Are you ready for yet another jumbo-sized Fed rate hike?

Markets have been preparing for such an outcome at the upcoming FOMC policy decision, which will star in next week’s economic calendar

Monday, July 25

EUR: Germany July IFO business climate

GBP: UK PM candidates’ debate – Rishi Sunak vs. Liz Truss

Tuesday, July 26

JPY: Bank of Japan June meeting minutes

USD: US July consumer confidence

IMF releases updated world economic outlook

Alphabet 2Q earnings

Wednesday, July 27

AUD: Australia Q2 CPI

CNH: China June industrial profits

USD: Fed rate decision

US crude: EIA weekly oil inventory report

Meta Platforms 2Q earnings

Thursday, July 28

AUD: Australia June retail sales

EUR: Germany July CPI, Eurozone July economic and consumer confidence

USD: US Q2 GDP, weekly jobless claims

Amazon 2Q earnings

Apple 2Q earnings

Friday, July 29

JPY: Japan June unemployment, retail sales, industrial production; July Tokyo CPI

EUR: Eurozone July CPI, Q2 GDP

USD: US June personal income and spending, PCE core deflator, July consumer sentiment

Exxon 2Q earnings

Chevron 2Q earnings

Markets have fully priced in a second consecutive 75-basis point hike at next week’s FOMC policy meeting, as the US central bank continues its battle against the hottest inflation in 40 years.

However, that 75bps hike is a relative step down from the 100-basis point hike that some segments of the markets were expecting. Hence the recent unwinding of gains in the equally-weighted USD index. Still, this instrument is well within its uptrend since Q1 2022.

Note that this index compares the US dollar’s performance against six of its major peers, all in equal weights:

Euro

British Pound

Swiss Franc

Australian Dollar

New Zealand Dollar

Canadian Dollar

Any other outcome that deviates from the 75bps script would be a surprise.

DOVISH: A “mere” 50bps hike, though still twice the size of the traditional 25bps rate adjustments per meeting deployed by central bankers worldwide, should prompt more declines in the USD index, potentially moving it closer to its 50-day simple moving average (SMA) around the 1.175 region.

HAWKISH: Although the bar has been set high for a hawkish outcome at next week’s meeting, a 100bps shocker would reinvigorate dollar bulls into sending this USD index back above the 1.20 line. More dollar gains may also ensue if Fed Chair Jerome Powell, during his press conference, refuses to rule out a 100bps hike at upcoming meetings.

Ultimately, policymakers at the US central bank, as well as market participants, will continue to be guided by the inflation data.

And on that point, after the FOMC meeting concludes, next Friday’s release of the June PCE deflator will be closely watched, considering that it’s the Fed’s preferred way of measuring inflation.

The PCE deflator is forecasted to come in at 6.6% in June, which would mean that it has posted a reading of 6% or higher for every month so far this year. 6.6% is also more than three times the Fed’s 2% target, underscoring the tremendous task that the Fed is up against.

Further evidence of stubbornly elevated price pressures is set to force the Fed into triggering even more jumbo-sized rate hikes over the coming months. Such hawkish expectations could then see the USD index being restored to the last cycle high at 1.21859, or perhaps even higher.

Overall, as long as the Fed keeps the “pedal to the metal” while leaving other major central banks struggling to catch up with their own rate hikes, that should leave the buck with an easier path to climb even higher.

The US stock indices increased yesterday on the technology sector’s growth, as better-than-expected Tesla earnings supported the sector. The Dow Jones (US30) added 0.51% at the close, while the S&P 500 (US500) increased by 0.99%. The Technology Index NASDAQ (US100) jumped by 1.36%.

Shares of Tesla Inc (TSLA) jumped by 9.7% yesterday, giving confidence to the entire industry and the sector. Shares of Snap Inc (SNAP) fell by 24% in over-the-counter trading Thursday as the company said third-quarter revenue growth was flat and its results were affected by Apple’s privacy changes. Shares of American Airlines (AAL) fell by 7% on the report, even as the company projected third-quarter earnings thanks to increased demand for travel services.

Biden tested positive for coronavirus. The US president has moderate symptoms and is working remotely.

Stock markets in Europe traded flat Thursday. German DAX (DE30) decreased by 0.27% yesterday, French CAC 40 (FR40) added 0.27%, Spanish IBEX 35 (ES35) lost 0.20%, British FTSE 100 (UK100) was up by 0.09%.

The European Central Bank unexpectedly raised its interest rate by 0.5%, even though Christine Lagarde had promised the first increase of 0.25%. The ECB report indicates that the decision is based on an updated assessment of inflation risks, as rising prices are a growing concern for households and companies. The future trajectory of interest rates will depend on the new data. ECB policymakers also agreed to provide additional assistance to the currency bloc’s 19 heavily indebted countries, including Italy, with a new bond-buying scheme designed to limit their rising borrowing costs and thus limit financial fragmentation.

Investors are also closely watching the political situation in Italy, as Prime Minister Mario Draghi resigned on Thursday, and the president accepted his resignation, followed by the dissolution of parliament.

The Nord Stream 1 pipeline reopened after a 10-day hiatus. Germany’s grid regulator has indicated that they are back to a capacity level of 40%. With the resumption of gas flows through Nord Stream, investors are more conciliatory on the part of Russia to continue supplying oil and petroleum products to Europe in the coming weeks or months.

Oil prices have fallen below $100 after a massive inventory build-up in the United States. But demand remains strong in mid-summer, so with production levels lagging, traders should not expect a significant drop in prices.

Asian markets mostly rose yesterday. Japan’s Nikkei 225 (JP225) gained 2.67%, Hong Kong’s Hang Seng (HK50) added 1.11%, and Australia’s S&P/ASX 200 (AU200) closed by 1.65% higher.

Japan’s key inflation indicator was even higher than the Bank of Japan’s target of 2%. According to data released on Friday by the Ministry of the Interior, core consumer prices (excluding food and fuel prices) reached an annualized rate of 2.2%. The result was in line with economists’ estimates. Despite the continued rise in prices, the Bank of Japan is unlikely to budge anytime soon, as the Bank of Japan remains unconvinced that inflation in the country is sustainable. The BoJ Governor Kuroda has repeatedly said that current cost inflation is unsustainable and that the central bank needs constant easing until it is demand-driven and accompanied by sustained wage growth. But wage growth has not kept pace with inflation, with May data showing that real wages are down 1.8% from a year ago.

In Australia, a NAB report showed that the RBA would raise rates to 2.85% by the end of the year. Since the monetary rate is still well below “neutral,” this indicates continued rapid normalization in the coming months. This means a 50 bp interest rate hike at each of the next two meetings and then a pause to assess the impact of the rate hike.

S&P 500 (F) (US500) 3,998.95 +39.05 (+0.99%)

Dow Jones (US30) 32,036.90 +162.06 (+0.51%)

DAX (DE40) 13,246.64 −35.34 (−0.27%)

FTSE 100 (UK100) 7,270.51 +6.20 (+0.085%)

USD Index 106.77 −0.31 (−0.29%)

Important events for today:

– Australia Manufacturing PMI (m/m) at 02:00 (GMT+3);

– Japan National Core Consumer Price Index at 02:30 (GMT+3);

– UK Retail Sales (m/m) at 09:00 (GMT+3);

– Eurozone France Manufacturing PMI (m/m) at 10:15 (GMT+3);

– Eurozone France Services PMI (m/m) at 10:15 (GMT+3);

– Eurozone German Manufacturing PMI (m/m) at 10:30 (GMT+3);

– Eurozone German Services PMI (m/m) at 10:30 (GMT+3);

– Eurozone Manufacturing PMI (m/m) at 11:00 (GMT+3);

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

But understanding the hidden structures of key elements of social networks, such as subgroups, has remained elusive. My colleagues and I have found two complex patterns in these networks that can help researchers better understand the hierarchies and dynamics of these elements. We found a way to detect powerful “inner circles” in large organizations simply by studying networks that map emails being sent among employees.

We demonstrated the utility of our methods by applying them to the famous Enron network. Enron was an energy trading company that perpetrated fraud on a massive scale. Our study further showed that the method can potentially be used to detect people who wield enormous soft power in an organization regardless of their official title or position. This could be useful for historical, sociological and economic research, as well as government, legal and media investigations.

From pencil and paper to artificial intelligence

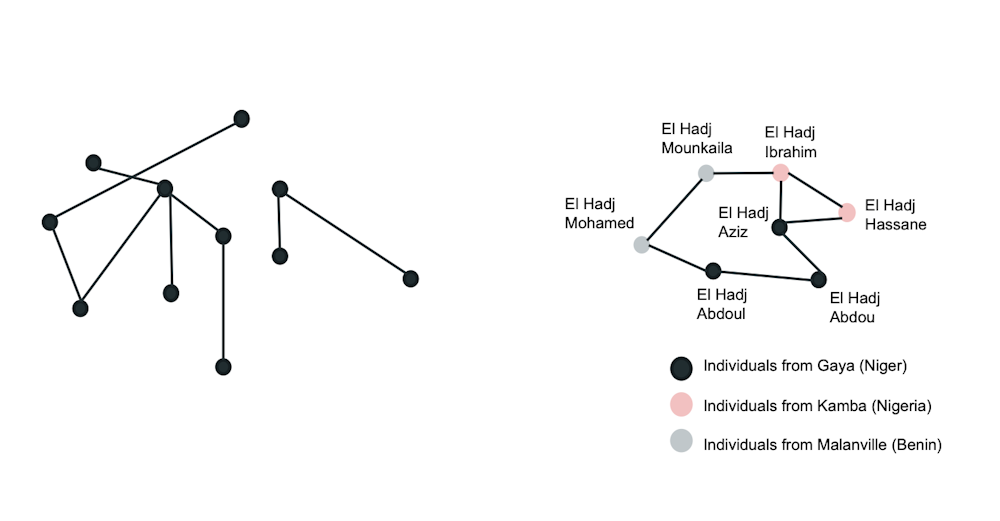

Sociologists have been constructing and studying smaller social networks in careful field experiments for at least 80 years, well before the advent of the internet and online social networks. The concept is so simple that it can be drawn on paper: Entities of interest – people, businesses, countries – are nodes represented as points, and relationships between pairs of nodes are links represented as lines drawn between the points.

An abstract network, at left, shows lines between points representing relationships. The network on the right shows a small fragment of a real-world network of West African traders, based on data from Oliver J. Walther. https://doi.org/10.1080/00220388.2015.1010152. Mayank Kejriwal, CC BY-ND

Using network science to study human societies and other complex systems took on new meaning in the late 1990s when researchers discovered some universal properties of networks. Some of these universal properties have since entered mainstream pop culture. One concept is the Six Degrees of Kevin Bacon, based on the famous empirical finding that any two people on Earth are six or fewer links apart. Similarly, versions of statements such as “the rich get richer” and “winner takes all” have also been replicated in some networks.

These global properties, meaning ones applying to the entire network, seemingly emerge from the myopic and local actions of independent nodes. When I connect with someone on LinkedIn, I am certainly not thinking of the global consequences of my connection on the LinkedIn network. Yet my actions, along with those of many others, eventually lead to predictable, rather than random, outcomes about how the network will evolve.

Along with studying emergent properties like the Six Degrees of Kevin Bacon, researchers have also used network science to focus on problems such as community detection. Stated simply, can a set of rules, otherwise known as an algorithm, automatically discover groups or communities within a collection of people?

Today there are hundreds, if not thousands, of community detection algorithms, some relying on advanced AI methods. They are used for many purposes, including finding communities of interest and uncovering malicious groups on social media. Such algorithms encode intuitive assumptions, such as the expectation that nodes belonging to the same group are more densely connected to one another than nodes belonging to different groups.

Although an exciting line of work, community detection does not study the internal structure of communities. Should communities be thought of only as collections of nodes in networks? And what about communities that are small but particularly influential, such as inner circles and in-crowds?

Two hypothetical structures for influential groups

In a manner of speaking, you likely already have some inkling of the structure of very small groups in social networks. The truth of the adage that “a friend of my friend is also my friend” can be tested statistically in friendship networks by counting the number of triangles in the network and determining whether this number is higher than chance alone could explain. And indeed, many social network studies have been used to verify the claim.

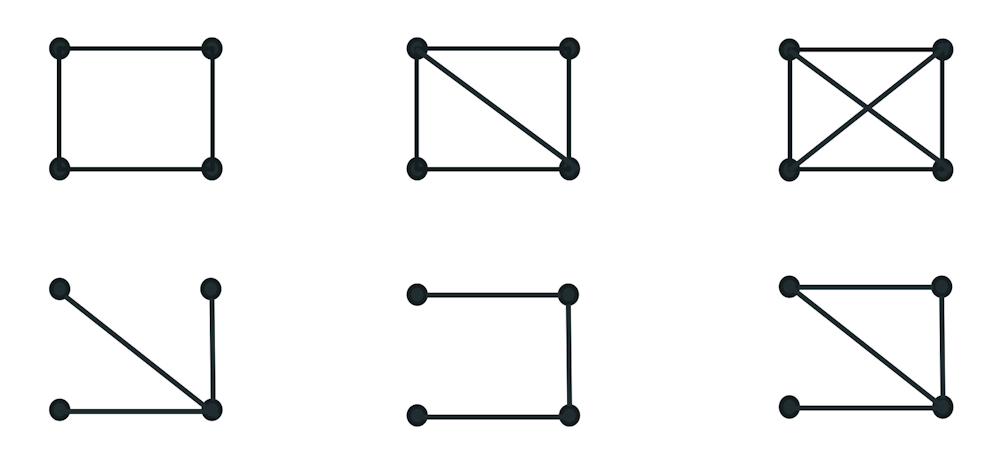

Unfortunately, the concept starts breaking down when extended to groups with more than three members. Although motifs have been well studied in both algorithmic computer science and biology, they have not been reliably linked to influential groups in real communication networks.

Six examples of motifs with four nodes. Mayank Kejriwal, CC BY-ND

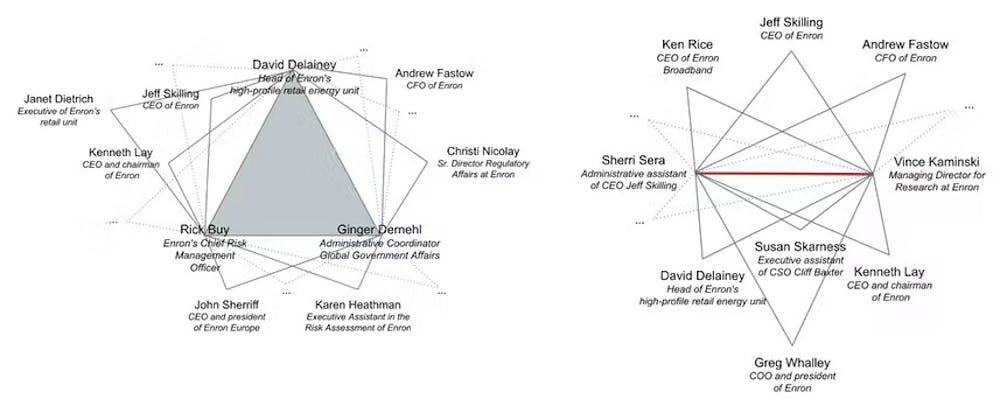

The first structure extends the triangle, not by adding more nodes, but by directly adding triangles. Specifically, there is a central triangle that is flanked by other peripheral triangles. Importantly, the third person in any peripheral triangle must not be linked to the third person on the central triangle, thereby excluding them from the true inner circle of influence.

The second structure is similar but assumes that there is no central triangle, and the inner circle is just a pair of nodes. A real-life example might be two co-founders of a startup like Sergey Brin and Larry Page of Google, or a power couple with joint interests, common in global politics, like Bill and Hillary Clinton.

Understanding influential groups in an infamous network

We tested our hypothesis on the Enron email network, which is well studied in network science, with nodes representing email addresses and links representing communication among those addresses. Despite being elaborate, not only were our proposed structures present in the network in greater numbers than chance alone would predict, but a qualitative analysis showed that there is merit to the claim that they represent influential groups.

Examples of the two structures found in the Enron network. More such structures are present in the network and cannot be explained by chance alone. Mayank Kejriwal, CC BY-ND

The main characters in the Enron saga are welldocumented by now. Intriguingly, some of these characters do not seem to have had much official influence but may have wielded significant soft power. An example is Sherri Reinartz-Sera, who was the longtime administrative assistant of Jeffrey K. Skilling, the former chief executive of Enron. Unlike Skilling, Sera was only mentioned in a New York Times article following investigative reporting that took place during the course of the scandal. However, our algorithm discovered an influential group with Sera occupying a central position.

Dissecting power dynamics

Society has intricate structures at the levels of individuals, friendships and communities. In-crowds are not just ragtag groups of characters talking to one another, or a single ringleader calling all the shots. Many in-crowds, or influential groups, have a sophisticated structure.

While much still remains to be discovered about such groups and their influence, network science can help uncover their complexity.

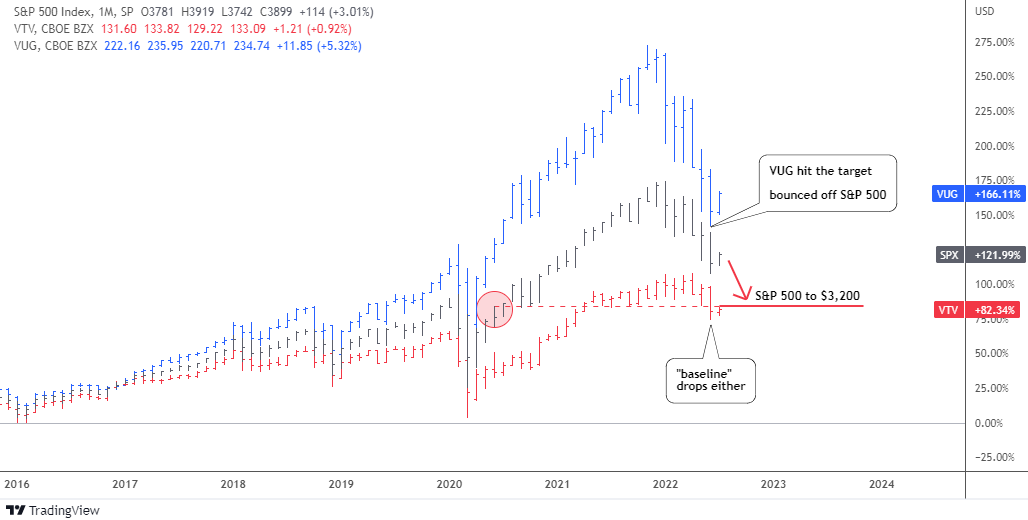

The index price was at $4,459 that time. The deepest valley since then was established at $3,637 last month. 18% of the index value evaporated since the idea had been posted and 25% from the top of this January ($4,819).

The majority of you voted for 10%-20% retracement and this was the closest call so far as we cannot be sure whether it is over or not.

To remind you, I had put together two ETFs and the S&P 500 index (black). I chose Vanguard Value Index Fund ETF (VTV) (red) and Vanguard Growth Index Fund ETF (VUG) (blue). Let us check the updated comparison chart below.

Source: TradingView

The bearish alert appeared to me when the value stocks (VTV, red) stopped contributing to the rise of the broad index. Moreover, the gap between the latter and the growth stocks (VUG, blue) has widened tremendously.

The retracement targets for VUG and the S&P 500 were based on the corresponding level of underlying / less performing instrument: for VUG it was the S&P 500 and for the S&P 500 – VTV.

It is amazing how accurately the VUG target at $217 was hit last month as the ETF dropped even lower in the valley of $213. The concept played out precisely as the VUG bounced off the broad index, blue bars approached but did not overlap black bars.

The S&P 500 index almost closed the gap with the VTV last month, however the VTV itself also dropped and hence wasn’t caught up. The retracement target has been set at $3,200 last September and the lowest level has been seen since then was $3,637 last month.

Let us look at the S&P 500 chart below to see what could happen next.

Source: TradingView

The price has shaped a familiar model of the Falling Wedge (purple) within the current retracement. The amplitude of fluctuations decreases as the price approached the apex of the pattern.

The RSI indicator has already built the invisible Bullish Divergence as it can be seen only through its readings: 30.2 vs. 30.5, which means higher valley versus the lower bottom in the price chart.

This combination of narrowing trendlines and bullish diverging indicator could result in the possible breakup anytime soon. Would it be a reversal or a dead cat bounce?

I added two paths on the chart. The red zigzag shows how the Falling Wedge would play out in the first place. The target (purple flat line) is located at the widest part of the pattern added to the breakup point. It coincides with the 61.8% Fibonacci retracement level at $4,367. It could be a double resistance.

The following drop should complete the complex correction down to $3,185. This target was calculated by subtracting the size of the Falling Wedge from the target of that pattern. And again, this area corresponds amazingly with the 61.8% Fibonacci retracement level and the first chart target based on a comparison with VTV.

The green path implies the sideways consolidation that should keep within the existing range of $3,637-$4,819.

Disclosure: This contributor has no positions in any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

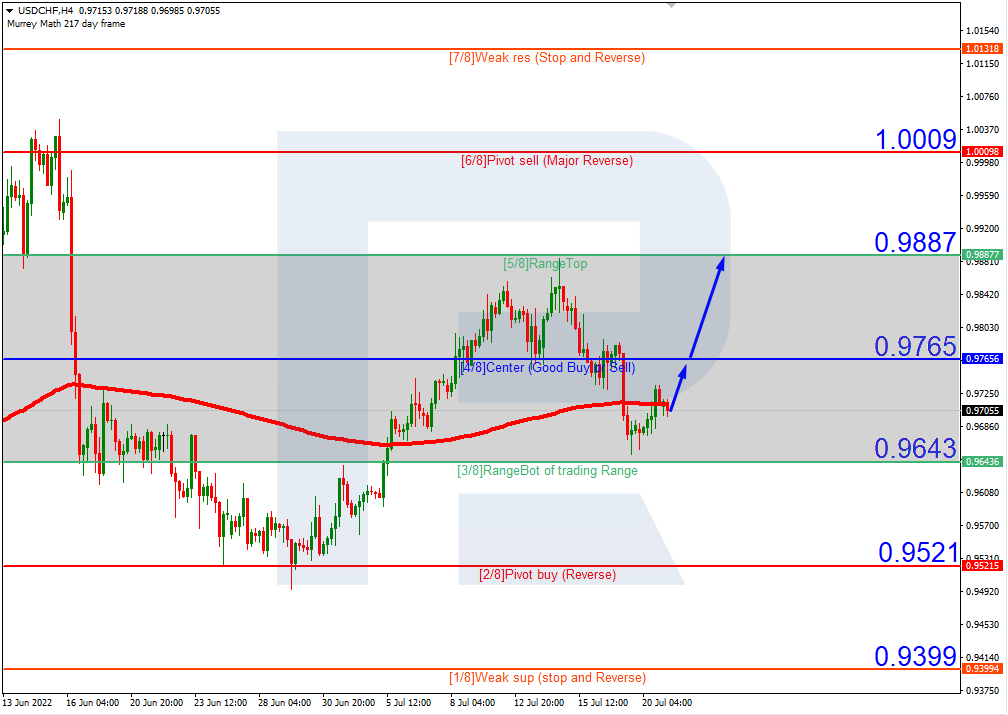

As we can see in the H4 chart, having rebounded from the support at 3/8, USDCHF is consolidating. In this case, the pair is expected to grow towards the resistance at 5/8. However, this scenario may be cancelled if the price breaks 3/8 to the downside. After that, the instrument may move downwards to reach the support at 2/8.

In the M15 chart, the pair may break the upside line of the VoltyChannel indicator and, as a result, continue its growth.

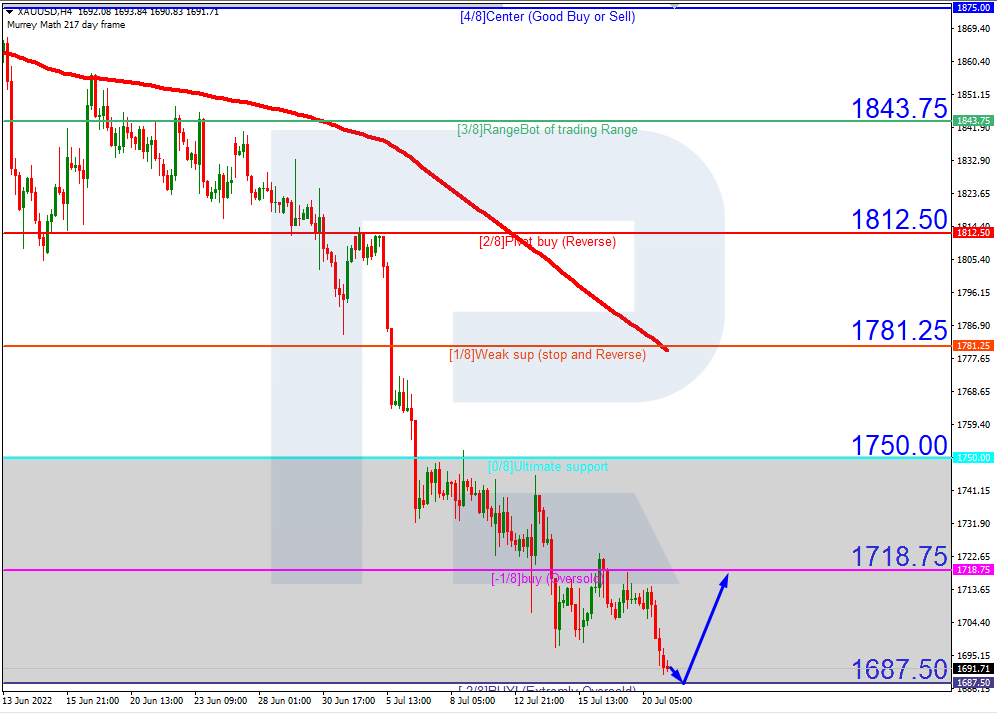

XAUUSD, “Gold vs US Dollar”

As we can see in the H4 chart, XAUUSD is trading inside the “oversold area”. In this case, the price is expected to test -2/8, rebound from it, and then resume moving upwards to reach the resistance at -1/8. However, this scenario may no longer be valid if the price breaks the support at -2/8 to the downside. After that, the lines in the chart will be redrawn, thus helping us to define new downside targets.

In the M15 chart, the pair may break the upside line of the VoltyChannel indicator and, as a result, continue trading upwards.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

As we can see in the H4 chart, having rebounded from the support at 3/8, USDCHF is consolidating. In this case, the pair is expected to grow towards the resistance at 5/8. However, this scenario may be cancelled if the price breaks 3/8 to the downside. After that, the instrument may move downwards to reach the support at 2/8.

In the M15 chart, the pair may break the upside line of the VoltyChannel indicator and, as a result, continue its growth.

XAUUSD, “Gold vs US Dollar”

As we can see in the H4 chart, XAUUSD is trading inside the “oversold area”. In this case, the price is expected to test -2/8, rebound from it, and then resume moving upwards to reach the resistance at -1/8. However, this scenario may no longer be valid if the price breaks the support at -2/8 to the downside. After that, the lines in the chart will be redrawn, thus helping us to define new downside targets.

In the M15 chart, the pair may break the upside line of the VoltyChannel indicator and, as a result, continue trading upwards.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

The long-awaited ECB meeting will be held today, and the ECB is expected to raise the interest rate. Analysts are leaning towards a 0.25% hike, even though there is talk of a 0.5% hike as well. Christine Lagarde will not risk her reputation, so it is easier for the ECB to hold the first rate hike of 0.25% and the next by 0.5% or even 0.75%. The attention of investors will also be directed towards the so-called “anti-fragmentation” package, which is expected to be announced together with the interest rate decision.

Trading recommendations

Support levels: 1.0154, 1.0106, 1.0035, 1.0000

Resistance levels: 1.0284, 1.0365, 1.0415, 1.050

From the technical point of view, the trend on the EUR/USD currency pair on the hourly time frame is bullish. But yesterday, the price corrected a little, and the MACD indicator became inactive. Under such market conditions, it is best to look for buy trades on intraday time frames from the support level of 1.0106, but only with confirmation. Sell trades can be considered from the resistance level of 1.0284, but only after additional confirmation and only with short targets.

Alternative scenario: if the price breaks down through the 1.0000 support level and fixes below, the downtrend will likely resume.

News feed for 2022.07.21:

– Eurozone ECB Monetary Policy Statement at 15:15 (GMT+3);

– Eurozone ECB Interest Rate Decision at 15:15 (GMT+3);

– US Initial Jobless Claims (w/w) at 15:30 (GMT+3);

– US Philadelphia Fed Manufacturing Index (m/m) at 15:30 (GMT+3);

– Eurozone ECB Press Conference at 15:45 (GMT+3).

The GBP/USD currency pair

Technical indicators of the currency pair:

Prev Open: 1.1988

Prev Close: 1.1978

% chg. over the last day: -0.08%

In the UK, the Consumer Price Index reached 9.4% on an annual basis compared to 9.1% in May. Monthly inflation rose by 0.8%. The biggest upward contributions to the annual inflation rate were made by household services (mainly electricity, gas, and other fuels) and transportation (mainly due to higher gasoline and diesel prices). The last time this level of inflation was seen in the country was in March 1991. The Bank of England is likely to raise the interest rate immediately by 0.5% at its next meeting.

Trading recommendations

Support levels: 1.1955, 1.1907, 1.1803

Resistance levels: 1.2065, 1.2137

From the technical point of view, the trend on the GBP/USD currency pair on the hourly time frame is bullish. The price has slightly corrected and is trading at the level of the moving averages. The MACD indicator has become inactive. Under such market conditions, it is best to look for buy trades on intraday time frames from the support level of 1.1955 or 1.1907, but only with confirmation. Sell trades can be considered intraday from the resistance level of 1.2065, but only after additional confirmation and with short targets.

Alternative scenario: if the price breaks down through the 1.1803 support level and fixes below, the downtrend will likely resume.

There is no news feed for today.

The USD/JPY currency pair

Technical indicators of the currency pair:

Prev Open: 138.65

Prev Close: 138.27

% chg. over the last day: -0.27%

The Bank of Japan kept interest rates and monetary policy unchanged. The monetary policy report highlights concerns about the economy above any potential effects on the yen. The BoJ lowered its economic growth forecast for this year, so a falling economy needs continued support. The inflation forecast is 2.3% for the end of the year. Thus, the BoJ is still targeting stimulus despite a wave of interest rate hikes by other central banks. The medium-term uptrend on the USD/JPY currency pair continues.

Trading recommendations

Support levels: 137.67, 137.43, 137.13, 136.48, 135.92, 135.40, 134.64, 134.11

Resistance levels: 138.71, 140.29

From the technical point of view, the medium-term trend on the USD/JPY currency pair is bullish. The MACD indicator has become positive, but the price is still forming a balance. Under such market conditions, buy trades can be sought intraday from the support level of 137.67, but with confirmation. For sell deals, traders can consider the resistance level of 138.71, but only with additional confirmation and short targets.

Alternative scenario: If the price fixes below 137.13, the downtrend will likely resume.

News feed for 2022.07.21:

– BoJ Outlook Report at 06:00 (GMT+3);

– BoJ Interest Rate Decision at 06:00 (GMT+3);

– BoJ Press Conference at 06:00 (GMT+3).

The USD/CAD currency pair

Technical indicators of the currency pair:

Prev Open: 1.2868

Prev Close: 1.2880

% chg. over the last day: +0.09%

Canada’s consumer price level increased by 0.7% last month, twice below expectations. But the country’s annual inflation reached 8.1% after 7.7% in May. This is the highest rate since January 1983. Excluding gasoline and food prices, the Consumer Price Index reached 6.5% on an annual basis in June after 6.3% in May. The acceleration in June was mainly due to higher gasoline prices, but price increases remained broad-based, with seven of the eight major components up 3% or more. Thus, there is no evidence of a slowdown in inflation, which means Canada’s Central Bank will keep pace with the US Federal Reserve and raise interest rates.

Trading recommendations

Support levels: 1.2853, 1.2781

Resistance levels: 1.2934, 1.3006, 1.3085, 1.3154

In terms of technical analysis, the trend on the USD/CAD currency pair is bearish. The price is trading below the moving average lines. The MACD indicator is in the negative zone, and sellers’ pressure remains, but there are the first signs of divergence. Under such market conditions, it is best to consider sell deals from the resistance level of 1.2934, but with confirmation. Buy trades should be viewed on the lower time frames from the support level 1.2853, but only with confirmation and short targets.

Alternative scenario: if the price breaks out and consolidates above the 1.3085 resistance level, the uptrend will likely resume.

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

Wall Street closed up yesterday thanks to a jump in tech stocks on optimistic earnings. At the close, the Dow Jones Index (US30) increased by 0.15%, and the S&P 500 (US500) added 0.59%. The NASDAQ Technology Index (US100) jumped by 1.58%. According to Definitiv, the S&P 500 (US 500) will show a 5.9% year-over-year gain this earnings season, down from an estimate of 6.8% at the beginning of the quarter. Unrestrained inflation initially led markets to estimate a 100 basis point interest rate hike at next week’s upcoming Fed meeting, but 80% probability is now on the side of a 75 basis point hike.

Shares of electric car maker Tesla (TSLA ) rose by 2% in extended trading after reporting higher quarterly earnings. Danaher (DHR), AT&T (T), Philip Morris (PM), Union Pacific (UNP), Blackstone Group (BX), Intuitive Surgical (ISRG), and Snap (SNAP) will report today.

Stock markets in Europe were mostly down on Wednesday. Germany’s DAX (DE30) decreased by 0.20% yesterday, France’s CAC 40 (FR40) lost 0.27%, Spain’s IBEX 35 (ES35) fell by 1.18%, and Britain’s FTSE 100 (UK100) closed down by 0.44%.

According to the German Federal Statistical Office (Destatis), producer prices for manufactured goods were 32.7% higher in June 2022 than in June 2021. In monthly terms, producer prices added 0.6%. In the UK, the Consumer Price Index reached 9.4% on an annual basis compared to 9.1% in May. Monthly inflation rose by 0.8%. The biggest upward contributions to the annual inflation rate were made by household services (mainly electricity, gas, and other fuels) and transportation (mainly due to higher gasoline and diesel prices). The last time this level of inflation was seen in the country was in March 1991. The Bank of England is very likely to raise the interest rate immediately by 0.5% at its next meeting.

Today is that long-awaited ECB interest rate meeting where the ECB will raise the interest rate. The single currency is up about 2% in the last three trading sessions on expectations that the ECB may raise interest rates significantly by 50 basis points, as well as Reuters reports that a key Russian gas pipeline will open on time after maintenance. But most likely, ECB head Christine Lagarde will not risk her reputation, so it is easier for the ECB to hold the first 0.25% increase and the next one already at 0.5% or even 0.75%. Investors’ attention will also be focused on the so-called “anti-fragmentation” package, which is expected to be announced along with the interest rate decision.

On Wednesday, the European Union urged member states to cut gas use by 15% by March as an emergency measure after President Vladimir Putin warned that Russian supplies routed through Europe’s largest pipeline could be cut or even halted.

Italian Prime Minister Mario Draghi won a vote of confidence in the upper chamber’s Senate on Wednesday, but the three main coalition parties refused to participate.

Oil prices are falling as demand concerns outweigh limited supply. US crude oil inventories increased by 3.5 million barrels last week, well above analysts forecasts.

Asian markets were mostly up yesterday. Japan’s Nikkei 225 (JP225) gained 2.67%, Hong Kong’s Hang Seng (HK50) added 1.11%, and Australia’s S&P/ASX 200 (AU200) was up by 1.65%.

The Bank of Japan kept interest rates and monetary policy unchanged. The monetary policy report highlights concerns about the economy above any potential impact on the yen. The BOJ lowered its economic growth forecast for this year, so the falling economy needs continued support. The inflation forecast was 2.3% for the end of the year. So the BoJ is still targeting stimulus, despite a wave of interest rate hikes by other central banks. But it should be noted that there are some changes in the Bank of Japan’s board members. The government announced Tuesday that it would appoint Hajime Takata and Naoki Tamura as new BOJ board members. Both representatives criticize excessive easing policies, especially Takata-san. Therefore, there is a possibility that there could be a change in the Bank of Japan’s rhetoric soon.

The economic outlook for China remains fragile, which fuels negative sentiment around the world as well. Despite China having recovered quickly from the stringent Covid restrictions, worries about the housing sector and the high likelihood of new restrictions are undermining confidence and keeping consumers on edge.

S&P 500 (F) (US500) 3,959.90 +23.21 (+0.59%)

Dow Jones (US30) 31,874.84 +47.79 (+0.15%)

DAX (DE40) 13,281.98 −26.43 (−0.20%)

FTSE 100 (UK100) 7,264.31 −31.97 (−0.44%)

USD Index 107.08 +0.40 (+0.37%)

Important events for today:

– BoJ Outlook Report at 06:00 (GMT+3);

– BoJ Interest Rate Decision at 06:00 (GMT+3);

– BoJ Press Conference at 06:00 (GMT+3);

– Eurozone ECB Monetary Policy Statement at 15:15 (GMT+3);

– Eurozone ECB Interest Rate Decision at 15:15 (GMT+3);

– US Initial Jobless Claims (w/w) at 15:30 (GMT+3);

– US Philadelphia Fed Manufacturing Index (m/m) at 15:30 (GMT+3);

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

On 18 June 2022, RM Investment Bank held an Open Day. The event was attended by clients and partners who had the opportunity to communicate with the company’s management in a relaxed, friendly atmosphere.

During the event, the RM Investment Bank team introduced the company and talked about the opportunities, prospects, and cooperation conditions it has to offer. The guests enjoyed drinks, a food buffet, and an entertainment programme. In addition, there was a giveaway of prizes and promotional merchandise.

Dr. Rostyslav Prus, RM Investment Bank Managing Director, commented: “This event helped us to strengthen our relationship with clients and partners so that they choose to continue investing with us. Many of them wanted to meet with the RM IB team before introducing large investors to the company”.

The RoboMarkets group had earlier announced the opening of an investment bank headquartered in Financial Park in Labuan. RM Investment Bank operates under Labuan FSA № 210138BI and its goal is to offer investment services to clients from Asian countries.

RM Investment Bank offers its clients and partners:

7 asset classes and over 12,000 investment instruments

5 account types with competitive investment conditions

Cutting-edge investment platforms

A multilevel affiliate programme

About RM Investment Bank

RM Investment Bank Ltd is an investment bank operating under Labuan FSA licence No. 210138BI. Find out more detailed information on www.rmib.com.

About RoboMarkets Group

The RoboMarkets Group consists of:

RoboMarkets Ltd, a multi-asset broker operating under CySEC (Cyprus Securities and Exchange Commission) licence No. 191/13, that provides investment services to European clients. Find out more detailed information on www.robomarkets.com

RM Investment Bank Ltd, an investment bank operating under Labuan FSA licence No. 210138BI

RoboMarkets Deutschland GMBH, located in Frankfurt am Main, with licence No. 10154068

RFund – RFund AIFLNP V.C.I.C. Ltd, an alternative investment fund located in Limassol, Cyprus, and regulated by CySEC under licence No. N. LPAIF118/2014

Investors and traders worldwide are keenly anticipating the European Central Bank’s policy announcements today.

Here are some major points to look out for:

The ECB’s first rate hike since 2011

It is widely expected that the ECB will raise its benchmark interest rates today for the first time since 2011.

What matters now is the size of the hike.

Markets have come to expect at least a 25 basis point hike. However, markets are also expecting about a 50% chance that we could see a larger-than-usual 50 basis point hike today (a la “two-in-one” hike).

This is because the ECB has to play catch up with record-high inflation. Europe’s June consumer price index (used to measure headline inflation) hit 8.6% in June – that’s over four times the ECB’s inflation target of 2%.

And with about 80 other central banks around the world already raising their respective rates, its high time that the ECB follows suit.

As the ECB raises rates and gradually reduces its bond buying, investors have been following suit, selling off European bonds in tandem with the central bank. That has resulted in European bond yields moving higher.

However, the fear is that “fragmentation” will occur, meaning to say that bond yields in more vulnerable economies down to the south (i.e. Italy) climb way higher relative to bond yields of relatively stronger economies (i.e. Germany).

Much-higher yields then make it that much more expensive for a government to raise debt (get money from investors). As the government uses more money to pay interest on the debt that they issue, that money would then not be available to be spent on supporting its economy.

Hence, soaring yields of highly-indebted members risks undermining the economy; a scenario that the ECB is trying to avoid.

Today, the ECB is expected to announce details of a new tool to help limit these so-called fragmentation risks.

More importantly, the ECB has to convince markets that this new tool can indeed achieve its goals.

When is it due?

Heads up, it’ll be later than usual.

The policy statement is due at 12:15PM GMT (30 minutes later than past release times)

ECB President Christine Lagarde is set to hold a press conference, starting at 12:45PM GMT (15 minutes later than past start times)

How could all this impact the euro currency?

If the ECB triggers only a 25-basis point hike, that could prompt EURUSD to unwind recent gains. This may be because markets think the ECB is falling further behind in the race to combat inflation.

If the ECB triggers a larger 50bps hike, that may only provide limited support for EURUSD, given that there are other major worries when considering the Eurozone’s economic outlook (more on this further down).

If markets are not convinced that the ECB’s anti-fragmentation tool can do the job, that could further erode sentiment surrounding the euro.

If markets are convinced about the efficacy of this new anti-fragmentation tool, that could help shore up the euro’s performance.

Also, expect a combination of the above scenarios.

Key support and resistance levels for EURUSD

Resistance: 21-day simple moving average (SMA) around 1.027.

Stronger resistance set to arrive around 1.035 region, which market the May and June lows.

Support : Parity =1.000 psychologically-important mark

Stronger support perhaps to arrive at the recent cycle low of 0.99522.

Other major concerns to keep an eye on

Italy’s political chaos

Italian Prime Minister Mario Draghi has resigned.

The political crisis in Europe’s third largest economy is a major concern for the ECB as policymakers try to combat record-high inflation without doing too much damage to the economy.

Such heightened uncertainty has already increased market fears surrounding Europe’s third-largest economy, prompting investors to sell Italian bonds and send their yields higher today, which exacerbates the “fragmentation risks” mentioned earlier.

Europe’s potential energy crisis.

Russia today restored its gas supplies to Germany via the Nord Stream 1 pipeline.

In the lead up to today, markets had feared that Russia could decide not to turn on the taps again after the pipeline has completed its scheduled maintenance. As I had written in last Thursday’s article:

“Such an apocalyptic event would spark an energy crisis in Europe, and further darken its economic outlook by making a recession all but certain. That could even send EURUSD careening past 0.95!”

So, phew … for now.

Still, energy supplies are expected to face further constraints further down the line, especially as we head closer to the winter. The lack of gas supplies may force factories and business to shutter operations, which would negatively impact the economy as well.

Back to today’s main event, if the ECB severely disappoints markets in just a few hours from now, we might even see in the coming sessions a new cycle low for EURUSD below parity.

In short, EURUSD is expected to remain firmly in its downtrend that its adhered to for the past year, with scant reason to expect a sustained recovery in the euro over the near-term.