Here’s what happened with a shelf of support in the chart of the long bond

By Elliott Wave International

The yield on U.S. Treasury bonds trended higher from 1942 to 1981 — that’s 39 years.

Interestingly, yields (or interest rates) then trended lower for 39 years (1981 to 2020).

Thirty-nine years is quite a long time — well long enough for observers to get used to the idea of exceptionally low yields, even the Fed.

Indeed, here’s a Sept. 16, 2020 headline from the Wall Street Journal:

Fed Signals Low Rates Likely to Last Several Years

Elliott Wave International President Robert Prechter had an entirely different perspective. Here’s what he said just a week later in his Sept. 23, 2020 issue of The Elliott Wave Theorist, a monthly publication which provides analysis of major financial and cultural trends:

On September 16, Fed Chairman Powell [said] he expected short term interest rates to stay near zero as long as inflation stays below 2%, a condition he believes will maintain … through “the end of 2023.” I think there is not a chance in the world of that scenario playing out. … The probability is high that interest rates have begun a process of rising. … [emphasis added]

As we all know, interest rates or yields have risen substantially since 2020.

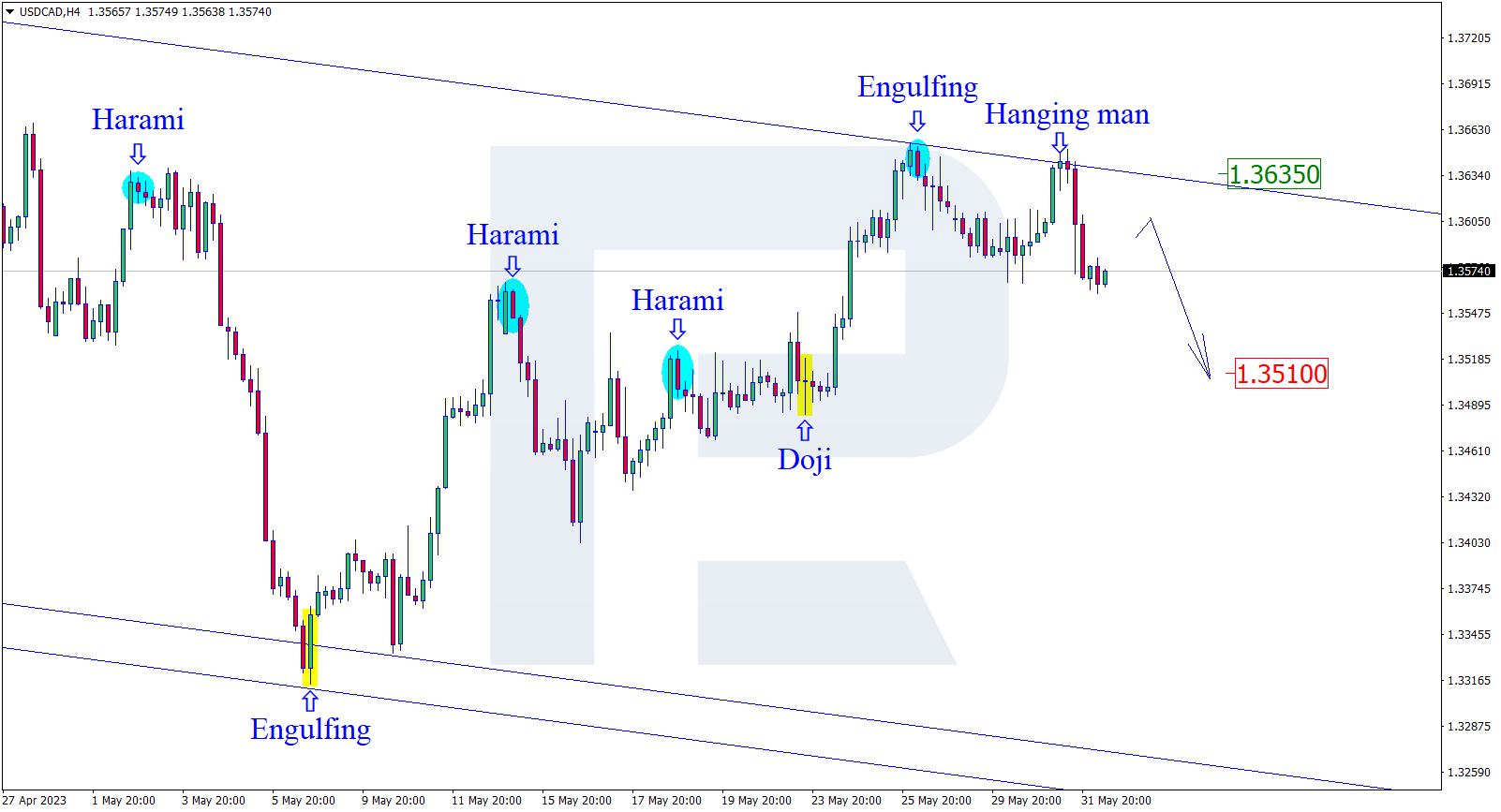

This chart and commentary from the May 19, 2023 Elliott Wave Theorist provide an update (Keep in mind that Elliott wave labeling is available to subscribers):

Treasury bond futures have been slipping again. As you can see in [the chart], bond prices broke a shelf of support this week and traded today at their lowest level in ten weeks. A debt crisis is brewing, and higher long term interest rates will add to the pressure.

Yes, servicing public and private debt is getting a lot more expensive. And that debt has been increasing dramatically and rapidly (CNBC, May 18):

The global debt pile grew by $8.3 trillion in the first quarter to a near-record high of $305 trillion … .

Getting back to the price pattern of the U.S. Treasury Long Bond, Elliott wave analysis can help you determine what’s next.

Of course, no method of analyzing financial markets can offer a guarantee, but Elliott Wave International knows of no other method which surpasses the usefulness of the Elliott wave model.

That said, here’s a quote from Frost & Prechter’s Wall Street classic, Elliott Wave Principle: Key to Market Behavior:

Without Elliott, there appear to be an infinite number of possibilities for market action. What the Wave Principle provides is a means of first limiting the possibilities and then ordering the relative probabilities of possible future market paths. Elliott’s highly specific rules reduce the number of valid alternatives to a minimum. Among those, the best interpretation, sometimes called the “preferred count,” is the one that satisfies the largest number of guidelines. Other interpretations are ordered accordingly. As a result, competent analysts applying the rules and guidelines of the Wave Principle objectively should usually agree on both the list of possibilities and the order of probabilities for various possible outcomes at any particular time. That order can usually be stated with certainty. Do not assume, however, that certainty about the order of probabilities is the same as certainty about one specific outcome. Under only the rarest of circumstances do you ever know exactly what the market is going to do. You must understand and accept that even an approach that can identify high odds for a fairly specific event must be wrong some of the time.

If you’d like to read the entire online version of the book, you may do so for free once you become a member of Club EWI, the world’s largest Elliott wave educational community.

A Club EWI membership is also free.

Get started right away by following this link: Elliott Wave Principle: Key to Market Behavior — get free access.

This article was syndicated by Elliott Wave International and was originally published under the headline Treasury Bonds: How This Forecast is Playing Out. EWI is the world’s largest market forecasting firm. Its staff of full-time analysts led by Chartered Market Technician Robert Prechter provides 24-hour-a-day market analysis to institutional and private investors around the world.

EU consumers are familiar making payments with traditional coins and bills, but soon they could be joined by an ‘e-euro”.

EU consumers are familiar making payments with traditional coins and bills, but soon they could be joined by an ‘e-euro”.

Business deals by foreign countries in the U.S. can be reviewed by the government for national security risks.

Business deals by foreign countries in the U.S. can be reviewed by the government for national security risks.

{kind=link}