this week. The futures price trades around the $19.15 level and has been in a range between $18 and $20 over the past three weeks.

Data Snapshot of Commodity Market Traders | Columns Legend

Oct-25-2022

OI

OI-Index

Spec-Net

Spec-Index

Com-Net

COM-Index

Smalls-Net

Smalls-Index

WTI Crude

1,436,942

0

249,079

10

-268,026

92

18,947

32

Gold

456,072

7

68,032

5

-80,213

94

12,181

10

Silver

139,085

12

-101

14

-8,857

87

8,958

14

Copper

179,344

17

-16,919

23

15,907

79

1,012

31

Palladium

7,343

7

-1,745

14

2,228

87

-483

13

Platinum

56,117

15

11,381

24

-14,971

77

3,590

16

Natural Gas

970,872

5

-151,766

33

133,397

73

18,369

24

Brent

166,931

14

-40,301

44

36,912

55

3,389

55

Heating Oil

272,663

25

20,411

72

-38,238

31

17,827

60

Soybeans

651,685

17

57,385

31

-35,301

76

-22,084

34

Corn

1,445,842

25

329,784

72

-273,645

33

-56,139

11

Coffee

208,280

18

11,351

37

-13,326

68

1,975

27

Sugar

723,503

6

111,888

59

-140,147

43

28,259

43

Wheat

324,137

16

-12,913

2

19,896

88

-6,983

74

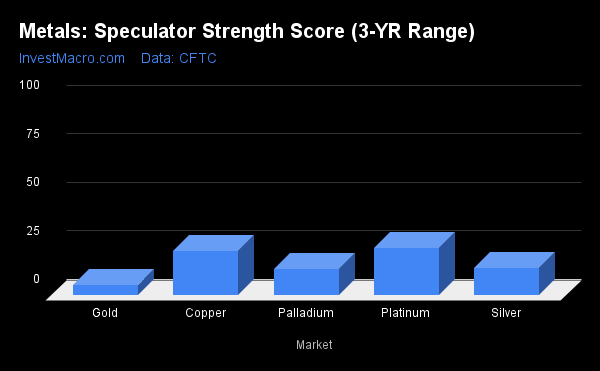

Strength Scores led by Platinum and Copper

Strength scores (a measure of the 3-Year range of Speculator positions, from 0 to 100 where above 80 is extreme bullish and below 20 is extreme bearish) show that Platinum (24.4 percent) and Copper (22.9 percent) lead the metals category.

On the downside, Gold (5.3 percent), Palladium (13.6 percent) and Silver (14.0 percent) are at the lowest strength levels currently and all are in extreme bearish positions (below 20 percent).

Strength Statistics: Gold (5.3 percent) vs Gold previous week (8.2 percent) Silver (14.0 percent) vs Silver previous week (15.5 percent) Copper (22.9 percent) vs Copper previous week (20.2 percent) Platinum (24.4 percent) vs Platinum previous week (20.5 percent) Palladium (13.6 percent) vs Palladium previous week (16.7 percent)

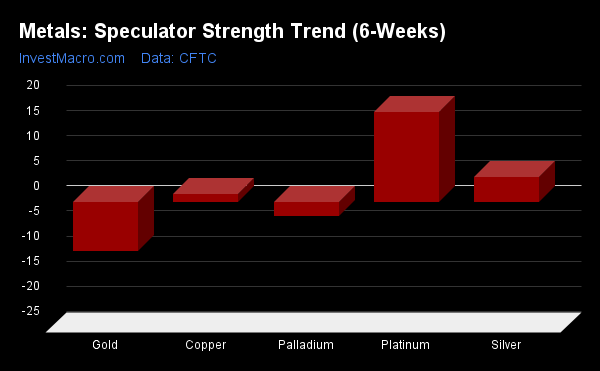

Platinum leads the Strength Trends

Strength Score Trends (or move index, calculates the 6-week changes in strength scores) show that Platinum (17.8 percent) leads the past six weeks trends for metals this week. Silver (5.0 percent) and Copper (1.6 percent) fill out the other positive movers in the latest trends data.

Gold (-9.7 percent) leads the downside trend scores currently while the next market with lower trend scores was Palladium (-2.8 percent).

Move Statistics: Gold (-9.7 percent) vs Gold previous week (-8.9 percent) Silver (5.0 percent) vs Silver previous week (15.5 percent) Copper (1.6 percent) vs Copper previous week (2.9 percent) Platinum (17.8 percent) vs Platinum previous week (20.5 percent) Palladium (-2.8 percent) vs Palladium previous week (2.3 percent)

Individual Markets:

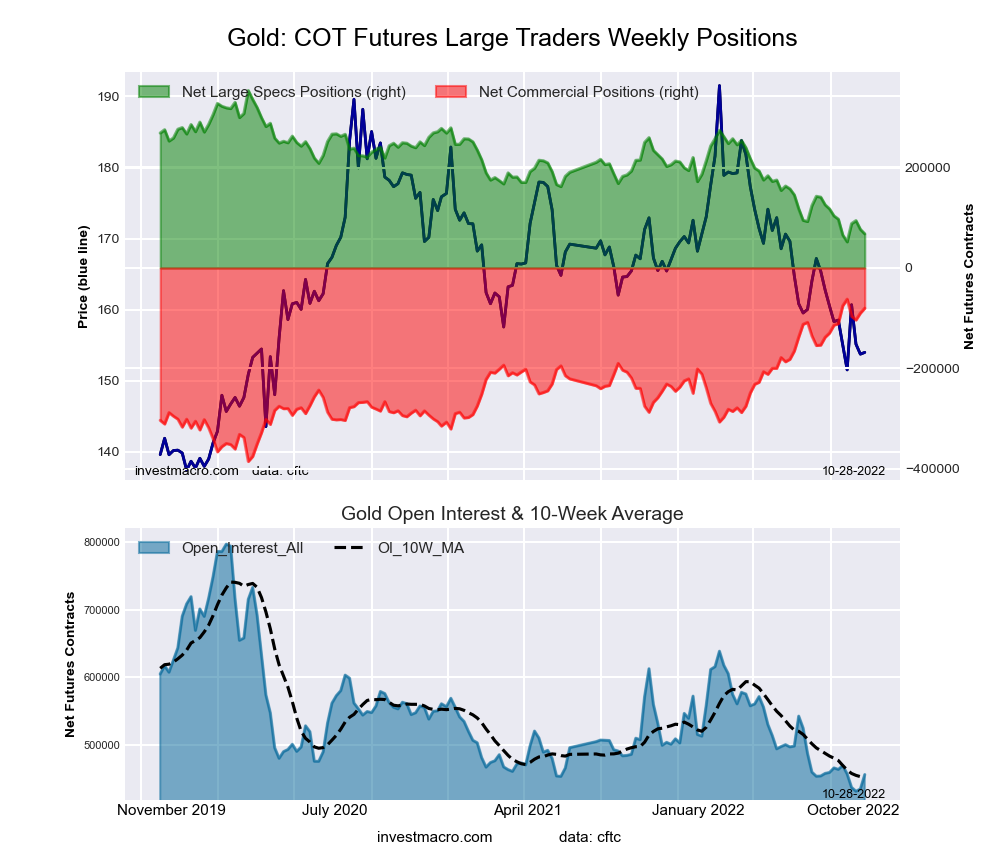

Gold Comex Futures:

The Gold Comex Futures large speculator standing this week reached a net position of 68,032 contracts in the data reported through Tuesday. This was a weekly lowering of -8,924 contracts from the previous week which had a total of 76,956 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 5.3 percent. The commercials are Bullish-Extreme with a score of 94.4 percent and the small traders (not shown in chart) are Bearish-Extreme with a score of 10.1 percent.

Gold Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

46.7

27.0

8.7

– Percent of Open Interest Shorts:

31.8

44.6

6.0

– Net Position:

68,032

-80,213

12,181

– Gross Longs:

212,853

123,085

39,637

– Gross Shorts:

144,821

203,298

27,456

– Long to Short Ratio:

1.5 to 1

0.6 to 1

1.4 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

5.3

94.4

10.1

– Strength Index Reading (3 Year Range):

Bearish-Extreme

Bullish-Extreme

Bearish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-9.7

9.5

-3.6

Silver Comex Futures:

The Silver Comex Futures large speculator standing this week reached a net position of -101 contracts in the data reported through Tuesday. This was a weekly reduction of -1,368 contracts from the previous week which had a total of 1,267 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 14.0 percent. The commercials are Bullish-Extreme with a score of 86.9 percent and the small traders (not shown in chart) are Bearish-Extreme with a score of 13.7 percent.

Silver Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

36.8

38.1

16.1

– Percent of Open Interest Shorts:

36.9

44.4

9.6

– Net Position:

-101

-8,857

8,958

– Gross Longs:

51,163

52,952

22,331

– Gross Shorts:

51,264

61,809

13,373

– Long to Short Ratio:

1.0 to 1

0.9 to 1

1.7 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

14.0

86.9

13.7

– Strength Index Reading (3 Year Range):

Bearish-Extreme

Bullish-Extreme

Bearish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

5.0

-6.0

8.5

Copper Grade #1 Futures:

The Copper Grade #1 Futures large speculator standing this week reached a net position of -16,919 contracts in the data reported through Tuesday. This was a weekly increase of 3,383 contracts from the previous week which had a total of -20,302 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 22.9 percent. The commercials are Bullish with a score of 79.3 percent and the small traders (not shown in chart) are Bearish with a score of 31.1 percent.

Copper Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

27.9

44.5

8.6

– Percent of Open Interest Shorts:

37.3

35.6

8.0

– Net Position:

-16,919

15,907

1,012

– Gross Longs:

50,000

79,742

15,339

– Gross Shorts:

66,919

63,835

14,327

– Long to Short Ratio:

0.7 to 1

1.2 to 1

1.1 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

22.9

79.3

31.1

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

1.6

-3.6

14.7

Platinum Futures:

The Platinum Futures large speculator standing this week reached a net position of 11,381 contracts in the data reported through Tuesday. This was a weekly boost of 2,887 contracts from the previous week which had a total of 8,494 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 24.4 percent. The commercials are Bullish with a score of 77.1 percent and the small traders (not shown in chart) are Bearish-Extreme with a score of 16.3 percent.

Platinum Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

50.7

33.3

12.2

– Percent of Open Interest Shorts:

30.5

60.0

5.8

– Net Position:

11,381

-14,971

3,590

– Gross Longs:

28,471

18,686

6,825

– Gross Shorts:

17,090

33,657

3,235

– Long to Short Ratio:

1.7 to 1

0.6 to 1

2.1 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

24.4

77.1

16.3

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bearish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

17.8

-16.3

-4.5

Palladium Futures:

The Palladium Futures large speculator standing this week reached a net position of -1,745 contracts in the data reported through Tuesday. This was a weekly reduction of -536 contracts from the previous week which had a total of -1,209 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 13.6 percent. The commercials are Bullish-Extreme with a score of 86.8 percent and the small traders (not shown in chart) are Bearish-Extreme with a score of 12.7 percent.

Palladium Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

22.0

60.0

14.6

– Percent of Open Interest Shorts:

45.8

29.6

21.2

– Net Position:

-1,745

2,228

-483

– Gross Longs:

1,618

4,403

1,074

– Gross Shorts:

3,363

2,175

1,557

– Long to Short Ratio:

0.5 to 1

2.0 to 1

0.7 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

13.6

86.8

12.7

– Strength Index Reading (3 Year Range):

Bearish-Extreme

Bullish-Extreme

Bearish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-2.8

4.5

-18.1

Article By InvestMacro – Receive our weekly COT Newsletter

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators) as well as their open interest (contracts open in the market at time of reporting). See CFTC criteria here.

Here are the latest charts and statistics for the Commitment of Traders (COT) reports data published by the Commodities Futures Trading Commission (CFTC).

The latest COT data is updated through Tuesday October 25th and shows a quick view of how large traders (for-profit speculators and commercial entities) were positioned in the futures markets.

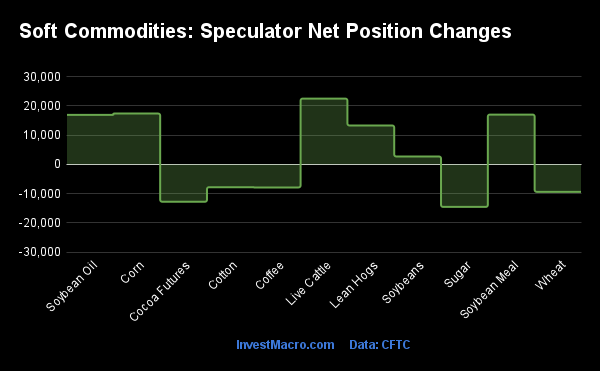

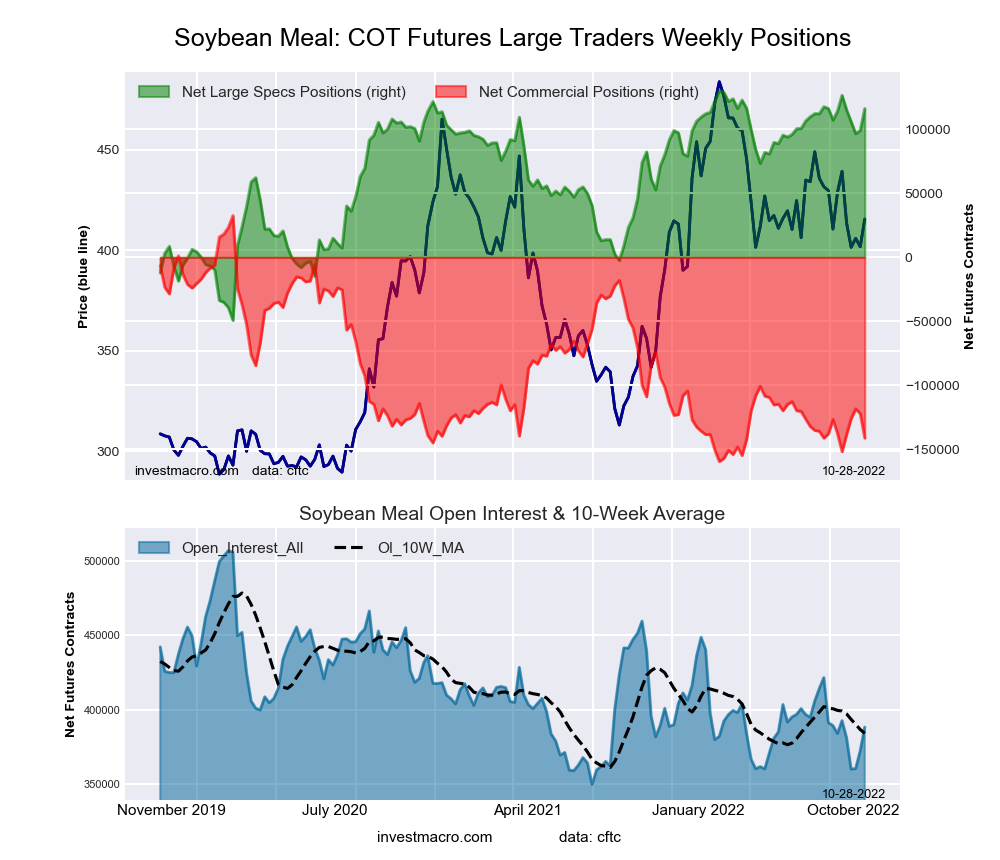

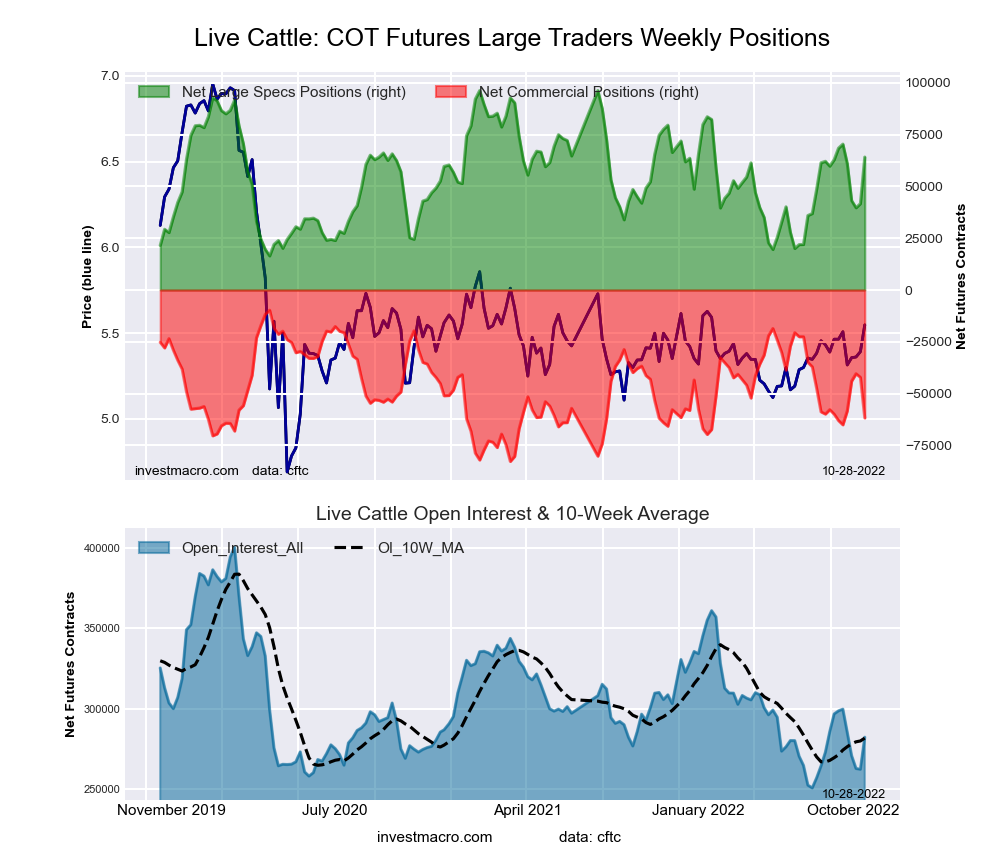

Live Cattle, Corn & Soybean Meal lead the Weekly Speculator Changes

The COT soft commodities speculator bets were slightly higher this week as six out of the eleven soft commodities markets we cover had higher positioning this week while the other five markets had decreases in contracts.

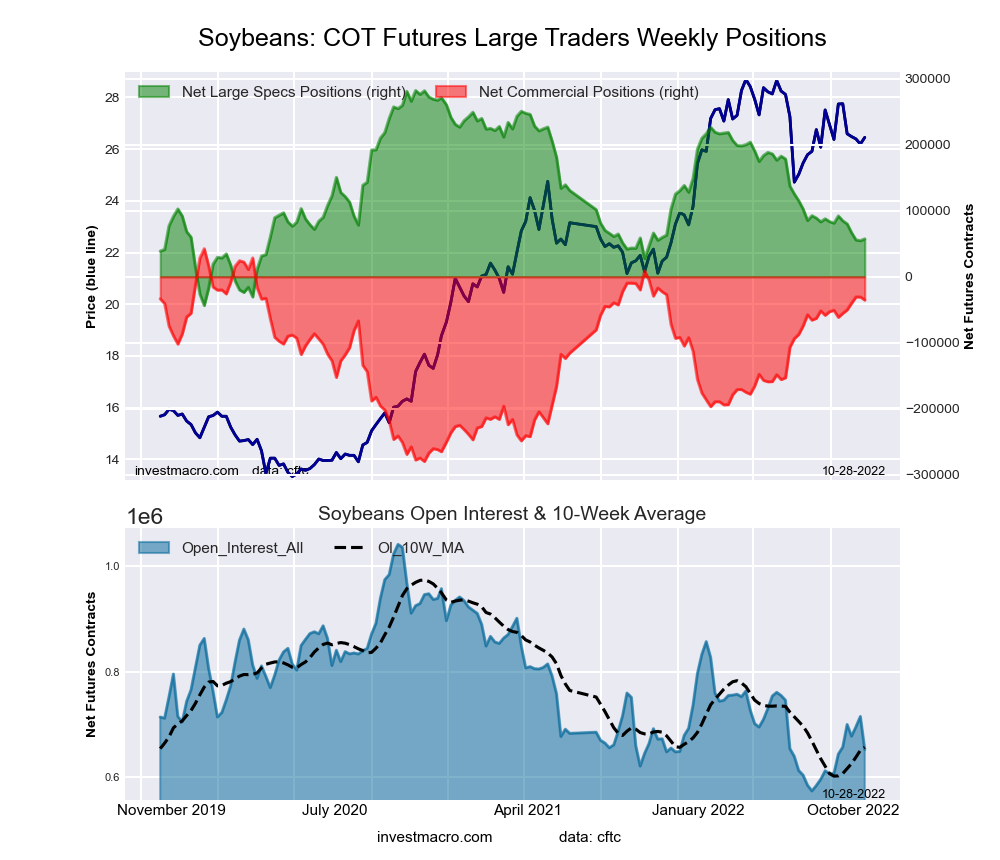

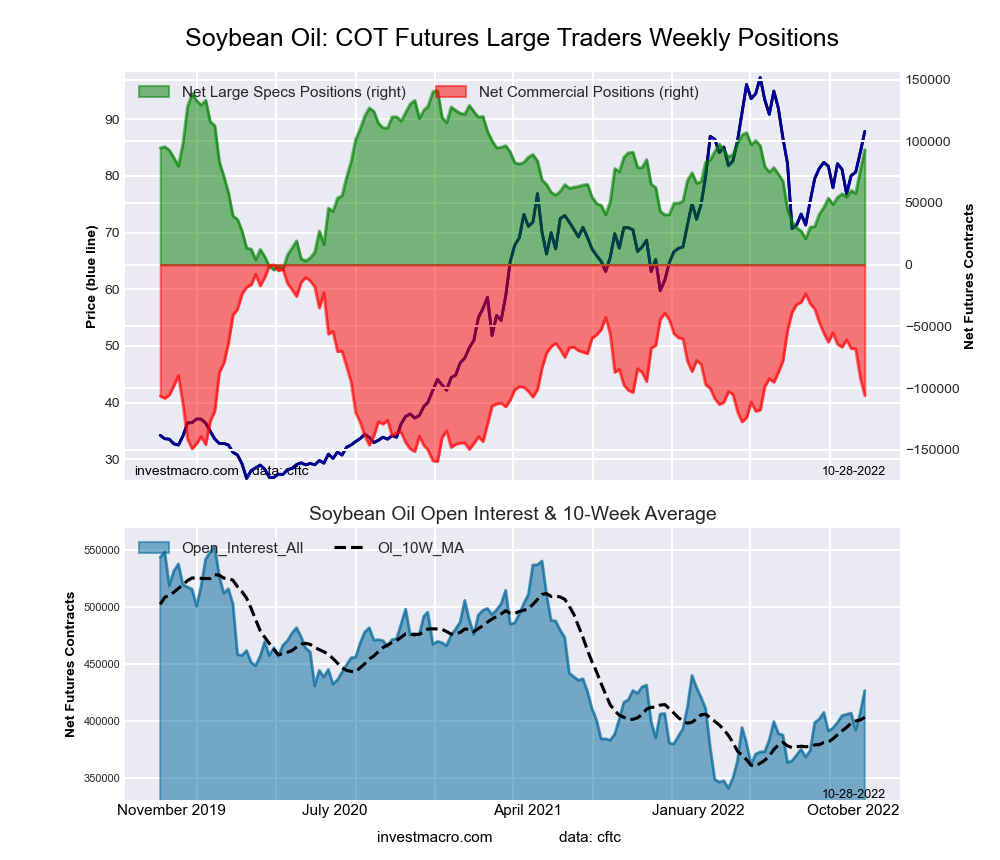

Leading the gains for soft commodities markets was Live Cattle (22,470 contracts) with Corn (17,365 contracts), Soybean Meal (17,014 contracts), Soybean Oil (16,918 contracts), Lean Hogs (13,290 contracts) and Soybeans (2,702 contracts) also showing positive weeks.

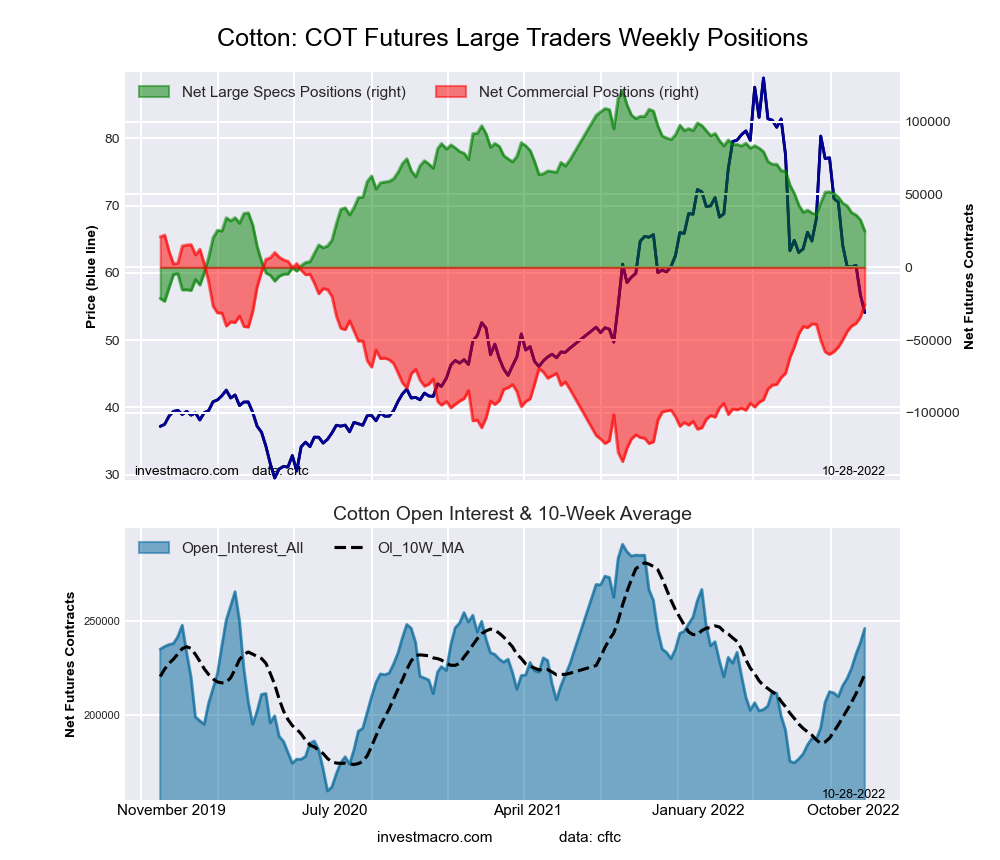

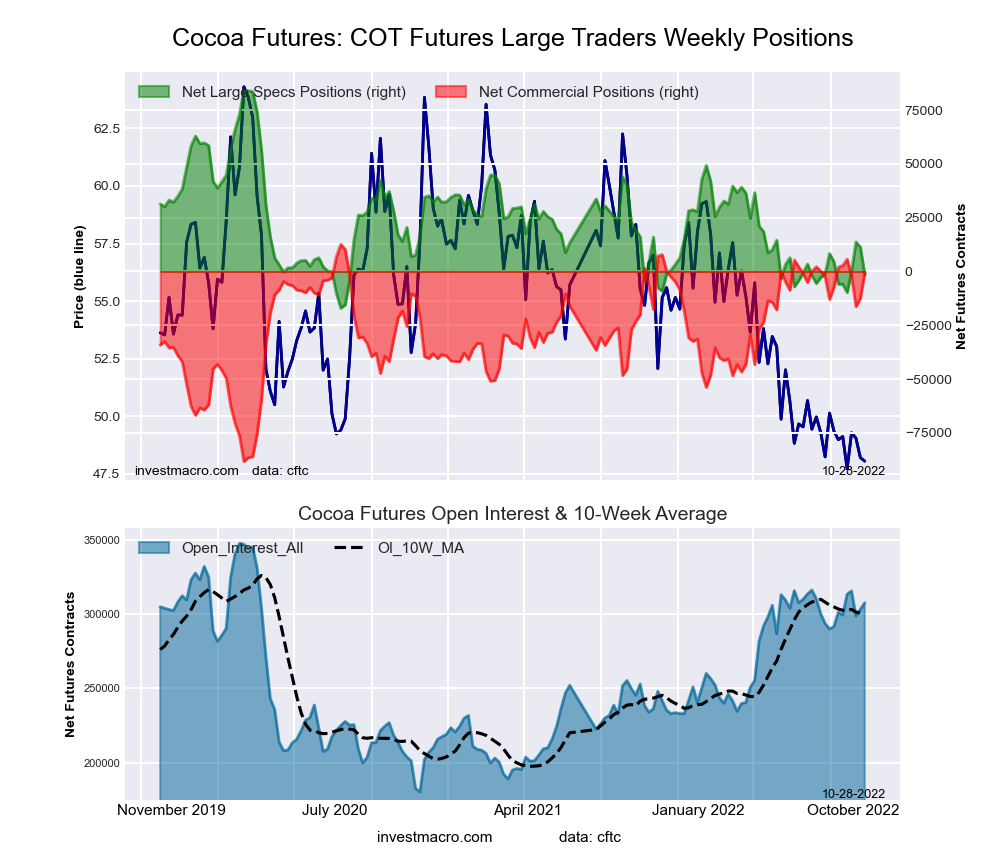

The softs market leading the declines in speculator bets this week was Sugar (-14,524 contracts) with Cocoa (-12,763 contracts), Wheat (-9,372 contracts), Coffee (-7,872 contracts) and Cotton (-7,787 contracts) also registering lower bets on the week.

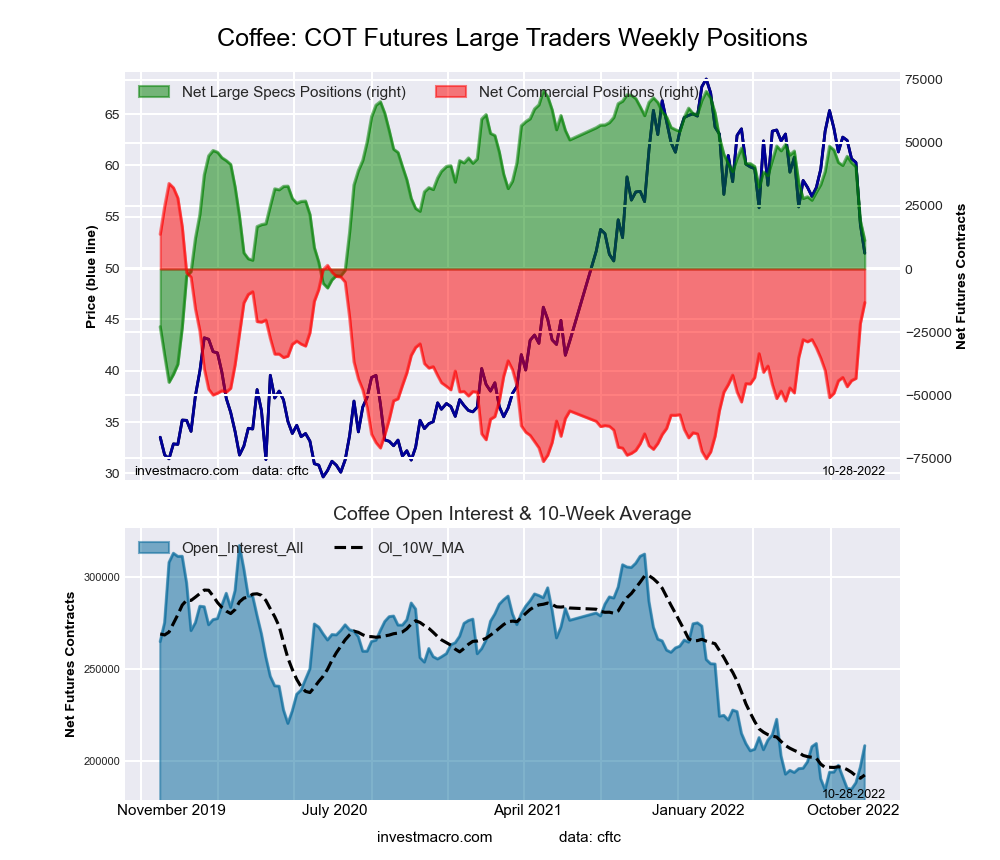

Highlighting the COT softs data this week is the continued fall in Coffee speculator positioning. Coffee large speculator bets have decreased for four straight weeks and in seven out of the past eight weeks. The recent weakness has taken a total of -37,336 contracts off the Coffee speculator position in just the past eight weeks. The overall position now sits at a total of +11,351 contracts, marking the lowest weekly level since July 21st of 2020, a span of 118 weeks.

The Coffee price has dropped by approximately 23 percent over the past three weeks and with a decline of almost 10 percent this week alone. The narrative for the Coffee price decline is that price increases have curtailed demand while a potential increase in supply out of Brazil is coming. However, the Intercontinental Exchange that monitors warehouse stocks of Arabica coffee beans has showed that Coffee stocks are at the lowest levels of the past 20 years. The short-term volatility notwithstanding, the big-picture Coffee story is one of rising worldwide demand and revenue but with some measures showing Coffee supply being hampered (current ICE Coffee stocks) and with climate change also likely to play a role in shaping the future Coffee production story as well.

Data Snapshot of Commodity Market Traders | Columns Legend

Oct-25-2022

OI

OI-Index

Spec-Net

Spec-Index

Com-Net

COM-Index

Smalls-Net

Smalls-Index

WTI Crude

1,436,942

0

249,079

10

-268,026

92

18,947

32

Gold

456,072

7

68,032

5

-80,213

94

12,181

10

Silver

139,085

12

-101

14

-8,857

87

8,958

14

Copper

179,344

17

-16,919

23

15,907

79

1,012

31

Palladium

7,343

7

-1,745

14

2,228

87

-483

13

Platinum

56,117

15

11,381

24

-14,971

77

3,590

16

Natural Gas

970,872

5

-151,766

33

133,397

73

18,369

24

Brent

166,931

14

-40,301

44

36,912

55

3,389

55

Heating Oil

272,663

25

20,411

72

-38,238

31

17,827

60

Soybeans

651,685

17

57,385

31

-35,301

76

-22,084

34

Corn

1,445,842

25

329,784

72

-273,645

33

-56,139

11

Coffee

208,280

18

11,351

37

-13,326

68

1,975

27

Sugar

723,503

6

111,888

59

-140,147

43

28,259

43

Wheat

324,137

16

-12,913

2

19,896

88

-6,983

74

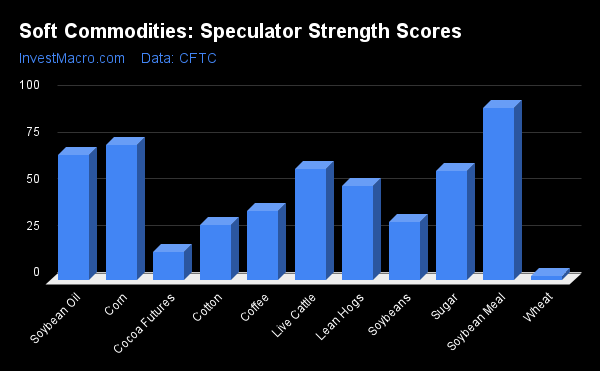

Strength Scores led by Soybean Meal

Strength Scores (a normalized measure of Speculator positions over a 3-Year range, from 0 to 100 where above 80 is extreme bullish and below 20 is extreme bearish) showed that Soybean Meal (92.1 percent) continues to lead the soft commodity markets and is in a bullish extreme position (above 80 percent). Corn (72.2 percent) and Soybean Oil (67.0 percent) come in as the next highest soft commodity markets in strength scores.

On the downside, Wheat (2.3 percent) and Cocoa (15.3 percent) come in at the lowest strength levels currently and are both in bearish extreme standings (below 20 percent).

Strength Statistics: Corn (72.2 percent) vs Corn previous week (69.9 percent) Sugar (58.7 percent) vs Sugar previous week (61.7 percent) Coffee (36.8 percent) vs Coffee previous week (45.2 percent) Soybeans (31.0 percent) vs Soybeans previous week (30.2 percent) Soybean Oil (67.0 percent) vs Soybean Oil previous week (55.4 percent) Soybean Meal (92.1 percent) vs Soybean Meal previous week (82.7 percent) Live Cattle (59.8 percent) vs Live Cattle previous week (31.6 percent) Lean Hogs (50.7 percent) vs Lean Hogs previous week (36.3 percent) Cotton (29.6 percent) vs Cotton previous week (35.3 percent) Cocoa (15.3 percent) vs Cocoa previous week (27.9 percent) Wheat (2.3 percent) vs Wheat previous week (14.4 percent)

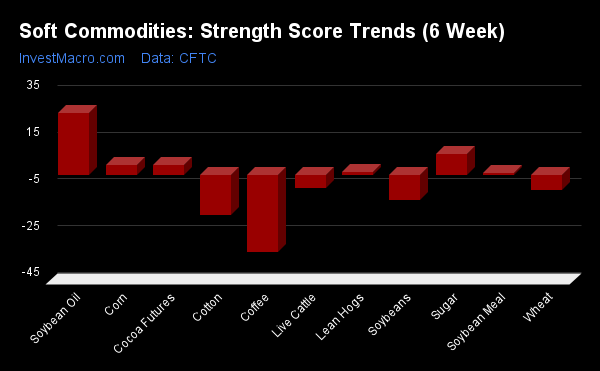

Strength Trends led by Soybean Oil and Sugar

Strength Score Trends (or move index, calculates the 6-week changes in strength scores) show that Soybean Oil (26.6 percent) leads the past six weeks trends for soft commodity markets this week. Sugar (9.2 percent), Corn (4.5 percent) and Cocoa (4.3 percent) are the next highest movers in the latest trends data.

Coffee (-32.9 percent) leads the downside trend scores currently while the next markets with lower trend scores were Cotton (-17.0 percent) followed by Soybeans (-10.7 percent).

Strength Trend Statistics: Corn (4.5 percent) vs Corn previous week (3.3 percent) Sugar (9.2 percent) vs Sugar previous week (14.4 percent) Coffee (-32.9 percent) vs Coffee previous week (-29.7 percent) Soybeans (-10.7 percent) vs Soybeans previous week (-8.2 percent) Soybean Oil (26.6 percent) vs Soybean Oil previous week (18.9 percent) Soybean Meal (1.1 percent) vs Soybean Meal previous week (-4.5 percent) Live Cattle (-5.4 percent) vs Live Cattle previous week (-26.5 percent) Lean Hogs (1.3 percent) vs Lean Hogs previous week (-10.1 percent) Cotton (-17.0 percent) vs Cotton previous week (-13.2 percent) Cocoa (4.3 percent) vs Cocoa previous week (6.7 percent) Wheat (-6.2 percent) vs Wheat previous week (8.1 percent)

Individual Soft Commodities Markets:

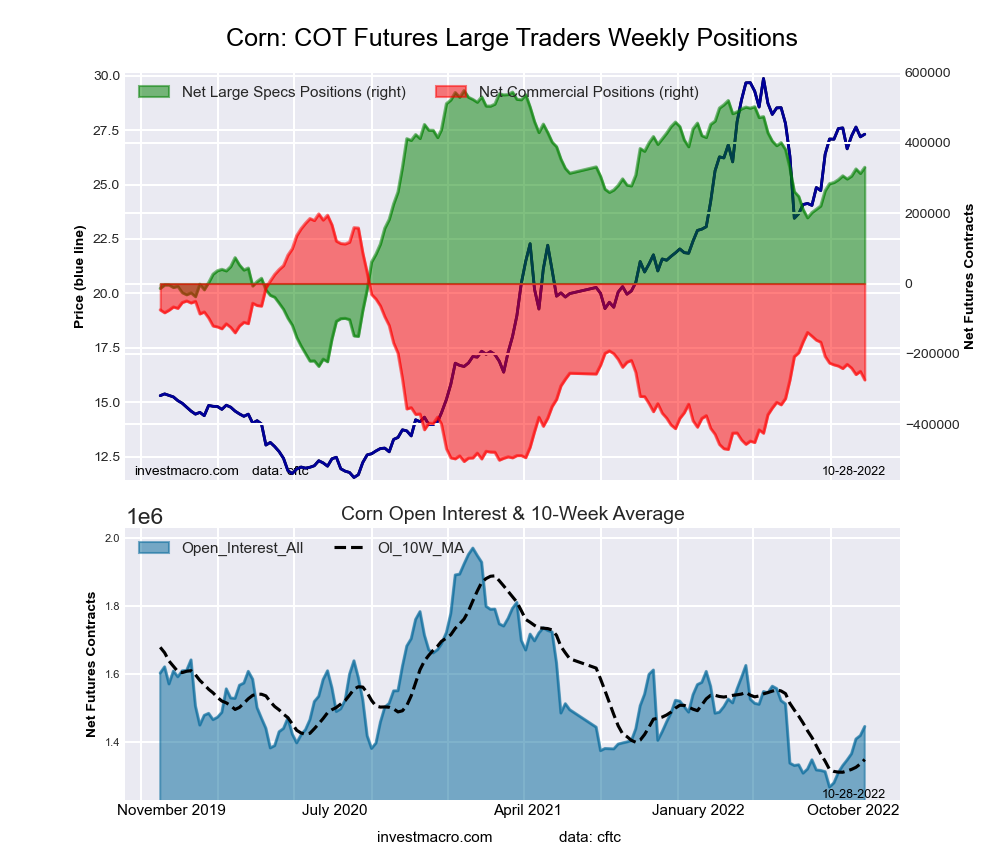

CORN Futures:

The CORN large speculator standing this week was a net position of 329,784 contracts in the data reported through Tuesday. This was a weekly rise of 17,365 contracts from the previous week which had a total of 312,419 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 72.2 percent. The commercials are Bearish with a score of 32.9 percent and the small traders (not shown in chart) are Bearish-Extreme with a score of 10.8 percent.

CORN Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

31.3

43.3

8.9

– Percent of Open Interest Shorts:

8.5

62.2

12.8

– Net Position:

329,784

-273,645

-56,139

– Gross Longs:

453,036

625,537

129,121

– Gross Shorts:

123,252

899,182

185,260

– Long to Short Ratio:

3.7 to 1

0.7 to 1

0.7 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

72.2

32.9

10.8

– Strength Index Reading (3 Year Range):

Bullish

Bearish

Bearish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

4.5

-5.6

2.5

SUGAR Futures:

The SUGAR large speculator standing this week was a net position of 111,888 contracts in the data reported through Tuesday. This was a weekly decline of -14,524 contracts from the previous week which had a total of 126,412 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 58.7 percent. The commercials are Bearish with a score of 43.3 percent and the small traders (not shown in chart) are Bearish with a score of 42.8 percent.

SUGAR Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

27.6

50.8

10.1

– Percent of Open Interest Shorts:

12.1

70.1

6.2

– Net Position:

111,888

-140,147

28,259

– Gross Longs:

199,761

367,374

72,823

– Gross Shorts:

87,873

507,521

44,564

– Long to Short Ratio:

2.3 to 1

0.7 to 1

1.6 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

58.7

43.3

42.8

– Strength Index Reading (3 Year Range):

Bullish

Bearish

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

9.2

-12.0

21.2

COFFEE Futures:

The COFFEE large speculator standing this week was a net position of 11,351 contracts in the data reported through Tuesday. This was a weekly lowering of -7,872 contracts from the previous week which had a total of 19,223 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 36.8 percent. The commercials are Bullish with a score of 67.7 percent and the small traders (not shown in chart) are Bearish with a score of 26.9 percent.

COFFEE Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

20.2

50.9

4.7

– Percent of Open Interest Shorts:

14.8

57.3

3.8

– Net Position:

11,351

-13,326

1,975

– Gross Longs:

42,119

106,110

9,859

– Gross Shorts:

30,768

119,436

7,884

– Long to Short Ratio:

1.4 to 1

0.9 to 1

1.3 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

36.8

67.7

26.9

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-32.9

33.3

-1.6

SOYBEANS Futures:

The SOYBEANS large speculator standing this week was a net position of 57,385 contracts in the data reported through Tuesday. This was a weekly rise of 2,702 contracts from the previous week which had a total of 54,683 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 31.0 percent. The commercials are Bullish with a score of 75.9 percent and the small traders (not shown in chart) are Bearish with a score of 33.8 percent.

SOYBEANS Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

19.4

54.4

7.9

– Percent of Open Interest Shorts:

10.6

59.8

11.3

– Net Position:

57,385

-35,301

-22,084

– Gross Longs:

126,693

354,542

51,670

– Gross Shorts:

69,308

389,843

73,754

– Long to Short Ratio:

1.8 to 1

0.9 to 1

0.7 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

31.0

75.9

33.8

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-10.7

8.1

14.6

SOYBEAN OIL Futures:

The SOYBEAN OIL large speculator standing this week was a net position of 93,241 contracts in the data reported through Tuesday. This was a weekly increase of 16,918 contracts from the previous week which had a total of 76,323 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 67.0 percent. The commercials are Bearish with a score of 33.6 percent and the small traders (not shown in chart) are Bullish with a score of 61.2 percent.

SOYBEAN OIL Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

29.0

43.0

8.7

– Percent of Open Interest Shorts:

7.1

67.9

5.7

– Net Position:

93,241

-106,036

12,795

– Gross Longs:

123,538

183,248

37,167

– Gross Shorts:

30,297

289,284

24,372

– Long to Short Ratio:

4.1 to 1

0.6 to 1

1.5 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

67.0

33.6

61.2

– Strength Index Reading (3 Year Range):

Bullish

Bearish

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

26.6

-26.1

11.0

SOYBEAN MEAL Futures:

The SOYBEAN MEAL large speculator standing this week was a net position of 116,146 contracts in the data reported through Tuesday. This was a weekly gain of 17,014 contracts from the previous week which had a total of 99,132 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 92.1 percent. The commercials are Bearish-Extreme with a score of 9.5 percent and the small traders (not shown in chart) are Bullish with a score of 62.9 percent.

SOYBEAN MEAL Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

33.6

39.7

12.6

– Percent of Open Interest Shorts:

3.7

76.0

6.1

– Net Position:

116,146

-141,232

25,086

– Gross Longs:

130,508

153,931

48,845

– Gross Shorts:

14,362

295,163

23,759

– Long to Short Ratio:

9.1 to 1

0.5 to 1

2.1 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

92.1

9.5

62.9

– Strength Index Reading (3 Year Range):

Bullish-Extreme

Bearish-Extreme

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

1.1

-1.8

7.7

LIVE CATTLE Futures:

The LIVE CATTLE large speculator standing this week was a net position of 64,126 contracts in the data reported through Tuesday. This was a weekly lift of 22,470 contracts from the previous week which had a total of 41,656 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 59.8 percent. The commercials are Bearish with a score of 28.8 percent and the small traders (not shown in chart) are Bullish-Extreme with a score of 86.7 percent.

LIVE CATTLE Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

37.5

32.1

10.8

– Percent of Open Interest Shorts:

14.7

53.9

11.7

– Net Position:

64,126

-61,708

-2,418

– Gross Longs:

105,722

90,481

30,509

– Gross Shorts:

41,596

152,189

32,927

– Long to Short Ratio:

2.5 to 1

0.6 to 1

0.9 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

59.8

28.8

86.7

– Strength Index Reading (3 Year Range):

Bullish

Bearish

Bullish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-5.4

1.8

12.3

LEAN HOGS Futures:

The LEAN HOGS large speculator standing this week was a net position of 40,379 contracts in the data reported through Tuesday. This was a weekly advance of 13,290 contracts from the previous week which had a total of 27,089 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 50.7 percent. The commercials are Bullish with a score of 57.6 percent and the small traders (not shown in chart) are Bearish with a score of 44.4 percent.

LEAN HOGS Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

40.1

33.2

9.2

– Percent of Open Interest Shorts:

19.7

48.6

14.3

– Net Position:

40,379

-30,337

-10,042

– Gross Longs:

79,180

65,528

18,149

– Gross Shorts:

38,801

95,865

28,191

– Long to Short Ratio:

2.0 to 1

0.7 to 1

0.6 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

50.7

57.6

44.4

– Strength Index Reading (3 Year Range):

Bullish

Bullish

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

1.3

-0.1

-5.9

COTTON Futures:

The COTTON large speculator standing this week was a net position of 24,776 contracts in the data reported through Tuesday. This was a weekly decline of -7,787 contracts from the previous week which had a total of 32,563 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 29.6 percent. The commercials are Bullish with a score of 72.3 percent and the small traders (not shown in chart) are Bearish-Extreme with a score of 16.2 percent.

COTTON Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

29.0

49.3

5.3

– Percent of Open Interest Shorts:

18.9

59.7

4.9

– Net Position:

24,776

-25,690

914

– Gross Longs:

71,296

121,240

13,075

– Gross Shorts:

46,520

146,930

12,161

– Long to Short Ratio:

1.5 to 1

0.8 to 1

1.1 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

29.6

72.3

16.2

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bearish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-17.0

19.5

-37.1

COCOA Futures:

The COCOA large speculator standing this week was a net position of -1,545 contracts in the data reported through Tuesday. This was a weekly fall of -12,763 contracts from the previous week which had a total of 11,218 net contracts.