By Analytical Department RoboForex

GBP/USD traded at 1.3364 on Thursday. The pair declined over the previous two sessions and is now showing signs of a tentative recovery amid expectations of a possible de-escalation in the Middle East conflict.

The US has reportedly presented Iran with a 15-point settlement plan following discussions about a potential month-long truce. However, Iran has rejected participation in negotiations, stating that US diplomacy cannot be trusted.

In the UK, February inflation figures matched expectations. Headline CPI held steady at 3%, while core inflation edged up slightly to 3.2% against a forecast of 3.1%. However, the data had limited impact on the market, as it reflected conditions prior to the latest escalation in the Middle East.

Against the backdrop of lower oil prices, investors are revising their expectations for Bank of England policy. The market is now pricing in fewer than two rate hikes before year-end, with total expected tightening estimated at approximately 68 basis points, down from nearly 75 basis points previously.

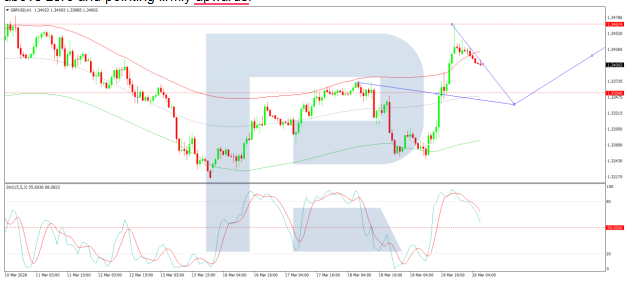

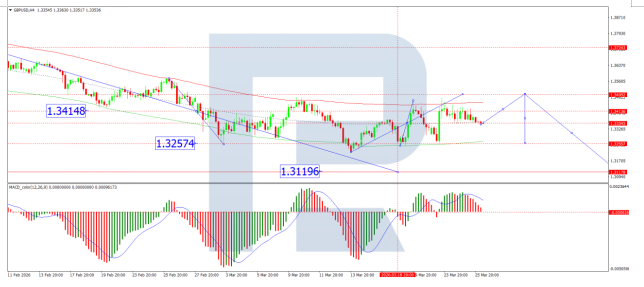

Technical Analysis

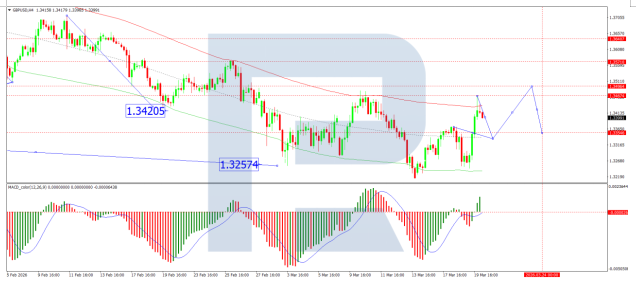

On the H4 GBP/USD chart, the market is forming a broad consolidation range around 1.3354, currently extending up to 1.3434. A decline to 1.3255 is expected in the near term, followed by the formation of a new consolidation range. An upside breakout would pave the way for a continuation wave to 1.3494, while a downside breakout would suggest further movement to 1.3119. Technically, this scenario is confirmed by the MACD indicator, whose signal line is above zero and pointing firmly downwards.

On the H1 chart, the market has formed a compact consolidation range around 1.3355. A downside breakout has initiated a wave structure extending to 1.3255. Should this level be breached, further downside towards 1.3125 is likely. Conversely, an upside breakout from the range could trigger a growth wave to 1.3494. Technically, this scenario is confirmed by the Stochastic oscillator, with its signal line below 20 and pointing firmly downwards.

Conclusion

GBP/USD is navigating competing forces amid short-term volatility driven by geopolitical headlines. While tentative signs of a potential US–Iran truce have offered some relief to markets, Iran’s rejection of negotiations underscores the fragility of hopes for de-escalation. Meanwhile, UK inflation data – though in line with forecasts – has been largely overlooked given its pre-escalation timeframe. Lower oil prices have prompted markets to scale back expectations for Bank of England tightening, offering modest support for sterling. With technical indicators pointing to continued consolidation and the Middle East situation remaining fluid, the pair’s near-term direction will likely hinge on further geopolitical developments.

Disclaimer

Any forecasts contained herein are based on the author’s particular opinion. This analysis may not be treated as trading advice. RoboForex bears no responsibility for trading results based on trading recommendations and reviews contained herein.