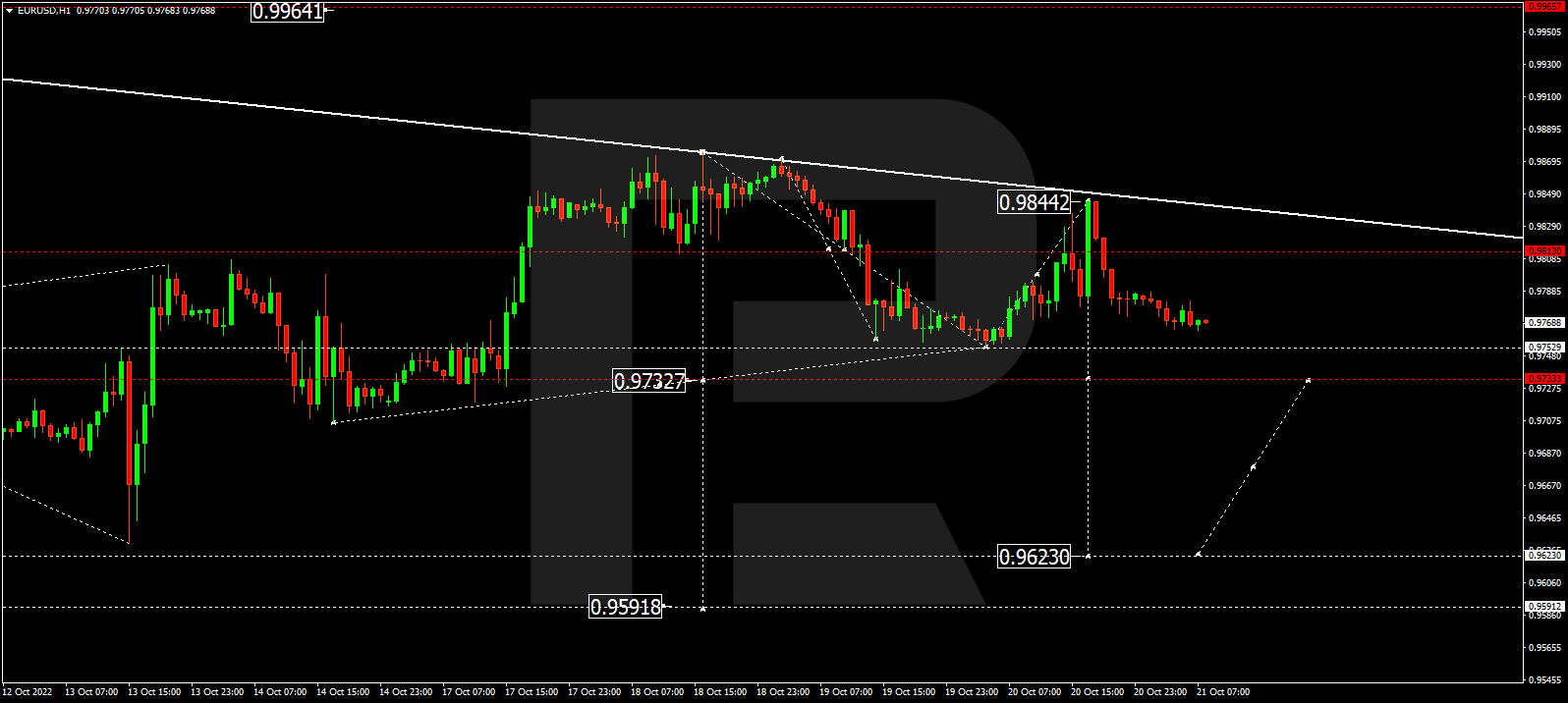

The euro gained about 1.4% against the US dollar last week, the best week since late May. On Friday, San Francisco Federal Reserve President Mary Daly said it was time to start talking about slowing borrowing costs and that the Fed should be less aggressive in its rate hike cycle. So the next rate hike is being considered at 0.5%. The statement came as a surprise to analysts as all previous statements of the Fed representatives were only aimed at an aggressive rate hike cycle with the next step at 0.75%. Because the ECB is planning to raise the rate by 0.75% this week, a reduction in the interest rate differential between the US Fed and the ECB might give confidence to the European currency.

From the technical point of view, the trend on the EUR/USD currency pair on the hourly time frame is bullish. The price is trading above the moving averages. The MACD indicator became positive, and the buyers’ pressure is prevailing again. Buy trades should be considered from the support level of 0.9817 or 0.9755, but with additional confirmation in the form of reverse initiative. Sell deals may be considered from the resistance level of 0.9961, but also with confirmation.

Alternative scenario: if the price breaks down through the support level of 0.9700 and fixes below it, the downtrend will likely resume.

News feed for 2022.10.24:

– French Manufacturing PMI (m/m) at 10:15 (GMT+3);

– French Services PMI (m/m) at 10:15 (GMT+3);

– German Manufacturing PMI (m/m) at 10:30 (GMT+3);

– German Services PMI (m/m) at 10:30 (GMT+3);

– Eurozone Manufacturing PMI (m/m) at 11:00 (GMT+3);

– Eurozone Services PMI (m/m) at 11:00 (GMT+3);

– US Manufacturing PMI (m/m) at 16:45 (GMT+3);

– US Services PMI (m/m) at 16:45 (GMT+3);

– US Treasury Secretary Yellen Speaks at 18:00 (GMT+3).

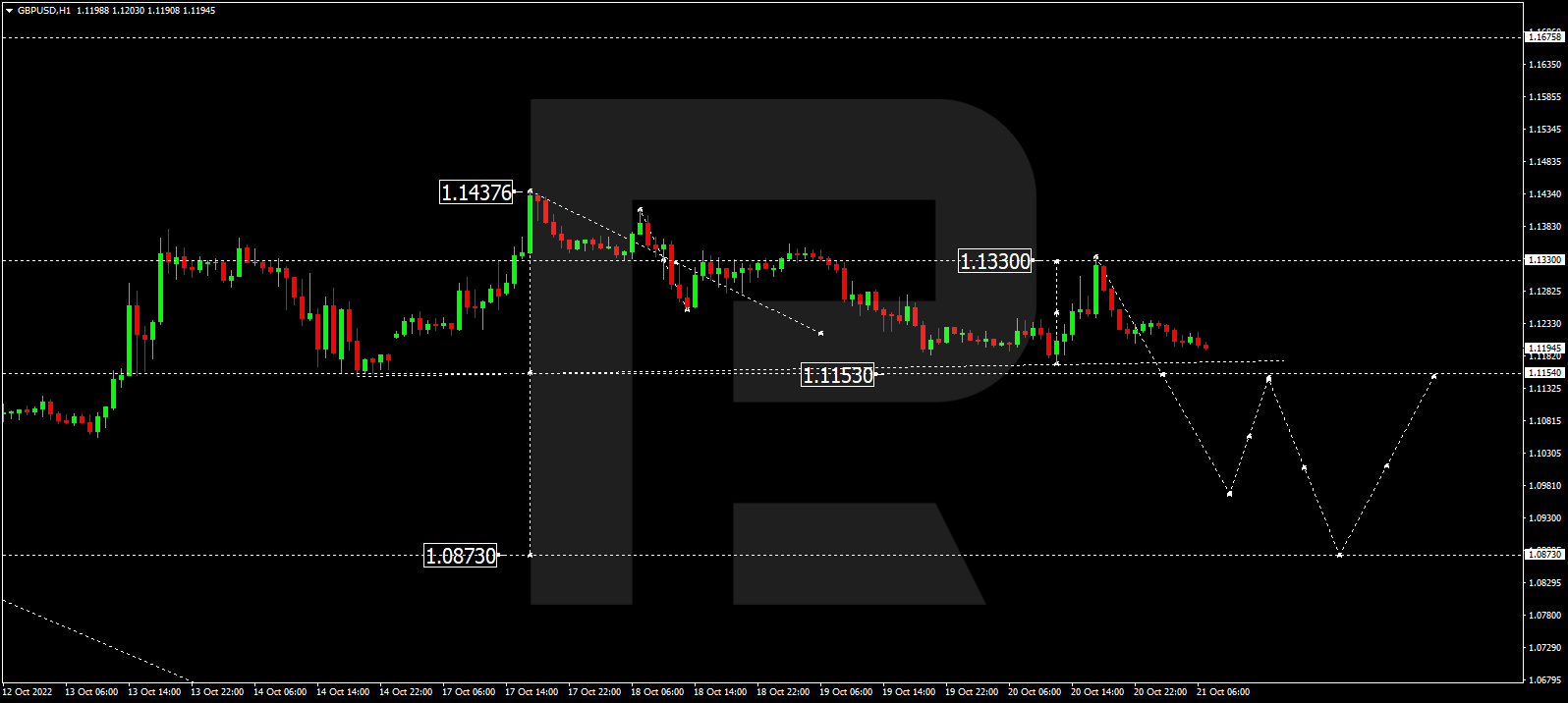

The GBP/USD currency pair

Technical indicators of the currency pair:

Prev Open: 1.1219

Prev Close: 1.1292

% chg. over the last day: +0.65 %

This week the Conservative Party of Great Britain must choose a new leader to become the fifth Prime Minister in Great Britain in the last six years. Boris Johnson has announced that he will not run for the Conservative Party leader and UK prime minister position. Thus, former finance minister Rishi Sunak is the front-runner for the prime minister. The next prime minister will inherit an economy on the road to a recession, with rising interest rates and inflation of more than 10%, leaving millions of people facing a cost-of-living crisis. Chancellor Jeremy Hunt, who is expected to remain in office under the new prime minister, said Friday that he would do “whatever is necessary” to reduce the national debt ahead of his new budget, to be announced on October 31.

From the technical point of view, the GBP/USD currency pair trend on the hourly time frame is bullish. But the price is trading below the moving averages. The price is trading below the moving averages again. The MACD indicator has become positive, and buyers’ pressure prevails. Under such market conditions, buy trades can be considered from the support level of 1.1172, but better after confirmation. Sell trades are best to look for on intraday time frames, the nearest resistance level is 1.1369.

Alternative scenario: if the price breaks down of the 1.1093 support level and fixes below it, the downtrend will likely resume.

News feed for 2022.10.24:

– UK Manufacturing PMI (m/m) at 11:30 (GMT+3);

– UK Services PMI (m/m) at 11:30 (GMT+3).

The USD/JPY currency pair

Technical indicators of the currency pair:

Prev Open: 150.13

Prev Close: 147.58

% chg. over the last day: -1.73 %

On Friday, the Japanese Ministry of Finance carried out another intervention to protect the yen from falling further. The background to this price movement is the continued monetary policy divergence between the Bank of Japan and the US Federal Reserve. The Japanese government is expected to announce a stimulus package by the end of this month. The weak yen exacerbates household problems by raising the expensive food and fuel costs. The Bank of Japan will also meet on monetary policy and interest rates this week. But analysts do not expect any changes and believe that the Bank of Japan will maintain its current loose monetary policy, which will continue to put pressure on the yen.

Trading recommendations

Support levels: 146.63, 145.88, 144.91, 144.16, 143.00

Resistance levels: 149.55, 150.00, 151.05

From the technical point of view, the medium-term trend on the currency pair USD/JPY is bullish despite the currency intervention. The price is trading below the moving levels. The MACD indicator is in the negative zone, but the buyers’ pressure remains. Under such market conditions, buy trades can be sought on intraday time frames from the support level of 146.63, but with confirmation. Sell deals can be searched from the resistance level of 150.00 or 151.05, but only with additional confirmation in the form of a reverse initiative.

Alternative scenario: If the price fixes below 145.88, the downtrend will likely resume.

News feed for 2022.10.24:

– Japan Manufacturing PMI (m/m) at 03:30 (GMT+3);

– Japan Services PMI (m/m) at 03:30 (GMT+3).

The USD/CAD currency pair

Technical indicators of the currency pair:

Prev Open: 1.3761

Prev Close: 1.3643

% chg. over the last day: -0.86 %

The Bank of Canada will hold its monetary policy and interest rate meeting this week. The Bank of Canada is expected to raise its benchmark interest rate by 50 basis points, although a move from 75 bps is possible as core inflation in Canada shows no signs of slowing. Also, keep in mind that the Canadian dollar is a commodity currency, so it is also highly exposed to oil price fluctuations. The medium-term oil outlook points to growth, so amid a decline in the dollar index, the Canadian currency can at least take over the initiative.

Trading recommendations

Support levels: 1.3639, 1.3619, 1.3583, 1.3535, 1.3454

Resistance levels: 1.3795, 1.3855, 1.3968

From the point of view of technical analysis, the trend on the USD/CAD currency pair is bullish. The price is trading at the level of moving averages. The MACD indicator has become negative, but the sellers’ pressure is weak. Under such market conditions, buy trades should be considered on the lower time frames from the support level of 1.3638 but better after confirmation. For sell deals, it is best to consider the resistance level of 1.3795, but only after additional confirmation in the form of a reverse initiative.

Alternative scenario: if the price breaks down and consolidates below the support level of 1.3619, the downtrend will likely resume.

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

The US stock indexes rose Friday after news that US Federal Reserve officials are discussing a 0.5% interest rate hike in November, raising hopes that the central bank may adopt a less aggressive policy. As the stock market closed on Friday, the Dow Jones Index (US30) increased by 2.47% (3.48% for the week), and the S&P 500 Index (US500) added 2.37% (2.93% for the week). The NASDAQ Technology Index (US100) jumped by 2.31% on Friday (2.69% for the week).

According to a Wall Street Journal report, some Fed officials have begun stating their desire to slow the pace of the increase soon. On Friday, San Francisco Federal Reserve President Mary Daly said it was time to start talking about slowing the pace of borrowing costs and that the Fed should be less aggressive in its rate hike cycle. Charles Evans, president of the Federal Reserve Bank of Chicago, also cited similar statements. According to Reuters calculations, speculators’ net long rates on the US dollar rose last week.

The four largest US companies by market capitalization are due to report this week. Investors are filled with optimism as corporate earnings help keep the stock market from falling amid soaring inflation and an aggressive Federal Reserve rate hike.

Stock markets in Europe were mostly down Friday, but all closed the week in positive territory. German DAX (DE30) decreased by 0.29% on Friday (+2.11% for the week), French CAC 40 (FR40) lost 0.85% (+1.44% for the week), Spanish IBEX 35 (ES35) fell by 1.29% (+1.72% for the week), British FTSE 100 (UK100) was up by 0.15% (+1.62% for the week).

Boris Johnson announced that he would not run for the Conservative Party leader and British Prime Minister post. Johnson’s announcement will pave the way for Rishi Sunak, who will likely become the next prime minister. Liz Truss was forced to resign after she launched an economic program that caused turmoil in the financial markets. Former Finance Minister Rishi Sunak earlier confirmed that he would be on the ballot, promising to handle the country’s “deep economic crisis” with “honesty, professionalism, and accountability.” Chancellor Jeremy Hunt, who is expected to remain in office under the new prime minister, said Friday that he would do “whatever is necessary” to reduce the national debt ahead of his new budget, to be announced on October 31.

Oil prices rebounded Friday as hopes for stronger demand in China and a weaker US dollar outweighed concerns about the global economic slowdown and the impact of higher interest rates. Overall, the oil market remains uncertain as, on the one hand, OPEC+ production cuts and European sanctions against Russia for its invasion of Ukraine are keeping oil prices from falling. On the other hand, falling oil demand in the largest importer China, along with the release of strategic reserves by the US, are keeping the price down.

Chinese President Xi Jinping secured an unprecedented third presidential term and introduced a top governing body made up of loyalists, cementing his place as the country’s most powerful ruler since Mao Zedong. On Monday, China released a slew of macroeconomic statistics, the publication of which was delayed by a week because of the presidential re-election. The data indicated that China’s GDP grew by 3.9% in the last quarter, but analysts believe the numbers do not correspond to reality. China now faces a host of economic challenges, and China’s biggest concerns remain the real estate market and falling manufacturing numbers due to the new Covid lockdowns.

Japan’s promised economic stimulus should be big enough to overcome the economy’s manufacturing deficit of about 15 trillion yen ($100 billion), a top ruling party official said Sunday. On Friday, Japan’s Finance Ministry held another intervention to protect the yen from falling further. The background to such price movement is the continuing unequal monetary policy between the Bank of Japan and the Federal Reserve.

At the commodities market, futures on lumber (+8.36%), silver (+7.35%), platinum (+4.44%), and Brent oil (+2.15%) showed the biggest gains over the week. Futures on natural gas (-22.64%), cotton (-4.51%), coffee (-3.94%), cocoa (-3.2%) and sugar (-2.49%) showed the biggest drop.

S&P 500 (F) (US500) 3,752.75 +86.97 (+2.37%)

Dow Jones (US30) 31,082.56 +748.97 (+2.47%)

DAX (DE40) 12,730.90 −36.51 (−0.29%)

FTSE 100 (UK100) 6,969.73 +25.82 (+0.37%)

USD Index 111.18 −0.14 (−0.12%)

Important events for today:

– Australia Manufacturing PMI (m/m) at 01:00 (GMT+3);

– Australia Services PMI (m/m) at 01:00 (GMT+3);

– Japan Manufacturing PMI (m/m) at 03:30 (GMT+3);

– Japan Services PMI (m/m) at 03:30 (GMT+3);

– China GDP (q/q) at 05:00 (GMT+3);

– China Retail Sales (m/m) at 05:00 (GMT+3);

– China Industrial Production (m/m) at 05:00 (GMT+3);

– China Unemployment Rate (m/m) at 05:00 (GMT+3);

– China Exports (m/m) at 06:00 (GMT+3);

– China Imports (m/m) at 06:00 (GMT+3);

– French Manufacturing PMI (m/m) at 10:15 (GMT+3);

– French Services PMI (m/m) at 10:15 (GMT+3);

– German Manufacturing PMI (m/m) at 10:30 (GMT+3);

– German Services PMI (m/m) at 10:30 (GMT+3);

– Eurozone Manufacturing PMI (m/m) at 11:00 (GMT+3);

– Eurozone Services PMI (m/m) at 11:00 (GMT+3);

– UK Manufacturing PMI (m/m) at 11:30 (GMT+3);

– UK Services PMI (m/m) at 11:30 (GMT+3);

– US Manufacturing PMI (m/m) at 16:45 (GMT+3);

– US Services PMI (m/m) at 16:45 (GMT+3);

– US Treasury Secretary Yellen Speaks at 18:00 (GMT+3).

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

Here are the latest charts and statistics for the Commitment of Traders (COT) reports data published by the Commodities Futures Trading Commission (CFTC).

The latest COT data is updated through Tuesday October 18th and shows a quick view of how large traders (for-profit speculators and commercial entities) were positioned in the futures markets.

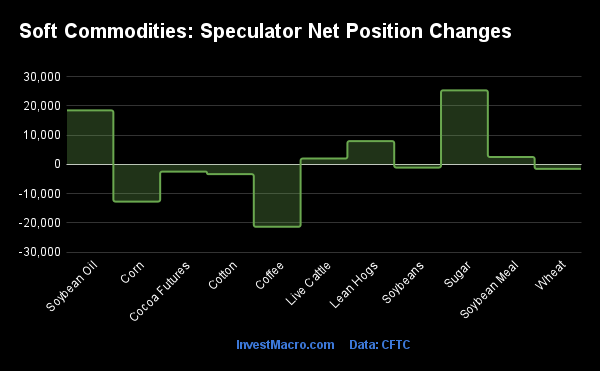

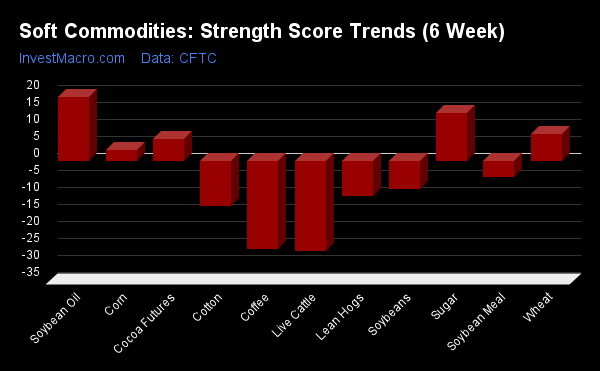

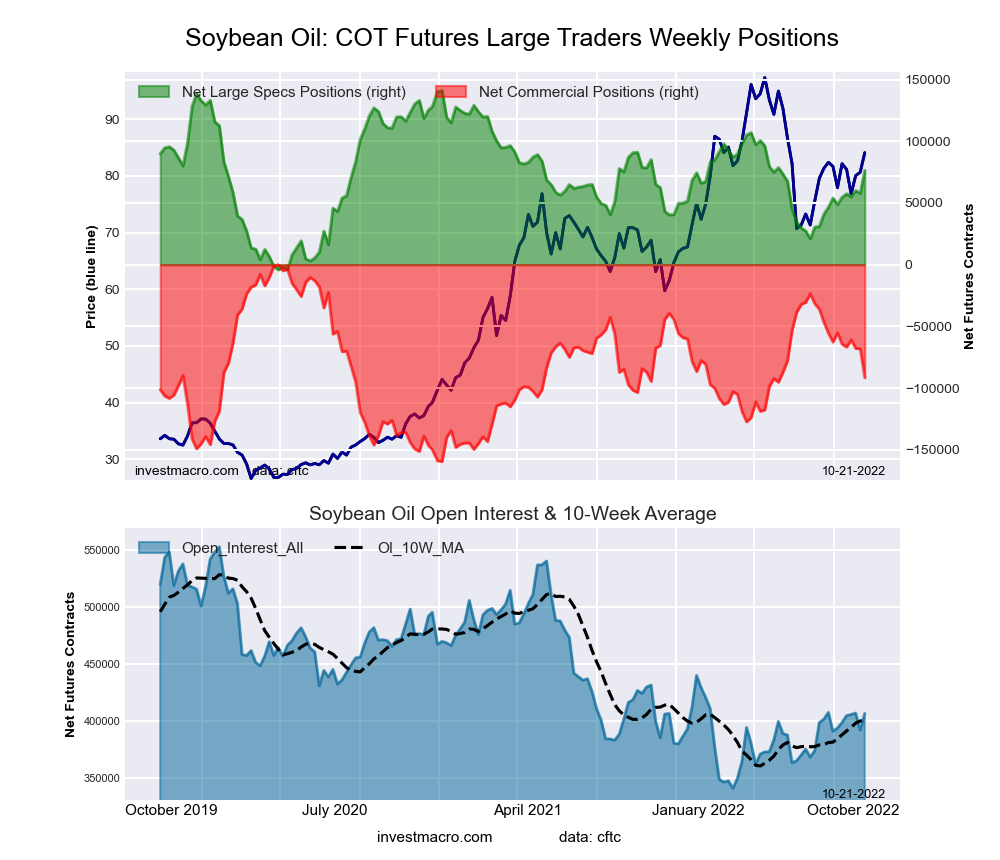

Sugar and Soybean Oil top Weekly Speculator Changes

The COT soft commodities speculator bets were slightly lower this week as five out of the eleven soft commodities markets we cover had higher positioning this week while the other six markets had decreases in contracts.

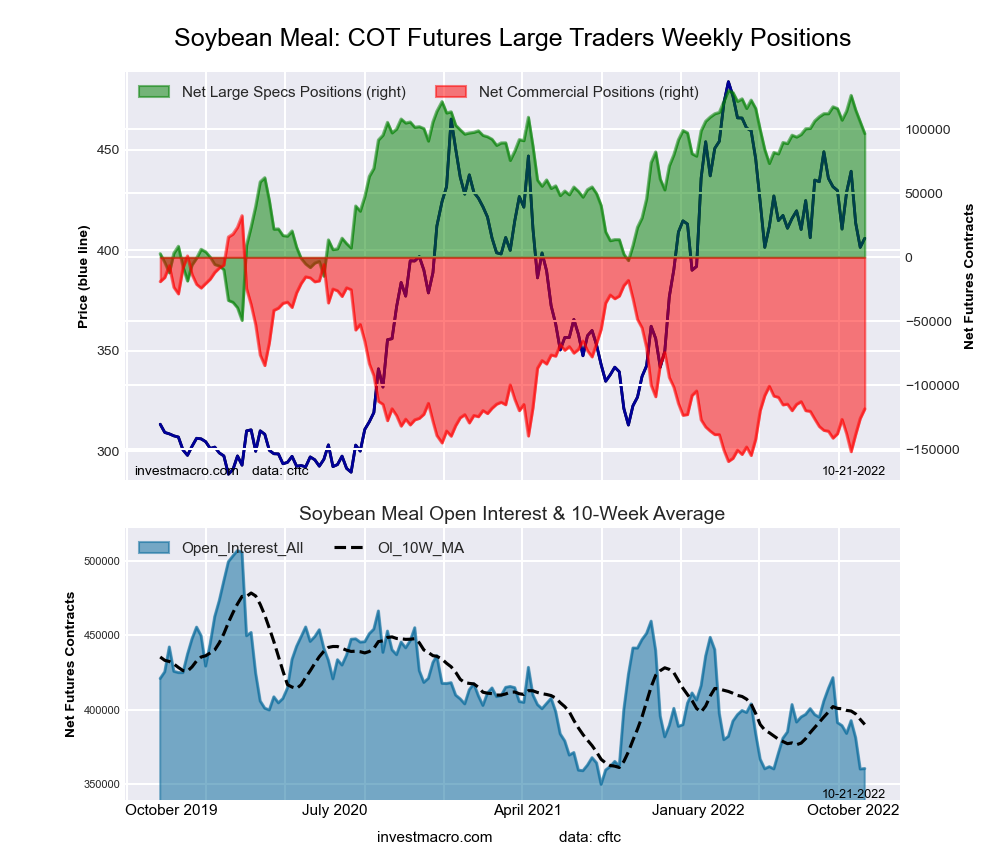

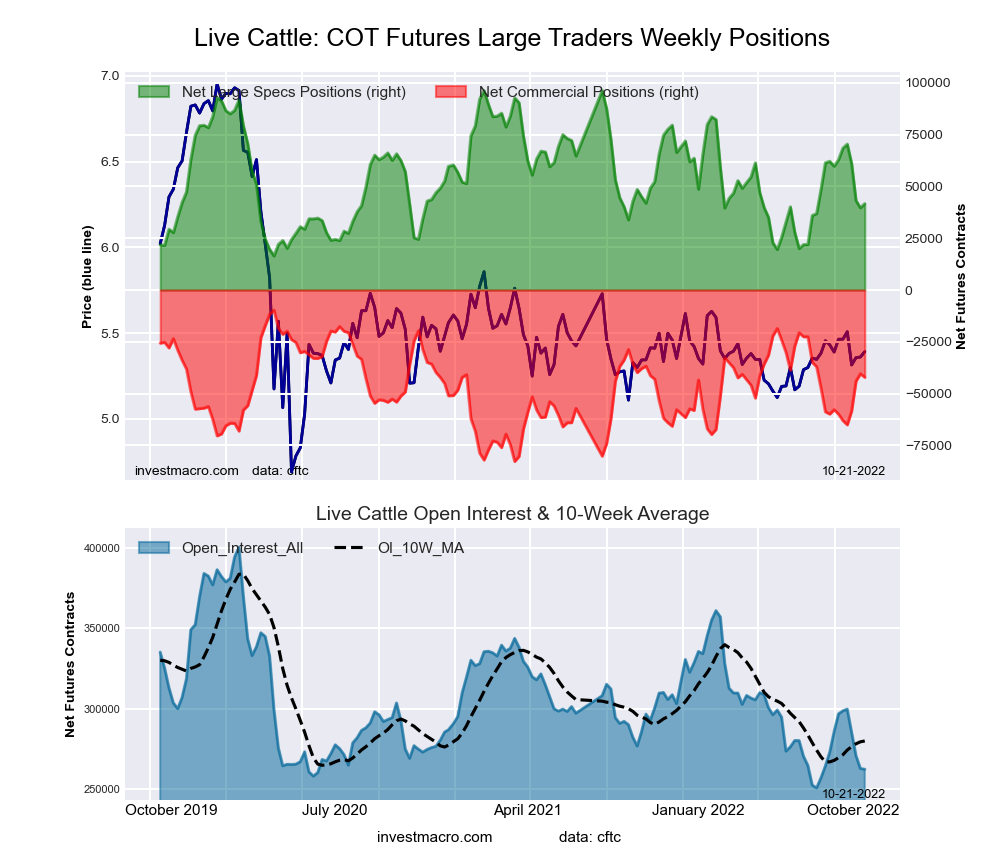

Leading the gains for soft commodities markets was Sugar (25,297 contracts) with Soybean Oil (18,444 contracts), Lean Hogs (7,948 contracts), Soybean Meal (2,531 contracts) and Live Cattle (1,991 contracts) also showing positive weeks.

The softs market leading the declines in speculator bets this week was Coffee (-21,311 contracts) with Corn (-12,702 contracts), Cotton (-3,338 contracts), Cocoa (-2,468 contracts), Wheat (-1,551 contracts) and Soybeans (-1,086 contracts) also registering lower bets on the week.

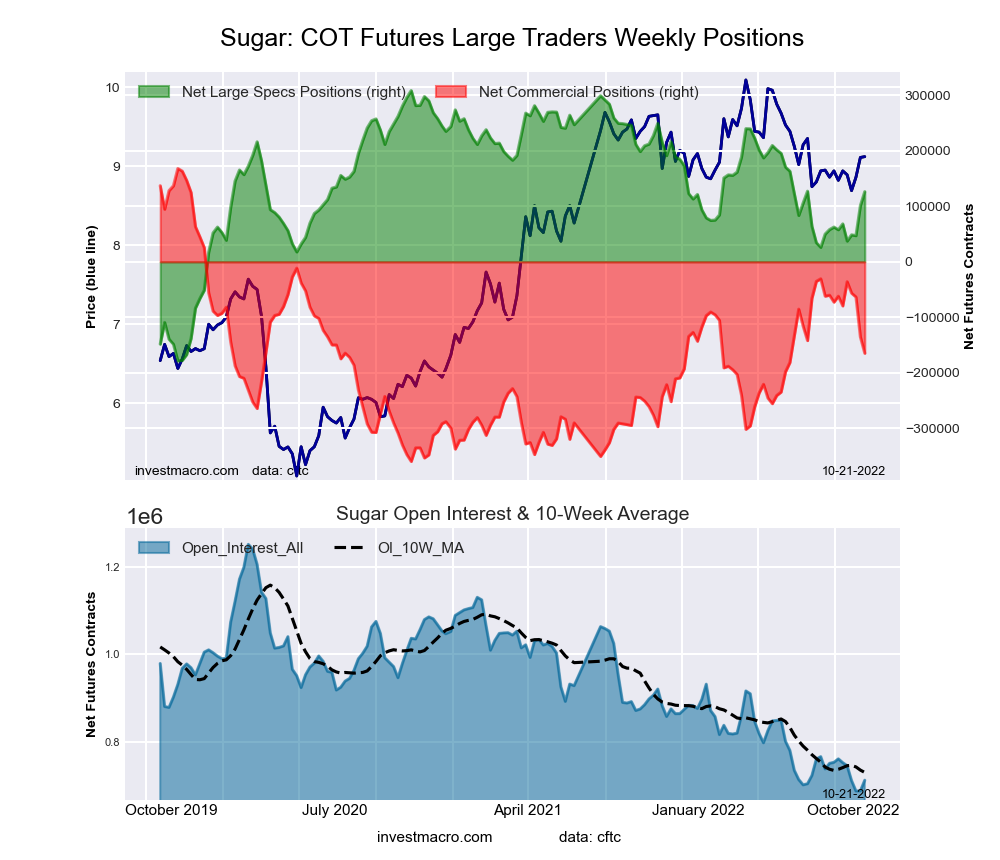

Highlighting the COT soft commodities data this week was the speculator positions in Sugar. The large speculative position for Sugar has risen sharply for two straight weeks and has advanced in seven out of the past ten weeks. This trader bullishness has brought a gain of +100,347 contracts over just the last ten-week period and pushed overall bullish standing back above the +100,000 net contract level for the first time since July.

Sugar prices and sentiment have been boosted higher by lower production numbers and higher prices out of Europe as well as Brazil this year. Prices closed this week around the 18.40 level and have been in a range between 17 and 20.70 since July of 2021.

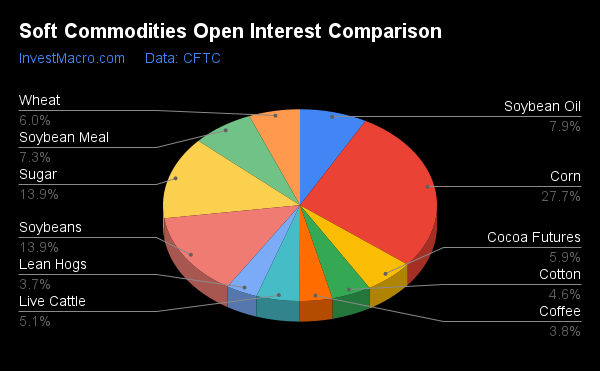

Data Snapshot of Commodity Market Traders | Columns Legend

Oct-18-2022

OI

OI-Index

Spec-Net

Spec-Index

Com-Net

COM-Index

Smalls-Net

Smalls-Index

WTI Crude

1,454,431

0

251,545

11

-273,757

90

22,212

37

Gold

434,701

1

76,956

8

-90,030

91

13,074

12

Silver

136,055

9

1,267

15

-9,085

87

7,818

8

Copper

178,730

17

-20,302

20

19,696

82

606

29

Palladium

6,805

4

-1,209

16

1,444

82

-235

30

Platinum

53,728

11

8,494

21

-11,632

81

3,138

10

Natural Gas

963,792

3

-154,734

32

126,760

71

27,974

46

Brent

163,296

11

-41,847

41

38,681

58

3,166

52

Heating Oil

283,702

29

24,555

79

-44,031

24

19,476

66

Soybeans

714,532

30

54,683

30

-30,595

77

-24,088

30

Corn

1,419,087

22

312,419

70

-249,255

36

-63,164

7

Coffee

196,729

9

19,223

53

-21,605

52

2,382

24

Sugar

711,664

4

126,412

63

-164,671

37

38,259

55

Wheat

309,429

10

-3,541

14

10,534

75

-6,993

74

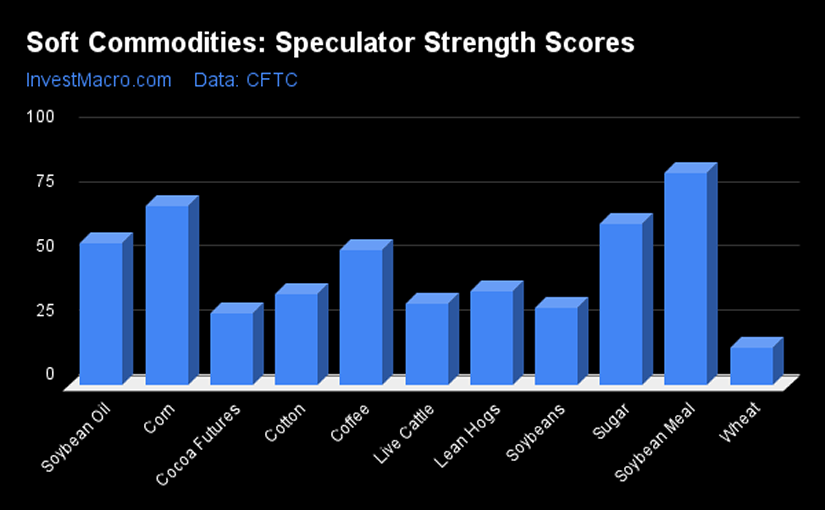

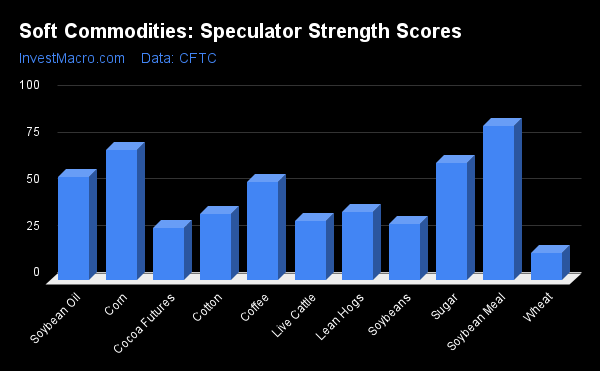

Soybean Meal leads Strength Scores

Strength Scores (a normalized measure of Speculator positions over a 3-Year range, from 0 to 100 where above 80 is extreme bullish and below 20 is extreme bearish) showed that Soybean Meal (82.7 percent) and the XXXX lead the soft commodity markets and remains in a bullish extreme position (above 80 percent). Corn (69.9 percent) and Sugar (62.5 percent) come in as the next highest soft commodity markets in strength scores.

On the downside, Wheat (14.4 percent) comes in at the lowest strength level currently and is a bearish extreme level (below 20 percent).

Strength Statistics: Corn (69.9 percent) vs Corn previous week (71.6 percent) Sugar (62.5 percent) vs Sugar previous week (57.3 percent) Coffee (52.5 percent) vs Coffee previous week (72.1 percent) Soybeans (30.2 percent) vs Soybeans previous week (30.5 percent) Soybean Oil (55.4 percent) vs Soybean Oil previous week (42.7 percent) Soybean Meal (82.7 percent) vs Soybean Meal previous week (81.3 percent) Live Cattle (31.6 percent) vs Live Cattle previous week (29.1 percent) Lean Hogs (36.3 percent) vs Lean Hogs previous week (27.6 percent) Cotton (35.3 percent) vs Cotton previous week (37.7 percent) Cocoa (27.9 percent) vs Cocoa previous week (30.4 percent) Wheat (14.4 percent) vs Wheat previous week (16.5 percent)

Strength Trends led by Soybean Oil and Sugar

Strength Score Trends (or move index, calculates the 6-week changes in strength scores) show that Soybean Oil (18.9 percent) leads the past six weeks trends for soft commodity markets this week. Sugar (14.1 percent), Wheat (8.1 percent), Cocoa (6.7 percent) and Corn (3.3 percent) fill out the other positive movers in the latest trends data.

Live Cattle (-26.5 percent) and Coffee (-25.7 percent) lead the downside trend scores currently while the next market with lower trend scores was Cotton (-13.2 percent) followed by Lean Hogs (-10.1 percent).

Strength Trend Statistics: Corn (3.3 percent) vs Corn previous week (5.3 percent) Sugar (14.1 percent) vs Sugar previous week (7.9 percent) Coffee (-25.7 percent) vs Coffee previous week (-7.5 percent) Soybeans (-8.2 percent) vs Soybeans previous week (-8.5 percent) Soybean Oil (18.9 percent) vs Soybean Oil previous week (2.7 percent) Soybean Meal (-4.5 percent) vs Soybean Meal previous week (-10.9 percent) Live Cattle (-26.5 percent) vs Live Cattle previous week (-25.2 percent) Lean Hogs (-10.1 percent) vs Lean Hogs previous week (-26.2 percent) Cotton (-13.2 percent) vs Cotton previous week (-11.6 percent) Cocoa (6.7 percent) vs Cocoa previous week (5.3 percent) Wheat (8.1 percent) vs Wheat previous week (12.4 percent)

Individual Soft Commodities Markets:

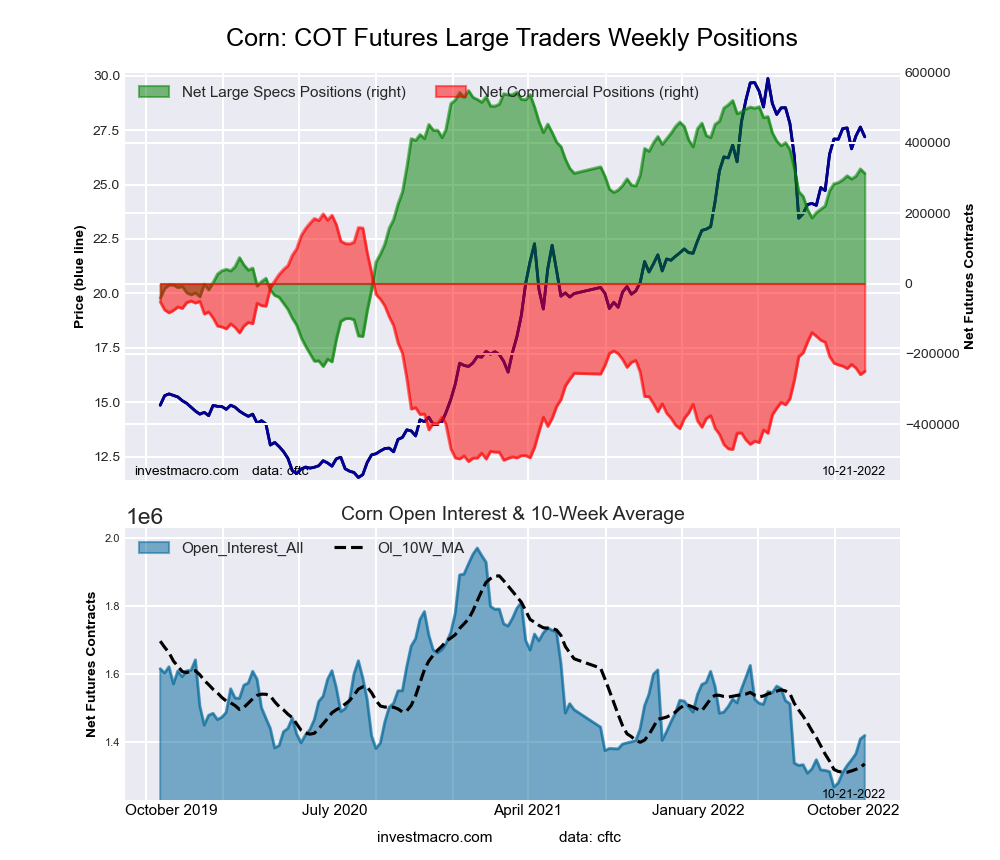

CORN Futures:

The CORN large speculator standing this week came in at a net position of 312,419 contracts in the data reported through Tuesday. This was a weekly decline of -12,702 contracts from the previous week which had a total of 325,121 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 69.9 percent. The commercials are Bearish with a score of 36.4 percent and the small traders (not shown in chart) are Bearish-Extreme with a score of 6.7 percent.

CORN Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

30.9

44.8

8.9

– Percent of Open Interest Shorts:

8.8

62.3

13.3

– Net Position:

312,419

-249,255

-63,164

– Gross Longs:

437,906

635,253

126,283

– Gross Shorts:

125,487

884,508

189,447

– Long to Short Ratio:

3.5 to 1

0.7 to 1

0.7 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

69.9

36.4

6.7

– Strength Index Reading (3 Year Range):

Bullish

Bearish

Bearish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

3.3

-2.6

-4.2

SUGAR Futures:

The SUGAR large speculator standing this week came in at a net position of 126,412 contracts in the data reported through Tuesday. This was a weekly increase of 25,297 contracts from the previous week which had a total of 101,115 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 62.5 percent. The commercials are Bearish with a score of 37.3 percent and the small traders (not shown in chart) are Bullish with a score of 55.2 percent.

SUGAR Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

28.9

48.1

11.8

– Percent of Open Interest Shorts:

11.1

71.2

6.4

– Net Position:

126,412

-164,671

38,259

– Gross Longs:

205,568

342,150

83,657

– Gross Shorts:

79,156

506,821

45,398

– Long to Short Ratio:

2.6 to 1

0.7 to 1

1.8 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

62.5

37.3

55.2

– Strength Index Reading (3 Year Range):

Bullish

Bearish

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

14.1

-19.6

42.1

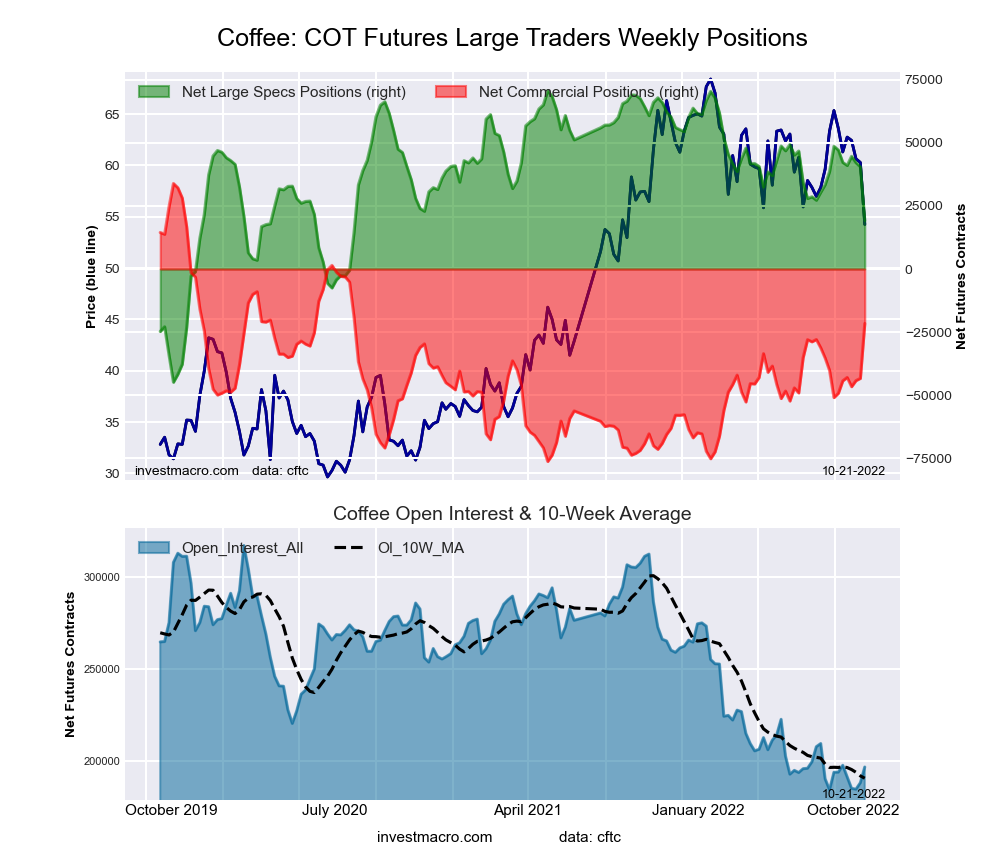

COFFEE Futures:

The COFFEE large speculator standing this week came in at a net position of 19,223 contracts in the data reported through Tuesday. This was a weekly reduction of -21,311 contracts from the previous week which had a total of 40,534 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 52.5 percent. The commercials are Bullish with a score of 52.4 percent and the small traders (not shown in chart) are Bearish with a score of 24.4 percent.

COFFEE Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

20.9

51.5

4.6

– Percent of Open Interest Shorts:

11.1

62.4

3.4

– Net Position:

19,223

-21,605

2,382

– Gross Longs:

41,151

101,222

9,017

– Gross Shorts:

21,928

122,827

6,635

– Long to Short Ratio:

1.9 to 1

0.8 to 1

1.4 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

52.5

52.4

24.4

– Strength Index Reading (3 Year Range):

Bullish

Bullish

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-25.7

26.5

2.9

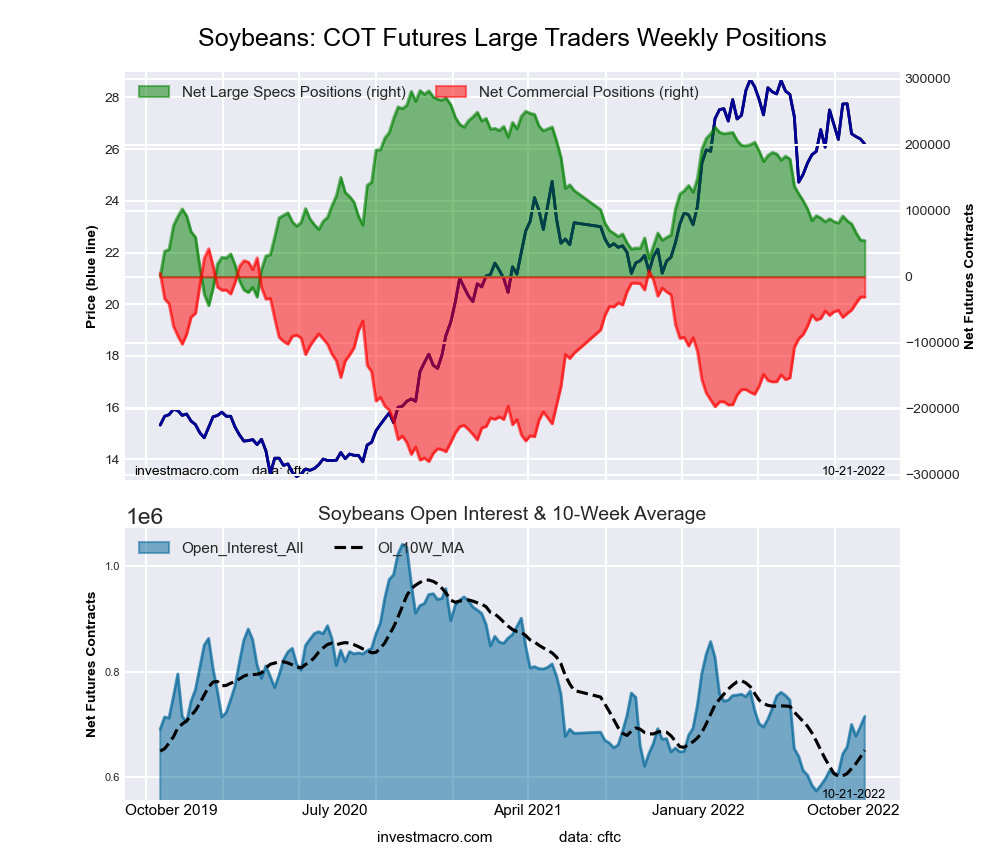

SOYBEANS Futures:

The SOYBEANS large speculator standing this week came in at a net position of 54,683 contracts in the data reported through Tuesday. This was a weekly lowering of -1,086 contracts from the previous week which had a total of 55,769 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 30.2 percent. The commercials are Bullish with a score of 77.3 percent and the small traders (not shown in chart) are Bearish with a score of 30.4 percent.

SOYBEANS Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

18.5

54.5

7.1

– Percent of Open Interest Shorts:

10.8

58.8

10.5

– Net Position:

54,683

-30,595

-24,088

– Gross Longs:

132,144

389,695

50,829

– Gross Shorts:

77,461

420,290

74,917

– Long to Short Ratio:

1.7 to 1

0.9 to 1

0.7 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

30.2

77.3

30.4

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-8.2

6.3

10.7

SOYBEAN OIL Futures:

The SOYBEAN OIL large speculator standing this week came in at a net position of 76,323 contracts in the data reported through Tuesday. This was a weekly boost of 18,444 contracts from the previous week which had a total of 57,879 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 55.4 percent. The commercials are Bearish with a score of 42.7 percent and the small traders (not shown in chart) are Bullish with a score of 70.2 percent.

SOYBEAN OIL Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

26.0

45.1

9.1

– Percent of Open Interest Shorts:

7.2

67.6

5.3

– Net Position:

76,323

-91,542

15,219

– Gross Longs:

105,679

183,264

36,918

– Gross Shorts:

29,356

274,806

21,699

– Long to Short Ratio:

3.6 to 1

0.7 to 1

1.7 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

55.4

42.7

70.2

– Strength Index Reading (3 Year Range):

Bullish

Bearish

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

18.9

-22.8

33.0

SOYBEAN MEAL Futures:

The SOYBEAN MEAL large speculator standing this week came in at a net position of 99,132 contracts in the data reported through Tuesday. This was a weekly boost of 2,531 contracts from the previous week which had a total of 96,601 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 82.7 percent. The commercials are Bearish-Extreme with a score of 19.5 percent and the small traders (not shown in chart) are Bullish with a score of 52.0 percent.

SOYBEAN MEAL Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

32.1

41.0

13.0

– Percent of Open Interest Shorts:

5.5

73.8

6.9

– Net Position:

99,132

-122,110

22,978

– Gross Longs:

119,484

152,664

48,567

– Gross Shorts:

20,352

274,774

25,589

– Long to Short Ratio:

5.9 to 1

0.6 to 1

1.9 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

82.7

19.5

52.0

– Strength Index Reading (3 Year Range):

Bullish-Extreme

Bearish-Extreme

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-4.5

2.4

17.9

LIVE CATTLE Futures:

The LIVE CATTLE large speculator standing this week came in at a net position of 41,656 contracts in the data reported through Tuesday. This was a weekly gain of 1,991 contracts from the previous week which had a total of 39,665 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 31.6 percent. The commercials are Bullish with a score of 55.6 percent and the small traders (not shown in chart) are Bullish-Extreme with a score of 98.4 percent.

LIVE CATTLE Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

32.4

36.3

12.7

– Percent of Open Interest Shorts:

16.5

52.4

12.5

– Net Position:

41,656

-42,115

459

– Gross Longs:

85,057

95,288

33,243

– Gross Shorts:

43,401

137,403

32,784

– Long to Short Ratio:

2.0 to 1

0.7 to 1

1.0 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

31.6

55.6

98.4

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bullish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-26.5

24.4

13.9

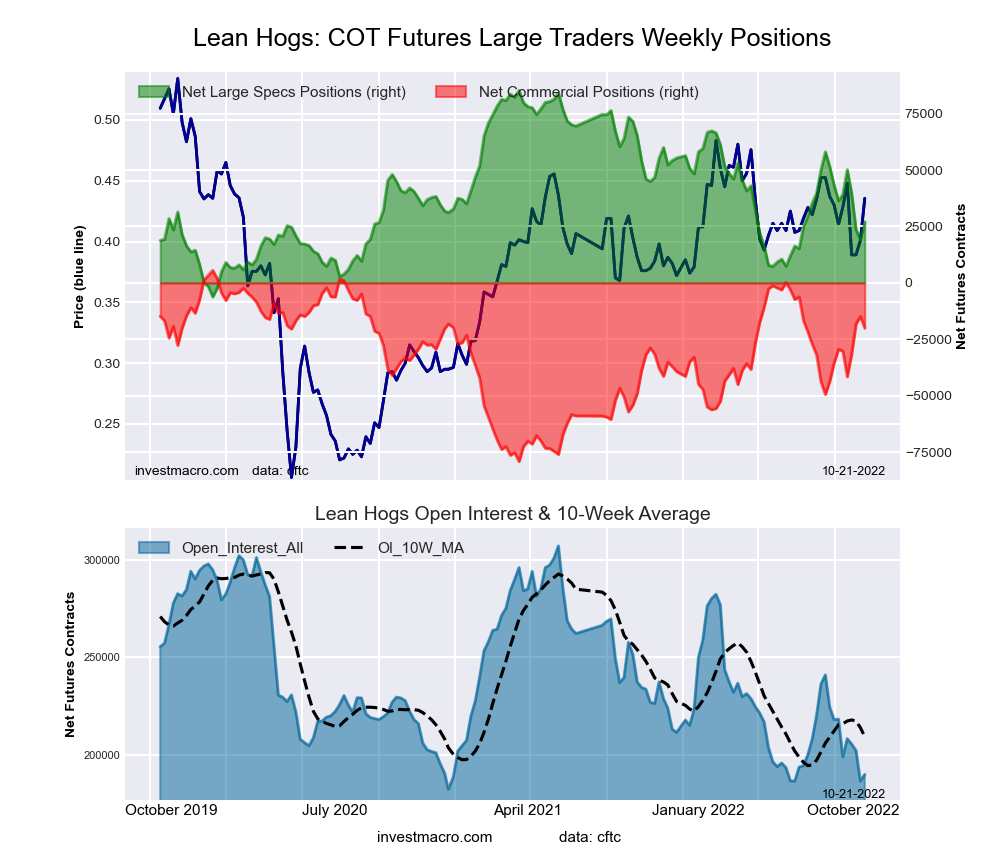

LEAN HOGS Futures:

The LEAN HOGS large speculator standing this week came in at a net position of 27,089 contracts in the data reported through Tuesday. This was a weekly advance of 7,948 contracts from the previous week which had a total of 19,141 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 36.3 percent. The commercials are Bullish with a score of 69.8 percent and the small traders (not shown in chart) are Bullish with a score of 59.7 percent.

LEAN HOGS Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

37.4

36.6

10.0

– Percent of Open Interest Shorts:

23.1

47.2

13.7

– Net Position:

27,089

-19,993

-7,096

– Gross Longs:

70,919

69,501

18,957

– Gross Shorts:

43,830

89,494

26,053

– Long to Short Ratio:

1.6 to 1

0.8 to 1

0.7 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

36.3

69.8

59.7

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-10.1

11.1

-0.8

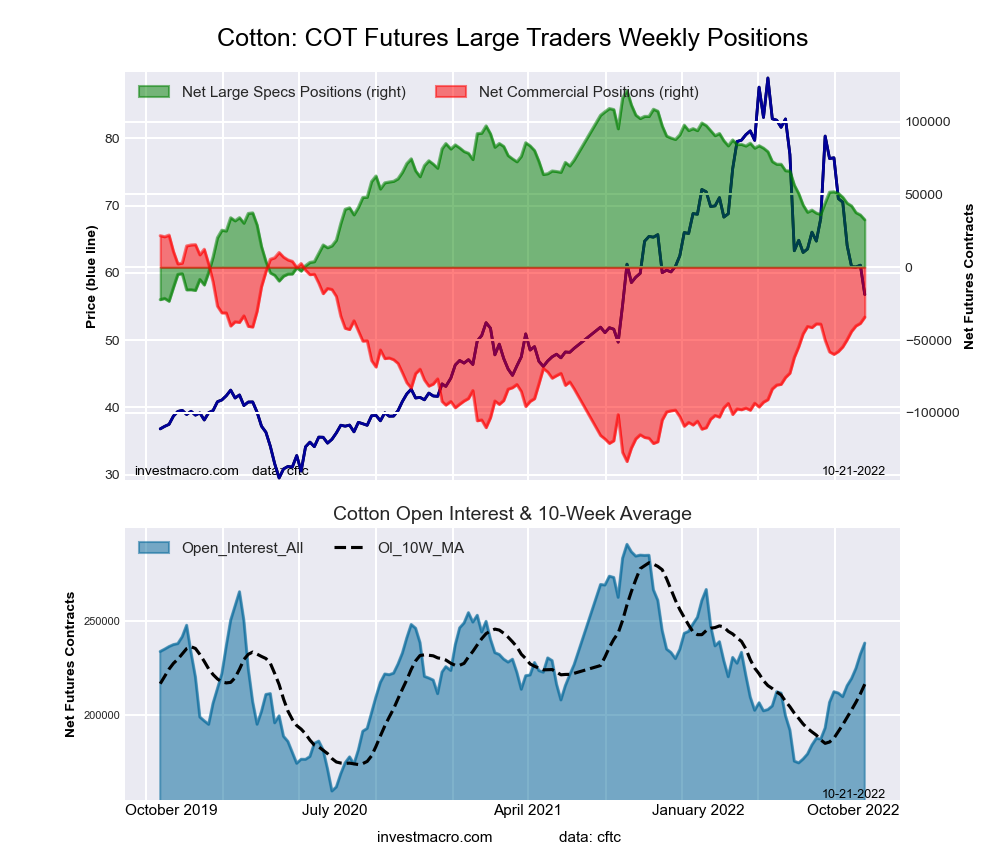

COTTON Futures:

The COTTON large speculator standing this week came in at a net position of 32,563 contracts in the data reported through Tuesday. This was a weekly reduction of -3,338 contracts from the previous week which had a total of 35,901 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 35.3 percent. The commercials are Bullish with a score of 66.6 percent and the small traders (not shown in chart) are Bearish with a score of 21.1 percent.

COTTON Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

29.9

50.2

5.4

– Percent of Open Interest Shorts:

16.3

64.5

4.7

– Net Position:

32,563

-34,238

1,675

– Gross Longs:

71,299

119,480

12,911

– Gross Shorts:

38,736

153,718

11,236

– Long to Short Ratio:

1.8 to 1

0.8 to 1

1.1 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

35.3

66.6

21.1

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-13.2

15.9

-35.4

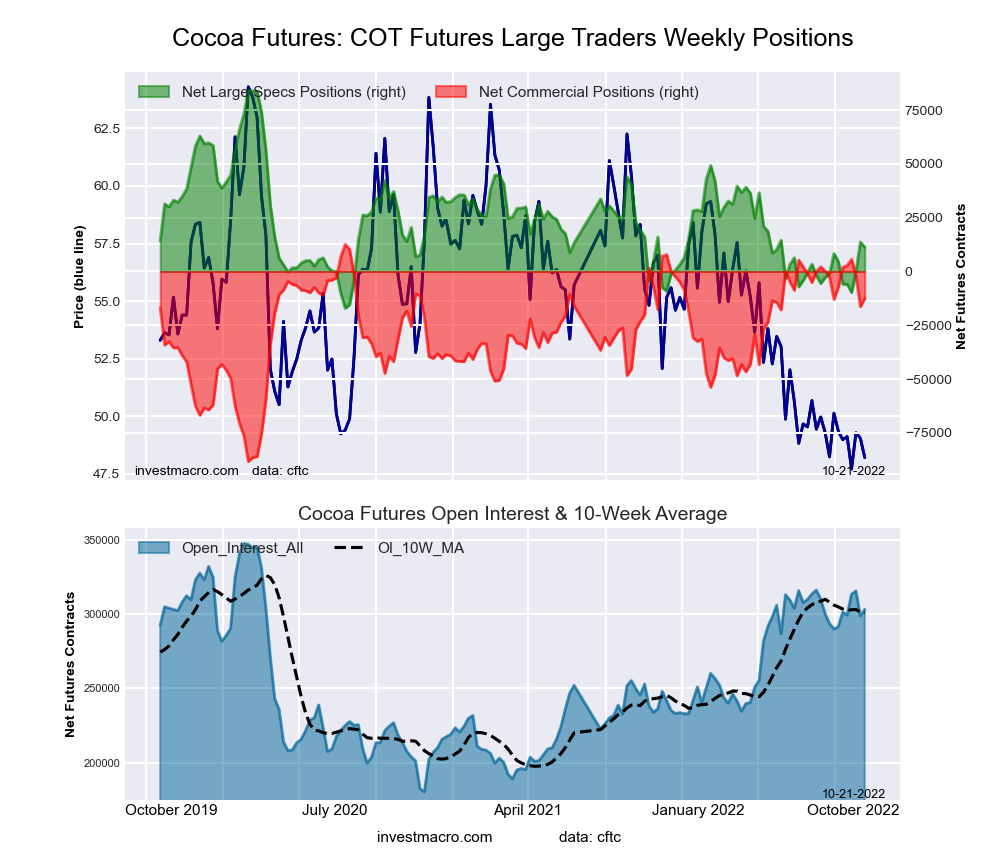

COCOA Futures:

The COCOA large speculator standing this week came in at a net position of 11,218 contracts in the data reported through Tuesday. This was a weekly fall of -2,468 contracts from the previous week which had a total of 13,686 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 27.9 percent. The commercials are Bullish with a score of 75.2 percent and the small traders (not shown in chart) are Bearish-Extreme with a score of 8.7 percent.

COCOA Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

31.7

46.2

4.0

– Percent of Open Interest Shorts:

28.0

50.3

3.6

– Net Position:

11,218

-12,445

1,227

– Gross Longs:

95,953

140,015

12,138

– Gross Shorts:

84,735

152,460

10,911

– Long to Short Ratio:

1.1 to 1

0.9 to 1

1.1 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

27.9

75.2

8.7

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bearish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

6.7

-5.2

-15.4

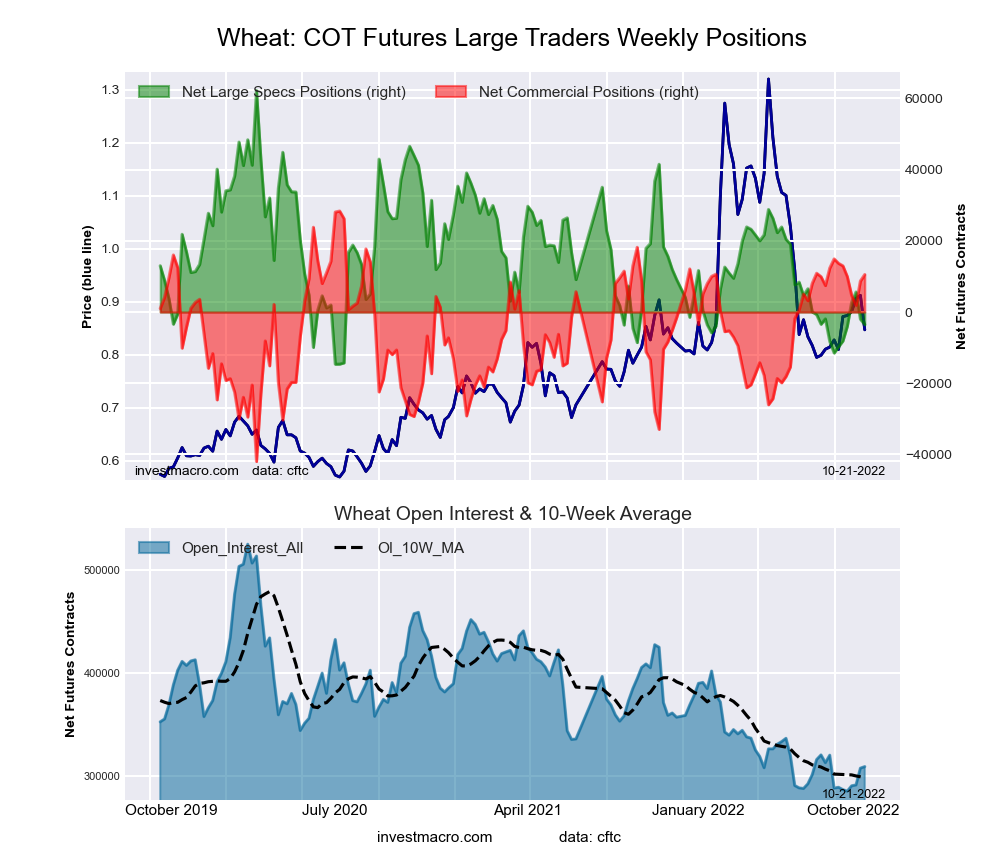

WHEAT Futures:

The WHEAT large speculator standing this week came in at a net position of -3,541 contracts in the data reported through Tuesday. This was a weekly reduction of -1,551 contracts from the previous week which had a total of -1,990 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 14.4 percent. The commercials are Bullish with a score of 74.6 percent and the small traders (not shown in chart) are Bullish with a score of 74.1 percent.

WHEAT Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

27.8

40.6

8.7

– Percent of Open Interest Shorts:

28.9

37.2

10.9

– Net Position:

-3,541

10,534

-6,993

– Gross Longs:

86,038

125,771

26,783

– Gross Shorts:

89,579

115,237

33,776

– Long to Short Ratio:

1.0 to 1

1.1 to 1

0.8 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

14.4

74.6

74.1

– Strength Index Reading (3 Year Range):

Bearish-Extreme

Bullish

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

8.1

-4.5

-16.0

Article By InvestMacro – Receive our weekly COT Newsletter

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators) as well as their open interest (contracts open in the market at time of reporting). See CFTC criteria here.

The latest COT data is updated through Tuesday October 18th and shows a quick view of how large traders (for-profit speculators and commercial hedgers) were positioned in the futures markets.

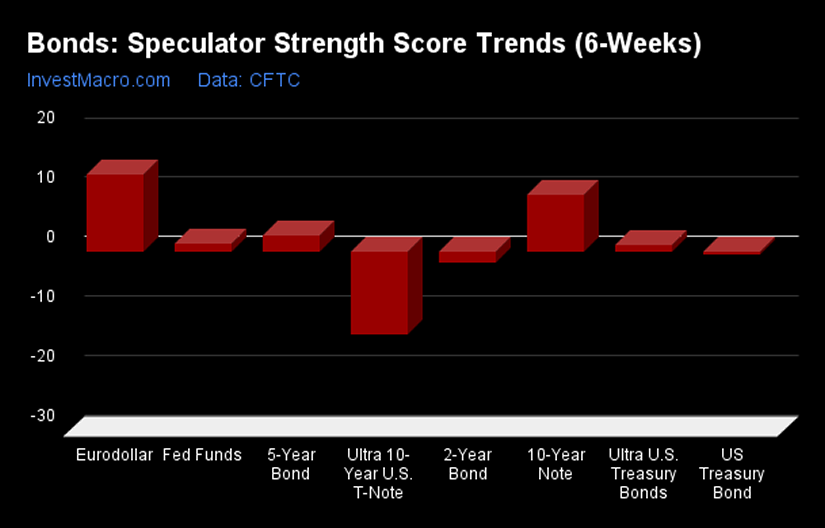

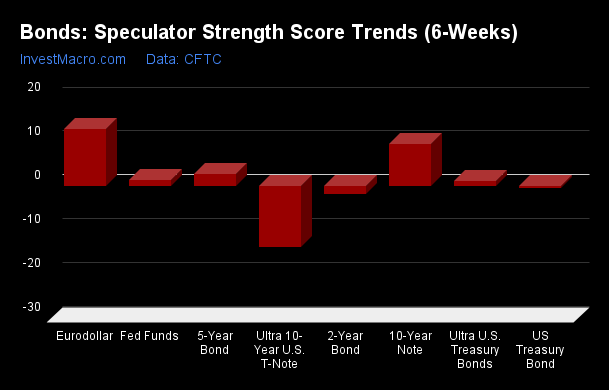

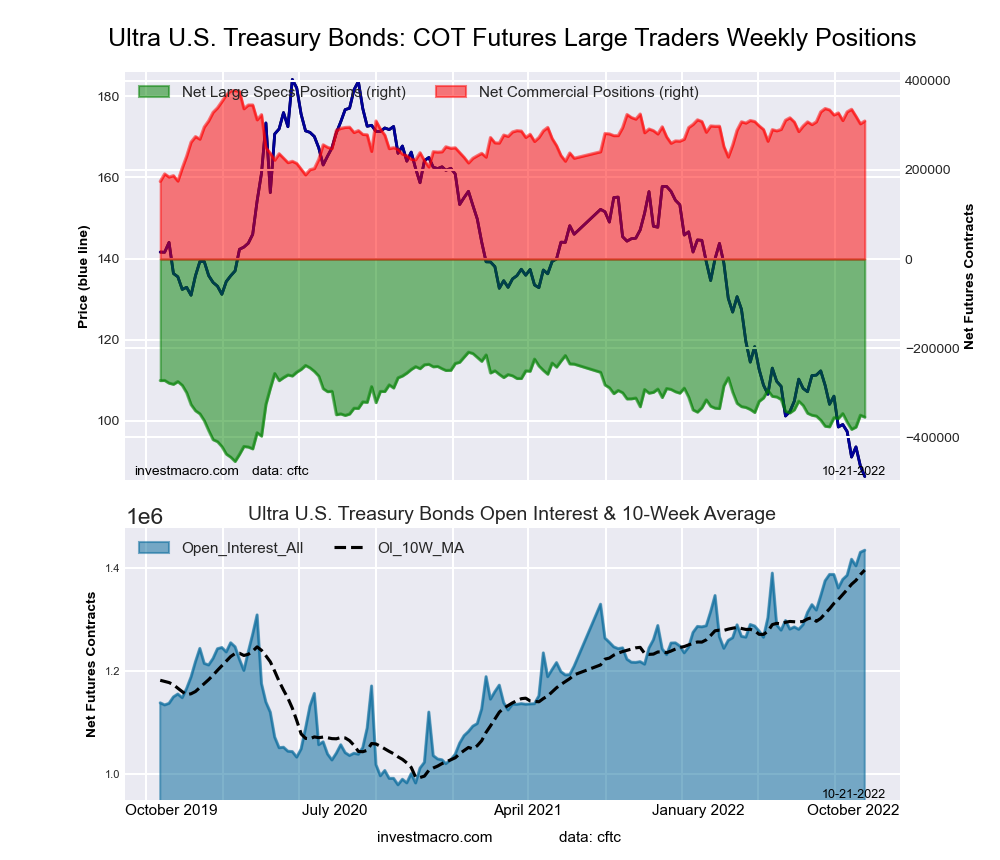

Eurodollar, Fed Funds & 10-Year lead Weekly Speculator Changes

The COTbond market speculator bets were evenly mixed this week as four out of the eight bond markets we cover had higher positioning this week while four markets had lower contracts.

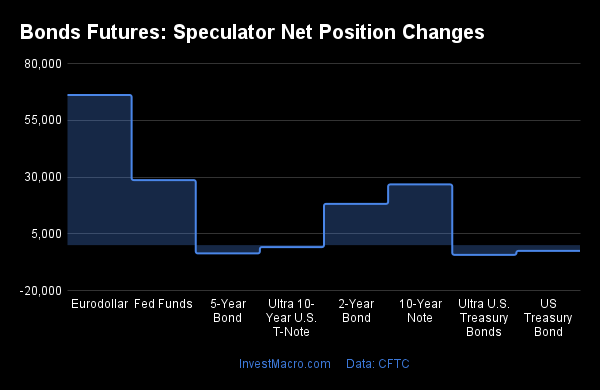

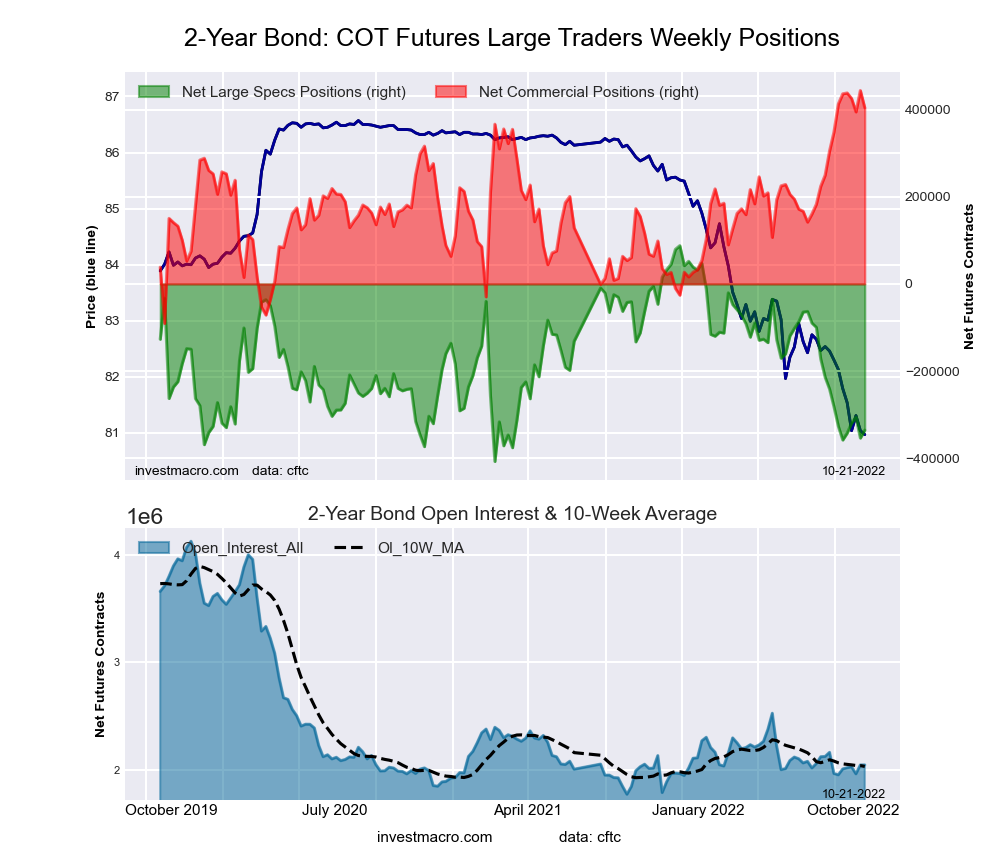

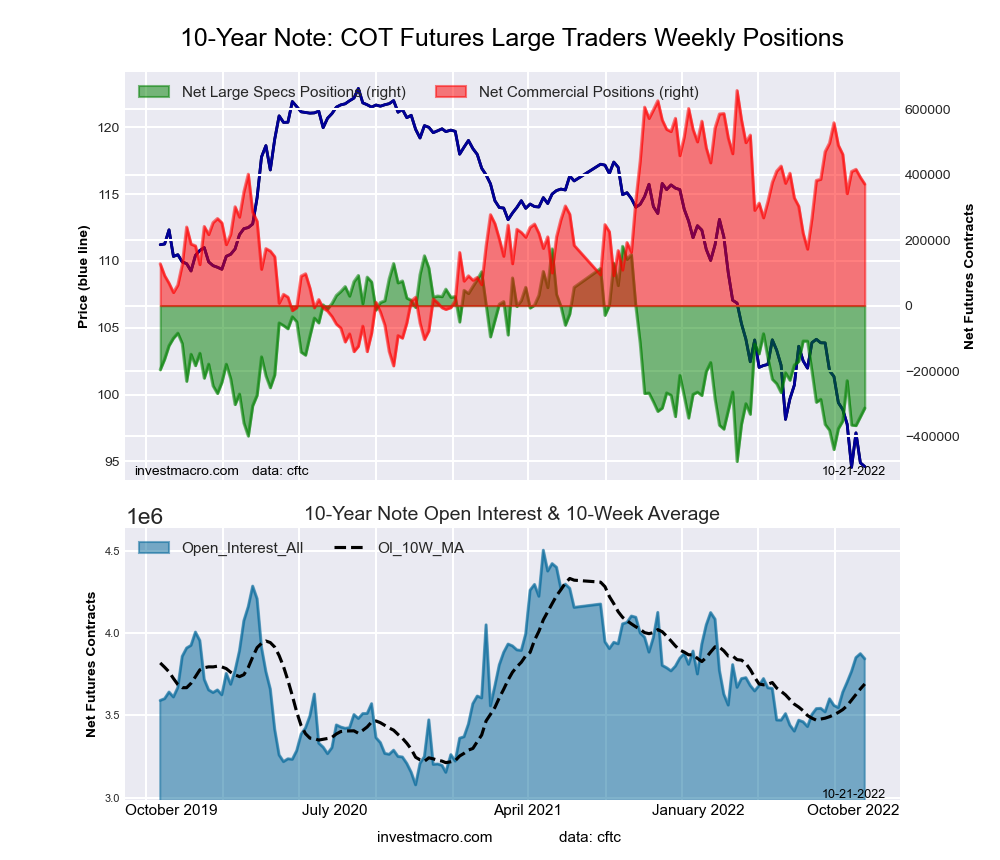

Leading the weekly gains for the bond markets was the Eurodollar (66,141 contracts) with the Fed Funds (28,633 contracts), the 10-Year Bond (26,725 contracts) and the 2-Year Bond (18,174 contracts) also showing a positive week.

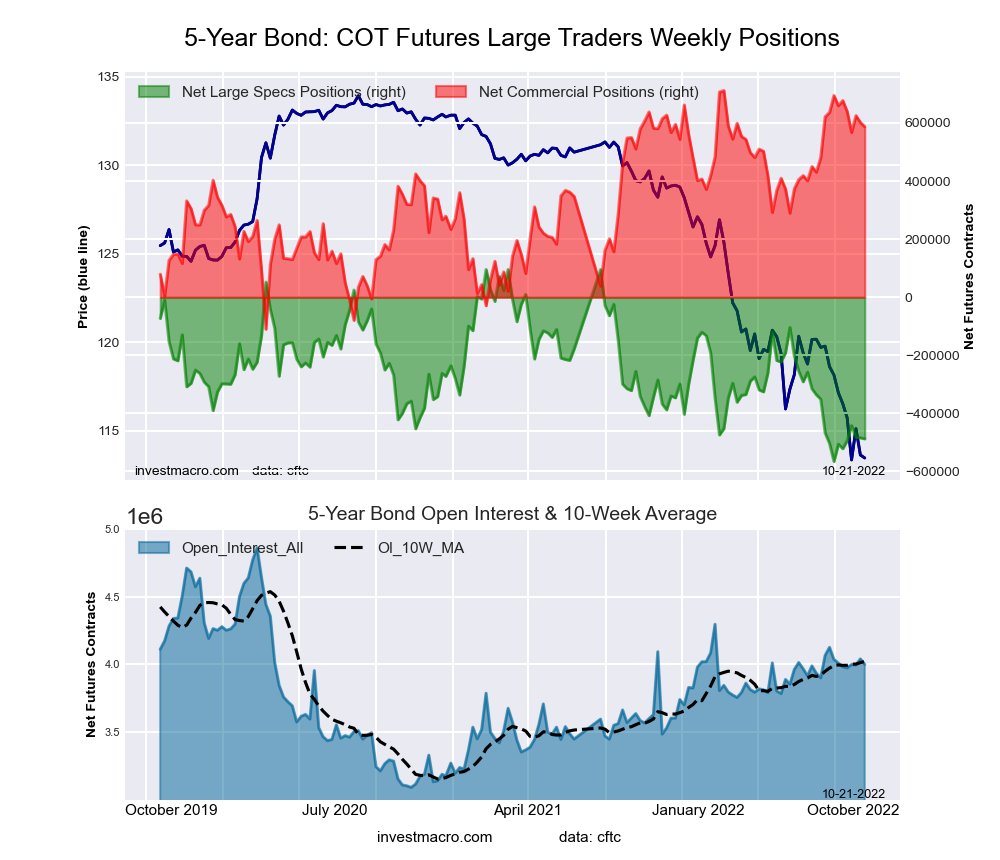

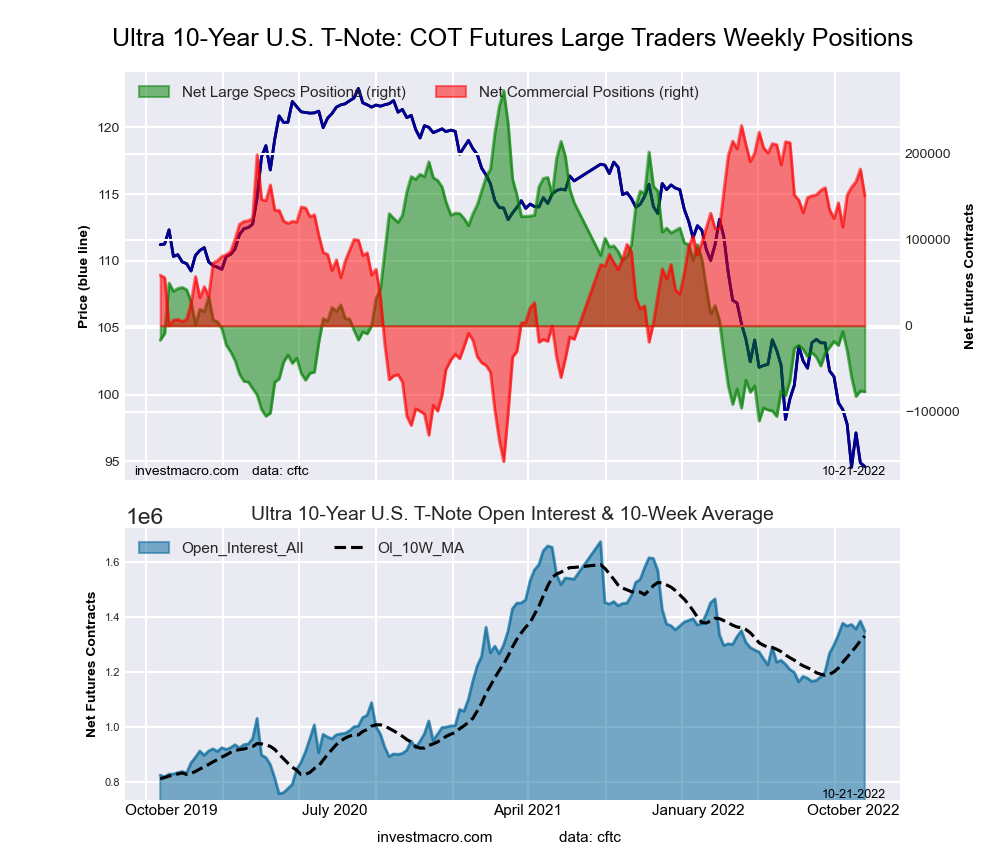

The bond markets leading the weekly declines in speculator bets this week was the Ultra US Bond (-4,286 contracts) with the 5-Year Bond (-3,657 contracts), the Long US Bond (-2,547 contracts) and the Ultra 10-Year (-880 contracts) also registering lower bets on the week.

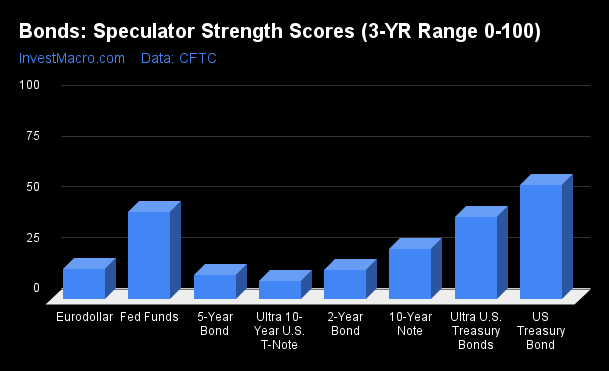

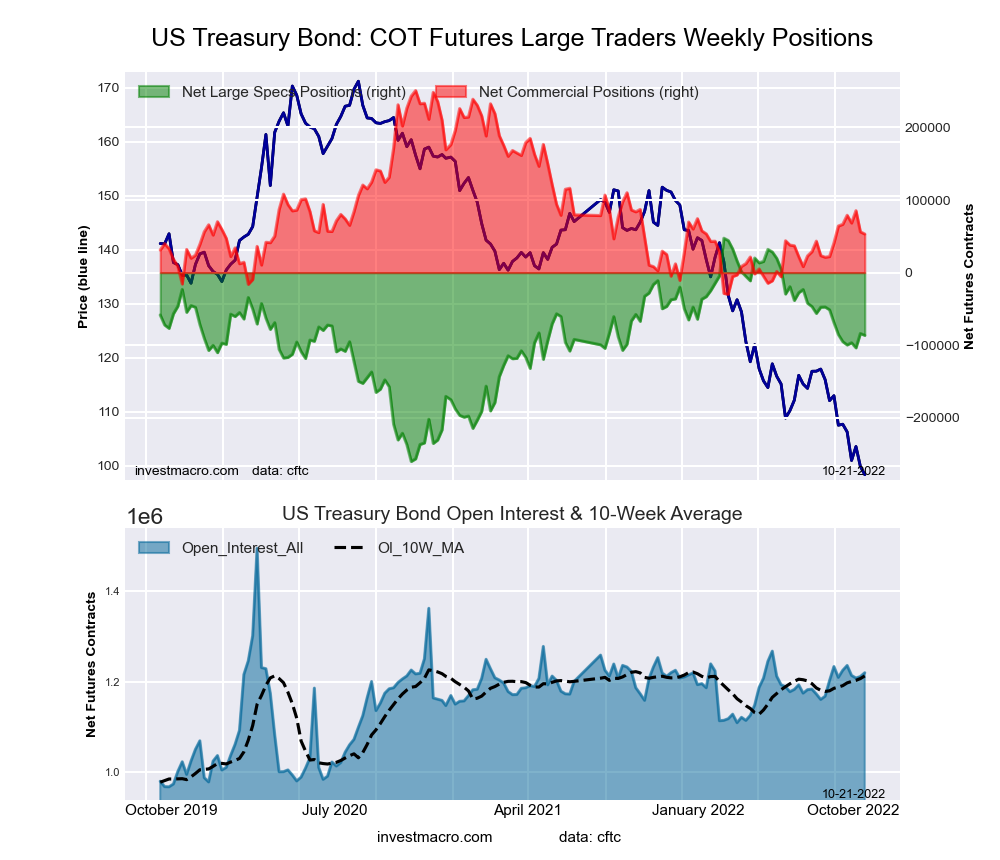

Strength Scores (a normalized measure of Speculator positions over a 3-Year range, from 0 to 100 where above 80 is extreme bullish and below 20 is extreme bearish) showed that the US Treasury Bond (56.5 percent) leads the bonds category for the week and is the only market above 50 percent or above the 3-Year midpoint.

On the downside, the Ultra 10-Year Bond (8.9 percent), 5-Year Bond (11.8 percent), 2-Year Bond (14.5 percent) and the Eurodollar (14.9 percent) came in at the lowest strength levels and are all in extreme bearish levels (below 20 percent).

Strength Statistics: Fed Funds (43.3 percent) vs Fed Funds previous week (39.7 percent) 2-Year Bond (14.5 percent) vs 2-Year Bond previous week (10.8 percent) 5-Year Bond (11.8 percent) vs 5-Year Bond previous week (12.3 percent) 10-Year Bond (24.8 percent) vs 10-Year Bond previous week (20.7 percent) Ultra 10-Year Bond (8.9 percent) vs Ultra 10-Year Bond previous week (9.1 percent) US Treasury Bond (56.5 percent) vs US Treasury Bond previous week (57.3 percent) Ultra US Treasury Bond (40.6 percent) vs Ultra US Treasury Bond previous week (42.3 percent) Eurodollar (14.9 percent) vs Eurodollar previous week (13.7 percent)

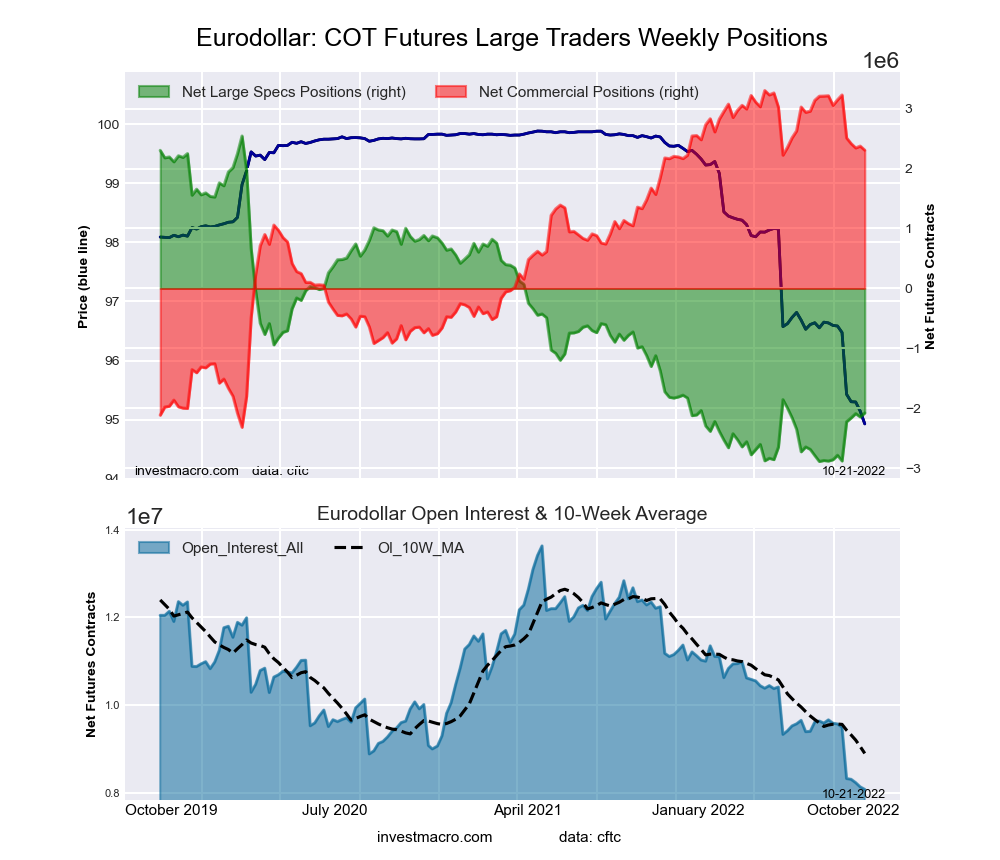

Eurodollar & 10-Year Bond top the Strength Trends

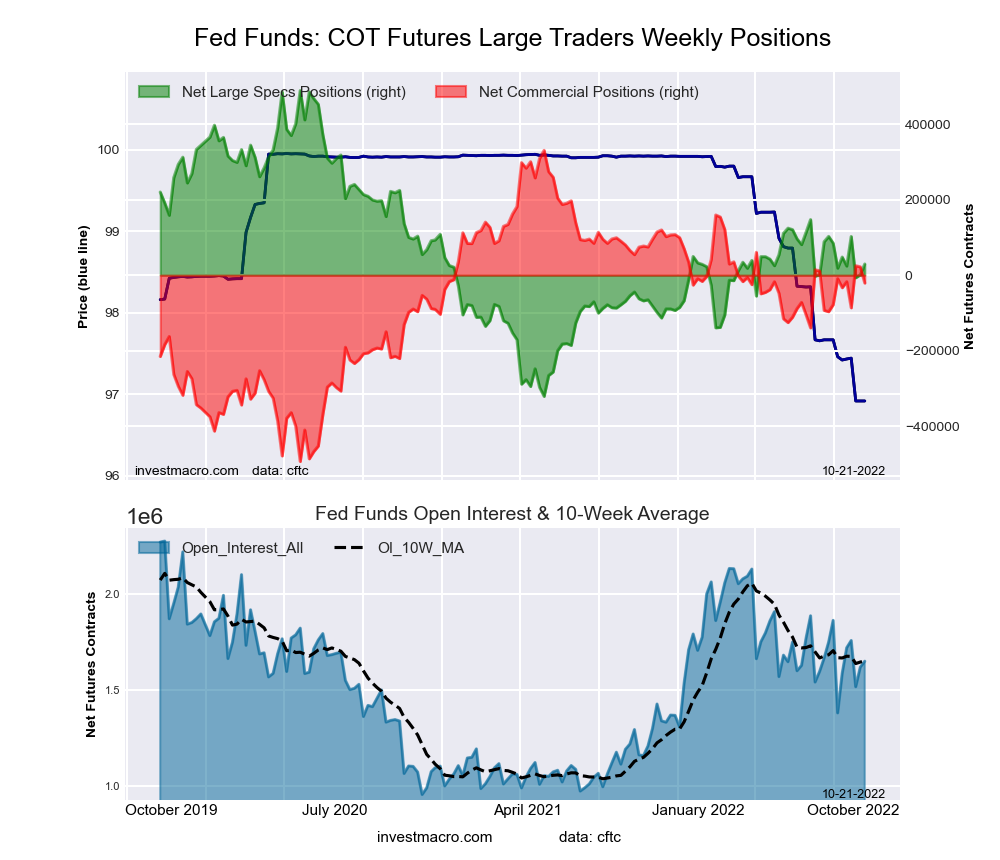

Strength Score Trends (or move index, calculates the 6-week changes in strength scores) showed that the Eurodollar (13.0 percent) leads the past six weeks trends for bonds this week. The 10-Year Bond (9.6 percent), the 5-Year Bond (2.8 percent), Fed Funds (1.3 percent) and the Ultra US Treasury Bond (1.2 percent) fill out the other positive movers in the latest trends data.

The Ultra 10-Year Bond (-14.0 percent) leads the downside trend scores currently while the next markets with lower trend scores were the 2-Year Bond (-1.8 percent) and the US Treasury Bond (-0.4 percent).

Strength Trend Statistics: Fed Funds (1.3 percent) vs Fed Funds previous week (-10.4 percent) 2-Year Bond (-1.8 percent) vs 2-Year Bond previous week (-14.6 percent) 5-Year Bond (2.8 percent) vs 5-Year Bond previous week (12.3 percent) 10-Year Bond (9.6 percent) vs 10-Year Bond previous week (15.2 percent) Ultra 10-Year Bond (-14.0 percent) vs Ultra 10-Year Bond previous week (-15.0 percent) US Treasury Bond (-0.4 percent) vs US Treasury Bond previous week (-4.9 percent) Ultra US Treasury Bond (1.2 percent) vs Ultra US Treasury Bond previous week (2.3 percent) Eurodollar (13.0 percent) vs Eurodollar previous week (13.2 percent)

Individual Bond Markets:

3-Month Eurodollars Futures:

The 3-Month Eurodollars large speculator standing this week came in at a net position of -2,077,075 contracts in the data reported through Tuesday. This was a weekly lift of 66,141 contracts from the previous week which had a total of -2,143,216 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 14.9 percent. The commercials are Bullish-Extreme with a score of 82.3 percent and the small traders (not shown in chart) are Bullish with a score of 54.1 percent.

3-Month Eurodollars Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

8.1

68.5

4.8

– Percent of Open Interest Shorts:

33.9

40.0

7.6

– Net Position:

-2,077,075

2,305,875

-228,800

– Gross Longs:

657,218

5,533,303

387,561

– Gross Shorts:

2,734,293

3,227,428

616,361

– Long to Short Ratio:

0.2 to 1

1.7 to 1

0.6 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

14.9

82.3

54.1

– Strength Index Reading (3 Year Range):

Bearish-Extreme

Bullish-Extreme

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

13.0

-15.0

29.8

30-Day Federal Funds Futures:

The 30-Day Federal Funds large speculator standing this week came in at a net position of 29,521 contracts in the data reported through Tuesday. This was a weekly lift of 28,633 contracts from the previous week which had a total of 888 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 43.3 percent. The commercials are Bullish with a score of 57.4 percent and the small traders (not shown in chart) are Bearish with a score of 37.5 percent.

30-Day Federal Funds Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

13.4

71.3

1.8

– Percent of Open Interest Shorts:

11.6

72.5

2.3

– Net Position:

29,521

-20,827

-8,694

– Gross Longs:

220,365

1,175,230

29,854

– Gross Shorts:

190,844

1,196,057

38,548

– Long to Short Ratio:

1.2 to 1

1.0 to 1

0.8 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

43.3

57.4

37.5

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

1.3

-1.4

2.1

2-Year Treasury Note Futures:

The 2-Year Treasury Note large speculator standing this week came in at a net position of -335,512 contracts in the data reported through Tuesday. This was a weekly gain of 18,174 contracts from the previous week which had a total of -353,686 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 14.5 percent. The commercials are Bullish-Extreme with a score of 92.3 percent and the small traders (not shown in chart) are Bearish with a score of 21.4 percent.

2-Year Treasury Note Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

7.0

83.6

7.8

– Percent of Open Interest Shorts:

23.4

63.8

11.2

– Net Position:

-335,512

404,181

-68,669

– Gross Longs:

143,755

1,709,706

160,055

– Gross Shorts:

479,267

1,305,525

228,724

– Long to Short Ratio:

0.3 to 1

1.3 to 1

0.7 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

14.5

92.3

21.4

– Strength Index Reading (3 Year Range):

Bearish-Extreme

Bullish-Extreme

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-1.8

-1.7

7.9

5-Year Treasury Note Futures:

The 5-Year Treasury Note large speculator standing this week came in at a net position of -487,577 contracts in the data reported through Tuesday. This was a weekly fall of -3,657 contracts from the previous week which had a total of -483,920 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 11.8 percent. The commercials are Bullish-Extreme with a score of 84.8 percent and the small traders (not shown in chart) are Bullish with a score of 53.8 percent.

5-Year Treasury Note Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

5.5

85.9

7.8

– Percent of Open Interest Shorts:

17.7

71.2

10.3

– Net Position:

-487,577

586,839

-99,262

– Gross Longs:

219,782

3,434,617

311,325

– Gross Shorts:

707,359

2,847,778

410,587

– Long to Short Ratio:

0.3 to 1

1.2 to 1

0.8 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

11.8

84.8

53.8

– Strength Index Reading (3 Year Range):

Bearish-Extreme

Bullish-Extreme

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

2.8

-8.8

14.9

10-Year Treasury Note Futures:

The 10-Year Treasury Note large speculator standing this week came in at a net position of -313,438 contracts in the data reported through Tuesday. This was a weekly increase of 26,725 contracts from the previous week which had a total of -340,163 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 24.8 percent. The commercials are Bullish with a score of 66.0 percent and the small traders (not shown in chart) are Bullish with a score of 66.3 percent.

10-Year Treasury Note Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

10.5

78.0

9.0

– Percent of Open Interest Shorts:

18.7

68.3

10.6

– Net Position:

-313,438

371,577

-58,139

– Gross Longs:

405,265

2,997,874

347,408

– Gross Shorts:

718,703

2,626,297

405,547

– Long to Short Ratio:

0.6 to 1

1.1 to 1

0.9 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

24.8

66.0

66.3

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

9.6

-14.1

13.2

Ultra 10-Year Notes Futures:

The Ultra 10-Year Notes large speculator standing this week came in at a net position of -76,651 contracts in the data reported through Tuesday. This was a weekly fall of -880 contracts from the previous week which had a total of -75,771 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 8.9 percent. The commercials are Bullish with a score of 79.1 percent and the small traders (not shown in chart) are Bullish with a score of 77.4 percent.

Ultra 10-Year Notes Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

7.1

80.6

11.6

– Percent of Open Interest Shorts:

12.8

69.4

17.1

– Net Position:

-76,651

151,326

-74,675

– Gross Longs:

96,245

1,087,382

155,853

– Gross Shorts:

172,896

936,056

230,528

– Long to Short Ratio:

0.6 to 1

1.2 to 1

0.7 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

8.9

79.1

77.4

– Strength Index Reading (3 Year Range):

Bearish-Extreme

Bullish

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-14.0

2.1

30.1

US Treasury Bonds Futures:

The US Treasury Bonds large speculator standing this week came in at a net position of -86,339 contracts in the data reported through Tuesday. This was a weekly reduction of -2,547 contracts from the previous week which had a total of -83,792 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 56.5 percent. The commercials are Bearish with a score of 29.6 percent and the small traders (not shown in chart) are Bullish with a score of 78.9 percent.

US Treasury Bonds Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

6.4

78.0

14.5

– Percent of Open Interest Shorts:

13.5

73.6

11.8

– Net Position:

-86,339

53,148

33,191

– Gross Longs:

78,416

951,261

176,693

– Gross Shorts:

164,755

898,113

143,502

– Long to Short Ratio:

0.5 to 1

1.1 to 1

1.2 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

56.5

29.6

78.9

– Strength Index Reading (3 Year Range):

Bullish

Bearish

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-0.4

-3.9

9.6

Ultra US Treasury Bonds Futures:

The Ultra US Treasury Bonds large speculator standing this week came in at a net position of -354,518 contracts in the data reported through Tuesday. This was a weekly lowering of -4,286 contracts from the previous week which had a total of -350,232 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 40.6 percent. The commercials are Bullish with a score of 63.9 percent and the small traders (not shown in chart) are Bullish with a score of 68.7 percent.

Ultra US Treasury Bonds Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

6.3

82.3

11.1

– Percent of Open Interest Shorts:

31.0

60.7

7.9

– Net Position:

-354,518

309,624

44,894

– Gross Longs:

90,476

1,179,562

158,799

– Gross Shorts:

444,994

869,938

113,905

– Long to Short Ratio:

0.2 to 1

1.4 to 1

1.4 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

40.6

63.9

68.7

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

1.2

-9.6

12.4

Article By InvestMacro – Receive our weekly COT Newsletter

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators) as well as their open interest (contracts open in the market at time of reporting). See CFTC criteria here.

“The primary value of the Wave Principle is that it provides a context for market analysis”

By Elliott Wave International

Elliott waves reflect the repetitive patterns of mass psychology — so they are ideally suited for analyzing the widely traded main stock indexes.

On the other hand, thinly traded individual stocks may not trace out Elliott wave price patterns nearly as well.

That said, there are many individual stocks which are widely traded — like most of the big and well-known companies (and others which have captured the interest of investors).

Consider the stock of the largest bank in the U.S. Back in March, our Global Market Perspective showed this chart and said:

This chart shows the five-wave pattern of JPMorgan Chase’s rise from March 2009 to September 2021.

Of course, the completion of a five-wave up pattern means a downtrend is next. When that analysis published, the share price was $134.40. As of this intraday writing on Oct.3, it’s $106.79.

Let’s go back in time to review another example of how Elliott wave analysis can be applied to an individual stock.

This case-in-point involves GE. The September Elliott Wave Theorist was discussing wave analysis with individual stocks and showed these side-by-side charts and said:

The October 27, 2000 [Global Market Perspective] published the chart on the left, showing a completed Elliott wave in GE stock. This quarter-century pattern portended a major reversal. The chart on the right shows what happened thereafter.

Not every forecast based on the Elliott wave model works out perfectly. At the same time, keep in mind these words from Frost & Prechter’s Wall Street classic, Elliott Wave Principle: Key to Market Behavior:

The primary value of the Wave Principle is that it provides a context for market analysis. This context provides both a basis for disciplined thinking and a perspective on the market’s general position and outlook. At times, its accuracy in identifying, and even anticipating changes in direction is almost unbelievable.

If you’d like to read the entire online version of the book for free, you may do so once you become a member of Club EWI, the world’s largest Elliott wave educational community (approximately 500,000 worldwide members).

A Club EWI membership also opens the door to free access to a wealth of other Elliott wave resources — such as videos and articles from Elliott Wave International’s analysts.

We all have to make hard decisions from time to time. The hardest of my life was whether or not to change research fields after my PhD, from fundamental physics to climate physics. I had job offers that could have taken me in either direction – one to join Stephen Hawking’s Relativity and Gravitation Group at Cambridge University, another to join the Met Office as a scientific civil servant.

I wrote down the pros and cons of both options as one is supposed to do, but then couldn’t make up my mind at all. Like Buridan’s donkey, I was unable to move to either the bale of hay or the pail of water. It was a classic case of paralysis by analysis.

Since it was doing my head in, I decided to try to forget about the problem for a couple of weeks and get on with my life. In that intervening time, my unconscious brain decided for me. I simply walked into my office one day and the answer had somehow become obvious: I would make the change to studying the weather and climate.

More than four decades on, I’d make the same decision again. My fulfilling career has included developing a new, probabilistic way of forecasting weather and climate which is helping humanitarian and disaster relief agencies make better decisions ahead of extreme weather events. (This and many other aspects are described in my new book, The Primacy of Doubt.)

But I remain fascinated by what was going on in my head back then, which led my subconscious to make a life-changing decision that my conscious could not. Is there something to be understood here not only about how to make difficult decisions, but about how humans make the leaps of imagination that characterise us as such a creative species? I believe the answer to both questions lies in a better understanding of the extraordinary power of noise.

Imprecise supercomputers

I went from the pencil-and-paper mathematics of Einstein’s theory of general relativity to running complex climate models on some of the world’s biggest supercomputers. Yet big as they were, they were never big enough – the real climate system is, after all, very complex.

In the early days of my research, one only had to wait a couple of years and top-of-the-range supercomputers would get twice as powerful. This was the era where transistors were getting smaller and smaller, allowing more to be crammed on to each microchip. The consequent doubling of computer performance for the same power every couple of years was known as Moore’s Law.

This story is part of Conversation Insights

The Insights team generates long-form journalism and is working with academics from different backgrounds who have been engaged in projects to tackle societal and scientific challenges.

There is, however, only so much miniaturisation you can do before the transistor starts becoming unreliable in its key role as an on-off switch. Today, with transistors starting to approach atomic size, we have pretty much reached the limit of Moore’s Law. To achieve more number-crunching capability, computer manufacturers must bolt together more and more computing cabinets, each one crammed full of chips.

But there’s a problem. Increasing number-crunching capability this way requires a lot more electric power – modern supercomputers the size of tennis courts consume tens of megawatts. I find it something of an embarrassment that we need so much energy to try to accurately predict the effects of climate change.

That’s why I became interested in how to construct a more accurate climate model without consuming more energy. And at the heart of this is an idea that sounds counterintuitive: by adding random numbers, or “noise”, to a climate model, we can actually make it more accurate in predicting the weather.

A constructive role for noise

Noise is usually seen as a nuisance – something to be minimised wherever possible. In telecommunications, we speak about trying to maximise the “signal-to-noise ratio” by boosting the signal or reducing the background noise as much as possible. However, in nonlinear systems, noise can be your friend and actually contribute to boosting a signal. (A nonlinear system is one whose output does not vary in direct proportion to the input. You will likely be very happy to win £100 million on the lottery, but probably not twice as happy to win £200 million.)

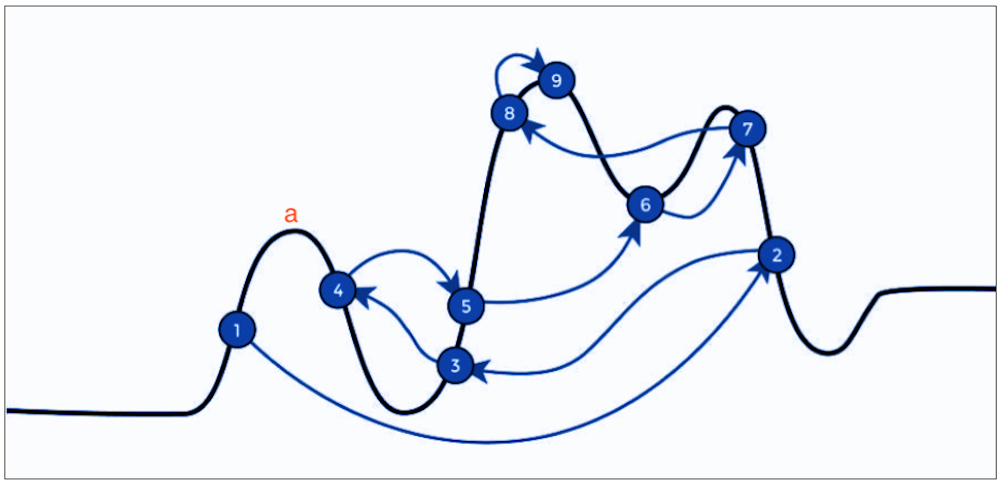

Noise can, for example, help us find the maximum value of a complicated curve such as in Figure 1, below. There are many situations in the physical, biological and social sciences as well as in engineering where we might need to find such a maximum. In my field of meteorology, the process of finding the best initial conditions for a global weather forecast involves identifying the maximum point of a very complicated meteorological function.

Figure 1

A curve with multiple local peaks and troughs. Author provided

However, employing a “deterministic algorithm” to locate the global maximum doesn’t usually work. This type of algorithm will typically get stuck at a local peak (for example at point a) because the curve moves downwards in both directions from there.

An answer is to use a technique called “simulated annealing” – so called because of its similarities with (annealing), the heat treatment process that changes the properties of metals. Simulated annealing, which employs noise to get round the issue of getting stuck at local peaks, has been used to solve many problems including the classic travelling salesman puzzle of finding the shortest path between a large number of cities on a map.

Figure 1 shows a possible route to locating the curve’s global maximum (point 9) by using the following criteria:

If a randomly chosen point is higher than the current position on the curve, then the new point is always moved to.

If it is lower than the current position, the suggested point isn’t necessarily rejected. It depends whether the new point is a lot lower or just a little lower.

However, the decision to move to a new point also depends on how long the analysis has been running. Whereas in the early stages, random points quite a bit lower than the current position may be accepted, in later stages only those that are higher or just a tiny bit lower are accepted.

The technique is known as simulated annealing because early on – like hot metal in the early phase of cooling – the system is pliable and changeable. Later in the process – like cold metal in the late phase of cooling – it is almost rigid and unchangeable.

How noise can help climate models

Noise was introduced into comprehensive weather and climate models around 20 years ago. A key reason was to represent model uncertainty in our ensemble weather forecasts – but it turned out that adding noise also reduced some of the biases the models had, making them more accurate simulators of weather and climate.

Unfortunately, these models require huge supercomputers and a lot of energy to run them. They divide the world into small gridboxes, with the atmosphere and ocean within each assumed to be constant – which, of course, it isn’t. The horizontal scale of a typical gridbox is around 100km – so one way of making a model more accurate is to reduce this distance to 50km, or 10km or 1km. However, halving the volume of a gridbox increases the computational cost of running the model by up to a factor of 16, meaning it consumes a lot more energy.

Here again, noise offered an appealing alternative. The proposal was to use it to represent the unpredictable (and unmodellable) variations in small-scale climatic processes like turbulence, cloud systems, ocean eddies and so on. I argued that adding noise could be a way of boosting accuracy without having to incur the enormous computational cost of reducing the size of the gridboxes. For example, as has now been verified, adding noise to a climate model increases the likelihood of producing extreme hurricanes – reflecting the potential reality of a world whose weather is growing more extreme due to climate change.

The computer hardware we use for this modelling is inherently noisy – electrons travelling along wires in a computer move in partly random ways due to its warm environment. Such randomness is called “thermal noise”. Could we save even more energy by tapping into it, rather than having to use software to generate pseudo-random numbers? To me, low-energy “imprecise” supercomputers that are inherently noisy looked like a win-win proposal.

But not all of my colleagues were convinced. They were uncomfortable that computers might not give the same answers from one day to the next. To try to persuade them, I began to think about other real-world systems that, because of limited energy availability, also use noise that is generated within their hardware. And I stumbled on the human brain.

Noise in the brain

Every second of the waking day, our eyes alone send gigabytes of data to the brain. That’s not much different to the amount of data a climate model produces each time it outputs data to memory.

The brain has to process this data and somehow make sense of it. If it did this using the power of a supercomputer, that would be impressive enough. But it does it using one millionth of that power, about 20W instead of 20MW – what it takes to power a lightbulb. Such energy efficiency is mind-bogglingly impressive. How on Earth does the brain do it?

An adult brain contains some 80 billion neurons. Each neuron has a long slender biological cable – the axon – along which electrical impulses are transmitted from one set of neurons to the next. But these impulses, which collectively describe information in the brain, have to be boosted by protein “transistors” positioned at regular intervals along the axons. Without them, the signal would dissipate and be lost.

The energy for these boosts ultimately comes from an organic compound in the blood called ATP (adenosine triphosphate). This enables electrically charged atoms of sodium and potassium (ions) to be pushed through small channels in the neuron walls, creating electrical voltages which, much like those in silicon transistors, amplify the neuronal electric signals as they travel along the axons.

With 20W of power spread across tens of billions of neurons, the voltages involved are tiny, as are the axon cables. And there is evidence that axons with a diameter less than about 1 micron (which most in the brain are) are susceptible to noise. In other words, the brain is a noisy system.

If this noise simply created unhelpful “brain fog”, one might wonder why we evolved to have so many slender axons in our heads. Indeed, there are benefits to having fatter axons: the signals propagate along them faster. If we still needed fast reaction times to escape predators, then slender axons would be disadvantageous. However, developing communal ways of defending ourselves against enemies may have reduced the need for fast reaction times, leading to an evolutionary trend towards thinner axons.

Perhaps, serendipitously, evolutionary mutations that further increased neuron numbers and reduced axon sizes, keeping overall energy consumption the same, made the brain’s neurons more susceptible to noise. And there is mounting evidence that this had another remarkable effect: it encouraged in humans the ability to solve problems that required leaps in imagination and creativity.

Perhaps we only truly became Homo Sapiens when significant noise began to appear in our brains?

Putting noise in the brain to good use

Many animals have developed creative approaches to solving problems, but there is nothing to compare with a Shakespeare, a Bach or an Einstein in the animal world.

How do creative geniuses come up with their ideas? Here’s a quote from Andrew Wiles, perhaps the most famous mathematician alive today, about the time leading up to his celebrated proof of the maths problem (misleadingly) known as Fermat’s Last Theorem:

When you reach a real impasse, then routine mathematical thinking is of no use to you. Leading up to that kind of new idea, there has to be a long period of tremendous focus on the problem without any distraction. You have to really think about nothing but that problem – just concentrate on it. And then you stop. [At this point] there seems to be a period of relaxation during which the subconscious appears to take over – and it’s during this time that some new insight comes.

BBC’s Horizon unpicks Andrew Wiles’s novel approach to solving Fermat’s Theorem.

This notion seems universal. Physics Nobel Laureate Roger Penrose has spoken about his “Eureka moment” when crossing a busy street with a colleague (perhaps reflecting on their conversation while also looking out for oncoming traffic). For the father of chaos theory Henri Poincaré, it was catching a bus.

And it’s not just creativity in mathematics and physics. Comedian John Cleese, of Monty Python fame, makes much the same point about artistic creativity – it occurs not when you are focusing hard on your trade, but when you relax and let your unconscious mind wander.

Of course, not all the ideas that bubble up from your subconscious are going to be Eureka moments. Physicist Michael Berry talks about these subconscious ideas as if they are elementary particles called “claritons”:

Actually, I do have a contribution to particle physics … the elementary particle of sudden understanding: the “clariton”. Any scientist will recognise the “aha!” moment when this particle is created. But there is a problem: all too frequently, today’s clariton is annihilated by tomorrow’s “anticlariton”. So many of our scribblings disappear beneath a rubble of anticlaritons.

Here is something we can all relate to: that in the cold light of day, most of our “brilliant” subconscious ideas get annihilated by logical thinking. Only a very, very, very small number of claritons remain after this process. But the ones that do are likely to be gems.

In his renowned book Thinking Fast and Slow, the Nobel prize-winning psychologist Daniel Kahneman describes the brain in a binary way. Most of the time when walking, chatting and looking around (in other words when multitasking), it operates in a mode Kahneman calls “system 1” – a rather fast, automatic, effortless mode of operation.

By contrast, when we are thinking hard about a specific problem (unitasking), the brain is in the slower, more deliberative and logical “system 2”. To perform a calculation like 37×13, we have to stop walking, stop talking, close our eyes and even put our hands over our ears. No chance for significant multitasking in system 2.

My 2015 paper with computational neuroscientist Michael O’Shea interpreted system 1 as a mode where available energy is spread across a large number of active neurons, and system 2 as where energy is focused on a smaller number of active neurons. The amount of energy per active neuron is therefore much smaller when in the system 1 mode, and it would seem plausible that the brain is more susceptible to noise when in this state. That is, in situations when we are multitasking, the operation of any one of the neurons will be most susceptible to the effects of noise in the brain.

Berry’s picture of clariton-anticlariton interaction seems to suggest a model of the brain where the noisy system 1 and the deterministic system 2 act in synergy. The anticlariton is the logical analysis that we perform in system 2 which, most of the time, leads us to reject our crazy system 1 ideas.

But sometimes one of these ideas turns out to be not so crazy.

This is reminiscent of how our simulated annealing analysis (Figure 1) works. Initially, we might find many “crazy” ideas appealing. But as we get closer to locating the optimal solution, the criteria for accepting a new suggestion becomes more stringent and discerning. Now, system 2 anticlaritons are annihilating almost everything the system 1 claritons can throw at them – but not quite everything, as Wiles found to his great relief.

The key to creativity

If the key to creativity is the synergy between noisy and deterministic thinking, what are some consequences of this?

On the one hand, if you do not have the necessary background information then your analytic powers will be depleted. That’s why Wiles says that leading up to the moment of insight, you have to immerse yourself in your subject. You aren’t going to have brilliant ideas which will revolutionise quantum physics unless you have a pretty good grasp of quantum physics in the first place.

But you also need to leave yourself enough time each day to do nothing much at all, to relax and let your mind wander. I tell my research students that if they want to be successful in their careers, they shouldn’t spend every waking hour in front of their laptop or desktop. And swapping it for social media probably doesn’t help either, since you still aren’t really multitasking – each moment you are on social media, your attention is still fixed on a specific issue.

But going for a walk or bike ride or painting a shed probably does help. Personally, I find that driving a car is a useful activity for coming up with new ideas and thoughts – provided you don’t turn the radio on.

When making difficult decisions, this suggests that, having listed all the pros and cons, it can be helpful not to actively think about the problem for a while. I think this explains how, years ago, I finally made the decision to change my research direction – not that I knew it at the time.

Because the brain’s system 1 is so energy efficient, we use it to make the vast majority of the many decisions in our daily lives (some say as many as 35,000) – most of which aren’t that important, like whether to continue putting one leg in front of the other as we walk down to the shops. (I could alternatively stop after each step, survey my surroundings to make sure a predator was not going to jump out and attack me, and on that basis decide whether to take the next step.)

However, this system 1 thinking can sometimes lead us to make bad decisions, because we have simply defaulted to this low-energy mode and not engaged system 2 when we should have. How many times do we say to ourselves in hindsight: “Why didn’t I give such and such a decision more thought?”

Of course, if instead we engaged system 2 for every decision we had to make, then we wouldn’t have enough time or energy to do all the other important things we have to do in our daily lives (so the shops may have shut by the time we reach them).

From this point of view, we should not view giving wrong answers to unimportant questions as evidence of irrationality. Kahneman cites the fact that more than 50% of students at MIT, Harvard and Princeton gave the incorrect answer to this simple question – a bat and ball costs $1.10; the bat costs one dollar more than the ball; how much does the ball cost? – as evidence of our irrationality. The correct answer, if you think about it, is 5 cents. But system 1 screams out ten cents.

If we were asked this question on pain of death, one would hope we would spend enough thought to come up with the correct answer. But if we were asked the question as part of an anonymous after-class test, when we had much more important things to spend time and energy doing, then I’d be inclined to think of it as irrational to give the right answer.

If we had 20MW to run the brain, we could spend part of it solving unimportant problems. But we only have 20W and we need to use it carefully. Perhaps it’s the 50% of MIT, Harvard and Princeton students who gave the wrong answer who are really the clever ones.

Just as a climate model with noise can produce types of weather that a model without noise can’t, so a brain with noise can produce ideas that a brain without noise can’t. And just as these types of weather can be exceptional hurricanes, so the idea could end up winning you a Nobel Prize.

So, if you want to increase your chances of achieving something extraordinary, I’d recommend going for that walk in the countryside, looking up at the clouds, listening to the birds cheeping, and thinking about what you might eat for dinner.

So could computers be creative?

Will computers, one day, be as creative as Shakespeare, Bach or Einstein? Will they understand the world around us as we do? Stephen Hawking famously warned that AI will eventually take over and replace mankind.

However, the best-known advocate of the idea that computers will never understand as we do is Hawking’s old colleague, Roger Penrose. In making his claim, Penrose invokes an important “meta” theorem in mathematics known as Gödel’s theorem, which says there are mathematical truths that can’t be proven by deterministic algorithms.

There is a simple way of illustrating Gödel’s theorem. Suppose we make a list of all the most important mathematical theorems that have been proven since the time of the ancient Greeks. First on the list would be Euclid’s proof that there are an infinite number of prime numbers, which requires one really creative step (multiply the supposedly finite number of primes together and add one). Mathematicians would call this a “trick” – shorthand for a clever and succinct mathematical construction.

But is this trick useful for proving important theorems further down the list, like Pythagoras’s proof that the square root of two cannot be expressed as the ratio of two whole numbers? It’s clearly not; we need another trick for that theorem. Indeed, as you go down the list, you’ll find that a new trick is typically needed to prove each new theorem. It seems there is no end to the number of tricks that mathematicians will need to prove their theorems. Simply loading a given set of tricks on a computer won’t necessarily make the computer creative.

Does this mean mathematicians can breathe easily, knowing their jobs are not going to be taken over by computers? Well maybe not.

I have been arguing that we need computers to be noisy rather than entirely deterministic, “bit-reproducible” machines. And noise, especially if it comes from quantum mechanical processes, would break the assumptions of Gödel’s theorem: a noisy computer is not an algorithmic machine in the usual sense of the word.

Does this imply that a noisy computer can be creative? Alan Turing, pioneer of the general-purpose computing machine, believed this was possible, suggesting that “if a machine is expected to be infallible then it cannot also be intelligent”. That is to say, if we want the machine to be intelligent then it had better be capable of making mistakes.

Others may argue there is no evidence that simply adding noise will make an otherwise stupid machine into an intelligent one – and I agree, as it stands. Adding noise to a climate model doesn’t automatically make it an intelligent climate model.

However, the type of synergistic interplay between noise and determinism – the kind that sorts the wheat from the chaff of random ideas – has hardly yet been developed in computer codes. Perhaps we could develop a new type of AI model where the AI is trained by getting it to solve simple mathematical theorems using the clariton-anticlariton model; by making guesses and seeing if any of these have value.

For this to be at all tractable, the AI system would need to be trained to focus on “educated random guesses”. (If the machine’s guesses are all uneducated ones, it will take forever to make progress – like waiting for a group of monkeys to type the first few lines of Hamlet.)

For example, in the context of Euclid’s proof that there are an unlimited number of primes, could we train an AI system in such a way that a random idea like “multiply the assumed finite number of primes together and add one” becomes much more likely than the completely useless random idea “add the assumed finite number of primes together and subtract six”? And if a particular guess turns out to be especially helpful, can we train the AI system so that the next guess is a refinement of the last one?

If we can somehow find a way to do this, it could open up modelling to a completely new level that is relevant to all fields of study. And in so doing, we might yet reach the so-called “singularity” when machines take over from humans. But only when AI developers fully embrace the constructive role of noise – as it seems the brain did many thousands of years ago.

For now, I feel the need for another walk in the countryside. To blow away some fusty old cobwebs – and perhaps sow the seeds for some exciting new ones.

Frontier Lithium Inc. announced the latest group of drill results from its Spark Deposit in northwestern Ontario. The firm reported it intersected 326.6m of pegmatite averaging 1.92% lithium oxide (Li2O), which included a 50m high-grade zone of 2.98% Li2O. Canaccord Genuity Corp. (Canada) advised in a research update that the positive results achieved in Frontier’s Phase XII drill program once again demonstrate grades that are well above the current mineral resource estimate of 1.38% Li2O.