By JustMarkets

At yesterday’s stock market close, the Dow Jones Index (US30) jumped by 1.16%, while the S&P 500 Index (US500) added 0.90%. The NASDAQ Technology Index (US100) closed positive by 0.61% on Monday.

Warren Buffett’s Berkshire Hathaway (BRK) reported better-than-expected quarterly results on the back of strong results from its insurance companies, sending its share price up more than 3% on the report. Palantir (PLTR) shares were up more than 2% after the company released its second-quarter results. The company’s revenue rose by 13% year-over-year to $533 million, slightly below the consensus estimate of $534.21 million.

The US Federal Reserve spokeswoman Michelle Bowman reiterated her view that the US central bank may need to raise rates further to fully restore price stability. “I supported an increase in the federal funds rate at our July meeting, and I expect that additional rate hikes will likely be needed to bring inflation down to the level set by the FOMC,” Bowman said.

Equity markets in Europe were mostly down yesterday. Germany’s DAX (DE40) was down by 0.01%, France’s CAC 40 (FR40) added 0.06% on Monday, Spain’s IBEX 35 (ES35) decreased by 0.10%, and the UK’s FTSE 100 (UK100) closed negative by 0.13%.

Germany’s Central Bank (Bundesbank) stops charging interest on government cash. Short-term German debt enjoyed strong demand on Monday after the country’s central bank said it would stop paying interest on domestic government deposits, which could lead to billions of euros flowing into higher-yielding securities.

UK food price inflation is likely to fall to around 10% later this year, but further policy tightening will be needed for overall consumer price inflation (CPI) to return to the 2% target, Bank of England (BoE) chief economist Huw Pill said on Monday. The policymaker also believes that multiple rate hikes have yet to hit the UK economy.

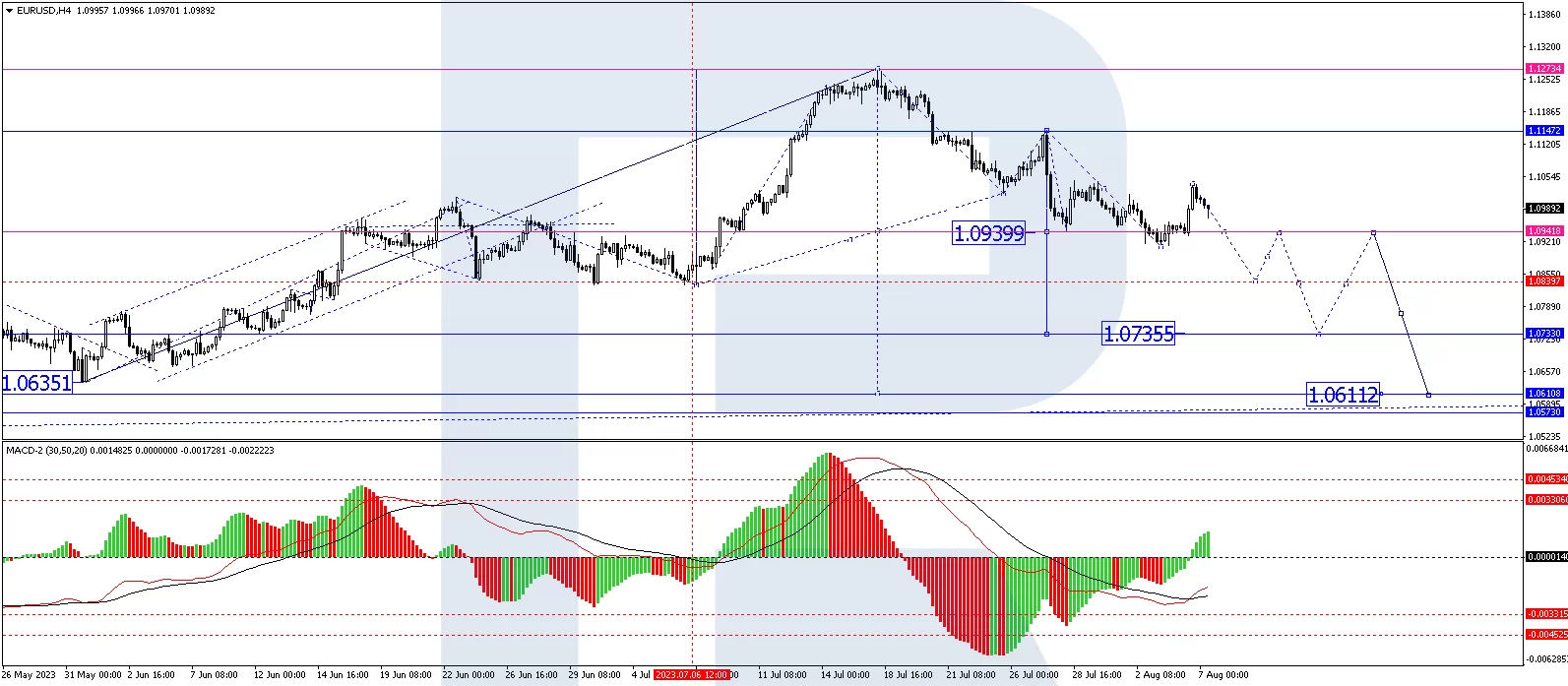

Natural gas prices have been mostly declining over the past week. Overall, prices for this natural gas have fallen by about 2.3% over the past two weeks. This is the worst performance in this interval since early July. However, despite the decline, natural gas remains in a neutral price range.

Asian markets were down yesterday. Japan’s Nikkei 225 (JP225) gained 0.19%, China’s FTSE China A50 (CHA50) fell by 0.58%, Hong Kong’s Hang Seng (HK50) ended the day down by 0.01%, and Australia’s S&P/ASX 200 (AU200) ended Monday negative by 0.22%.

Chinese indices extended declines at the open on Tuesday as trade balance data showed that the country’s exports and imports continued to decline in July. The data points to increased pressure on the Chinese economy due to weak demand and does not bode well for the broader Asian markets related to trade with the country.

Japanese authorities are unlikely to intervene in currency markets to support the yen, as the currency has already found some support and will rise significantly as US interest rates rise, according to former finance official Eisuke Sakakibara.

S&P 500 (F)(US500) 4,518.44 +40.41 (+0.90%)

Dow Jones (US30) 35,473.13 +407.51 (+1.16%)

DAX (DE40) 15,950.76 −1.10 (−0.01%)

FTSE 100 (UK100) 7,554.49 −9.88 (−0.13%)

USD Index 102.09 +0.08 (+0.07%)

- – Australia NAB Business Confidence (m/m) at 04:30 (GMT+3);

- – China Trade Balance (m/m) at 06:00 (GMT+3);

- – German Consumer Price Index (m/m) at 09:00 (GMT+3);

- – US Trade Balance (m/m) at 15:30 (GMT+3);

- – Canada Trade Balance (m/m) at 15:30 (GMT+3).

By JustMarkets

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.