By JustForex

The US indices fell on Tuesday as investors raised their bearish rates over fears that the Federal Reserve might signal a continuation of aggressive rate hikes. The Fed’s willingness to continue tightening monetary policy brings the economic recession closer. The bond market continues to signal the risk of a broader recession as the continued inversion in the key part of the Treasury yield curve has intensified further. As the stock market closed on Tuesday, the Dow Jones Index (US30) decreased by 1.01%, and the S&P 500 Index (US500) lost 1.13%. The NASDAQ Technology Index (US100) fell by 2.52% yesterday.

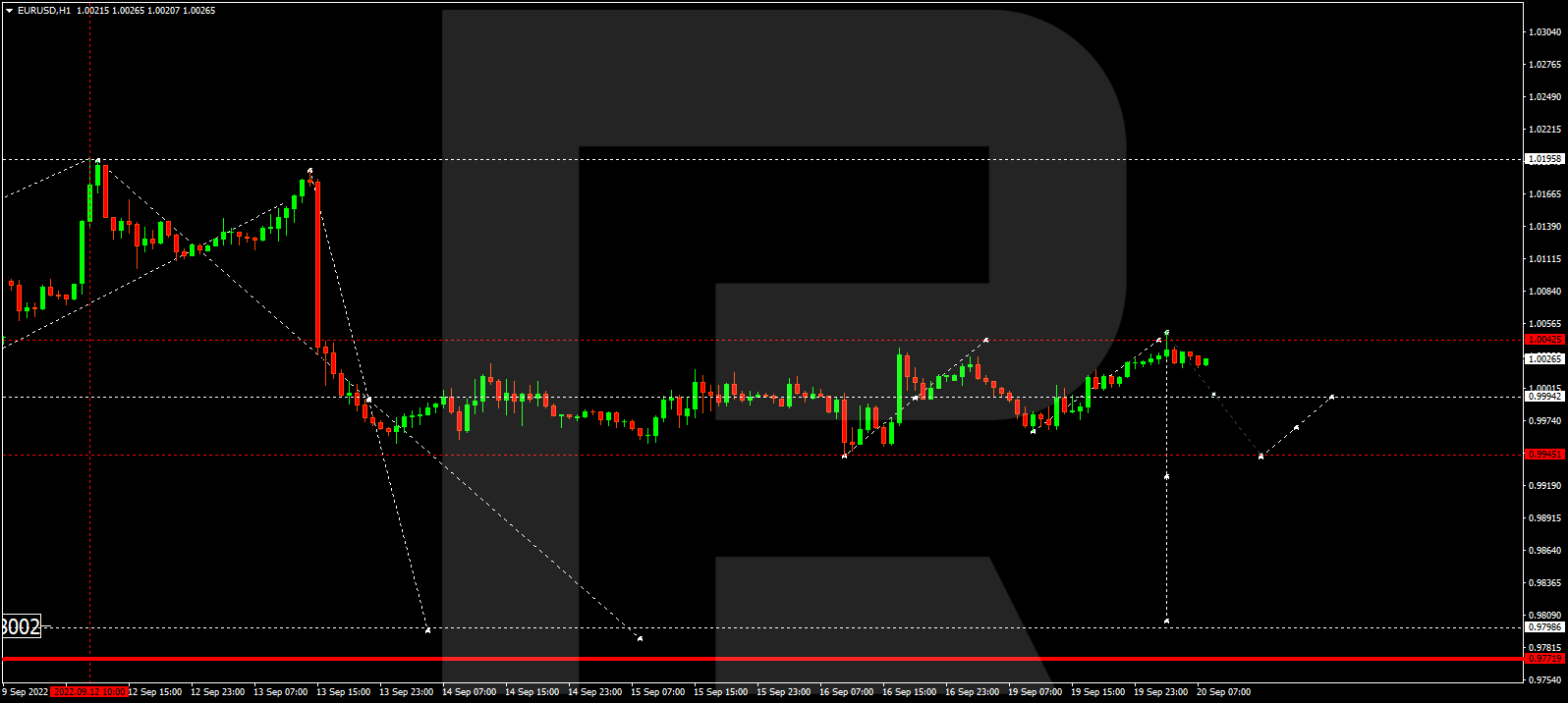

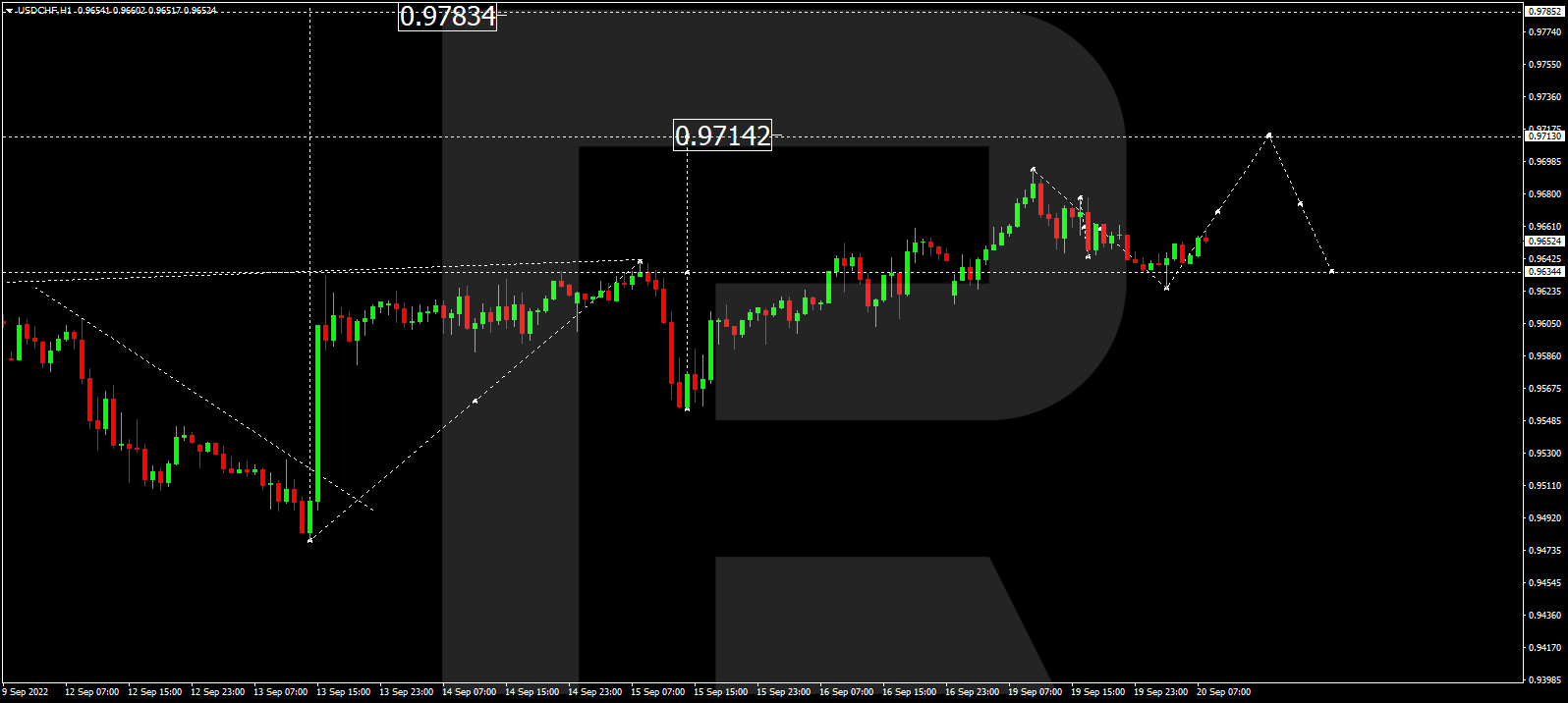

The Fed has an important monetary policy meeting today. Analysts expect the US Federal Reserve to raise interest rates by 0.75% for the third time in a row. If the data is worse than expected and the Fed raises the rate by 1%, the dollar index may see upward momentum. If, on the contrary, the Fed raises interest rates by 0.5%, the dollar index is likely to fall sharply as the Fed is less aggressive. If the fact is as expected, there is a high probability that the market will just temporarily increase volatility.

ECB head Christine Lagarde said yesterday that Europe is experiencing a record-high inflation rate for the tenth month in a row, and this streak will continue soon. When inflation is high, monetary policy cannot remain expansionary. That is why the ECB is pursuing a strategy of monetary policy normalization. Normalization involves stopping net asset purchases and then raising rates to a neutral level that is neither stimulative nor restrictive. This is why the ECB has not only begun to raise interest rates but has indicated that it expects to raise interest rates further over the next few meetings. The ECB will reconsider whether the normalization strategy is enough to return to 2% inflation in the medium term.

The Netherlands imposed price caps on gas and electricity on January 1.

Oil falls ahead of the Fed’s interest rate decision. The dollar rose for the third time in four sessions, adding weight to oil prices as industry analysts forecast a third consecutive weekly increase in domestic crude inventories.

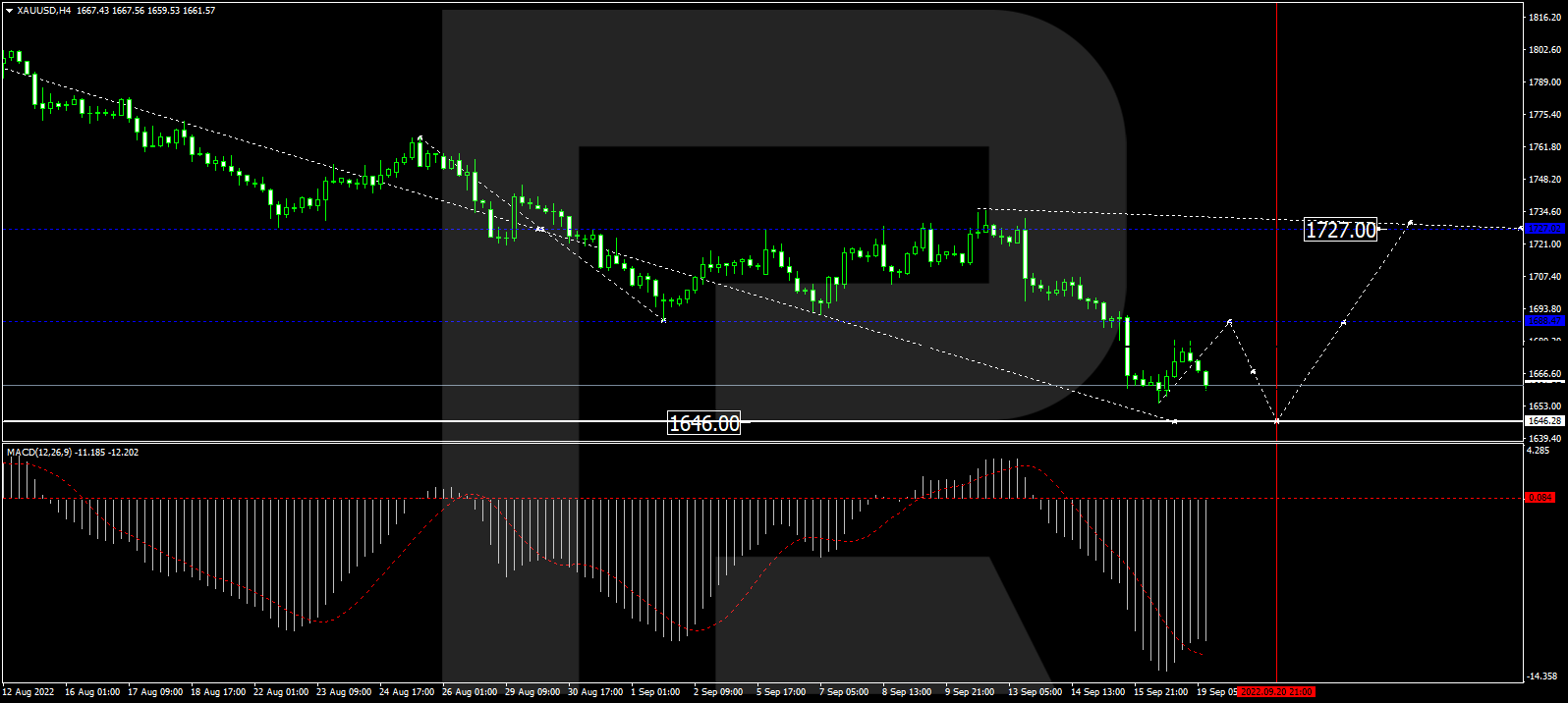

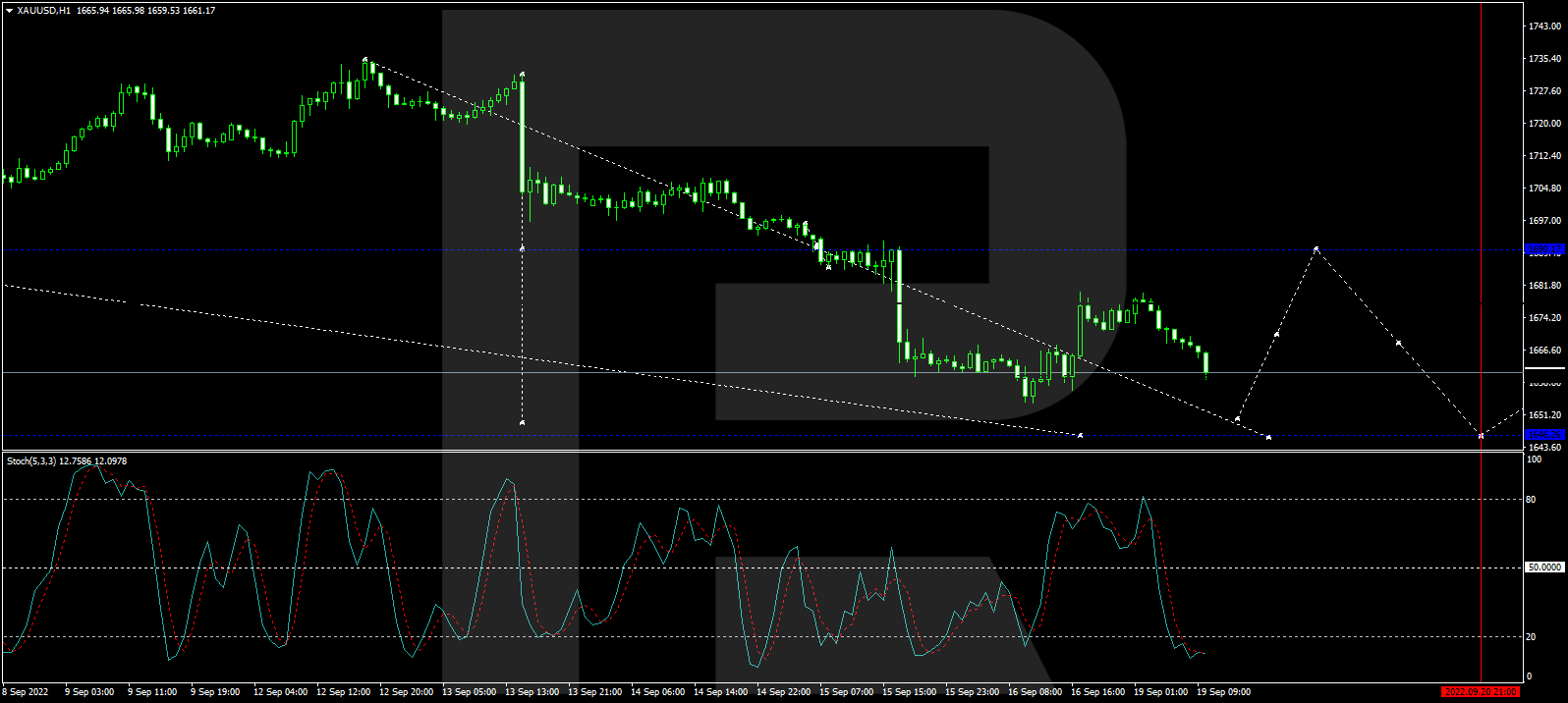

Gold prices are stuck at $1,600 a dollar, falling for the fifth time in six days. The rise in the dollar index is the main catalyst for gold’s weakness. Gold has lost about 4% in the last six sessions. Gold and silver could fall sharply if Powell can convince markets today not only that they will continue to aggressively tighten policy but that they will keep rates in place even as the economic downturn worsens.

Putin has announced a partial military mobilization in Russia. The Kremlin is still not calming down and has once again begun to intimidate Ukraine and the West with nuclear weapons.

Asian markets traded lower yesterday. Japan’s Nikkei 225 (JP225) gained 0.44%, Hong Kong’s Hang Seng (HK50) added 1.16% on Tuesday, while Australia’s S&P/ASX 200 (AU200) was up by 1.29% on the day.

China kept its benchmark lending rates on hold on Tuesday, as expected, as authorities postponed immediate monetary policy easing after a sharp drop in the local currency. The benchmark one-year lending rate (LPR) was kept at 3.65%, while the five-year LPR remained unchanged at 4.30%. Analysts believe that the growing divergence in the US and Chinese monetary policy could heighten fears of capital flight from China as Beijing seeks to mobilize resources to restore sluggish growth.

S&P 500 (F) (US500) 3,855.93 −43.96 (−1.13%)

Dow Jones (US30) 30,706.23 −313.45 (−1.01%)

DAX (DE40) 12,670.83 −132.41 (−1.03%)

FTSE 100 (UK100) 7,192.66 −44.02 (−0.61%)

USD Index 110.15 +0.41 (+0.38%)

- – US Existing Home Sales (m/m) at 17:00 (GMT+3);

- – US Crude Oil Reserves (w/w) at 17:30 (GMT+3);

- – US Fed Interest Rate Decision at 21:00 (GMT+3);

- – US FOMC Statement at 21:00 (GMT+3);

- – US FOMC Economic Projections at 21:00 (GMT+3);

- – US FOMC Press Conference at 21:30 (GMT+3).

By JustForex

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.