By JustMarkets

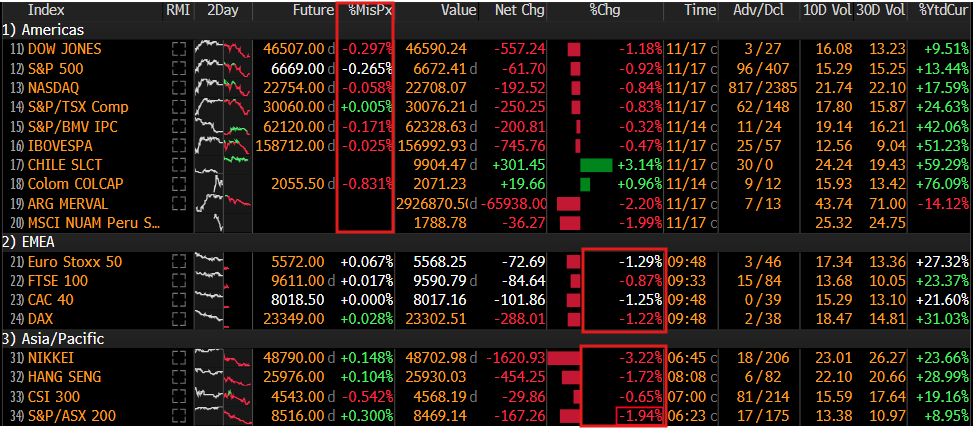

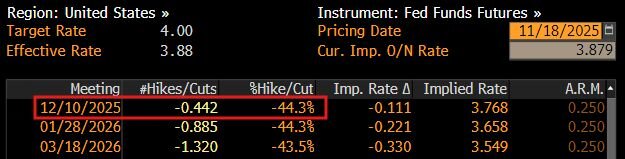

On Wednesday, the US stocks recovered slightly. The Dow Jones Index (US30) rose by 0.10%. The S&P 500 Index (US500) gained 0.38%. The Nasdaq (US100) closed higher at 0.59%. Markets digested the mixed Fed minutes. The minutes from the October FOMC meeting revealed divisions among officials over the appropriateness of further easing. Traders reduced expectations of another Fed rate cut in December. The probability of a 25 bps cut in the federal funds rate is now estimated at about 34%.

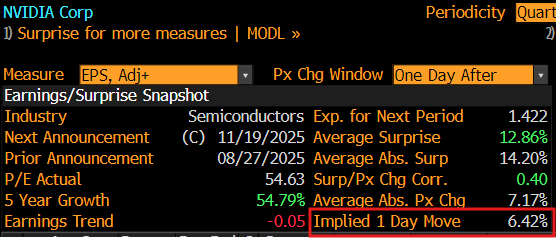

Chip giant Nvidia beat Wall Street expectations for revenue and guidance, easing some concerns about slowing AI investment that had fueled recent market volatility. According to Wednesday’s report, revenue for the three months to October rose 62% to $57 billion, reflecting persistently strong demand for its AI data‑center chips. Sales in the key data‑center segment increased 66%. Shares rose more than 5% after the close of the main session.

The Mexican peso strengthened to 18.35 per US dollar, near July 2024 highs, amid falling domestic inflation and cautious rhetoric from the Bank of Mexico. Headline CPI fell to 3.57% in October, while core inflation dropped just above 4%, strengthening arguments for continuing a mild easing cycle. Banxico cut rates by 25 bps to 7.25%, accompanying the decision with a restrained, data‑dependent tone. This confirmed expectations of gradual rather than aggressive easing and reduced risks of unexpected moves by the regulator.

In Europe, Germany’s DAX (DE40) continued to decline, closing 0.08% lower, France’s CAC 40 (FR40) fell by 0.18%, Spain’s IBEX 35 (ES35) rose 0.39%, and the UK’s FTSE 100 (UK100) dropped 0.47%. European stocks showed modest gains overall, breaking a four‑day losing streak, as investors continued to assess Fed monetary policy prospects and tried to determine fair value for highly speculative tech companies. Performance of European AI‑related firms was mixed: ASML rose by 2.5%, while Infineon slipped slightly. Nokia shares fell by 7% after announcing the spin‑off of its AI business into a separate unit – a move following Nvidia’s $1 billion investment.

WTI crude oil prices fell more than 2% to $59.3 per barrel on Wednesday after reports that the US is pressing for an end to the war between Russia and Ukraine. According to a Ukrainian official, Kyiv received signals of possible US proposals for conflict resolution, reviving hopes for renewed diplomatic talks. Meanwhile, Russia stated that sanctions against Rosneft and Lukoil had not affected production, which also influenced market sentiment. On the supply side, US Energy Information Administration (EIA) data showed crude inventories fell by more than 3.4 million barrels in the week ending November 14, to 424.2 million barrels.

Asian markets mostly declined yesterday. Japan’s Nikkei 225 (JP225) fell by 0.34%, China’s FTSE China A50 (CHA50) rose by 0.74%, Hong Kong’s Hang Seng (HK50) dropped 0.38%, and Australia’s ASX 200 (AU200) closed negative 0.25%.

On Thursday, the offshore yuan held around 7.11 per dollar, stabilizing after recent fluctuations, as China signaled that further monetary easing is not a priority amid ongoing domestic and external challenges. The one‑year Loan Prime Rate (LPR) remained at 3%, while the five‑year LPR, a key benchmark for mortgage lending, was kept at 3.5% after a 10 bps cut in May 2025. The decision followed the People’s Bank of China’s earlier move in November to leave the seven‑day reverse repo rate unchanged, reinforcing expectations of a cautious, “wait‑and‑see” approach to further stimulus.

S&P 500 (US500) 6,642.16 +24.84 (+0.38%)

Dow Jones (US30) 46,138.77 +47.03 (+0.10%)

DAX (DE40) 23,162.92 −17.61 (−0.08%)

FTSE 100 (UK100) 9,507.41 −44.89 (−0.47%)

USD Index 100.16 +0.61% (+0.61%)

News feed for: 2025.11.20

- China PBoC Loan Prime Rate (m/m) at 03:15 (GMT+2); HK50, CHA50 (MED)

- Switzerland Trade Balance (m/m) at 09:00 (GMT+2); – CHF (LOW)

- Hong Kong Inflation Rate (m/m) at 10:30 (GMT+2); – HKD (LOW)

- US Non-Farm Employment Change (m/m) at 15:30 (GMT+2); – USD, XAU (HIGH)

- US Unemployment Rate (m/m) at 15:30 (GMT+2); – USD, XAU/USD (HIGH)

- US Existing Home Sales (m/m) at 17:00 (GMT+2); – USD, (LOW)

- US Natural Gas Storage (w/w) at 17:30 (GMT+2); – XNG (HIGH)

- New Zealand Trade Balance at 23:45 (GMT+2). – NZD (LOW)

By JustMarkets

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.