By InvestMacro

Here are the latest charts and statistics for the Commitment of Traders (COT) data published by the Commodities Futures Trading Commission (CFTC).

The latest COT data is updated through Tuesday May 5th and shows a quick view of how large market participants (for-profit speculators and commercial traders) were positioned in the futures markets. All currency positions are in direct relation to the US dollar where, for example, a bet for the euro is a bet that the euro will rise versus the dollar while a bet against the euro will be a bet that the euro will decline versus the dollar.

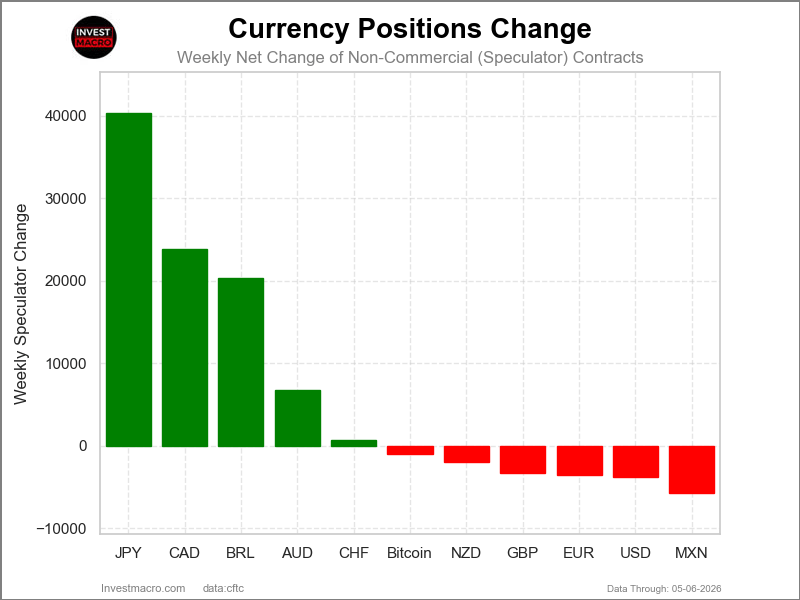

Weekly Speculator Changes led by Japanese Yen & Canadian Dollar

The COT currency market speculator bets were overall slightly lower this week as five out of the eleven currency markets we cover had higher positioning while the other six markets had lower speculator contracts.

Leading the gains for the currency markets was the Japanese Yen (40,321 contracts) with the Canadian Dollar (23,817 contracts), the Brazilian Real (20,354 contracts), the Australian Dollar (6,805 contracts) and the Swiss Franc (700 contracts) also showing positive weeks.

The currencies seeing declines in speculator bets on the week were the Mexican Peso (-5,696 contracts), the US Dollar Index (-3,815 contracts), the EuroFX (-3,510 contracts), the British Pound (-3,269 contracts), the New Zealand Dollar (-1,929 contracts) and Bitcoin (-951 contracts) also registering lower bets on the week.

Yen Speculator Bets jump after intervention, CAD & AUD Bets continue higher as USD Index Bets fall

Highlighting the Currency speculator positions this week was a boost in the Japanese Yen, the Canadian Dollar, and the Brazilian Real positions while the US Dollar Index bets fell by the most since the fall.

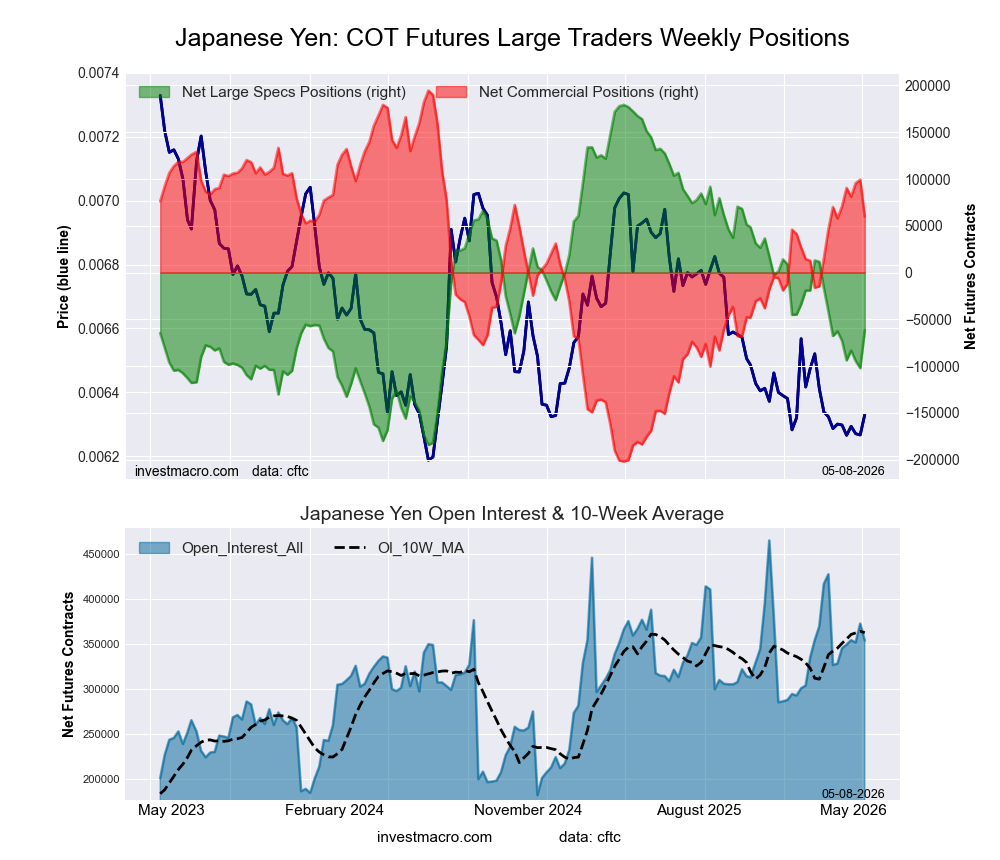

First off, the Japanese Yen speculator position jumped by over 40,000 contracts this week after it had previously fallen in four out of the previous five weeks. This has a lot to do with the Bank of Japan intervening in the Currency market last week, as the BOJ has been trying to arrest the Japanese Yen’s fall. Currently, the speculator net position for the Japanese Yen contracts remains in a bearish level for a 10th straight week, with the total net position this week at -61,738 net contracts. The BOJ currency intervention has stemmed the slide in the yen for the time being, but this week’s USD/JPY currency pair closed out the week at 156.68.

The Brazilian Real saw its speculator bets jump this week by over 20,000 net contracts. This is a third consecutive week of positive changes and this week’s boost has pushed the net position over 66,000 bullish contracts. This is the highest level for the Brazilian Real contracts since September 30th of 2025, a span of 31 weeks. In the Futures market, the Brazilian Real continues to be on a strong bullish uptrend against the US Dollar, and this week closed at the highest level since February of 2024.

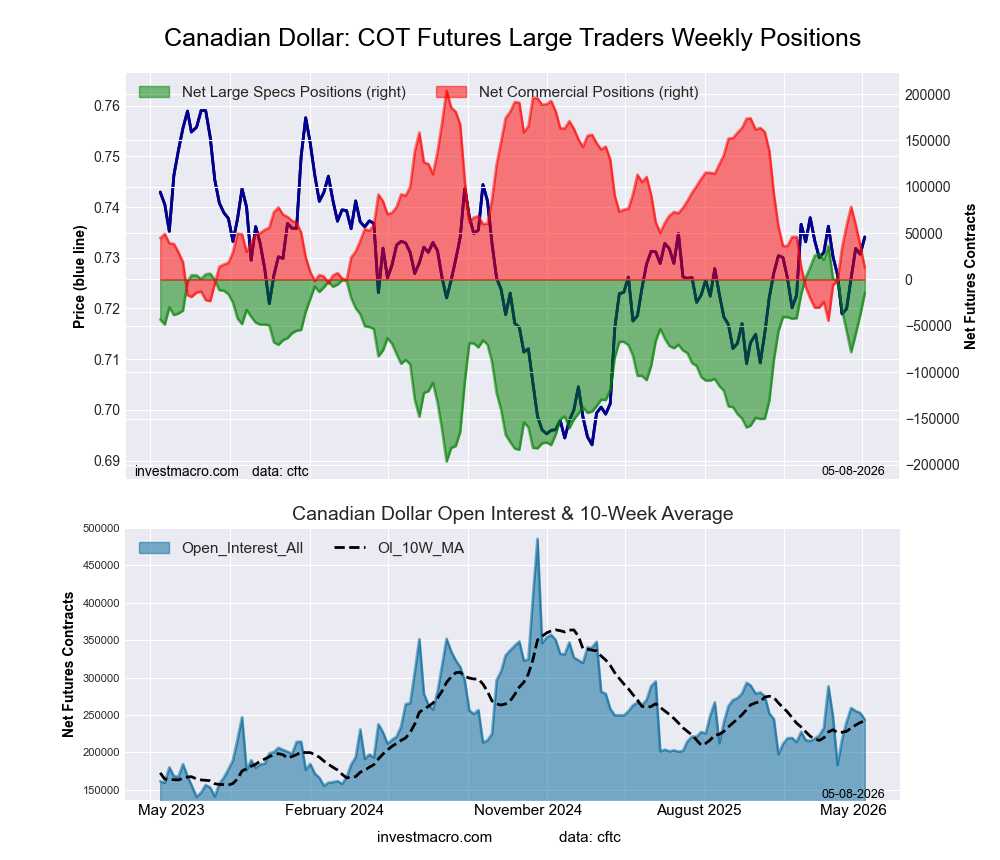

Canadian Dollar contracts continued their strong weekly gains with a third consecutive weekly rise and a boost by over 23,000 contracts this week. This recent positive sentiment for the Canadian Dollar has taken the net speculator bearish standing down to a total of -14,659 net contracts — the best position (least bearish) of the past six weeks. In the Foreign Exchange markets this week, the Canadian Dollar cooled off after four consecutive gaining weeks, and this week closed out at a 0.7321 exchange level. The CAD is still in an ascending triangle pattern and would need to rise clean above 0.7400 to the upside for a further bullish break out.

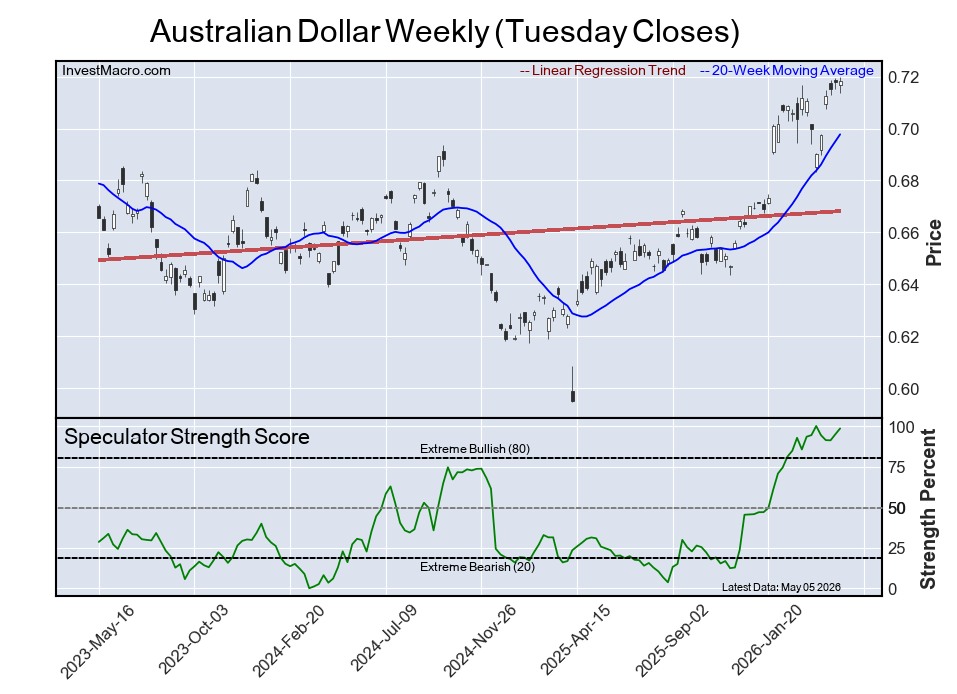

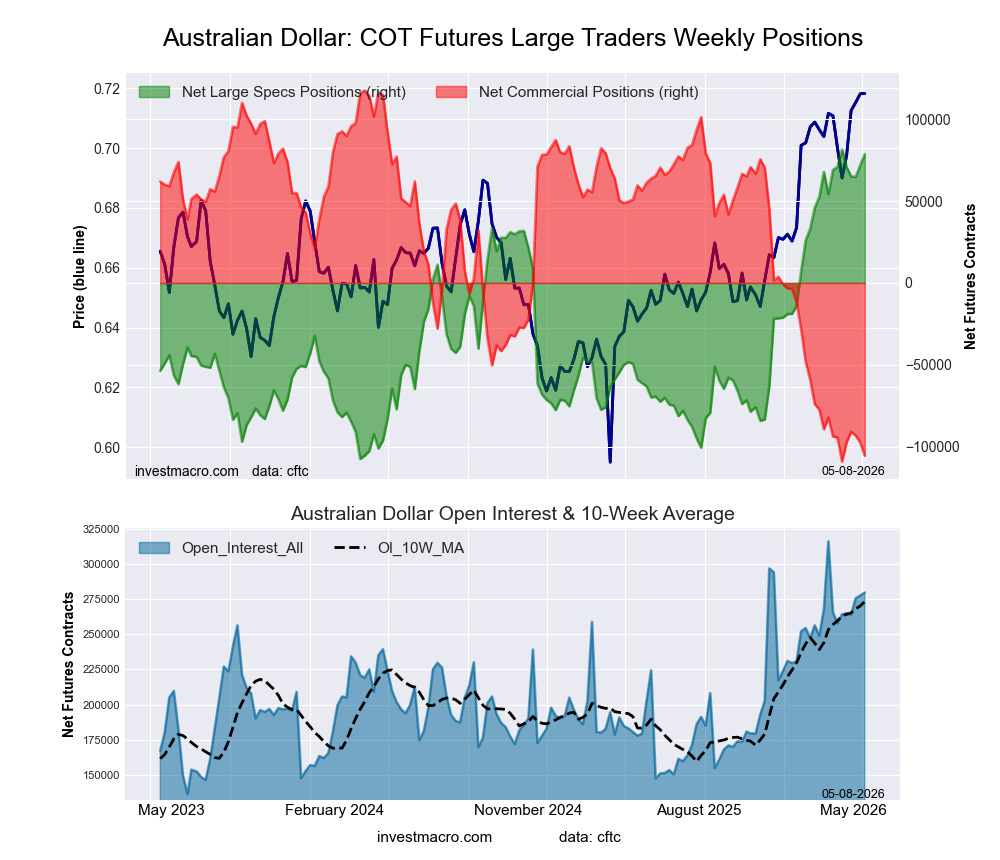

The Australian Dollar net position saw a second straight weekly gain and is now at the highest speculator position of the past five weeks. Overall, the Australian Dollar speculator positioning is in a super strong position, considering it’s near the top of its three-year range with a strength score of 98.5%. The Australian Dollar bets have now been in bullish territory for 15 consecutive weeks. In the Foreign Exchange market, the Australian Dollar has continued on a strong uptrend after falling as low as 0.5920 in April of 2025. Since that low, the AUD has ascended by over 20% and now trades at 0.7237 against the US Dollar, the highest level since 2022.

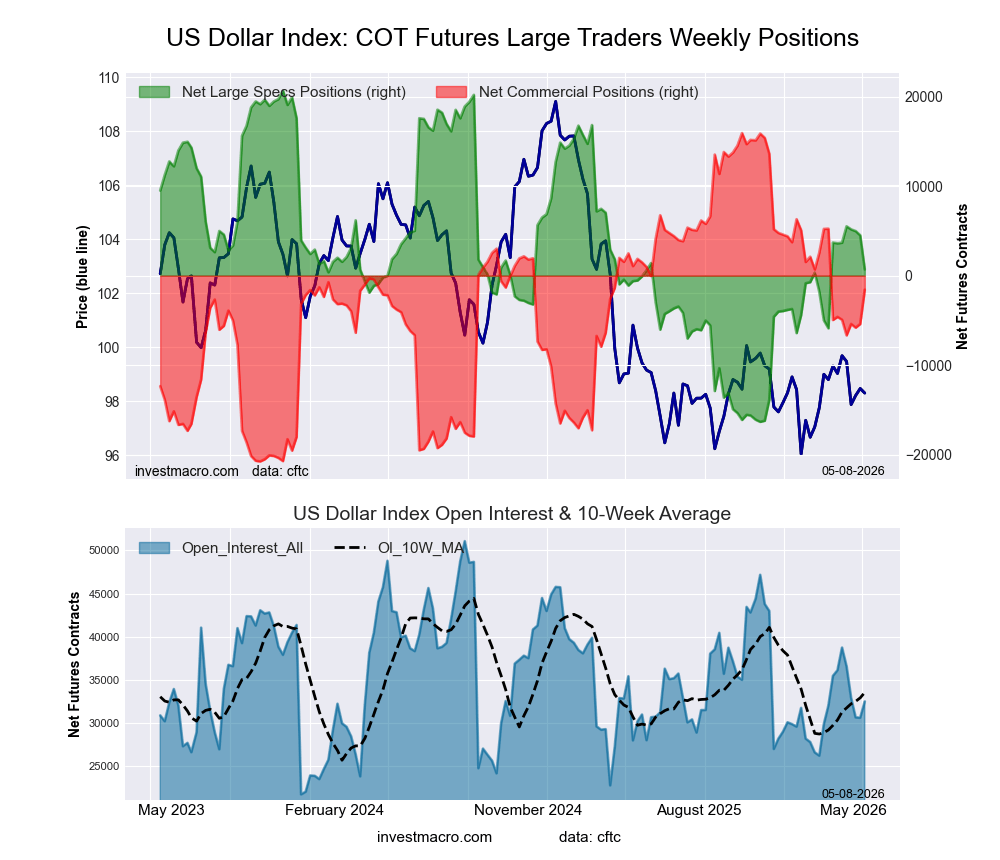

The US Dollar Index saw speculator bets dropped this week by -3,815 contracts and marks the biggest one-week fall since September. The US Dollar Index speculator bets have now declined for four consecutive weeks and have taken the overall net position to a virtual neutral level at just 693 net contracts. The US Dollar Index in the Foreign Exchange markets dipped this week for a second consecutive week, however, it remains in its range that has persisted for almost a year with a low support level of 96.50 and a high resistance level of 100.00 (the USD Index is currently trading at 97.78).

Bitcoin, Mexican Peso, and Brazilian Real lead major Currency price performances.

This week saw Bitcoin lead the pack in price gains with a modest 1.98% rise on the week. The Mexican Peso came in second with a 1.50% gain, while the Brazilian Real was also higher by 1% with a 1.17% uptick. The New Zealand Dollar was higher by approximately 1% this week, while the Swiss Franc rose by 0.58%.

The Euro gained by 0.47%. The Australian Dollar was higher by 0.41%, and the British Pound Sterling rounded out the gainers with a modest uptick of 0.27% on the week.

On the downside, the US Dollar Index tripped by -0.17% this week, while the Japanese Yen was lower by -0.30%. The Canadian Dollar was the biggest negative returner with a -0.67% shortfall.

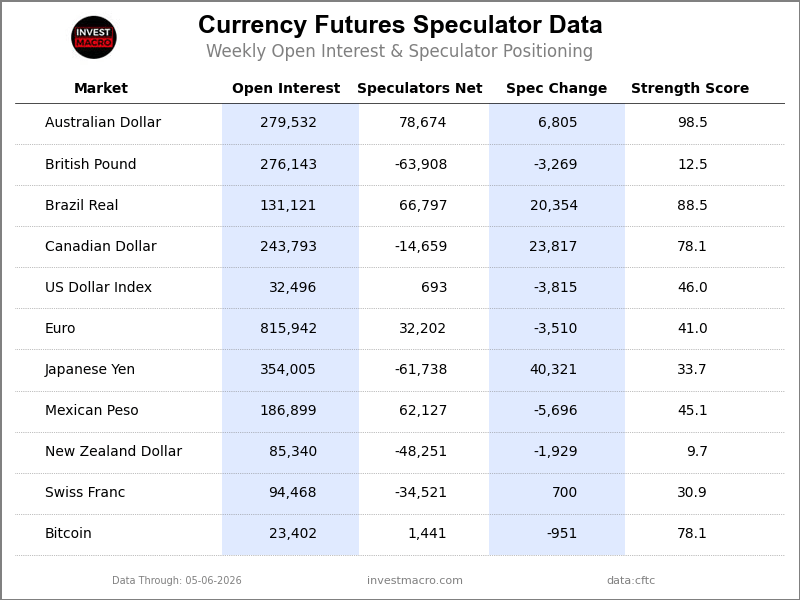

Currencies Data:

Legend: Open Interest | Speculators Current Net Position | Weekly Specs Change | Specs Strength Score compared to last 3-Years (0-100 range)

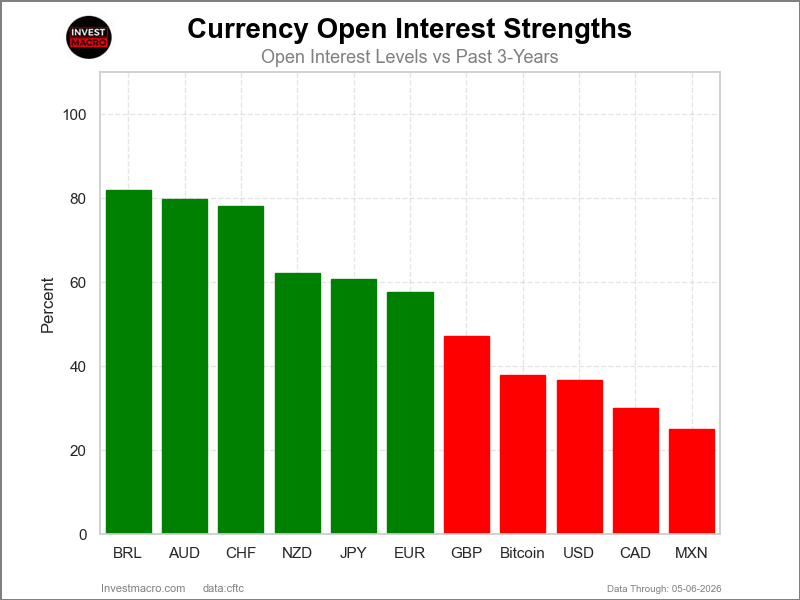

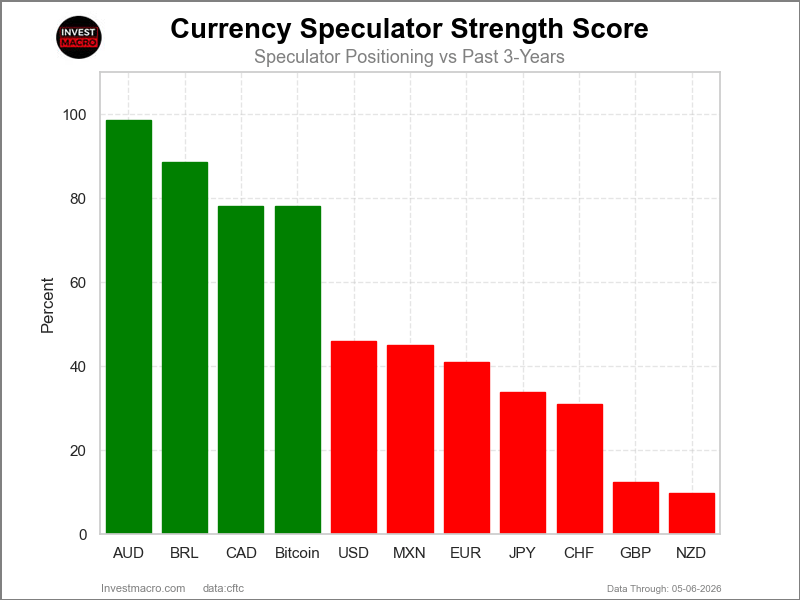

Strength Scores led by Australian Dollar & Brazilian Real

COT Strength Scores (a normalized measure of Speculator positions over a 3-Year range, from 0 to 100 where above 80 is Extreme-Bullish and below 20 is Extreme-Bearish) showed that the Australian Dollar (99 percent) and the Brazilian Real (89 percent) lead the currency markets this week. The Canadian Dollar (78 percent) and Bitcoin (78 percent) come in as the next highest in the weekly strength scores.

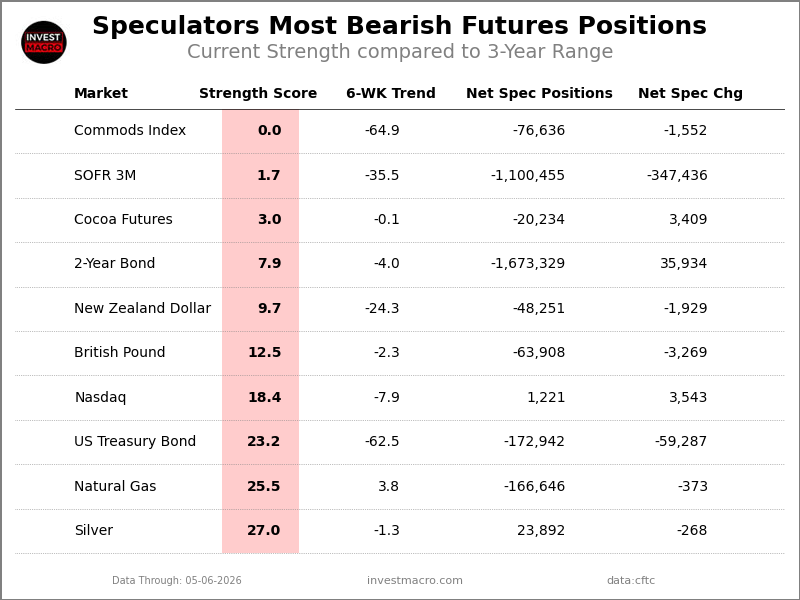

On the downside, the New Zealand Dollar (10 percent) and the British Pound (12 percent) come in at the lowest strength levels currently and are in Extreme-Bearish territory (below 20 percent). The next lowest strength scores are the Swiss Franc (31 percent) and the Japanese Yen (34 percent).

3-Year Strength Statistics:

US Dollar Index (46.0 percent) vs US Dollar Index previous week (56.3 percent)

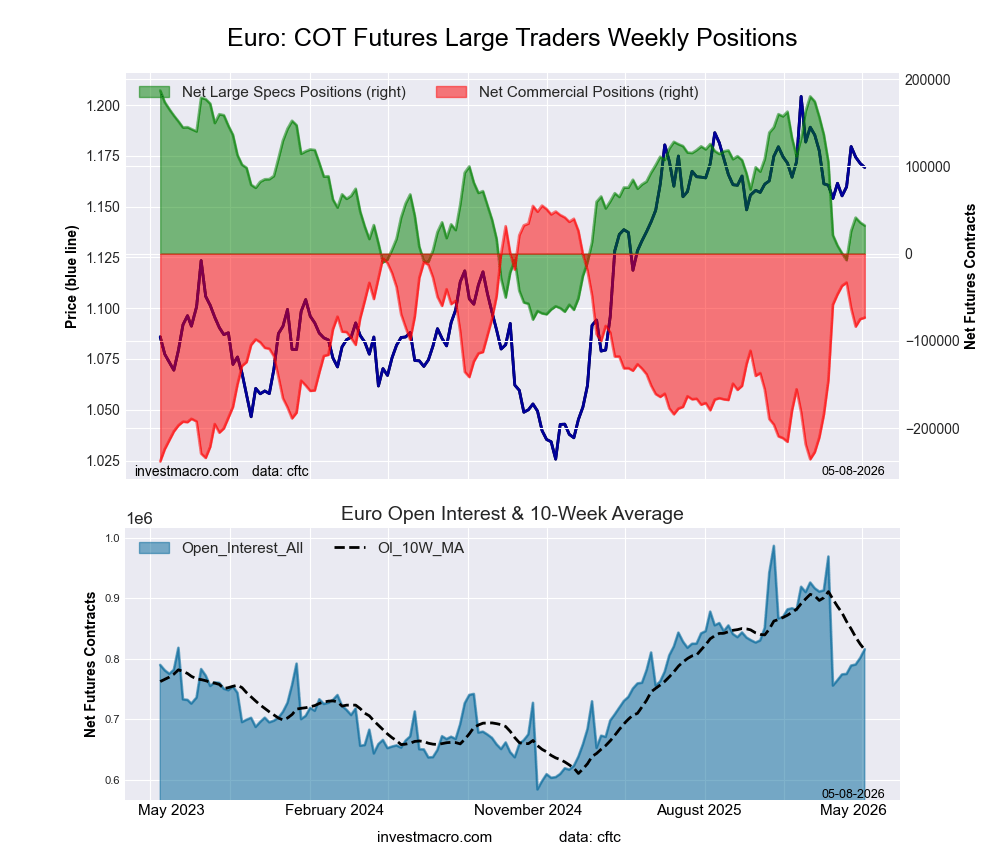

EuroFX (41.0 percent) vs EuroFX previous week (42.4 percent)

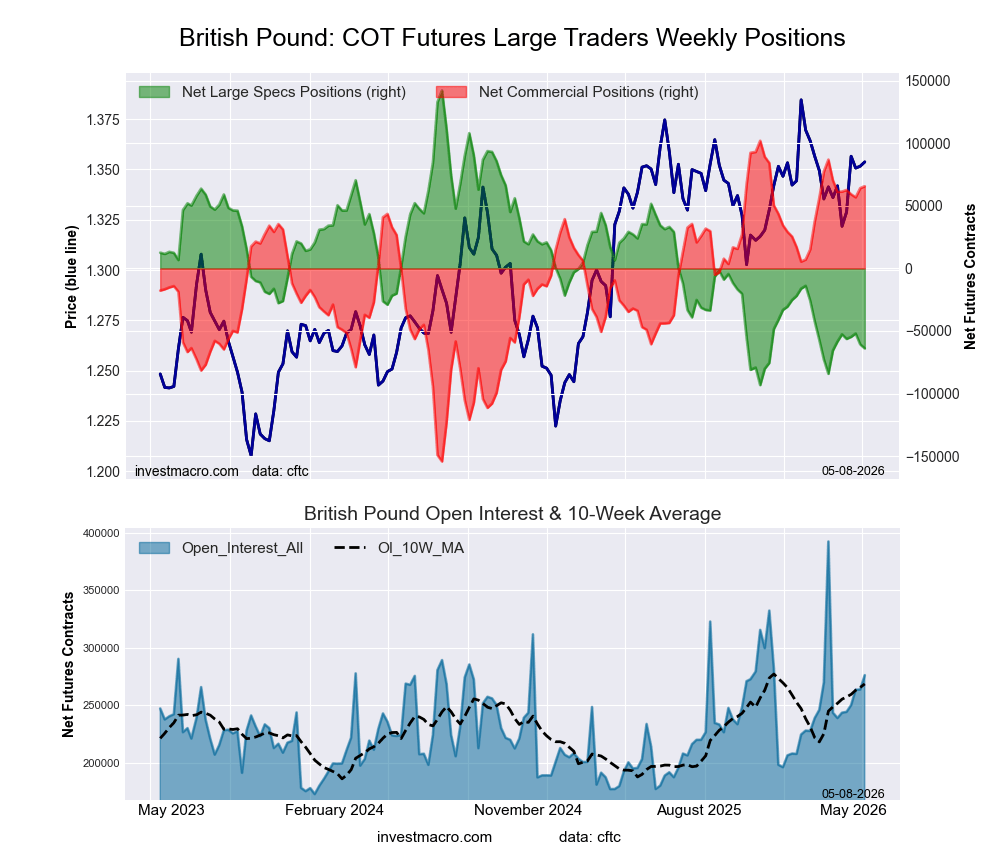

British Pound Sterling (12.5 percent) vs British Pound Sterling previous week (13.8 percent)

Japanese Yen (33.7 percent) vs Japanese Yen previous week (22.6 percent)

Swiss Franc (30.9 percent) vs Swiss Franc previous week (29.5 percent)

Canadian Dollar (78.1 percent) vs Canadian Dollar previous week (67.9 percent)

Australian Dollar (98.5 percent) vs Australian Dollar previous week (94.9 percent)

New Zealand Dollar (9.7 percent) vs New Zealand Dollar previous week (11.9 percent)

Mexican Peso (45.1 percent) vs Mexican Peso previous week (49.1 percent)

Brazilian Real (88.5 percent) vs Brazilian Real previous week (73.7 percent)

Bitcoin (78.1 percent) vs Bitcoin previous week (97.1 percent)

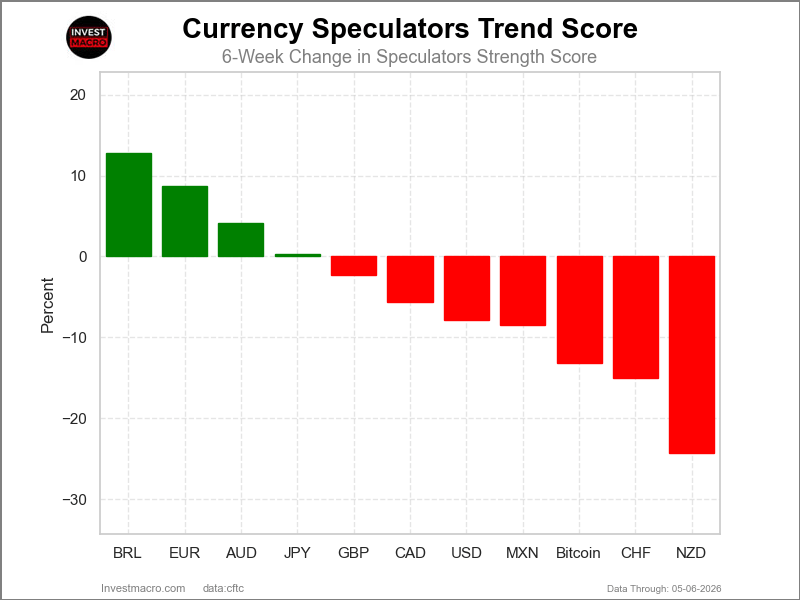

Brazilian Real & EuroFX top the 6-Week Strength Trends

COT Strength Score Trends (or move index, calculates the 6-week changes in strength scores) showed that the Brazilian Real (13 percent) and the EuroFX (9 percent) lead the past six weeks trends for the currencies. The Australian Dollar (4 percent) is the next highest positive mover in the 3-Year trends data.

The New Zealand Dollar (-24 percent) leads the downside trend scores currently with the Swiss Franc (-15 percent), Bitcoin (-13 percent) and the Mexican Peso (-8 percent) following next with lower trend scores.

3-Year Strength Trends:

US Dollar Index (-7.9 percent) vs US Dollar Index previous week (2.2 percent)

EuroFX (8.7 percent) vs EuroFX previous week (5.6 percent)

British Pound Sterling (-2.3 percent) vs British Pound Sterling previous week (2.1 percent)

Japanese Yen (0.3 percent) vs Japanese Yen previous week (-9.4 percent)

Swiss Franc (-15.0 percent) vs Swiss Franc previous week (-20.3 percent)

Canadian Dollar (-5.6 percent) vs Canadian Dollar previous week (-16.9 percent)

Australian Dollar (4.1 percent) vs Australian Dollar previous week (1.5 percent)

New Zealand Dollar (-24.3 percent) vs New Zealand Dollar previous week (-26.6 percent)

Mexican Peso (-8.5 percent) vs Mexican Peso previous week (-0.5 percent)

Brazilian Real (12.8 percent) vs Brazilian Real previous week (-2.1 percent)

Bitcoin (-13.2 percent) vs Bitcoin previous week (12.3 percent)

Individual COT Forex Markets:

US Dollar Index Futures:

Positioning Notes:

Positioning Notes:

- US Dollar Index large speculator standing this week equaled a net position of 693 contracts in the data reported through Tuesday.

- Weekly Speculator position decline of -3,815 contracts from the previous week which had a total of 4,508 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 46.0 percent.

- The Commercials are Bullish with a score of 52.3 percent.

- The Small Traders (not shown in chart) are Bullish with a score of 54.3 percent.

Price Trend-Following Model: Weak Uptrend

Our weekly trend-following model classifies the current market price position as: Weak Uptrend.

| US DOLLAR INDEX Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 52.5 | 30.9 | 8.1 |

| – Percent of Open Interest Shorts: | 50.3 | 35.7 | 5.4 |

| – Net Position: | 693 | -1,569 | 876 |

| – Gross Longs: | 17,048 | 10,035 | 2,634 |

| – Gross Shorts: | 16,355 | 11,604 | 1,758 |

| – Long to Short Ratio: | 1.0 to 1 | 0.9 to 1 | 1.5 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 46.0 | 52.3 | 54.3 |

| – Strength Index Reading (3 Year Range): | Bearish | Bullish | Bullish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -7.9 | 8.3 | -2.1 |

Euro Currency Futures:

Positioning Notes:

Positioning Notes:

- Euro Currency large speculator standing this week equaled a net position of 32,202 contracts in the data reported through Tuesday.

- Weekly Speculator position fall of -3,510 contracts from the previous week which had a total of 35,712 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 41.0 percent.

- The Commercials are Bullish with a score of 56.2 percent.

- The Small Traders (not shown in chart) are Bullish with a score of 61.4 percent.

Price Trend-Following Model: Weak Downtrend

Our weekly trend-following model classifies the current market price position as: Weak Downtrend.

| EURO Currency Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 26.7 | 58.9 | 10.8 |

| – Percent of Open Interest Shorts: | 22.7 | 67.9 | 5.8 |

| – Net Position: | 32,202 | -73,379 | 41,177 |

| – Gross Longs: | 217,474 | 480,886 | 88,156 |

| – Gross Shorts: | 185,272 | 554,265 | 46,979 |

| – Long to Short Ratio: | 1.2 to 1 | 0.9 to 1 | 1.9 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 41.0 | 56.2 | 61.4 |

| – Strength Index Reading (3 Year Range): | Bearish | Bullish | Bullish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 8.7 | -9.1 | 7.8 |

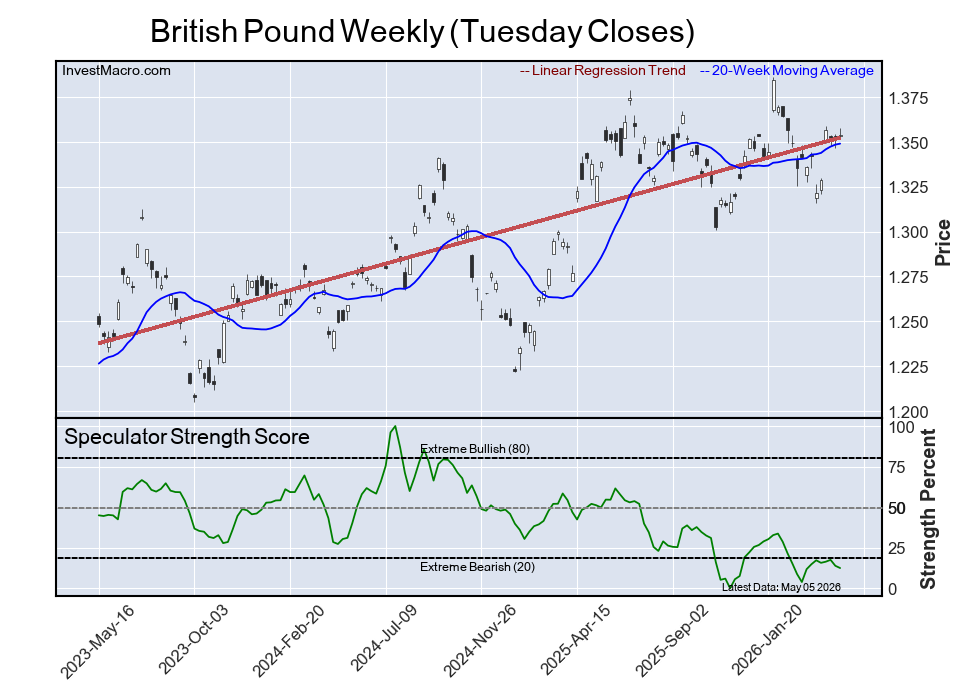

British Pound Sterling Futures:

Positioning Notes:

Positioning Notes:

- British Pound Sterling large speculator standing this week equaled a net position of -63,908 contracts in the data reported through Tuesday.

- Weekly Speculator position lowering of -3,269 contracts from the previous week which had a total of -60,639 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 12.5 percent.

- The Commercials are Bullish-Extreme with a score of 85.8 percent.

- The Small Traders (not shown in chart) are Bearish with a score of 48.6 percent.

Price Trend-Following Model: Weak Downtrend

Our weekly trend-following model classifies the current market price position as: Weak Downtrend.

| BRITISH POUND Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 22.7 | 65.5 | 9.3 |

| – Percent of Open Interest Shorts: | 45.8 | 41.7 | 9.9 |

| – Net Position: | -63,908 | 65,684 | -1,776 |

| – Gross Longs: | 62,573 | 180,932 | 25,560 |

| – Gross Shorts: | 126,481 | 115,248 | 27,336 |

| – Long to Short Ratio: | 0.5 to 1 | 1.6 to 1 | 0.9 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 12.5 | 85.8 | 48.6 |

| – Strength Index Reading (3 Year Range): | Bearish-Extreme | Bullish-Extreme | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -2.3 | 1.8 | 2.6 |

Japanese Yen Futures:

Positioning Notes:

Positioning Notes:

- Japanese Yen large speculator standing this week equaled a net position of -61,738 contracts in the data reported through Tuesday.

- Weekly Speculator position rise of 40,321 contracts from the previous week which had a total of -102,059 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 33.7 percent.

- The Commercials are Bullish with a score of 66.0 percent.

- The Small Traders (not shown in chart) are Bearish with a score of 42.1 percent.

Price Trend-Following Model: Weak Downtrend

Our weekly trend-following model classifies the current market price position as: Weak Downtrend.

| JAPANESE YEN Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 30.8 | 52.7 | 10.7 |

| – Percent of Open Interest Shorts: | 48.2 | 35.8 | 10.1 |

| – Net Position: | -61,738 | 59,650 | 2,088 |

| – Gross Longs: | 109,035 | 186,544 | 37,725 |

| – Gross Shorts: | 170,773 | 126,894 | 35,637 |

| – Long to Short Ratio: | 0.6 to 1 | 1.5 to 1 | 1.1 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 33.7 | 66.0 | 42.1 |

| – Strength Index Reading (3 Year Range): | Bearish | Bullish | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 0.3 | 0.4 | -7.3 |

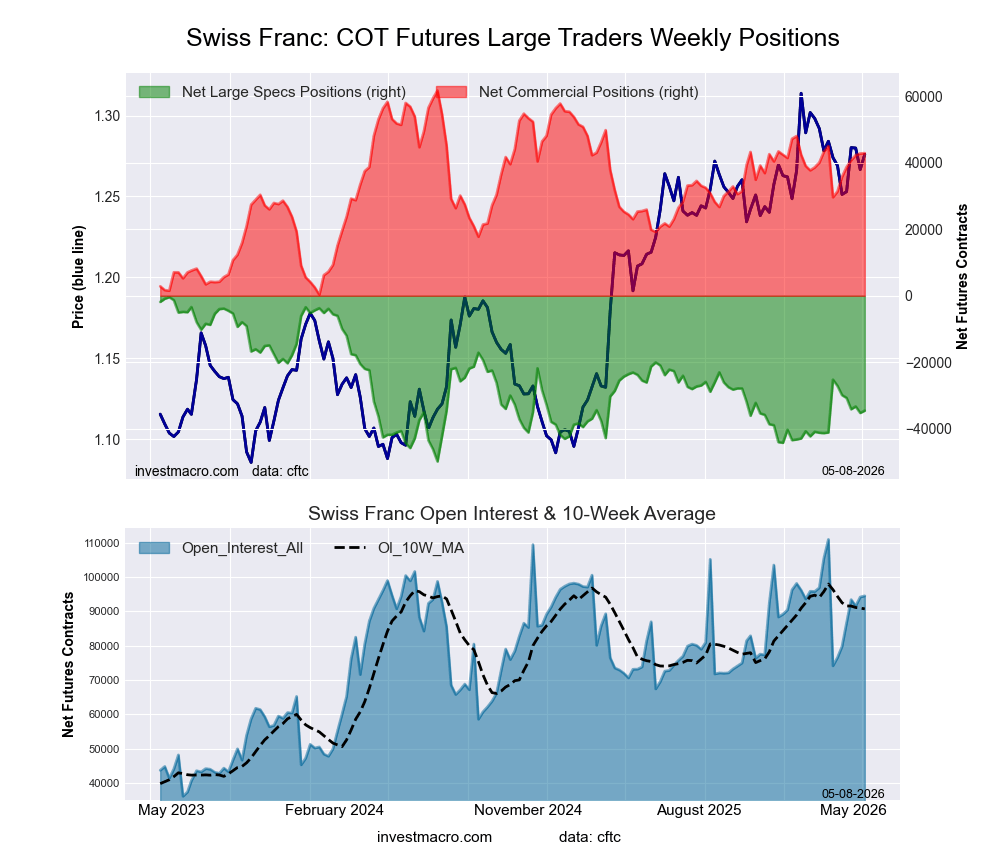

Swiss Franc Futures:

Positioning Notes:

Positioning Notes:

- Swiss Franc large speculator standing this week equaled a net position of -34,521 contracts in the data reported through Tuesday.

- Weekly Speculator position boost of 700 contracts from the previous week which had a total of -35,221 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 30.9 percent.

- The Commercials are Bullish with a score of 69.4 percent.

- The Small Traders (not shown in chart) are Bearish with a score of 43.4 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| SWISS FRANC Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 7.6 | 80.5 | 11.7 |

| – Percent of Open Interest Shorts: | 44.1 | 35.2 | 20.5 |

| – Net Position: | -34,521 | 42,861 | -8,340 |

| – Gross Longs: | 7,145 | 76,076 | 11,018 |

| – Gross Shorts: | 41,666 | 33,215 | 19,358 |

| – Long to Short Ratio: | 0.2 to 1 | 2.3 to 1 | 0.6 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 30.9 | 69.4 | 43.4 |

| – Strength Index Reading (3 Year Range): | Bearish | Bullish | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -15.0 | 18.7 | -17.3 |

Canadian Dollar Futures:

Positioning Notes:

Positioning Notes:

- Canadian Dollar large speculator standing this week equaled a net position of -14,659 contracts in the data reported through Tuesday.

- Weekly Speculator position advance of 23,817 contracts from the previous week which had a total of -38,476 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 78.1 percent.

- The Commercials are Bearish with a score of 23.0 percent.

- The Small Traders (not shown in chart) are Bullish with a score of 50.5 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| CANADIAN DOLLAR Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 30.2 | 55.1 | 12.7 |

| – Percent of Open Interest Shorts: | 36.2 | 49.9 | 11.9 |

| – Net Position: | -14,659 | 12,794 | 1,865 |

| – Gross Longs: | 73,650 | 134,383 | 30,958 |

| – Gross Shorts: | 88,309 | 121,589 | 29,093 |

| – Long to Short Ratio: | 0.8 to 1 | 1.1 to 1 | 1.1 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 78.1 | 23.0 | 50.5 |

| – Strength Index Reading (3 Year Range): | Bullish | Bearish | Bullish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -5.6 | 5.7 | -3.1 |

Australian Dollar Futures:

Positioning Notes:

Positioning Notes:

- Australian Dollar large speculator standing this week equaled a net position of 78,674 contracts in the data reported through Tuesday.

- Weekly Speculator position gain of 6,805 contracts from the previous week which had a total of 71,869 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 98.5 percent.

- The Commercials are Bearish-Extreme with a score of 1.5 percent.

- The Small Traders (not shown in chart) are Bullish-Extreme with a score of 96.8 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| AUSTRALIAN DOLLAR Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 51.2 | 33.0 | 15.1 |

| – Percent of Open Interest Shorts: | 23.1 | 70.8 | 5.4 |

| – Net Position: | 78,674 | -105,545 | 26,871 |

| – Gross Longs: | 143,214 | 92,272 | 42,086 |

| – Gross Shorts: | 64,540 | 197,817 | 15,215 |

| – Long to Short Ratio: | 2.2 to 1 | 0.5 to 1 | 2.8 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 98.5 | 1.5 | 96.8 |

| – Strength Index Reading (3 Year Range): | Bullish-Extreme | Bearish-Extreme | Bullish-Extreme |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 4.1 | -4.9 | 7.2 |

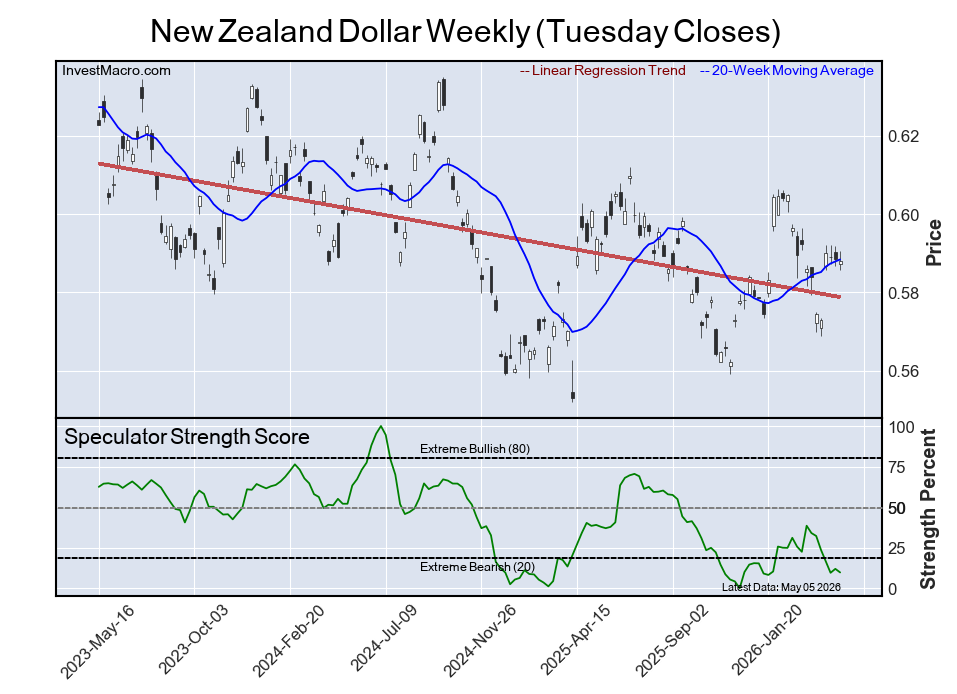

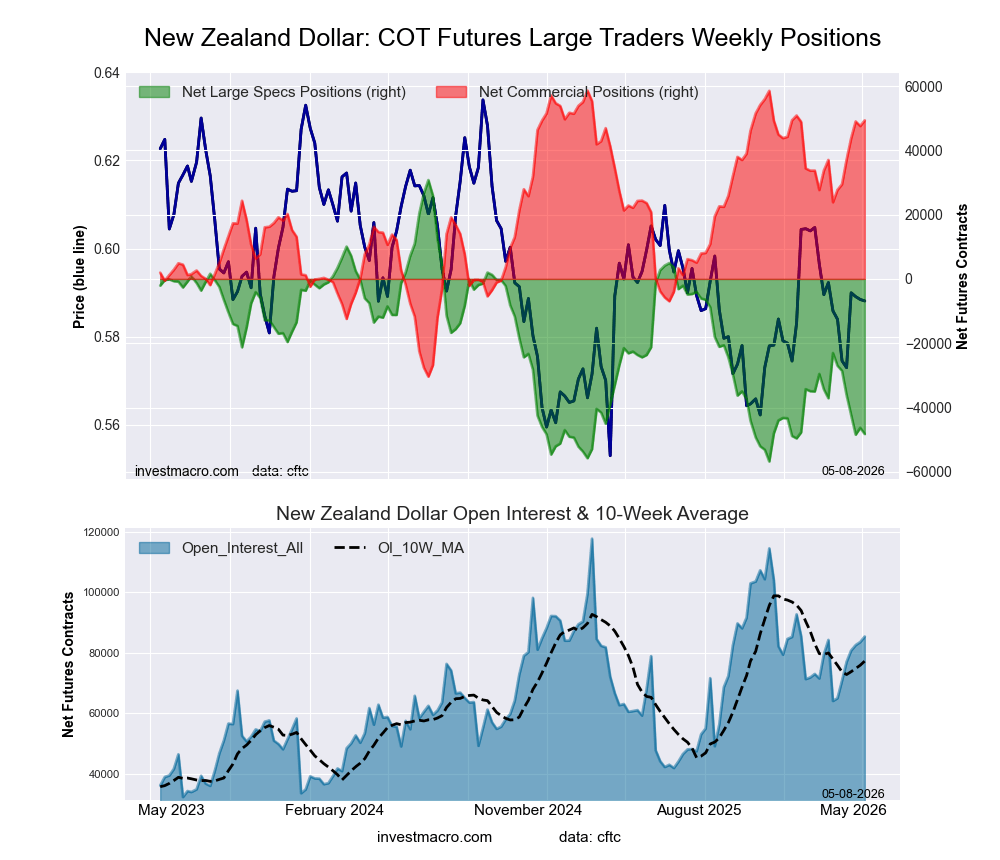

New Zealand Dollar Futures:

Positioning Notes:

Positioning Notes:

- New Zealand Dollar large speculator standing this week equaled a net position of -48,251 contracts in the data reported through Tuesday.

- Weekly Speculator position decline of -1,929 contracts from the previous week which had a total of -46,322 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 9.7 percent.

- The Commercials are Bullish-Extreme with a score of 89.6 percent.

- The Small Traders (not shown in chart) are Bearish with a score of 38.3 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| NEW ZEALAND DOLLAR Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 10.6 | 85.0 | 4.1 |

| – Percent of Open Interest Shorts: | 67.2 | 27.2 | 5.3 |

| – Net Position: | -48,251 | 49,327 | -1,076 |

| – Gross Longs: | 9,063 | 72,581 | 3,486 |

| – Gross Shorts: | 57,314 | 23,254 | 4,562 |

| – Long to Short Ratio: | 0.2 to 1 | 3.1 to 1 | 0.8 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 9.7 | 89.6 | 38.3 |

| – Strength Index Reading (3 Year Range): | Bearish-Extreme | Bullish-Extreme | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -24.3 | 24.3 | -5.0 |

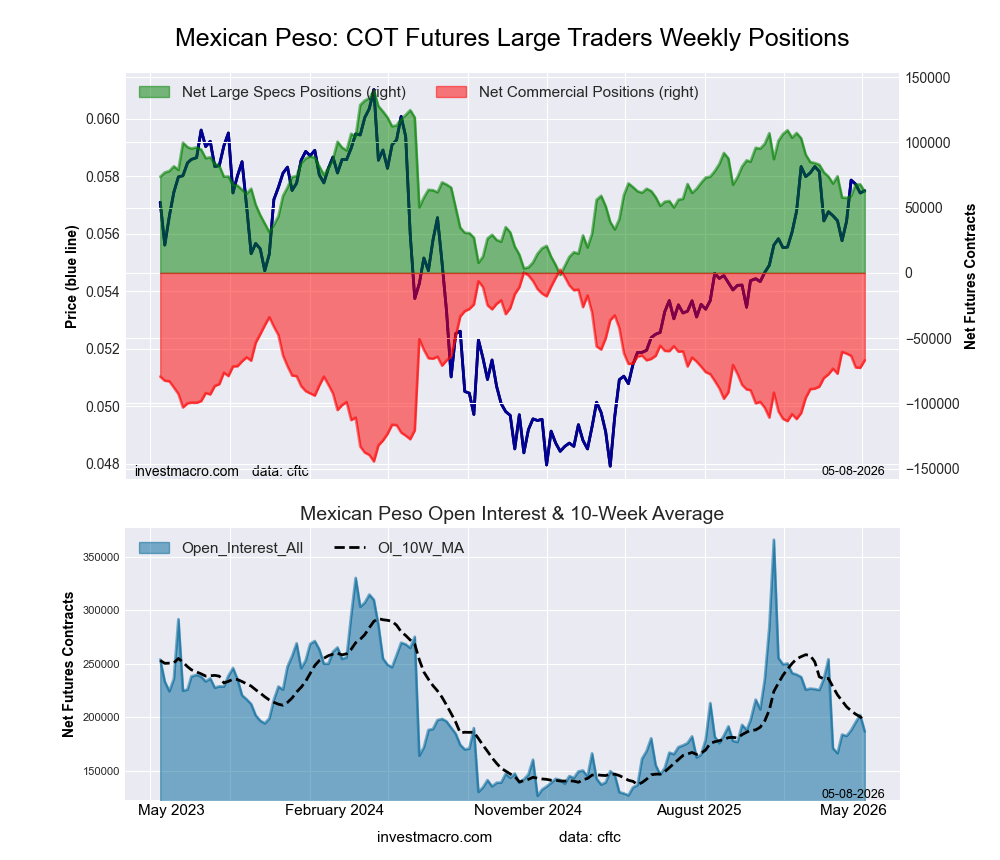

Mexican Peso Futures:

Positioning Notes:

Positioning Notes:

- Mexican Peso large speculator standing this week equaled a net position of 62,127 contracts in the data reported through Tuesday.

- Weekly Speculator position lowering of -5,696 contracts from the previous week which had a total of 67,823 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 45.1 percent.

- The Commercials are Bullish with a score of 52.8 percent.

- The Small Traders (not shown in chart) are Bearish with a score of 49.5 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| MEXICAN PESO Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 49.0 | 46.9 | 3.5 |

| – Percent of Open Interest Shorts: | 15.8 | 82.7 | 1.0 |

| – Net Position: | 62,127 | -66,944 | 4,817 |

| – Gross Longs: | 91,592 | 87,636 | 6,627 |

| – Gross Shorts: | 29,465 | 154,580 | 1,810 |

| – Long to Short Ratio: | 3.1 to 1 | 0.6 to 1 | 3.7 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 45.1 | 52.8 | 49.5 |

| – Strength Index Reading (3 Year Range): | Bearish | Bullish | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -8.5 | 7.0 | 9.2 |

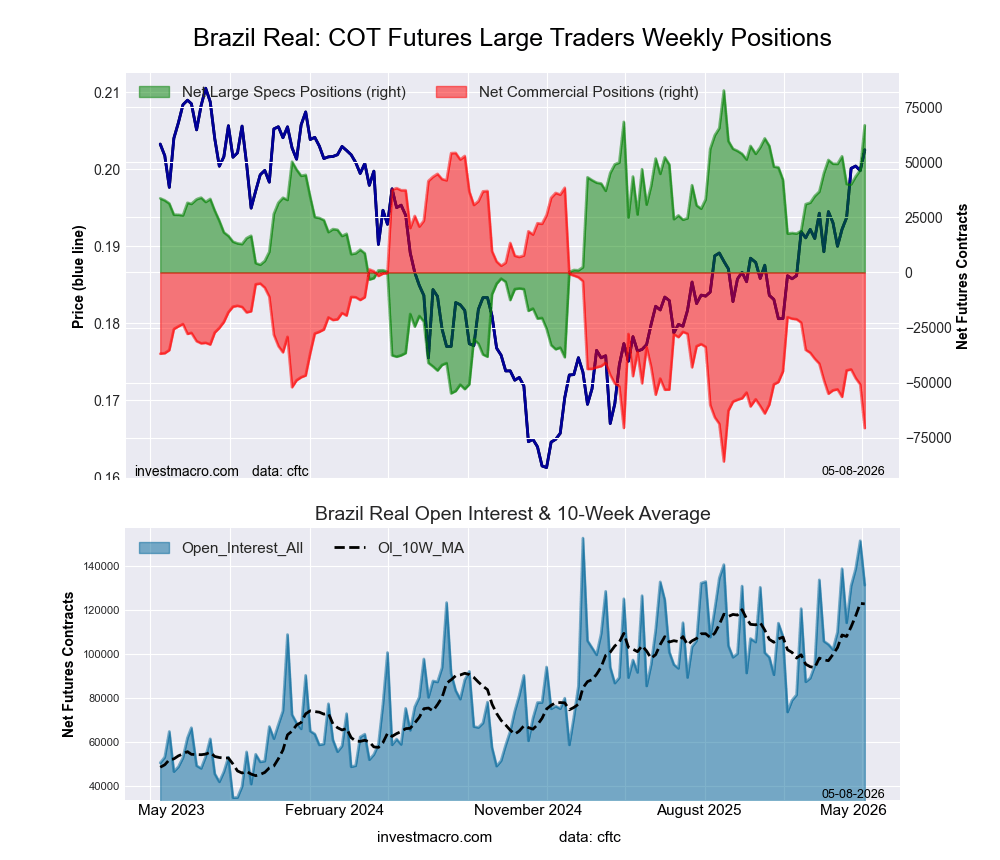

Brazilian Real Futures:

Positioning Notes:

Positioning Notes:

- Brazilian Real large speculator standing this week equaled a net position of 66,797 contracts in the data reported through Tuesday.

- Weekly Speculator position gain of 20,354 contracts from the previous week which had a total of 46,443 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 88.5 percent.

- The Commercials are Bearish-Extreme with a score of 10.8 percent.

- The Small Traders (not shown in chart) are Bearish with a score of 42.6 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| BRAZIL REAL Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 71.3 | 24.2 | 3.9 |

| – Percent of Open Interest Shorts: | 20.4 | 78.1 | 1.0 |

| – Net Position: | 66,797 | -70,648 | 3,851 |

| – Gross Longs: | 93,500 | 31,743 | 5,099 |

| – Gross Shorts: | 26,703 | 102,391 | 1,248 |

| – Long to Short Ratio: | 3.5 to 1 | 0.3 to 1 | 4.1 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 88.5 | 10.8 | 42.6 |

| – Strength Index Reading (3 Year Range): | Bullish-Extreme | Bearish-Extreme | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 12.8 | -12.6 | 0.2 |

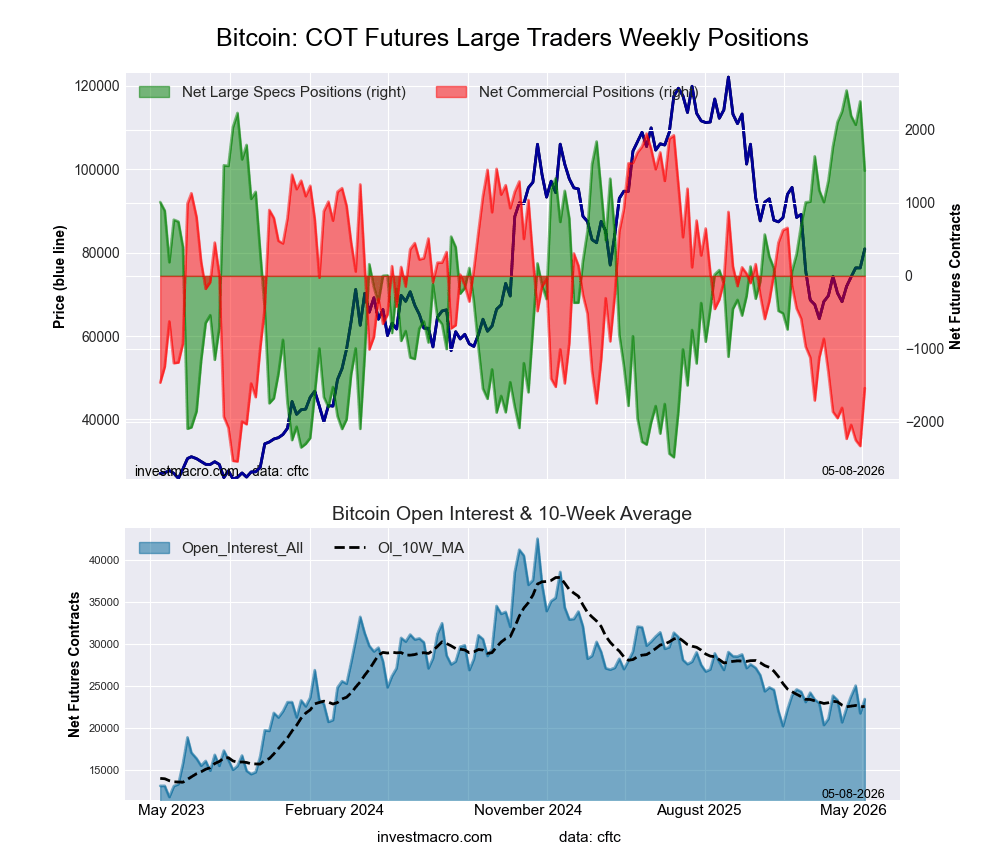

Bitcoin Futures:

Positioning Notes:

Positioning Notes:

- Bitcoin large speculator standing this week equaled a net position of 1,441 contracts in the data reported through Tuesday.

- Weekly Speculator position decline of -951 contracts from the previous week which had a total of 2,392 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 78.1 percent.

- The Commercials are Bearish with a score of 22.4 percent.

- The Small Traders (not shown in chart) are Bearish with a score of 42.4 percent.

Price Trend-Following Model: Weak Downtrend

Our weekly trend-following model classifies the current market price position as: Weak Downtrend.

| BITCOIN Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 82.5 | 1.5 | 5.1 |

| – Percent of Open Interest Shorts: | 76.3 | 8.1 | 4.6 |

| – Net Position: | 1,441 | -1,539 | 98 |

| – Gross Longs: | 19,301 | 349 | 1,184 |

| – Gross Shorts: | 17,860 | 1,888 | 1,086 |

| – Long to Short Ratio: | 1.1 to 1 | 0.2 to 1 | 1.1 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 78.1 | 22.4 | 42.4 |

| – Strength Index Reading (3 Year Range): | Bullish | Bearish | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -13.2 | 9.1 | 13.2 |

Article By InvestMacro – Receive our weekly COT Newsletter

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators) as well as their open interest (contracts open in the market at time of reporting). See CFTC criteria here.