By InvestMacro

Here are the latest charts and statistics for the Commitment of Traders (COT) reports data published by the Commodities Futures Trading Commission (CFTC).

The latest COT data is updated through Tuesday May 5th and shows a quick view of how large traders (for-profit speculators and commercial entities) were positioned in the futures markets.

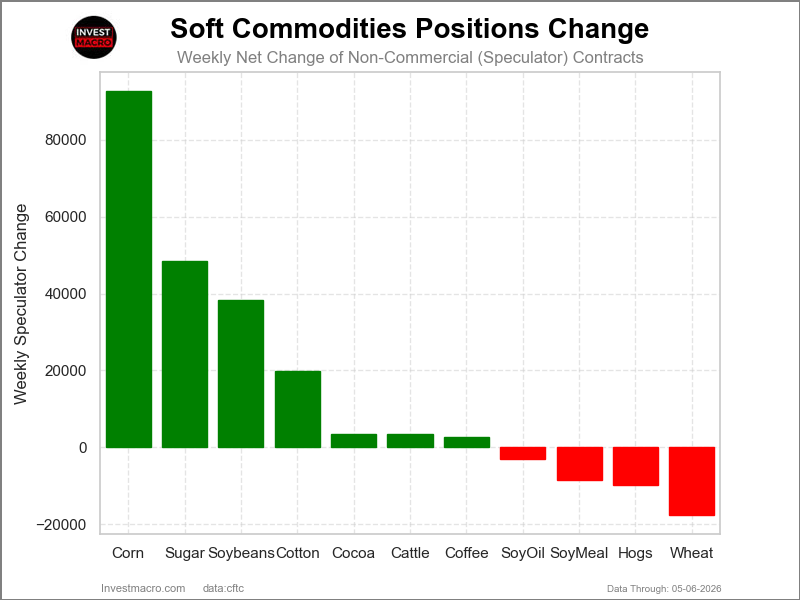

Weekly Speculator Changes led by Corn & Sugar

The COT soft commodities markets speculator bets were overall higher this week as seven out of the eleven softs markets we cover had higher positioning while the other four markets had lower speculator contracts.

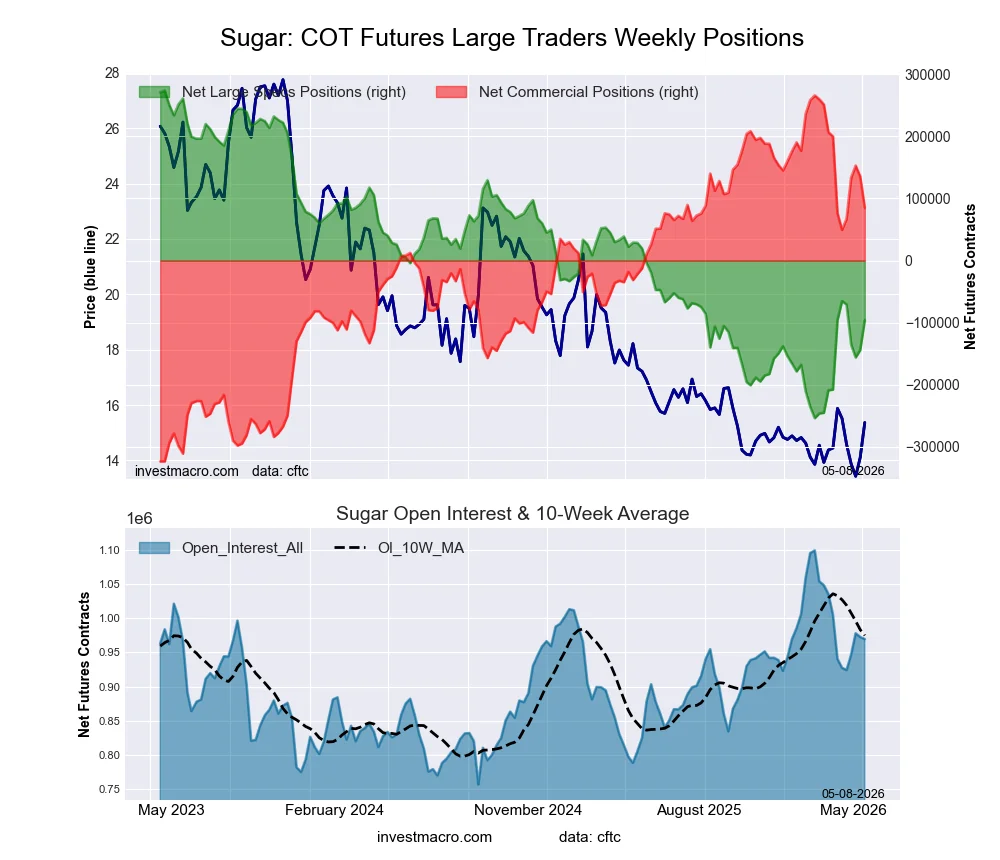

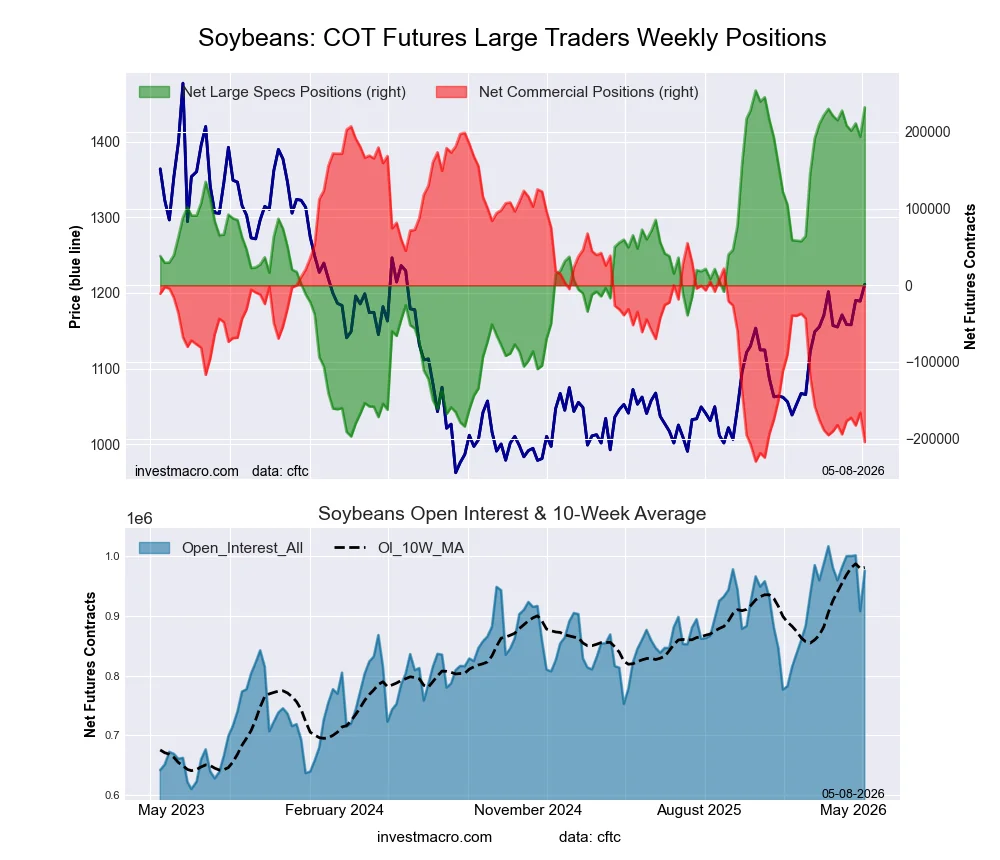

Leading the gains for the softs markets was Corn (92,644 contracts) with Sugar (48,432 contracts), Soybeans (38,259 contracts), Cotton (19,741 contracts), Cocoa (3,409 contracts) and Live Cattle (3,381 contracts) also showing positive weeks.

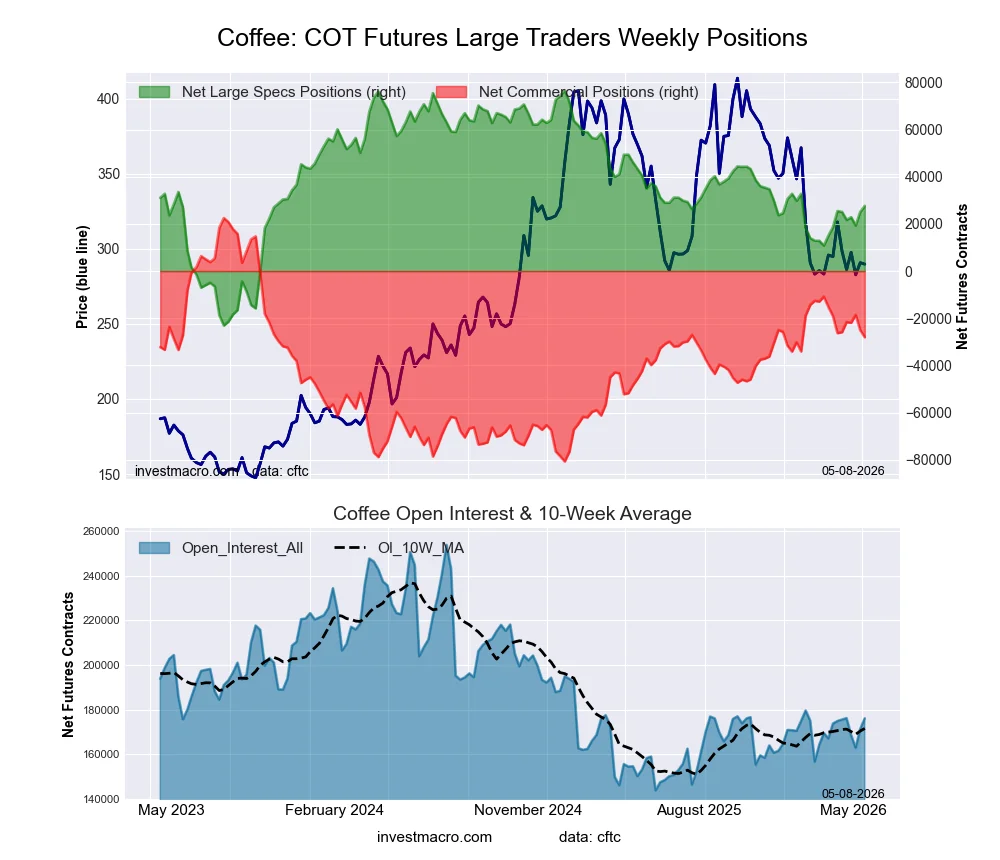

The markets with the declines in speculator bets this week were Wheat (-17,534 contracts) with Lean Hogs (-9,721 contracts), Soybean Meal (-8,387 contracts), Soybean Oil (-2,925 contracts) and Coffee (2,599 contracts) also registering lower bets on the week.

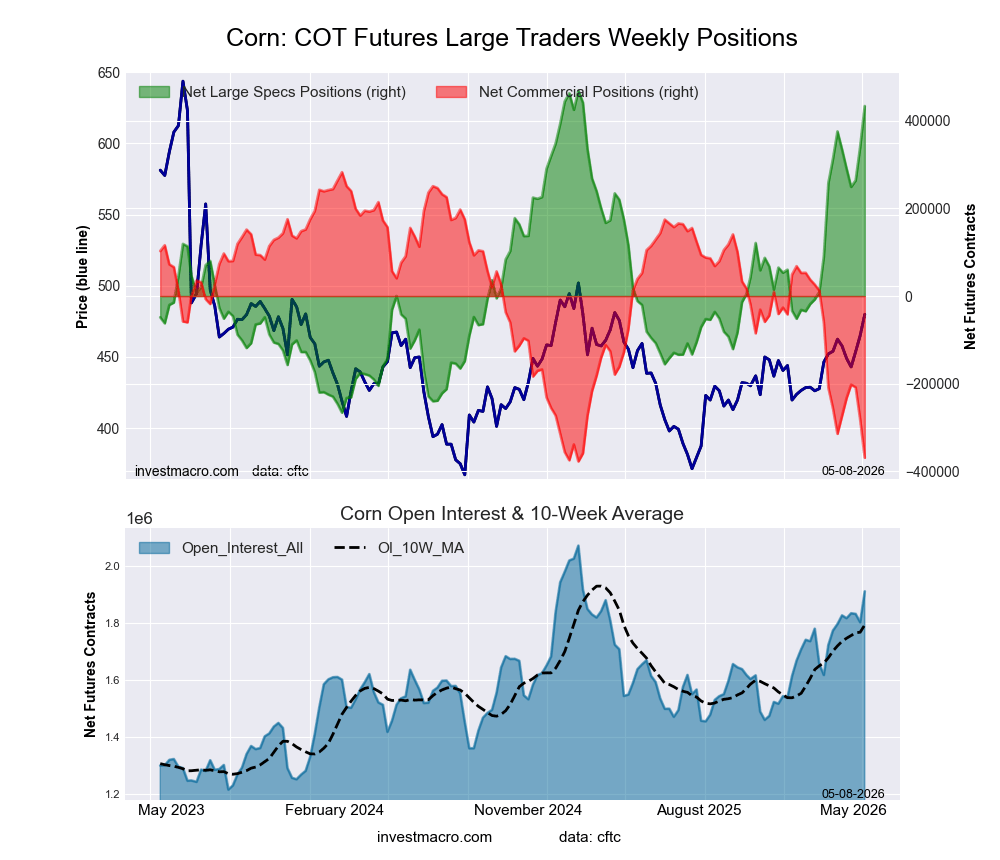

Corn Speculator Bets surge higher for 3rd Week to 1-Year High

Highlighting the Soft Commodities market this week is Corn, which has been on a spectacular run in speculator positioning. This week, Corn speculator bets jumped by over 92,000 contracts and rose for a third consecutive week. The Corn speculator position has now increased in eight out of the last 11 weeks and has added a whopping +441,219 contracts to its overall standing in just those 11 weeks. This recent climb higher has seen the overall speculator position from a total of -7,835 net contracts on February 17th to this week’s net speculator standing of 433,384 net contracts — marking the highest level for Corn bets in over a year.

Corn’s futures price has been on a steady uptrend since a recent bottom in August of 2025. Since then, the Corn price has been up by roughly 25% and is trading right below its 200-weekly moving average. Corn’s overall price is still down by roughly 70% since 2022, when the height of the Russian-Ukraine War saw the Corn price go parabolic and reach its highest level in 10 years.

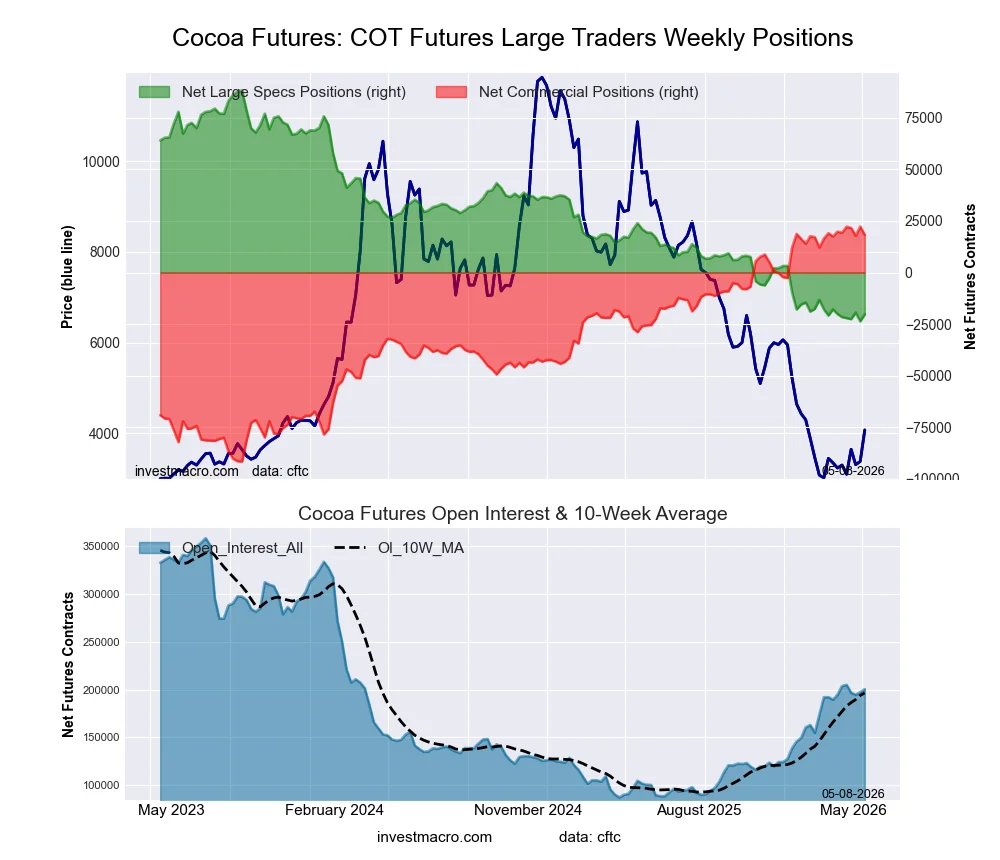

Cocoa leads Soft Commodities price performances this week.

Leading the price performances for the Soft Commodities on the week was Cocoa, which had a very strong week this week and was only one of two Soft Commodities markets that saw gaining returns this week. Cocoa jumped by 17.87% over the past five days and gained for a third consecutive week. Cocoa’s overall price over the past few years has taken a sharp fall after an incredible run-up that brought the Cocoa future prices over 12,000 in late 2024. Currently, Cocoa’s price has fallen by over 60% since that timeframe but has been rebounding since March.

Next up, Cotton was the only other gainer on the week with a 0.76% gain. On the downside, Soybeans dipped by a virtually unchanged amount of -0.14%, followed by Soybean Meal, which also dipped by -0.16%. Wheat fell by over a percent with a -1.35% decline, followed by Live Cattle, which dipped by -1.51%, while Soybean Oil fell by a similar -1.54%. Corn was next up and fell lower this week with -1.72%. Sugar followed suit with a -1.74% decline, while Lean Hogs dropped by -2.62% on the week. Coffee was the biggest negative returner this week with a -4.26% shortfall.

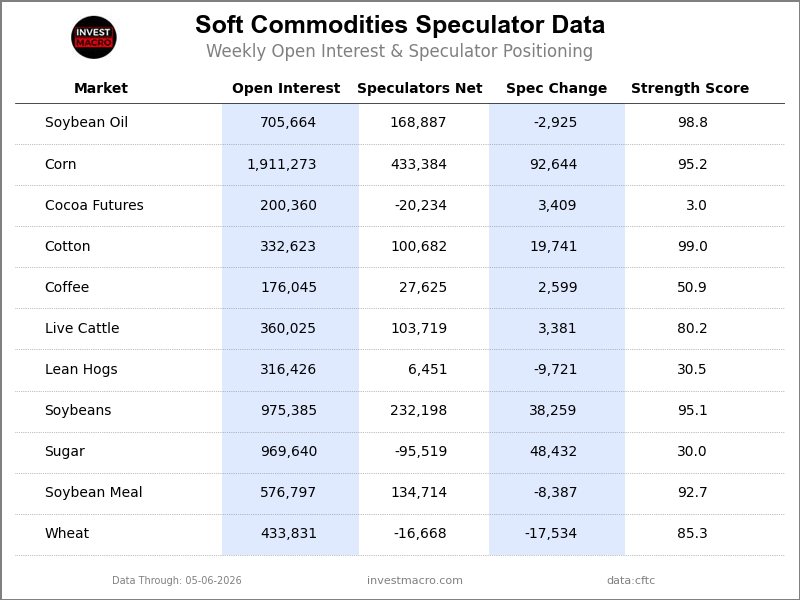

Soft Commodities Data:

Legend: Weekly Speculators Change | Speculators Current Net Position | Speculators Strength Score compared to last 3-Years (0-100 range)

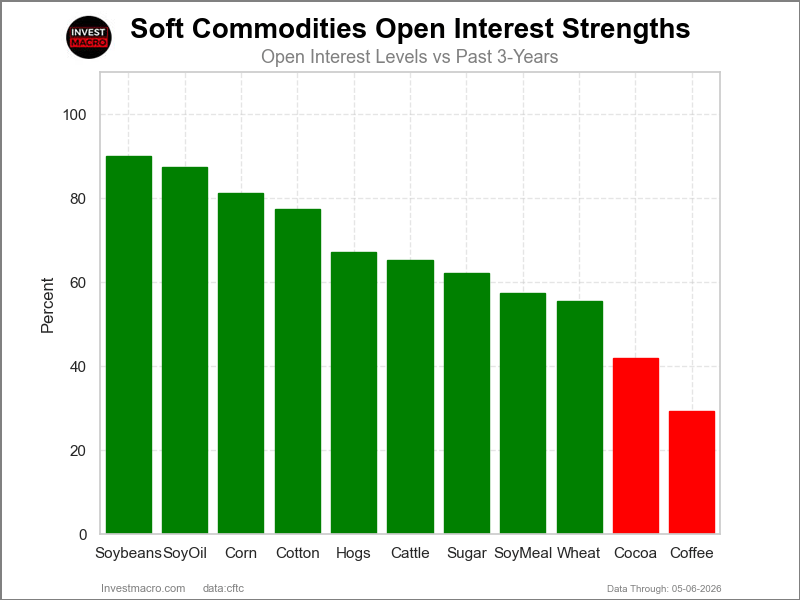

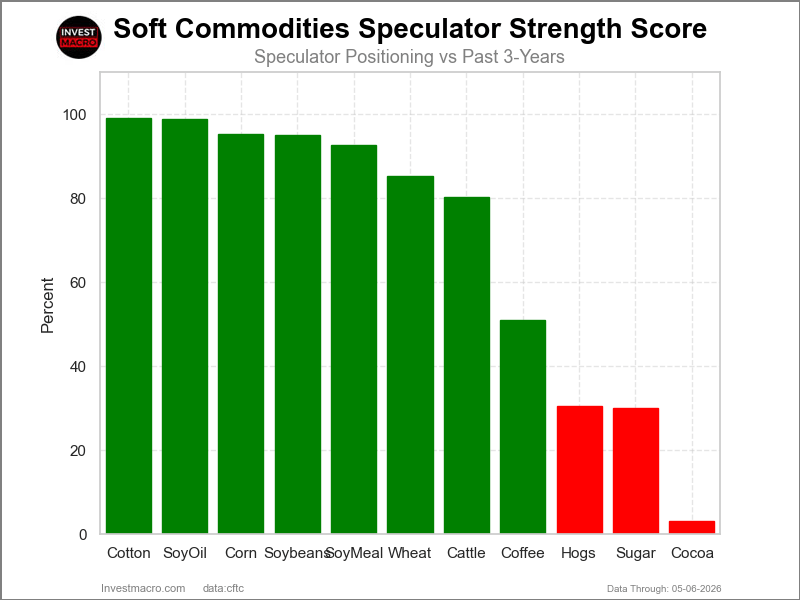

Strength Scores led by Soybean Oil & Cotton

COT Strength Scores (a normalized measure of Speculator positions over a 3-Year range, from 0 to 100 where above 80 is Extreme-Bullish and below 20 is Extreme-Bearish) showed that Soybean Oil (99 percent) and Cotton (99 percent) lead the softs markets this week. Soybeans (95 percent), Corn (95 percent) and Soybean Meal (93 percent) come in as the next highest in the weekly strength scores.

On the downside, Cocoa (3 percent) comes in at the lowest strength levels currently and is in Extreme-Bearish territory (below 20 percent). The next lowest strength scores are Sugar (30 percent) and Lean Hogs (31 percent).

Strength Statistics:

Corn (95.2 percent) vs Corn previous week (82.6 percent)

Sugar (30.0 percent) vs Sugar previous week (20.8 percent)

Coffee (50.9 percent) vs Coffee previous week (48.3 percent)

Soybeans (95.1 percent) vs Soybeans previous week (86.7 percent)

Soybean Oil (98.8 percent) vs Soybean Oil previous week (100.0 percent)

Soybean Meal (92.7 percent) vs Soybean Meal previous week (96.2 percent)

Live Cattle (80.2 percent) vs Live Cattle previous week (76.9 percent)

Lean Hogs (30.5 percent) vs Lean Hogs previous week (37.5 percent)

Cotton (99.0 percent) vs Cotton previous week (87.3 percent)

Cocoa (3.0 percent) vs Cocoa previous week (0.0 percent)

Wheat (85.3 percent) vs Wheat previous week (100.0 percent)

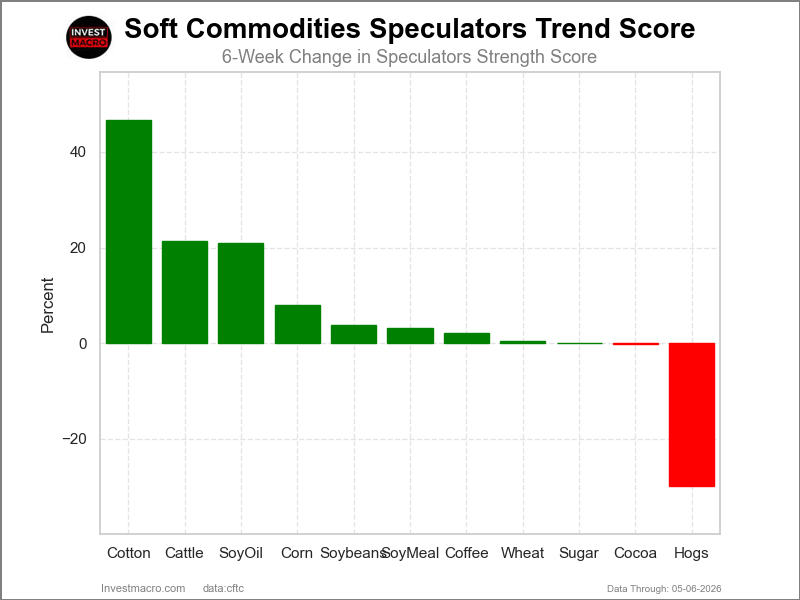

Cotton, Live Cattle & Soybean Oil top the 6-Week Strength Trends

COT Strength Score Trends (or move index, calculates the 6-week changes in strength scores) showed that Cotton (47 percent), Soybean Oil (21 percent) and Live Cattle (21 percent) lead the past six weeks trends for soft commodities. Corn (8 percent) and Soybeans (4 percent) are the next highest positive movers in the latest trends data.

Lean Hogs (-30 percent) leads the downside trend scores currently with Cocoa (-0.1 percent) following next with a lower trend score.

Strength Trend Statistics:

Corn (7.9 percent) vs Corn previous week (3.9 percent)

Sugar (0.1 percent) vs Sugar previous week (12.1 percent)

Coffee (2.2 percent) vs Coffee previous week (6.5 percent)

Soybeans (3.8 percent) vs Soybeans previous week (-6.0 percent)

Soybean Oil (20.9 percent) vs Soybean Oil previous week (20.9 percent)

Soybean Meal (3.2 percent) vs Soybean Meal previous week (17.0 percent)

Live Cattle (21.4 percent) vs Live Cattle previous week (22.0 percent)

Lean Hogs (-29.9 percent) vs Lean Hogs previous week (-33.6 percent)

Cotton (46.7 percent) vs Cotton previous week (38.5 percent)

Cocoa (-0.1 percent) vs Cocoa previous week (-5.2 percent)

Wheat (0.4 percent) vs Wheat previous week (22.3 percent)

Individual Soft Commodities Markets:

CORN Futures:

Positioning Notes:

Positioning Notes:

- CORN large speculator standing this week came in at a net position of 433,384 contracts in the data reported through Tuesday.

- Weekly Speculator position boost of 92,644 contracts from the previous week which had a total of 340,740 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 95.2 percent.

- The Commercials are Bearish-Extreme with a score of 1.3 percent.

- The Small Traders (not shown in chart) are Bearish with a score of 31.4 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| CORN Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 31.5 | 39.4 | 7.0 |

| – Percent of Open Interest Shorts: | 8.8 | 58.7 | 10.4 |

| – Net Position: | 433,384 | -368,848 | -64,536 |

| – Gross Longs: | 601,877 | 752,467 | 133,696 |

| – Gross Shorts: | 168,493 | 1,121,315 | 198,232 |

| – Long to Short Ratio: | 3.6 to 1 | 0.7 to 1 | 0.7 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 95.2 | 1.3 | 31.4 |

| – Strength Index Reading (3 Year Range): | Bullish-Extreme | Bearish-Extreme | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 7.9 | -8.3 | -4.0 |

SUGAR Futures:

Positioning Notes:

Positioning Notes:

- SUGAR large speculator standing this week came in at a net position of -95,519 contracts in the data reported through Tuesday.

- Weekly Speculator position rise of 48,432 contracts from the previous week which had a total of -143,951 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 30.0 percent.

- The Commercials are Bullish with a score of 69.3 percent.

- The Small Traders (not shown in chart) are Bearish with a score of 45.3 percent.

Price Trend-Following Model: Weak Downtrend

Our weekly trend-following model classifies the current market price position as: Weak Downtrend.

| SUGAR Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 25.5 | 49.7 | 8.8 |

| – Percent of Open Interest Shorts: | 35.3 | 40.9 | 7.7 |

| – Net Position: | -95,519 | 84,974 | 10,545 |

| – Gross Longs: | 247,159 | 481,686 | 85,327 |

| – Gross Shorts: | 342,678 | 396,712 | 74,782 |

| – Long to Short Ratio: | 0.7 to 1 | 1.2 to 1 | 1.1 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 30.0 | 69.3 | 45.3 |

| – Strength Index Reading (3 Year Range): | Bearish | Bullish | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 0.1 | 1.5 | -11.1 |

COFFEE Futures:

Positioning Notes:

Positioning Notes:

- COFFEE large speculator standing this week came in at a net position of 27,625 contracts in the data reported through Tuesday.

- Weekly Speculator position boost of 2,599 contracts from the previous week which had a total of 25,026 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 50.9 percent.

- The Commercials are Bullish with a score of 51.0 percent.

- The Small Traders (not shown in chart) are Bearish with a score of 22.9 percent.

Price Trend-Following Model: Downtrend

Our weekly trend-following model classifies the current market price position as: Downtrend.

| COFFEE Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 31.6 | 35.4 | 4.5 |

| – Percent of Open Interest Shorts: | 15.9 | 51.3 | 4.3 |

| – Net Position: | 27,625 | -28,056 | 431 |

| – Gross Longs: | 55,703 | 62,259 | 7,936 |

| – Gross Shorts: | 28,078 | 90,315 | 7,505 |

| – Long to Short Ratio: | 2.0 to 1 | 0.7 to 1 | 1.1 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 50.9 | 51.0 | 22.9 |

| – Strength Index Reading (3 Year Range): | Bullish | Bullish | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 2.2 | -1.7 | -7.9 |

SOYBEANS Futures:

Positioning Notes:

Positioning Notes:

- SOYBEANS large speculator standing this week came in at a net position of 232,198 contracts in the data reported through Tuesday.

- Weekly Speculator position rise of 38,259 contracts from the previous week which had a total of 193,939 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 95.1 percent.

- The Commercials are Bearish-Extreme with a score of 5.8 percent.

- The Small Traders (not shown in chart) are Bearish with a score of 25.5 percent.

Price Trend-Following Model: Uptrend

Our weekly trend-following model classifies the current market price position as: Uptrend.

| SOYBEANS Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 31.2 | 43.4 | 5.5 |

| – Percent of Open Interest Shorts: | 7.3 | 64.4 | 8.3 |

| – Net Position: | 232,198 | -204,545 | -27,653 |

| – Gross Longs: | 303,880 | 423,322 | 53,507 |

| – Gross Shorts: | 71,682 | 627,867 | 81,160 |

| – Long to Short Ratio: | 4.2 to 1 | 0.7 to 1 | 0.7 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 95.1 | 5.8 | 25.5 |

| – Strength Index Reading (3 Year Range): | Bullish-Extreme | Bearish-Extreme | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 3.8 | -5.1 | 17.2 |

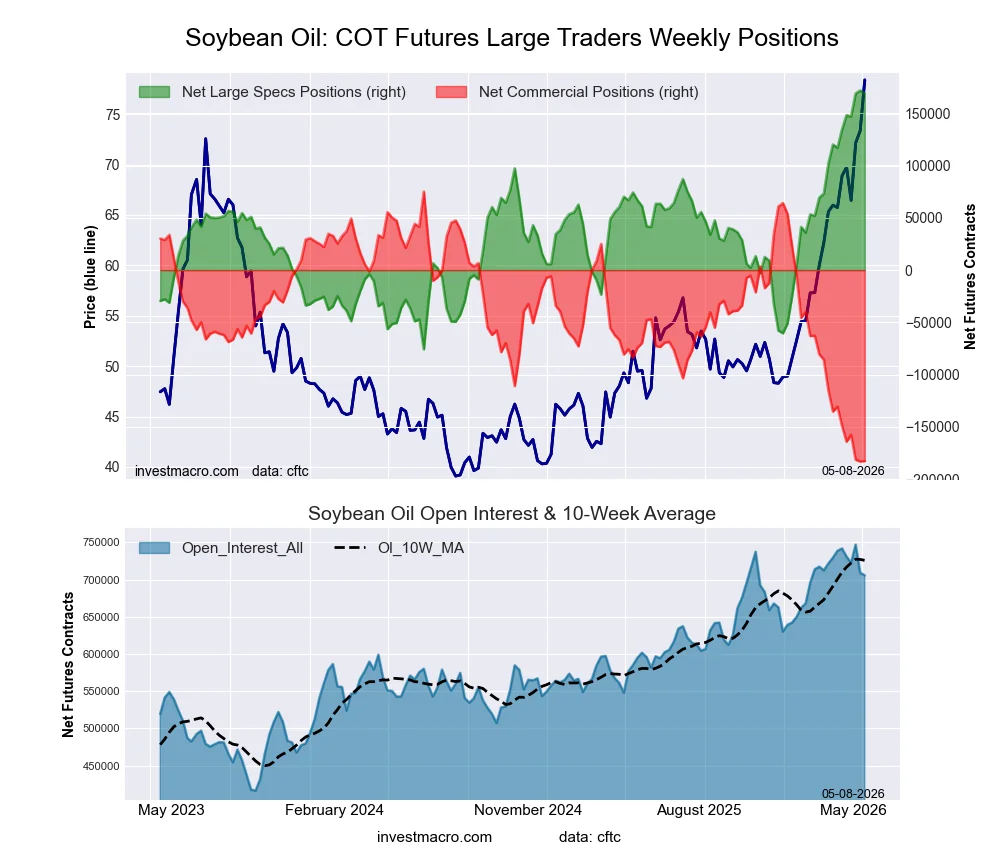

SOYBEAN OIL Futures:

Positioning Notes:

Positioning Notes:

- SOYBEAN OIL large speculator standing this week came in at a net position of 168,887 contracts in the data reported through Tuesday.

- Weekly Speculator position fall of -2,925 contracts from the previous week which had a total of 171,812 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 98.8 percent.

- The Commercials are Bearish-Extreme with a score of 0.2 percent.

- The Small Traders (not shown in chart) are Bullish-Extreme with a score of 87.1 percent.

Price Trend-Following Model: Uptrend

Our weekly trend-following model classifies the current market price position as: Uptrend.

| SOYBEAN OIL Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 31.3 | 40.9 | 5.8 |

| – Percent of Open Interest Shorts: | 7.4 | 66.8 | 3.9 |

| – Net Position: | 168,887 | -182,706 | 13,819 |

| – Gross Longs: | 220,821 | 288,809 | 41,182 |

| – Gross Shorts: | 51,934 | 471,515 | 27,363 |

| – Long to Short Ratio: | 4.3 to 1 | 0.6 to 1 | 1.5 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 98.8 | 0.2 | 87.1 |

| – Strength Index Reading (3 Year Range): | Bullish-Extreme | Bearish-Extreme | Bullish-Extreme |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 20.9 | -20.2 | 2.0 |

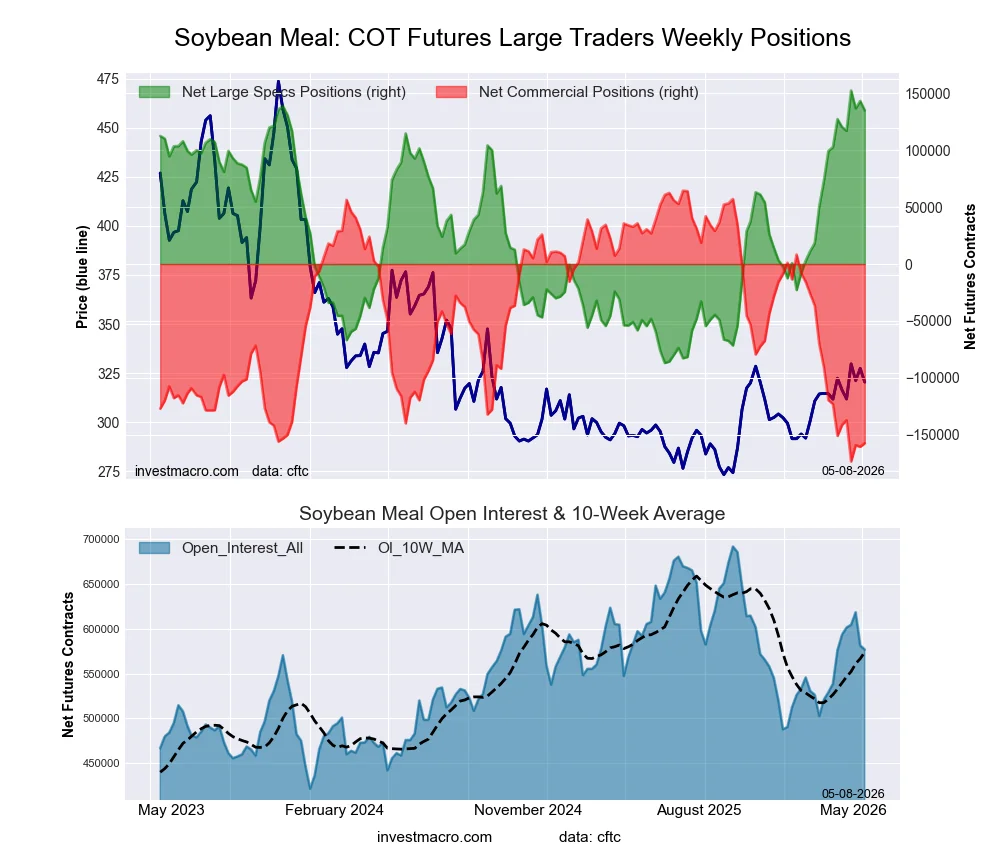

SOYBEAN MEAL Futures:

Positioning Notes:

Positioning Notes:

- SOYBEAN MEAL large speculator standing this week came in at a net position of 134,714 contracts in the data reported through Tuesday.

- Weekly Speculator position lowering of -8,387 contracts from the previous week which had a total of 143,101 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 92.7 percent.

- The Commercials are Bearish-Extreme with a score of 6.7 percent.

- The Small Traders (not shown in chart) are Bullish with a score of 70.2 percent.

Price Trend-Following Model: Uptrend

Our weekly trend-following model classifies the current market price position as: Uptrend.

| SOYBEAN MEAL Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 33.0 | 41.6 | 8.4 |

| – Percent of Open Interest Shorts: | 9.7 | 68.9 | 4.5 |

| – Net Position: | 134,714 | -157,289 | 22,575 |

| – Gross Longs: | 190,466 | 239,910 | 48,705 |

| – Gross Shorts: | 55,752 | 397,199 | 26,130 |

| – Long to Short Ratio: | 3.4 to 1 | 0.6 to 1 | 1.9 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 92.7 | 6.7 | 70.2 |

| – Strength Index Reading (3 Year Range): | Bullish-Extreme | Bearish-Extreme | Bullish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 3.2 | -2.7 | -6.1 |

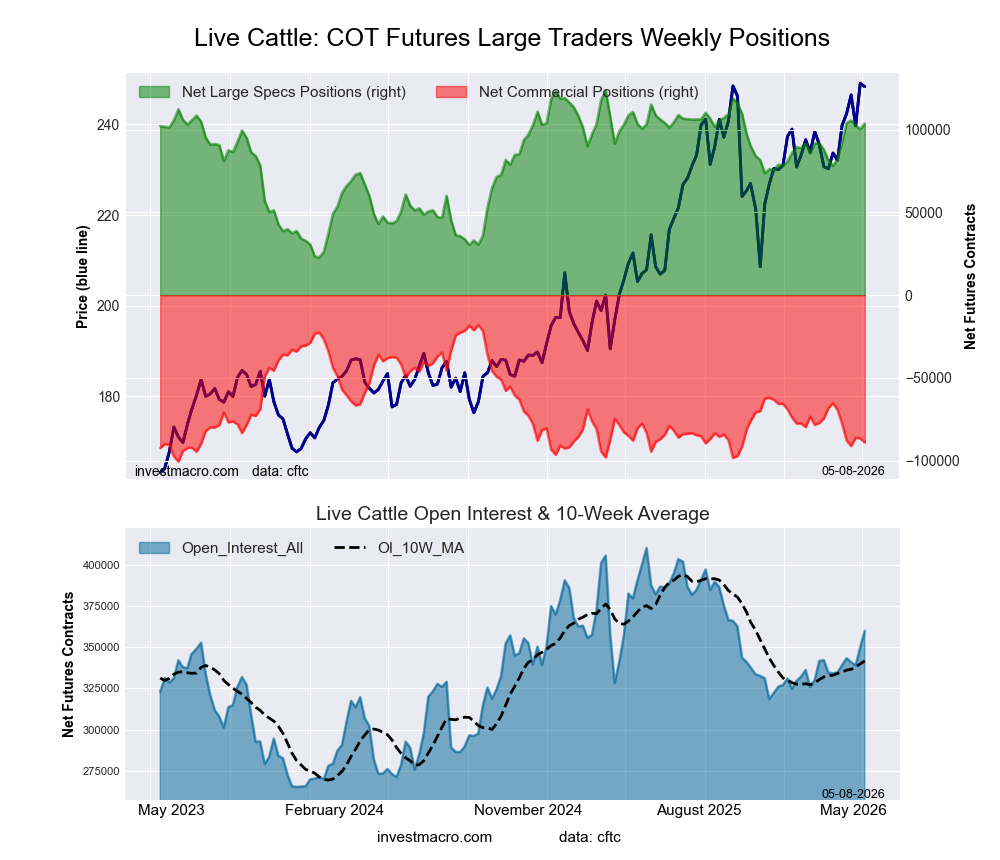

LIVE CATTLE Futures:

Positioning Notes:

Positioning Notes:

- LIVE CATTLE large speculator standing this week came in at a net position of 103,719 contracts in the data reported through Tuesday.

- Weekly Speculator position gain of 3,381 contracts from the previous week which had a total of 100,338 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 80.2 percent.

- The Commercials are Bearish-Extreme with a score of 13.9 percent.

- The Small Traders (not shown in chart) are Bearish with a score of 46.7 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| LIVE CATTLE Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 45.9 | 28.0 | 7.6 |

| – Percent of Open Interest Shorts: | 17.1 | 52.7 | 11.7 |

| – Net Position: | 103,719 | -89,036 | -14,683 |

| – Gross Longs: | 165,391 | 100,646 | 27,527 |

| – Gross Shorts: | 61,672 | 189,682 | 42,210 |

| – Long to Short Ratio: | 2.7 to 1 | 0.5 to 1 | 0.7 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 80.2 | 13.9 | 46.7 |

| – Strength Index Reading (3 Year Range): | Bullish-Extreme | Bearish-Extreme | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 21.4 | -24.0 | -6.1 |

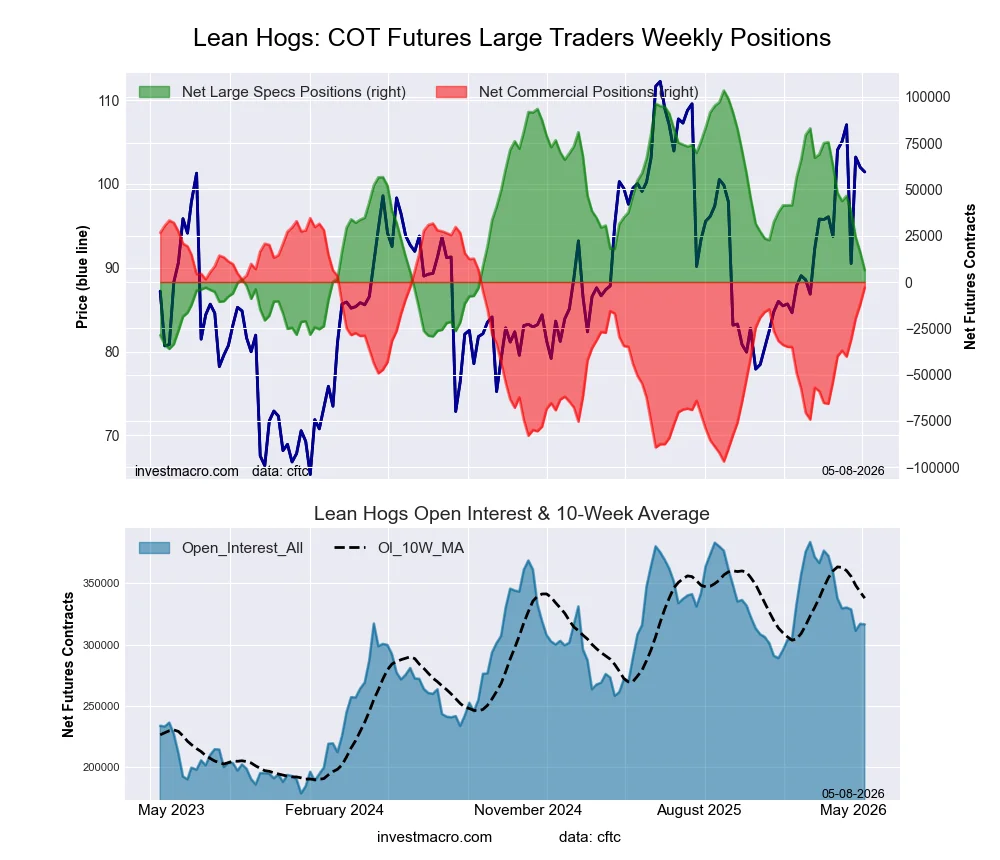

LEAN HOGS Futures:

Positioning Notes:

Positioning Notes:

- LEAN HOGS large speculator standing this week came in at a net position of 6,451 contracts in the data reported through Tuesday.

- Weekly Speculator position fall of -9,721 contracts from the previous week which had a total of 16,172 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 30.5 percent.

- The Commercials are Bullish with a score of 71.6 percent.

- The Small Traders (not shown in chart) are Bullish with a score of 57.0 percent.

Price Trend-Following Model: Uptrend

Our weekly trend-following model classifies the current market price position as: Uptrend.

| LEAN HOGS Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 28.1 | 39.2 | 7.3 |

| – Percent of Open Interest Shorts: | 26.1 | 40.2 | 8.4 |

| – Net Position: | 6,451 | -2,889 | -3,562 |

| – Gross Longs: | 89,062 | 124,191 | 22,980 |

| – Gross Shorts: | 82,611 | 127,080 | 26,542 |

| – Long to Short Ratio: | 1.1 to 1 | 1.0 to 1 | 0.9 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 30.5 | 71.6 | 57.0 |

| – Strength Index Reading (3 Year Range): | Bearish | Bullish | Bullish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -29.9 | 28.4 | 27.3 |

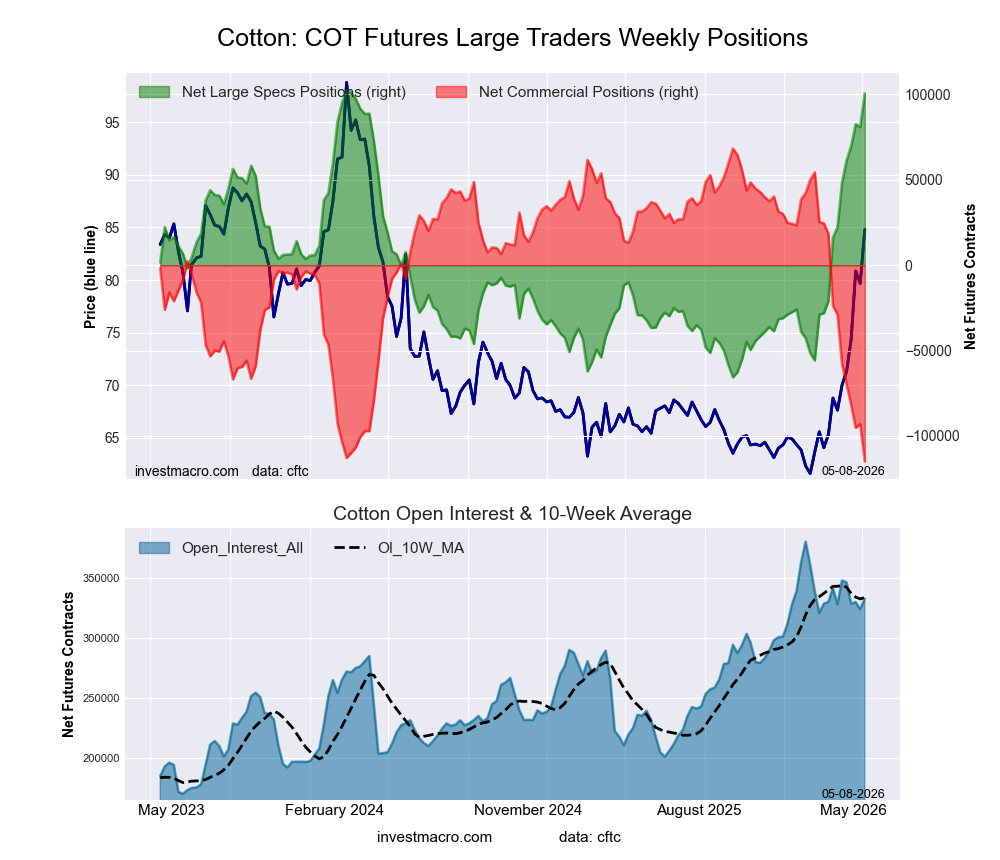

COTTON Futures:

Positioning Notes:

Positioning Notes:

- COTTON large speculator standing this week came in at a net position of 100,682 contracts in the data reported through Tuesday.

- Weekly Speculator position rise of 19,741 contracts from the previous week which had a total of 80,941 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 99.0 percent.

- The Commercials are Bearish-Extreme with a score of 0.0 percent.

- The Small Traders (not shown in chart) are Bullish-Extreme with a score of 100.0 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| COTTON Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 43.3 | 30.3 | 6.8 |

| – Percent of Open Interest Shorts: | 13.0 | 64.9 | 2.5 |

| – Net Position: | 100,682 | -114,931 | 14,249 |

| – Gross Longs: | 144,088 | 100,805 | 22,683 |

| – Gross Shorts: | 43,406 | 215,736 | 8,434 |

| – Long to Short Ratio: | 3.3 to 1 | 0.5 to 1 | 2.7 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 99.0 | 0.0 | 100.0 |

| – Strength Index Reading (3 Year Range): | Bullish-Extreme | Bearish-Extreme | Bullish-Extreme |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 46.7 | -46.9 | 43.6 |

COCOA Futures:

Positioning Notes:

Positioning Notes:

- COCOA large speculator standing this week came in at a net position of -20,234 contracts in the data reported through Tuesday.

- Weekly Speculator position boost of 3,409 contracts from the previous week which had a total of -23,643 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 3.0 percent.

- The Commercials are Bullish-Extreme with a score of 96.5 percent.

- The Small Traders (not shown in chart) are Bearish with a score of 46.3 percent.

Price Trend-Following Model: Weak Downtrend

Our weekly trend-following model classifies the current market price position as: Weak Downtrend.

| COCOA Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 23.2 | 51.2 | 5.7 |

| – Percent of Open Interest Shorts: | 33.3 | 42.1 | 4.7 |

| – Net Position: | -20,234 | 18,225 | 2,009 |

| – Gross Longs: | 46,562 | 102,506 | 11,501 |

| – Gross Shorts: | 66,796 | 84,281 | 9,492 |

| – Long to Short Ratio: | 0.7 to 1 | 1.2 to 1 | 1.2 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 3.0 | 96.5 | 46.3 |

| – Strength Index Reading (3 Year Range): | Bearish-Extreme | Bullish-Extreme | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -0.1 | -1.4 | 16.3 |

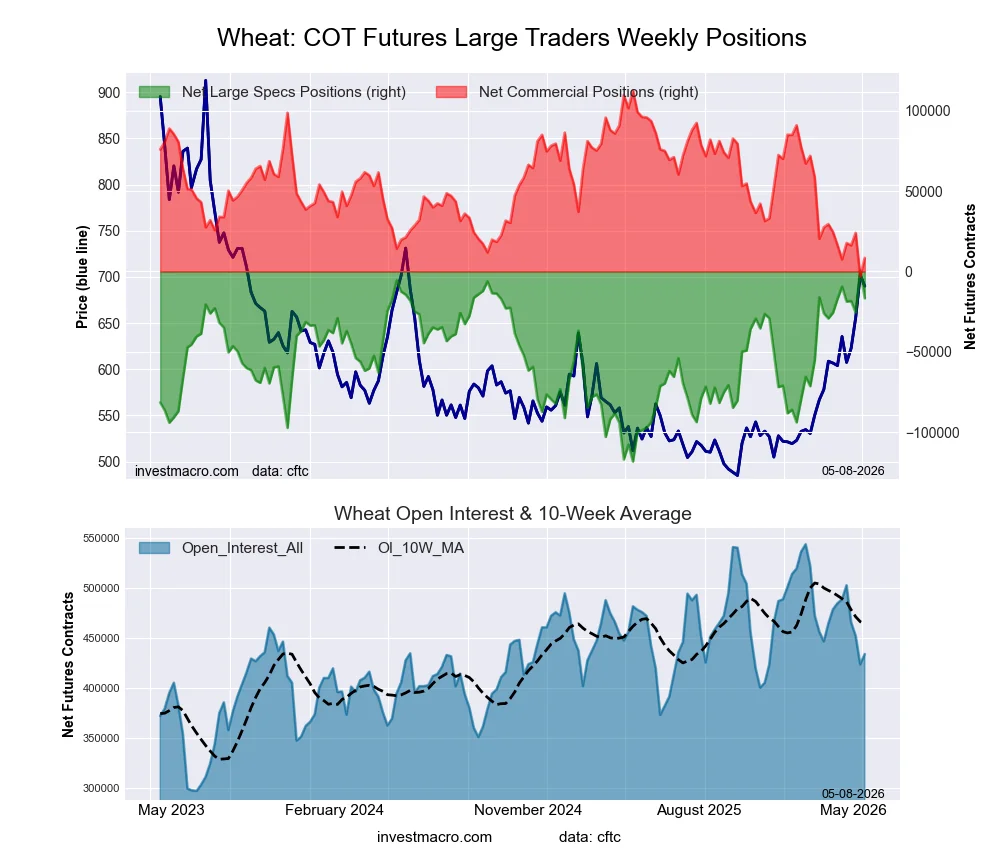

WHEAT Futures:

Positioning Notes:

Positioning Notes:

- WHEAT large speculator standing this week came in at a net position of -16,668 contracts in the data reported through Tuesday.

- Weekly Speculator position decrease of -17,534 contracts from the previous week which had a total of 866 net contracts.

- This week’s current strength score (range over the past 3 years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 85.3 percent.

- The Commercials are Bearish-Extreme with a score of 9.9 percent.

- The Small Traders (not shown in chart) are Bullish-Extreme with a score of 100.0 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| WHEAT Futures Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 29.7 | 31.6 | 8.7 |

| – Percent of Open Interest Shorts: | 33.5 | 29.7 | 6.8 |

| – Net Position: | -16,668 | 8,425 | 8,243 |

| – Gross Longs: | 128,830 | 137,098 | 37,730 |

| – Gross Shorts: | 145,498 | 128,673 | 29,487 |

| – Long to Short Ratio: | 0.9 to 1 | 1.1 to 1 | 1.3 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 85.3 | 9.9 | 100.0 |

| – Strength Index Reading (3 Year Range): | Bullish-Extreme | Bearish-Extreme | Bullish-Extreme |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 0.4 | -6.9 | 43.0 |

Article By InvestMacro – Receive our weekly COT Newsletter

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators) as well as their open interest (contracts open in the market at time of reporting). See CFTC criteria here.