By InvestMacro

Here are the latest charts and statistics for the Commitment of Traders (COT) reports data published by the Commodities Futures Trading Commission (CFTC).

The latest COT data is updated through Tuesday July 21st and shows a quick view of how large traders (for-profit speculators and commercial entities) were positioned in the futures markets.

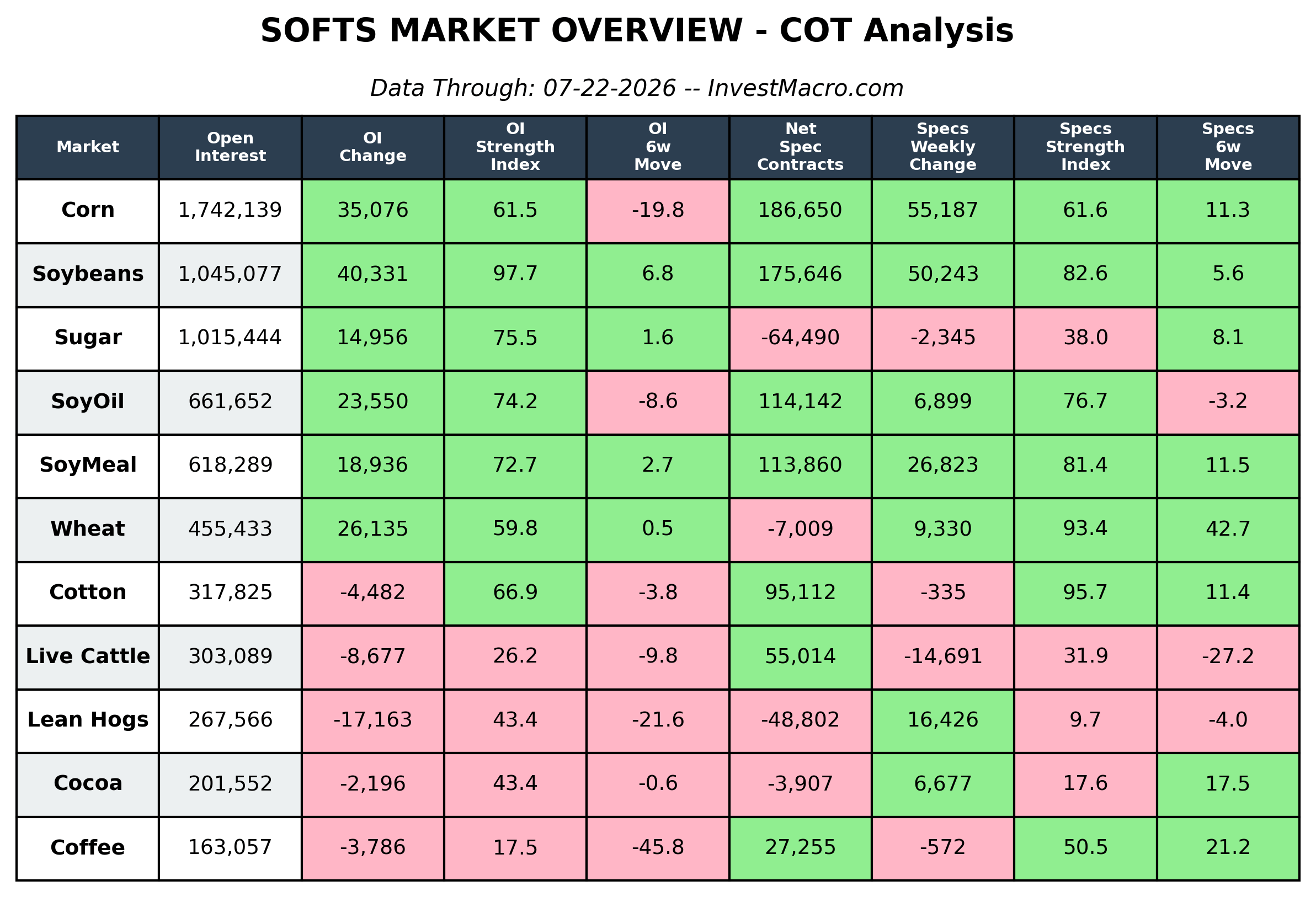

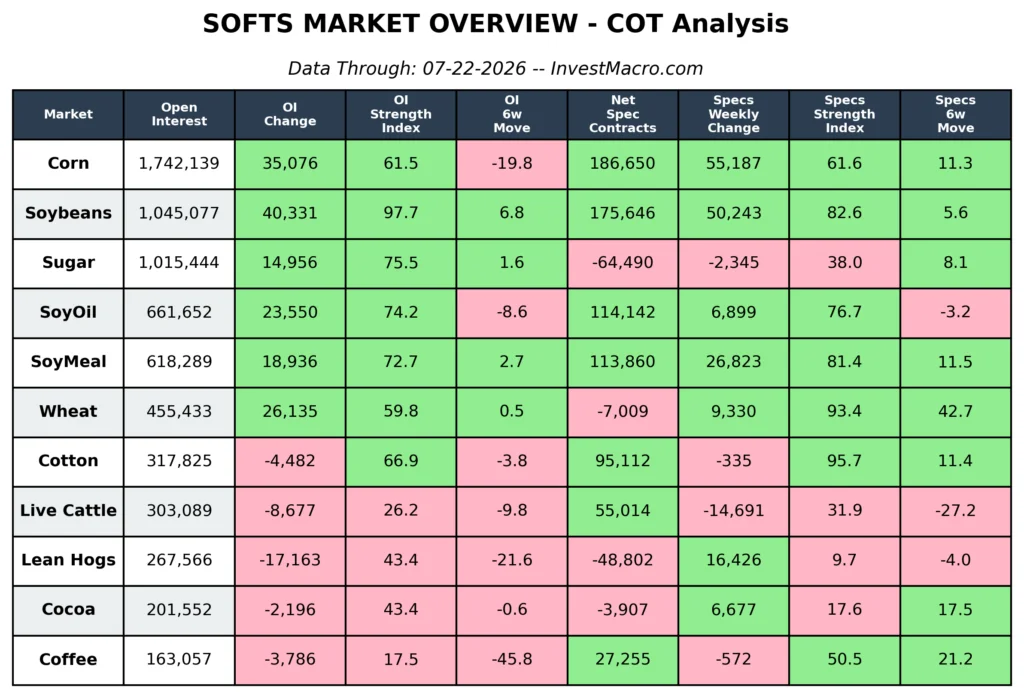

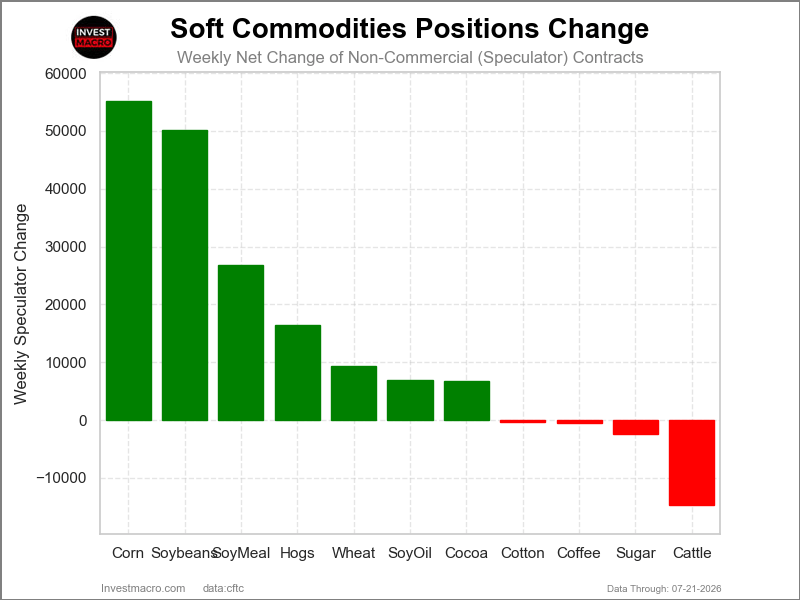

Weekly Speculator Changes led by Corn & Soybeans

The COT soft commodities markets speculator bets were overall higher this week as seven out of the eleven softs markets we cover had higher positioning while the other four markets had lower speculator contracts.

Leading the gains for the softs markets was Corn (55,187 contracts) with Soybeans (50,243 contracts), Soybean Meal (26,823 contracts), Lean Hogs (16,426 contracts), Wheat (9,330 contracts), Soybean Oil (6,899 contracts) and Cocoa (6,677 contracts) also showing positive weeks.

The markets with the declines in speculator bets this week were Live Cattle (-14,691 contracts) with Sugar (-2,345 contracts), Coffee (-572 contracts) and with Cotton (-335 contracts) also registering lower bets on the week.

Soybean Meal leads the weekly Soft Commodities Price Performance Leaders

This week’s highest price performance for the Soft Commodities markets was Soybean Meal, which rose by over 5% with a 5.29% gain. Soybeans was next up with a 3.77% gain, followed by Soybean Oil, which rose by 3.42%. Not far behind was Corn with a 3.28% gain over the past five days, while Wheat was higher by 1.53%.

Live Cattle saw a small boost by 0.71% on the week, while Cotton rounded out the gainers with a 0.60% increase.

On the downside, Sugar saw a small dip by -0.40%. Coffee was lower by -2.15%, while Cocoa fell by almost 5% with a -4.97% decline. The biggest decliner on the week was Lean Hogs, which dropped by -12.42% over the past five days.

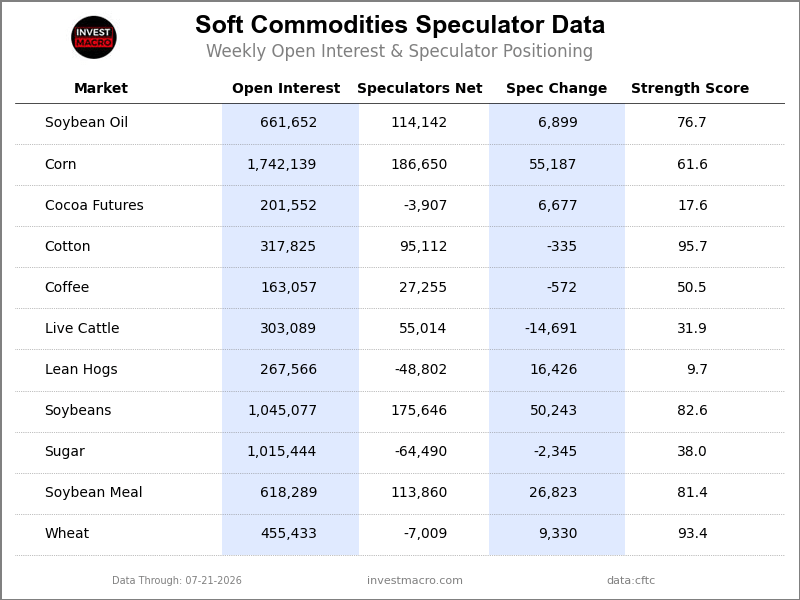

Soft Commodities Data:

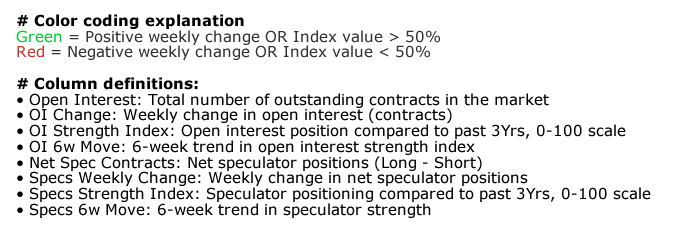

Legend: Weekly Speculators Change | Speculators Current Net Position | Speculators Strength Score compared to last 3-Years (0-100 range)

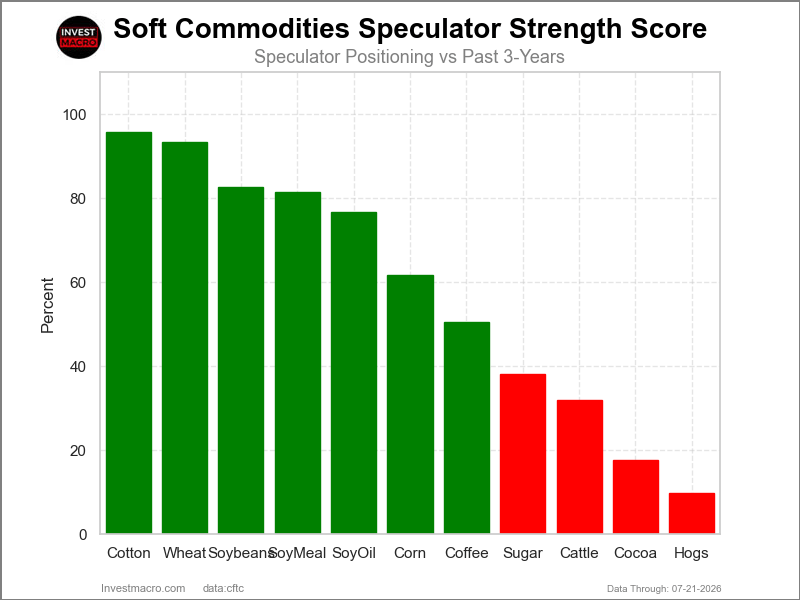

Strength Scores led by Cotton & Wheat

COT Strength Scores (a normalized measure of Speculator positions over a 3-Year range, from 0 to 100 where above 80 is Extreme-Bullish and below 20 is Extreme-Bearish) showed that Cotton (96 percent) and Wheat (93 percent) lead the softs markets this week. Soybeans (83 percent), Soybean Meal (81 percent) and Soybean Oil (77 percent) come in as the next highest in the weekly strength scores.

On the downside, Lean Hogs (10 percent) and Cocoa (18 percent) come in at the lowest strength levels currently and are in Extreme-Bearish territory (below 20 percent). The next lowest strength scores are the Live Cattle (32 percent) and the Sugar (38 percent).

Strength Statistics:

Corn (61.6 percent) vs Corn previous week (54.1 percent)

Sugar (38.0 percent) vs Sugar previous week (38.4 percent)

Coffee (50.5 percent) vs Coffee previous week (51.1 percent)

Soybeans (82.6 percent) vs Soybeans previous week (71.5 percent)

Soybean Oil (76.7 percent) vs Soybean Oil previous week (73.9 percent)

Soybean Meal (81.4 percent) vs Soybean Meal previous week (70.5 percent)

Live Cattle (31.9 percent) vs Live Cattle previous week (46.5 percent)

Lean Hogs (9.7 percent) vs Lean Hogs previous week (0.0 percent)

Cotton (95.7 percent) vs Cotton previous week (95.9 percent)

Cocoa (17.6 percent) vs Cocoa previous week (11.7 percent)

Wheat (93.4 percent) vs Wheat previous week (85.5 percent)

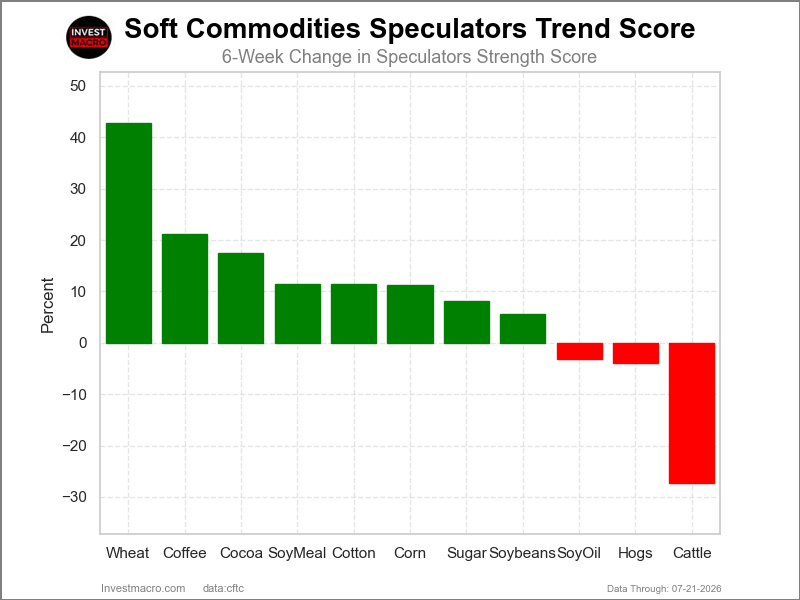

Wheat & Coffee top the 6-Week Strength Trends

COT Strength Score Trends (or move index, calculates the 6-week changes in strength scores) showed that Wheat (43 percent) and Coffee (21 percent) lead the past six weeks trends for soft commodities. Cocoa (18 percent), Corn (11 percent) and Soybean Meal (11 percent) are the next highest positive movers in the latest trends data.

Live Cattle (-27 percent) leads the downside trend scores currently with Lean Hogs (-4 percent) and Soybean Oil (-3 percent) following next with lower trend scores.

Strength Trend Statistics:

Corn (11.3 percent) vs Corn previous week (-9.3 percent)

Sugar (8.1 percent) vs Sugar previous week (9.0 percent)

Coffee (21.2 percent) vs Coffee previous week (14.5 percent)

Soybeans (5.6 percent) vs Soybeans previous week (-13.8 percent)

Soybean Oil (-3.2 percent) vs Soybean Oil previous week (-16.6 percent)

Soybean Meal (11.5 percent) vs Soybean Meal previous week (-28.0 percent)

Live Cattle (-27.2 percent) vs Live Cattle previous week (-15.7 percent)

Lean Hogs (-4.0 percent) vs Lean Hogs previous week (-16.7 percent)

Cotton (11.4 percent) vs Cotton previous week (6.1 percent)

Cocoa (17.5 percent) vs Cocoa previous week (6.0 percent)

Wheat (42.7 percent) vs Wheat previous week (20.5 percent)

Individual Soft Commodities Markets:

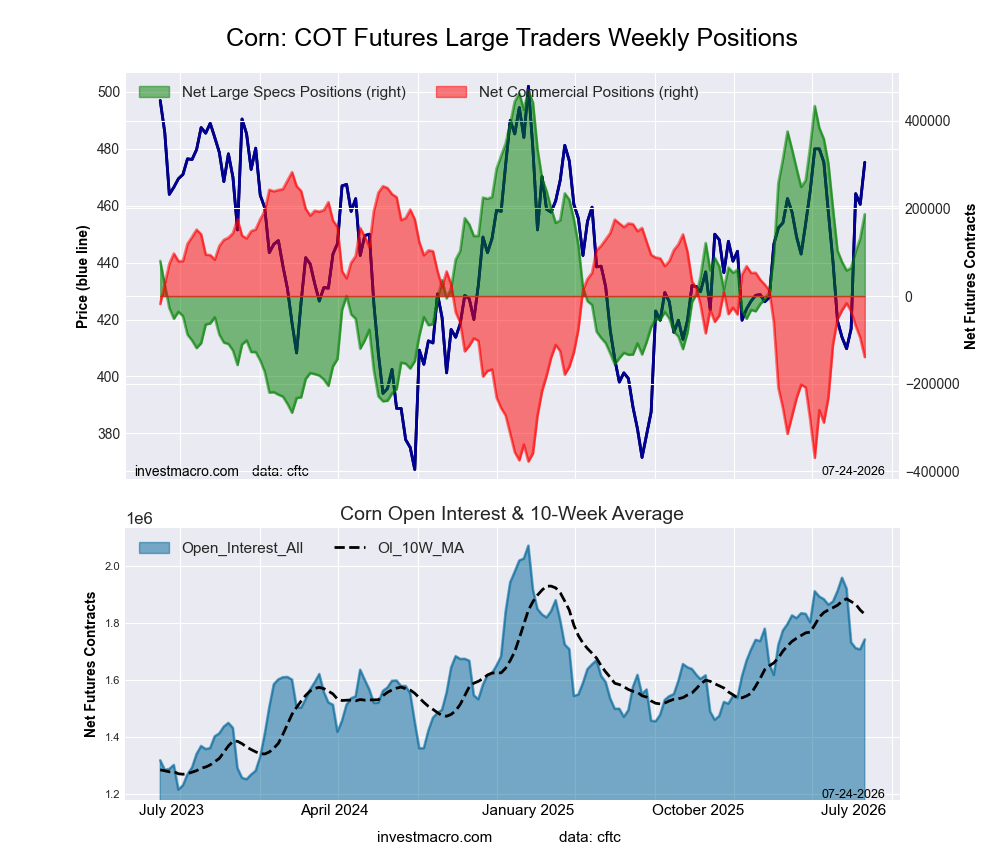

CORN Futures:

Positioning Notes:

Positioning Notes:

- CORN large speculator standing this week reached a net position of 186,650 contracts in the data reported through Tuesday.

- Weekly Speculator position increase of 55,187 contracts from the previous week which had a total of 131,463 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 61.6 percent.

- The Commercials are Bearish with a score of 36.1 percent.

- The Small Traders (not shown in chart) are Bullish with a score of 64.6 percent.

Price Trend-Following Model: Uptrend

Our weekly trend-following model classifies the current market price position as: Uptrend.

| CORN Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 28.3 | 40.8 | 7.8 |

| – Percent of Open Interest Shorts: | 17.5 | 48.8 | 10.5 |

| – Net Position: | 186,650 | -139,254 | -47,396 |

| – Gross Longs: | 492,296 | 710,336 | 135,901 |

| – Gross Shorts: | 305,646 | 849,590 | 183,297 |

| – Long to Short Ratio: | 1.6 to 1 | 0.8 to 1 | 0.7 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 61.6 | 36.1 | 64.6 |

| – Strength Index Reading (3 Year Range): | Bullish | Bearish | Bullish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 11.3 | -13.1 | 2.6 |

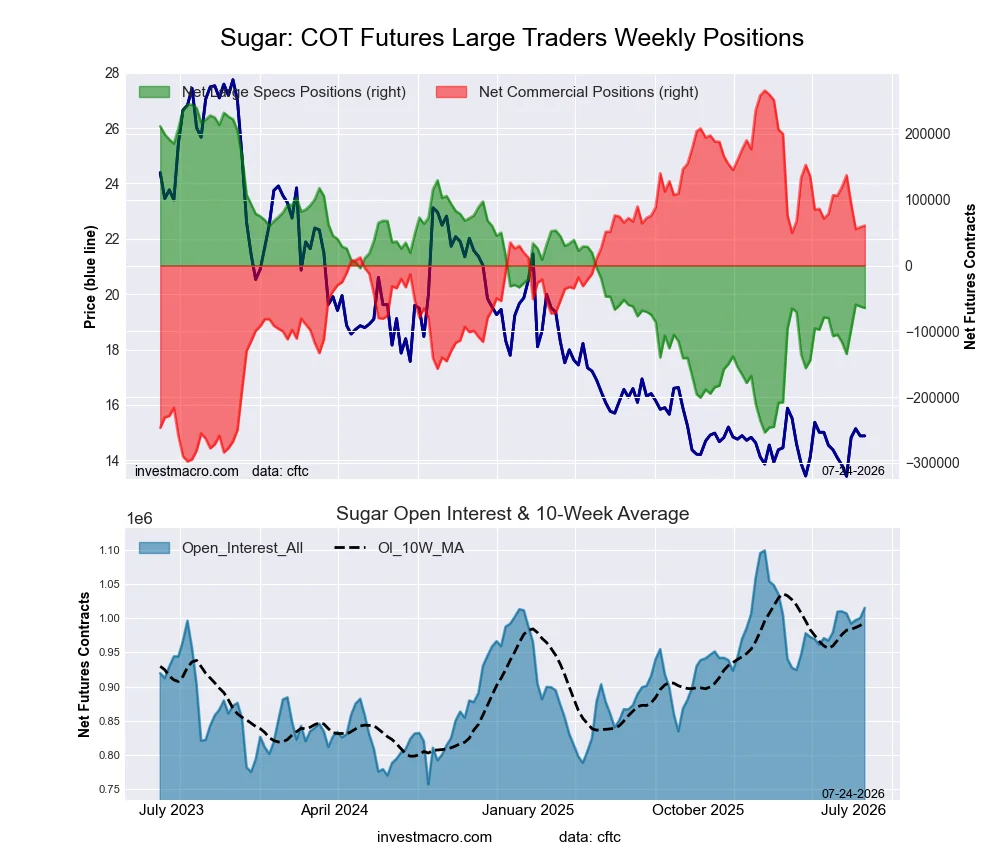

SUGAR Futures:

Positioning Notes:

Positioning Notes:

- SUGAR large speculator standing this week reached a net position of -64,490 contracts in the data reported through Tuesday.

- Weekly Speculator position decrease of -2,345 contracts from the previous week which had a total of -62,145 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 38.0 percent.

- The Commercials are Bullish with a score of 63.6 percent.

- The Small Traders (not shown in chart) are Bearish with a score of 37.0 percent.

Price Trend-Following Model: Weak Downtrend

Our weekly trend-following model classifies the current market price position as: Weak Downtrend.

| SUGAR Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 26.5 | 47.1 | 7.6 |

| – Percent of Open Interest Shorts: | 32.8 | 41.1 | 7.2 |

| – Net Position: | -64,490 | 60,615 | 3,875 |

| – Gross Longs: | 268,757 | 478,396 | 77,257 |

| – Gross Shorts: | 333,247 | 417,781 | 73,382 |

| – Long to Short Ratio: | 0.8 to 1 | 1.1 to 1 | 1.1 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 38.0 | 63.6 | 37.0 |

| – Strength Index Reading (3 Year Range): | Bearish | Bullish | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 8.1 | -8.1 | 6.5 |

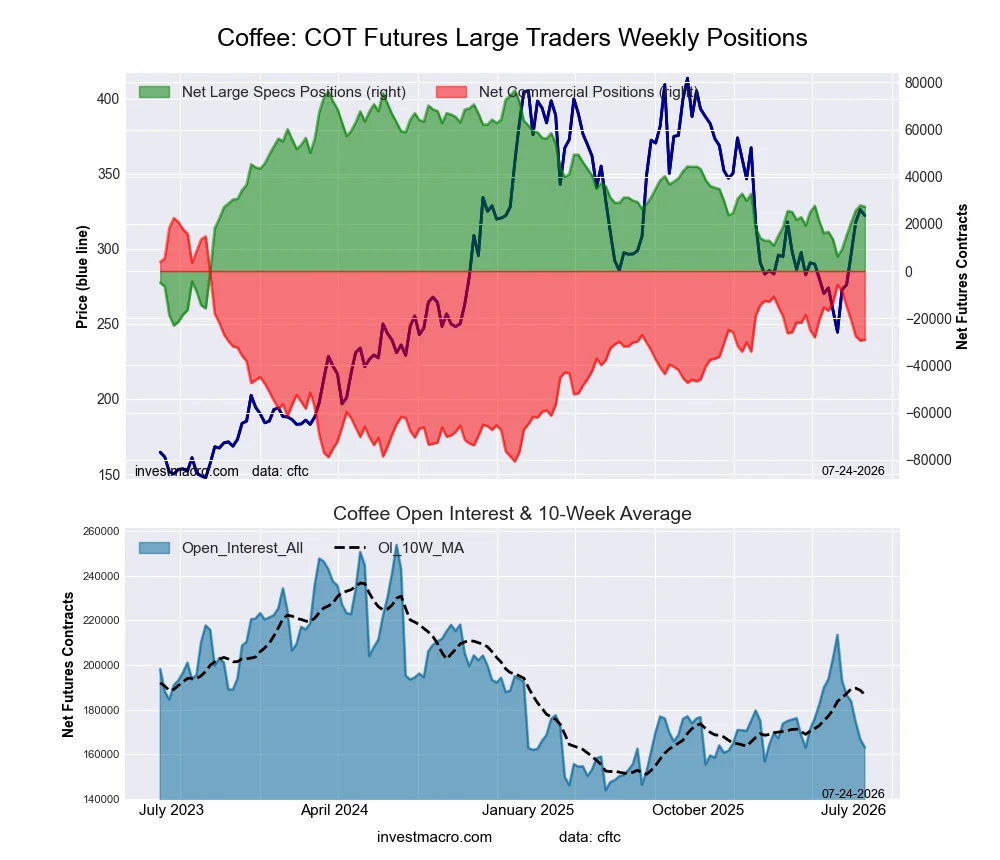

COFFEE Futures:

Positioning Notes:

Positioning Notes:

- COFFEE large speculator standing this week reached a net position of 27,255 contracts in the data reported through Tuesday.

- Weekly Speculator position decline of -572 contracts from the previous week which had a total of 27,827 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 50.5 percent.

- The Commercials are Bullish with a score of 50.0 percent.

- The Small Traders (not shown in chart) are Bearish with a score of 47.4 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| COFFEE Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 32.1 | 37.7 | 4.5 |

| – Percent of Open Interest Shorts: | 15.4 | 55.6 | 3.4 |

| – Net Position: | 27,255 | -29,089 | 1,834 |

| – Gross Longs: | 52,395 | 61,550 | 7,362 |

| – Gross Shorts: | 25,140 | 90,639 | 5,528 |

| – Long to Short Ratio: | 2.1 to 1 | 0.7 to 1 | 1.3 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 50.5 | 50.0 | 47.4 |

| – Strength Index Reading (3 Year Range): | Bullish | Bullish | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 21.2 | -22.6 | 38.8 |

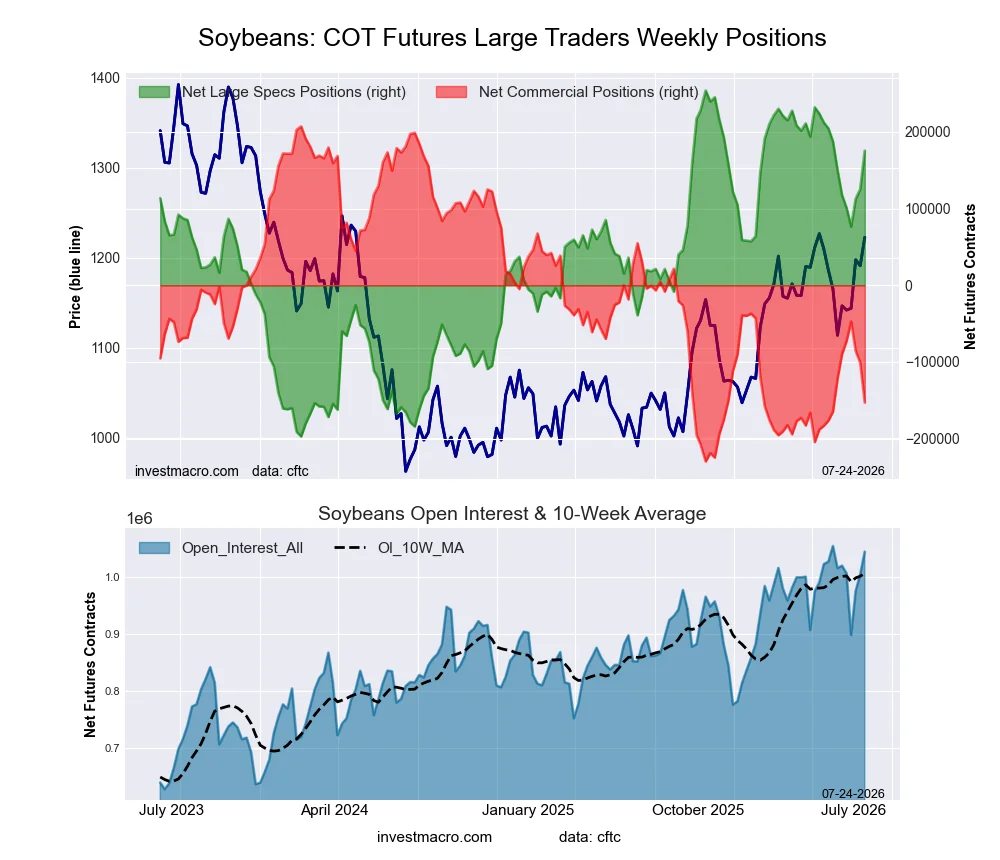

SOYBEANS Futures:

Positioning Notes:

Positioning Notes:

- SOYBEANS large speculator standing this week reached a net position of 175,646 contracts in the data reported through Tuesday.

- Weekly Speculator position boost of 50,243 contracts from the previous week which had a total of 125,403 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 82.6 percent.

- The Commercials are Bearish-Extreme with a score of 17.6 percent.

- The Small Traders (not shown in chart) are Bearish with a score of 42.5 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| SOYBEANS Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 24.4 | 46.7 | 4.6 |

| – Percent of Open Interest Shorts: | 7.6 | 61.4 | 6.8 |

| – Net Position: | 175,646 | -152,981 | -22,665 |

| – Gross Longs: | 255,148 | 488,307 | 48,547 |

| – Gross Shorts: | 79,502 | 641,288 | 71,212 |

| – Long to Short Ratio: | 3.2 to 1 | 0.8 to 1 | 0.7 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 82.6 | 17.6 | 42.5 |

| – Strength Index Reading (3 Year Range): | Bullish-Extreme | Bearish-Extreme | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 5.6 | -7.1 | 18.2 |

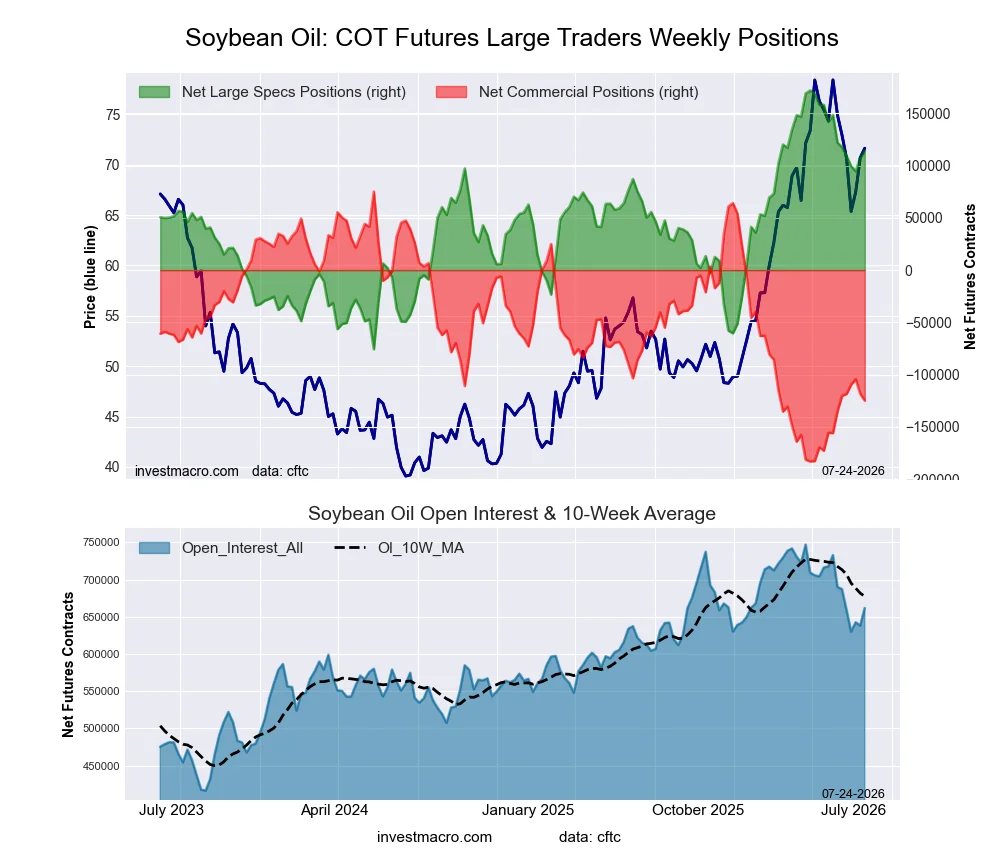

SOYBEAN OIL Futures:

Positioning Notes:

Positioning Notes:

- SOYBEAN OIL large speculator standing this week reached a net position of 114,142 contracts in the data reported through Tuesday.

- Weekly Speculator position uptick of 6,899 contracts from the previous week which had a total of 107,243 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 76.7 percent.

- The Commercials are Bearish with a score of 22.6 percent.

- The Small Traders (not shown in chart) are Bullish with a score of 71.8 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| SOYBEAN OIL Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 25.8 | 46.8 | 5.7 |

| – Percent of Open Interest Shorts: | 8.5 | 65.7 | 4.0 |

| – Net Position: | 114,142 | -124,875 | 10,733 |

| – Gross Longs: | 170,407 | 309,756 | 37,450 |

| – Gross Shorts: | 56,265 | 434,631 | 26,717 |

| – Long to Short Ratio: | 3.0 to 1 | 0.7 to 1 | 1.4 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 76.7 | 22.6 | 71.8 |

| – Strength Index Reading (3 Year Range): | Bullish | Bearish | Bullish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -3.2 | 4.0 | -12.0 |

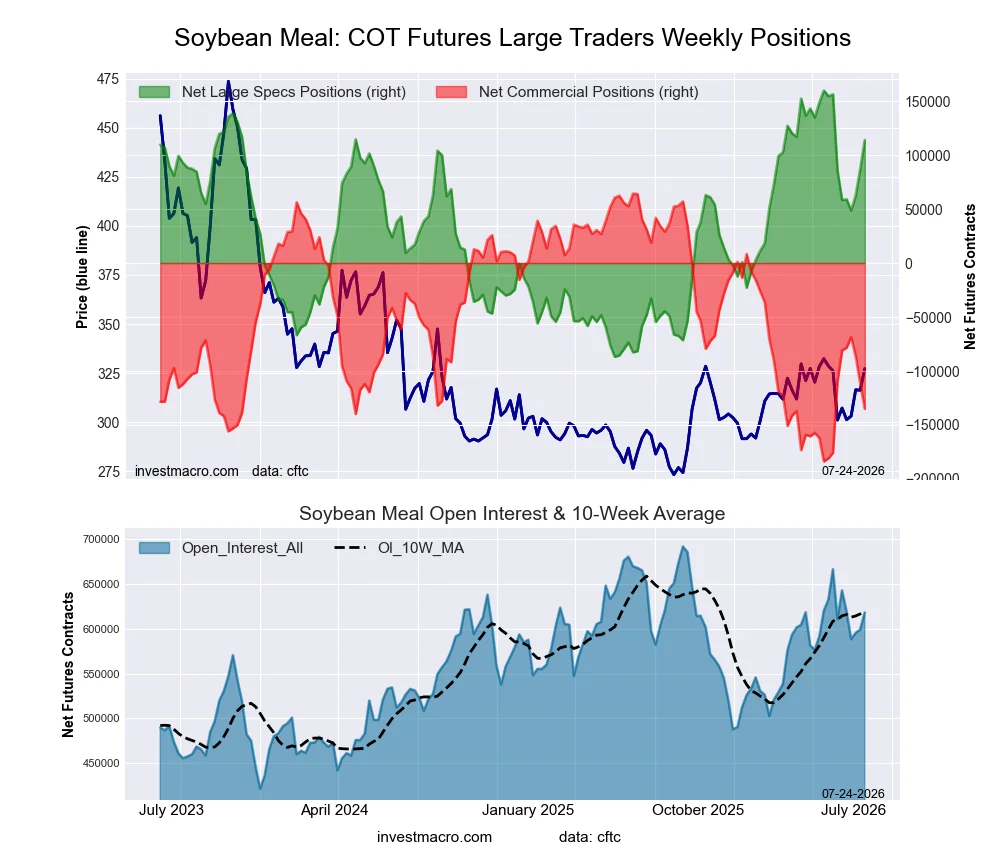

SOYBEAN MEAL Futures:

Positioning Notes:

Positioning Notes:

- SOYBEAN MEAL large speculator standing this week reached a net position of 113,860 contracts in the data reported through Tuesday.

- Weekly Speculator position rise of 26,823 contracts from the previous week which had a total of 87,037 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 81.4 percent.

- The Commercials are Bearish-Extreme with a score of 19.7 percent.

- The Small Traders (not shown in chart) are Bullish with a score of 60.7 percent.

Price Trend-Following Model: Weak Downtrend

Our weekly trend-following model classifies the current market price position as: Weak Downtrend.

| SOYBEAN MEAL Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 29.6 | 41.5 | 8.0 |

| – Percent of Open Interest Shorts: | 11.2 | 63.4 | 4.6 |

| – Net Position: | 113,860 | -135,003 | 21,143 |

| – Gross Longs: | 182,923 | 256,752 | 49,534 |

| – Gross Shorts: | 69,063 | 391,755 | 28,391 |

| – Long to Short Ratio: | 2.6 to 1 | 0.7 to 1 | 1.7 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 81.4 | 19.7 | 60.7 |

| – Strength Index Reading (3 Year Range): | Bullish-Extreme | Bearish-Extreme | Bullish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 11.5 | -10.2 | -17.4 |

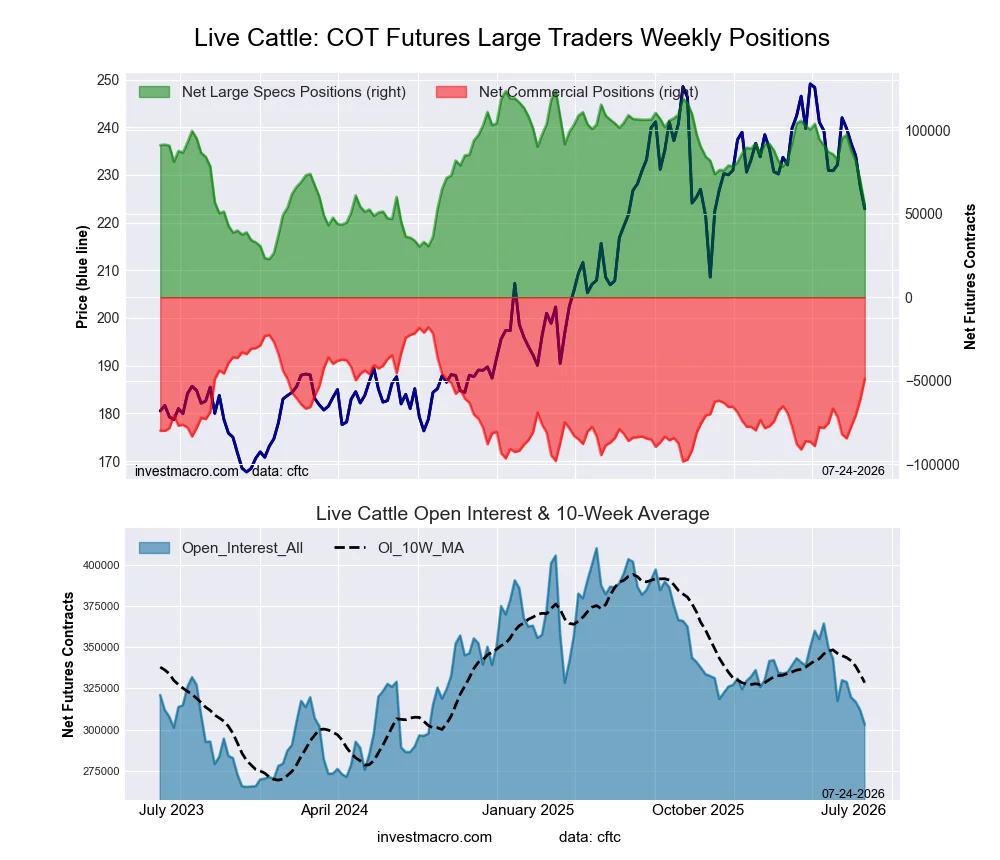

LIVE CATTLE Futures:

Positioning Notes:

Positioning Notes:

- LIVE CATTLE large speculator standing this week reached a net position of 55,014 contracts in the data reported through Tuesday.

- Weekly Speculator position decline of -14,691 contracts from the previous week which had a total of 69,705 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 31.9 percent.

- The Commercials are Bullish with a score of 61.5 percent.

- The Small Traders (not shown in chart) are Bullish with a score of 77.0 percent.

Price Trend-Following Model: Strong Downtrend

Our weekly trend-following model classifies the current market price position as: Strong Downtrend.

| LIVE CATTLE Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 34.0 | 36.4 | 9.4 |

| – Percent of Open Interest Shorts: | 15.9 | 52.6 | 11.4 |

| – Net Position: | 55,014 | -48,925 | -6,089 |

| – Gross Longs: | 103,155 | 110,398 | 28,352 |

| – Gross Shorts: | 48,141 | 159,323 | 34,441 |

| – Long to Short Ratio: | 2.1 to 1 | 0.7 to 1 | 0.8 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 31.9 | 61.5 | 77.0 |

| – Strength Index Reading (3 Year Range): | Bearish | Bullish | Bullish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -27.2 | 28.3 | 16.8 |

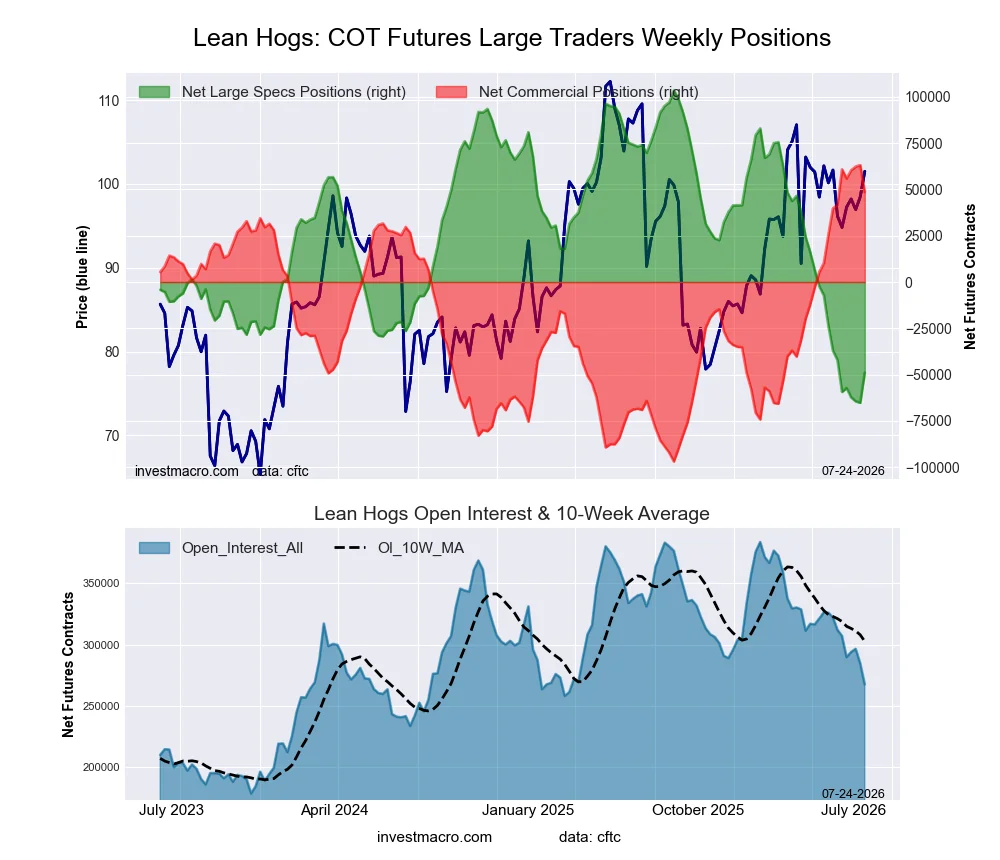

LEAN HOGS Futures:

Positioning Notes:

Positioning Notes:

- LEAN HOGS large speculator standing this week reached a net position of -48,802 contracts in the data reported through Tuesday.

- Weekly Speculator position uptick of 16,426 contracts from the previous week which had a total of -65,228 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 9.7 percent.

- The Commercials are Bullish-Extreme with a score of 90.8 percent.

- The Small Traders (not shown in chart) are Bullish-Extreme with a score of 87.7 percent.

Price Trend-Following Model: Strong Downtrend

Our weekly trend-following model classifies the current market price position as: Strong Downtrend.

| LEAN HOGS Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 24.1 | 41.9 | 7.6 |

| – Percent of Open Interest Shorts: | 42.3 | 23.8 | 7.5 |

| – Net Position: | -48,802 | 48,492 | 310 |

| – Gross Longs: | 64,456 | 112,104 | 20,434 |

| – Gross Shorts: | 113,258 | 63,612 | 20,124 |

| – Long to Short Ratio: | 0.6 to 1 | 1.8 to 1 | 1.0 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 9.7 | 90.8 | 87.7 |

| – Strength Index Reading (3 Year Range): | Bearish-Extreme | Bullish-Extreme | Bullish-Extreme |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -4.0 | 4.3 | -0.8 |

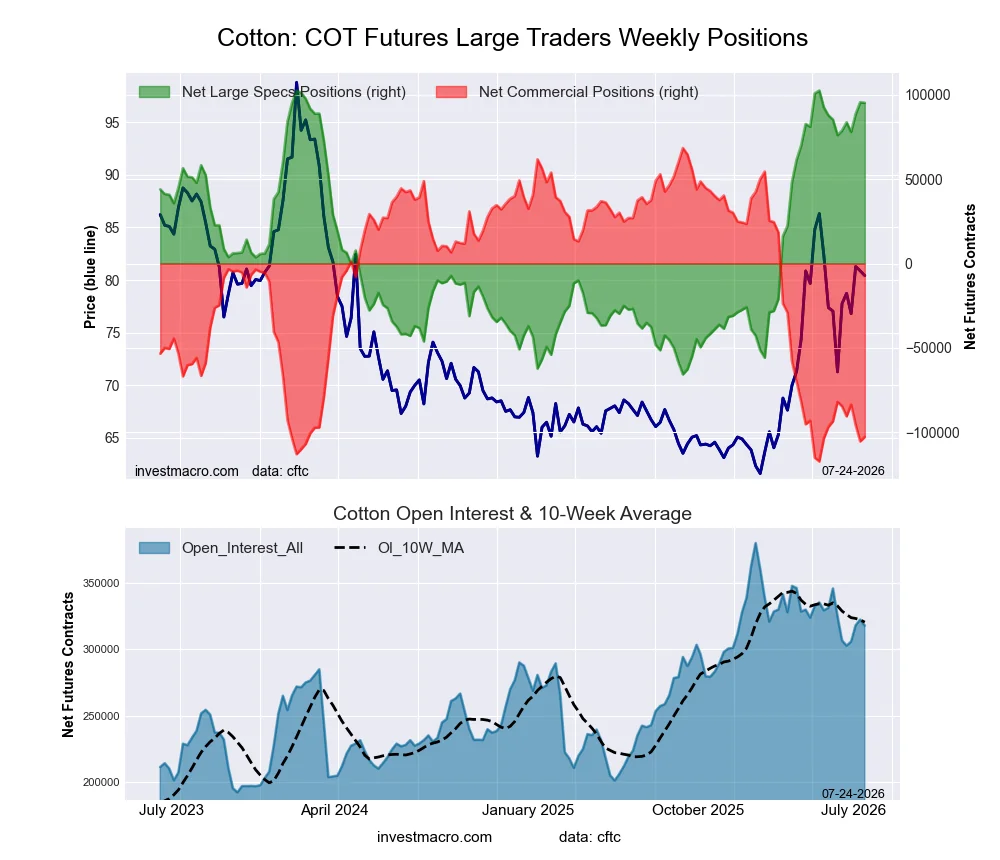

COTTON Futures:

Positioning Notes:

Positioning Notes:

- COTTON large speculator standing this week reached a net position of 95,112 contracts in the data reported through Tuesday.

- Weekly Speculator position lowering of -335 contracts from the previous week which had a total of 95,447 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 95.7 percent.

- The Commercials are Bearish-Extreme with a score of 7.8 percent.

- The Small Traders (not shown in chart) are Bullish with a score of 59.6 percent.

Price Trend-Following Model: Uptrend

Our weekly trend-following model classifies the current market price position as: Uptrend.

| COTTON Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 42.6 | 35.6 | 4.9 |

| – Percent of Open Interest Shorts: | 12.7 | 67.9 | 2.5 |

| – Net Position: | 95,112 | -102,678 | 7,566 |

| – Gross Longs: | 135,353 | 113,037 | 15,433 |

| – Gross Shorts: | 40,241 | 215,715 | 7,867 |

| – Long to Short Ratio: | 3.4 to 1 | 0.5 to 1 | 2.0 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 95.7 | 7.8 | 59.6 |

| – Strength Index Reading (3 Year Range): | Bullish-Extreme | Bearish-Extreme | Bullish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 11.4 | -11.2 | 9.0 |

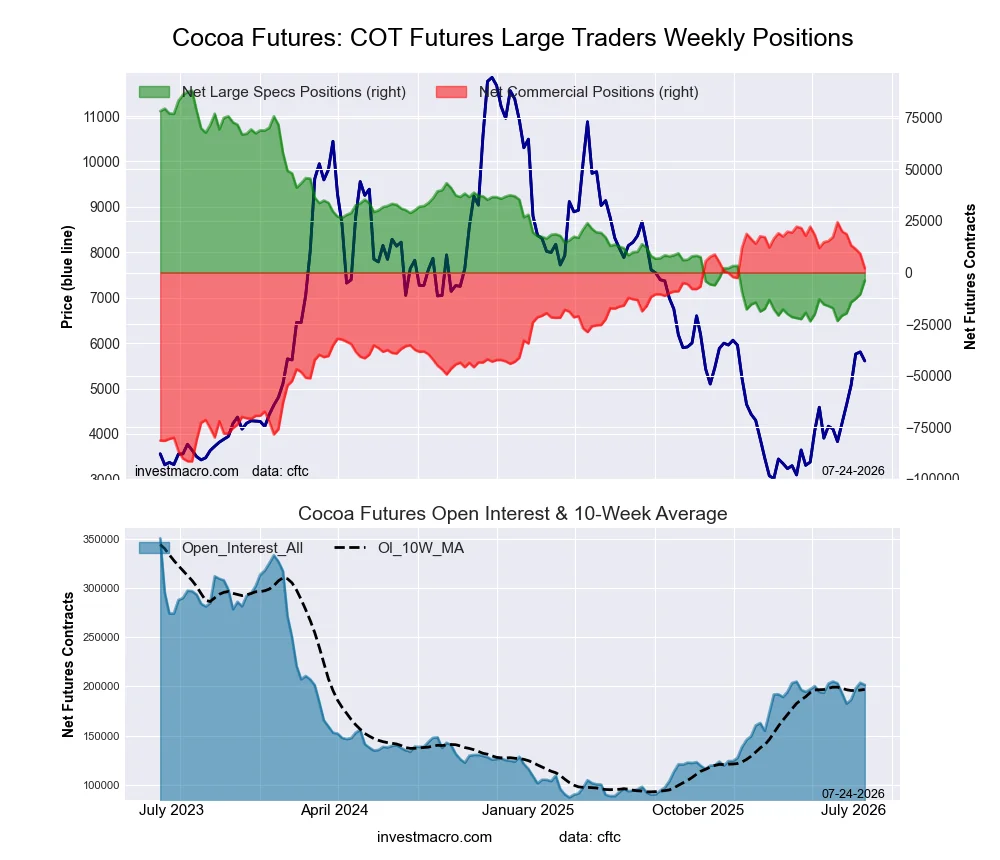

COCOA Futures:

Positioning Notes:

Positioning Notes:

- COCOA large speculator standing this week reached a net position of -3,907 contracts in the data reported through Tuesday.

- Weekly Speculator position boost of 6,677 contracts from the previous week which had a total of -10,584 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 17.6 percent.

- The Commercials are Bullish-Extreme with a score of 80.8 percent.

- The Small Traders (not shown in chart) are Bearish with a score of 43.9 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| COCOA Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 17.5 | 49.5 | 5.0 |

| – Percent of Open Interest Shorts: | 19.5 | 48.5 | 4.2 |

| – Net Position: | -3,907 | 2,157 | 1,750 |

| – Gross Longs: | 35,311 | 99,839 | 10,125 |

| – Gross Shorts: | 39,218 | 97,682 | 8,375 |

| – Long to Short Ratio: | 0.9 to 1 | 1.0 to 1 | 1.2 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 17.6 | 80.8 | 43.9 |

| – Strength Index Reading (3 Year Range): | Bearish-Extreme | Bullish-Extreme | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 17.5 | -19.2 | 25.5 |

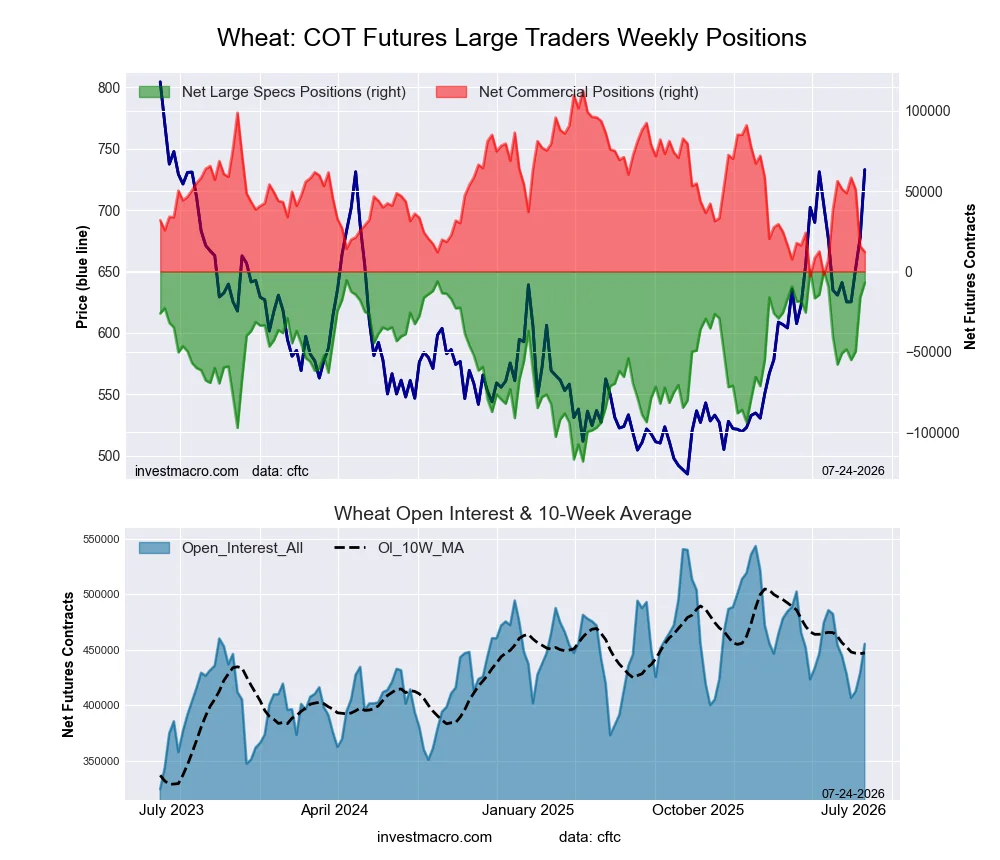

WHEAT Futures:

Positioning Notes:

Positioning Notes:

- WHEAT large speculator standing this week reached a net position of -7,009 contracts in the data reported through Tuesday.

- Weekly Speculator position uptick of 9,330 contracts from the previous week which had a total of -16,339 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 93.4 percent.

- The Commercials are Bearish-Extreme with a score of 13.2 percent.

- The Small Traders (not shown in chart) are Bearish with a score of 23.1 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| WHEAT Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 24.1 | 38.6 | 7.3 |

| – Percent of Open Interest Shorts: | 25.6 | 35.9 | 8.4 |

| – Net Position: | -7,009 | 12,187 | -5,178 |

| – Gross Longs: | 109,575 | 175,701 | 33,254 |

| – Gross Shorts: | 116,584 | 163,514 | 38,432 |

| – Long to Short Ratio: | 0.9 to 1 | 1.1 to 1 | 0.9 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 93.4 | 13.2 | 23.1 |

| – Strength Index Reading (3 Year Range): | Bullish-Extreme | Bearish-Extreme | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 42.7 | -38.1 | -39.2 |

Article By InvestMacro – Receive our weekly COT Reports by Email

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators) as well as their open interest (contracts open in the market at time of reporting).See CFTC criteria here.

All information and opinions on this website and contained in this article are for general informational purposes only and do not constitute investment advice.