By InvestMacro

Here are the latest charts and statistics for the Commitment of Traders (COT) data published by the Commodities Futures Trading Commission (CFTC).

The latest COT data is updated through Tuesday May 7th and shows a quick view of how large market participants (for-profit speculators and commercial traders) were positioned in the futures markets. All currency positions are in direct relation to the US dollar where, for example, a bet for the euro is a bet that the euro will rise versus the dollar while a bet against the euro will be a bet that the euro will decline versus the dollar.

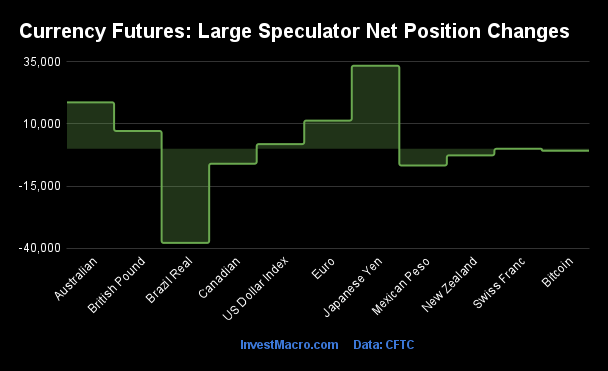

Weekly Speculator Changes led by Japanese Yen & Australian Dollar

The COT currency market speculator bets were slightly lower this week as five out of the eleven currency markets we cover had higher positioning while the other six markets had lower speculator contracts.

Leading the gains for the currency markets was the Japanese Yen (33,466 contracts) with the Australian Dollar (18,719 contracts), the EuroFX (11,367 contracts), the British Pound (7,177 contracts) and the US Dollar Index (1,888 contracts) also showing a positive week.

The currencies with declines in speculator bets on the week were the Brazilian Real (-37,929 contracts), the Mexican Peso (-6,733 contracts), the Canadian Dollar (-6,020 contracts), the New Zealand Dollar (-2,640 contracts), Bitcoin (-789 contracts) and the Swiss Franc (-1 contract) also registering lower bets on the week.

Speculators boost Yen bets, bring Euro, USD Index out of bearish levels

Highlighting the COT currency’s data this week is that both the Euro and the US dollar index speculator positions were modestly boosted out of their bearish levels into small positive positions. Also, the Japanese yen and Australian dollar positions were well bid through Tuesday.

Here is this week’s COT currency roundup:

The Japanese yen contracts jumped this week by over +33,000 contracts which marked the highest one-week amount since 2020. The yen speculator position has now gained for two weeks in a row amid rumored currency intervention by the Japanese authorities that are trying to arrest deep declines in the yen. The USDJPY currency pair still trades over 155.00 which is close to over thirty-year highs for the US dollar against the yen.

The Australian dollar speculator position rose strongly this week by over +18,000 contracts following a boost by +13,004 contracts on April 30th. The AUD speculator bets have now gained for three straight weeks and for six out of the past seven weeks. Recently, the speculator position for the Aussie had dropped to an all-time record low on March 19th at a total of -107,538 contracts. Since then, speculator bets have improved significantly and are currently at -64,516 contracts.

The Euro bounced back again this week with a gain of +11,367 contracts and a follows up a small rise last week. The improvement in the overall net position has brought the speculative standing back into bullish territory following two straight weeks in bearish territory. That was the first time the Euro contracts had been in bearish territory since September of 2022.

The US dollar index bets also came out of bearish territory this week for the first time in seven weeks. The USD Index bets rose by 1,888 contracts and gained for the fifth straight week. The contracts had been in bullish territory for a total of 142 straight weeks before dropping into a bearish position on March 26th.

The Mexican Peso speculative position decreased this week for a fourth straight week but did so modestly (-6,733 contracts) and remains in a strong bullish level. The MXN speculator’s current standing (+112,312 contracts) remains above +100,000 contract level for 1oth consecutive week. The MXN peso exchange rate has bounced back with gains in the past two weeks after a steep pullback in the middle of April.

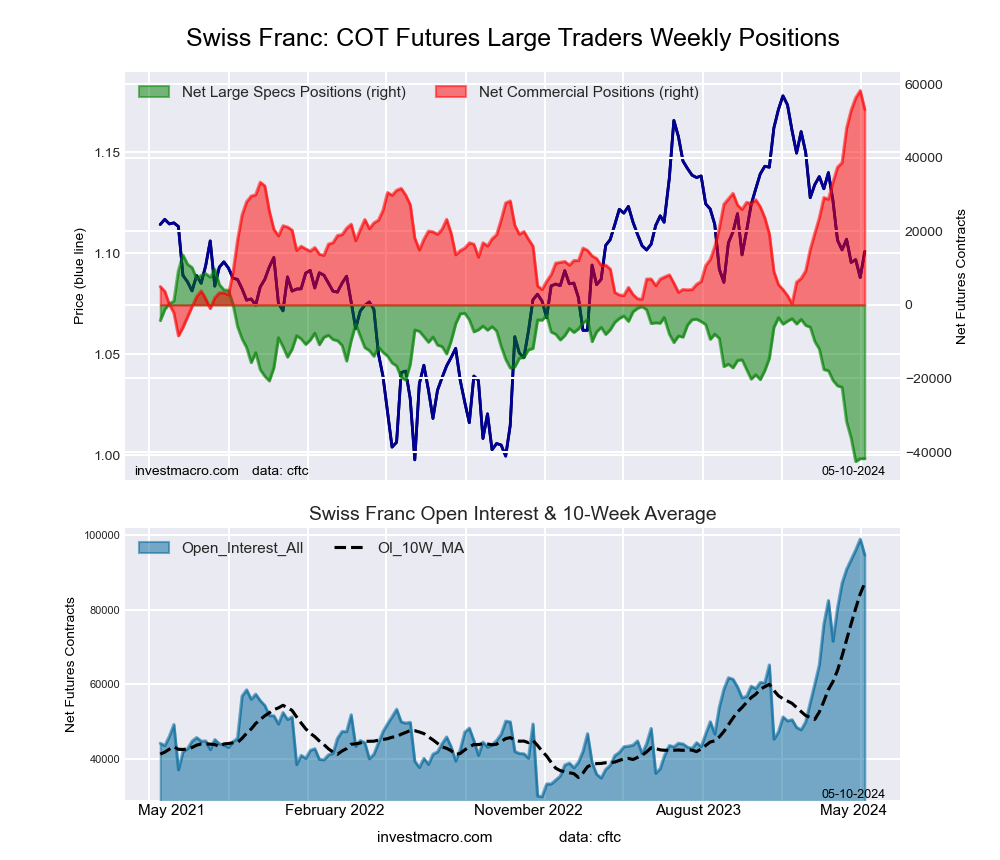

The Swiss franc position was virtually unchanged this week (-1 contract) but continues to remain near the lowest levels since 2019 at a total of -41,787 contracts. The franc is one of the most extremely bearish markets in the COT data we follow. The franc’s exchange rate against the US dollar has been on the decline with an approximate drop by over 8 percent since December 2023. The CHFUSD currently trades around the major levels near 1.1050 – 1.1100.

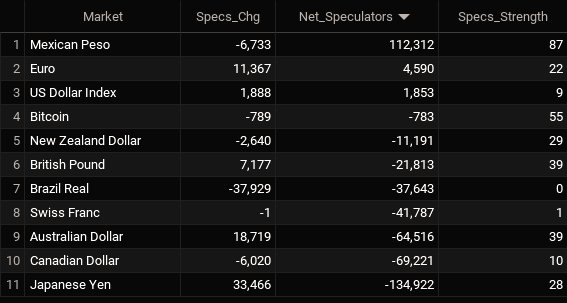

Currencies Net Speculators Leaderboard

Legend: Weekly Speculators Change | Speculators Current Net Position | Speculators Strength Score compared to last 3-Years (0-100 range)

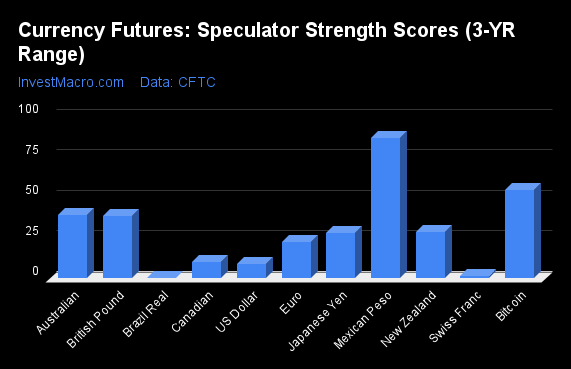

Strength Scores led by Mexican Peso & Bitcoin

COT Strength Scores (a normalized measure of Speculator positions over a 3-Year range, from 0 to 100 where above 80 is Extreme-Bullish and below 20 is Extreme-Bearish) showed that the Mexican Peso (87 percent) and the Bitcoin (55 percent) lead the currency markets this week. The British Pound (39 percent), Australian Dollar (39 percent) and the New Zealand Dollar (29 percent) come in as the next highest in the weekly strength scores.

On the downside, the Brazilian Real (0 percent) and the Swiss Franc (1 percent) come in at the lowest strength levels currently and are in Extreme-Bearish territory (below 20 percent). The next lowest strength scores are the US Dollar Index (9 percent) and the Canadian Dollar (10 percent).

Strength Statistics:

US Dollar Index (8.8 percent) vs US Dollar Index previous week (4.8 percent)

EuroFX (22.3 percent) vs EuroFX previous week (17.4 percent)

British Pound Sterling (38.8 percent) vs British Pound Sterling previous week (34.1 percent)

Japanese Yen (28.1 percent) vs Japanese Yen previous week (7.2 percent)

Swiss Franc (1.4 percent) vs Swiss Franc previous week (1.4 percent)

Canadian Dollar (10.3 percent) vs Canadian Dollar previous week (14.9 percent)

Australian Dollar (38.9 percent) vs Australian Dollar previous week (22.0 percent)

New Zealand Dollar (28.6 percent) vs New Zealand Dollar previous week (36.1 percent)

Mexican Peso (86.6 percent) vs Mexican Peso previous week (89.9 percent)

Brazilian Real (0.0 percent) vs Brazilian Real previous week (43.0 percent)

Bitcoin (54.6 percent) vs Bitcoin previous week (66.5 percent)

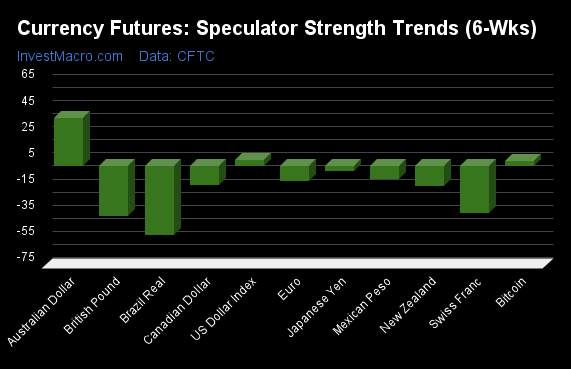

Australian Dollar & US Dollar Index top the 6-Week Strength Trends

COT Strength Score Trends (or move index, calculates the 6-week changes in strength scores) showed that the Australian Dollar (37 percent) and the US Dollar Index (5 percent) lead the past six weeks trends for the currencies. The Bitcoin (4 percent), the Japanese Yen (-4 percent) and the Mexican Peso (-10 percent) are the next highest positive movers in the latest trends data.

The Brazilian Real (-53 percent) leads the downside trend scores currently with the British Pound (-38 percent), Swiss Franc (-35 percent) and the New Zealand Dollar (-15 percent) following next with lower trend scores.

Strength Trend Statistics:

US Dollar Index (5.2 percent) vs US Dollar Index previous week (-1.5 percent)

EuroFX (-11.3 percent) vs EuroFX previous week (-23.5 percent)

British Pound Sterling (-37.8 percent) vs British Pound Sterling previous week (-54.5 percent)

Japanese Yen (-3.6 percent) vs Japanese Yen previous week (-32.8 percent)

Swiss Franc (-35.3 percent) vs Swiss Franc previous week (-37.9 percent)

Canadian Dollar (-14.4 percent) vs Canadian Dollar previous week (-19.8 percent)

Australian Dollar (37.0 percent) vs Australian Dollar previous week (22.0 percent)

New Zealand Dollar (-14.7 percent) vs New Zealand Dollar previous week (-23.7 percent)

Mexican Peso (-9.7 percent) vs Mexican Peso previous week (-4.7 percent)

Brazilian Real (-52.6 percent) vs Brazilian Real previous week (-11.4 percent)

Bitcoin (4.4 percent) vs Bitcoin previous week (31.6 percent)

Individual COT Forex Markets:

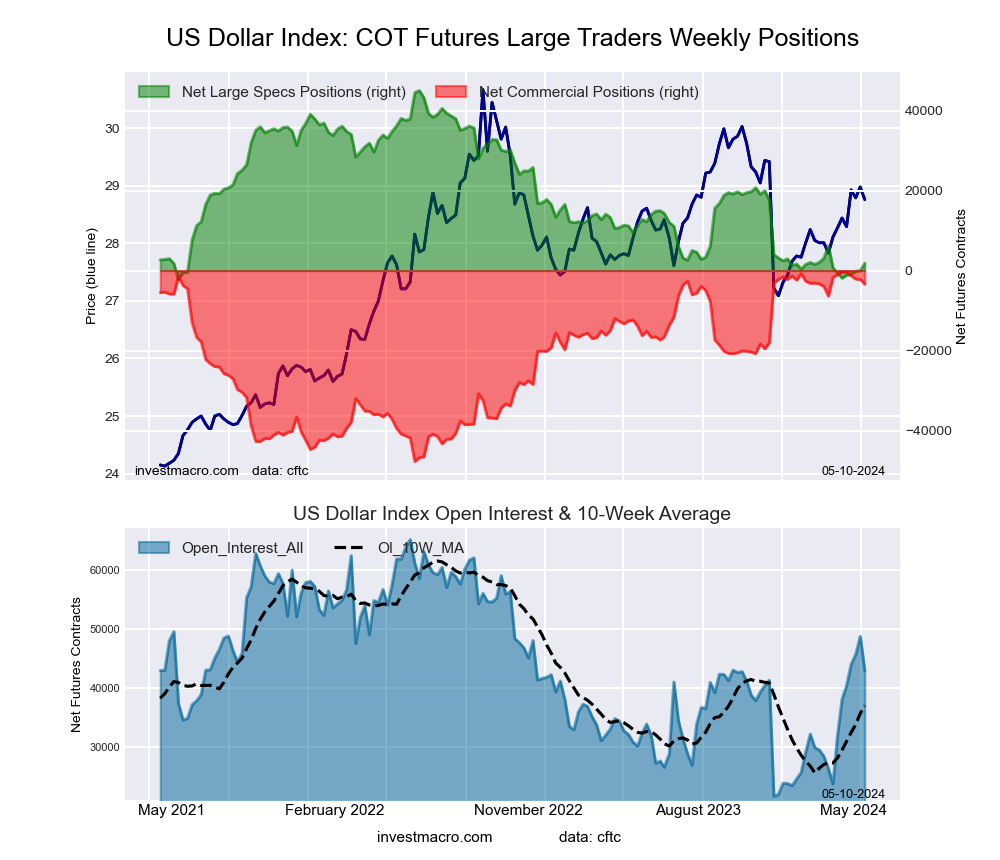

US Dollar Index Futures:

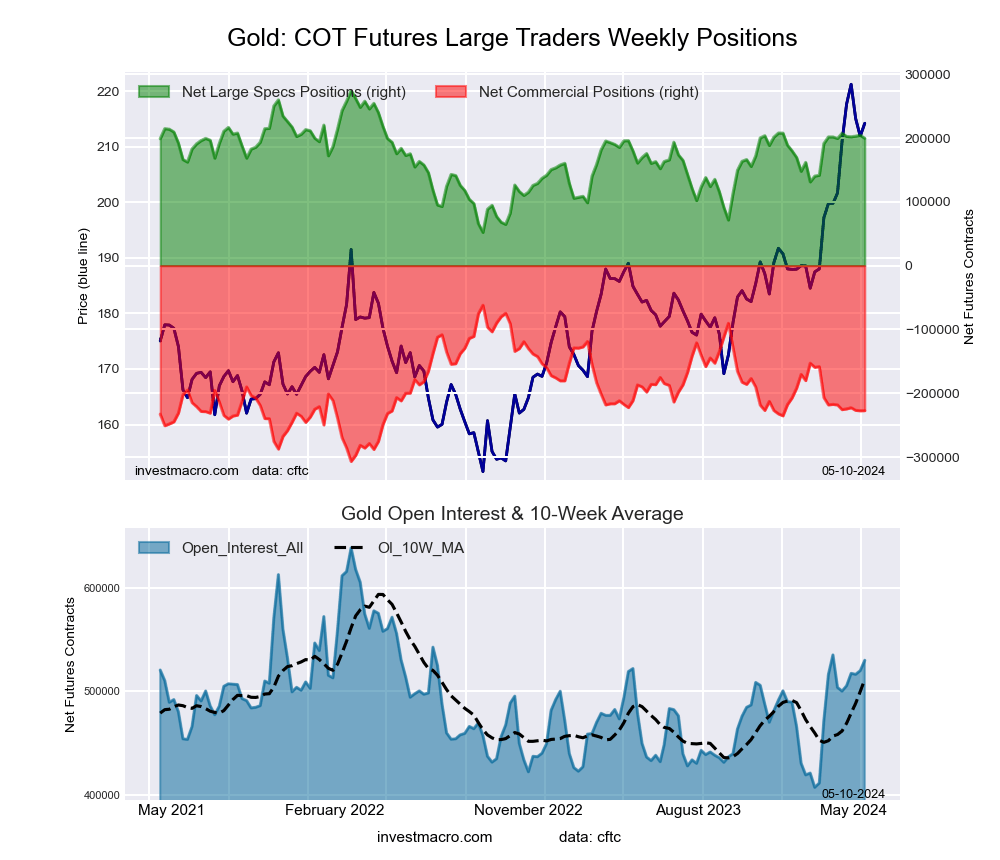

The US Dollar Index large speculator standing this week reached a net position of 1,853 contracts in the data reported through Tuesday. This was a weekly increase of 1,888 contracts from the previous week which had a total of -35 net contracts.

The US Dollar Index large speculator standing this week reached a net position of 1,853 contracts in the data reported through Tuesday. This was a weekly increase of 1,888 contracts from the previous week which had a total of -35 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 8.8 percent. The commercials are Bullish-Extreme with a score of 93.5 percent and the small traders (not shown in chart) are Bearish with a score of 29.1 percent.

Price Trend-Following Model: Uptrend

Our weekly trend-following model classifies the current market price position as: Uptrend. The current action for the model is considered to be: Hold – Maintain Long Position.

| US DOLLAR INDEX Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 67.2 | 21.6 | 8.7 |

| – Percent of Open Interest Shorts: | 62.9 | 29.4 | 5.2 |

| – Net Position: | 1,853 | -3,392 | 1,539 |

| – Gross Longs: | 28,881 | 9,260 | 3,753 |

| – Gross Shorts: | 27,028 | 12,652 | 2,214 |

| – Long to Short Ratio: | 1.1 to 1 | 0.7 to 1 | 1.7 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 8.8 | 93.5 | 29.1 |

| – Strength Index Reading (3 Year Range): | Bearish-Extreme | Bullish-Extreme | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 5.2 | -5.0 | -1.2 |

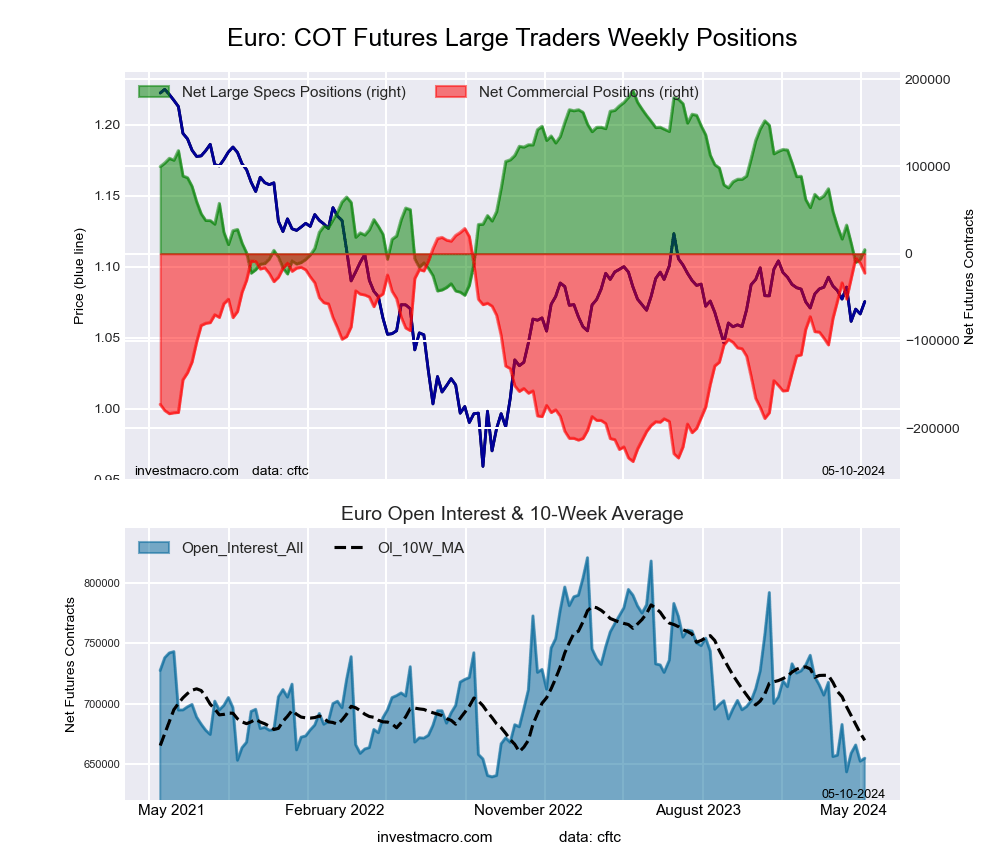

Euro Currency Futures:

The Euro Currency large speculator standing this week reached a net position of 4,590 contracts in the data reported through Tuesday. This was a weekly gain of 11,367 contracts from the previous week which had a total of -6,777 net contracts.

The Euro Currency large speculator standing this week reached a net position of 4,590 contracts in the data reported through Tuesday. This was a weekly gain of 11,367 contracts from the previous week which had a total of -6,777 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 22.3 percent. The commercials are Bullish-Extreme with a score of 80.9 percent and the small traders (not shown in chart) are Bearish-Extreme with a score of 7.2 percent.

Price Trend-Following Model: Downtrend

Our weekly trend-following model classifies the current market price position as: Downtrend. The current action for the model is considered to be: Hold – Maintain Short Position.

| EURO Currency Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 26.1 | 60.1 | 11.5 |

| – Percent of Open Interest Shorts: | 25.4 | 63.5 | 8.8 |

| – Net Position: | 4,590 | -22,279 | 17,689 |

| – Gross Longs: | 170,594 | 393,845 | 75,156 |

| – Gross Shorts: | 166,004 | 416,124 | 57,467 |

| – Long to Short Ratio: | 1.0 to 1 | 0.9 to 1 | 1.3 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 22.3 | 80.9 | 7.2 |

| – Strength Index Reading (3 Year Range): | Bearish | Bullish-Extreme | Bearish-Extreme |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -11.3 | 11.9 | -8.4 |

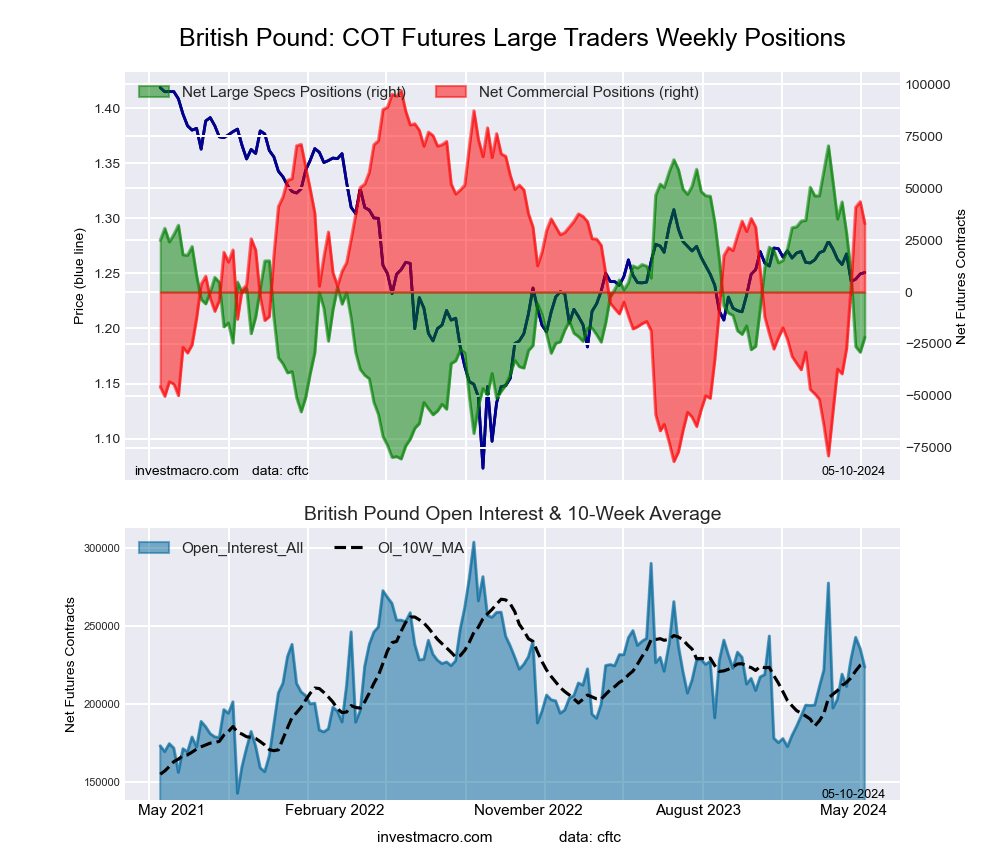

British Pound Sterling Futures:

The British Pound Sterling large speculator standing this week reached a net position of -21,813 contracts in the data reported through Tuesday. This was a weekly advance of 7,177 contracts from the previous week which had a total of -28,990 net contracts.

The British Pound Sterling large speculator standing this week reached a net position of -21,813 contracts in the data reported through Tuesday. This was a weekly advance of 7,177 contracts from the previous week which had a total of -28,990 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 38.8 percent. The commercials are Bullish with a score of 64.1 percent and the small traders (not shown in chart) are Bearish with a score of 36.6 percent.

Price Trend-Following Model: Downtrend

Our weekly trend-following model classifies the current market price position as: Downtrend. The current action for the model is considered to be: Hold – Maintain Short Position.

| BRITISH POUND Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 23.1 | 63.4 | 9.6 |

| – Percent of Open Interest Shorts: | 32.9 | 48.7 | 14.6 |

| – Net Position: | -21,813 | 32,970 | -11,157 |

| – Gross Longs: | 51,777 | 141,835 | 21,445 |

| – Gross Shorts: | 73,590 | 108,865 | 32,602 |

| – Long to Short Ratio: | 0.7 to 1 | 1.3 to 1 | 0.7 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 38.8 | 64.1 | 36.6 |

| – Strength Index Reading (3 Year Range): | Bearish | Bullish | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -37.8 | 39.2 | -26.0 |

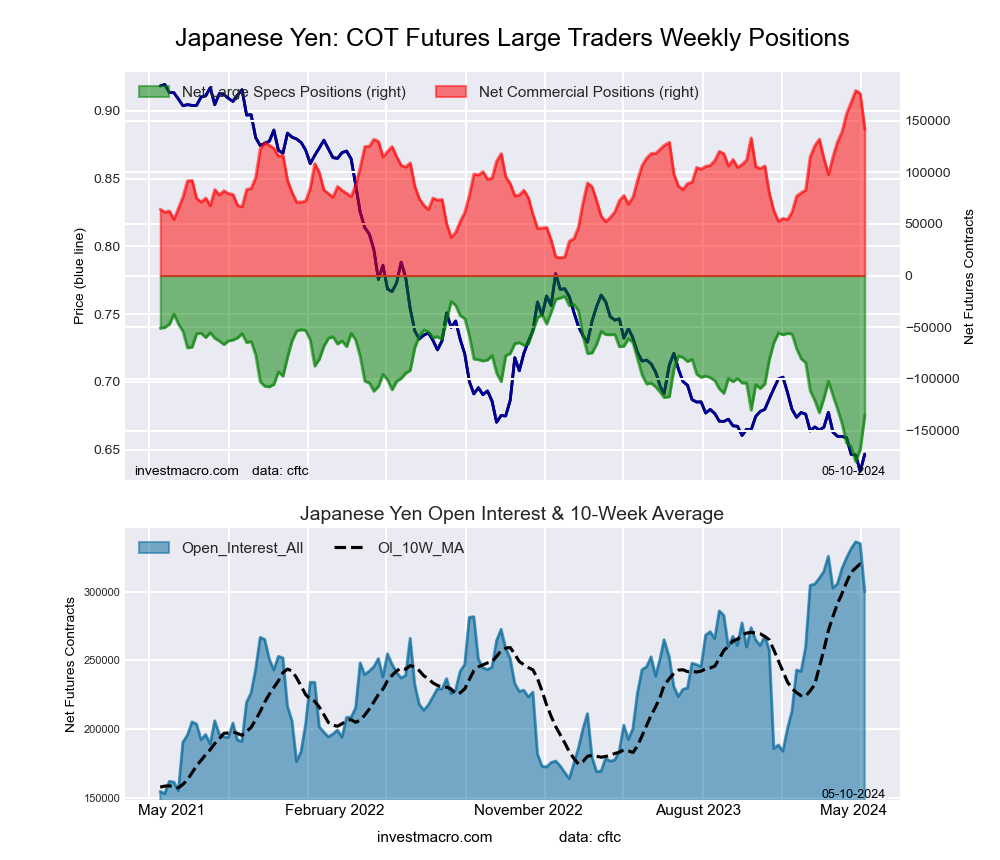

Japanese Yen Futures:

The Japanese Yen large speculator standing this week reached a net position of -134,922 contracts in the data reported through Tuesday. This was a weekly advance of 33,466 contracts from the previous week which had a total of -168,388 net contracts.

The Japanese Yen large speculator standing this week reached a net position of -134,922 contracts in the data reported through Tuesday. This was a weekly advance of 33,466 contracts from the previous week which had a total of -168,388 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 28.1 percent. The commercials are Bullish with a score of 76.9 percent and the small traders (not shown in chart) are Bullish with a score of 61.1 percent.

Price Trend-Following Model: Downtrend

Our weekly trend-following model classifies the current market price position as: Downtrend. The current action for the model is considered to be: Hold – Maintain Short Position.

| JAPANESE YEN Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 11.7 | 73.1 | 12.5 |

| – Percent of Open Interest Shorts: | 56.7 | 25.9 | 14.7 |

| – Net Position: | -134,922 | 141,773 | -6,851 |

| – Gross Longs: | 34,990 | 219,305 | 37,333 |

| – Gross Shorts: | 169,912 | 77,532 | 44,184 |

| – Long to Short Ratio: | 0.2 to 1 | 2.8 to 1 | 0.8 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 28.1 | 76.9 | 61.1 |

| – Strength Index Reading (3 Year Range): | Bearish | Bullish | Bullish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -3.6 | 7.5 | -20.0 |

Swiss Franc Futures:

The Swiss Franc large speculator standing this week reached a net position of -41,787 contracts in the data reported through Tuesday. This was a weekly lowering of -1 contracts from the previous week which had a total of -41,786 net contracts.

The Swiss Franc large speculator standing this week reached a net position of -41,787 contracts in the data reported through Tuesday. This was a weekly lowering of -1 contracts from the previous week which had a total of -41,786 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 1.4 percent. The commercials are Bullish-Extreme with a score of 92.2 percent and the small traders (not shown in chart) are Bearish with a score of 25.8 percent.

Price Trend-Following Model: Downtrend

Our weekly trend-following model classifies the current market price position as: Downtrend. The current action for the model is considered to be: Hold – Maintain Short Position.

| SWISS FRANC Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 9.8 | 77.9 | 11.2 |

| – Percent of Open Interest Shorts: | 53.9 | 21.7 | 23.1 |

| – Net Position: | -41,787 | 53,109 | -11,322 |

| – Gross Longs: | 9,237 | 73,684 | 10,557 |

| – Gross Shorts: | 51,024 | 20,575 | 21,879 |

| – Long to Short Ratio: | 0.2 to 1 | 3.6 to 1 | 0.5 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 1.4 | 92.2 | 25.8 |

| – Strength Index Reading (3 Year Range): | Bearish-Extreme | Bullish-Extreme | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -35.3 | 23.5 | 18.9 |

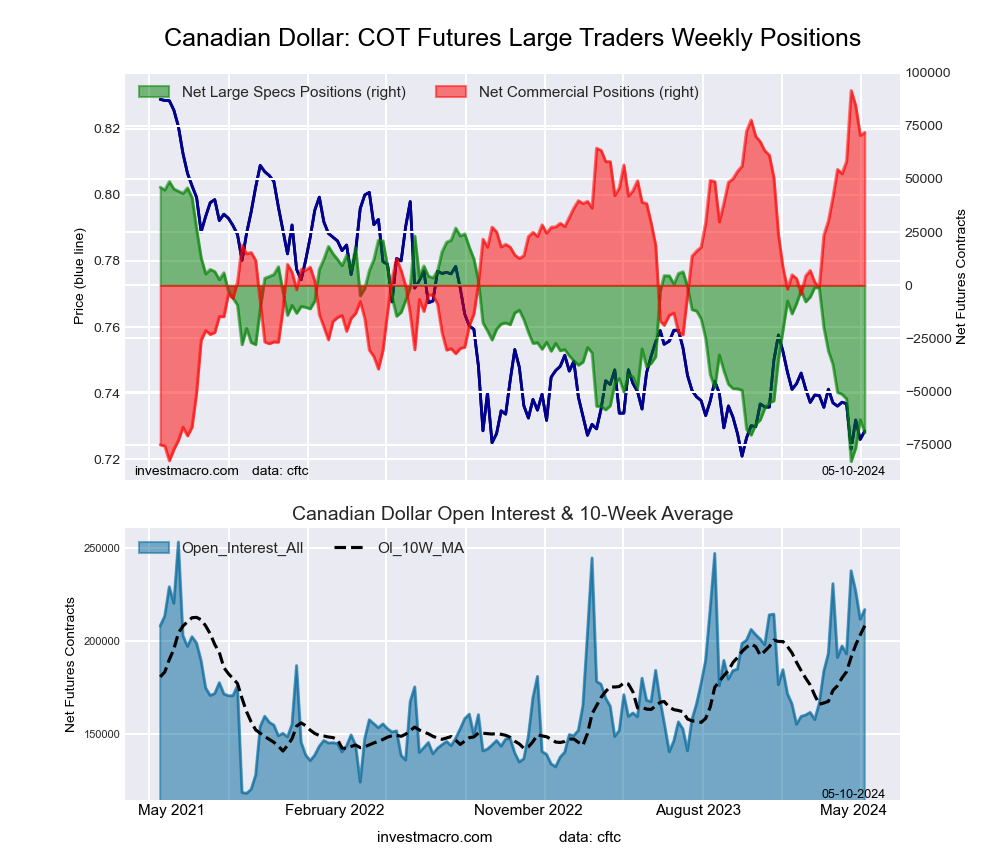

Canadian Dollar Futures:

The Canadian Dollar large speculator standing this week reached a net position of -69,221 contracts in the data reported through Tuesday. This was a weekly fall of -6,020 contracts from the previous week which had a total of -63,201 net contracts.

The Canadian Dollar large speculator standing this week reached a net position of -69,221 contracts in the data reported through Tuesday. This was a weekly fall of -6,020 contracts from the previous week which had a total of -63,201 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 10.3 percent. The commercials are Bullish-Extreme with a score of 88.7 percent and the small traders (not shown in chart) are Bearish-Extreme with a score of 17.4 percent.

Price Trend-Following Model: Downtrend

Our weekly trend-following model classifies the current market price position as: Downtrend. The current action for the model is considered to be: Hold – Maintain Short Position.

| CANADIAN DOLLAR Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 15.2 | 68.5 | 13.7 |

| – Percent of Open Interest Shorts: | 47.1 | 35.3 | 14.9 |

| – Net Position: | -69,221 | 71,845 | -2,624 |

| – Gross Longs: | 32,945 | 148,390 | 29,719 |

| – Gross Shorts: | 102,166 | 76,545 | 32,343 |

| – Long to Short Ratio: | 0.3 to 1 | 1.9 to 1 | 0.9 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 10.3 | 88.7 | 17.4 |

| – Strength Index Reading (3 Year Range): | Bearish-Extreme | Bullish-Extreme | Bearish-Extreme |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -14.4 | 10.0 | 3.6 |

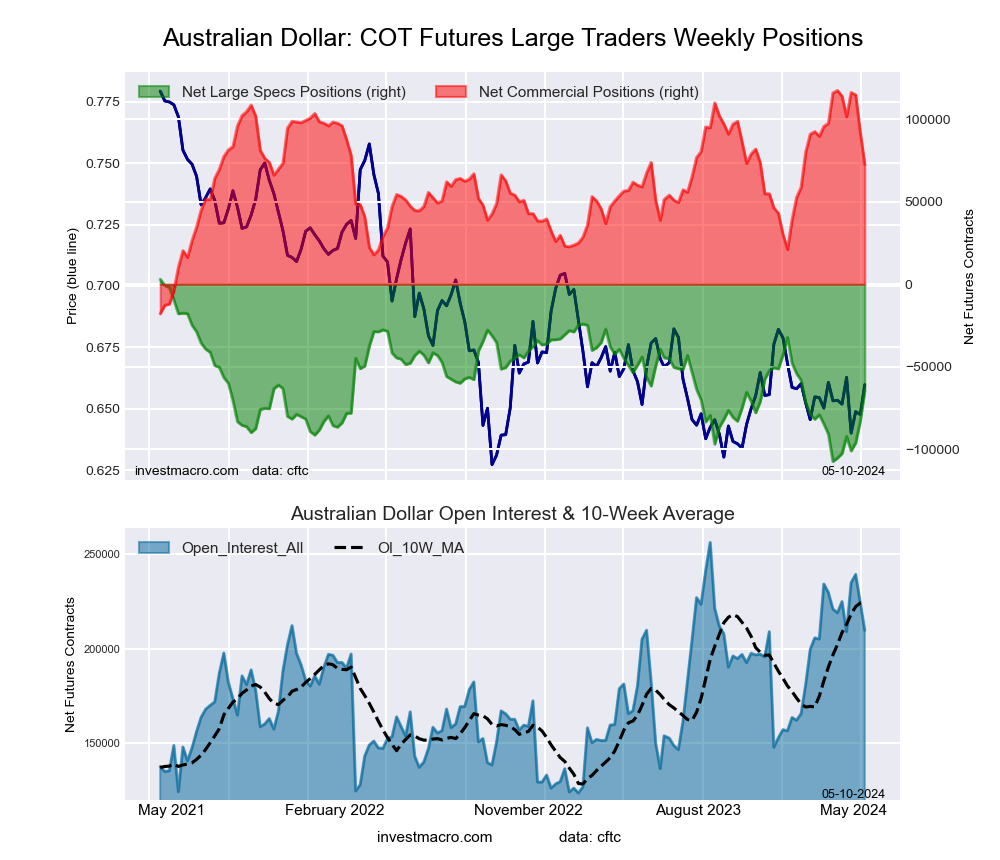

Australian Dollar Futures:

The Australian Dollar large speculator standing this week reached a net position of -64,516 contracts in the data reported through Tuesday. This was a weekly rise of 18,719 contracts from the previous week which had a total of -83,235 net contracts.

The Australian Dollar large speculator standing this week reached a net position of -64,516 contracts in the data reported through Tuesday. This was a weekly rise of 18,719 contracts from the previous week which had a total of -83,235 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 38.9 percent. The commercials are Bullish with a score of 66.8 percent and the small traders (not shown in chart) are Bearish with a score of 36.8 percent.

Price Trend-Following Model: Weak Downtrend

Our weekly trend-following model classifies the current market price position as: Weak Downtrend. The current action for the model is considered to be: Hold – Maintain Short Position.

| AUSTRALIAN DOLLAR Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 23.6 | 64.4 | 9.5 |

| – Percent of Open Interest Shorts: | 54.4 | 29.8 | 13.3 |

| – Net Position: | -64,516 | 72,522 | -8,006 |

| – Gross Longs: | 49,480 | 135,023 | 19,859 |

| – Gross Shorts: | 113,996 | 62,501 | 27,865 |

| – Long to Short Ratio: | 0.4 to 1 | 2.2 to 1 | 0.7 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 38.9 | 66.8 | 36.8 |

| – Strength Index Reading (3 Year Range): | Bearish | Bullish | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 37.0 | -33.2 | 11.1 |

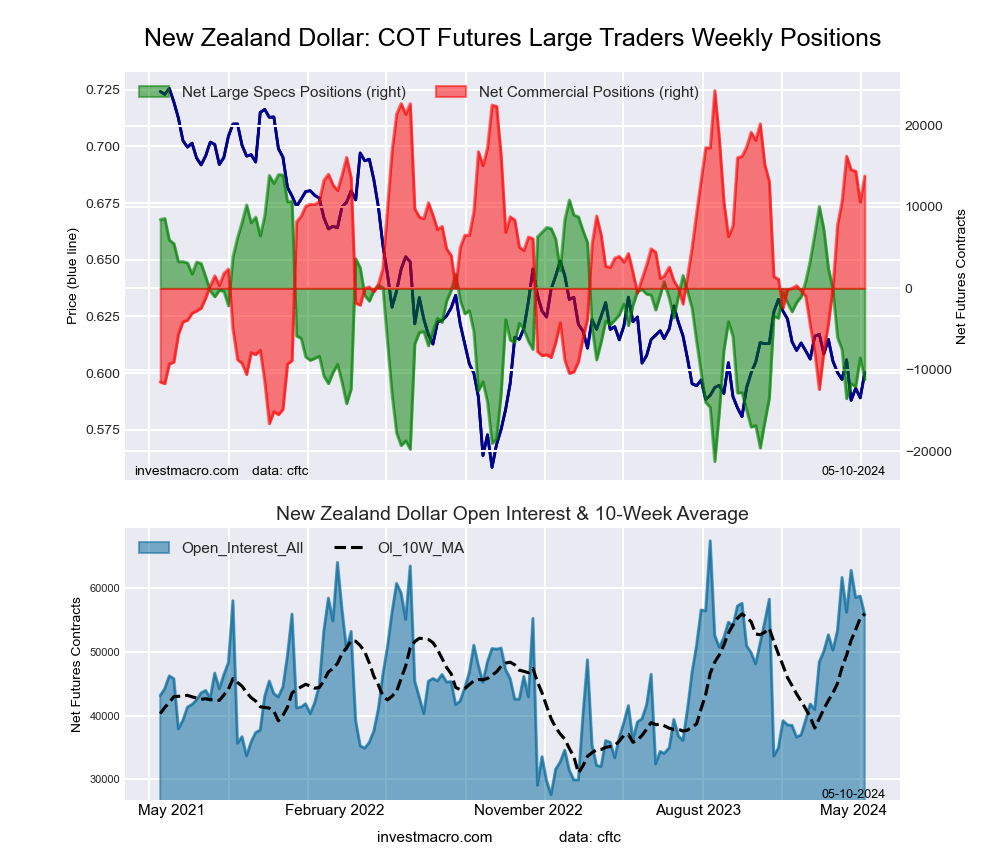

New Zealand Dollar Futures:

The New Zealand Dollar large speculator standing this week reached a net position of -11,191 contracts in the data reported through Tuesday. This was a weekly fall of -2,640 contracts from the previous week which had a total of -8,551 net contracts.

The New Zealand Dollar large speculator standing this week reached a net position of -11,191 contracts in the data reported through Tuesday. This was a weekly fall of -2,640 contracts from the previous week which had a total of -8,551 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 28.6 percent. The commercials are Bullish with a score of 74.3 percent and the small traders (not shown in chart) are Bearish with a score of 20.6 percent.

Price Trend-Following Model: Downtrend

Our weekly trend-following model classifies the current market price position as: Downtrend. The current action for the model is considered to be: Hold – Maintain Short Position.

| NEW ZEALAND DOLLAR Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 34.1 | 60.1 | 5.6 |

| – Percent of Open Interest Shorts: | 54.2 | 35.4 | 10.3 |

| – Net Position: | -11,191 | 13,792 | -2,601 |

| – Gross Longs: | 19,060 | 33,531 | 3,124 |

| – Gross Shorts: | 30,251 | 19,739 | 5,725 |

| – Long to Short Ratio: | 0.6 to 1 | 1.7 to 1 | 0.5 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 28.6 | 74.3 | 20.6 |

| – Strength Index Reading (3 Year Range): | Bearish | Bullish | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -14.7 | 14.8 | -11.5 |

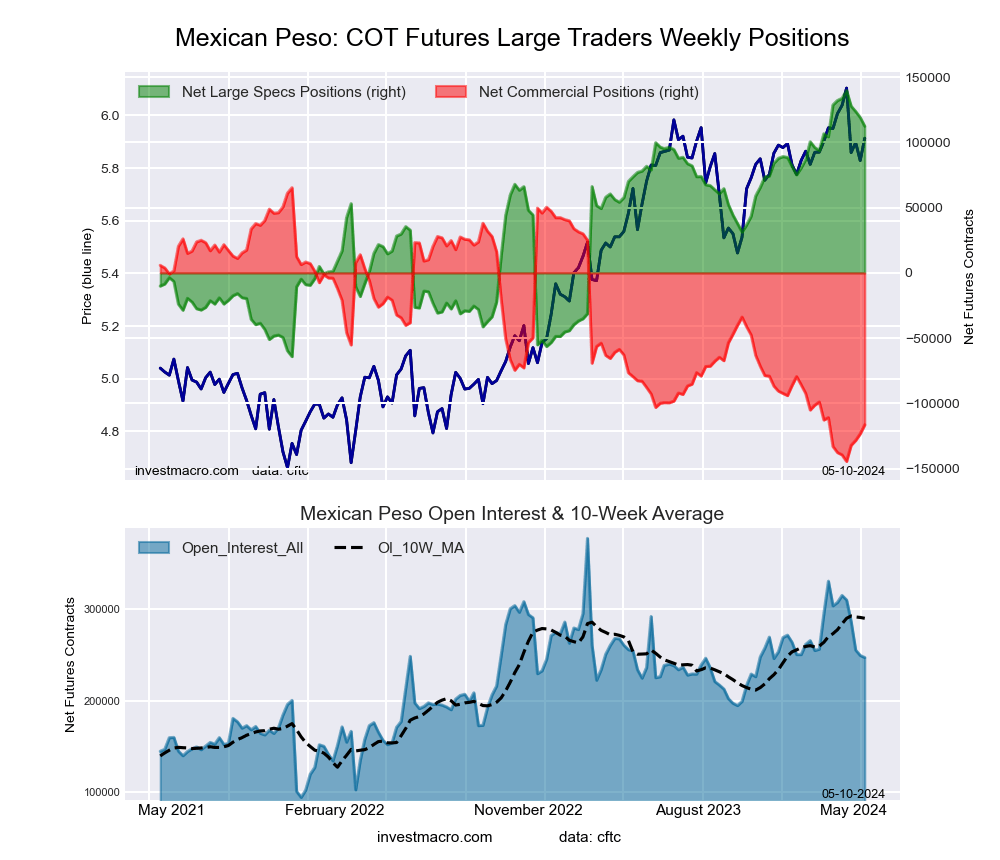

Mexican Peso Futures:

The Mexican Peso large speculator standing this week reached a net position of 112,312 contracts in the data reported through Tuesday. This was a weekly fall of -6,733 contracts from the previous week which had a total of 119,045 net contracts.

The Mexican Peso large speculator standing this week reached a net position of 112,312 contracts in the data reported through Tuesday. This was a weekly fall of -6,733 contracts from the previous week which had a total of 119,045 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 86.6 percent. The commercials are Bearish-Extreme with a score of 13.4 percent and the small traders (not shown in chart) are Bearish with a score of 37.1 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend. The current action for the model is considered to be: Hold – Maintain Long Position.

| MEXICAN PESO Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 55.7 | 40.9 | 2.8 |

| – Percent of Open Interest Shorts: | 10.2 | 88.1 | 1.1 |

| – Net Position: | 112,312 | -116,374 | 4,062 |

| – Gross Longs: | 137,564 | 101,075 | 6,829 |

| – Gross Shorts: | 25,252 | 217,449 | 2,767 |

| – Long to Short Ratio: | 5.4 to 1 | 0.5 to 1 | 2.5 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 86.6 | 13.4 | 37.1 |

| – Strength Index Reading (3 Year Range): | Bullish-Extreme | Bearish-Extreme | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -9.7 | 10.2 | -9.8 |

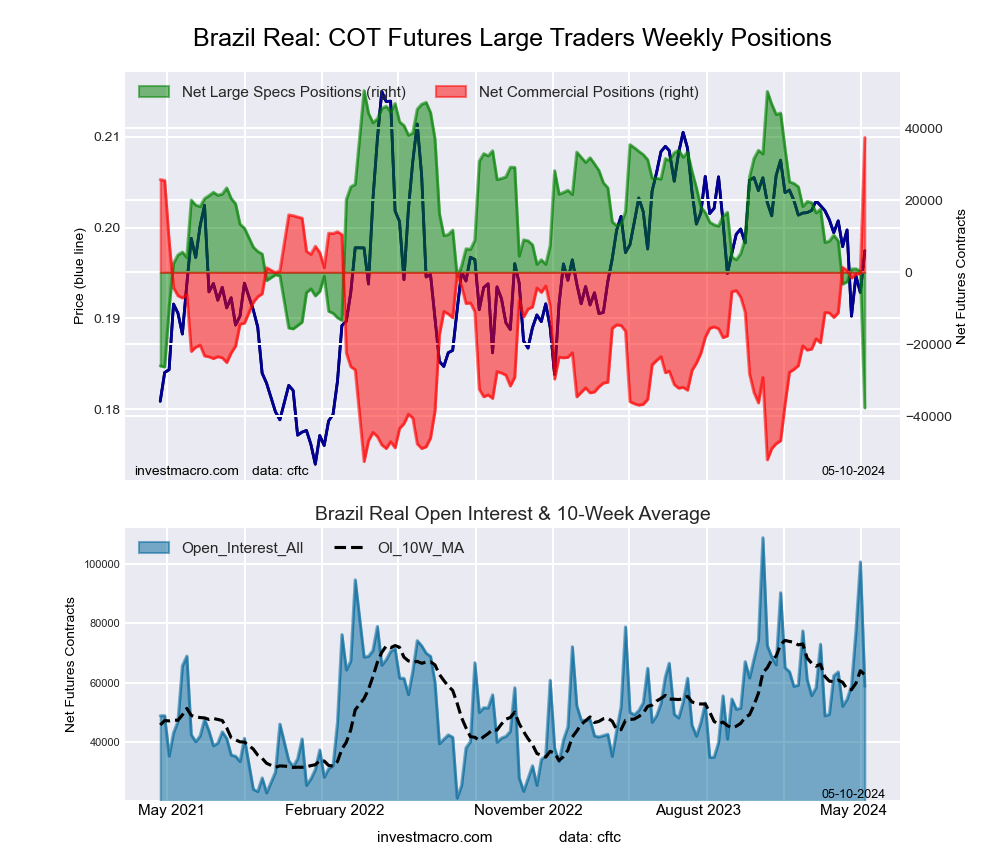

Brazilian Real Futures:

The Brazilian Real large speculator standing this week reached a net position of -37,643 contracts in the data reported through Tuesday. This was a weekly lowering of -37,929 contracts from the previous week which had a total of 286 net contracts.

The Brazilian Real large speculator standing this week reached a net position of -37,643 contracts in the data reported through Tuesday. This was a weekly lowering of -37,929 contracts from the previous week which had a total of 286 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 0.0 percent. The commercials are Bullish-Extreme with a score of 100.0 percent and the small traders (not shown in chart) are Bearish with a score of 36.1 percent.

Price Trend-Following Model: Strong Downtrend

Our weekly trend-following model classifies the current market price position as: Strong Downtrend. The current action for the model is considered to be: Hold – Maintain Short Position.

| BRAZIL REAL Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 16.2 | 79.9 | 3.8 |

| – Percent of Open Interest Shorts: | 80.3 | 16.2 | 3.5 |

| – Net Position: | -37,643 | 37,468 | 175 |

| – Gross Longs: | 9,546 | 46,966 | 2,236 |

| – Gross Shorts: | 47,189 | 9,498 | 2,061 |

| – Long to Short Ratio: | 0.2 to 1 | 4.9 to 1 | 1.1 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 0.0 | 100.0 | 36.1 |

| – Strength Index Reading (3 Year Range): | Bearish-Extreme | Bullish-Extreme | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -52.6 | 54.1 | -22.4 |

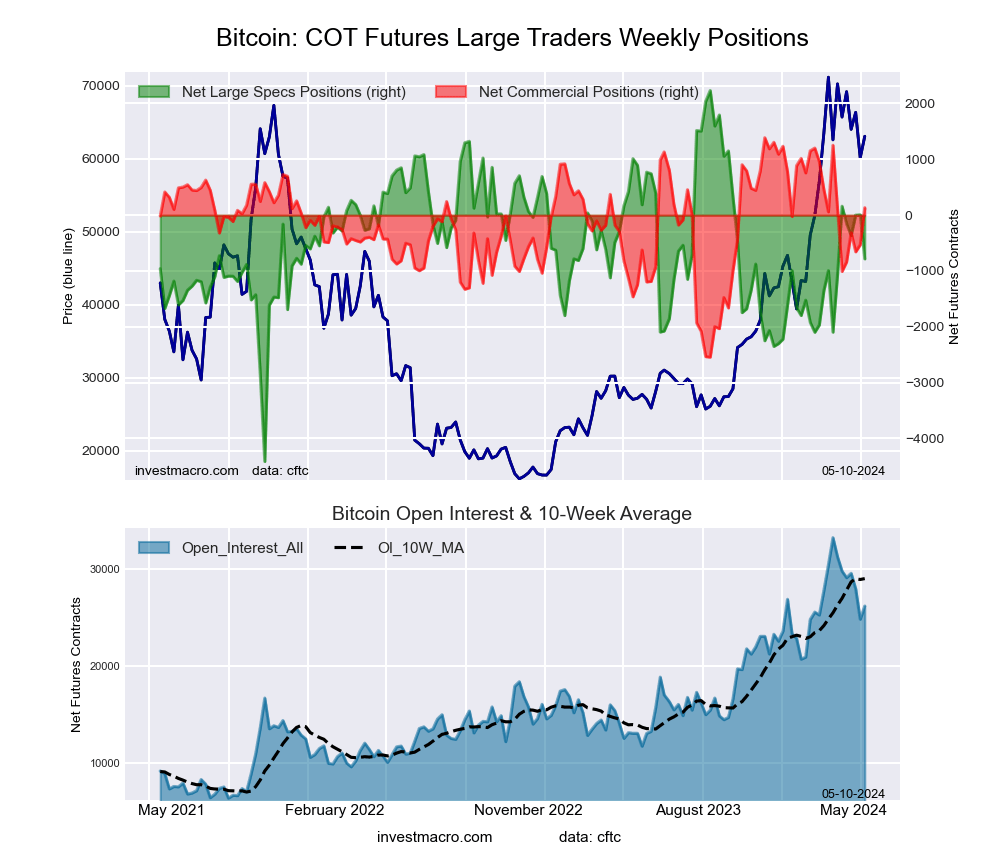

Bitcoin Futures:

The Bitcoin large speculator standing this week reached a net position of -783 contracts in the data reported through Tuesday. This was a weekly reduction of -789 contracts from the previous week which had a total of 6 net contracts.

The Bitcoin large speculator standing this week reached a net position of -783 contracts in the data reported through Tuesday. This was a weekly reduction of -789 contracts from the previous week which had a total of 6 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 54.6 percent. The commercials are Bullish with a score of 68.1 percent and the small traders (not shown in chart) are Bearish with a score of 27.7 percent.

Price Trend-Following Model: Uptrend

Our weekly trend-following model classifies the current market price position as: Uptrend. The current action for the model is considered to be: Hold – Maintain Long Position.

| BITCOIN Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 79.4 | 4.5 | 6.1 |

| – Percent of Open Interest Shorts: | 82.4 | 4.0 | 3.6 |

| – Net Position: | -783 | 134 | 649 |

| – Gross Longs: | 20,770 | 1,181 | 1,588 |

| – Gross Shorts: | 21,553 | 1,047 | 939 |

| – Long to Short Ratio: | 1.0 to 1 | 1.1 to 1 | 1.7 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 54.6 | 68.1 | 27.7 |

| – Strength Index Reading (3 Year Range): | Bullish | Bullish | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 4.4 | 0.6 | -7.2 |

Article By InvestMacro – Receive our weekly COT Newsletter

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators) as well as their open interest (contracts open in the market at time of reporting). See CFTC criteria here.