Source: Streetwise Reports (12/22/22)

For new investors, mining stocks can be an excellent gateway to learning about investing in general. Explore how and where you can buy gold stocks and more.

Are you one of the many people who go through life with a vague curiosity about investing?

Perhaps you think you’ll get to it when you’re older or when you have more disposable income. Maybe you see it as gambling and, although interested, you don’t really know where to begin. If that sounds like you, then this guide will serve as a pathway to your investing future. We’ll help you explore the major types of metals people buy and show you some places to buy them.

Explore the most popular types of metal stocks people invest in, including what they are, where you can research them, and how you can begin investing the moment you finish this article.

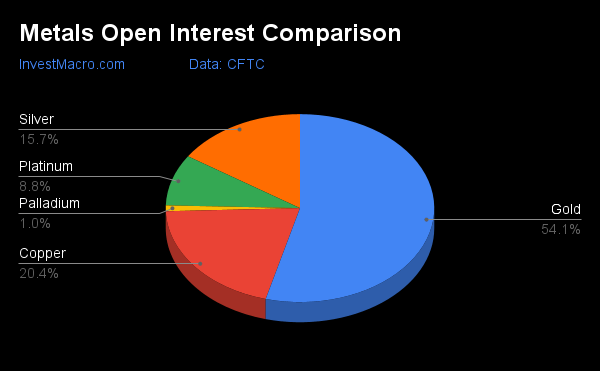

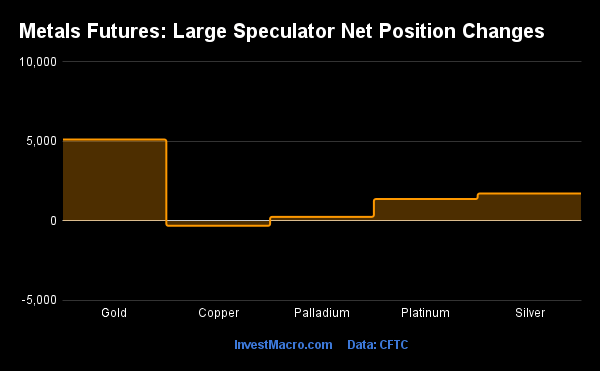

Which Metals Do People Invest In?

While the most common mining stocks people invest in are gold and silver stocks, most others are viable investments as well. When you buy the stock of a particular metal, like gold stocks, you’re actually investing in one of the companies that mines that particular mineral. It’s these types of metal stocks that are covered in this article, not purchasing physical metals.

Nevertheless, it helps as an investor to understand what makes these metals so highly valued in the first place. From the beginning of time and throughout every culture, gold, silver, nickel, and other metals have been used as currency.

When America issued its first paper money in 1690, these metals remained valuable. From jewelry to circuitry, building to computing, these metals are deeply ingrained into our society.

Unique for their hardness, beauty, and rarity, precious metals are known as one of the safest and most traditionally stable assets you can invest in.

Precious Metals

The main type of metals people invest in is also the rarest and most valuable. Precious metal stocks are primarily used as a hedge against inflation, and gold, silver, and platinum are the most popular.

Each metal has its own traits, tendencies in the market, and uses in society. Learn more about precious metals and consider which might be worth adding to your portfolio.

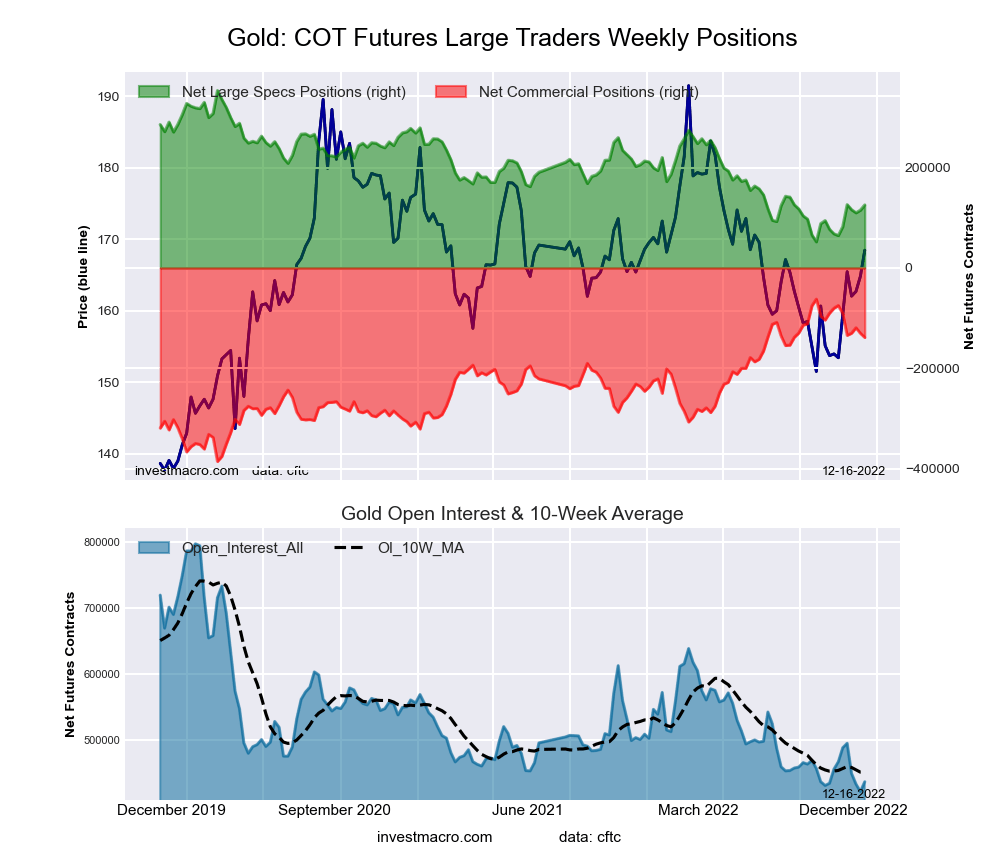

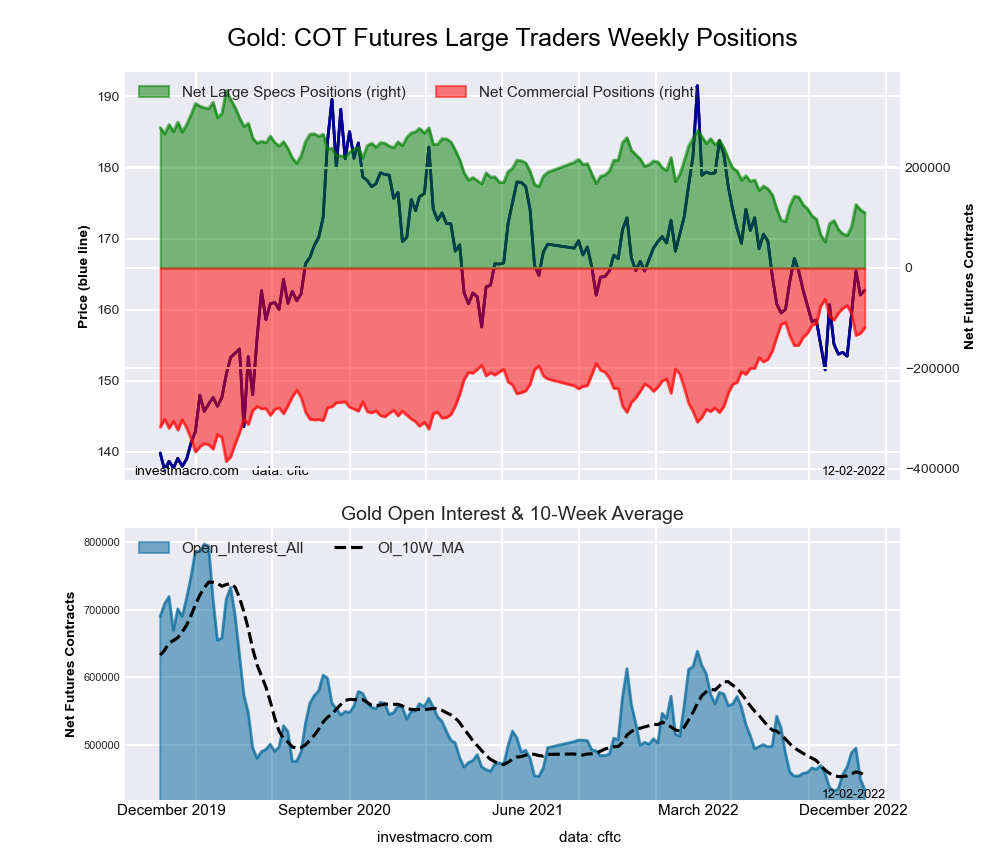

Gold

Ancient civilizations placed a lot of value on gold; thousands of years later, it’s still one of the most highly-coveted substances on Earth. Most frequently used as jewelry and a form of currency, gold has special traits that add to its mystique. These include

Unique Facts About Gold

– Gold is special in that it doesn’t rust or corrode and can conduct heat and electricity.

– The United States has the largest reserve of gold in the world, with 8,867 tons.

– Investors love gold and gold stocks for their tendency to hold value in volatile markets.

Where Can You Learn More About Investing in Gold?

As the most widely-invested metal, there are numerous sources of information on gold stocks and other gold-related investments. Some reputable sources you may want to explore include The Gold Report, Barron’s, and USAGOLD.

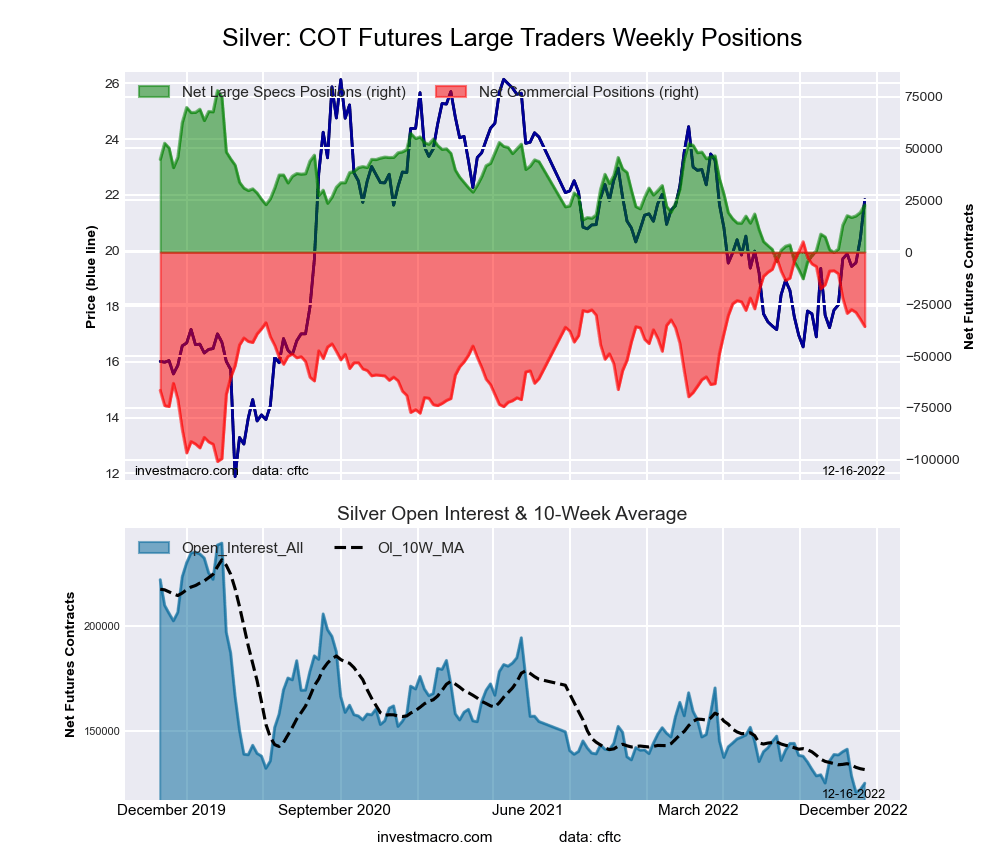

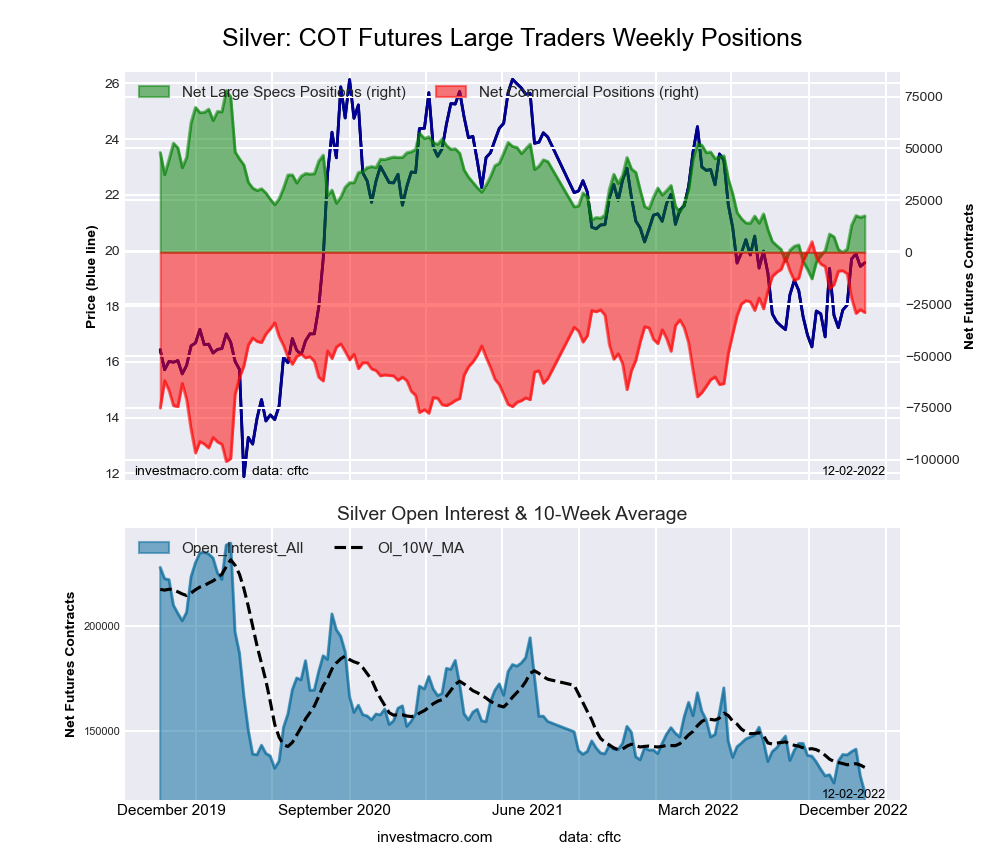

Silver

Also a staple in jewelry, in addition to numerous other things, silver is less precious but far more useful than gold. From scrap to batteries, smartphones to car parts, silver is highly-versatile and constantly in demand.

Unique Facts About Silver

– Silver is one of the easiest investments to liquidate; jewelers will pay the market price for silver.

– Unlike stocks, silver is never likely to crash because it holds real-world, inherent value.

– One of the oldest elements, silver has been traded as a currency since 700 BC.

Whether you choose to invest in silver or silver stocks, consider it a viable and popular investment to add to your portfolio.

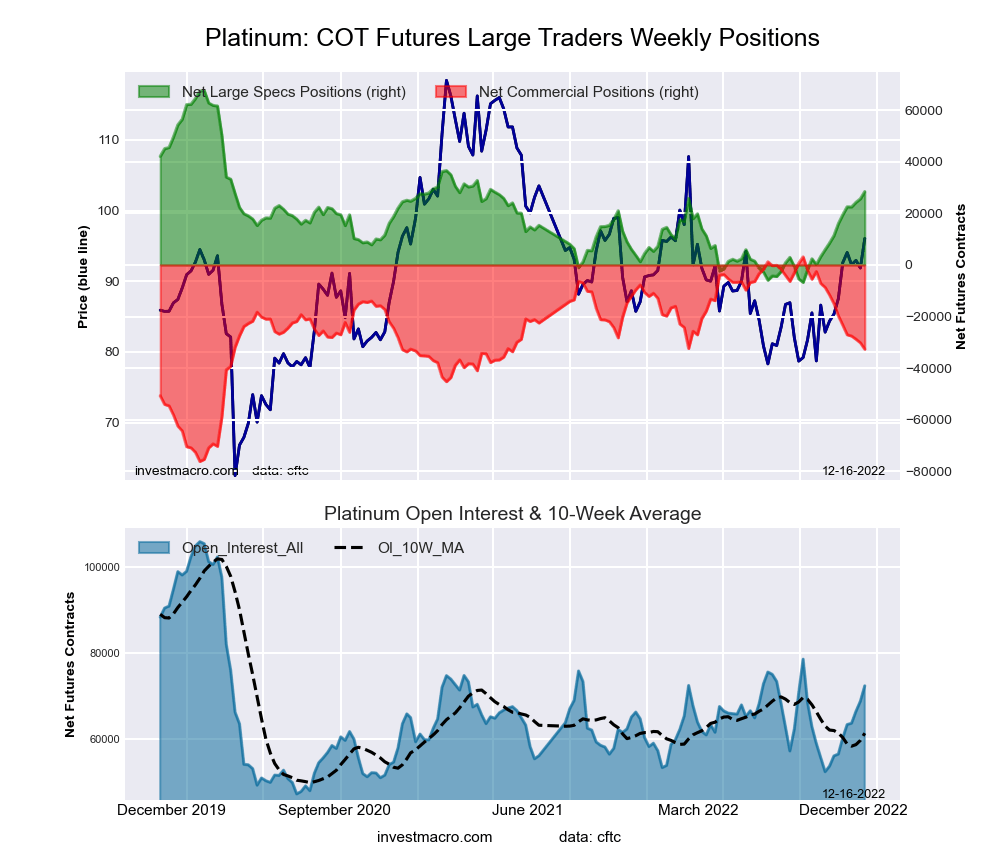

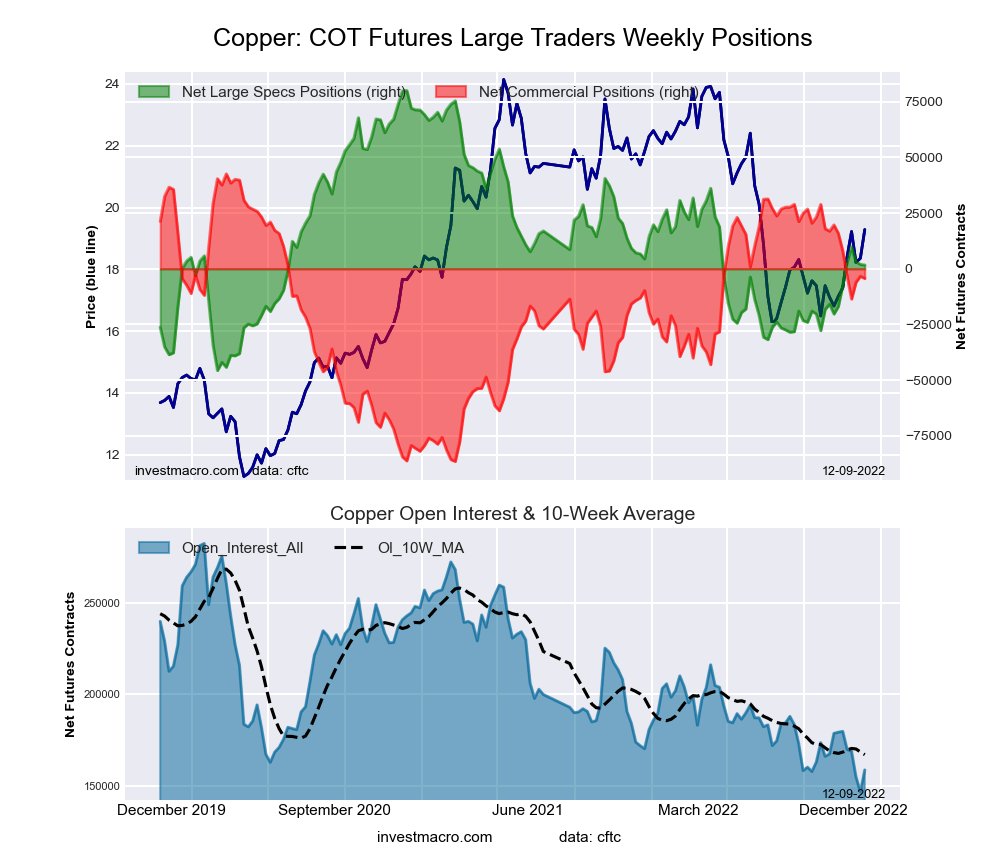

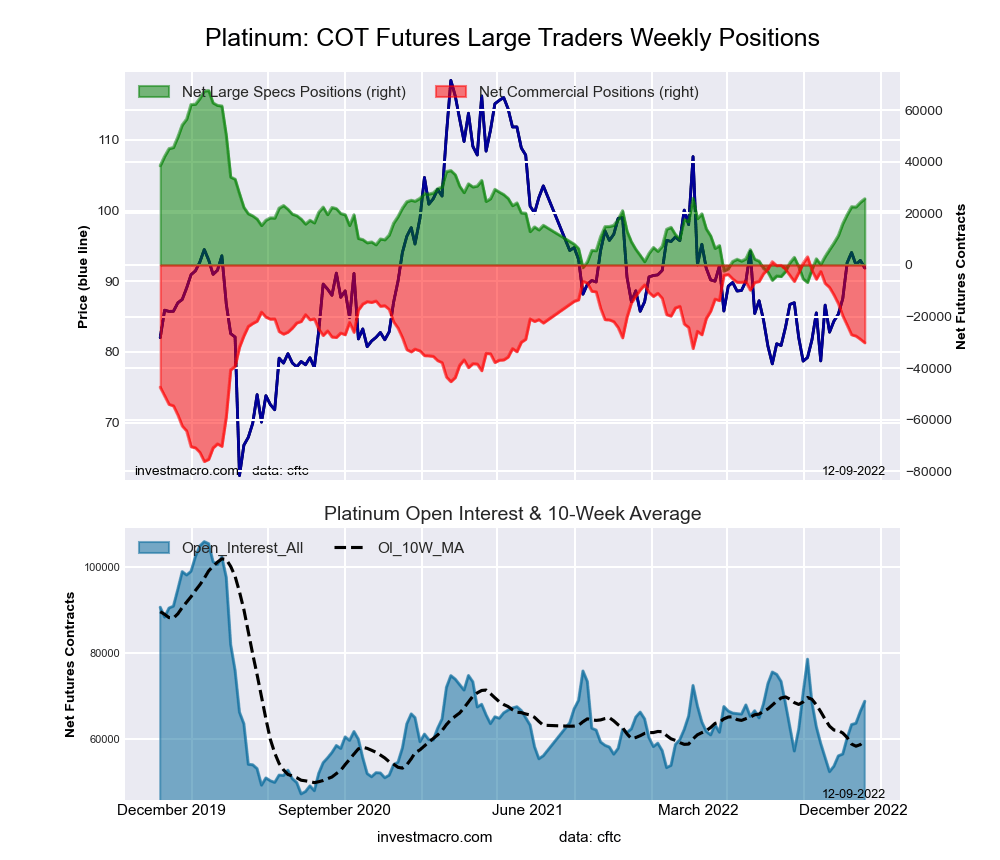

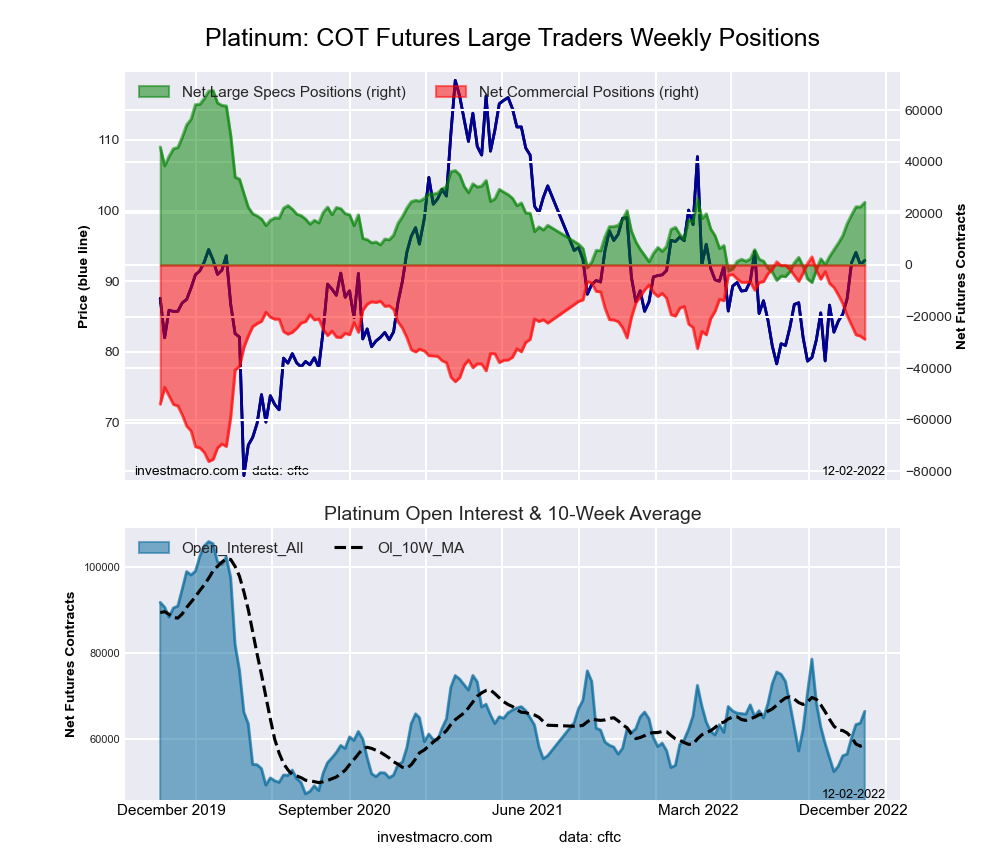

Platinum

Rounding out the top three precious metals, platinum is just as highly-coveted as gold and silver. As the only material suitable for the electrodes in pacemakers, platinum is extremely valuable to humanity as well as savvy investors.

Unique Facts About Platinum

– The price of platinum typically fluctuates with manufacturing and industrial industries.

– Platinum is even rarer than gold; all the platinum ever found would fill a pool up to your ankles.

– Platinum is among the heaviest metals: a 6-inch cube weighs as much as an average person.

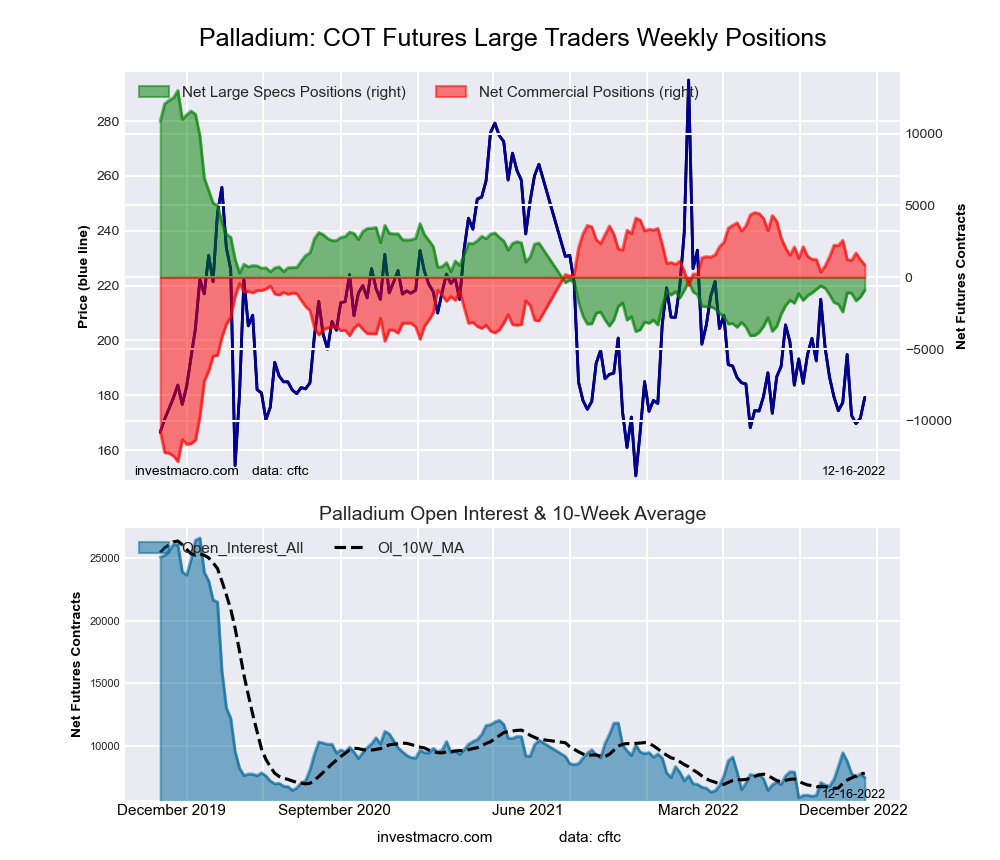

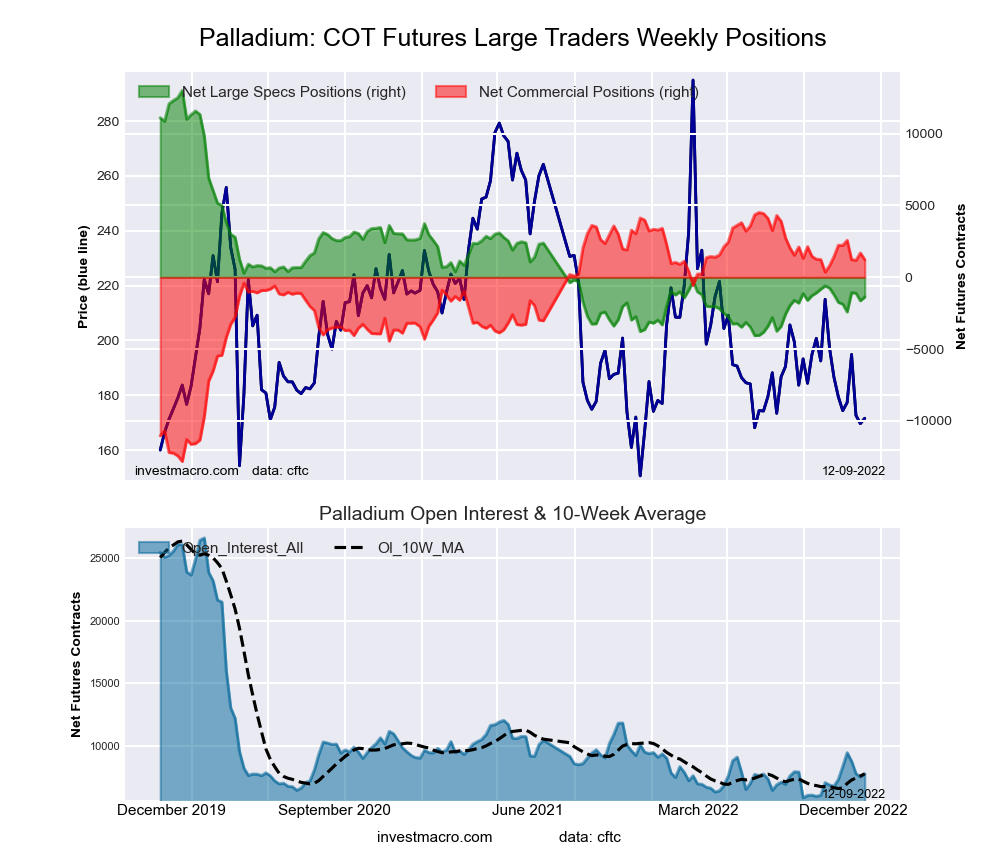

Palladium and Other Precious Metals

The list of precious metals goes far beyond the three most popular options. From palladium to rhodium, there are numerous metals available, each with its own value as an investment.

If you’re curious about some of the other precious metals you can invest in, here’s a list of some that are worth exploring:

- Palladium

- Rhodium

- Ruthenium

- Osmium

- Iridium

Whichever precious metal appeals most to you, it’s worth taking some time to research how they’re known to perform as an investment.

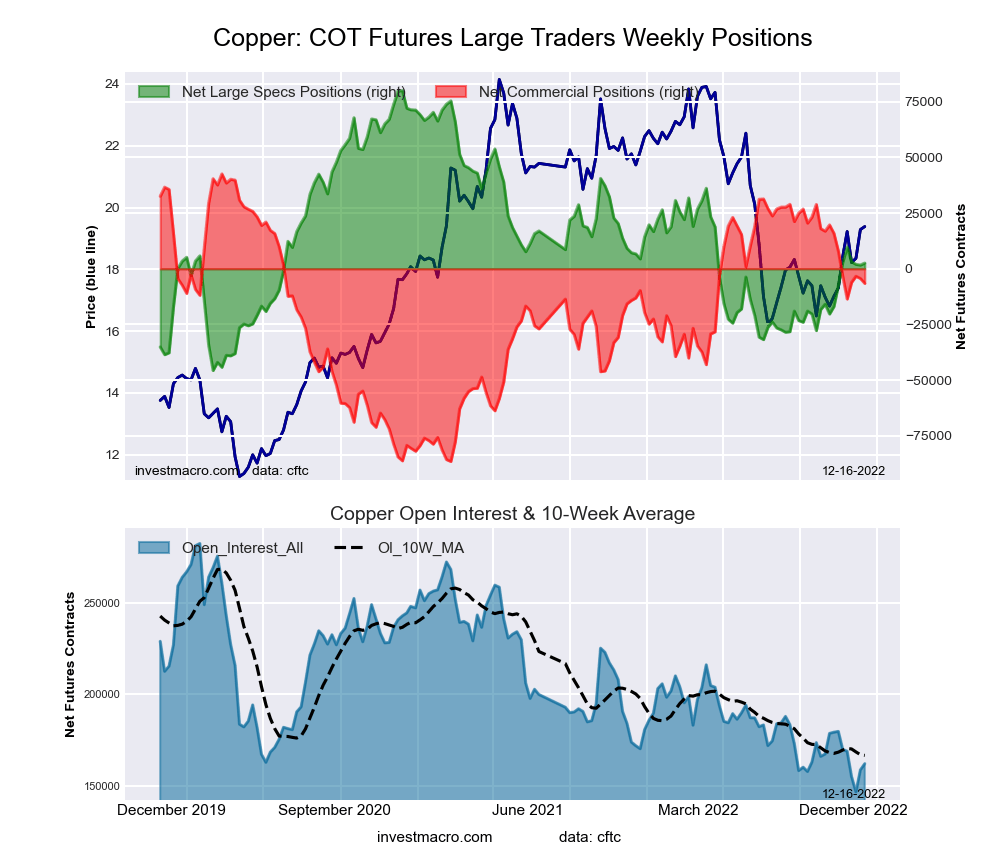

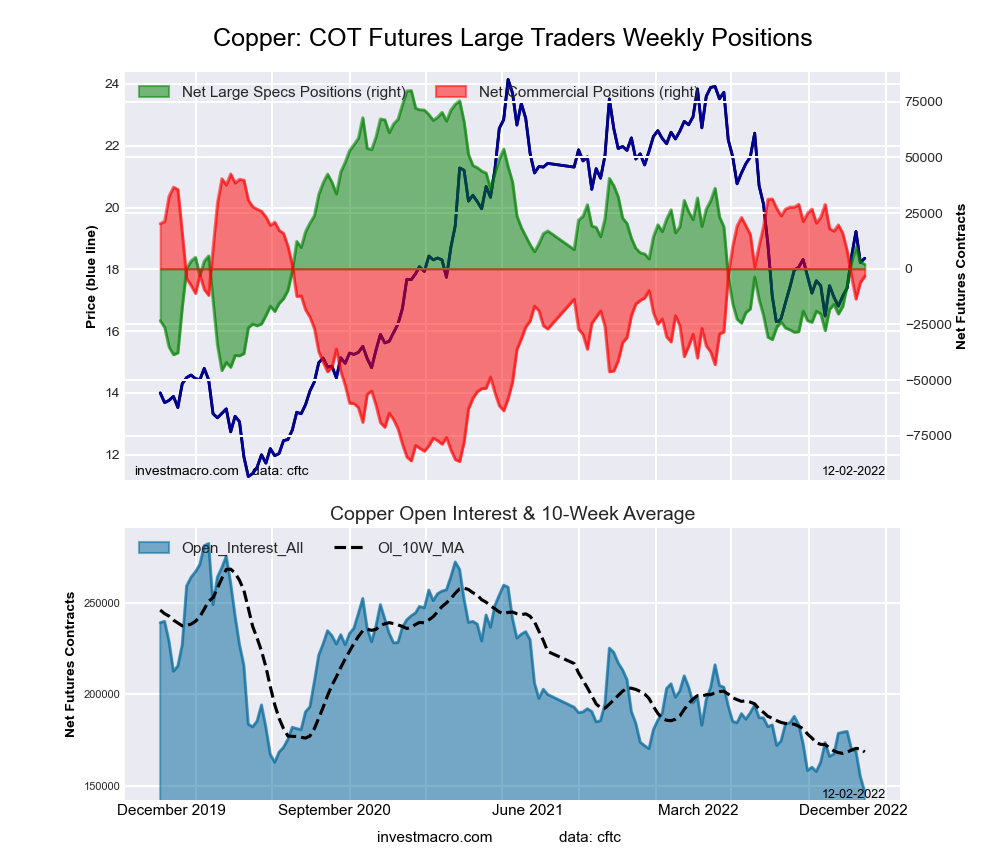

Brief Note on Base Metals

In addition to precious metals, you can also choose to invest in base metals. Base metals are used in manufacturing and are typically more vulnerable to corrosion than precious metals.

Common examples of base metals include iron, steel, copper, nickel, aluminum, lead, zinc, tin, and tungsten. While they lack the rarity of precious metals, base metals are in high demand nonetheless, so consider investing in them to balance your portfolio.

How to Start Investing in Mining Stocks

Whenever you’re ready to buy stocks from a company that mines a particular metal, there are many safe places to do it online.

The first thing you’ll need to begin trading stocks online is your credit card, bank account info, or another account, like PayPal for example. This information will be required when making an account so you can buy stocks and metals online.

Making purchases is easy, regardless of the site you’re using. I recommend a few you may want to look into below.

When reviewing investments, there are numbers and symbols that can get confusing until you know what they mean. Remember that it’s critical to understand the measurements of the metals you’re buying and to stay within your budget while investing.

Once you’ve bought metal stocks, you can monitor their progress over time. If you need to liquidate your money by selling the stocks, every stock site will have slightly different guidelines for doing so.

Important Notes on Mining Stocks

If you plan on buying precious metals stocks, it’s worth having a formidable understanding of mining stocks. Here are some useful things to know before purchasing silver stocks or any other mining stock.

The Two Types of Mining Stocks: Juniors and Majors

Juniors are typically related to mining commodities like oil and natural gas. It’s important to know that they’re a risky investment compared to majors.

Junior mining companies are involved in exploring, preparing, and attaining permits for various metals.

Majors are widely considered a safer and much more mature investment. Majors are typically much larger companies that have been successfully mining and producing metals for many years.

What Factors Affect Mining Stocks?

Every type of stock is impacted by different factors, and the same is true for mining stocks.

Factors like fluctuating cost of the metal their mining and external problems at the physical mine, including geopolitical conflict and weather, all affect mining stock prices.

Where are the Best Places to Invest Online?

It’s worthwhile to check out multiple options before choosing which site to purchase mining stocks from. Each site will have unique pricing plans, features, and rules for liquidating your money and making trades.

Investing online is completely normal now with numerous options, and many precautions are in place to keep it as safe as possible.

If you’re interested in purchasing metal mining stocks such as gold stocks, check out these popular sites:

Fine-Tuning Your Investment Strategy

Depending on how deep you want to take your investment knowledge, you may opt to do additional research online. Many stock experts eagerly offer guidance and advice on maximizing your portfolio.

While you’ll find experts on every side of an investment argument, it’s critical to remember that it’s your money being invested.

Expert opinions may be valuable, but it’s ultimately you who will be celebrating the gains or suffering the losses in your portfolio. For that reason, it’s typically best to look at a variety of sources before making an investment decision.

How To Use Stock Advice From Experts

As a new investor, seeing detailed stock reports may initially seem overwhelming. When first starting, if you can focus on one or two key takeaways and truly understand them, you’ll become increasingly familiar with the terms and concepts.

Over time, some investment experts or websites may resonate with you, becoming a critical part of your research process.

Examples of Popular Sources of Investment Information

Consider these popular sources of stock news and updates, along with a key takeaway from each of them.

Stockhead: “Gold to Shine in 2023, says Bloomberg”

This article is immensely useful for metal investors, as it provides updates on iron ore, gold, and lithium.

Among the many details is this key takeaway: Bloomberg senior strategist, Mike McGlome, explains how gold is already trending more positively and that it’s poised to go up in value in 2023.

The Gold Report: “Expert Says Silver May Have a ‘Stellar Performance in 2023’”

Always a valuable source due to many knowledgeable contributors, The Gold Report covers all metal mining stocks, including gold. This highly-detailed article focuses on comments by expert Michael Ballanger.

One key takeaway is that Ballanger explained the parallel between the performance of silver and that of copper and stated that silver is in a position for a “stellar performance in 2023.”

Ultimately, understanding how to interpret investment news and advice will get easier with practice and will likely help you become a smarter, more savvy investor.

Trust Streetwise Reports for the Latest News on Metals

Streetwise Reports is a one-stop hub for anyone whose curious about investing. Featuring articles and valuable information you won’t find anywhere else, you can count on Streetwise Reports to provide detailed and updated investment news daily.

Those interested in mining stocks will want to check out the Gold Report. There you’ll find new, in-depth articles on the events affecting stock prices worldwide.

Our team at Streetwise Reports works around the clock to compile meaningful stock information from a wide range of sources. We hope you’ll make Streetwise Reports the main source for investment news that matters.

Disclosures:

1) Nicholas Napier wrote this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. They members of their household own securities of the following companies mentioned in the article: None. They or members of their household are paid by the following companies mentioned in this article: None.

2) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

4) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

{kind=link}