The US Treasury Secretary’s trip to China this week will be a hit with investors around the world, affirms the CEO and founder of one of the world’s largest independent financial advisory, asset management and fintech organizations.

The comments from Nigel Green of deVere Group come as Janet Yellen heads to Beijing between July 3 and 6 as part of continuing efforts by the Biden administration to strengthen communication between the US and China after a series of spates and instability between the two nations.

He says: “Yellen’s trip to Beijing this week is important to global markets for two main reasons.

“First, she is the top US economic policymaker, meaning that the US government appears serious about rebuilding economic ties between the world’s two largest economies.

“Also, Yellen’s visit to meet counterparts in China comes just three weeks after Secretary of State Antony Blinken visited the country, highlighting the attempts by the Biden administration to revive a more cordial relationship with the emerging superpower.”

The deVere CEO continues: “Second – and perhaps more importantly – it shows a commitment to globalisation.

“Investors are looking for global leaders to dismiss the prevailing protectionist narrative of the last few years as many countries have looked increasingly inwards, becoming more and more nationalistic.

“Globalization opens-up a wider array of investment opportunities beyond domestic markets. Investors can access a diverse range of industries, sectors, and geographies, allowing them to build well-diversified portfolios.

“History teaches us that by investing globally, investors can gain exposure to companies at the forefront of technological advancements, disruptive business models, and emerging trends. This exposure to innovation can drive portfolio growth and potentially generate above-average returns.”

Yellen’s forthcoming trip also comes a week after China’s premier Li Qiang condemned recent Western efforts to limit trade and business ties with the country, and encouraged international economic co-operation.

In the keynote address at a World Economic Forum event in which he criticised “the politicization of economic issues”, Li said: “Governments should not over-reach themselves, still less stretch the concept of risk or turn it into an ideological tool.”

This denouncing of economic “politicization” and defence of globalization in his speech at the so-called ‘Summer Davos’ address, was, says Nigel Green, “music to the ears of investors around the world.”

Yellen is expected to meet with senior Chinese officials as well as leading US firms with operations in China.

The Treasury says she will discuss “areas of concern” to cool tensions between the two largest economies in the world, ways to work competition between the two powers, as well as subjects where they can cooperate on international issues, such as climate change.

“Financial markets around the world will be cheered by the efforts being made by the superpower economies to foster policies of globalization,” concludes Nigel Green.

About:

deVere Group is one of the world’s largest independent advisors of specialist global financial solutions to international, local mass affluent, and high-net-worth clients. It has a network of more than 70 offices across the world, over 80,000 clients and $12bn under advisement.

BTC reached 30,710 USD on Friday, marking a weekly growth of 2.35%.

Improvement in the domestic news landscape and the reestablished correlation with the US stock market are working in favour of the flagship cryptocurrency. At the same time, it should be noted that the rally is not formed yet because buyers remain cautious. For the BTC exchange rate to confidently move upwards, the cryptocurrency needs to secure above 31,150 USD. Once this is achieved, the next target for growth would be 33,000 USD.

The capitalisation of the cryptocurrency market is gradually increasing and currently stands at 1.190 trillion USD. The share of BTC remains at 50.2%, while the share of ETH has decreased to 18.9%.

BTC mining has become less complicated

According to a recent calculation, the complexity of mining the leading cryptocurrency has decreased by 3.26%. For May, the cumulative revenue of miners amounted to 916 million USD, which shows consistent growth since November last year.

The King of the UK ratifies cryptocurrency legislation

The King of the UK has ratified a draft bill allowing regulators to oversee digital assets and stablecoins. This is a formal measure, as the legislation was previously agreed upon at the House of Lords.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

AUDUSD set to post 1.8% climb in June – first monthly gain since January 2023

Bloomberg’s FX model forecasts trading range of 0.6524 – 0.6732 for AUDUSD in first week of July

AUDUSD’s presence above/below 0.660 next week could be dictated by China PMIs, RBA decision, FOMC minutes, and US jobs report.

AUDUSD is recovering slightly in recent sessions, despite having it tough so far in 2023.

The “Aussie” has a year-to-date decline of 2.8%, no thanks to the resilient US dollar as well as China’s faltering economic recovery.

Whether or not the “Aussie” can extend its recent recovery into the new month may well depend on the fundamental catalysts contained within the global economic calendar for the coming week:

Monday, July 3

AUD: Australia June inflation; manufacturing PMI (final)

CNH: China June Caixin manufacturing PMI

EUR: Eurozone June manufacturing PMI (final); Germany May trade balance

GBP: UK June manufacturing PMI (final)

USD: US June ISM manufacturing

Tuesday, July 4

AUD: Reserve Bank of Australia rate decision

EUR: Eurozone April retail sales; Germany April factory orders

US markets closed for Independence Day

Wednesday, July 5

AUD: Australia June services PMI (final)

CNH: China Caixin services and composite PMIs

EUR: Eurozone May PPI, services PMI (final)

GBP: UK June services PMI (final)

USD: FOMC minutes; speech by New York Fed President John Williams

Thursday, July 6

AUD: Australia May external trade

EUR: Eurozone May retail sales; Germany May factory orders

USD: US weekly initial jobless claims; speech by Dallas Fed President Lorie Logan

Friday, July 7

CNH: China June forex reserves

EUR: Speech by ECB President Christine Lagarde; Germany May industrial production

GBP: Speech by BOE policymaker Catherine Mann

USD: US June nonfarm payrolls

CAD: Canada June unemployment rate

In determining whether AUDUSD can keep its head above the crucial support 0.660 level next week …

Traders and investors will be casting their sights across 3 countries, namely China, the US, and Australia (of course).

Here are some key events to pay close attention to:

1) July 3rd: China June Caixin manufacturing PMI

Note that the Australian economy is very much reliant on China, being Australia’s largest trading partner.

Hence, when the Chinese Yuan strengthens, the Australian Dollar tends to follow suit.

(AUDUSD has a strong inverse correlation with USDCNY of -0.72 over a 5-day rolling period in the past 10 years)

AUDUSD may move higher should China’s Caixin manufacturing PMI come in above the 50 mark, which shows expanding conditions in China’s manufacturing sector.

AUDUSD may move lower should China’s Caixin manufacturing PMI come in below the 50 mark, which would show contracting conditions among factories in the world’s second largest economy.

2) July 4th: Reserve Bank of Australia (RBA) rate decision

The futures market predicts only a 1-in-3 chance that Australia’s central bank will hike by further 25-basis points.

On the other hand, the 27 economists surveyed by Bloomberg are split (13-14) on whether we will see a July RBA hike.

The economists in the “no July hike” camp would point to the latest Australian consumer price index (CPI – which measures headline inflation) of 5.6% for May.

That 5.6% number was below market forecasts for 6.1% and also lower than April’s 6.8% reading.

Should this coming Monday’s (July 3rd) inflation readings by the Melbourne Institute also show easing inflationary pressures, that may bolster the case for another RBA pause at next week’s meeting.

However, note that the RBA surprised markets with unexpected hikes at its past two policy meetings.

For the upcoming RBA decision:

AUDUSD may move higher if the RBA raises its Cash Rate Target to 4.35%

AUDUSD may move lower if the RBA leaves rates unchanged at 4.10%

3) July 5th: FOMC June meeting minutes

Recall how the Fed tried to warn markets at that mid-June FOMC meeting about two more incoming rate hikes this year.

Such warnings by Fed Chair Jerome Powell had little initial impact, as markets were willing to challenge the Fed’s forecasts.

However, the economic data since then suggests that the world’s largest economy remains resilient, likely paving the way for the Fed to raise its benchmark rates even higher so as to quell still-stubborn inflation.

AUDUSD may move higher if the June FOMC meeting minutes reveals a more dovish policy stance held by Fed officials who are adamant that US interest rates have moved high enough and are not willing to risk further economic damage.

AUDUSD may move lower if the June FOMC meeting minutes reveals a more hawkish policy stance held by Fed officials who are adamant about moving US interest rates even higher.

4) July 7th: US jobs report for June

Markets predict that 200,000 new jobs were added to the US economy in June.

If so, that 200k figure would be the lowest headline nonfarm payrolls (NFP) print since December 2019.

Yet, seasoned market watchers are only too aware that the NFP number has been notoriously hard to predict in recent months, frustrating many top economists.

After all, every single headline NFP number for each month of 2023 so far has exceeded market forecasts. Recall the recent blockbuster NFP print for May (released on June 2nd) which came in at a whopping 339k, far exceeding Wall Street’s forecast of 195k.

The June unemployment rate (also released on Friday, July 7th) is even expected to tick lower to 3.6% compared to May’s 3.7% jobless rate.

Still, with recession alarm bells ringing loudly in certain parts of global financial markets, investors are always looking further down the line and already asking when we will see the first negative NFP print (job losses) and a significantly higher unemployment rate.

AUDUSD may move higher on a weaker US Dollar if the June NFP report produces a lower-than-200k headline number, along with a higher unemployment rate. A weaker-than-expected US jobs report may allow the Fed to start thinking about pausing its rate hikes.

AUDUSD may move lower on a stronger US Dollar if the June NFP report, yet again, delivers another positive shocker that far exceeds the forecasted 200k print, while the unemployment rate moves lower. Another blockbuster US jobs report should force the Fed to hike twice more before 2023 ends.

Key levels

At the time of writing, Bloomberg’s FX model forecasts a 36.7% chance that AUDUSD might break below the 0.66 over the next one-week period.

The model also forecasts a trading range of 0.6524 – 0.6732 for AUDUSD through the first week of July.

Here are some key levels to watch within that forecasted trading range:

POTENTIAL SUPPORT

0.6600: psychologically-important level

0.65641 – 0.65738: March, May cycle lows

0.6524: lower end of Bloomberg model forecasted range; key battleground for bulls and bears in late May/early June.

POTENTIAL RESISTANCE

0.66627: June 23rd intraday low

100-day SMA

0.67255: 23.6% Fibonacci level from AUDUSD’s 1H23 peak-to-trough

The US indices mostly rose yesterday. The Federal Reserve stress test showed that the 23 largest US banks could withstand a severe recession scenario. At yesterday’s stock market close, the Dow Jones Index (US30) increased by 0.80%, and the S&P 500 (US500) added 0.45%. The NASDAQ Technology Index (US100) closed yesterday at opening level.

Wells Fargo & Company (WFC), JPMorgan Chase & Co (JPM), and Goldman Sachs Group Inc (GS) led the rally in the banking sector amid growing optimism after passing the stress tests. But analysts don’t share that optimism, as there are big doubts that the nation’s regional banks will be able to withstand the recession.

Atlanta Fed President Rafael Bostic continued to signal yesterday that the Fed should take a pause, saying it would be wise to keep rates at current levels in future meetings, as inflation is likely to slow without additional tightening.

Nike (NKE) posted mixed results for the fourth quarter as earnings came in below Wall Street estimates, but revenue exceeded forecasts on the back of the ongoing recovery in China. Sales in North America rose by 5% year-over-year in the fourth quarter, while sales in China, an important market for the sportswear giant, jumped by 16%.

The US Gross Domestic Product (GDP) for the second quarter was 2%, exceeding economists’ forecasts of 1.4%. Because of the Fed’s hawkish stance and strong economic data, the inversion of the US yield curve is deepening. This is a sign that investors are increasingly worried about slowing economic growth. An inverted yield curve occurs when short-term Treasury bond yields exceed long-term yields, reflecting bets that the Central Bank will have to cut rates in the future to support an economy hit by higher borrowing costs.

Equity markets in Europe traded flat yesterday. German DAX (DE30) closed at the opening level, French CAC 40 (FR40) gained 0.36%, Spanish IBEX 35 (ES35) added 0.36%, and British FTSE 100 (UK100) was negative by 0.38%.

Inflationary pressure is growing again in Germany. The consumer price level in the country rose from 6.1% to 6.4% in annual terms. Eurozone’s inflation data will be released today. General inflation is expected to fall from 6.1% to 5.6% y/y, but core inflation is expected to rise from 5.3% to 5.5% y/y. This will be a hawkish signal for the ECB.

Asian markets were mostly down yesterday. Japan’s Nikkei 225 (JP225) gained 0.12% yesterday, China’s FTSE China A50 (CHA50) lost 0.94%, Hong Kong’s Hang Seng (HK50) ended the day down by 0.80%, and Australia’s S&P/ASX 200 (AU200) ended Thursday negative by 0.02%.

Bank of Japan Deputy Governor Ryozo Himino said the country’s banking sector remains resilient and has enough reserves to withstand any stress caused by future interest rate hikes. The least favorable condition for domestic financial institutions would be for Japan to keep interest rates ultra-low for too long amid a weak economy, Himino said. Analysts believe the Bank of Japan has been slow to prepare for monetary policy normalization.

Tokyo’s core consumer price index rose to 3.2% from 3.1% (forecast 3.4%). This Index is seen as a leading indicator of inflation across the country. Despite the fact that the inflation value was below the forecast, consumer prices are showing steady growth, which is exactly what the Bank of Japan wants to see before it changes its monetary policy.

China’s manufacturing activity declined for the third month in a row in June, while weakness in other sectors intensified. The official manufacturing purchasing managers’ index (PMI) rose to 49.0 from 48.8 in May, remaining below the 50-point mark that separates growth from contraction. The non-manufacturing PMI fell to 53.2 from 54.50 in May, indicating slowing activity in the services and construction sectors. New orders and new export orders declined for the third straight month, with export orders declining at a faster pace. This situation adds to the pressure on the authorities to do more to support growth as demand falls both at home and abroad.

S&P 500 (F) (US500) 4,396.44 +19.58 (+0.45%)

Dow Jones (US30)34,122.42 +269.76 (+0.80%)

DAX (DE40) 15,949.00 −2.28 (−0.014%)

FTSE 100 (UK100) 7,471.69 −28.80 (−0.38%)

USD Index 103.35 +0.45 (+0.43%)

Important events for today:

– Japan Tokyo Core CPI (m/m) at 02:30 (GMT+3);

– Japan Unemployment Rate (m/m) at 02:30 (GMT+3);

– Japan Industrial Production (m/m) at 02:50 (GMT+3);

– China Manufacturing PMI (m/m) at 04:30 (GMT+3);

– China Non-Manufacturing PMI (m/m) at 04:30 (GMT+3);

– UK GDP (q/q) at 09:00 (GMT+3);

– German Retail Sales (m/m) at 09:00 (GMT+3);

– Switzerland Retail Sales (m/m) at 09:30 (GMT+3);

– German Unemployment Rate (m/m) at 10:55 (GMT+3);

– Eurozone Consumer Price Index (m/m) at 12:00 (GMT+3);

– Eurozone Unemployment Rate (m/m) at 12:00 (GMT+3);

– US PCE Price index (m/m) at 15:30 (GMT+3);

– Canada GDP (q/q) at 15:30 (GMT+3);

– US Michigan Consumer Sentiment (m/m) at 17:00 (GMT+3);

– Canada BoC Business Outlook Survey at 17:30 (GMT+3).

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

Numerous government agencies, including the FBI, Department of Defense, National Security Agency, Treasury Department, Defense Intelligence Agency, Navy and Coast Guard, have purchased vast amounts of U.S. citizens’ personal information from commercial data brokers. The revelation was published in a partially declassified, internal Office of the Director of National Intelligence report released on June 9, 2023.

The report shows the breathtaking scale and invasive nature of the consumer data market and how that market directly enables wholesale surveillance of people. The data includes not only where you’ve been and who you’re connected to, but the nature of your beliefs and predictions about what you might do in the future. The report underscores the grave risks the purchase of this data poses, and urges the intelligence community to adopt internal guidelines to address these problems.

As a privacy, electronic surveillance and technology law attorney, researcher and law professor, I have spent years researching, writing and advising about the legal issues the report highlights.

These issues are increasingly urgent. Today’s commercially available information, coupled with the now-ubiquitous decision-making artificial intelligence and generative AI like ChatGPT, significantly increases the threat to privacy and civil liberties by giving the government access to sensitive personal information beyond even what it could collect through court-authorized surveillance.

What is commercially available information?

The drafters of the report take the position that commercially available information is a subset of publicly available information. The distinction between the two is significant from a legal perspective. Publicly available information is information that is already in the public domain. You could find it by doing a little online searching.

Commercially available information is different. It is personal information collected from a dizzying array of sources by commercial data brokers that aggregate and analyze it, then make it available for purchase by others, including governments. Some of that information is private, confidential or otherwise legally protected.

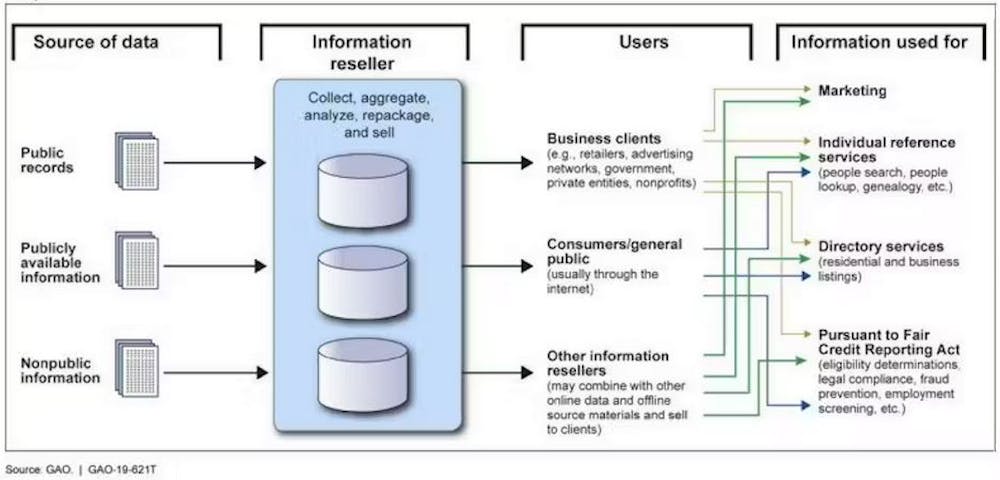

The commercial data market collects and packages vast amounts of data and sells it for various commercial, private and government uses. Government Accounting Office

The sources and types of data for commercially available information are mind-bogglingly vast. They include public records and other publicly available information. But far more information comes from the nearly ubiquitous internet-connected devices in people’s lives, like cellphones, smart home systems, cars and fitness trackers. These all harness data from sophisticated, embedded sensors, cameras and microphones. Sources also include data from apps, online activity, texts and emails, and even health care provider websites.

This data provides companies and governments a window into the “Internet of Behaviors,” a combination of data collection and analysis aimed at understanding and predicting people’s behavior. It pulls together a wide range of data, including location and activities, and uses scientific and technological approaches, including psychology and machine learning, to analyze that data. The Internet of Behaviors provides a map of what each person has done, is doing and is expected to do, and provides a means to influence a person’s behavior.

Smart homes could be good for your wallet and good for the environment, but really bad for your privacy.

Better, cheaper and unrestricted

The rich depths of commercially available information, analyzed with powerful AI, provide unprecedented power, intelligence and investigative insights. The information is a cost-effective way to surveil virtually everyone, plus it provides far more sophisticated data than traditional electronic surveillance tools or methods like wiretapping and location tracking.

Complying with these laws takes time and money, plus electronic surveillance law restricts what, when and how data can be collected. Commercially available information is cheaper to obtain, provides far richer data and analysis, and is subject to little oversight or restriction compared to when the same data is collected directly by the government.

The threats

Technology and the burgeoning volume of commercially available information allow various forms of the information to be combined and analyzed in new ways to understand all aspects of your life, including preferences and desires.

How the collection, aggregation and sale of your data violates your privacy.

The Office of the Director of National Intelligence report warns that the increasing volume and widespread availability of commercially available information poses “significant threats to privacy and civil liberties.” It increases the power of the government to surveil its citizens outside the bounds of law, and it opens the door to the government using that data in potentially unlawful ways. This could include using location data obtained via commercially available information rather than a warrant to investigate and prosecute someone for abortion.

The report also captures both how widespread government purchases of commercially available information are and how haphazard government practices around the use of the information are. The purchases are so pervasive and agencies’ practices so poorly documented that the Office of the Director of National Intelligence cannot even fully determine how much and what types of information agencies are purchasing, and what the various agencies are doing with the data.

Is it legal?

The question of whether it’s legal for government agencies to purchase commercially available information is complicated by the array of sources and complex mix of data it contains.

There is no legal prohibition on the government collecting information already disclosed to the public or otherwise publicly available. But the nonpublic information listed in the declassified report includes data that U.S. law typically protects. The nonpublic information’s mix of private, sensitive, confidential or otherwise lawfully protected data makes collection a legal gray area.

Despite decades of increasingly sophisticated and invasive commercial data aggregation, Congress has not passed a federal data privacy law. The lack of federal regulation around data creates a loophole for government agencies to evade electronic surveillance law. It also allows agencies to amass enormous databases that AI systems learn from and use in often unrestricted ways. The resulting erosion of privacy has been a concern for more than a decade.

Throttling the data pipeline

The Office of the Director of National Intelligence report acknowledges the stunning loophole that commercially available information provides for government surveillance: “The government would never have been permitted to compel billions of people to carry location tracking devices on their persons at all times, to log and track most of their social interactions, or to keep flawless records of all their reading habits. Yet smartphones, connected cars, web tracking technologies, the Internet of Things, and other innovations have had this effect without government participation.”

However, it isn’t entirely correct to say “without government participation.” The legislative branch could have prevented this situation by enacting data privacy laws, more tightly regulating commercial data practices, and providing oversight in AI development. Congress could yet address the problem. Representative Ted Lieu has introduced the a bipartisan proposal for a National AI Commission, and Senator Chuck Schumer has proposed an AI regulation framework.

Effective data privacy laws would keep your personal information safer from government agencies and corporations, and responsible AI regulation would block them from manipulating you.

Inflation, a slowing global economy, and high stock valuations present the three major challenges for investors in the second half of 2023. They must be prepared to navigate through ‘significant headwinds’ while capitalizing on the tailwinds that offer promising prospects.

This is the analysis of Nigel Green, CEO and founder of deVere Group, one of the world’s largest independent financial advisory, asset management and fintech organizations, as we approach the year’s second half, when investors are typically analysing the market outlook, macro risks, and forecasts.

He says: “2023 has been a better year to date for economies than many had expected, but we expect three significant investment headwinds for the second half of the year that investors need to consider.

“First, the persisting challenge of inflation remains a top concern for investors in the second half of 2023. Core and headline inflation are edging down, slowly, but core still remains comparatively high in major developed economies.

“Therefore, central banks will argue they need to continue with, or resume, interest rate rises to bring inflation back to target.”

Stock markets typically experience declines or volatility when interest rates are raised.

Borrowing becomes more expensive for individuals and businesses, affecting corporate profitability as companies face higher costs of borrowing to finance their operations, expansion, or investment projects. Rates hikes typically lead to a decrease in corporate earnings, which negatively impacts stock prices.

The jumped-up borrowing costs also discourage consumers from taking on new loans, such as mortgages or car loans, which can impact sectors such as real estate and automotive industries. Reduced consumer spending will likely then have a ripple effect on businesses’ revenues and earnings.

In addition, investors may reallocate their portfolios to take advantage of the relatively safer returns offered by bonds, reducing demand for stocks and putting downward pressure on markets.

The deVere CEO continues: “Most developed markets will experience the lag effect of monetary policy tightening during the second-half 2023. The time lag for monetary policies is incredibly lengthy. It takes around 18 months for the full effect of rate hikes to make their way into the economy – which is what we expect to see in H2 of this year.

“As the impact of monetary policy agendas kick in, we expect economies around the world to slow.

“Investors should closely monitor key indicators and adjust their investment strategies accordingly.

“And third, the current market environment is characterised by elevated valuations across various asset classes.

“This poses a serious challenge for investors seeking attractive entry points. The risk of overpaying for investments is amplified, increasing the importance of thorough analysis and due diligence. Investors should exercise caution and focus on identifying quality investments with solid fundamentals and reasonable valuations.”

However, the second half of 2023 will also present several tailwinds that can guide investment decisions and unlock opportunities.

“Amidst the challenges, there are attractive opportunities in both value and growth sectors,” affirms Nigel Green.

“Value investors can identify undervalued companies with strong fundamentals and the potential for future growth. Meanwhile, growth investors can capitalise on sectors that continue to demonstrate robust performance, such as technology, healthcare, and renewable energy.

“In an uncertain market environment, quality stocks tend to provide stability and resilience. Companies with solid financials, strong management teams, and competitive advantages are more likely to weather market volatility.

“Investors should focus on identifying companies with sustainable business models and a track record of delivering consistent returns to shareholders.

“Diversification remains a time-tested strategy for mitigating risks and maximizing returns.

“By spreading investments across different asset classes, sectors, and geographies, investors can reduce their exposure to any single risk factor. Diversification helps to smooth out volatility and provides a cushion against potential downturns in specific areas of the market.”

He concludes: “The second half of 2023 presents a mixed bag of headwinds and tailwinds for investors.

“While challenges like inflation, an economic slowdown, and high valuations persist, there are also opportunities in both value and growth sectors.

“By focusing on quality stocks and implementing a diversified investment strategy, investors can position themselves to navigate through uncertainty and capitalize on the inevitable rewards that lie ahead.”

About:

deVere Group is one of the world’s largest independent advisors of specialist global financial solutions to international, local mass affluent, and high-net-worth clients. It has a network of more than 70 offices across the world, over 80,000 clients and $12bn under advisement.

Could a new currency be set to challenge the dominance of the dollar? Perhaps, but that may not be the point.

In August 2023, South Africa will host the leaders of Brazil, Russia, India, China and South Africa – a group of nations known by the acronym BRICS. Among the items on the agenda is the creation of a new joint BRICS currency.

As a scholar who has studied the BRICS countries for over a decade, I can certainly see why talk of a BRICS currency is, well, gaining currency. The BRICS summit comes as countries across the world are confronting a changing geopolitical landscape that is challenging the traditional dominance of the West. And while the BRICS countries have been seeking to reduce their reliance on the dollar for over a decade, Western sanctions on Russia after its invasion of Ukraine have accelerated the process.

Meanwhile, rising interest rates and the recent debt-ceiling crisis in the U.S. have raised concerns among other countries about their dollar-denominated debt and the demise of the dollar should the world’s leading economy ever default.

That all said, a new BRICS currency faces major hurdles before becoming a reality. But what currency discussions do show is that the BRICS countries are seeking to discover and develop new ideas about how to shake up international affairs and effectively coordinate policies around these ideas.

The BRICS countries have been pursuing a wide range of initiatives to decrease their dependence on the dollar. Over the past year, Russia, China and Brazil have turned to greater use of non-dollar currencies in their cross-border transactions. Iraq, Saudi Arabia and the United Arab Emirates are actively exploring dollar alternatives. And central banks have sought to shift more of their currency reserves away from the dollar and into gold.

All the BRICS nations have been critical of the dollar’s dominance for different reasons. Russian officials have been championing de-dollarization to ease the pain from sanctions. Because of sanctions, Russian banks have been unable to use SWIFT, the global messaging system that enables bank transactions. And the West froze Russia’s US$330 billion in reserves last year.

Meanwhile, the 2022 election in Brazil reinstated Luiz Inácio Lula da Silva as president. Lula is a longtime proponent of BRICS who previously sought to reduce Brazil’s dependence on and vulnerability to the dollar. He has reenergized the group’s commitment to de-dollarization and spoken about creating a new Euro-like currency.

The Chinese government has also clearly laid out its concerns with the dollar’s dominance, labeling it “the main source of instability and uncertainty in the world economy.” Beijing directly blamed the Fed’s interest rate hike for causing turmoil in the international financial market and substantial depreciation of other currencies. Together with other BRICS countries, China has also criticized the use of sanctions as a geopolitical weapon.

The appeal of de-dollarization and a possible BRICS currency would be to mitigate such problems. Experts in the U.S. are deeply divided on its prospects. U.S. Treasury Secretary Janet Yellen believes the dollar will remain dominant as most countries have no alternative. Yet a former White House economist sees a way that a BRICS currency could end dollar dominance.

Currency ambitions

Although talk of a BRICS currency has gained momentum, there is limited information on various models under consideration.

The most ambitious path would be something akin to the Euro, the single-currency adopted by 11 member states of the European Union in 1999. But negotiating a single currency would be difficult given the economic power asymmetries and complex political dynamics within BRICS. And for a new currency to work, BRICS would need to agree to an exchange rate mechanism, have efficient payment systems and a well-regulated, stable and liquid financial market. To achieve a global currency status, BRICS would need a strong track record of joint currency management to convince others that the new currency is reliable.

A BRICS version of the Euro is unlikely for now; none of the countries involved show any desire to discontinue its local currency. Rather, the goal appears to be to create an efficient integrated payment system for cross-border transactions as the first step and then introduce a new currency.

Building blocks for this already exist. In 2010, the BRICS Interbank Cooperation Mechanism was launched to facilitate cross-border payments between BRICS banks in local currencies. BRICS nations have been developing “BRICS pay” – a payment system for transactions among the BRICS without having to convert local currency into dollars. And there has been talk of a BRICS cryptocurrency and of strategically aligning the development of Central Bank Digital Currencies to promote currency interoperability and economic integration. Since many countries expressed an interest in joining BRICS, the group is likely to scale its de-dollarization agenda.

From BRICS vision to reality

To be sure, some of the group’s most ambitious past initiatives to set up major BRICS projects to parallel non-Western infrastructures have failed. Big ideas like developing a BRICS credit rating agency and creating a BRICS undersea cable never materialized.

And de-dollarization efforts have been struggling both at the multilateral and bilateral level. In 2014, when the BRICS countries launched the New Development Bank, its founding agreement outlined that its operations may provide financing in the local currency of the country in which the operation takes place. Yet, in 2023, the bank remains heavily dependent on the dollar for its survival. Local currency financing represents around 22% of the bank’s portfolio, although its new president hopes to increase that to 30% by 2026.

Similar challenges exist in bilateral de-dollarization pursuits. Russia and India have sought to develop a mechanism for trading in local currencies, which would enable Indian importers to pay for Russia’s cheap oil and coal in rupees. However, talks were suspended after Moscow cooled on the idea of rupee accumulation.

Despite the barriers to de-dollarization, the BRICS group’s determination to act should not be dismissed – the group has been known for defying expectations in the past.

Despite many differences among the five countries, the bloc managed to develop joint policies and survive major crises such as the 2020-21 China-India border clashes and the war in Ukraine. BRICS has deepened its cooperation, invested in new financial institutions and has been continuously broadening the range of policy issues it addresses.

It now has a huge network of interlinked mechanisms that connect governmental officials, businesses, academics, think tanks and other stakeholders across countries. Even if there is no movement on the joint currency front, there are multiple issues on which BRICS finance ministers as well as central bankers regularly coordinate – and the potential for developing new financial collaborations is particularly strong.

No doubt, talk of a new BRICS currency in itself is an important indicator of the desire of many nations to diversify away from the dollar. But I believe focusing on the BRICS currency risks missing the forest for the trees. A new global economic order will not emerge out of a new BRICS currency or de-dollarization happening overnight. But it can potentially emerge out of BRICS’ commitment to coordinating their policies and innovating – something this currency initiative represents.

About the Author:

Mihaela Papa, Adjunct Assistant Professor of Sustainable Development and Global Governance, The Fletcher School, Tufts University

The US indices traded yesterday without a single trend. By the close of trading yesterday, the Dow Jones Index (US30) decreased by 0.22%, while the S&P 500 Index (US500) was down by 0.04%. The Technology Index NASDAQ (US100) closed yesterday positive by 0.27%.

The US trade deficit narrowed by 6.1% to $91.1 billion from $97.1 billion in April. But even with the reduction in May, the trade deficit is up more than 10% since March. According to analysts, trade is likely to be a drag on US economic growth in the second quarter.

Tesla (TSLA) shares jumped more than 2% on optimism that lower prices supported demand and pushed sales to record levels in the April-June quarter. Analysts estimate Tesla could sell 155,000 vehicles in China in Q2, up 13% from the first quarter.

Stock markets in Europe mostly rose Wednesday. German DAX (DE30) gained 0.64%, French CAC 40 (FR40) added 0.98% yesterday, Spanish IBEX 35 (ES35) jumped by 0.99%, and British FTSE 100 (UK100) closed positive by 0.52%.

ECB President Christine Lagarde said yesterday that if the base case scenario holds, the European Central Bank will continue to raise rates in July. She added that core inflation is not declining as expected and did not comment on the September meeting. At the same time, Fed Chairman Powell indicated that monetary policy was not restrictive enough and said he did not rule out the possibility of raising rates at the next meetings. The Fed chief added that the strong labor market continues to fuel consumer spending, which accounts for about two-thirds of economic growth. The policymaker’s comments increased the likelihood of a Fed rate hike in July to about 82%, up from 74% the day before.

Governor Bailey told the European Central Bank Forum that last week’s decision to raise the bank rate from 4.5% to 5% was the best way the Bank of England could have responded to the latest economic data. Market indicators imply further bank rate hikes to 6.00% by the end of the year as service sector price-fixing boosted core inflation for the second month in a row. That said, markets are predicting no rate cuts this year and for most of 2024 through September.

Inflation in Italy was softer than expected and down significantly from the previous month, which bodes well for the broader EU inflation figure to be released Friday. Italy’s inflation rate fell to 6.4% from 7.6% y/y. Germany will release the inflation data today.

Asian markets were mostly bullish yesterday. Japan’s Nikkei 225 (JP225) gained 2.02%, China’s FTSE China A50 (CHA50) gained 0.36%, Hong Kong’s Hang Seng (HK50) added 0.12% on the day, while Australia’s S&P/ASX 200 (AU200) closed up by 1.10% on Wednesday.

Bank of Japan (BOJ) Governor Kazuo Ueda said Wednesday that the Central Bank would see a good reason to change monetary policy if it is “reasonably confident” that the country’s inflation rate will accelerate in 2024 after a period of slowdown. The Bank of Japan expects inflation to slow due to the waning effects of past import price hikes before rising again in 2024, Ueda said at the Central Bank forum. Asked whether Japan could intervene in the currency market to support the yen, Ueda said that the decision fell under the jurisdiction of the Finance Ministry.

S&P 500 (F) (US500) 4,376.86 −1.55 (−0.035%)

Dow Jones (US30)33,852.66 −74.08 (−0.22%)

DAX (DE40) 15,949.00 +102.14 (+0.64%)

FTSE 100 (UK100) 7,500.49 +39.03 (+0.52%)

USD Index 103.01 +0.52 (+0.50%)

Important events for today:

– Japan Retail Sales (m/m) at 02:50 (GMT+3);

– Australia Retail Sales (m/m) at 04:30 (GMT+3);

– US Fed Chair Powell Speaks (m/m) at 09:30 (GMT+3);

– German Consumer Price Index (m/m) at 15:00 (GMT+3);

– US GDP (q/q) at 15:30 (GMT+3);

– US Initial Jobless Claims (w/w) at 15:30 (GMT+3);

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

Coming into 2023, no one would’ve expected a banking crisis on either side of the Atlantic (recall how SVB and Credit Suisse collapsed), nor being a whisker away from a civil war in Russia.

But traders and investors have taken things in stride, weathering bouts of volatility and uncertainty.

Of course, spot gold needed the help of an unexpected banking crisis in the US and Europe to send investors scurrying towards the safe haven asset.

But after coming to within 0.57% or about $12 away from its record high ($2074.87 on 7th August 2020), gold has crumbled since May.

Why has gold fallen since May?

This is because markets have pushed back expectations for a Fed rate CUT.

Back in early May, markets had expected the Fed to LOWER its benchmark rates by September 2023.

However, US inflation has since proven stubborn and the Fed appears willing to trigger more rate hikes than previously expected.

Today (June 29th), markets expect a 70% chance that the Fed will CUT rates only in May 2024!

Hence, given that investors are not paid to hold on to gold (a zero-yielding asset), markets have since dumped the precious metal in favour of other asset classes.

Gold remains the second best-performing traditional asset class so far this year.

(excluding cryptos such as Bitcoin which has soared by more than 85% over the same period).

First place in 1H23 goes to global stocks (measured by MSCI ACWI Index) which climbed by 11.4%.

Second-placed bullion has a year-to-date gain of about 4.4% at the time of writing.

2) USDJPY back down to 125?

No, but it came close.

USDJPY initially appeared destined to claim the 125 target, reaching as low as 127.224 by mid-January.

Since then, USDJPY broke out of its downtrend to recently form a golden cross (when 50-day moving average crosses above 200-day moving average – a technical signal that often implies further gains ahead).

This major FX pair is now trading around its highest levels since November 2022.

Still-dovish BoJ: the incoming BoJ Governor keeps Japan’s benchmark rate mired in negative territory on signs that inflation is not as sticky as hoped.

This scenario would be made worse if the Fed stays hawkish and keeps sending US interest rates much higher than the currently forecasted peak of around 5%.

The “wrong” scenario cited above has instead been the case so far this year.

The Bank of Japan (BoJ) apparently isn’t yet budging from its negative interest rates regime, while the Fed now projects US rates to peak around 5.6%.

Hence, Yen bulls (those hoping the Yen will strengthen) have given up for now.

However, note that markets are still predicting a greater-than-even chance (55%) of a BoJ rate hike by Dec 2023.

Should those odds firm up, that may yet restore hope for a Yen recovery and a lower USDJPY eventually.

3) FTSE China A50 Index back above 14,000?

Yes. 14k line was breached on January 14th.

To be honest, when I saw that the psychologically-important 14,000 mark had been surpassed a mere 10 days after my January 4th article, I initially chided myself, thinking I should have been more bullish in my predictions.

Instead, this turned out to be a rather PRUDENT forecast.

Since peaking at 14,420 in late January, which was a further 3% beyond the 14k mark, this stocks index (which tracks the 50 largest A-share Chinese companies) has embarked on a downtrend (a series of lower highs and lower lows).

In other words …

The 14k mark was just about as good as it got for the CHNA50_m index so far in 2023.

This is because China’s much-hyped recovery has fizzled out.

The economic momentum has clearly struggled post lockdowns, to the point that the People’s Bank of China (PBOC – China’s central bank) has pivoted to a supportive policy stance.

The PBOC’s support policy stance is in stark contrast to that at other major central banks (Fed, ECB, BOE, etc.) who are still busy hiking interest rates.

Until China’s economic recovery can find a more solid footing, Chinese assets ranging from its stock markets to the Yuan are set to find it difficult to stage a meaningful recovery.

Same goes for other assets that are reliant on the Chinese economy, including the likes of the Australian dollar (AUDUSD) as well as oil prices.

So there you have it.

Surely, it has been an eventful first half.

If the 2nd half of 2023 proves to be as eventful, that may herald more trading opportunities across global financial markets.

Bitcoin boosters like to claim Bitcoin, and other cryptocurrencies, are becoming mainstream. There’s a good reason to want people to believe this.

The only way the average punter will profit from crypto is to sell it for more than they bought it. So it’s important to talk up the prospects to build a “fear of missing out”.

But the hard data on Bitcoin use shows it is rarely bought for the purpose it ostensibly exists: to buy things.

Little use for payments

The whole point of Bitcoin, as its creator “Satoshi Nakamoto” stated in the opening sentence of the 2008 white paper outlining the concept, was that:

A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial institution.

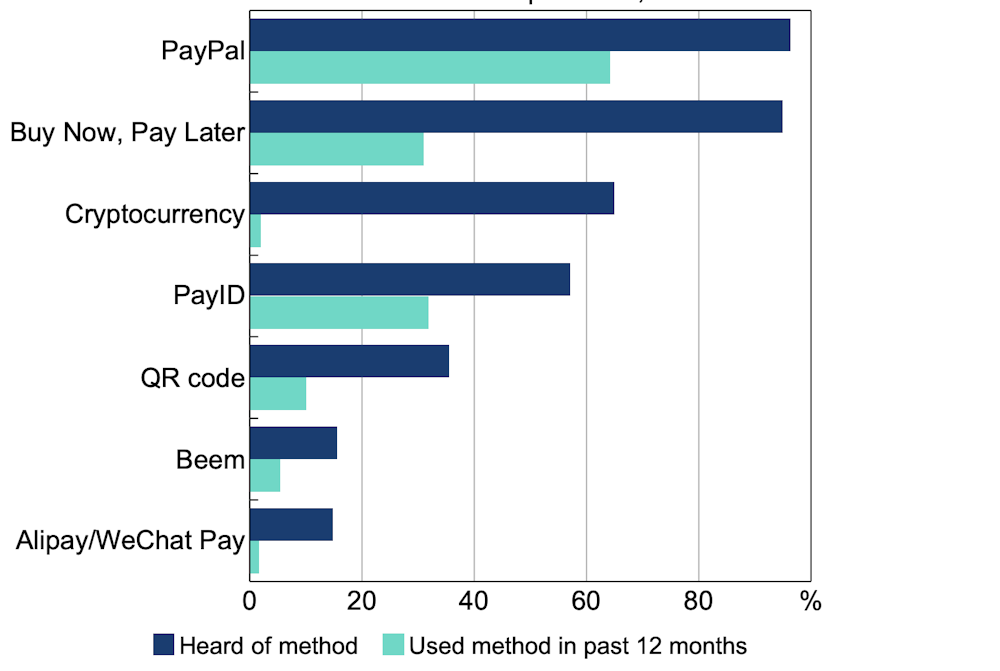

The latest data demolishing this idea comes from Australia’s central bank.

Every three years the Reserve Bank of Australia surveys a representative sample of 1,000 adults about how they pay for things. As the following graph shows, cryptocurrency is making almost no impression as a payments instrument, being used by no more than 2% of adults.

Payment methods being used by Australians

Reserve Bank calculations of Australians’ awareness vs use of different payment methods, based on Ipsos data.

By contrast more recent innovations, such as “buy now, pay later” services and PayID, are being used by around a third of consumers.

These findings confirm 2022 data from the US Federal Reserve, showing just 2% of the adult US population made a payment using a cryptocurrrency, and Sweden’s Riksbank, showing less than 1% of Swedes made payments using crypto.

The problem of price volatility

One reason for this, and why prices for goods and services are virtually never expressed in crypto, is that most fluctuate wildly in value. A shop or cafe with price labels or a blackboard list of their prices set in Bitcoin could be having to change them every hour.

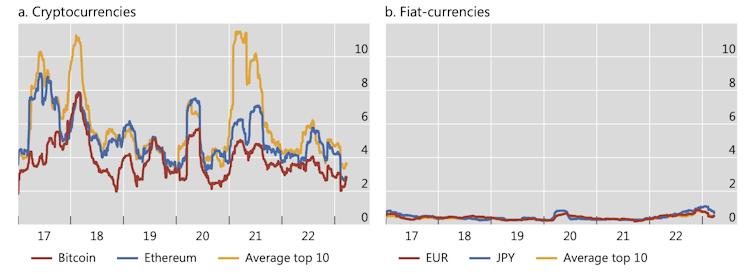

The following graph from the Bank of International Settlements shows changes in the exchange rate of ten major cryptocurrencies against the US dollar, compared with the Euro and Japan’s Yen, over the past five years. Such volatility negates cryptocurrency’s value as a currency.

There have been attempts to solve this problem with so-called “stablecoins”. These promise to maintain steady value (usually against the US dollar).

But the spectacular collapse of one of these ventures, Terra, once one of the largest cryptocurrencies, showed the vulnerability of their mechanisms. Even a company with the enormous resources of Facebook owner Meta has given up on its stablecoin venture, Libra/Diem.

This helps explain the failed experiments with making Bitcoin legal tender in the two countries that have tried it: El Salvador and the Central African Republic. The Central African Republic has already revoked Bitcoin’s status. In El Salvador only a fifth of firms accept Bitcoin, despite the law saying they must, and only 5% of sales are paid in it.

Storing value, hedging against inflation

If Bitcoin’s isn’t used for payments, what use does it have?

The major attraction – one endorsed by mainstream financial publications – is as a store of value, particularly in times of inflation, because Bitcoin has a hard cap on the number of coins that will ever be “mined”.

In terms of quantity, there are only 21 million Bitcoins released as specified by the ASCII computer file. Therefore, because of an increase in demand, the value will rise which might keep up with the market and prevent inflation in the long run.

The only problem with this argument is recent history. Over the course of 2022 the purchasing power of major currencies (US, the euro and the pound) dropped by about 7-10%. The purchasing power of a Bitcoin dropped by about 65%.

Speculation or gambling?

Bitcoin’s price has always been volatile, and always will be. If its price were to stabilise somehow, those holding it as a speculative punt would soon sell it, which would drive down the price.

But most people buying Bitcoin essentially as a speculative token, hoping its price will go up, are likely to be disappointed. A BIS study has found the majority of Bitcoin buyers globally between August 2015 and December 2022 have made losses.

The “market value” of all cryptocurrencies peaked at US$3 trillion in November 2021. It is now about US$1 trillion.

Bitcoins’s highest price in 2021 was about US$60,000; in 2022 US$40,000 and so far in 2023 only US$30,000. Google searches show that public interest in Bitcoin also peaked in 2021. In the US, the proportion of adults with internet access holding cryptocurrencies fell from 11% in 2021 to 8% in 2022.

UK government research published in 2022 found that 52% of British crypto holders owned it as a “fun investment”, which sounds like a euphemism for gambling. Another 8% explicitly said it was for gambling.

The UK parliament’s Treasury Committee, a group of MPs who examine economics and financial issues, has strongly recommended regulating cryptocurrency as form of gambling rather than as a financial product. They argue that continuing to treat “unbacked crypto assets as a financial service will create a ‘halo’ effect that leads consumers to believe that this activity is safer than it is, or protected when it is not”.

Whatever the merits of this proposal, the UK committtee’s underlying point is solid. Buying crypto does have more in common with gambling than investing. Proceed at your own risk, and and don’t “invest” what you can’t afford to lose.