Expert Ron Struthers believes TC Energy is a well-run pipeline company as it is yielding about 6.5% and has increased its dividend every year since the turn of the century. He also discusses how oil tanker rates are soaring as the market tightens more with the Ukraine war, but DHT Holdings is a laggard worth a look.

Has gold bottomed? It is possible, but it appears today it is retreating from its resistance area. We need a solid break above $1740 for more proof the bottom is in, which would also break the downtrend.

A good thing we got stopped out of most of our gold stocks in June. Near term, I believe there is more potential in the energy sector, where I have been making most of my new picks this year and two more below.

There is renewed interest in GICs and term deposits at the banks now that interest rates have gone up. A person can get 4% to 5% by locking into three to five year terms. Rates vary by type and bank, but that is a good ballpark number.

While this is a safe investment, the downfall is your money is tied up, and there is no chance of getting a higher rate or making a capital gain.

A better alternative is TC Energy Corp. (TRP:NYSE).

TC Energy Corp.

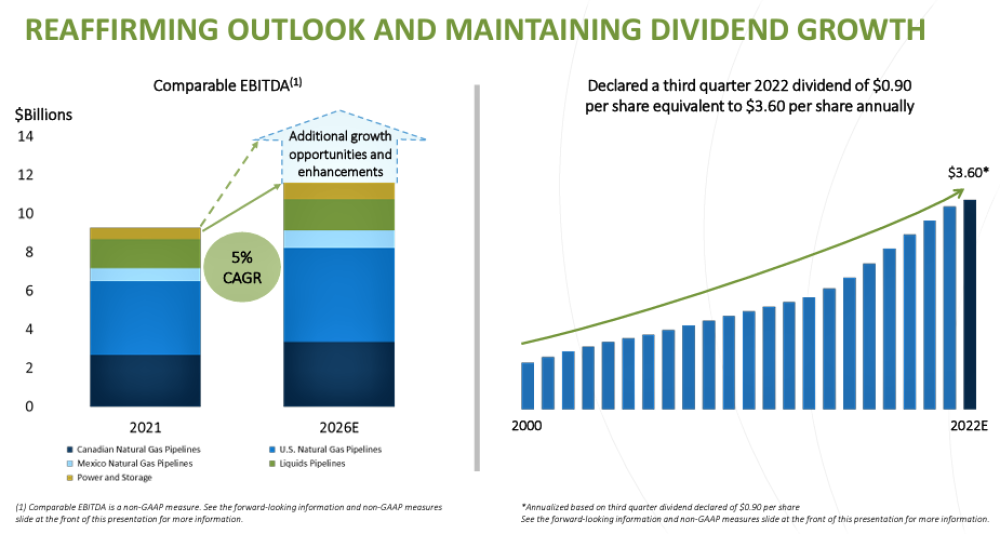

TC Energy offers more potential than GICs, with comparatively small risks. At CA$55.75 and an annual payout of $3.60, TC Energy yields 6.5%.

TC Energy owns and operates 93,300 kilometers of natural gas pipelines and 653 billion cubic feet of storage space in Canada, the United States, and Mexico. It also has a 4,900km network of oil pipelines, which supply Alberta crude to the U.S. market.

It also invests in several power-generation facilities, including wind, solar and nuclear. The current quarterly dividend is $0.90 per share. The company has raised its payout every year since the turn of the century.

The company is projecting 5% annual growth, and I see no reason why dividends will not keep increasing. Second-quarter results came in slightly ahead of analysts’ expectations.

Net income attributable to shareholders was $889 million ($0.90 per share), compared with $975 million ($1 per share) in the same period of 2021.

For the first six months of the fiscal year, net income was $1.24 billion ($1.27 a share). In the same period of the prior year, the company reported a loss of $82 million.

TC Energy announced a major expansion into Mexico on August 4, 2022. TC Energy and Mexico’s state-owned electricity producer Comision Federal de Electricidad (CFE) announced the launch of a $4.5 billion pipeline that will deliver natural gas from the southwestern U.S. to southern Mexico.

TC Energy said the CFE’s decision to take a 15% share in the project — the 715-kilometer offshore Southeast Gateway pipeline — is a landmark transaction for the Mexican utility as its first public-private partnership.

The Southeast Gateway pipeline is expected to be operational by 2025, and TC Energy said the project enjoys broad-based support from all levels of government, environmentalists, and regulators.

The project will allow the CFE to replace power plants currently fuelled by high-sulfur oil with natural gas-fired facilities that produce half the greenhouse-gas emissions. Over the course of this decade, Mexico’s appetite for natural gas is expected to increase by 50%.

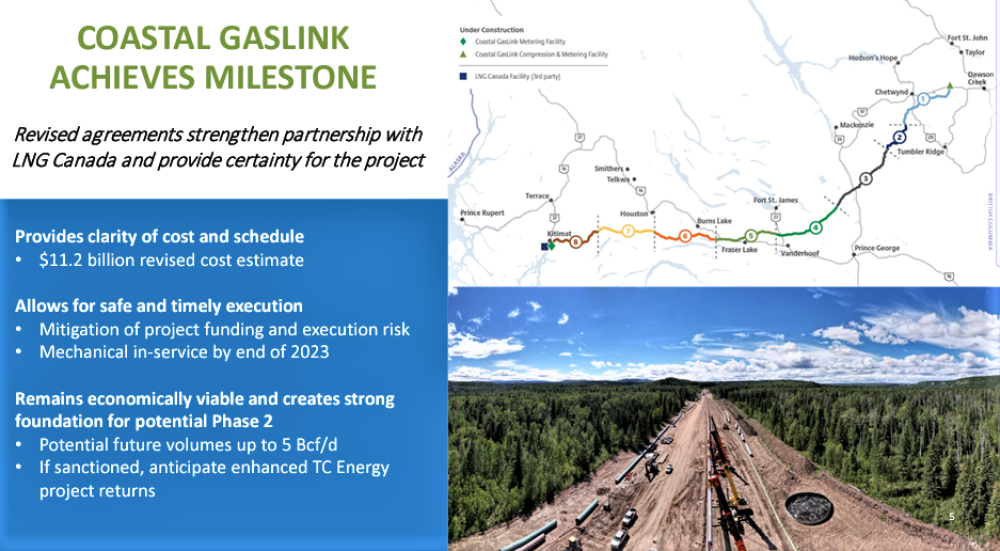

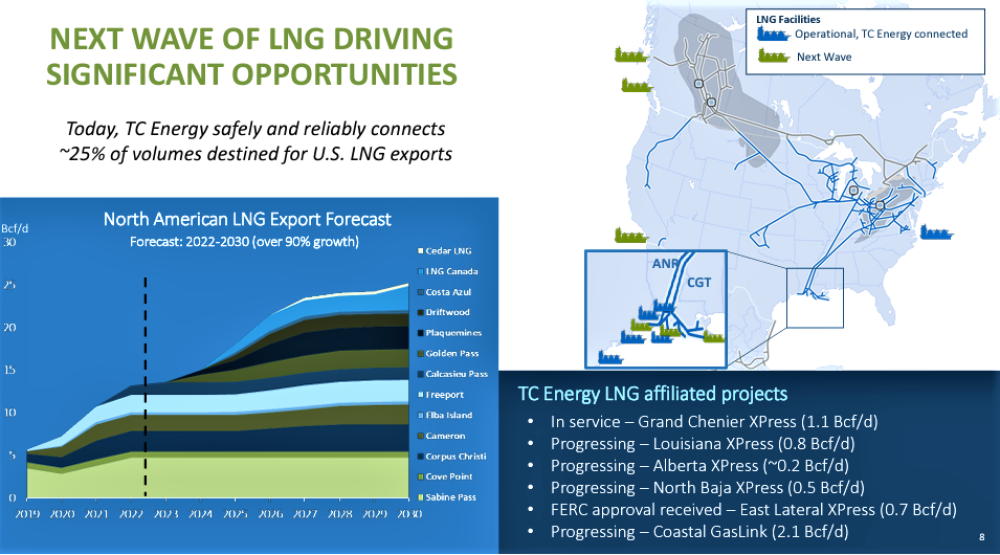

TC Energy is also expanding into what I see as a high-growth market with strong future growth, exporting Liquid Natural Gas (LNG). Their $40-billion LNG Canada project will have an export terminal in Kitimat, B.C., at the end of TC Energy’s Coastal GasLink pipeline and aims to be up and running by 2025.

This next graphic is from TC Energy’s presentation

In March this year, TC Energy announced the signing of option agreements to sell a 10% equity interest in the Coastal GasLink Pipeline Limited Partnership to Indigenous communities across the project corridor.

The opportunity to become business partners through equity ownership was made available to all 20 Nations holding existing agreements with Coastal GasLink.

The formal establishment of these agreements comes from an interest expressed by Indigenous groups across the project corridor to become owners in Coastal GasLink alongside Alberta Investment Management Corporation, KKR, and TC Energy.

The next graphic from their presentation illustrates that TC Energy is already benefiting from the LNG boom and will continue to do so and especially with its own Kitimat terminal in 2025.

The stock has dropped to the lowest level in almost two years, simply correcting too far in sympathy with oil stocks.

It does not matter the price of oil and gas; TC Energy is paid to move it at whatever price. The stock is of great value here.

Atlas Corp.

With Atlas Corp. (ATCO:NYSE), we are sitting on a big gain from our $7.33 Buy price, and there currently is a cash offer of $15.50 per share to take Atlas private.

Assuming that happens in six months, an investor who buys the stock now would see a $1.40 return plus $0.25 in dividends for a total of $1.65 or 11.7%, not bad for six months in today’s markets.

I am surprised arbitrage traders have not bid the stock higher, but it may be a function of this terrible market.

To recap, in April 2022, Fairfax Financial Holdings Limited (“Fairfax”) exercised warrants to purchase 25.0 million common shares of Atlas. The warrants, which were originally issued on July 16, 2018, had an exercise price of $8.05 per common share for an aggregate exercise price of $201.3 million.

Immediately following this exercise, Fairfax and its affiliates held in aggregate 124,805,753 common shares, representing approximately 45.1% of the then-issued and outstanding common shares of Atlas.

Fairfax continues to hold 6.0 million warrants.

On August 4, 2022, Atlas’ Board of Directors received a non-binding proposal letter, dated August 4, 2022, from Poseidon Acquisition Corp., an entity formed by certain affiliates of Fairfax, certain affiliates of the Washington Family (“Washington”), David Sokol, Chairman of the Board of Atlas, and Ocean Network Express Pte. Ltd., and certain of their respective affiliates, to acquire all of the outstanding common shares of Atlas, other than common shares owned by Fairfax, Washington, Mr. Sokol and certain executive officers of the Company, for $14.45 cash per common share.

On Sept 28, 2022, Poseidon Acquisition Corp. revised its price upwards to $15.50 cash per common share.

On or about November 1, 2022, Atlas will pay another $0.125 dividend, and on Feb 1, 2023, another $0.125 dividend.

Atlas is our only shipping stock at this time, so I am suggesting replacing it with DHT Holdings.

DHT Holdings

DHT Holdings Inc. (DHT:NYSE) is an independent crude oil tanker company with a fleet trading internationally and consists of crude oil tankers in the VLCC segment.

On June 30, 2022, DHT had a fleet of 24 VLCCs, with a total dwt of 7,453,519. I have followed this company for many years and see now as a good time to buy.

A recovery in the VLCC market was expected in 2022 after two years of Covid restrictions affecting oil demand. Tankers International reported that the data shows a definite boost.

Globally they count an additional 27 monthly liftings in the VLCC spot market in the first half of this year compared to the 2021 annual average, and we are very close to reaching pre-Covid fixing volumes.

27 additional cargoes per month would employ more than 30 VLCCs full-time if they were all traded between the AG and Singapore. Of course, some travel shorter distances, and some travel further.

Then add in the Ukraine war, and we see more tankers heading to Europe to make up for Russia’s supply. All things combined have caused tanker rates to soar.

On September 12, 2022, Tradewinds reported spot tanker rates at $43,600 per day, and now they are at $49,000 per day. This is about double from a year ago. This will give a big boost to DHT’s cash flow and earnings late this year and in 2023.

September 8, 2022, DHT Holdings announced a new dividend policy with 100% of net income being returned to shareholders in the form of quarterly cash dividends. The new policy will be implemented in the third quarter of 2022.

Svein Moxnes Harfjeld, President & CEO, stated, “The key considerations behind the new policy are the strength of our balance sheet and liquidity position in combination with no current plans for significant capital expenditures. The timing of the decision and its implementation reflects our constructive market outlook.”

I expect this will result in a minimum dividend of $0.50 per year and could easily go well over $1.00 if tanker rates stay high. At a $7.40 share price and a $0.50 dividend is a 6.8% yield.

DHT had a good second quarter

Quarterly Highlights:

- In the second quarter of 2022, the Company’s VLCCs achieved an average rate of $24,300 per day.

- Adjusted EBITDA for the second quarter of 2022 was $32.5 million. Net profit for the quarter was $10.0 million, which equates to $0.06 per basic share.

- In May 2022, the Company entered into agreements to sell DHT Hawk, built in 2007, and DHT Falcon, built in 2006, for $40 million and $38 million, respectively. The vessels were both delivered during the second quarter of 2022, and the sales generated a combined gain of $12.7 million. The Company repaid the outstanding debt of $13.3 million combined on the two vessels.

- In June 2022, the Company prepaid $23.1 million under the Nordea Credit Facility. The voluntary prepayment was made under the revolving credit facility tranche and may be re-borrowed.

- In the second quarter of 2022, the Company purchased 2,826,771 of its own shares in the open market for an aggregate consideration of $15.9 million at an average price of $5.6256. All shares were retired upon receipt.

- For the second quarter of 2022, the Company declared a cash dividend of $0.04 per share of outstanding common stock, payable on August 30, 2022, to shareholders of record as of August 23, 2022. This marks the 50th consecutive quarterly cash dividend. The shares will trade ex-dividend from August 22, 2022.

So far, in the third quarter of 2022, 68% of the available VLCC days have been booked at an average rate of $23,600 per day on a discharge-to-discharge basis (not including any potential profit splits on time charters).

This is not much different than Q2, but as time goes on, the cheaper rates will drop off and be replaced with the higher rates that are currently in the market.

For example, in July 2022, the Company entered into a five-year time charter for DHT Osprey at $37,000 per day, with the charterer’s option to extend two additional years at $40,000 per day and $45,000 per day respectively. The vessel is expected to deliver into the contract in August.

DHT has a relatively new fleet of ships compared to most tanker companies, with only three of their 24 VLCCs pre-2011. Those three were built in 2007. Newer builds are more efficient, have less maintenance, and are not subject to discount rates that can be applied to older tankers.

At the end of 2020, Statista reports that 46% of oil tankers are 15 years old and older.

I like DHT because they are well-run and very efficient. The stock has pulled back and is not reflecting its new dividend policy, which few, if any, other tanker companies can afford to do.

Most important is the low valuation of peers. Tanker stocks started to rally in April and May and have all pulled back in the past month. When I compared DHT to several other tanker stocks, it is at the bottom of the pack, with only a +15% gain in the past year. I see no good reason for this and believe the stock can play catch up and pay a good dividend too.

All forecasts and recommendations are based on opinion. Markets change direction with consensus beliefs, which may change at any time and without notice. The author/publisher of this publication has taken every precaution to provide the most accurate information possible. The information & data were obtained from sources believed to be reliable, but because the information & data source are beyond the author’s control, no representation or guarantee is made that it is complete or accurate.

The reader accepts information on the condition that errors or omissions shall not be made the basis for any claim, demand or cause for action. Because of the ever-changing nature of information & statistics the author/publisher strongly encourages the reader to communicate directly with the company and/or with their personal investment adviser to obtain up to date information.

Past results are not necessarily indicative of future results. Any statements non-factual in nature constitute only current opinions, which are subject to change. The author/publisher may or may not have a position in the securities and/or options relating thereto, & may make purchases and/or sales of these securities relating thereto from time to time in the open market or otherwise. Neither the information, nor opinions expressed, shall be construed as a solicitation to buy or sell any stock, futures or options contract mentioned herein. The author/publisher of this letter is not a qualified financial adviser & is not acting as such in this publication.

1) Ron Struthers: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: TC Energy Corp. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company currently has a financial relationship with the following companies mentioned in this article: None. I determined which companies would be included in this article based on my research and understanding of the sector.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services, or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees, or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in the securities mentioned. Directors, officers, employees, or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.