By ForexTime

- RBA expected to HIKE interest rates

- BoC, Fed, BoJ, BoE, ECB, SNB and Riks seen leaving rates unchanged

- Central banks may express caution conflict-induced inflation shocks

- AUD expected to be the most volatile FX vs USD

- EURUSD, USDJPY & GBPUSD on breakout watch

Growing concerns around conflict-induced inflation shocks may prompt central banks to reassess their policy strategies for 2026.

The Federal Reserve (Fed), European Central Bank (ECB) and Bank of England (BoE), among many others will be under the spotlight in the week ahead.

These high-impact events will be complemented with ongoing geopolitical developments in the Middle East and top-tier data from across the globe:

Monday, 16th March

- CN50: China retail sales, industrial production

- USDInd: US Empire State manufacturing, industrial production

- Nvidia’s GTC – a global AI conference in California

Tuesday, 17th March

- AUD: RBA rate decision

- EUR: Germany ZEW survey expectations

- NZD: New Zealand food prices

Wednesday, 18th March

- CAD: BoC rate decision

- EUR: Eurozone CPI

- ZAR: South Africa CPI, retail sales

- USInd: Fed rate decision, PPI

Thursday, 19th March

- AUD: Australia unemployment

- JPY: BoJ rate decision

- EUR: ECB rate decision

- GBP: BoE rate decision

- CHF: SNB rate decision

- SEK: Riksbank rate decision

Friday, 20th March

- CAD: Canada retail sales

- CNY: China loan prime rates

- RUB: Russia rate decision

- US500: Quadruple witching in US markets

Before we take a deep dive, it’s worth keeping in mind that the ongoing conflict in the Middle East has rocked global sentiment and sparked fears of inflation shocks amid surging oil prices.

This may force central banks to adopt a more hawkish stance – meaning favoring higher rates to combat inflation.

Note: A quick central bank’s cheat sheet of what to expect in the week ahead. (Source Bloomberg)

Here are 8 assets that could be rocked by 8 central bank announcements:

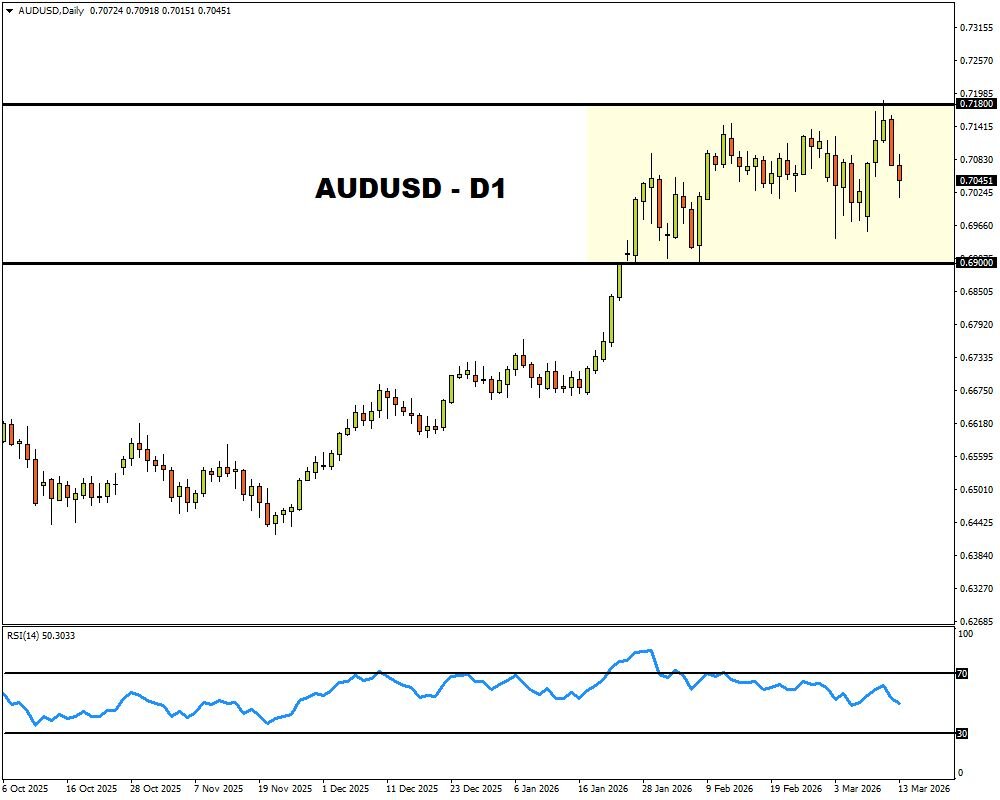

RBA meeting: AUDUSD

Traders are currently pricing a 65% chance that the RBA raises rates at its meeting on Tuesday 17th March.

This will be its second consecutive rate increase due to growing fears of conflict-induced inflation.

Note: The RBA decision is forecasted to trigger upside moves of as much as 0.5% up, or as much as 0.3% down in a 6-hour window post-release.

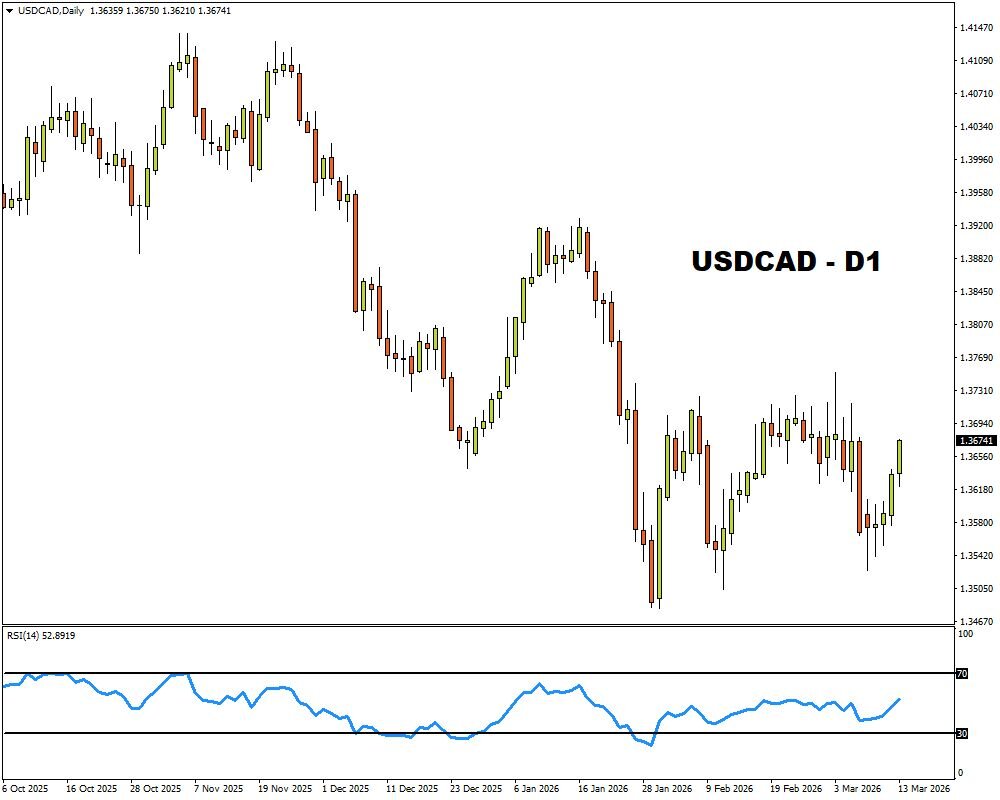

BoC meeting: USDCAD

The Bank of Canada is expected to leave rates unchanged at its meeting on 18th March.

However, any hint of potential rate hikes down the road to combat inflation may support the CAD which has already been boosted by surging oil prices.

Note: The BoC decision is forecasted to trigger upside moves of as much as 0.2% up, or as much as 0.5% down in a 6-hour window post-release.

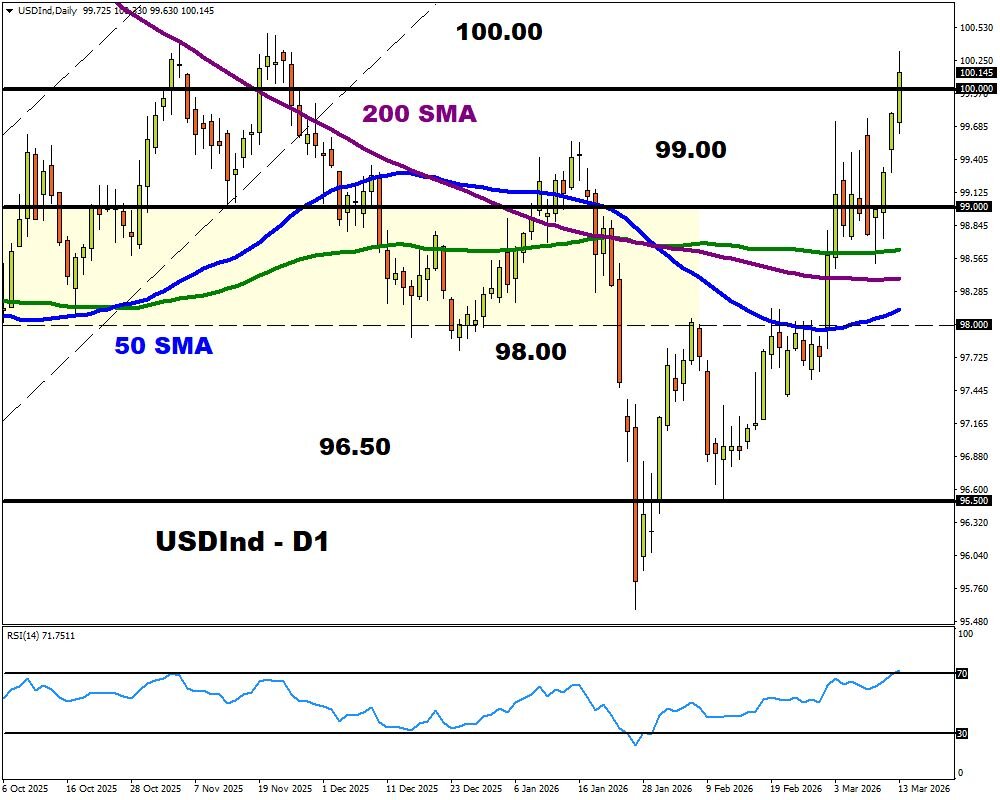

Fed meeting: USDInd

Market expectations have rapidly evaporated over the Fed cutting rates anytime soon with traders pricing a 75% chance of just one Fed cut in 2026.

The dollar is likely to surge further if the Fed strikes a hawkish note during its meeting on 18th March.

Note: The Fed decision is forecasted to trigger upside moves of as much as 0.4% up, or as much as 0.3% down in a 6-hour window post-release.

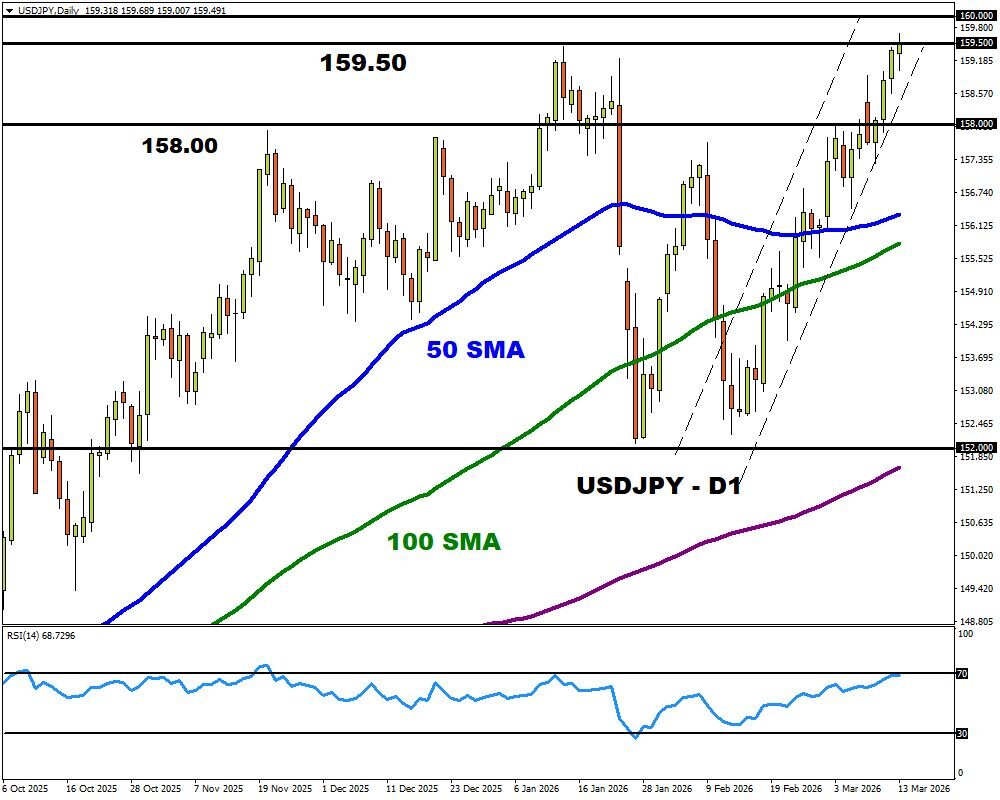

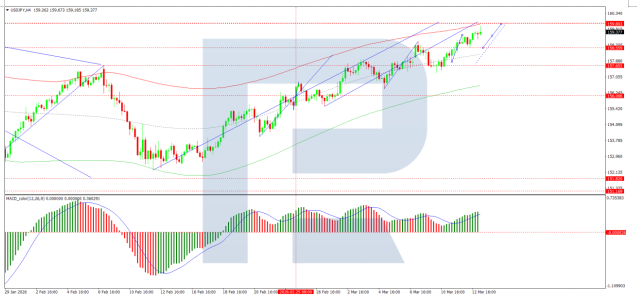

BoJ meeting: USDJPY

As the USDJPY ventures back into danger zones, traders are on high alert for any signs of potential intervention.

No changes are expected to interest rates but any clues about future policy moves may rock the USDJPY.

Note: The BoJ decision is forecasted to trigger upside moves of as much as 0.8% up, or as much as 0.1% down in a 6-hour window post-release.

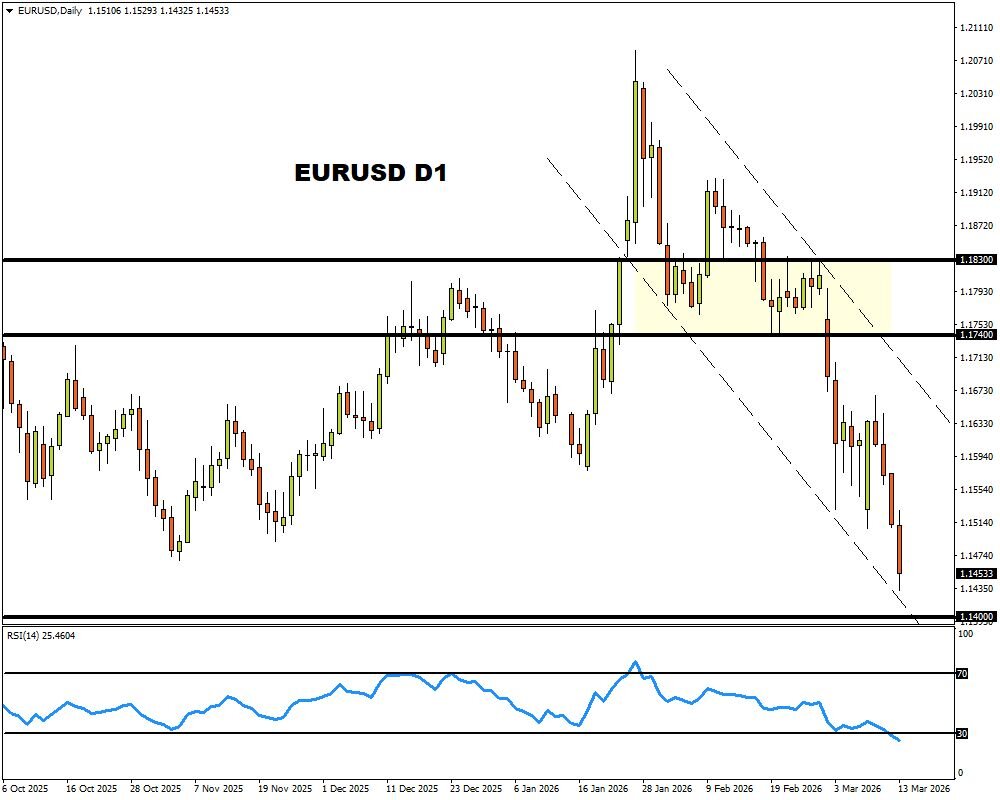

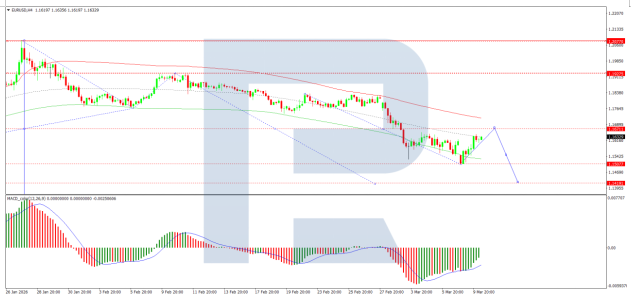

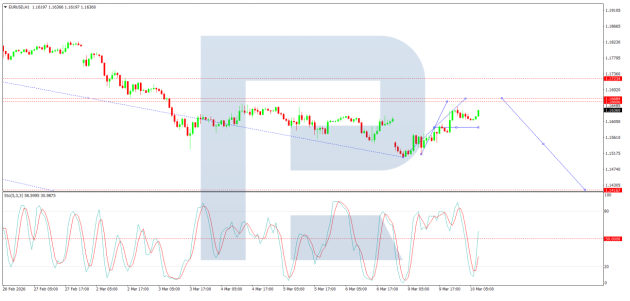

ECB meeting: EURUSD

No changes are expected to interest rates when the ECB meets, but any hints about potential rate hikes in 2026 may boost the euro.

Note: The ECB decision is forecasted to trigger upside moves of as much as 0.3% up, or as much as 0.2% down in a 6-hour window post-release.

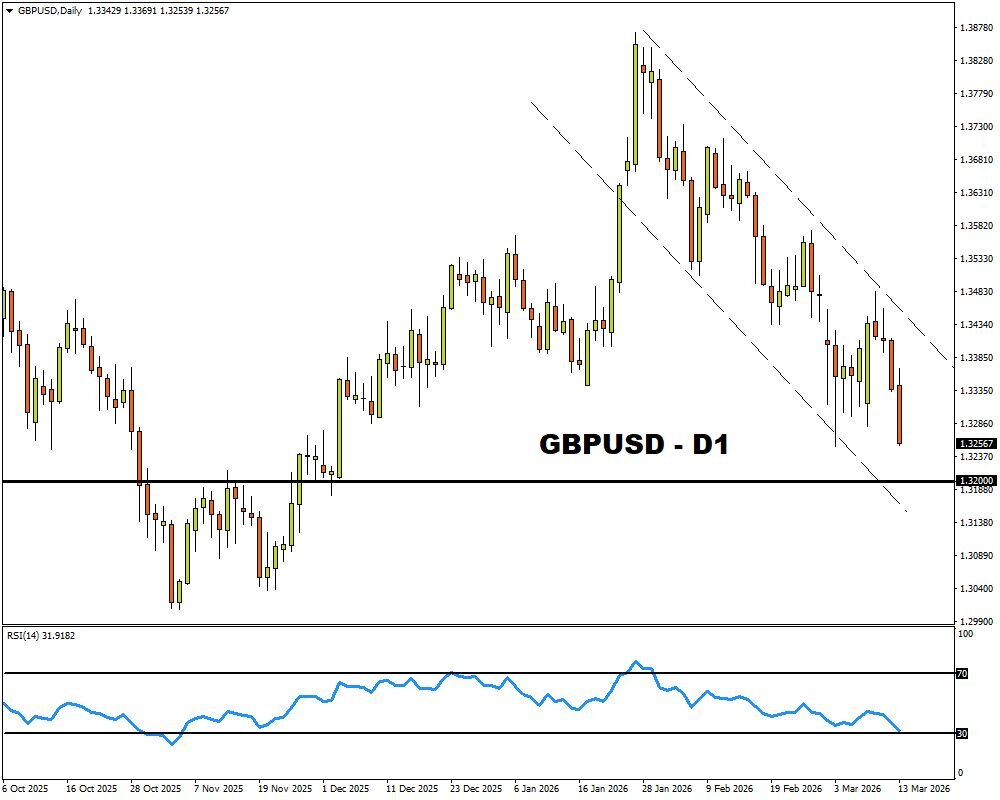

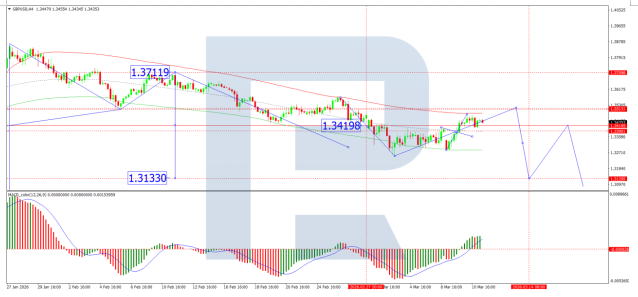

BoE meeting: GBPUSD

Fears of rising inflation have frightened away BoE doves with hawks likely to dominate the scene when the central bank meets on Thursday 19th March.

Note: The BoE decision is forecasted to trigger upside moves of as much as 0.3% up, or as much as 0.3% down in a 6-hour window post-release.

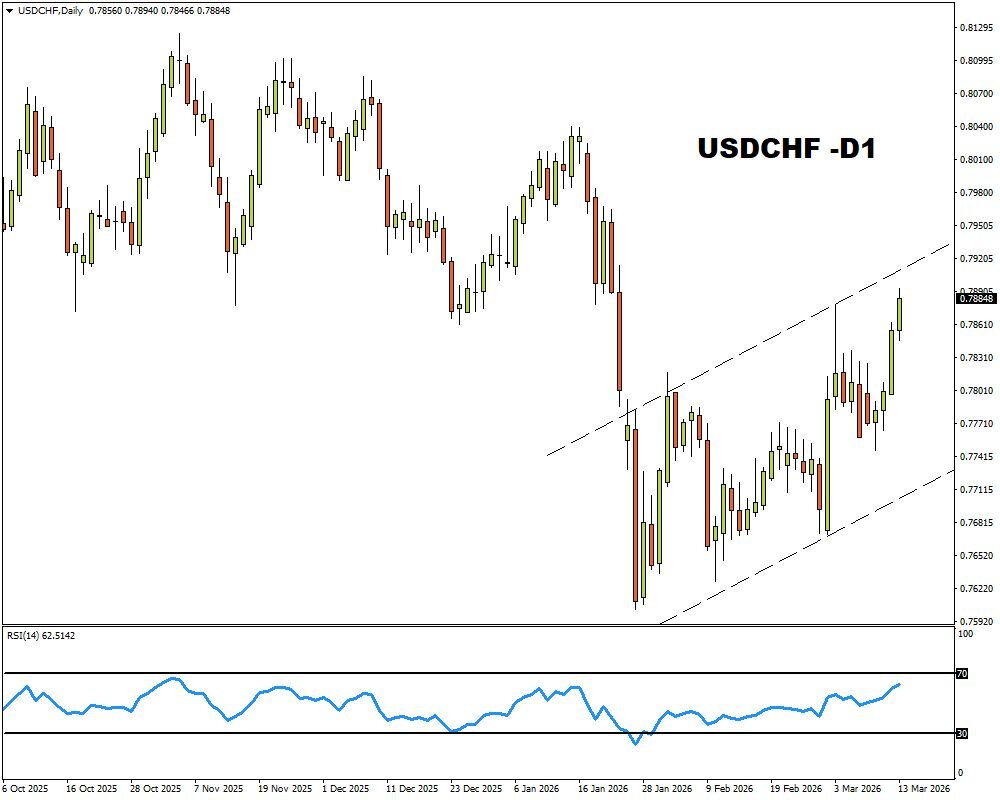

SNB meeting: USDCHF

The Swiss National Bank is expected to leave rates unchanged at its meeting on 19th March.

Note: The SNB decision is forecasted to trigger upside moves of as much as 0.5% up, or as much as 0.4% down in a 6-hour window post-release.

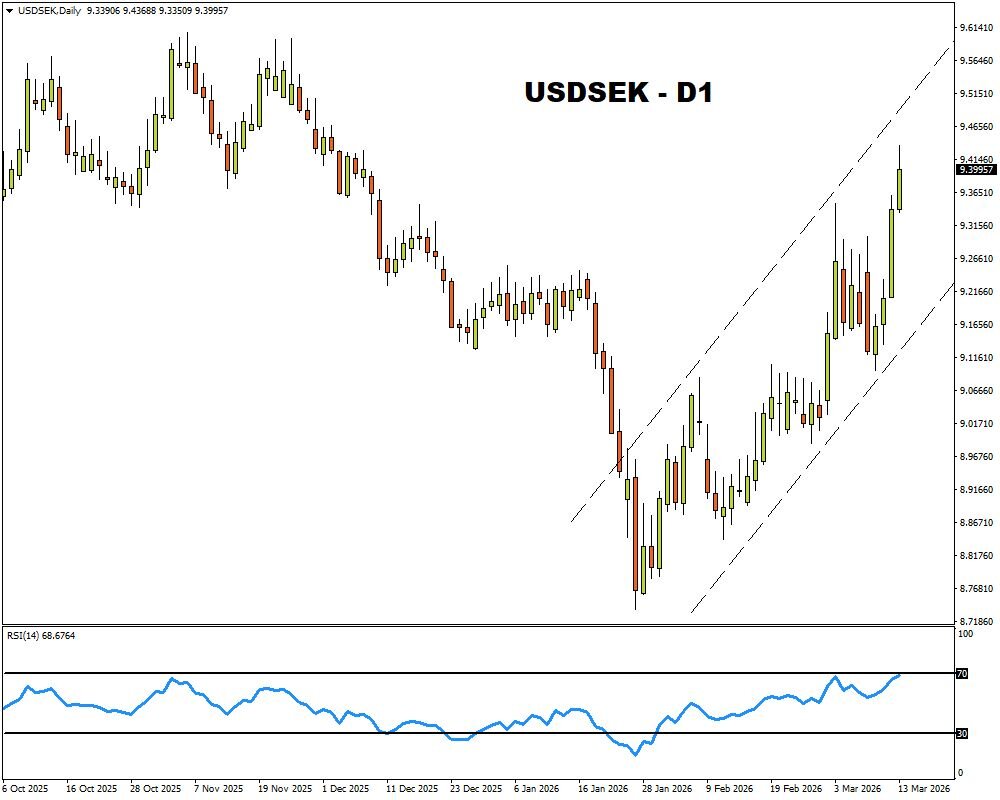

Riksbank meeting: USDSEK

Sweden’s Riksbank will also keep rates unchanged, with a rate hike down the road a possibility amid inflation fears.

Note: The Riksbank decision is forecasted to trigger upside moves of as much as 0.4% up, or as much as 0.4% down in a 6-hour window post-release.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

A mechanical claw holds a polymetallic nodule, one of several seafloor sources of critical minerals.

A mechanical claw holds a polymetallic nodule, one of several seafloor sources of critical minerals.

{kind=link}

{kind=link}