Opinion — Source: Michael Ballanger (3/2/26)

Michael Ballanger of GGM Advisory Inc. shares his view of current moves in geopolitics and the stock market. He also looks at one copper stock on his list and discusses PDAC.

As we head into the month of March, the headline that dominated the last weekend of February was the U.S.-Israeli attacks on key Iranian targets, which included the killing of Iranian Supreme Leader Ayatollah Ali Khamenei and (allegedly) several of his top military and political staff. Described as a “massive intelligence failure” by the Iranian leadership, the stage has been set for regime change in a country that has been threatening “Death to America” since the overthrow of the Shah of Iran in February of 1979.

CNN, Fox, the BBC, and Bloomberg have been flashing headlines for the past 48 hours that have viewers morbidly riveted to the television screens grasping for any and all confirmation that the theocracy has been eliminated. Unfortunately, despite there being a democratically-elected president in Iran, the only real power lies with the Islamic clerics whose foreign policy strategy has supported (and funded) many terrorist organizations over the past three decades.

- Hezbollah (Lebanon): Iran’s most powerful and capable proxy, receiving an estimated $700 million annually. Iran provided the foundation for the group in the 1980s and continues to supply sophisticated missiles and air-defence systems.

- Hamas (Palestinian Territories): A Sunni militant group that has received up to $350 million per year as of 2023 for its operations against Israel. Support includes rocket technology and military training.

- Palestinian Islamic Jihad (PIJ): Heavily dependent on Iran for its budget, training, and weaponry. It is often described as Tehran’s most loyal Palestinian proxy.

- The Houthis (Yemen): Formally known as Ansar Allah, they receive advanced UAVs (drones), ballistic missiles, and maritime attack capabilities from Iran, which they have used to target international shipping in the Red Sea.

As a result, years of waffling by Western nations, including the U.S., have allowed the Iranians to construct an informal yet effective counter presence to the domination of the Israeli military in the Middle East region. As always, heavy lobbying by the Israeli supporters in Washington has turned the tide, and now the world faces a direct declaration of war against Iran led by Israel and backstopped by the massive American strike force now positioned in the Gulf, armed and ready to unleash shock-and-awe power on the Iranians. I suspect that surveillance over the Straits of Hormuz will be intense, as over 20 million barrels of oil pass through the waterway each day, representing over 20% of global oil production. As the passage is only 21 miles across at its narrowest point, any steps to block tankers from navigating the Straits would be catastrophic to the world economy.

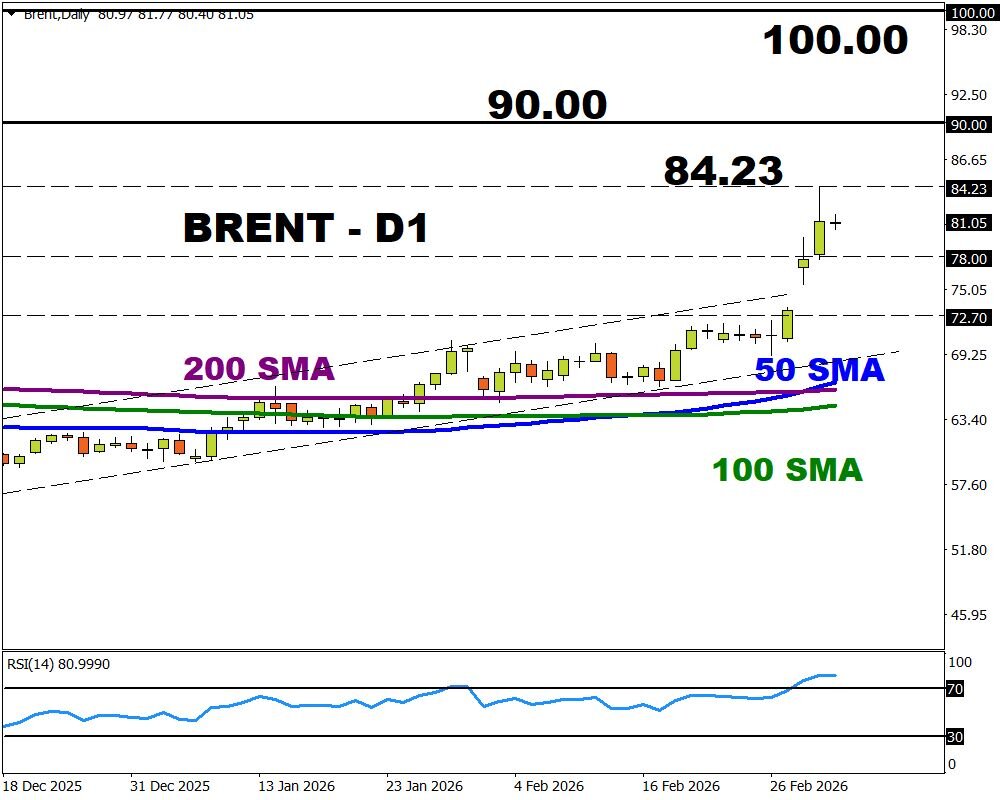

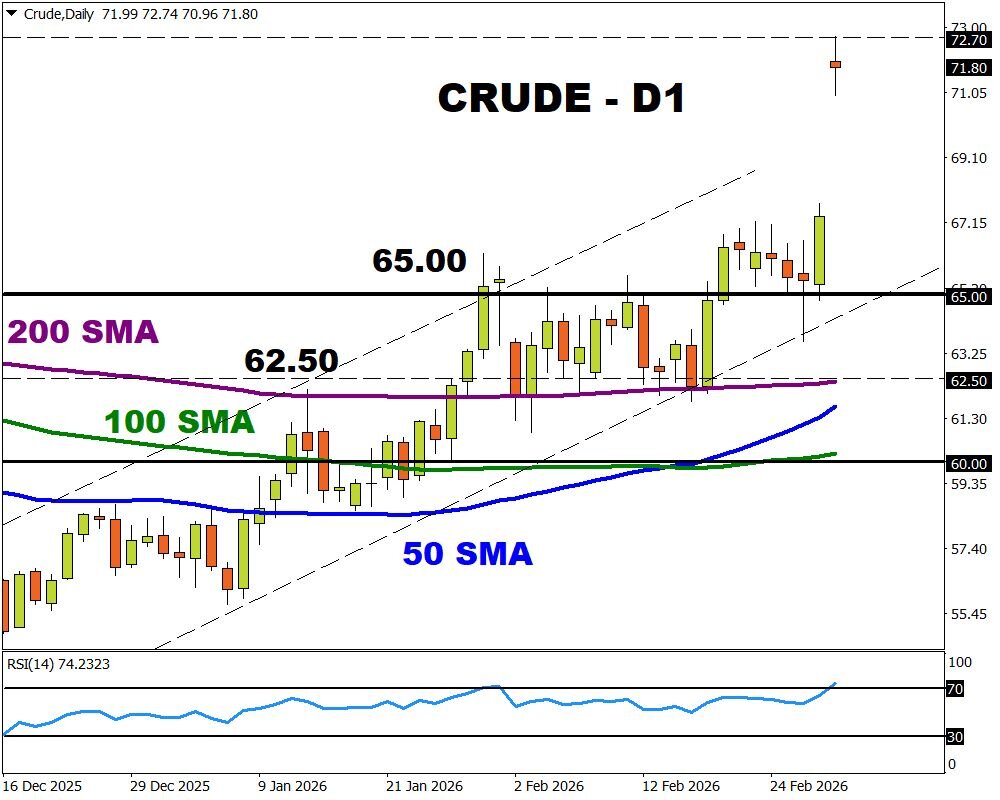

However, as is the case with all geopolitical events, their impact on markets is usually short, sharp, and swift and rarely cause protracted declines in stocks or rises in gold but ancillary effects of the conflict such as the closing of the Straits of Hormuz would send oil prices into a vertical trajectory that has some pundits calling for $100/bbl. as a result. The inflationary impact of such a price spike would be immediate, so the beneficiaries would be gold and silver, but not the mining stocks, because the greater portion of input costs for those miners is energy, with a specific focus on diesel, which powers trucks, and front-end loaders and drill rigs.

I expect oil to gap up into the $70 range overnight unless the evidence shows that the oil-producing facilities are untouched or that hostilities have abated.

As much as I have narrowed this discussion to the weekend attacks on Iran and the death of Khamenei, it has camouflaged what I believe was an even bigger story for the global capital markets last week and that was the sudden failure of Market Financial Solutions (MFS) which specialized in housing bridging loans and, as was well-stated by Zerohedge on Sunday, “is a mutant melange of all the worst traits of both Tricolor and First Brands — last year’s Private Credit implosion superstars — which collapsed virtually overnight having previously attracted backing from firms such financial giants as Barclays, Apollo’s Atlas SP Partners unit, Jefferies (which is now two for two after its participation in the First Brands bankruptcy) and TPG.

The practice that sank this outfit was the “rehypothecation” of underlying collateral with multiple lenders many times over, such that an asset worth £230 million has over £1.2 billion in debt pledged against it. While these practices are essentially fraud, they never get revealed until there is concern over the underlying asset, and once any one lender demands the collateral, the Ponzi scheme collapses, taking everyone with it.

The MFS story surfaced on Thursday night, but the initial hiccup on Wall Street with the DJIA off over 700 points in the first hour was met with aggressive dip-buying all session, with the bulk of the sell-off not in the software stocks but in the financials, where the selling was broadly-based and across-the-board.

Global skirmishes rarely cause prolonged market declines, but credit events do, as we saw in 2008 with the initial collapse of the two Bear Stearns hedge funds tied to subprime loans. Wall Street shrugged off those two failures, citing “containment” to only one firm. As we all found out later, it was not “contained” and was in fact “systemic,” eventually taking the entire global financial system to the point of full-on collapse.

I would point to the failures of Tricolor and First Brands last October, followed by last week’s blow-up by MFS, as evidence of more cockroaches appearing in the kitchen of private credit, and just like Wall Street’s full denial back in 2007 of any possible contagion, these were the headlines in October worth noting:

- Wall Street lenders see limited fallout from bankruptcies

- JPMorgan CEO warns of potential credit market excess

- BlackRock CFO sees strong credit quality despite bankruptcies

To see the name “Blackrock” up there referring to “strong credit quality” is far more impactful than the events in Iran, which are now looking like a purposeful distraction, deflecting all eyes away from the escalating rot that is again starting to envelop the financial sector just as it did eighteen years ago.

So, when I see the gold and silver miners in retreat next week despite rising gold and silver prices, I will look to rising oil and collapsing credit as the culprits.

Fitzroy

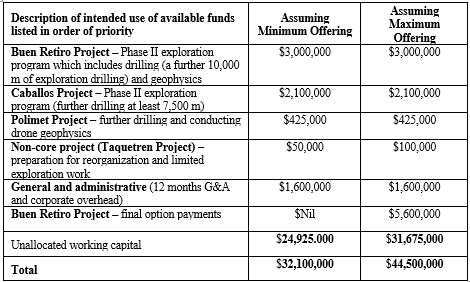

I had the pleasure of sitting down to a luncheon with Fitzroy Minerals Inc. (FTZ:TSX.V; FTZFF:OTCQB) Chairman Campbell Smyth as well as CEO Merlin Marr-Johnson along with two current investors on Saturday and watched and listened as they mapped out the game plan for Fitzroy for 2026 and the rationale for raising over CA$20 million (announced last week) while sitting with nearly CA$12 million in the bank. A large number of investors have asked me why they elected to dilute current shareholders now instead of more drilling at both Buen Retiro and Caballos before financing. With 330 million shares issued, the new financing for “up to CA$26 million” by way of LIFE and concurrent private placement offerings could add up to 78 million additional shares, which would capitalize the deal at CA$204 million (assuming full dilution).

A few subscribers came back with the “CA$204m for an exploration company not yet in production? Isn’t that rich?” so when I threw that out in front of Smyth and Marr-Johnson, their explanation was at once both revealing and exciting.

The key to the transaction lies in the agreement signed on July 3, 2023, when pre-Fitzroy company Ptolemy Inc. entered into the earn-in with Pucobre SA, which at the time was a US$800m Chilean copper miner specializing in small-scale oxide deposits. The terms included:

- Work Commitment: Ptolemy must carry out a US$7,000,000 work program over four years.

- Year 1: US$2,000,000.

- Years 2–4: US$5,000,000 (minimum US$1,000,000 in any consecutive 12-month period).

- Option Exercise: In Year 5, Ptolemy can exercise the option to acquire 100% ownership with a US$4,000,000 payment.

- Royalties: Vendors retain a 2% Net Smelter Royalty (NSR), with a 1% buyback provision for US$5,000,000 prior to production.

Pucobre’s 30% Clawback Right

- Clawback Right: After Ptolemy completes the acquisition, Pucobre has the right to purchase back up to 30% of the local subsidiary holding the asset.

- Purchase Price: The price is calculated as three times 30% of the sum of:

- A fixed US$300,000 amount.

- All investment made by Ptolemy related to the Buen Retiro Option.

- Post-Clawback: If exercised, Pucobre will fund the project pro rata or face dilution.

Following these initial agreements, Fitzroy Minerals Inc. completed the acquisition of Ptolemy Mining Limited in March 2025, thereby assuming these option terms.

So now, Fitzroy Minerals has until July 3, 2028, to complete the remaining terms after which they will have earned a full 100% interest in the Buen Retiro project. Where this gets interesting lies in that “clawback provision” (“CP”). If Pucobre SA elects to exercise the CP, they are obligated to pay FTZ/FTZFF 90% of all expenditures retroactive to Day One. So, if the company were to spend the entire CA$26 million in expanding both the economically-viable oxides and the newly-discovered sulphide zone, they would be refunded CA$23.4 million and wind up with 70% interest in the project.

The initial expectation is an operation generating 20m lbs. of Cu with a margin of around US$4/lb. at US$6.00/lb. Cu. The CAPEX for this operation would be approximately US$50m of which Fitzroy’s portion would be 70% or US$35m. Commencing in 2028, the company could potentially receive US$56m/year of free cash flow with an expected mine life of eight years.

According to Marr-Johnson, that would justify a US$400m market cap or a little under US$1.00 per share for FTZ/FTZFF, and since the copper-bearing oxides at Buen Retiro have been thoroughly tested with over 40k metres of drilling, there is little risk (other than the copper price) to the achievement of that valuation.

However, it will require money and lots of it in order to successfully execute the milestones set out in the earn-in agreement, so rather than gamble on the financing environment down the line, they elected to take the prudent course of action and access the larger institutional market now, and that, my friends, was simply a brilliant move. At the end of the day, they will have a CA$32m war chest with which to compete all terms of the earn-in and still have enough money for a 10,000m drill program at Buen Retiro and “at least” 7,500m of drilling at Caballos.

I have never encountered any exploration company in my five-decade career that can drill out a project knowing with confidence that 90% of whatever they spend will be returned by an eager and established partner. More importantly, since equity markets are valued at over two standard deviations above the norm, with technology stocks led by “AI” now rolling over, there is no need for concern about a funding shortfall at least until well into 2027. Hopefully, by then, the company has established economic viability of the deeper Cu-bearing sulphide zone(s) and the same for Caballos, two accomplishments that would move the implied market cap for FTZ/FTZFF to north of US$1 billion (or around US$2.50 on a fully-diluted basis).

One final observation from the luncheon: This is a well-oiled and seasoned team of proven professionals running Fitzroy’s two flagship programs. With this financing, they have brought in large, deep-pocketed global investment firms from the U.K. and Australia as strategic investors. One of these investors that constituted the lead order in the raise gave instructions to Merlin Marr-Johnson which resonate strongly: “Go find us “BIG COPPER.” With that as a clarion call, I urge all subscribers to heed the words because with that, FTZ/FTZFF has finally entered the “big leagues” of junior exploration and development as there is less risk today at CA$0.50 than there was last June at CA$0.30.

PDAC

The largest collection of mining promoters on the planet can be found at noon on Sunday at the Toronto Metro Convention Centre where the Prospectors and Developers Association of Canada (“PDAC”) annual convention gets underway with what could be the largest attendance in the history of the show. Established in 1932, the association expanded their annual meeting to a full-day affair and then later in 1944 moved to the Royal York Hotel to accommodate the large increase in both members and attendees.

Since 1997, it has become the biggest gong-show in North America with hundreds of mining companies both junior and senior all vying for the attention of the retail and institutional investor complete with contests, featured speakers, investment workshops, and the usual parade of carnival barkers, confidence men, and charlatans all doing what they must to relieve us of our hard-earned savings all in the quest for untold wealth and instant enrichment by way of the drill bit.

Mark Twain was once asked the definition of a gold mine, and he answered, “a hole in the ground with a liar at the top,” in what over the years has grown to be a somewhat accurate measure of the veracity of the claims made by those looking for investors to finance a project. In the old days of the early 1900’s it was farmers from southwest Ontario what had most of the disposable wealth in the country and it was their money that funded big discoveries in the north in small towns like Cobalt and Kirkland Lake that led to the discovery of the mighty Abitibi Greenstone Belt, a geological province stretching from northwestern Quebec to Wawa, Ontario that was the source of over 190–200 million ounces of gold, more than 35 billion pounds of zinc, 15 billion pounds of copper, and at least 400 million ounces of silver.

Many of these discoveries were aided and abetted by the PDAC convention, where it showcased actual samples of rock containing all of the metals mentioned above. When I first attended in 1981, the booths were filled with mining people with few “suits”, many “lumberjack jackets”, and rarely a female. That all changed in the 1980s during a particularly flat period for the metals. During the years after gold’s top in 1980 at $857 per ounce, PDAC conventions needed to re-invent themselves from standard industrial-style “workshops” that featured core shacks and claim maps to something more akin to the trade shows in Miami and Las Vegas, where the marketing wizards utilized new technologies to attract investors. By the mid-1980s, the booths were lit up with lights and music and free giveaways like key chains, calendars, and baseball caps, all designed to get bodies into the aisles where they could be corralled into booth after booth and in front of arguably the finest pitchmen on the planet.

My friend Robert Bishop and I were once having a conversation in the newsletter section where Bob was signing up the odd straggler to his advisory service “The Gold Mining Stock Report” which at the time was the singular best source of junior mining information and advice that money could buy. However, Bob was struggling to make a living while twenty feet away, another newsletter writer, James Dines, had engaged two gorgeous, tall platinum blondes to man the booth, complete with jaw-dropping cleavages bursting from low-cut evening gowns. Lined up to subscribe to the vastly inferior Dines Letter were perhaps fifty to one hundred goggle-eyed “investors”, all male and all clamouring for a chance to stand and fill out the forms handed to them by ladies as they bent over lasciviously to deliver the papers. Eventually, Bishop’s research and diligence moved him to the pinnacle of his industry and when he retired in 2007, he was the heavyweight champion of the junior mining newsletter world with no one within miles of his title. That day, however, he was an afterthought as Dines ruled the venue.

I also recall the period in the mid-1990’s after Bob had delivered Dia Met Minerals ($0.60 to $60), Arequipa ($0.25 to $34.75), and Diamondfields ($0.25 to $160) and had several thousand paid subscribers as I was walking with him down one of the aisles at the convention centre when I said “Hey Bob, look behind you.” at which point we both turned to see a line of perhaps fifty or sixty promoters, investor relations executives, and seniors carrying shopping bags full of baseball caps, calendars, and key chains all waiting for a chance to catch Bob’s attention. I turned to him and said, “Nice entourage you’ve developed!”

PDAC can be a great source of networking and idea-generation, but with the advent and rise of social media and the internet, the value of the conference these days is catching up with old colleagues who have enough scars on their backs and faces to have earned the right of PDAC passage. Those Johnny-come-Latelys attending for the first time after dumping all of their crypto or artificial intelligence stocks have zero scars and little right to assume the role of “PDAC Member” despite the fact that they paid the fee and now have a name tag. Attendance in 2020 was 23,000 people, and after being strictly “virtual” in 2021, it has since grown to 27,000+ in 2025. This year, the estimates are for a full 30,000 or more people to be in attendance.

It should be remembered that there is a seasonal hangover just after the convention that can last for up to four months. In fact, one of the older veterans I used to speak with used to sell all of his junior mining issues and not take any phone calls until August. He once emailed me the results, and while this was back in 2011, it showed an uncanny track record of avoiding the summer doldrums in most years when interest in exploration and development issues waned, and prices retrenched right up until mid-August. His spreadsheet confirmed that the performance of the TSX Venture Exchange was inferior in most years between March and August but vastly superior between August and March. From my own years of experience, June and July can be problematic, but I always tried to focus on companies that had active catalysts attracting investor attention during those months, and have been fortunate to have benefited, for the most part.

I think that the trend of metal prices will have copper at the forefront at PDAC 2026, whereas last year it was gold and silver. I also believe that the rise in valuation for many of the mid-tier metal producers are going to force investors to move down the risk-curve to begin to include non-producers and favour the developers. That should favour those companies fortunate enough to have established an economic resource. As valuations increase for the developers, it will ultimately force investors to populate the bottom rung of the junior mining food chain — the explorers — and that is where the fun should start, and also, regrettably, mark the end of the cycle. When the junior explorers start to rise on rank speculation, that is when we will be exiting the space and raising cash.

As for the PDAC “curse” that has the TSXV regressing into a three to four month corrective phase, I will need to watch metal prices and energy to see if they can countermand the seasonal softness that accompanies the post-PDAC period.

My guess is that the developers may dodge the bullet, but that the seniors and mid-tier names trade flat or lower. I shall remain focused on those companies with solid stories and active catalysts, most of which are contained in the GGMA 2026 Trading and Portfolio accounts.

Important Disclosures:

- As of the date of this article, officers, contractors, shareholders, and/or employees of Streetwise Reports LLC (including members of their household) own securities of Fitzroy Minerals.

- Michael Ballanger: I, or members of my immediate household or family, own securities of: Fitzroy Minerals. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.