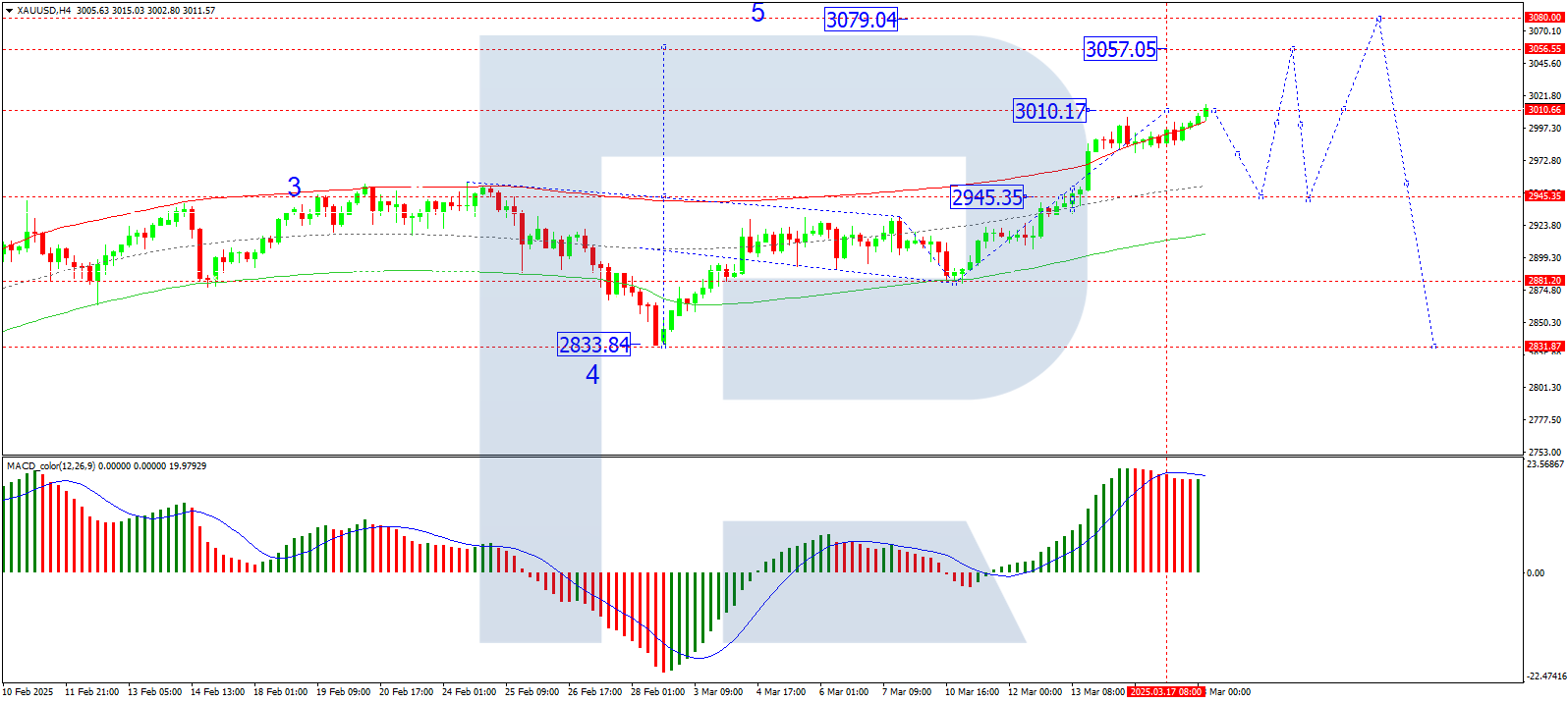

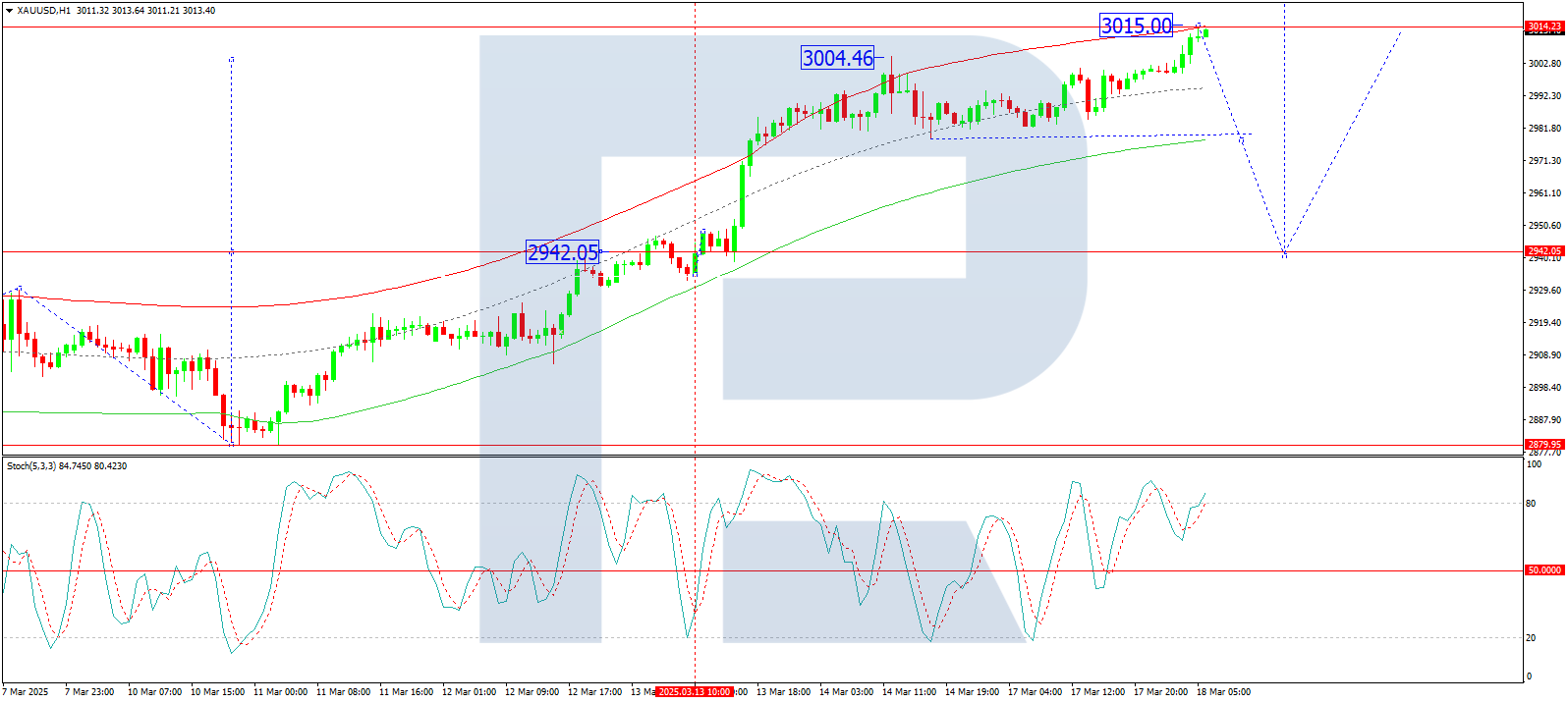

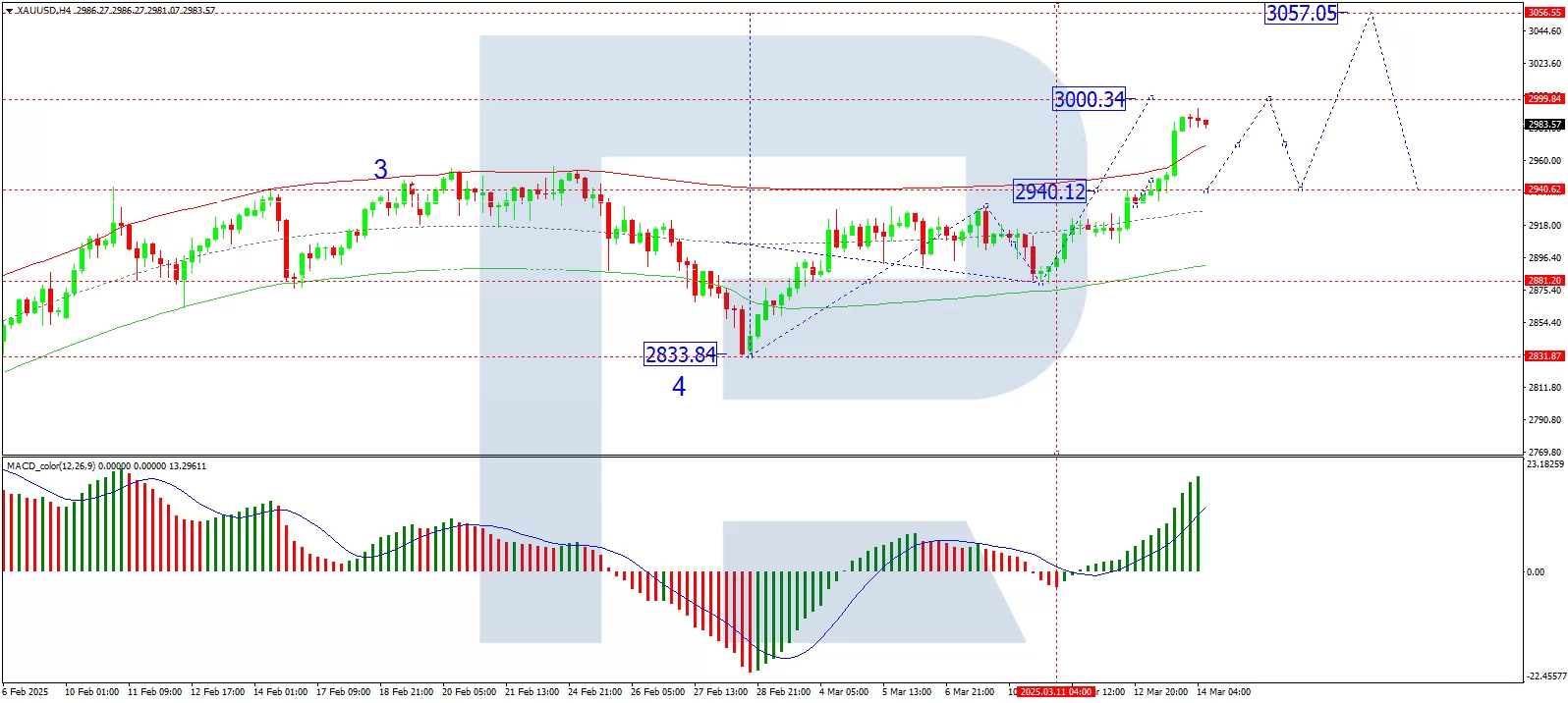

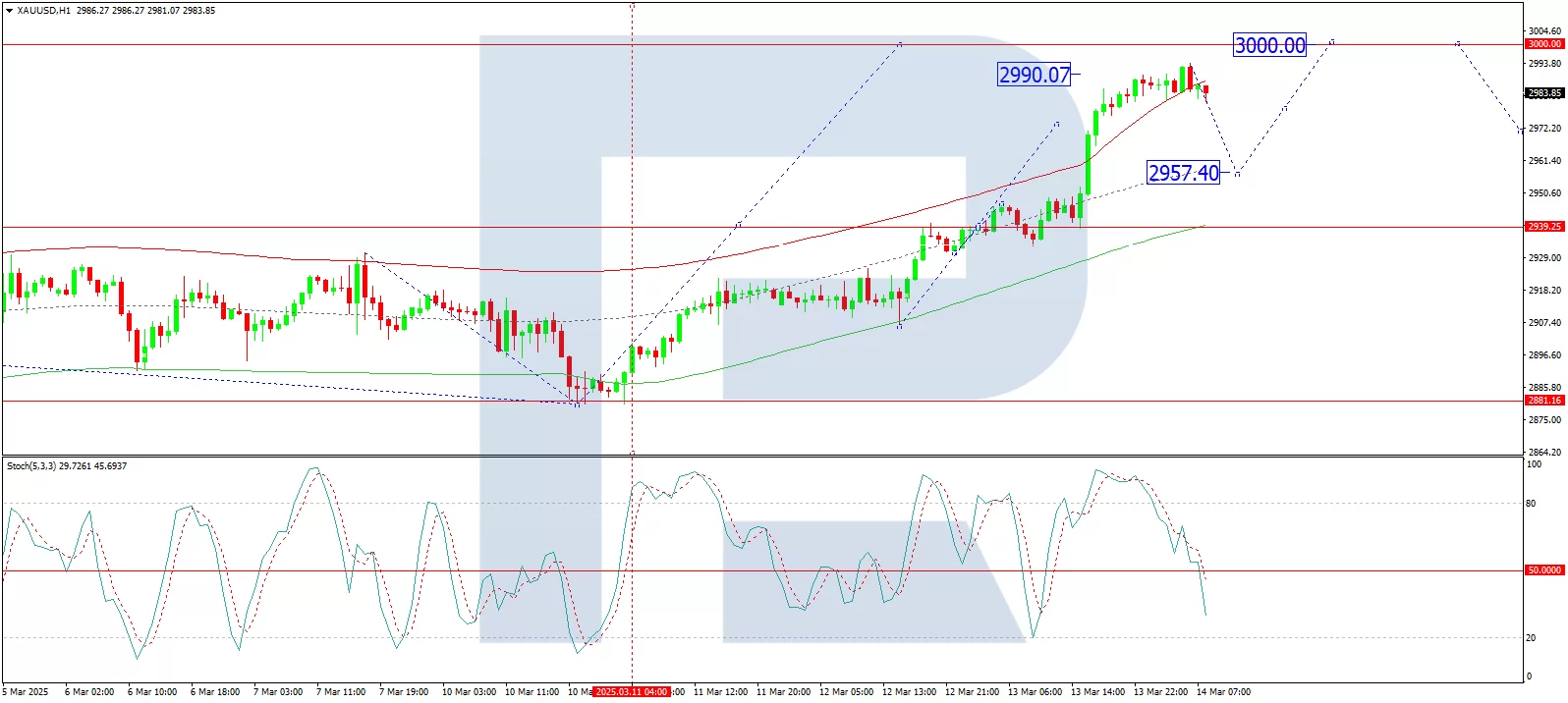

By JustMarkets

Stocks on Wall Street started the week on an optimistic note. On Monday, the Dow Jones (US30) rose 0.85%. The S&P 500 Index (US500) gained 0.64%. The Nasdaq Technology Index (US100) was up 0.55%. Softer-than-expected retail sales data, which showed a modest 0.2% increase in February, fueled speculation that the Federal Reserve may lean toward cutting rates later this year. Despite the broad market rally, major technology stocks lagged, with Tesla down 4.8% and Nvidia down 1.7% as investors overestimated their high valuations amid ongoing economic uncertainty. Finance Minister Bessent attempted to calm markets by characterizing the correction as “healthy” while acknowledging that recession risks remain. Market participants are now turning their attention to the upcoming Fed meeting, awaiting signals on how Trump’s shifting trade policies may affect future economic decisions.

The Canadian dollar strengthened to 1.43 per US dollar — a three-week high — to ease trade tensions, a weaker US dollar, and an improved outlook for foreign exchange inflows. Senior Canadian officials reported tangible progress in US-Canada trade talks, with both sides reaching tentative agreements to phase out retaliatory tariffs designed to stabilize trade flows and address key concerns such as escalating tariffs on critical goods.

The OECD lowered its 2025 growth expectations for G20 economies to 3.1% from 3.3% and for 2026 to 2.9% from 3.2%, citing rising trade barriers and political uncertainty holding back investment and spending. The US economy is now expected to grow 2.2% in 2025 (vs. 2.4% projections in December) and 1.6% in 2026 (vs. 2.1%). Canada’s growth expectations have been sharply lowered to 0.7% in both years (from 2%) and Mexico is expected to contract by 1.3% in 2025 and 0.6% in 2026, reversing previous growth estimates. In Europe, the Eurozone is expected to grow by 1.0% in 2025 (down from 1.3%) and 1.2% in 2026 (up from 1.5%), with downgrades for Germany, France, and Italy partially offset by an upgrade for Spain. The UK growth projections have also been lowered to 1.4% in 2025 (vs. 1.7%) and 1.2% in 2026 (vs. 1.3%). Meanwhile, China’s economy is expected to grow at 4.8% this year (vs. 4.7%) before slowing to 4.4% in 2026.

Equity markets in Europe were mostly up yesterday. Germany’s DAX (DE40) rose by 0.73%, France’s CAC 40 (FR40) closed higher by 0.57%, Spain’s IBEX 35 (ES35) added 1.09%, and the UK’s FTSE 100 (UK100) closed positive 0.56%. In Germany, traders awaited a crucial vote on Germany’s spending plan set for tomorrow. The proposed reform aims to exempt defense spending from debt restrictions and create a €500 billion infrastructure investment fund. It requires a two-thirds majority in both legislative chambers to pass, but the CDU/CSU bloc, led by election winner Friedrich Merz, is expected to garner the necessary number of votes to amend the constitution.

WTI crude oil prices rose to $67.8 a barrel on Tuesday, marking the third straight session of gains, amid concerns over supply disruptions caused by ongoing conflicts in the Middle East. Israel launched a large-scale offensive on the Gaza Strip today, the first major strike since a truce went into effect in January. In addition, US President Trump on Monday threatened to hold Iran responsible for any attacks by Yemen’s Houthis, stepping up his campaign of pressure on Tehran.

Asian markets traded higher yesterday. Japan’s Nikkei 225 (JP225) rose by 0.93%, China’s FTSE China A50 (CHA50) gained 0.06%, Hong Kong’s Hang Seng (HK50) added 0.77% and Australia’s ASX 200 (AU200) gained 0.90%.

On Monday, Chinese economic data sparked optimism with retail sales accelerating and industrial production exceeding expectations, but lower factory output and a two-year high in the urban unemployment rate tempered prognoses. Meanwhile, Trump announced that Xi Jinping will visit Washington amid escalating trade tensions, although no official dates for the visit were confirmed, adding to investor uncertainty.

The New Zealand dollar traded near US$0.581 on Tuesday, at its highest level since early December, driven by growing optimism about China’s economic outlook. This followed the release of favorable retail sales data and new Chinese initiatives aimed at boosting consumer spending, which boosted the China-focused kiwi. Further boosting the antipodean currency was the continued weakening of the US dollar amid economic uncertainty and heightened trade tensions.

S&P 500 (US500) 5,675.12 +36.18 (+0.64%)

Dow Jones (US30) 41,841.63 +353.44 (+0.85%)

DAX (DE40) 23,154.57 +167.75 (+0.73%)

FTSE 100 (UK100) 8,680.29 +47.96 (+0.56%)

USD Index 103.41 −0.31 (−0.30%)

News feed for: 2025.03.18

- German ZEW Economic Sentiment (m/m) at 12:00 (GMT+2);

- Eurozone ZEW Economic Sentiment (m/m) at 12:00 (GMT+2);

- Eurozone Trade Balance (m/m) at 12:00 (GMT+2);

- Canada Consumer Price Index (m/m) at 14:30 (GMT+2);

- US Building Permits (m/m) at 14:30 (GMT+2);

- US Industrial Production (m/m) at 15:15 (GMT+2).

By JustMarkets

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.