By InvestMacro

The latest update for the weekly Commitment of Traders (COT) report was released by the Commodity Futures Trading Commission (CFTC) on Friday for data ending on January 30th.

This weekly Extreme Positions report highlights the Most Bullish and Most Bearish Positions for the speculator category. Extreme positioning in these markets can foreshadow strong moves in the underlying market.

To signify an extreme position, we use the Strength Index (also known as the COT Index) of each instrument, a common method of measuring COT data. The Strength Index is simply a comparison of current trader positions against the range of positions over the previous 3 years. We use over 80 percent as extremely bullish and under 20 percent as extremely bearish. (Compare Strength Index scores across all markets in the data table or cot leaders table)

Here Are This Week’s Most Bullish Speculator Positions:

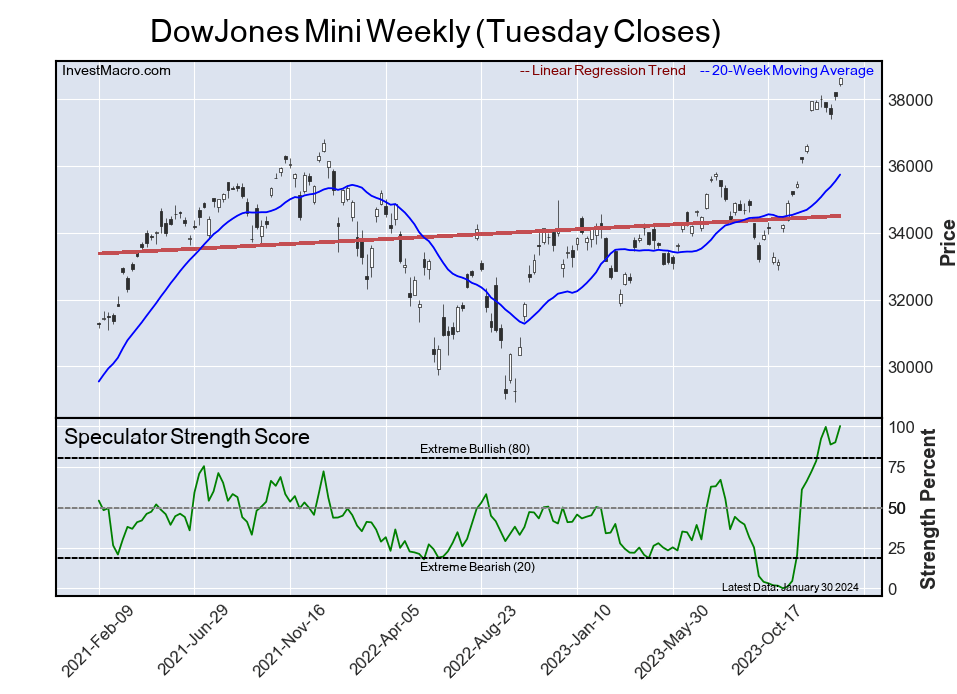

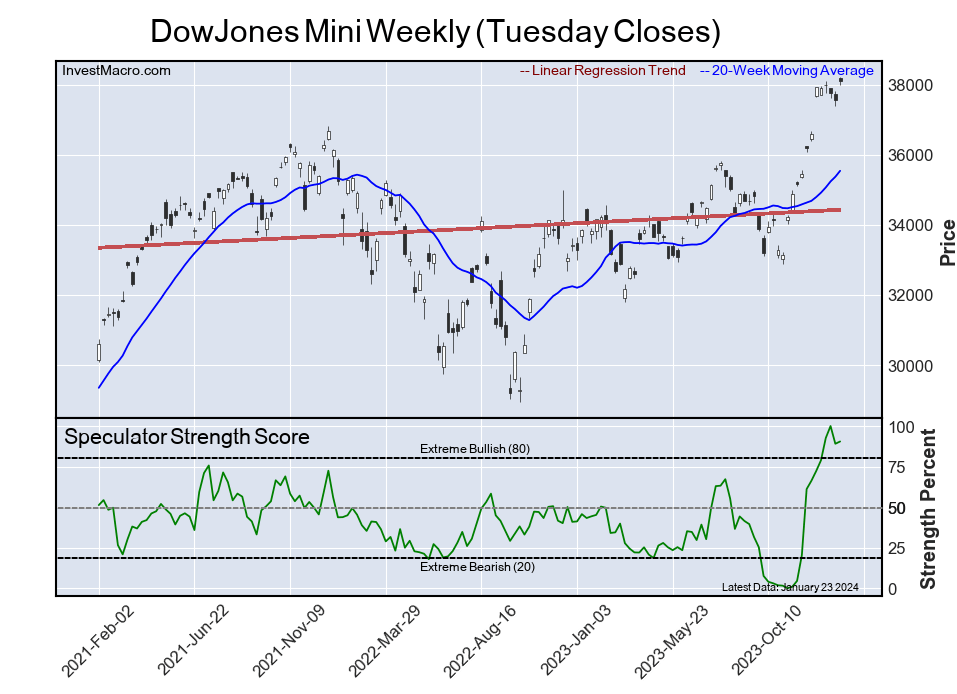

DowJones Mini

The DowJones Mini speculator position comes in as the most bullish extreme standing this week. The DowJones Mini speculator level is currently at a 100.0 percent score of its 3-year range.

The six-week trend for the percent strength score totaled 28.1 this week. The overall net speculator position was a total of 24,410 net contracts this week with a rise of 6,162 contract in the weekly speculator bets.

Speculators or Non-Commercials Notes:

Speculators, classified as non-commercial traders by the CFTC, are made up of large commodity funds, hedge funds and other significant for-profit participants. The Specs are generally regarded as trend-followers in their behavior towards price action – net speculator bets and prices tend to go in the same directions. These traders often look to buy when prices are rising and sell when prices are falling. To illustrate this point, many times speculator contracts can be found at their most extremes (bullish or bearish) when prices are also close to their highest or lowest levels.

These extreme levels can be dangerous for the large speculators as the trade is most crowded, there is less trading ammunition still sitting on the sidelines to push the trend further and prices have moved a significant distance. When the trend becomes exhausted, some speculators take profits while others look to also exit positions when prices fail to continue in the same direction. This process usually plays out over many months to years and can ultimately create a reverse effect where prices start to fall and speculators start a process of selling when prices are falling.

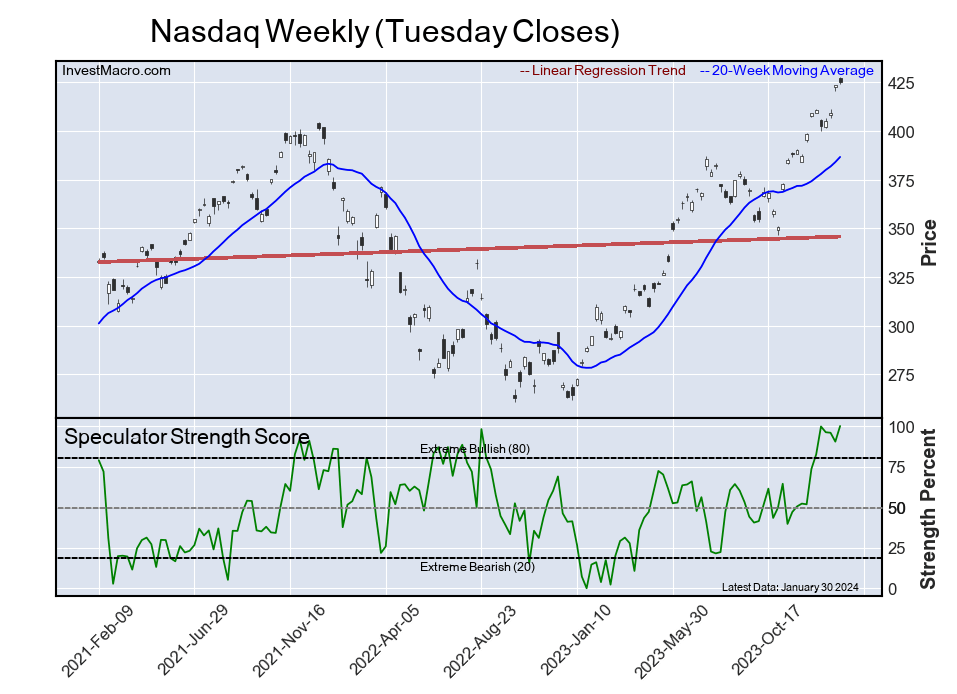

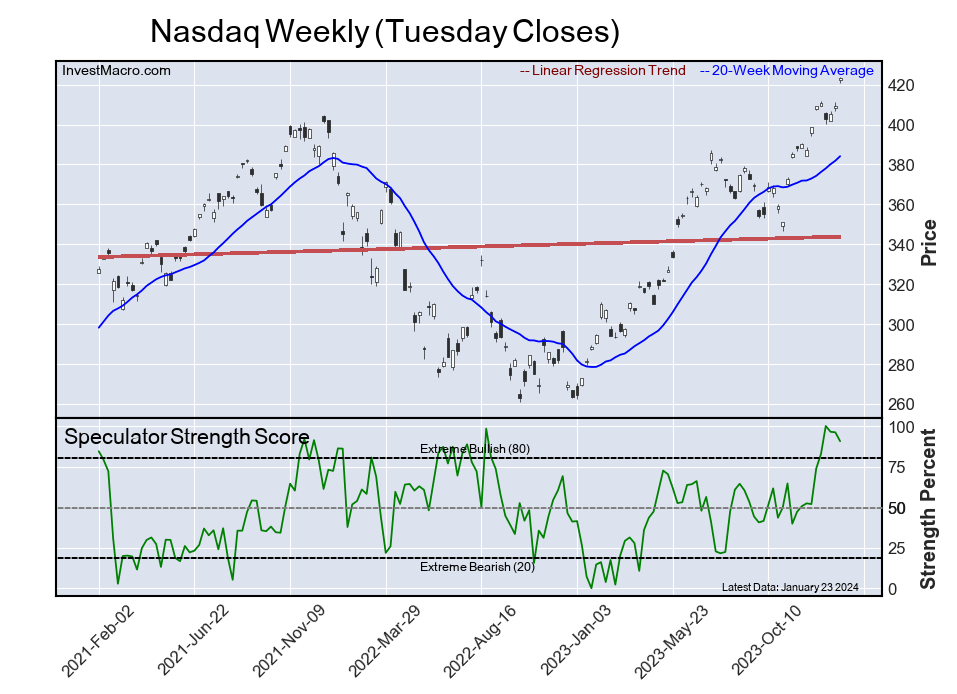

Nasdaq

The Nasdaq speculator position comes next in the extreme standings this week. The Nasdaq speculator level is now at a 100.0 percent score of its 3-year range.

The six-week trend for the percent strength score was 26.5 this week. The speculator position registered 39,251 net contracts this week with a weekly increase of 6,209 contracts in speculator bets.

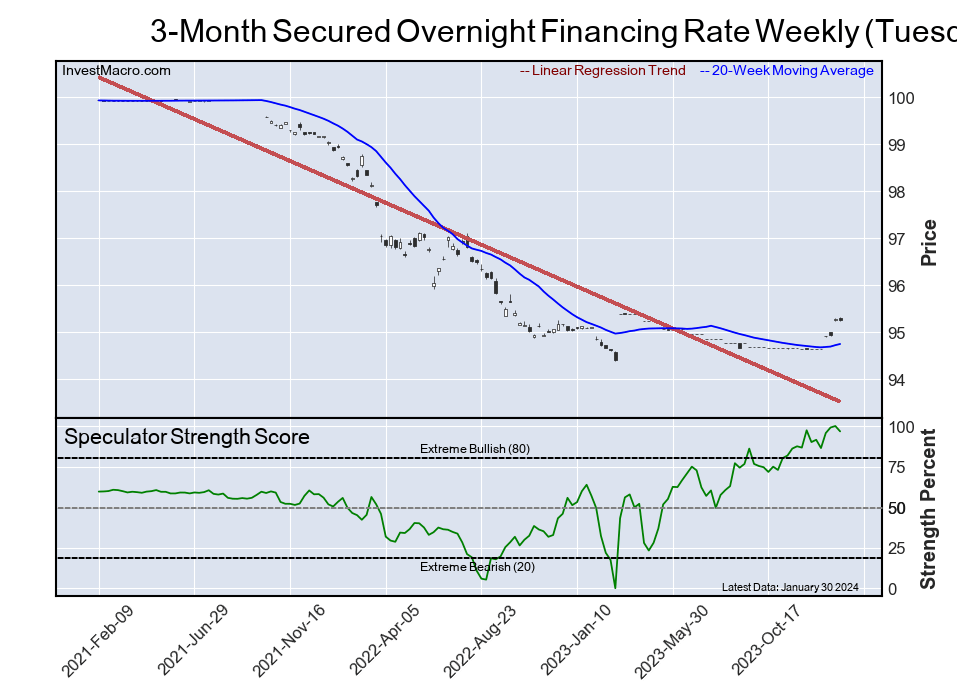

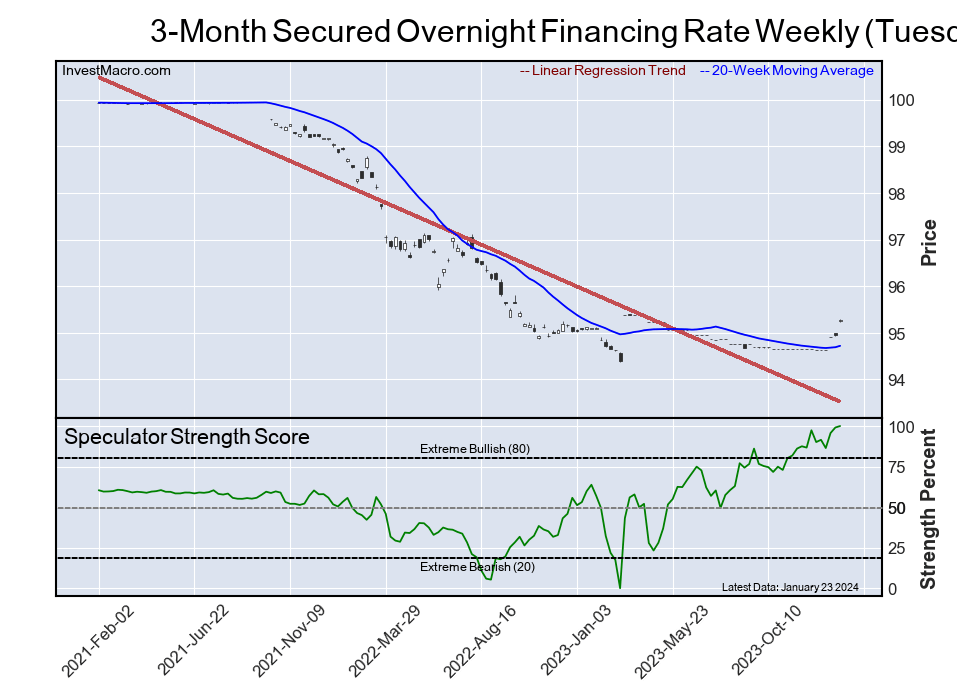

3-Month Secured Overnight Financing Rate

The 3-Month Secured Overnight Financing Rate speculator position comes in third this week in the extreme standings. The 3-Month Secured Overnight Financing Rate speculator level resides at a 96.7 percent score of its 3-year range.

The six-week trend for the speculator strength score came in at 6.6 this week. The overall speculator position was 705,145 net contracts this week with a decline of -64,042 contracts in the weekly speculator bets.

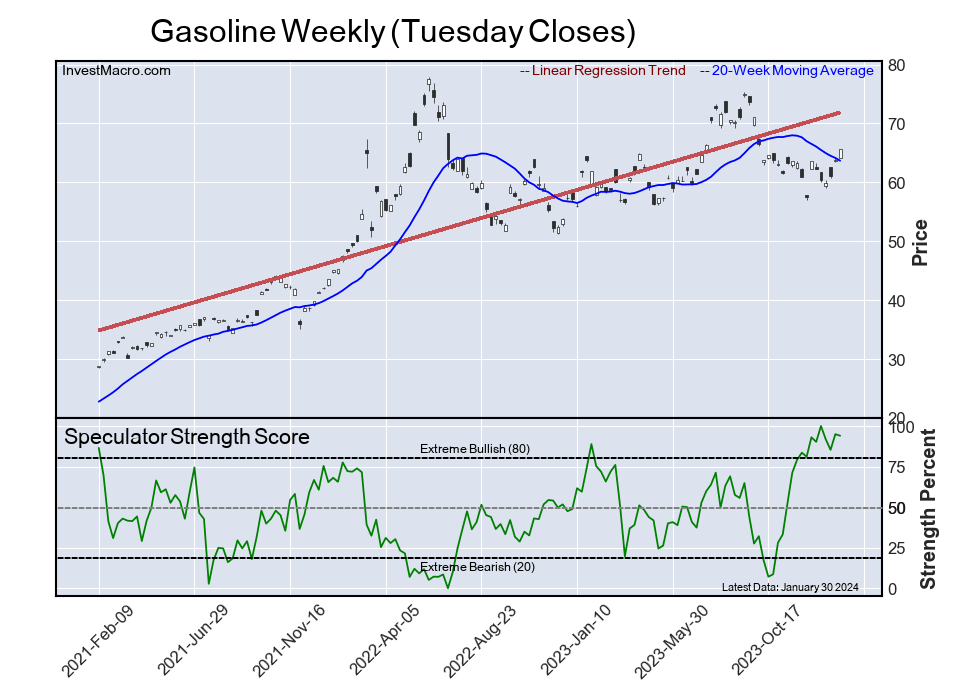

Gasoline

The Gasoline speculator position comes up number four in the extreme standings this week. The Gasoline speculator level is at a 94.0 percent score of its 3-year range.

The six-week trend for the speculator strength score totaled a change of 1.0 this week. The overall speculator position was 73,270 net contracts this week with a dip of -471 contracts in the speculator bets.

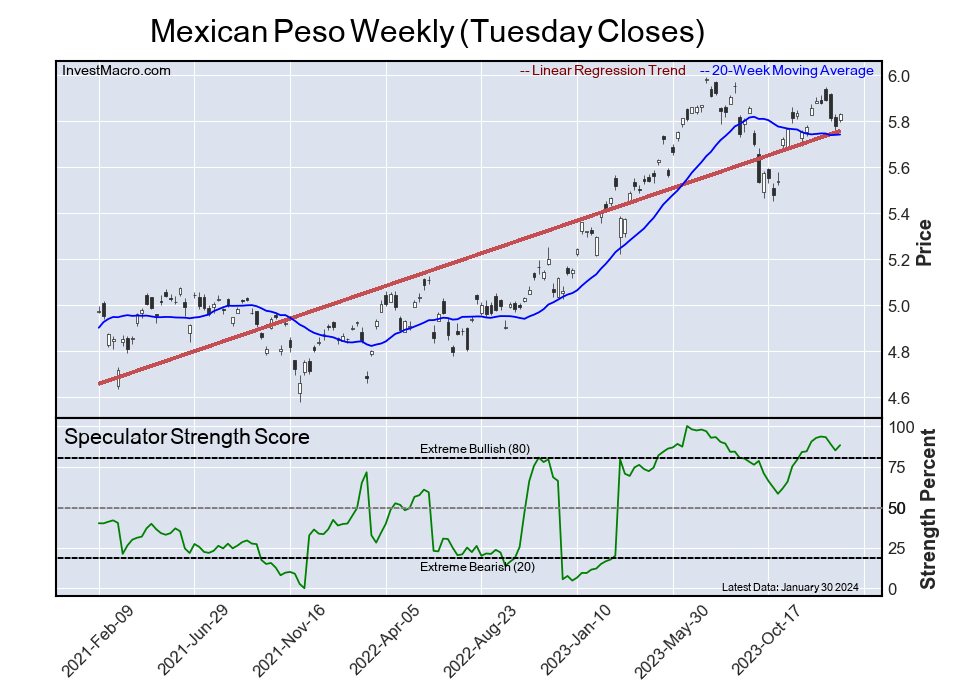

Mexican Peso

The Mexican Peso speculator position rounds out the top five in this week’s bullish extreme standings. The Mexican Peso speculator level sits at a 88.2 percent score of its 3-year range. The six-week trend for the speculator strength score was -2.2 this week.

The speculator position was 80,393 net contracts this week with an increase of 5,294 contracts in the weekly speculator bets.

This Week’s Most Bearish Speculator Positions:

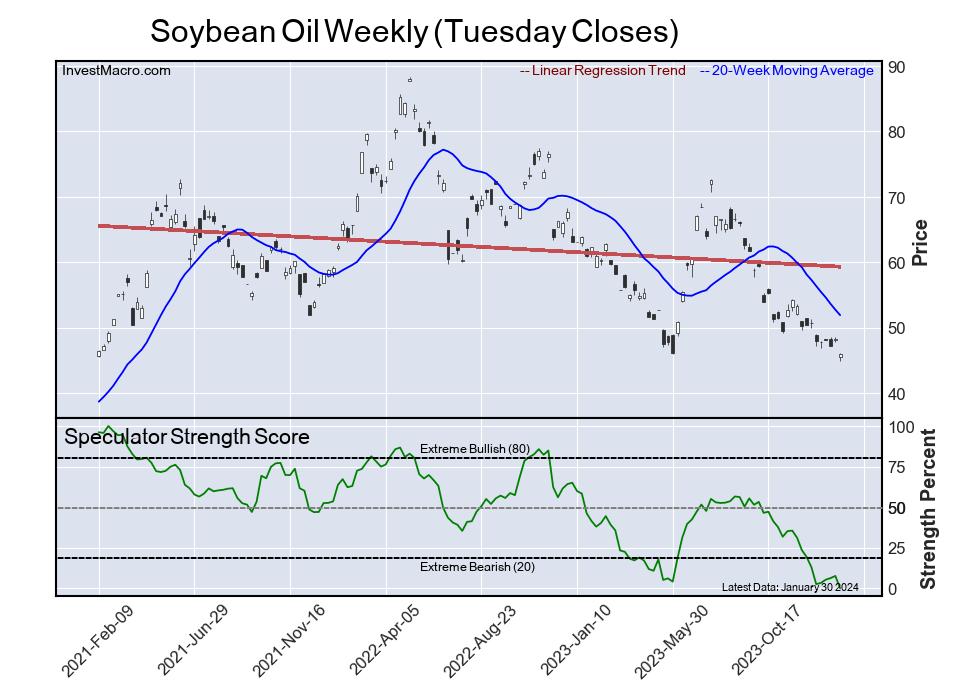

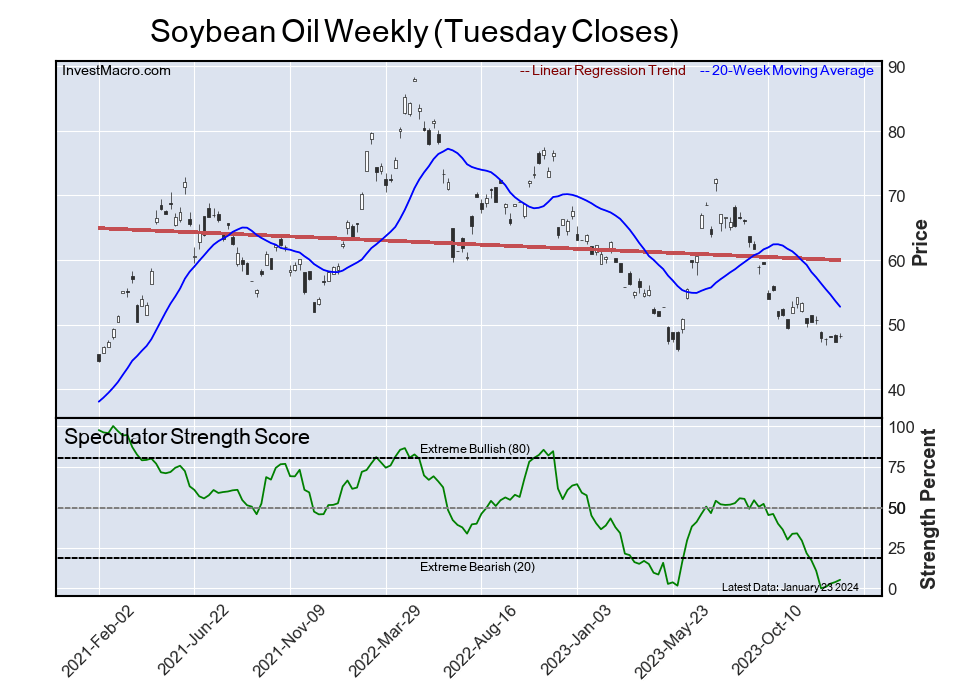

Soybean Oil

The Soybean Oil speculator position comes in as the most bearish extreme standing this week. The Soybean Oil speculator level is at a 0.0 percent score of its 3-year range.

The six-week trend for the speculator strength score was -13.0 this week. The overall speculator position was -38,035 net contracts this week with a drop of -12,677 contracts in the speculator bets.

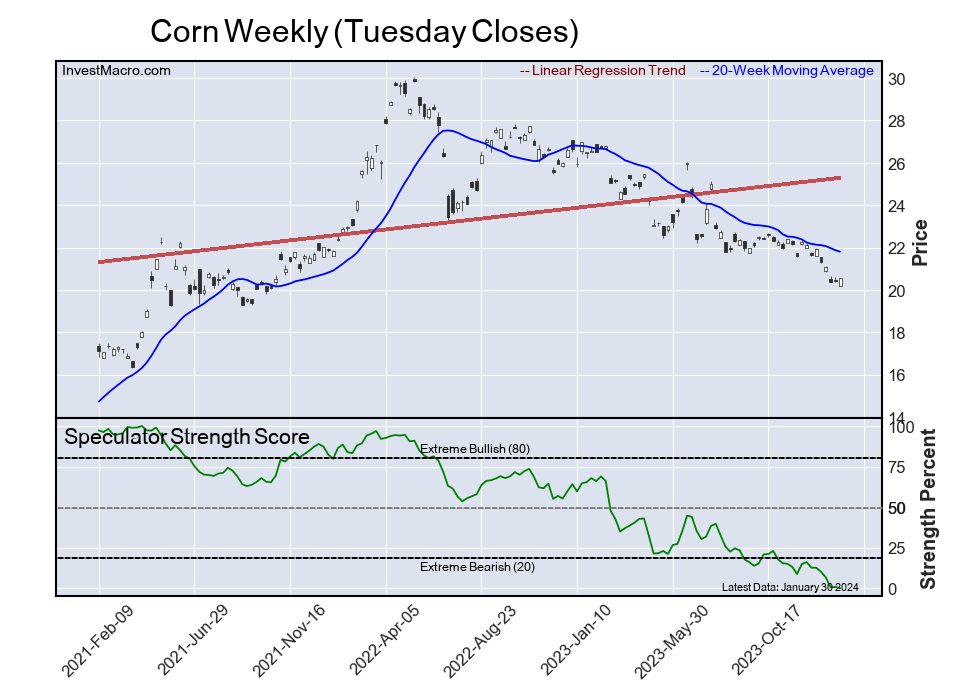

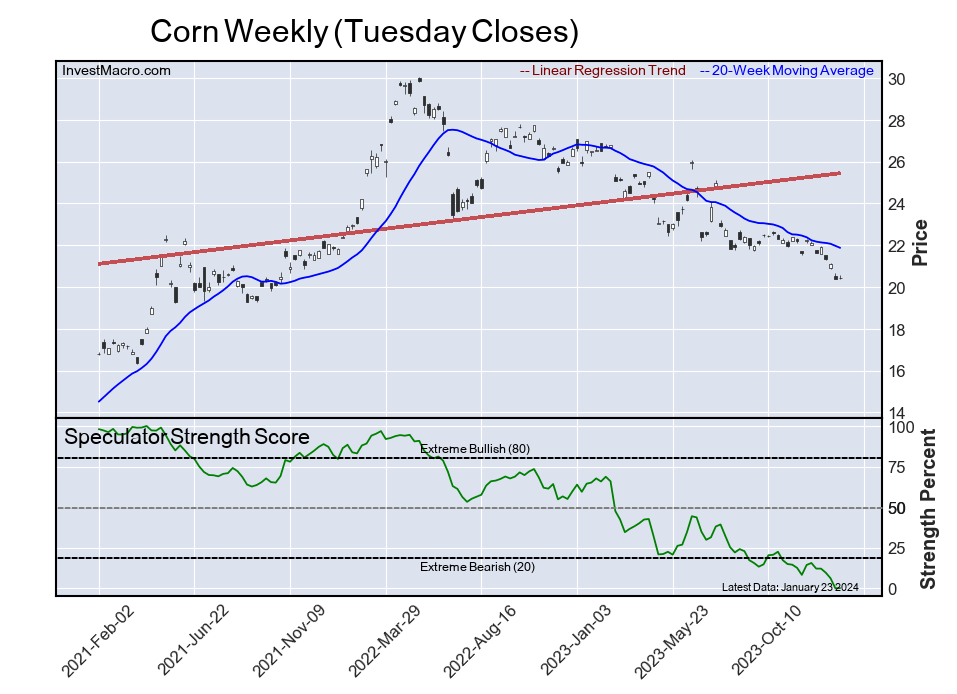

Corn

The Corn speculator position comes in next for the most bearish extreme standing on the week. The Corn speculator level is at a 0.0 percent score of its 3-year range.

The six-week trend for the speculator strength score was -12.7 this week. The speculator position was -224,832 net contracts this week with a decline of -5,632 contracts in the weekly speculator bets.

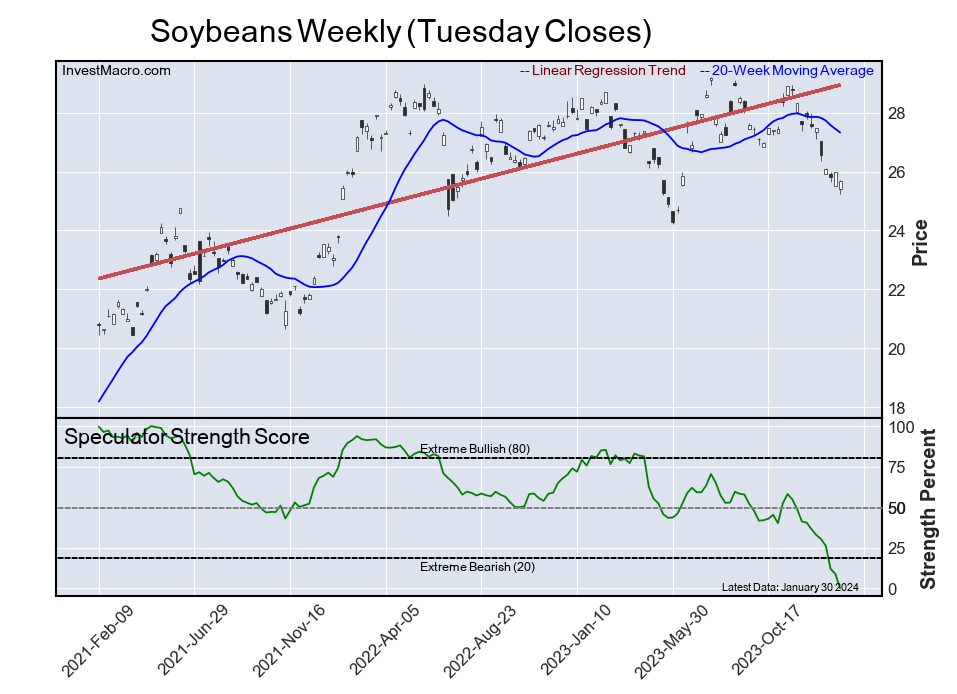

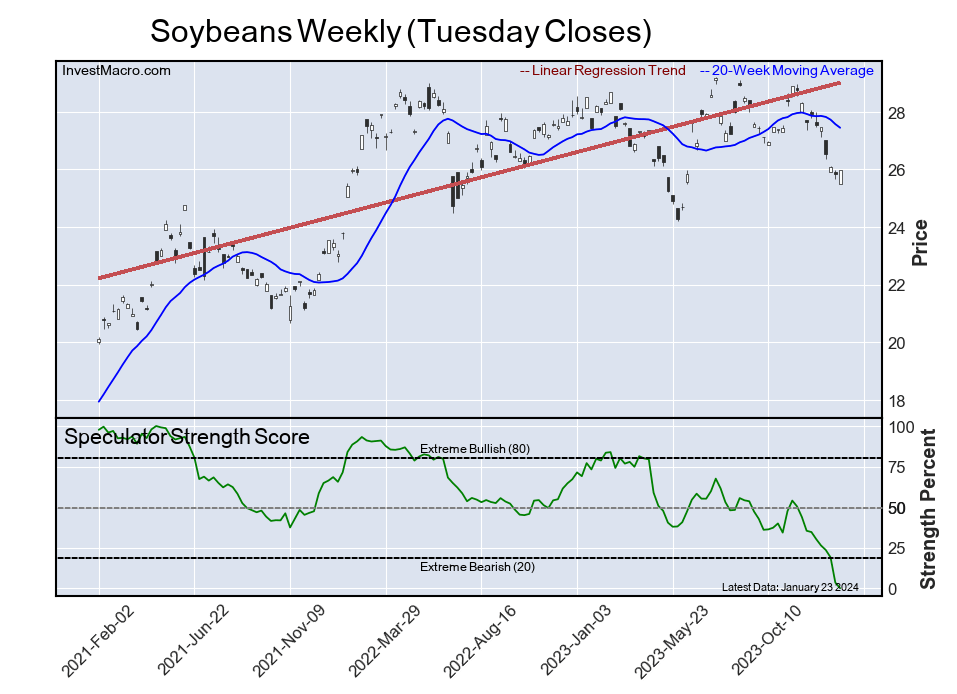

Soybeans

The Soybeans speculator position comes in as third most bearish extreme standing of the week. The Soybeans speculator level resides at a 0.0 percent score of its 3-year range.

The six-week trend for the speculator strength score was -36.4 this week. The overall speculator position was -140,577 net contracts this week with a reduction of -34,583 contracts in the speculator bets.

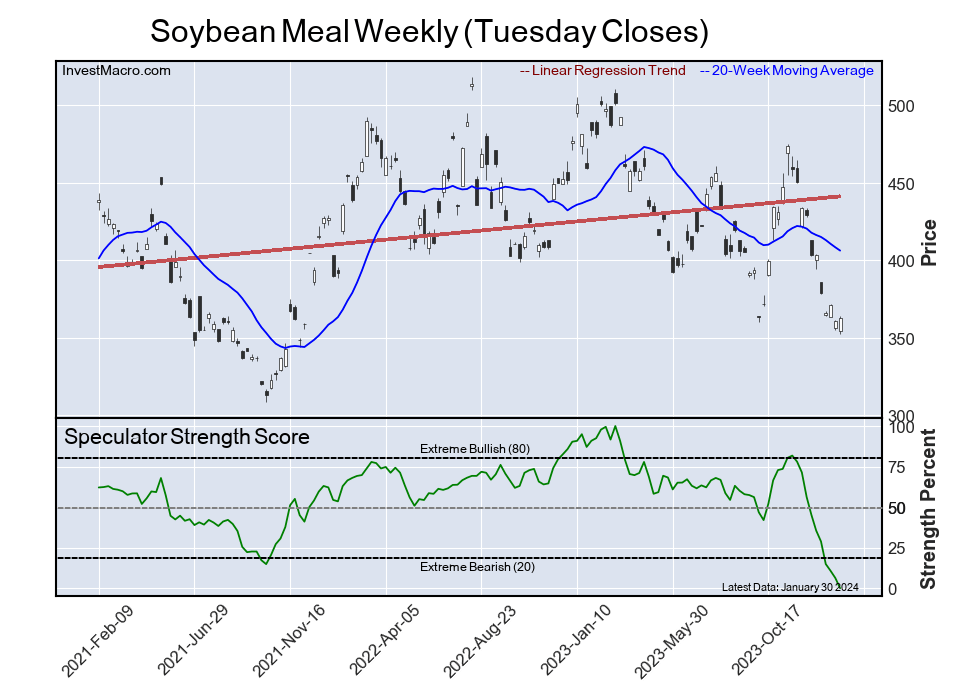

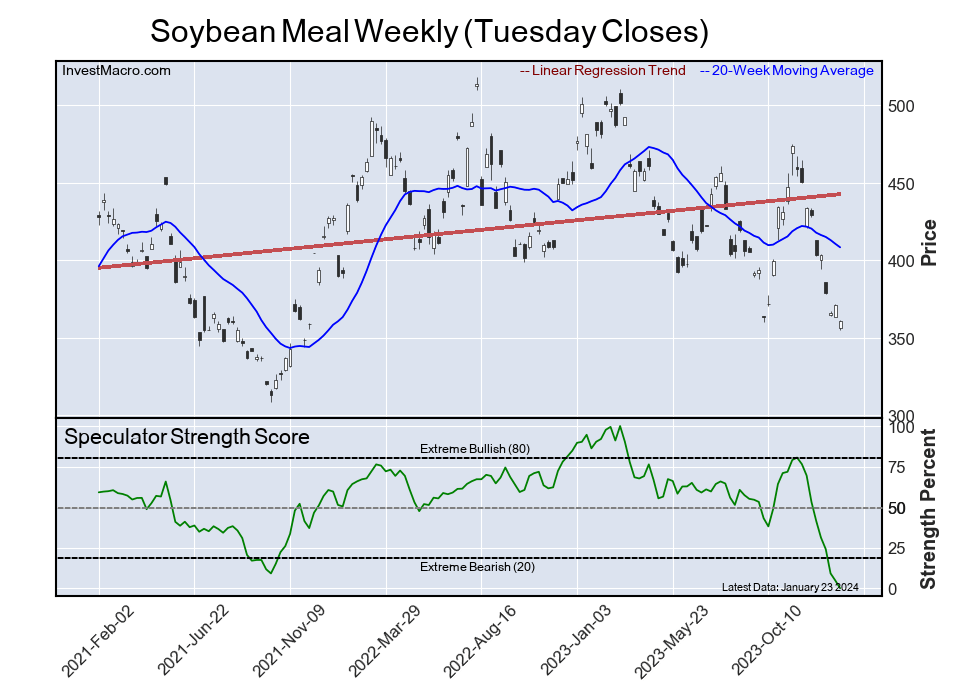

Soybean Meal

The Soybean Meal speculator position comes in as this week’s fourth most bearish extreme standing. The Soybean Meal speculator level is at a 0.0 percent score of its 3-year range.

The six-week trend for the speculator strength score was -45.2 this week. The speculator position was -33,932 net contracts this week with a shortfall of -13,316 contracts in the weekly speculator bets.

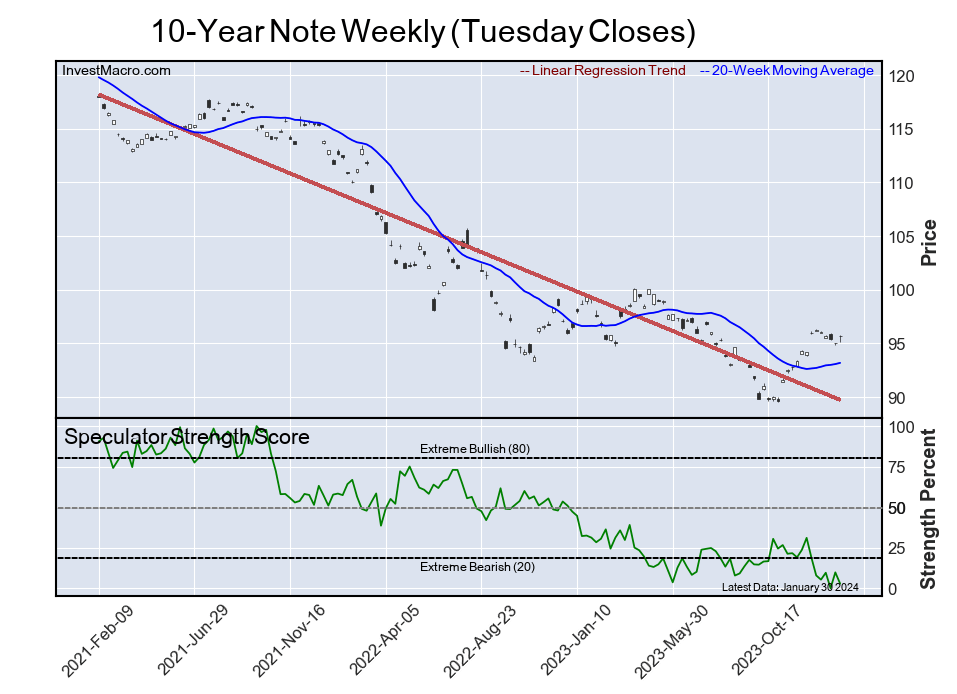

10-Year Note

Finally, the 10-Year Note speculator position comes in as the fifth most bearish extreme standing for this week. The 10-Year Note speculator level is at a 2.8 percent score of its 3-year range.

The six-week trend for the speculator strength score was -16.0 this week. The speculator position was -859,015 net contracts this week with a decline of -74,337 contracts in the weekly speculator bets.

Article By InvestMacro – Receive our weekly COT Newsletter

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators) as well as their open interest (contracts open in the market at time of reporting). See CFTC criteria here.

{kind=link}