By Tyler Hansen, Dartmouth College; Abraham Silverman, Johns Hopkins University; Elizabeth J. Wilson, Dartmouth College, and Erin Baker, UMass Amherst

Offshore winds have the potential to supply coastlines with massive, consistent flows of clean electricity. One study estimates wind farms just offshore could meet 11 times the projected global electricity demand in 2040.

In the U.S., the East Coast is an ideal location to capture this power, but there’s a problem: getting electricity from ocean wind farms to the cities and towns that need it.

While everyone wants reliable electricity in their homes and businesses, few support the construction of the transmission lines necessary to get it there. This has always been a problem, both in the U.S. and internationally, but it is becoming an even bigger challenge as countries speed toward net-zero carbon energy systems that will use more electricity.

The U.S. Department of Energy and 10 states in the Northeast States Collaborative on Interregional Transmission are working on a potentially transformative solution: plans for an offshore electric power grid.

Illustrations by Billy Roberts, NREL

At the core of this grid would be backbone transmission lines off the East Coast, from North Carolina to Maine, where dozens of offshore wind projects are already in the pipeline.

The plans envision it supporting at least 85 gigawatts of offshore wind power by 2050 – close to the U.S. goal of 110 GW of installed wind power by mid-century, enough to power 40 million homes and up from 0.2 GW today. The Northeast States Collaborative formalized their goals in July 2024 through a multistate memorandum of understanding.

Emerging research from the Department of Energy, the research company Brattle and other groups suggests that an offshore electric power grid could mitigate key challenges to building new transmission lines on land and reduce the costs of offshore wind power.

Cutting costs would be welcome news – offshore wind project costs rose as much as 50% from 2021 to 2023. While some of the underlying causes have subsided, such as inflation and global supply chain disruptions, interest rates remain high, and the industry is still trying to find its footing in the U.S.

What is an offshore electric power grid?

Today’s offshore wind projects use a point-to-point, or radial design, where each offshore wind farm is individually connected to the onshore grid.

This method works if a region has only a few projects, but it quickly becomes more expensive due to the cabling and other infrastructure. Its lines are also disruptive to communities and marine life. And it requires more costly onshore grid upgrades.

Coordinated offshore transmission can avoid many of those costs with what the Department of Energy calls “meshed” or “backbone” designs.

Rather than individual connections to land, many offshore wind farms would be connected to a shared transmission line, which would connect to the onshore grid through strategically placed “points of interconnection.” This way, electricity produced by an offshore wind farm would be transmitted to where it is most needed, up and down the East Coast.

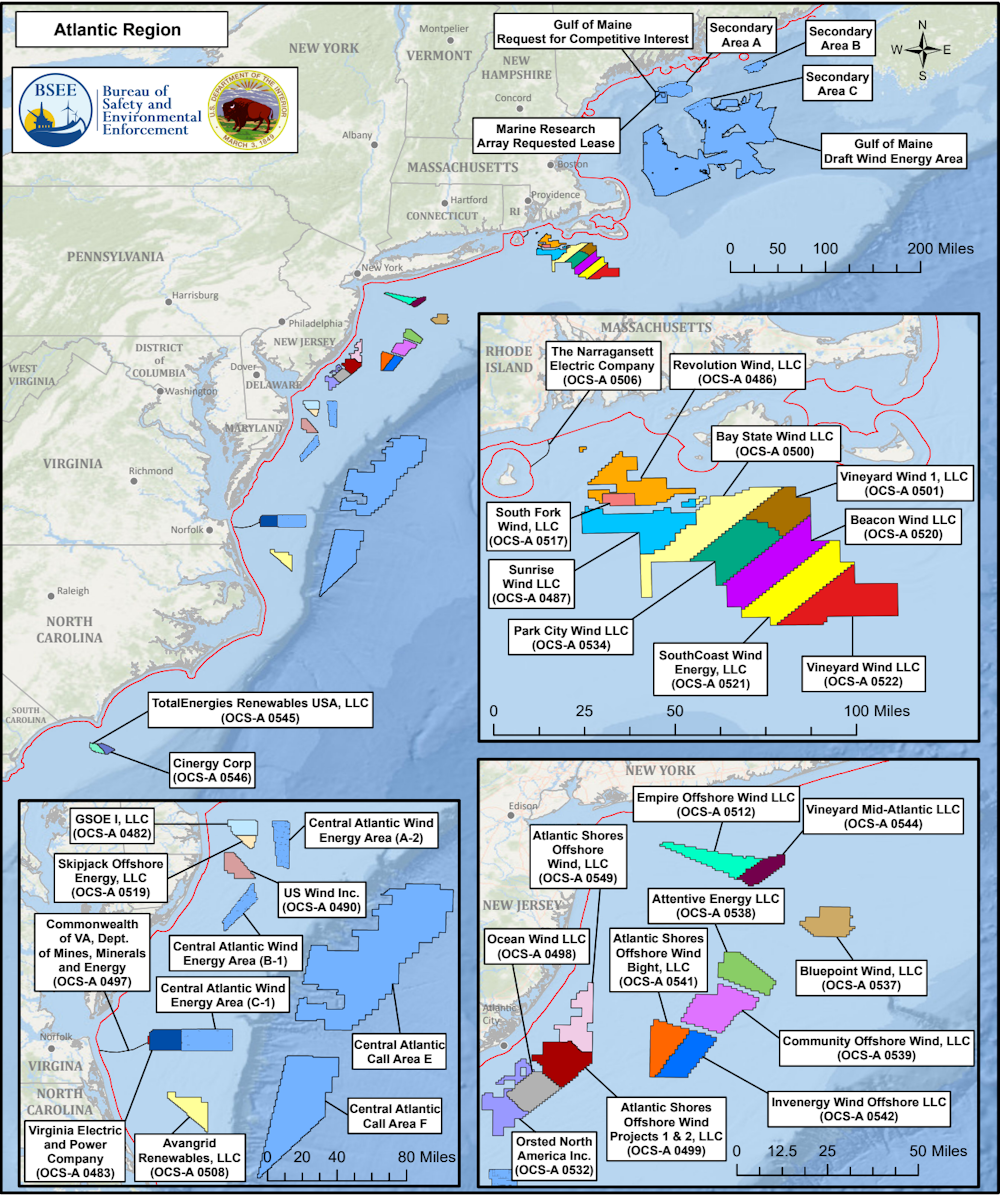

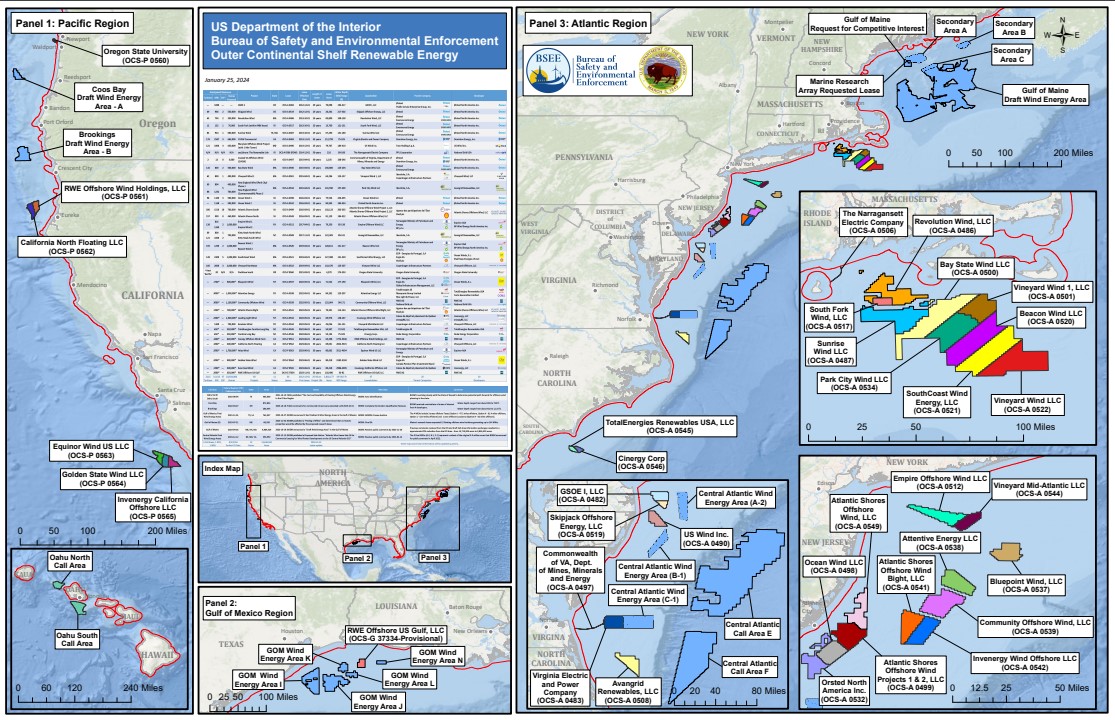

U.S. Department of the Interior, 2024

Even better, electricity generated onshore could also be transmitted through these shared lines to move energy to where it is needed. This could improve the resilience of power grids and reduce the need for new transmission lines over land, which have been notoriously difficult to gain approval for, especially on the East Coast.

Coordinated offshore transmission was part of early U.S. discussions on offshore wind planning and development. In the late 2000s when Google and partners first proposed the Atlantic Wind Connection, an offshore transmission project, the benefits in both offshore renewables and the entire energy system were intriguing. At the time, the U.S. had just one utility-scale offshore wind project in the pipeline, and it ultimately failed.

Today, the U.S. has 53 GW of offshore wind projects being planned or developed. As energy researchers, we believe coordinated offshore transmission is important for the industry to succeed at scale.

Offshore grid could save money, reduce impacts

By enabling power from offshore wind farms and onshore electricity generators to travel to more places, coordinated transmission can enhance grid reliability and enable electricity to get to where it is most needed. This reduces the need for more expensive and often more polluting power plants.

A 2024 report from the National Renewable Energy Lab found the benefits of a coordinated design are nearly three times higher than the costs when compared with a standard point-to-point design.

Studies from Europe, the U.K. and Brattle have pointed to additional benefits, including reducing planet-warming carbon emissions, cutting the number of beach crossings by a third and reducing the miles of transmission cables needed by 35% to 60%.

Illustrations by Billy Roberts, NREL

In the U.S., offshore transmission lines would be almost entirely in federal waters, potentially avoiding many of the conflicts associated with onshore projects, though it would still face challenges.

Challenges and next steps

Building an offshore grid will require some important changes.

First is changing government incentives. The federal investment tax credit for offshore wind, which covers at least 30% of the upfront capital cost of a project, does not currently help pay for coordinated transmission designs.

Second, planning needs to take everyone’s concerns into account from the beginning. While the overall benefits of coordinated transmission designs outweigh overall costs, who receives the benefits and who bears the costs matters. For example, more expensive power generators could earn less, and some communities feel threatened by offshore development.

Third, greater coordination will be needed among everyone involved to dispatch power to and from the regional grids. The Federal Energy Regulatory Commission’s recent Order 1920, requiring power providers to plan for future needs, may serve as a blueprint, but it does not apply to interregional projects, such as an offshore transmission backbone connecting over a dozen states across three regions.

Elizabeth J. Wilson, CC BY-ND

The U.S. reached an important milestone in March 2024 with the completion of South Fork Wind, the country’s first utility-scale wind farm, bringing U.S. offshore wind power capacity to nearly 200 megawatts. Eight more projects are under construction or approved for construction. Once built, they would bring installed capacity to over 13 gigawatts, roughly the same as three dozen coal-fired power plants.

An offshore transmission backbone could support offshore wind development and the East Coast’s energy needs for generations to come.

This article was updated July 31, 2024, to clarify that the states formalized the memorandum of understanding.![]()

About the Authors:

Tyler Hansen, Research Associate in Environmental Studies, Dartmouth College; Abraham Silverman, Research Scholar, Ralph O’Connor Sustainable Energy Institute, Johns Hopkins University; Elizabeth J. Wilson, Professor of Environmental Studies, Dartmouth College, and Erin Baker, Professor of Industrial Engineering Applied to Energy Policy, UMass Amherst

This article is republished from The Conversation under a Creative Commons license. Read the original article.

{kind=link}