John Newell of John Newell & Associates answers the question: is silver poised for a dramatic move higher?

A Case for Silver’s Rise

Silver has long been a precious metal that plays a dual role: a store of value and an industrial commodity. With recent economic trends and historical patterns, the case for a significant price increase in silver is becoming more compelling.

Below, we outline key fundamental reasons why silver could be on the verge of a dramatic move higher, supported by two charts, one short-term and one long-term, illustrating its potential trajectory.

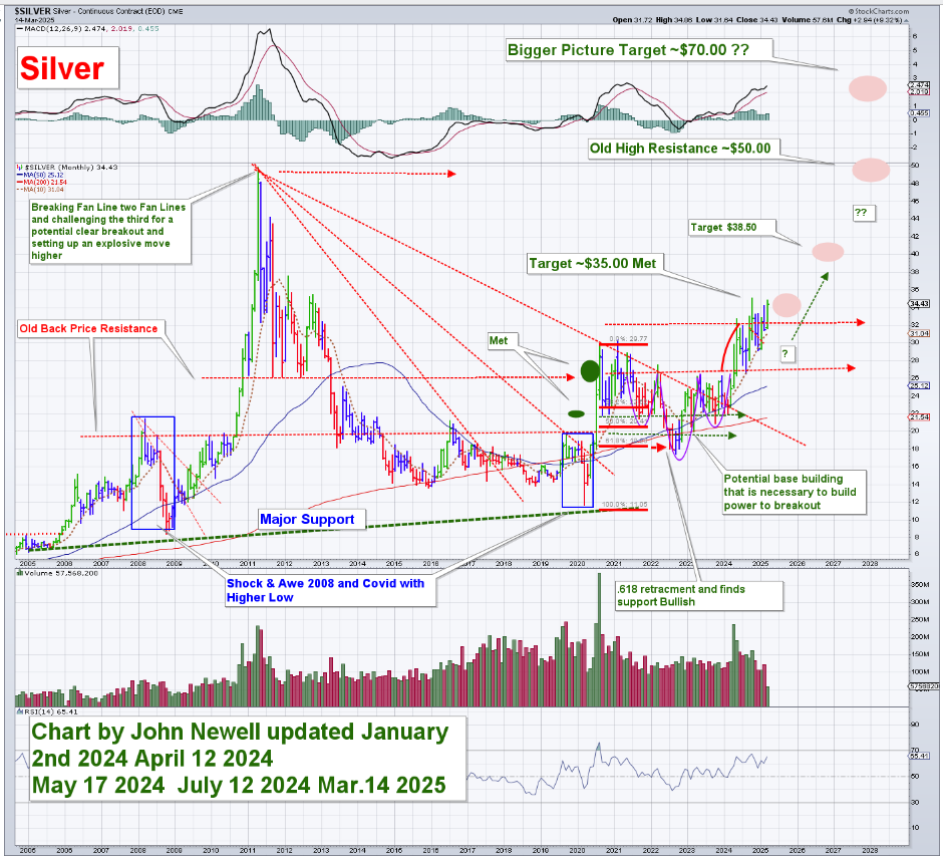

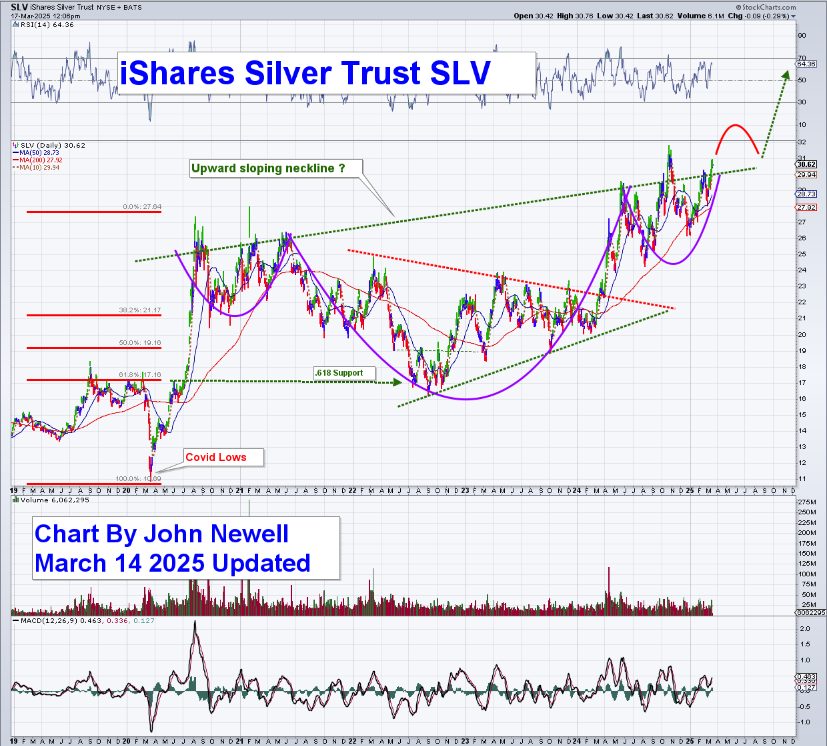

Technical: Silver Hits $35, Is $50 Next? And a March towards $70

The shorter-term chart shows that silver has recently achieved its $35 target and is building momentum toward higher levels.

Historically, when silver entered strong uptrends, it experienced parabolic moves. Looking at the past two major silver bull runs, if the metal were to repeat even an average of these moves (7x from its lows), silver could trade at $70 per ounce.

The long-term 50-year chart further strengthens this thesis. In previous major price surges, most notably in the late 1970s and 2010-2011, silver saw exponential growth over relatively short periods.

Given the similarities in today’s economic conditions to those times, there is reason to believe silver could be gearing up for another major bull cycle.

Fundamental Reasons for Silver’s Rise

- Hedge Against Inflation

Silver, like gold, is a well-known hedge against inflation. With rising inflation concerns and central banks continuing to lose monetary policies, silver provides a means to preserve purchasing power. Historically, when inflation accelerates, precious metals tend to perform well.

- Growing Industrial Demand

Unlike gold, silver is an essential industrial metal with applications in:

Electronics: Silver is used in high-performance electronic devices due to its superior conductivity.

Solar Panels: The renewable energy push is expected to drive increased demand for silver in solar technology.

Medical Uses: Silver’s antibacterial properties make it vital in the medical industry. As global industries expand and modernize, silver’s demand is expected to rise, creating upward pressure on prices.

- Affordability and Accessibility

Compared to gold, silver remains much more affordable. This makes it an attractive investment for a wider range of investors, particularly in emerging markets where gold prices may be out of reach for many. If gold continues to rise, silver could see increased inflows as an alternative store of value.

- Portfolio Diversification

Silver provides diversification benefits as it often moves independently from traditional asset classes such as stocks and bonds. In uncertain times, investors flock to safe-haven assets like silver, reducing overall portfolio risk.

- Market Volatility and Economic Uncertainty

Silver has historically performed well during periods of economic instability. If global markets experience turmoil—whether from geopolitical events, recession fears, or monetary instability, silver could benefit as a safe-haven asset.

Ways to Participate in Silver’s Potential Upside

While buying physical silver in the form of coins or bars is a traditional method of investing, there are other ways to gain exposure to silver’s expected price appreciation. Exchange-traded funds (ETFs) offer a convenient alternative:

SLV (iShares Silver Trust): The largest silver ETF, holding physical silver. It provides a direct investment in silver without needing to store it.

Sprott Physical Silver Trust (PSLV): Another option for direct silver exposure, backed by physical silver held in secure vaults.

SIL (Global X Silver Miners ETF): Holds shares in approximately 33 silver mining companies, allowing investors to gain exposure to the industry.

SILJ (Amplify Junior Silver Miners ETF): Tracks small-cap companies primarily engaged in silver mining, exploration, and development, providing leveraged exposure to silver price movements.

Additionally, several silver mining companies are currently trading at low price-to-earnings (P/E) ratios. As the silver price rises, these companies could experience a leveraged effect, potentially amplifying returns for investors.

A Modern ‘Hunt Brothers’ Scenario?

In the late 1970s, the Hunt brothers attempted to corner the silver market, causing prices to skyrocket. While modern regulations prevent such extreme market manipulation, a global shift in investor sentiment could replicate similar price movements.

Imagine a scenario where large populations, such as those in BRICS nations, turn to silver as an alternative to gold. If gold becomes prohibitively expensive for average investors, silver could become their precious metal of choice.

Potential Outcomes of a Global Silver Rush:

Surging Prices: Increased demand from millions of investors could push silver prices significantly higher.

Increased Market Volatility: Rapid price increases may lead to volatile market conditions.

Silver Mining Stocks Boom: Companies producing silver could see substantial gains.

Industrial Costs Rise: Industries reliant on silver (e.g., solar panels and electronics) could face higher production costs.

Regulatory Intervention: Governments and financial institutions may take action to stabilize the market.

Conclusion: Silver’s Future Looks Bright

Given silver’s role as an inflation hedge, its growing industrial demand, and its affordability compared to gold, there are strong fundamental reasons for its price to rise significantly.

Technically, the metal has reached its $35 target and appears to be building momentum toward higher levels. If history is any guide, a move toward $50, and even $70, is well within the realm of possibility.

For investors looking to position themselves in an asset with significant upside potential, silver presents a compelling opportunity in today’s economic landscape.

The link to a previous article on the fundamentals of silver can be found here.

Important Disclosures:

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

John Newell Disclaimer

As always it is important to note that investing in precious metals like silver carries risks, and market conditions can change violently with shock and awe tactics, that we have seen over the past 20 years. Before making any investment decisions, it’s advisable consult with a financial advisor if needed. Also the practice of conducting thorough research and to consider your investment goals and risk tolerance.