By JustMarkets

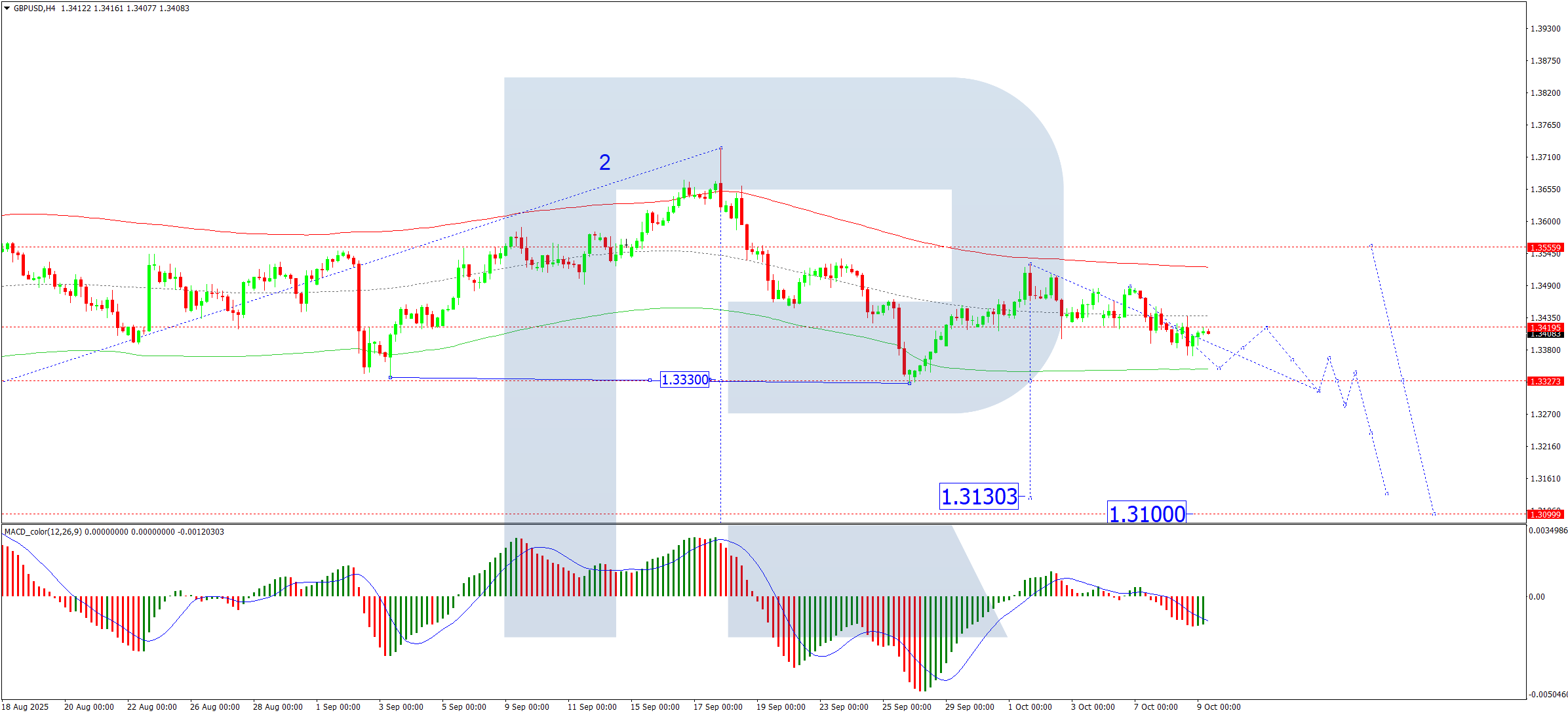

The Dow Jones (US30) Index fell by 0.01% at the close of Wednesday. The S&P 500 (US500) rose by 0.58%. The technological Nasdaq (US100) Index closed higher by 1.12%. The latest FOMC minutes showed that the majority of Federal Reserve officials noted the advisability of transitioning the federal funds rate to a more neutral level, as, in their view, the risks to employment had increased. However, according to the latest FOMC meeting minutes, the majority still emphasized that the risks to inflation remain tilted to the upside. Furthermore, a majority of participants deemed further policy easing likely for the remainder of the year, with about half of the officials expecting two more interest rate cuts by the end of 2025. Officials continued to state that they would weigh risks to both inflation and employment when considering their future actions.

AMD surged by 11.3% during the session and is up more than 40% since the start of the week as markets continued to price in the chipmaker’s deal with OpenAI, which marked over $1 trillion for the ChatGPT maker in a series of circular deals. Micron shares jumped 5.9%, while Nvidia, Oracle, and Amazon each rose by more than 2%. Cisco stock climbed 2% on the back of the release of a new artificial intelligence chip for data centers. Conversely, shares of defensive consumer companies and banks declined.

Stock markets in Europe rose yesterday. The German DAX (DE40) increased by 0.87%, the French CAC 40 (FR40) closed up by 1.07%, the Spanish IBEX35 (ES35) gained 0.97%, and the UK FTSE 100 (UK100) closed 0.69% higher. The Frankfurt DAX Index reached an all-time high on Wednesday. Market sentiment was lifted by new EU trade measures and plans to limit steel imports, although weak data from Germany and political uncertainty in France capped gains. Industrial production in Germany fell by 4.3% in August, the sharpest decline since March 2022, far exceeding the expected drop of 1%.

WTI oil prices rose by 1.5% to $62.65 per barrel after EIA data showed a sharp inventory drawdown at the key Cushing, Oklahoma hub. Inventories there shrank by 763,000 barrels last week, the largest drop since June, while nationwide crude inventories grew more than expected but remained close to seasonal lows. The report also showed a decline in refined product inventories, suggesting strengthening demand. Nevertheless, price gains were limited by expectations of abundant global supply. OPEC+ continues to ramp up production, and US oil output is expected to hit a record high this year.

Silver gained over 3% on Wednesday, nearing the $50 per ounce mark, an all-time high, as the protracted US government shutdown amid heightened geopolitical and economic uncertainty spurred demand for safe-haven assets. Markets are also anticipating the US Federal Reserve to cut its rate by a quarter point this month and likely one more in December. Concurrently, strong physical demand from the solar energy and electronics sectors continued to support prices, with the Silver Institute projecting a global supply deficit in 2025 for the fifth consecutive year.

Asian markets mostly fell yesterday. Japan’s Nikkei 225 (JP225) dropped by 0.45%, China’s FTSE China A50 (CHA50) did not trade yesterday, the Hang Seng (HK50) declined by 0.48%, and Australia’s ASX 200 (AU200) posted a negative result of 0.10%.

On Thursday, Chinese indices rose as mainland Chinese markets resumed trading after the long “Golden Week” holidays, during which a record 2.43 billion inter-regional passenger trips were recorded. Mining stocks led the gains after Beijing imposed export controls on rare-earth processing technology in a bid to solidify its dominance in the sector amid growing competition with the US.

The Australian dollar (AUD) climbed to around $0.660 on Thursday, extending gains from the previous session, as higher inflation expectations strengthened the Reserve Bank of Australia’s (RBA) hawkish stance. Consumer inflation expectations rose to 4.8% in October 2025 from 4.7% in September, the highest since June, on fears that third-quarter inflation could top prognoses. This reinforces the Central Bank’s cautious position, which is expected to keep its policy rate unchanged after setting it at 3.6% in September.

On Thursday, the New Zealand dollar (NZD) rose to $0.58, recovering from losses during the previous session when the Reserve Bank surprised markets with a larger-than-expected rate cut. On Wednesday, the Central Bank slashed the official cash rate (OCR) by 50 basis points to 2.50%, the lowest level since July 2022, citing concerns over the unsustainable state of the economy and leaving the door open for further easing. Markets are pricing in an 80% chance of a 25 bps rate cut at the RBNZ’s next meeting in November, and see roughly even odds that rates could fall to 2.0% by next year.

S&P 500 (US500) 6,753.72 +39.13 (+0.58%)

Dow Jones (US30) 46,601.78 −1.20 (−0.01%)

DAX (DE40) 24,597.13 +211.35 (+0.87%)

FTSE 100 (UK100) 9,548.87 +65.29 (+0.69%)

USD Index 98.85 +0.28 (+0.28%)

News feed for: 2025.10.09

- German Trade Balance (m/m) at 09:00 (GMT+3);

- Eurozone ECB Monetary Meeting Accounts at 14:30 (GMT+3);

- Mexico Inflation Rate (m/m) at 15:00 (GMT+3);

- US Initial Jobless Claims (w/w) at 15:30 (GMT+3) (Tentative);

- US Fed Chair Powell Speaks at 15:30 (GMT+3);

- US Natural Gas Storage (w/w) at 17:30 (GMT+3).

By JustMarkets

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

{kind=link}