Global investors are “desperate for signs” that China’s Xi and France’s Macron can secure better business ties between China and the EU during the French President’s three-day visit to Beijing and Guangzhou.

The assessment from Nigel Green, CEO of deVere Group, one of the world’s largest independent financial advisory, asset management and fintech organisations, comes as a state visit by Emmanuel Macron to China kicked off on Wednesday.

He will have extended face time with Xi, and after formal meetings in Beijing on Thursday, which will also include European Commission President Ursula von der Leyen, the two national leaders will head to the southern city of Guangzhou.

Key themes said to be planned for discussion will be the Ukraine war, the climate crisis, renewable energy, and travel following the lifting of zero-Covid regulations by Beijing.

Nigel Green comments: “Geopolitical issues are at the top of the agenda for Macron’s visit to Xi in China.

“But as many top business leaders from France have also been invited along, and because Macron will meet with Chinese investors in Guangzhou, there are hopes that international trading relations will also be a major priority.

“Global investors are desperate for signs that Xi and Macron can secure better business ties between China and the EU.”

The EU is already China’s largest trading partner, and China is the EU’s second-largest trading partner.

In January 2021, the trade deficit was €14.6 billion. It reached a high of €36.0 billion in September 2022 before falling to €27.4 billion in December 2022.

Recent developments have “reignited” global investors’ interest in the world’s second largest economy.

“The break-up of Alibaba, the Chinese mega-conglomerate, in the last couple of weeks is, we believe, the start of a wave of enormous opportunities in China for investors from around the world,” says the deVere CEO.

“It represents the end of Beijing-led regulatory crackdowns on various sectors, including tech, real estate and education, which have deterred foreign investors from China in the last few years.”

He continues: “The cooling of corporate crackdowns, and Beijing seemingly becoming more pro-private enterprise, also coincides with the re-opening of the world’s second largest economy following years of Covid restrictions and as the Chinese currency, the yuan, becomes more dominant in international finance.”

Russia’s Vladimir Putin has recently stated that his country is now in favour of using the Chinese yuan for oil settlements, rather than the US dollar. It’s also been reported that Saudi Arabia is in talks with Beijing to use the Chinese currency, instead of the dollar for oil trades.

“Global investors are increasingly bullish on China and financial markets around the world are hoping for indicators of a strengthening relationship between the European Union (EU) and China during this important state visit,” confirms Nigel Green.

“A stronger relationship would lead to increased trade and investment between the two regions, creating new opportunities for businesses and investors in both regions, leading to access to new markets, and increased profitability and growth.”

“Stronger ties would also reduce uncertainty in financial markets, meaning a more stable and predictable environment for investors.”

He concludes: “Global investors will be carefully analysing the words and actions of Xi and Macron over the next few days in order to seize opportunities and sidestep potential risks.”

About:

deVere Group is one of the world’s largest independent advisors of specialist global financial solutions to international, local mass affluent, and high-net-worth clients. It has a network of more than 70 offices across the world, over 80,000 clients and $12bn under advisement.

UK high-street banks that are imposing limits and restrictions on their customers who are investing in cryptocurrency have been slammed as using “an outrageous, overreaching diktat” against account holders by the CEO of one of the world’s largest independent financial advisory, asset management and fintech organizations.

The criticism from deVere Group’s Nigel Green follows reports that some of the country’s biggest banks have “cracked down” by applying daily limits for customers, restricting credit cards from making crypto purchases, banning customers from buying stocks of companies with Bitcoin exposure and, in some cases, temporarily freezing accounts.

Nigel Green says: “Your bank has no business telling you how or what to invest in, if what you’re planning to invest in is perfectly legal – which crypto is in the UK.

“This kind of control over people’s private, personal financial decision-making sounds like something from the pages of Orwell’s 1984 and goes against the values of Britain’s proud banking heritage.”

Most of the banks say that they are imposing the new restrictions to help protect customers and to try and keep their money safe.

“Of course, this is a noble ambition and part of a bank’s remit.

“However, the actions that they are imposing imply that potential illicit activity is unique to crypto and not the traditional financial system – which is, of course, complete nonsense.

“Why have they decided to ‘step up’ on crypto but not in other areas where their customers may or may not decide to invest?” says the deVere CEO.

“It appears that some banks are using an outrageous, overreaching diktat against account holders because they are anti-crypto over concerns it poses a threat to the power and influence of traditional banking, presumably.

“But, again, you should be free to do with your own money as you please – even if they disagree with it.

“What comes next? Will they move on to placing restrictions on those who invest in alcohol, tobacco or energy companies, or those who make political donations to parties they deem unsuitable, for example?”

He adds: “It’s an infringement on your privacy, rights, and ability to control your own money.”

The comments from Nigel Green come as institutional investors are once again increasing their exposure to cryptocurrencies such as Bitcoin. Michael Saylor’s MicroStrategy is amongst them.

MicroStrategy, whose primary focus is on developing and selling software that enables companies to analyse and visualise large amounts of data, using tools such as dashboards and reports, has bought 6,455 Bitcoins over the last five weeks, according to a recent filing with the US financial regulator, the SEC.

Institutional investors, like individuals, are investing in cryptocurrencies for various reasons. These include portfolio diversification, the potential for high returns, a hedge against inflation, and access to a new future-focused asset class.

About:

deVere Group is one of the world’s largest independent advisors of specialist global financial solutions to international, local mass affluent, and high-net-worth clients. It has a network of more than 70 offices across the world, over 80,000 clients and $12bn under advisement.

The US stock indices were mostly up on Monday as energy stocks rose on higher oil prices after the Organization of the Petroleum Exporting Countries and its allies (OPEC+) unexpectedly cut oil production by 1 million BPD. As the stock market closed Monday, the Dow Jones Index (US30) increased by 0.98%, and the S&P 500 Index (US500) added 0.37%. Technology Index NASDAQ (US100) lost 0.27% yesterday.

In the US, the ISM manufacturing activity index fell to 46.3 in March from 47.7 a month earlier, while the pay-per-view price index fell to 49.2 from 51.3, indicating that the disinflationary trend in the commodities sector also remains unchanged.

Elon Musk believes that interest rate hikes by the Federal Reserve will hurt companies and provoke an economic downturn. The head of Twitter agreed with the opinion of his longtime friend, venture capitalist David Sachs, who pointed out that further Fed interest rate increases could hit banks, commercial real estate, and national debts. According to Sachs, the first stage of the crisis has already begun, with the second and third stages still to come.

Stock markets in Europe were trading Monday without a single dynamic. German DAX (DE30) decreased by 0.31%, and French CAC 40 (FR40) added 0.32%, Spanish IBEX 35 (ES35) was down by 0.81%, British FTSE 100 (UK100) closed yesterday up by 0.54%.

European business activity data showed no significant changes over the last month. Most industries are in contraction territory, and as long as the ECB raises interest rates and tightens the screws on the banking sector, the situation is unlikely to improve anytime soon.

Gold is back to the $2000 an-ounce mark. Gold has a lot of fundamentals for strengthening right now. The banking crisis, the impending recession in the US and Europe, and falling government bond yields on the soon-to-be-completed tightening cycle. In addition, the sanctioning countries are actively getting rid of dollar reserves, increasing gold reserves. There are all preconditions for the continuation of the medium-term upward movement.

Due to voluntary cuts in oil production by OPEC countries, oil prices posted their biggest one-day gain of the year. The US West Texas Intermediate (WTI) ended Monday trading at $80.42, plus 6.3% for the day. Brent closed at $84.93, also plus 6.3% for the day. Traders and analysts are already analyzing what the Federal Reserve will do in terms of raising rates to counter the new inflationary pressure that is almost inevitable because of OPEC’s inflated oil price. Analysts are predicting a further rise in quotes, up to $90-100 per barrel.

Asian markets were mostly on the rise yesterday. Japan’s Nikkei 225 (JP225) gained 0.52%, China’s FTSE China A50 (CHA50) decreased by 0.16%, Hong Kong’s Hang Seng (HK50) gained 0.04%, India’s NIFTY 50 (IND50) gained 0.22%, and Australia’s S&P/ASX 200 (AU200) increased by 0.63% on the day.

The Reserve Bank of Australia (RBA) kept interest rates at 3.6%, signaling a pause in its rate hike cycle. The bank said it wanted to see the full effect of the rate hike and assess Australia’s economic prospects while noting that inflation has probably peaked. But with inflation still well above the bank’s target range of 2% to 3%, the RBA warned that further monetary tightening might be needed.

The Reserve Bank of New Zealand will hold its monetary policy meeting tomorrow. Investors expect a 0.25% rate hike with a hint of an end to the tightening cycle. New Zealand’s GDP fell by 0.6% in the last quarter of 2022, more than the RBNZ forecast in its last report. Meanwhile, GDP growth and inflation are expected to be negative in the first half of 2023 due to disruptions from hurricanes on the North Island.

According to analysts, the Monetary Authority of Singapore (MAS) is likely to tighten monetary policy this month amid continuing price pressures. It should be noted that instead of interest rates, MAS manages policy by allowing the local dollar to rise or fall against the currencies of its major trading partners within an undisclosed range known as the Nominal Effective Exchange Rate of the Singapore dollar. The Reserve Bank of India is also set to meet later this week and is expected to raise interest rates.

S&P 500 (F) (US500) 4,124.51 +15.20 (+0.37%)

Dow Jones (US30)33,601.15 +327.00 (+0.98%)

DAX (DE40) 15,580.92 −47.92 (−0.31%)

FTSE 100 (UK100) 7,673.00 +41.26 (+0.54%)

USD Index 102.04 −0.36 (−0.45%)

Important events for today:

– Australia RBA Interest Rate Decision at 07:30 (GMT+3);

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

Brazilian president Luiz Inácio Lula da Silva was scheduled to visit his Chinese counterpart Xi Jinping at the end of March. Beijing would have been Lula’s fourth international destination in less than 100 days in office.

Lula had to cancel his trip, which was set to include 200 business people, after catching pneumonia but it is now expected to take place in April or May. His administration had hoped the China visit would alleviate political pressure at home.

Since returning to the presidency (his previous term was 2003-2010), Lula has already been to visit partners in the South American trade bloc Mercosur, Argentina and Uruguay, and recently flew to Washington DC for conversations with US president Joe Biden and members of the Democratic party over infrastructure investments, trade and climate change.

Globetrotting seems like quite an effort for a 77-year-old, third-term president who faces a deeply divided society. But Lula does it with a smile on his face. Since he first took office 20 years ago, the former metalworker has risen to the challenge of international diplomacy as a natural negotiator with political charm.

Building political legitimacy

As Lula kicks off his third term, foreign policy will be a tool for building his own domestic political legitimacy. His reputation currently appears to be greater abroad than at home.

Always a determined player on the international stage, Lula’s administration spearheaded the construction of Unasur, a South American organisation set up to offset US economic and political power in the region. He also forged several alliances in the developing world.

Although Lula left office in 2010 with an impressive 83% approval rating, much of his political capital waned in the years that followed. This was largely thanks to his successor Dilma Rousseff’s pitiful economic performance and to the mounting accusations of graft against top figures in his Workers’ party.

So, at the age of 77 – and with health problems – a big diplomatic play might be his best bet of leaving a presidential legacy.

Challenges of a new world order

But Brazil’s capacity as a meaningful international player will depend on the administration’s ability to navigate a world that is fundamentally different from the one of the early 2000s.

So, while Lula must capitalise on any residual international popularity to relaunch Brazil as a global player, he has a lot to do to restore his own country’s economy and to heal the wounds of a divided society.

Lula’s first task internationally – a tough challenge – is to strike a balance in his relationships with Washington and Beijing, Brazil’s two foremost partners. So far, his new administration’s even-handed strategy has worked fine. But if tensions between Joe Biden and Xi Jinping lead to further political instability – or if a Republican with a zero-sum approach to China gets elected in 2024, Brazil could find itself in a difficult position.

Lula has attempted to anticipate these problems by offering to broker peace between Russia and Ukraine. It was a way to dodge criticism by western powers, who wanted Brazil to engage in military assistance to the Ukrainian government – while still preserving Brazil’s longstanding ties with Russia.

Lula’s take on the war is part of what researchers have dubbed “active non-alignment”. It is part of a broader Latin American strategy to safeguard policy space and instruments for national development strategies in an increasingly polarised international order. By offering itself as a high-profile mediator, Brazil wants to maintain trade and cooperation with all sides in the conflict.

Lula’s balancing trick

But Russian-Ukrainian peace appears to be a long way off – and it will hardly come via mediators from the developing world. If Lula wants to create a legacy, he needs to build on Brazil’s preexisting capacity, in both multilateral and regional terms.

One possible way is to restore Brazil’s activism at the United Nations. He must also reestablish cooperation in issues as diverse as climate change, biodiversity, indigenous rights, vaccines, food security and development.

Another way is to rebuild South American integration. Regional organisations such as Mercosur and Unasur could help bolster global supply chains in critical sectors like energy and food that have been disrupted by the war in Ukraine. To do so, Brazil must reclaim its role as the continent’s centre of economic gravity.

But there is an obstacle: Venezuelan president Nicolás Maduro. A persistent political, economic and humanitarian crisis in Venezuela has exposed the dangers of left-wing authoritarianism. Lula is one of the few leaders who have open channels with Maduro and may be able to help the country work towards a national reconciliation.

The question is whether Lula wants to get involved. Unlike left-wing leaders who recently rose to power in Chile and Colombia, Lula and the Workers’ party have been unapologetically sympathetic towards dictators such as Venezuela’s Maduro and Nicaragua’s Daniel Ortega.

Overcoming the Brazilian left’s outdated views on authoritarian socialism and anti-imperialism may be as daunting a challenge for the Lula administration as leaving a sound diplomatic legacy. But both steps are necessary if Lula really wants to make a difference in the region – and the world.

European shares were painted green on Tuesday even as oil prices extended gains following the unexpected production cuts from OPEC+ on Sunday. However, a sense of caution lingered in the air with US equity futures pointing to a mixed open amid the prospects of higher oil prices fueling fears of higher inflation. In the currency space, the dollar found itself pressured by weak economic data and expectations around the Fed potentially pivoting down the road. Gold struggled for direction while WTI crude ventured towards $81 after surging more than 6% in the previous session.

The next few days promise to be eventful for financial markets thanks to the latest developments concerning OPEC+, with more volatility expected despite the holiday-shortened week. Investors will be presented with key economic data from major economies, speeches by financial heavyweights, and the US jobs report on Friday. The spike in oil prices and renewed fears around rising inflation are likely to spice things up, together with thin liquidity on Friday which could result in whippy price action across the board.

In overnight news, the Reserve Bank of Australia (RBA) left its key interest rate unchanged in April marking its first pause since lifting rates in May 2022. However, the RBA left the door open to future rate hikes in the future to ensure that inflation returned to target. Markets responded by sending the Australian dollar lower across the board.

Are Oil bulls back in town?

Oil prices have certainly kicked off the new quarter on a solid note.

The global commodity extended gains this morning after surging over 6% on Monday following the OPEC+ shock decision to cut production over the weekend. Given how this announcement came just a day after OPEC members indicated that they would keep production policy unchanged, the cartel completely caught markets off-guard. OPEC+ decided to lower oil output by over 1 million barrels per day starting in May as a “precautionary measure” aimed at promoting market stability. Nevertheless, the prospects of higher oil prices in the face of tighter supply could spark fears around rising inflation. In the meantime, WTI has staged a sharp rebound and is currently approaching resistance around $82. A strong breakout and weekly close above this point could open the door toward $90.

All eyes on the NFP report

Friday’s March nonfarm payrolls (NFP) report could play in role in determining whether the Federal Reserve raises interest rates by 25 basis points in May. Expectations are rising over rates reaching their peak with the chances of another 25-basis point move in May currently priced at 67%, according to Fed funds futures. The US economy is projected to have created 240,000 jobs in March with the unemployment rate unchanged at 3.6% and average hourly earnings rising 4.3% year-on-year. A stronger-than-expected report is likely to feed expectations around the Fed cautiously raising interest rates while paying attention to the US banking sector. Alternatively, further signs of a weakening labour markets may fuel speculation around the Fed pausing its rate hikes, before cutting them into the latter part of the year. It will be interesting to see how the Fed reacts to the latest developments concerning OPEC+ and whether this will invite hawks back into the scene.

The dollar has kicked off Q2 on a negative note with the Dollar Index extending losses on Tuesday. Prices remain under pressure with downside momentum potentially taking the DXY towards 101.50 in the short term.

Commodity Spotlight – Gold

Gold struggled for direction Tuesday as oil prices hijacked the spotlight.

It feels like the precious metal could be waiting for a fresh fundamental spark and this could come in the form of the US jobs report on Friday. A stronger-than-expected US jobs report may be bad news for zero-yielding gold, as markets evaluate the possibility of the Fed raising interest rates further. Alternatively, a disappointing NFP report could feed speculation around the Fed pivoting, ultimately supporting gold bulls. Looking at the technical picture, gold has found itself back within a choppy range with support at $1950 and resistance at $2000. Prices are likely to range until a weekly close is achieved above or below the identified support or resistance levels.

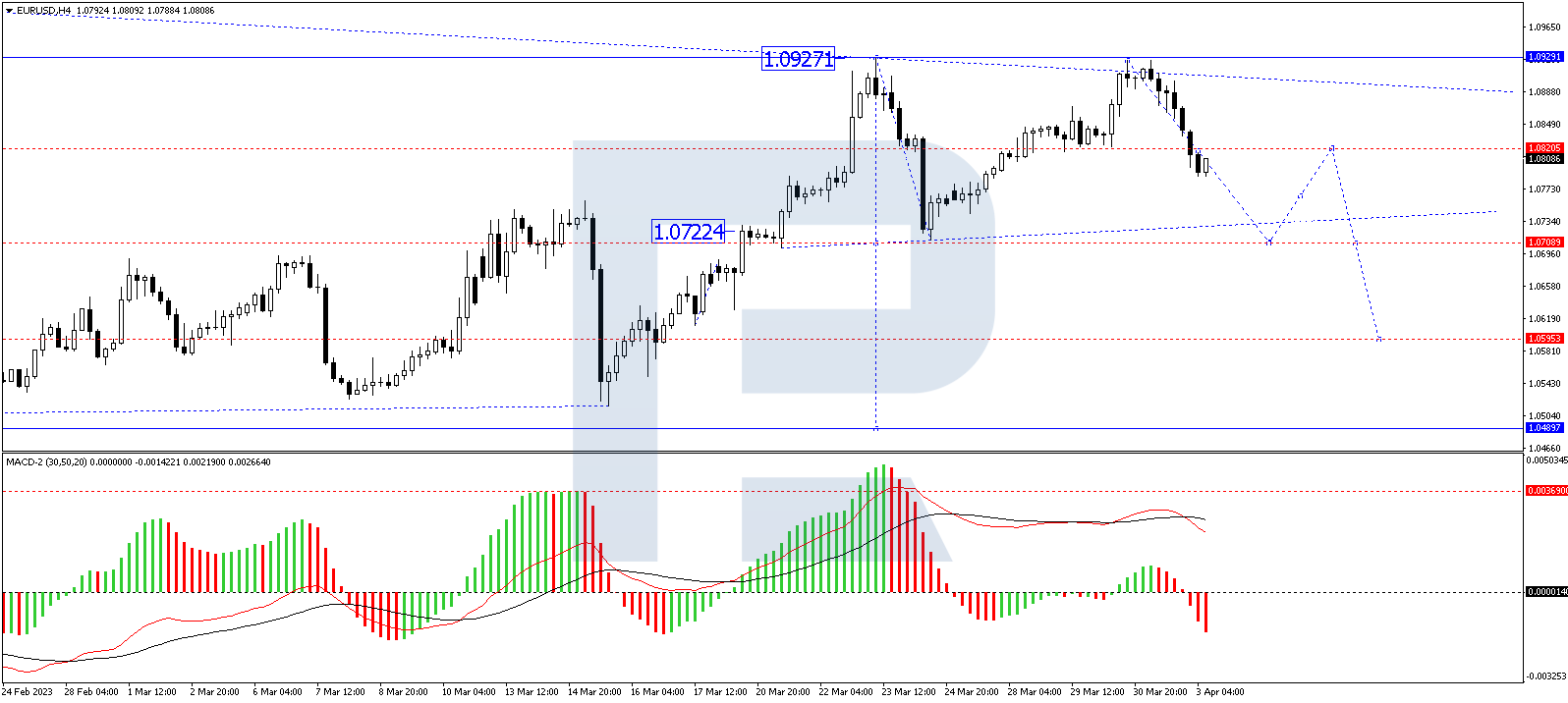

The EUR/USD pair is trading close to the 1.0900 level on the first Tuesday of April. The market is taking into consideration the latest data on the Core PCE index, which grew by only 0.3% m/m in February, lower than the expected figures. The year-to-year data also dropped by 5.0%, which could be a reason for the Federal Reserve System to pause in its monetary policy tightening.

Despite the fact that no meetings of the Fed management are scheduled for April, investors will keep a close eye on important statistics from the US this week. This includes the PMI in services and production, the factory orders report, and the employment market statistics of last month.

Looking at the technical analysis, the EUR/USD pair has formed a structure of a declining impulse to 1.0788 on H4, and the market is currently consolidating above this level. There is a possibility of a link of growth to 1.0850, followed by a decline to 1.0707, from where the wave could extend to 1.0595. The MACD confirms this scenario, with its signal line above zero and aiming downwards to renew the lows.

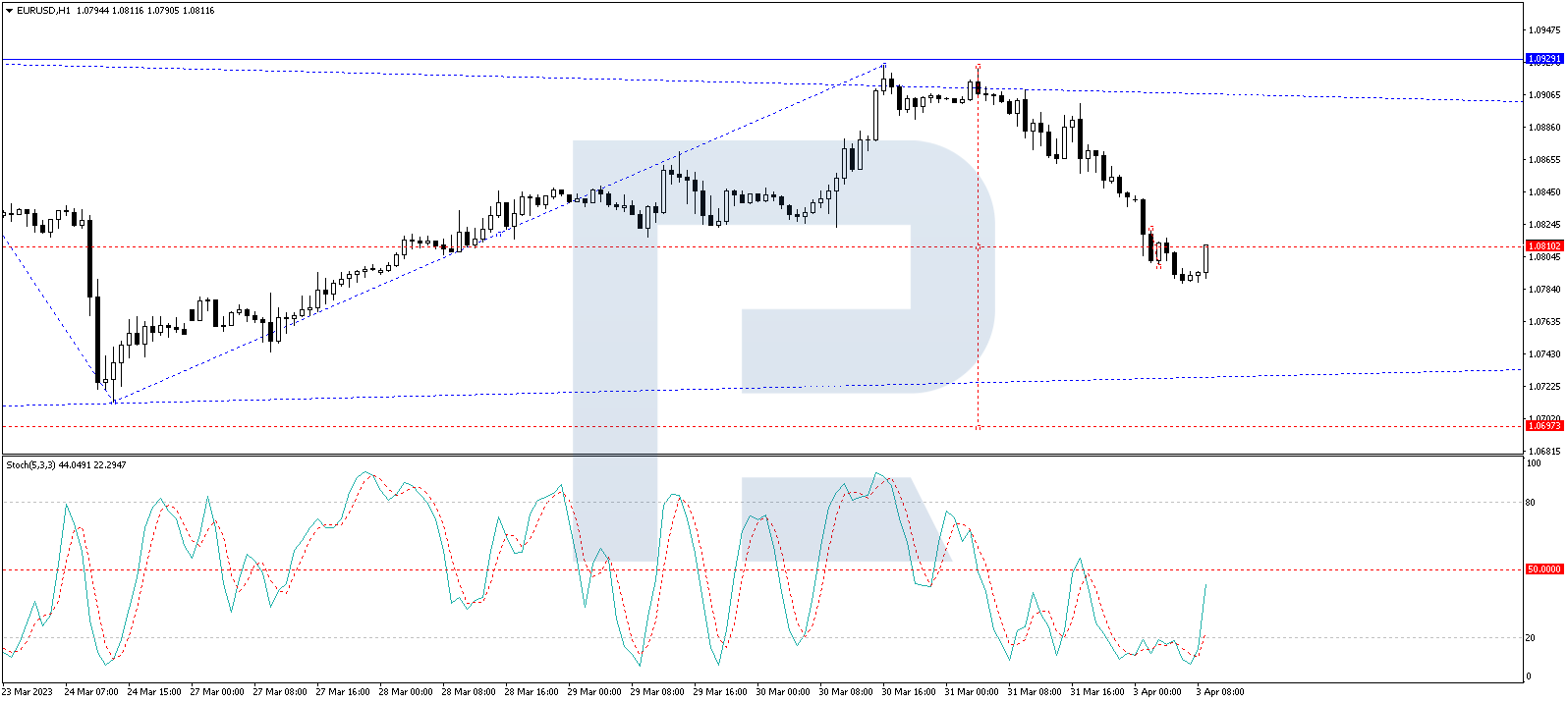

On H1, the EUR/USD pair has completed the structure of a declining wave to 1.0788, and a consolidation range is forming above this level. The price is expected to break the range upwards, reaching 1.0850, and then decline to 1.0697. The target is local, and this is only half of the declining wave. The Stochastic oscillator confirms this scenario, with its signal line near 50, expected to grow to 80 and then fall to 20.

Overall, the market is closely monitoring the data releases from the US this week and waiting for further signals from the Federal Reserve System to make a weighted decision on its monetary policy.

Disclaimer

Any forecasts contained herein are based on the author’s particular opinion. This analysis may not be treated as trading advice. RoboForex bears no responsibility for trading results based on trading recommendations and reviews contained herein.

From fake photos of Donald Trump being arrested by New York City police officers to a chatbot describing a very-much-alive computer scientist as having died tragically, the ability of the new generation of generative artificial intelligence systems to create convincing but fictional text and images is setting off alarms about fraud and misinformation on steroids. Indeed, a group of artificial intelligence researchers and industry figures urged the industry on March 29, 2023, to pause further training of the latest AI technologies or, barring that, for governments to “impose a moratorium.”

These technologies – image generators like DALL-E, Midjourney and Stable Diffusion, and text generators like Bard, ChatGPT, Chinchilla and LLaMA – are now available to millions of people and don’t require technical knowledge to use.

Given the potential for widespread harm as technology companies roll out these AI systems and test them on the public, policymakers are faced with the task of determining whether and how to regulate the emerging technology. The Conversation asked three experts on technology policy to explain why regulating AI is such a challenge – and why it’s so important to get it right.

To jump ahead to each response, here’s a list of each:

S. Shyam Sundar, Professor of Media Effects & Director, Center for Socially Responsible AI, Penn State

The reason to regulate AI is not because the technology is out of control, but because human imagination is out of proportion. Gushing media coverage has fueled irrational beliefs about AI’s abilities and consciousness. Such beliefs build on “automation bias” or the tendency to let your guard down when machines are performing a task. An example is reduced vigilance among pilots when their aircraft is flying on autopilot.

Numerous studies in my lab have shown that when a machine, rather than a human, is identified as a source of interaction, it triggers a mental shortcut in the minds of users that we call a “machine heuristic.” This shortcut is the belief that machines are accurate, objective, unbiased, infallible and so on. It clouds the user’s judgment and results in the user overly trusting machines. However, simply disabusing people of AI’s infallibility is not sufficient, because humans are known to unconsciously assume competence even when the technology doesn’t warrant it.

Research has also shown that people treat computers as social beings when the machines show even the slightest hint of humanness, such as the use of conversational language. In these cases, people apply social rules of human interaction, such as politeness and reciprocity. So, when computers seem sentient, people tend to trust them, blindly. Regulation is needed to ensure that AI products deserve this trust and don’t exploit it.

AI poses a unique challenge because, unlike in traditional engineering systems, designers cannot be sure how AI systems will behave. When a traditional automobile was shipped out of the factory, engineers knew exactly how it would function. But with self-driving cars, the engineers can never be sure how it will perform in novel situations.

Lately, thousands of people around the world have been marveling at what large generative AI models like GPT-4 and DALL-E 2 produce in response to their prompts. None of the engineers involved in developing these AI models could tell you exactly what the models will produce. To complicate matters, such models change and evolve with more and more interaction.

All this means there is plenty of potential for misfires. Therefore, a lot depends on how AI systems are deployed and what provisions for recourse are in place when human sensibilities or welfare are hurt. AI is more of an infrastructure, like a freeway. You can design it to shape human behaviors in the collective, but you will need mechanisms for tackling abuses, such as speeding, and unpredictable occurrences, like accidents.

AI developers will also need to be inordinately creative in envisioning ways that the system might behave and try to anticipate potential violations of social standards and responsibilities. This means there is a need for regulatory or governance frameworks that rely on periodic audits and policing of AI’s outcomes and products, though I believe that these frameworks should also recognize that the systems’ designers cannot always be held accountable for mishaps.

Artificial intelligence researcher Joanna Bryson describes how professional organizations can play a role in regulating AI.

Combining ‘soft’ and ‘hard’ approaches

Cason Schmit, Assistant Professor of Public Health, Texas A&M University

Regulating AI is tricky. To regulate AI well, you must first define AI and understand anticipated AI risks and benefits. Legally defining AI is important to identify what is subject to the law. But AI technologies are still evolving, so it is hard to pin down a stable legal definition.

Understanding the risks and benefits of AI is also important. Good regulations should maximize public benefits while minimizing risks. However, AI applications are still emerging, so it is difficult to know or predict what future risks or benefits might be. These kinds of unknowns make emerging technologies like AI extremely difficult to regulate with traditional laws and regulations.

“Soft laws” are the alternative to traditional “hard law” approaches of legislation intended to prevent specific violations. In the soft law approach, a private organization sets rules or standards for industry members. These can change more rapidly than traditional lawmaking. This makes soft laws promising for emerging technologies because they can adapt quickly to new applications and risks. However, soft laws can mean soft enforcement.

Copyleft licensing allows for content to be used, reused or modified easily under the terms of a license – for example, open-source software. The CAITE model uses copyleft licenses to require AI users to follow specific ethical guidelines, such as transparent assessments of the impact of bias.

In our model, these licenses also transfer the legal right to enforce license violations to a trusted third party. This creates an enforcement entity that exists solely to enforce ethical AI standards and can be funded in part by fines from unethical conduct. This entity is like a patent troll in that it is private rather than governmental and it supports itself by enforcing the legal intellectual property rights that it collects from others. In this case, rather than enforcement for profit, the entity enforces the ethical guidelines defined in the licenses – a “troll for good.”

This model is flexible and adaptable to meet the needs of a changing AI environment. It also enables substantial enforcement options like a traditional government regulator. In this way, it combines the best elements of hard and soft law approaches to meet the unique challenges of AI.

Though generative AI has been grabbing headlines of late, other types of AI have been posing challenges for regulators for years, particularly in the area of data privacy.

Four key questions to ask

John Villasenor, Professor of Electrical Engineering, Law, Public Policy, and Management, University of California, Los Angeles

The extraordinary recent advances in large language model-based generative AI are spurring calls to create new AI-specific regulation. Here are four key questions to ask as that dialogue progresses:

1) Is new AI-specific regulation necessary? Many of the potentially problematic outcomes from AI systems are already addressed by existing frameworks. If an AI algorithm used by a bank to evaluate loan applications leads to racially discriminatory loan decisions, that would violate the Fair Housing Act. If the AI software in a driverless car causes an accident, products liability law provides a framework for pursuing remedies.

2) What are the risks of regulating a rapidly changing technology based on a snapshot of time? A classic example of this is the Stored Communications Act, which was enacted in 1986 to address then-novel digital communication technologies like email. In enacting the SCA, Congress provided substantially less privacy protection for emails more than 180 days old.

The logic was that limited storage space meant that people were constantly cleaning out their inboxes by deleting older messages to make room for new ones. As a result, messages stored for more than 180 days were deemed less important from a privacy standpoint. It’s not clear that this logic ever made sense, and it certainly doesn’t make sense in the 2020s, when the majority of our emails and other stored digital communications are older than six months.

A common rejoinder to concerns about regulating technology based on a single snapshot in time is this: If a law or regulation becomes outdated, update it. But this is easier said than done. Most people agree that the SCA became outdated decades ago. But because Congress hasn’t been able to agree on specifically how to revise the 180-day provision, it’s still on the books over a third of a century after its enactment.

3) What are the potential unintended consequences? The Allow States and Victims to Fight Online Sex Trafficking Act of 2017 was a law passed in 2018 that revised Section 230 of the Communications Decency Act with the goal of combating sex trafficking. While there’s little evidence that it has reduced sex trafficking, it has had a hugely problematic impact on a different group of people: sex workers who used to rely on the websites knocked offline by FOSTA-SESTA to exchange information about dangerous clients. This example shows the importance of taking a broad look at the potential effects of proposed regulations.

4) What are the economic and geopolitical implications? If regulators in the United States act to intentionally slow the progress in AI, that will simply push investment and innovation — and the resulting job creation — elsewhere. While emerging AI raises many concerns, it also promises to bring enormous benefits in areas including education, medicine, manufacturing, transportation safety, agriculture, weather forecasting, access to legal services and more.

I believe AI regulations drafted with the above four questions in mind will be more likely to successfully address the potential harms of AI while also ensuring access to its benefits.

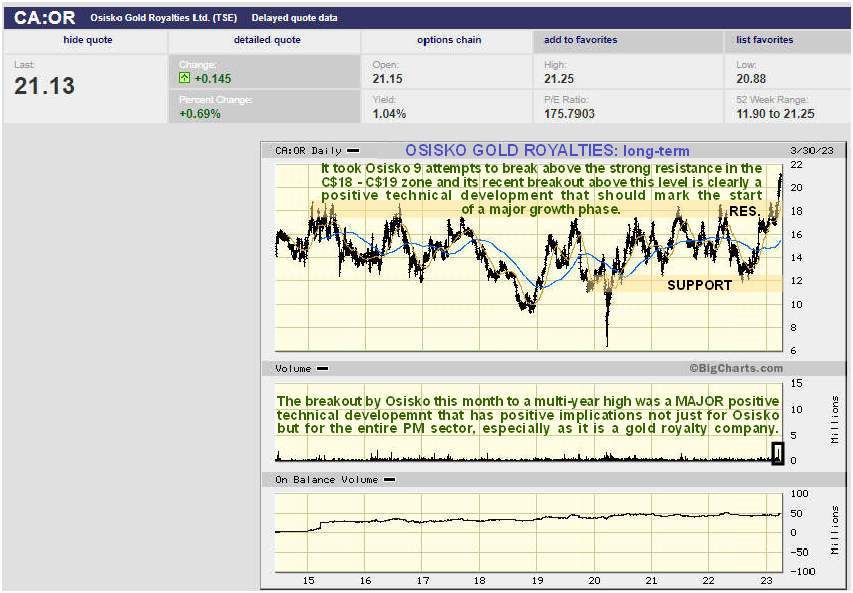

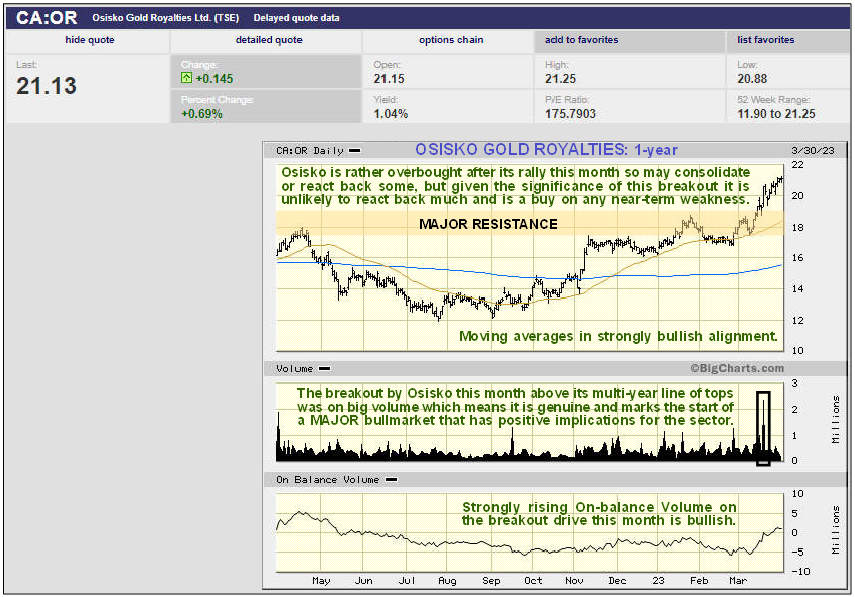

Technical analyst Clive Maund reviews Osisko Gold Royalties’ long-term and 1-year charts to explain why he believes this company is a Buy.

My attention was drawn to Osisko Gold Royalties Ltd. (OR:TSX; OR:NYSE) by a number of bullish articles on it, in particular one by Adrian Day that was posted a few days before its major high-volume breakout on the 17th.

It has risen significantly this month and while we are not normally minded to chase after stocks that have already taken off higher, I consider it worth bringing it to your attention here because of the strong bullish implications of this breakout which is believed to mark the start of a major bull market in Osisko for reasons that will soon become apparent which has important implications for the sector as a whole, it being a gold royalty company.

It very quickly becomes clear why the breakout in Osisko this month was so significant when we look at its long-term chart going back to 2014, for here we see that it has finally broken out above the strong resistance at a line of tops that goes back to 2015, on its eighth attempt to do so, so clearly this was an important technical development that in all probability marks the start of a major bull market.

Source: Bigcharts.com

On its 1-year chart, we can see recent action in much more detail. The most important point to note is the very high volume on the breakout this month on the 17th. This high volume is a sign that the breakout is genuine.

Everything about this chart is bullish — the trend is up with moving averages in bullish alignment, momentum positive, and the strong upside volume this month driving the On-balance Volume line higher in a robust manner.

However, there is no arguing the fact that after its strong rise this month which has opened up a considerable gap with its moving averages, it is short-term overbought, but that said this breakout was so significant that it has created support in the CA$18 – CA$19 zone (the former resistance level) which should now serve to put a floor under the price on any reaction.

Source: Bigcharts.com

The main point is that the breakout this month was of such importance that it is thought to mark the start of a major bullmarket in Osisko that will eventually result in much higher prices, and this should hardly be surprising considering the way that the financial system is “flying apart” in a manner that can be expected to result in vastly higher prices for gold and silver which most investors at this time would probably consider to be in the realms of fantasy, even many of you reading this.

The conclusion is that Osisko Gold Royalties has just made a major breakout that promises much higher prices in the future for it and not just that, but much higher prices ahead for gold and silver themselves. It is rated a strong conservative buy on all minor dips.

Osisko Gold Royalties Ltd. closed for trading at CA$21.10, $15.58 at 2.45 pm EDT on March 30, 2023.

CliveMaund.com Disclosures

The above represents the opinion and analysis of Mr. Maund, based on data available to him, at the time of writing. Mr. Maund’s opinions are his own, and are not a recommendation or an offer to buy or sell securities. Mr. Maund is an independent analyst who receives no compensation of any kind from any groups, individuals or corporations mentioned in his reports. As trading and investing in any financial markets may involve serious risk of loss, Mr. Maund recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction and do your own due diligence and research when making any kind of a transaction with financial ramifications. Although a qualified and experienced stock market analyst, Clive Maund is not a Registered Securities Advisor. Therefore Mr. Maund’s opinions on the market and stocks can only be construed as a solicitation to buy and sell securities when they are subject to the prior approval and endorsement of a Registered Securities Advisor operating in accordance with the appropriate regulations in your area of jurisdiction.

Disclosures: 1) Clive Maund: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: None. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with: None. Please click here for more information.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Following the OPEC+ shocker overnight, commodity currencies have rallied against the New Zealand dollar.

Given the cartels decision to lower oil output by over 1 million barrels per day starting from May, that promises more support for the likes of AUD, CAD and NOK in the months ahead.

However, for the rest of this week Antipodean central bank action could inject more volatility for AUDNZD.

This Antipodean central bank action could also offer a break from the dollar ahead of Friday’s US jobs report.

Investors will be served a central bank combo this week featuring the Reserve Bank of Australia (RBA) and Reserve Bank of New Zealand (RBNZ). There are mixed expectations over what to expect from the RBA while the RBNZ is expected to hike rates by 25 basis points. But before we take a deep dive into how the pending central bank decisions could play out, it is worth keeping in mind that the aussie weakened against most G10 currencies in Q1 2023.

It was a similar theme for the New Zealand dollar which weakened across the board.

Taking a brief look at the technical picture, the AUDNZD remains trapped within a range on the daily charts with support at 1.0675 and resistance at 1.0800.

Zooming out, the weekly charts look like a choppy affair with another layer of resistance found at 1.0900 and key support at 1.0470. The current price action suggests that the AUDNZD could be waiting for a fresh fundamental catalyst to make its next big move.

What to expect from the RBA on Tuesday?

Expectations remain split on whether the RBA will hike interest rates by 25 basis points or leave them unchanged. If the central bank opts for the latter, this will be the first pause since lifting interest rates in May 2022.

It’s been an incredible run for RBA hawks with rates rising by 3.5% in ten straight hikes between May last year and March 2023. However, the party could be coming to an end thanks to slower-than-expected inflation and repeated signs of slowing economic growth. On top of this, the recent market turmoil following the collapse of 3 US banks and the Credit Suisse drama have strengthened the argument for a potential pause. Given the rising unemployment and weak growth, the central bank is likely to adopt a cautious stance regardless of whether rates are hiked or left unchanged. The key question is if this meeting will mark the end of the hiking cycle. The Aussie could be in store for a world of pain if the RBA stands pat on rates, strikes a cautious note, and signals that the next move may be a rate cut.

RBNZ expected to hike rates

It will be wise to pay very close attention to the RBA meeting, considering how it will be the first G10 central bank decision after the OPEC+ shocker.

Initially, expectations were split on whether the RBA will hike interest rates by 25 basis points or leave them unchanged. However, the latest developments concerning OPEC+ have boosted the prospects of higher oil prices – ultimately fuelling fears of higher inflation. This could bring not only RBA hawks back into the scene but may prompt other central banks to turn hawkish once again. Much attention will be directed to any comments made by the RBA relating to the spike in oil prices and any potential impact on the central bank’s monetary policy stance.

It’s been an incredible run for RBA hawks with rates rising by 3.5% in ten straight hikes between May last year and March 2023. But the party could be coming to an end thanks to slower-than-expected inflation and repeated signs of slowing economic growth. On top of this, the recent market turmoil following the collapse of 3 US banks and the Credit Suisse drama have strengthened the argument for a potential pause. Given the rising unemployment and weak growth, the central bank has the potential to adopt a cautious stance. Ultimately, the key question is what impact the OPEC+ shocker will have on the monetary policy outlook and whether this may lead to further hikes down the road.

If the central bank leaves rates unchanged, this will be the first pause since lifting interest rates in May 2022. The Aussie could be in store for a world of pain on this outcome, especially if the RBA signals that this could be the end of the hiking cycle.

AUDNZD in breakout mode

The AUDNZD has been trapped within a range since early March. On the daily timeframe, prices are trading below the 50, 100, and 200-day Simple Moving Average (SMA) while the MACD trades below zero. Zooming out on the weekly charts, the trend is turning bearish thanks to the consistent lower lows and lower highs. However, the support at 1.0675 has halted bears in their tracks for the past four weeks.

A major breakout could be on the horizon with the pending central bank decisions acting as fundamental sparks. A strong daily close above 1.0800 could inspire an incline towards 1.0900 and 1.1030, respectively. If prices are able to break under 1.0675, this may open a path toward 1.0470.

For the last month, the inflation rate in the Eurozone declined from 8.5% to 6.9% on an annualized basis. But the core inflation (excluding food and energy prices) remains steady. Last month’s increase was 0.1%, annualized at 5.6% to 5.7%, which is a new record. After the published data, ECB head Christine Lagarde pointed out that core inflation remains too high, but the economy is resilient, the financial system is strong, and the recent banking stress will not hinder the fight against inflation. Thus, analysts are betting on another 0.5% rate hike at the May meeting of Europe’s Central Bank.

Trading recommendations

Support levels: 1.0770, 1.0680, 1.0519, 1.0482

Resistance levels: 1.0839, 1.0924, 1.1017

The trend on the EUR/USD currency pair on the hourly time frame is bullish. At the moment, the price is correcting and trading below the moving averages. The MACD indicator is in the negative zone, with no signs of divergence. Buy trades are best considered from the support level of 1.0770, but only with confirmation. It is worth buying after confirmation on the intraday time frames in the form of a structure change. Sell positions can be considered from the resistance level of 1.0839, subject to a reversal.

Alternative scenario: if the price breaks down through the support level of 1.0711 and fixes below it, the downtrend will likely resume.

News feed for 2023.04.03:

– German Manufacturing PMI (m/m) at 10:55 (GMT+3);

– Eurozone Manufacturing PMI (m/m) at 11:00 (GMT+3);

– US ISM Manufacturing PMI (m/m) at 17:00 (GMT+3).

The GBP/USD currency pair

Technical indicators of the currency pair:

Prev Open: 1.2380

Prev Close: 1.2329

% chg. over the last day: -0.41 %

The British GDP grew by 0.1% in the last quarter. Thus, the UK managed to avoid a technical recession. According to the latest Bank of England monetary policy report, inflation is expected to fall significantly in the second quarter of 2023 due to the extension of the energy price guarantee (EPG) announced in the new budget and falling wholesale energy prices. The Bank of England may not need to raise rates aggressively in the coming months. The next Bank of England meeting is in mid-May, giving Governor Bailey plenty of time to process a range of fresh data on inflation, GDP, and employment. Recent data on the likelihood of a rate hike by the Bank of England shows that one 25 basis point rate hike is expected in the second quarter before the Central Bank hits the pause button.

Trading recommendations

Support levels: 1.2266, 1.2178, 1.2112, 1.2009, 1.1963, 1.1929, 1.1843

Resistance levels: 1.2343, 1.2415, 1.2519

From the technical point of view, the trend on the GBP/USD currency pair on the hourly time frame is bullish. But now the price is correcting. The MACD indicator has become negative, and there is weak seller’s pressure inside the day. Under such market conditions, it is best to consider buying after a pullback to the nearest support level of 1.2266 but with confirmation in the form of a reverse reaction. Sell trades are best to look for on intraday time frames from the resistance level of 1.2343, with confirmation in the form of a false breakout.

Alternative scenario: if the price breaks down through the 1.2178 support level and fixes below it, the downtrend will likely resume.

News feed for 2023.04.03:

– UK Manufacturing PMI (m/m) at 11:30 (GMT+3).

The USD/JPY currency pair

Technical indicators of the currency pair:

Prev Open: 132.68

Prev Close: 132.76

% chg. over the last day: +0.06 %

A senior International Monetary Fund official said Friday the Bank of Japan should consider more flexible changes to long-term interest rates even as it maintains an ultra-soft monetary policy. The IMF sees bilateral risks to Japan’s inflation outlook: “upside surprises” stem from larger-than-expected wage hikes resulting from companies’ spring talks with labor unions. Japan’s central bank may ease the burden on financial institutions by allowing the longer end of the curve (YCC) to move more in line with its policy of controlling bond yields. Markets are full of rumors that the Bank of Japan may modify or abandon the YCC to mitigate the side effects of this approach when new Governor Kazuo Ueda and his team fully assume office.

Trading recommendations

Support levels: 132.47, 131.90, 130.91, 127.80

Resistance levels: 133.84, 135.11, 136.07, 137.91

From the technical point of view, the medium-term trend on the currency pair USD/JPY has changed to bullish. At the moment, the price is trading above the moving averages, and there is buying pressure. But the MACD indicator is overbought, and there is a divergence. It is better to look for buy trades from the support level of 132.47 or 131.90, but only with confirmation on the lower time frames. Sell deals can be sought from the resistance level of 133.84, but also with additional confirmation in the change of structure on the intraday time frames.

Alternative scenario: if the price fixes below the 130.91 support level, the downtrend will be resumed with a high probability.

News feed for 2023.04.03:

– Japan Tankan Large Manufacturers Index (q/q) at 02:50 (GMT+3);

– Japan Tankan Large Non-Manufacturers Index (q/q) at 02:50 (GMT+3);

– Japan Manufacturing PMI (m/m) at 03:30 (GMT+3).

The USD/CAD currency pair

Technical indicators of the currency pair:

Prev Open: 1.3521

Prev Close: 1.3515

% chg. over the last day: -0.04 %

The Canadian economy is recovering. The latest GDP data showed that the economy added 0.5% for the month of March (expectation of 0.4%). Overall, the economy for the fourth and first quarters is ahead of the Bank of Canada’s forecasts and continues to show resilience. The Bank of Canada’s GDP forecasts for the two quarters are trending upward. Markets are estimating a quarter-point cut in the Bank of Canada’s rate by September or October this year. At the same time, Saudi Arabia and OPEC+ producers on Sunday announced voluntary cuts in oil production. This is positive for the Canadian dollar because, as a commodity currency, production cuts tend to drive up oil prices.

From the point of view of technical analysis, the trend on the USD/CAD currency pair is bearish. The price is trading below the moving averages. But the MACD indicator is oversold, and there are signs of divergence, which suggests that an upward correction should be expected in the near future. Under such market conditions, it is better to buy from the support level of 1.3515 but with a confirmation in the form of a change in the structure on the lower time frames. Sell positions can be sought from the resistance level of 1.3568, but only with confirmation in the form of a reverse initiative.

Alternative scenario: if the price breaks out and consolidates above the resistance level of 1.3694, the uptrend will likely resume.

News feed for 2023.04.03:

– OPEC Meeting (m/m) at 13:00 (GMT+3);

– Canada Manufacturing PMI (m/m) at 16:30 (GMT+3);

– Canada BoC Business Outlook Survey at 17:30 (GMT+3).

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.