GBPUSD is trading at 1.3333; the instrument is moving above Ichimoku Cloud, thus indicating an ascending tendency. The markets could indicate that the price may test Tenkan-Sen and Kijun-Sen at 1.3275 and then resume moving upwards to reach 1.3495. Another signal in favour of a further uptrend will be a rebound from the support level. However, the bullish scenario may no longer be valid if the price breaks the cloud’s downside border and fixes below 1.3180. In this case, the pair may continue falling towards 1.3095.

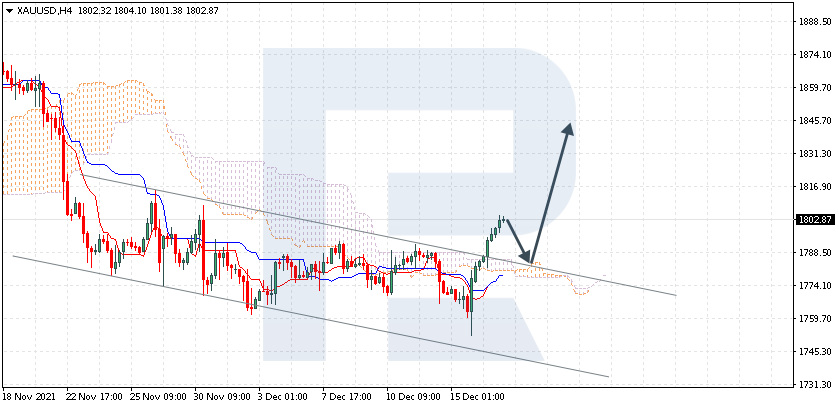

XAUUSD, “Gold vs US Dollar”

XAUUSD is trading at 1802.00; the instrument is moving above Ichimoku Cloud, thus indicating an ascending tendency. The markets could indicate that the price may test the cloud’s upside border at 1785.00 and then resume moving upwards to reach 1845.00. Another signal in favour of a further uptrend will be a rebound from the descending channel’s upside border. However, the bullish scenario may no longer be valid if the price breaks the cloud’s downside border and fixes below 1770.00. In this case, the pair may continue falling towards 1745.00.

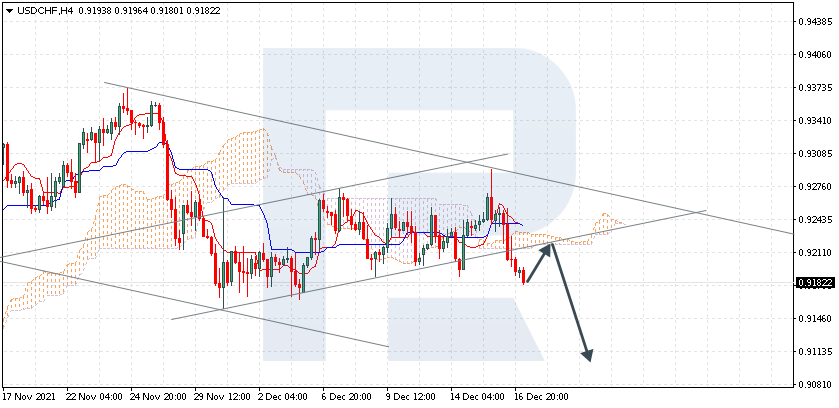

USDCHF, “US Dollar vs Swiss Franc”

USDCHF is trading at 0.9182; the instrument is moving below Ichimoku Cloud, thus indicating a descending tendency. The markets could indicate that the price may test the cloud’s downside border at 0.9210 and then resume moving downwards to reach 0.9105. Another signal in favour of a further downtrend will be a rebound from the rising channel’s downside border. However, the bearish scenario may no longer be valid if the price breaks the cloud’s upside border and fixes above 0.9255. In this case, the pair may continue growing towards 0.9345.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

As we can see in the H4 chart, after forming several reversal patterns, including Inverted Hammer, close to the support level, USDCAD may reverse in the form of another rising wave. In this case, the upside target may be the resistance area at 1.2900. However, an alternative scenario implies that the asset may correct to reach 1.2740 first and then resume trading upwards.

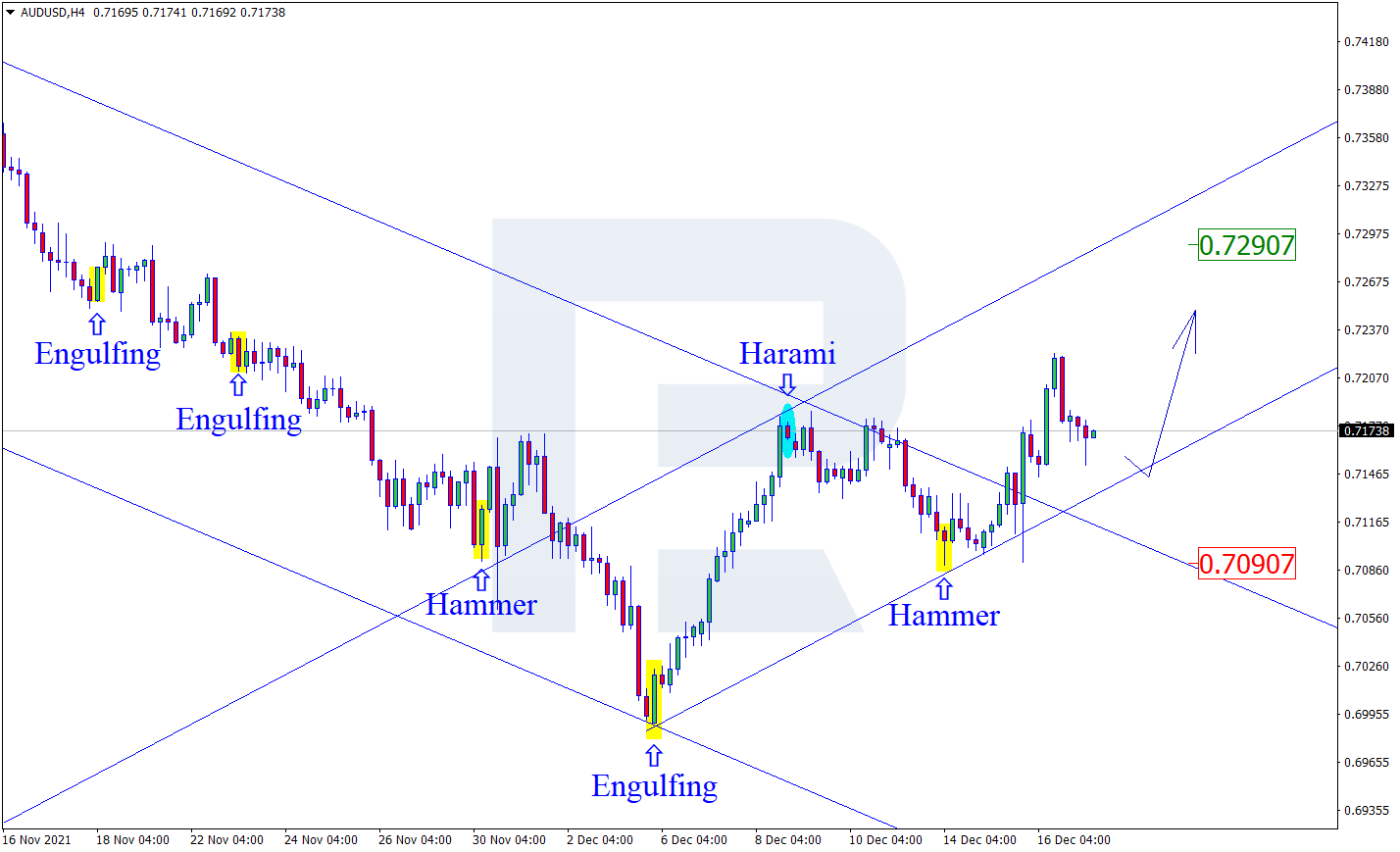

AUDUSD, “Australian Dollar vs US Dollar”

As we can see in the H4 chart, AUDUSD has formed a Hammer reversal pattern near the support area. At the moment, the asset is reversing in the form of another rising impulse. In this case, the upside target may be the resistance level at 0.7290. At the same time, an opposite scenario implies that the price may continue falling to reach 0.7090 before resuming its ascending tendency.

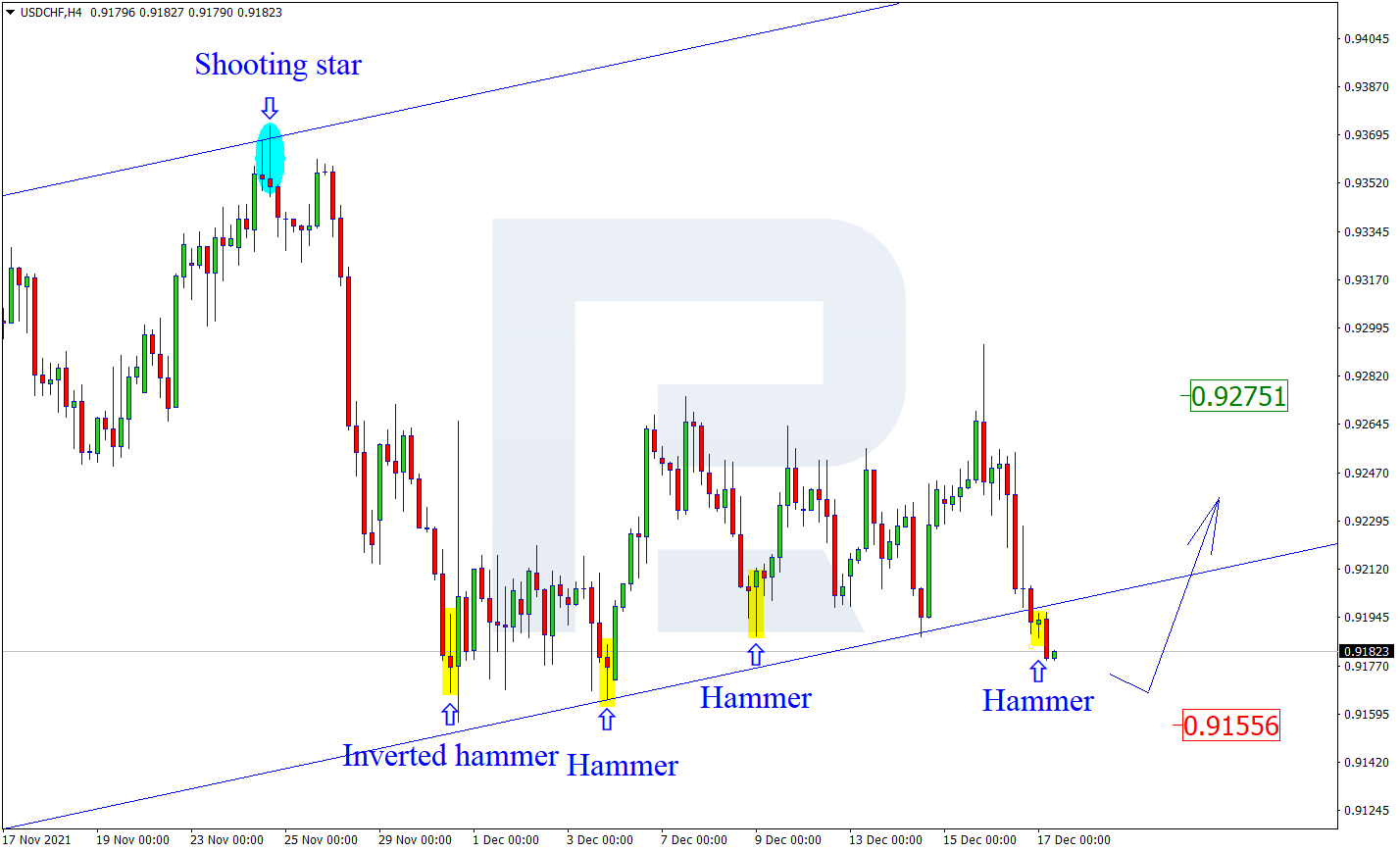

USDCHF, “US Dollar vs Swiss Franc”

As we can see in the H4 chart, after testing the support area, the pair has formed several reversal patterns, for example, Hammer. At the moment, USDCHF may reverse in the form of a new rising wave towards the resistance level. In this case, the upside target may be at 0.9275. Still, there might be an alternative scenario, according to which the asset may continue falling to reach 0.9155 before resuming its growth.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

The ECB expectedly kept the base interest rate at zero level, while the deposit rate was left at minus 0.5%. The ECB will end its PEPP program in March 2022. The ECB can also extend PEPP reinvestment until at least the end of 2024. With a high probability, investors should not expect the ECB to raise interest rates in 2022. Eurozone inflation data will be released today.

From a technical point of view, the EUR/USD on the hour time frame is still bearish. The price is trading in a wide corridor. Yesterday, there was an attempt to break out through the priority change level, but the sellers were stronger. The MACD indicator became positive, and the buyers’ pressure is still strong. Under such market conditions, traders should consider sell positions from the priority change level, but with additional confirmation. Buy trades can be considered after a true breakout of the priority change level.

Alternative scenario: if the price breaks out through the 1.1360 resistance level and fixes above, the mid-term uptrend will likely resume.

News feed for 2021.12.17:

– Germany IFO Business Climate Index (m/m) at 11:00 (GMT+2);

– Eurozone Consumer Price Index (m/m) at 12:00 (GMT+2);

– US FOMC Member Wallers’ speech at 20:00 (GMT+2).

The GBP/USD currency pair

Technical indicators of the currency pair:

Prev Open: 1.3256

Prev Close: 1.3324

% chg. over the last day: +0.52%

The Bank of England unexpectedly raised its key interest rate to 0.25% from 0.1%. At the same time, the central bank left the volume of the government bond-buying program at 875 billion pounds. According to the Bank of England forecasts, inflation may reach 6% in the coming months.

On the hourly time frame, the trend on GBP/USD has changed to bullish. An interest rate hike from the central bank played a key role. The price broke through the priority change level and closed higher. The MACD indicator became positive. Under such market conditions, traders should consider buy positions from the support levels near the moving average. Sell trades can be considered from the resistance levels of the higher time frame, but only with additional confirmation; as an option – to sell after a false breakout of the 1.3365 level.

Alternative scenario: if the price breaks down through the 1.3189 support level and consolidates below, the bearish scenario will likely resume.

News feed for 2021.12.17:

– UK Retail Sales (m/m) at 09:00 (GMT+2).

The USD/JPY currency pair

Technical indicators of the currency pair:

Prev Open: 113.98

Prev Close: 113.69

% chg. over the last day: -0.26%

The Bank of Japan has made no changes to its ultra-soft monetary policy as it monitors the impact of the new variant of the Omicron coronavirus. At the same time, the Bank of Japan decided to cut its funding support program from the effects of COVID-19 as financing conditions for large companies improved. The interest rate remained unchanged.

Trading recommendations

Support levels: 113.30, 112.62, 112.30

Resistance levels: 113.95, 114.17, 115.15, 115.50

The global trend on the USD/JPY currency pair is bearish. Yesterday, the price tried to break out through the priority change level, but the sellers managed to protect the level. Today, on the news from the Bank of Japan, the yen strengthened against the dollar, as the Bank of Japan began to take the first steps to tighten its policy. Under such market conditions, traders can look for sell positions from the 113.95 resistance level but with additional confirmation. Buy positions should be considered from the 113.30 support level, but with additional confirmation in the form of a buyers’ initiative or after the price breakout the priority change level.

Alternative scenario: if the price rises above 114.17, the uptrend will likely resume.

News feed for 2021.12.17:

– Japan BoJ Interest Rate Decision at 04:30 (GMT+2);

– Japan BoJ Monetary Policy Statement at 04:30 (GMT+2).

The USD/CAD currency pair

Technical indicators of the currency pair:

Prev Open: 1.2831

Prev Close: 1.2774

% chg. over the last day: -0.44%

The USD/CAD quotes are declining again amid rising oil prices and a decline in the dollar index. The Canadian dollar is a commodity currency, so it is highly correlated with these instruments. The tightening of the monetary policy from the US Federal Reserve will stimulate the dollar index to grow, while oil prices will depend on the demand for fuel.

Trading recommendations

Support levels: 1.2721, 1.2677, 1.2638

Resistance levels: 1.2828, 1.2891, 1.2951

From a technical point of view, the USD/CAD currency pair trend is bullish. The MACD became negative; the price corrected the dynamic moving average level. Under such market conditions, it is better to look for buy deals from the support levels near the moving average on the lower time frames. It is best to look for sell deals from the false breakout area, but with additional confirmation.

Alternative scenario: if the price breaks down through the 1.2721 support level and fixes below, the downtrend will likely resume.

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

The US stock indices ended Thursday’s trading in the red zone. The technology sector saw a strong sell-off, which negatively affected the entire market. The S&P 500 (US500) decreased by 0.9%, the Dow Jones (US30) decreased by 0.1%, and the Nasdaq (US100) lost 2.5%. Meanwhile, the financial sector was the best performing, as investors believe that US Treasury yields will rise in the coming months after the Fed meeting.

European stock indices, on the other hand, looked green yesterday. French CAC 40 (FR40) gained 1.12%, German DAX (DE30) added 1.03%, Spanish IBEX (ES35) increased by 1.27%, while British FTSE 100 jumped by 1.25%. The Bank of England unexpectedly raised its key rate to 0.25% from 0.1%. At the same time, the central bank left the volume of the government bond-buying program at the level of 875 billion pounds.

The main theses from the head of the Bank of England Andrew Bailey:

inflation could reach 6% in the coming months;

inflation is also on the rise due to tensions with Russia;

Omicron will undoubtedly have a significant impact on economic activity;

the labor market is currently very tight.

On Thursday, the European Central Bank raised its inflation forecasts and lowered expectations for economic growth in 2022 because of the impact of the coronavirus pandemic and supply chain problems. The ECB expectedly kept its prime rate at zero level, while the deposit rate was left at minus 0.5%. The ECB will end its PEPP program in March 2022. The ECB can also extend PEPP reinvestment until at least the end of 2024. With a high probability, investors should not expect the ECB to raise interest rates in 2022. The ECB’s inflation forecasts are 2.6% (revised from 2.2%) for 2021, 3.2% (revised from 1.7%) for 2022, 1.8% (revised from 1.5%) for 2023, and 1.8% for 2024.

On Thursday, the Swiss National Bank (SNB) remained its ultra-soft monetary policy, deviating from the tightening course that a growing number of central banks are following. The SNB said its current policy, which combines the world’s lowest interest rates with intervention in the foreign exchange market, remains appropriate, despite the Swiss franc’s rise to six-and-a-half-year highs. As expected, Norway’s central bank raised its benchmark interest rate on Thursday and predicts more hikes to follow next year.

Germany’s regulator doesn’t expect Nord Stream 2 to start in the 1st half of 2022.

The Turkish lira fell to another record low as Turkey’s central bank cut interest rates from another 100 bps to 14%. The Turkish central bank cut its benchmark rate for the 4th consecutive quarter despite a sharp rise in inflation and the lira falling to record lows. The lira lost 51% against the dollar since the beginning of the year.

The ECB’s oil price forecast: $71.8 per barrel for 2021, $77.5 per barrel for 2022, $72.3 per barrel for 2023, and $69.4 per barrel for 2024. On Thursday, oil prices increased as an indicator of consumer demand for gasoline in the US rising to a record high. Also, the price increase affects a sharp decline in crude oil reserves, which was published on Wednesday.

Stock markets in the Asia-Pacific region ended Thursday trading on the green territory, except for the Australian stock index. Hong Kong’s Hang Seng (HK50) increased by 0.2%, Japan’s Nikkei index (JP225) added 2.1%. Australia’s S&P/ASX 200 (AU200) decreased by 0.4%. Japan has seen a significant increase in exports. It was driven by strong demand from Japanese companies ahead of the holiday season and some easing of supply chain problems.

Stock markets in the Asia-Pacific region ended Thursday trading on the green territory, except for the Australian stock index. Hong Kong’s Hang Seng (HK50) increased by 0.2%, Japan’s Nikkei index (JP225) added 2.1%. Australia’s S&P/ASX 200 (AU200) decreased by 0.4%. Japan has seen a significant increase in exports. It was driven by strong demand from Japanese companies ahead of the holiday season and some easing of supply chain problems.

The Bank of Japan made no changes to its ultra-soft monetary policy as it monitors the impact of a new variant of the Omicron coronavirus. At the same time, the Bank of Japan decided to cut its funding support program due to the effects of COVID-19 as financing conditions for large companies improve. The interest rate remained unchanged.

Main market quotes:

S&P 500 (F) (US500) 4,668.67 −41.18 (−0.87%)

Dow Jones (US30) 35,897.64 −29.79 (−0.083%)

DAX (DE40) 15,636.40 +160.05 (+1.03%)

FTSE 100 (UK100) 7,260.61 +89.86 (+1.25%)

USD Index 95.98 −0.53 (−0.55%)

Important events for today:

– Japan BoJ Interest Rate Decision at 04:30 (GMT+2);

– Japan BoJ Monetary Policy Statement at 04:30 (GMT+2);

– UK Retail Sales (m/m) at 09:00 (GMT+2);

– Germany IFO Business Climate Index (m/m) at 11:00 (GMT+2);

– Eurozone Consumer Price Index (m/m) at 12:00 (GMT+2);

– US FOMC Member Wallers’ speech at 20:00 (GMT+2).

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

It’s been a veritable feast of central bank meetings (in case you were on a different planet) over the last few days. Markets are desperately trying to digest all the new forecasts, projections, dot plots and statements before the holiday season kicks in for good.

The latest meetings have seen all the main policymakers who control the monetary policy mechanisms dial in the emergency measures enacted over 18 months ago.

This has primarily been due to inflation being the biggest threat to the economic outlook.

Central banks in Europe have followed the Fed’s lead and pivoted – at varying speeds – toward tighter policy to fight rising price pressures not seen in many years.

In turn, central banks are looking through the uncertainty brought about by the Omicron variant. In effect, they are saying the coronavirus is no longer calling the shots in their economies, even if more social restrictions may cause more protracted issues with supply bottlenecks and shortages. Indeed, Goldman Sachs said overnight Omicron hasn’t had much of an impact on mobility and oil demand so far.

BoE first G7 bank to hike

Upside surprises to inflation convinced the BoE to tighten pre-emptively yesterday, despite mounting Omicron uncertainty. CPI is expected to peak at 6% in April next year, up from 5% previously.

The labour market is the bank’s main worry as it is continuing to tighten. Perhaps the biggest surprise on the day was how many MPC members voted for a hike, after the disappointment of not raising rates at its last meeting.

The key question now is the path of the rate hike cycle and the timing of the next move. Not forgetting the impact of Omicron which as the MPC say, is unclear at this stage.

Cable had shown signs of stabilising around 1.32 before the meeting with a base forming. A “rounding bottom” is often found at the end of extended downward trends and signifies a reversal in the long-term trend. Wednesday had a bullish outside reversal day and prices pushed up above 1.33 after the BoE. Major resistance is 1.3411 and 1.3571/79.

Markets cautious into the weekend

For risk markets, the rally immediately after the Fed meeting has reversed abruptly, with growth stocks hit particularly hard. The tech-laden Nasdaq closed lower by 2.47% while the more defensive Dow tipped into the red even as banks rallied. Asian markets are being sold and US futures point to more losses to end the week.

It’s probably no surprise if we see more selling as traders take risk positions off with the unknown of Omicron lingering.

Safe haven currencies are outperforming this morning with CHF and JPY all showing strength.

Gold bugs welcomed the move lower in the dollar and the precious metal has moved above $1800 for the first time in over two weeks. Both the 50-day and 200-day simple moving average should offer support around $1789. The first upside target and resistance comes in at $1830.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Turkey’s central bank lowered its main interest rate for the fourth month in a row but said it would now pause while it monitors the impact of recent policy decisions during the first quarter of next year when it will consider all aspects of its policy framework “to create a foundation for a sustainable price stability.” The Central Bank of the Republic of Turkey (CBRT) cut its policy rate, the one-week repurchase auction rate, by another 100 basis points to 14.0 percent and has now cut it 5 percentage points following cuts starting in September though today. The easing of monetary policy – which began after the current governor Sahap Kavcioglu was installed in March by Turkish President Tayyip Erdogan – reversed a monetary tightening cycle that was begun under the previous governor to curb rising inflationary pressures.

“The Committee decided to complete the use of the limited room implied by transitory effects of supply-side factors and other factors beyond monetary policy’s control on price increases and reduced the policy rate by 100 basis points,” the bank’s monetary policy committee said.

Today’s rate cut was expected after CBRT in November said it would consider completing the use of the limited room to lower interest rates in light of the transitory impact on inflation and Erdogan’s repeated call for lower interest rates as part of what he says is the country’s “economic war of independence.”

In November the central bank also said it expected the transitory effects on inflation to persist through the first half of 2022 but omitted this reference today.

However, CBRT reiterated it would “decisively” use all available instruments until data points to a permanent fall in inflation and the 5.0 percent inflation target is achieved.

Turkey’s inflation rate rose to 21.3 percent in November form 19.9 percent in October and 15 percent in January this year.

The Central Bank of the Republic of Turkey issued the following press release:

“Participating Committee Members

Şahap Kavcıoğlu (Governor), Taha Çakmak, Mustafa Duman, Elif Haykır Hobikoğlu, Emrah Şener, Yusuf Tuna.

The Monetary Policy Committee (MPC) has decided to reduce the policy rate (one-week repo auction rate) from 15 percent to 14 percent.

The reintroduction of travel restrictions and lockdowns due to the new variants keeps the downside risks to global economic activity alive and raises the uncertainty. Recovery in global demand, high course of commodity prices, supply constraints in some sectors and rise in transportation costs have led to producer and consumer price increases internationally. While the effects of high global inflation on inflation expectations and international financial markets are closely monitored, central banks in advanced economies assess that the rise in inflation on the back of rising energy prices and imbalances between supply and demand may last longer than previously anticipated. Accordingly, while monetary policy communication of central banks in advanced economies varies with their diverse outlook for economic activity, labor market and inflation expectations, they continue their supportive monetary stances and asset purchase programs.

National income data and leading indicators show that domestic economic activity remains strong, with the help of robust external demand. The spread of domestic vaccination throughout the society facilitates the recovery in services, tourism and related sectors, which have been adversely affected by the pandemic, and leads to a more balanced composition in economic activity. Current account balance is expected to post a surplus in 2022 due to the strengthening of the upward trend in exports. Strengthening of the improvement trend in current account balance is important for price stability objective, and in that respect, developments in commercial and consumer loans are closely monitored.

Increase in inflation in November has been driven by developments in exchange rates and supply side factors such as the rise in global food and agricultural commodity prices, supply constraints, and demand developments. The Committee decided to complete the use of the limited room implied by transitory effects of supply-side factors and other factors beyond monetary policy’s control on price increases and reduced the policy rate by 100 basis points. Cumulative impact of the recent policy decisions will be monitored in the first quarter of 2022 and during this period, all aspects of the policy framework will be reassessed in order to create a foundation for a sustainable price stability.

The CBRT will continue to use decisively all available instruments until strong indicators point to a permanent fall in inflation and the medium-term 5 percent target is achieved in pursuit of the primary objective of price stability. Stability in the general price level will foster macroeconomic stability and financial stability through the fall in country risk premium, continuation of the reversal in currency substitution and the upward trend in foreign exchange reserves, and durable decline in financing costs. This would create a viable foundation for investment, production and employment to continue growing in a healthy and sustainable way.

The Committee will continue to take its decisions in a transparent, predictable and data-driven framework.

The summary of the Monetary Policy Committee Meeting will be released within five working days.”

Norway’s central bank lived up to its guidance and raised its benchmark interest rate for the second time this year and said it would most likely raise the rate again in March next year as it continues to unwind the expansionary monetary policy and move the rate back to a more normal level. However, Norges Bank’s monetary policy and financial stability committee also said there was “considerable uncertainty about the evolution of the pandemic and its effects on the economy” and if there is a need for more stringent and protracted containment measures the lower economic activity, further rate hikes may be postponed. On the other hand, if there are signs of persistently high inflation from higher-than-expected domestic wages and prices from capacity constraints and global price pressures, NB said “the policy rate may be raised more quickly.” NBs’ policy committee unanimously raised the policy rate by 25 basis points to 0.50 percent and has now raised it half a percentage point this year following a rate hike in September, the bank’s first rate hike since September 2019, and today. In addition to the rate hike, NB also raised banks’ countercyclical capital buffer by 1 percentage point to 2.0 percent as of Dec. 31, 2022, saying the profitability of banks is solid, credit losses are low, and businesses and households have ample access to credit. “Based on the Committee’s current assessment of economic developments and the prospects for bank losses and lending capacity, the buffer rate will be raised to 2.5 percent in the first half of 2022, taking effect one year later,” NB’s Governor, Oeystein Olsen said. In response to the outbreak of the COVID-19 pandemic early last year, NB cut its rate three times and by a total of 1.50 percentage points to 0.0 percent, and also slashed the countercyclical capital buffer by 1.5 percentage points to 1.0 percent to counter any tightening of banks’ lending standards, which would amplify an economic downturn.

Norges Bank released the following statements about its monetary policy decision and the countercyclical capital buffer:

“Policy rate raised to 0.5 percent

Norges Bank’s Monetary Policy and Financial Stability Committee has unanimously decided to raise the policy rate from 0.25 percent to 0.5 percent.

The upswing in the Norwegian economy has continued. Unemployment has fallen further, and capacity utilisation is estimated to be above a normal level. In recent weeks, the number of new cases and Covid-related hospitalisations have reached a new peak since the onset of the pandemic. Increased infection rates and extensive containment measures are expected to dampen activity in the near term. When infection rates subside further out and containment measures are eased, the economic upswing will likely continue. Higher electricity prices have resulted in elevated CPI inflation, but underlying inflation is lower than the inflation target. Rising wage growth and higher imported goods inflation is expected to push up underlying inflation ahead.

Monetary policy is expansionary. In the Committee’s assessment, the objective of stabilising inflation around the target somewhat further out suggests that the policy rate should be raised towards a more normal level. A gradual normalisation of the policy rate is consistent with continued high employment. Higher interest rates will also help to counter a build-up of financial imbalances.

In its discussion of the balance of risks, the Committee was concerned with the potential economic effects of the pandemic and containment measures in the period ahead. If there is a need for more stringent and protracted containment measures that pull down economic activity through spring next year, further rate hikes may be postponed. The Committee was also concerned with a potentially higher-than-projected rise in domestic wages and prices due to capacity constraints and persistent global price pressures. If there are prospects of persistently high inflation, the policy rate may be raised more quickly.

“There is considerable uncertainty about the evolution of the pandemic and its effects on the economy. But if economic developments evolve broadly in line with the projections, the policy rate will most likely be raised in March”, says Governor Øystein Olsen.

The policy rate forecast is little changed from the September 2021 Monetary Policy Report and indicates a gradual rise in the policy rate in the coming years.”

“The countercyclical capital buffer will be raised to 2.0 percent

Norges Bank’s Monetary Policy and Financial Stability Committee has decided to raise the countercyclical capital buffer rate to 2.0 percent, effective from 31 December 2022.

The objective of the countercyclical capital buffer is to bolster banks’ resilience and to mitigate the amplifying effects of bank lending during downturns. Banks’ loss-absorbing capacity is fundamentally sound, and a higher countercyclical capital buffer rate will contribute to maintaining this capacity.

The upswing in the Norwegian economy has continued. Higher infection rates and extensive containment measures are expected to weigh on activity in the near term. When infection rates subside further out and containment measures are eased, the economic upswing will likely continue.

For Norwegian banks, profitability is solid and credit losses are low. A relatively small share of banks’ exposures is to industries that have been most directly affected by containment measures, limiting banks’ risk of losses. If there is a need for more protracted containment measures that can pull down economic activity, bank losses may rise.

Creditworthy businesses and households appear to have ample access to credit. Norwegian banks are well equipped to meet a higher countercyclical capital buffer rate while maintaining credit supply.

Prior to the reduction in March 2020, the countercyclical capital buffer rate was set at 2.5 percent against the background of a build-up of financial imbalances over a long period. During the pandemic, residential and commercial property prices have increased markedly, and household credit growth has accelerated. Over the past six months, property price inflation has been more moderate. The consideration of financial imbalances suggests a higher buffer rate.

“Based on the Committee’s current assessment of economic developments and the prospects for bank losses and lending capacity, the buffer rate will be raised to 2.5 percent in the first half of 2022, taking effect one year later”, says Governor Øystein Olsen.”

RoboMarkets, a provider of investment services in Europe, announced the reception of the “Best Mobile Trading Platform” award from the Professional Trader Awards. The winners have been determined by the votes of the professional trader community.

The award-winning companies were announced at the ceremonial reception that took place in London on 9 December 2021. RoboMarkets was honoured as the prize winner in the “Best Mobile Trading Platform” category for the second straight year. The award is presented to the broker that is dedicated to offering the best mobile product on the professional account market.

RoboMarkets was recognised for its mobile workstation, R StocksTrader — a powerful and user-friendly application. R StocksTrader is a universal application for trading from smartphones and tablet PCs. The R StocksTrader platform offers over 12,000 instruments for trading, including more than 3,000 stocks, indices, ETFs, and CFDs.

How are the winners of the Professional Trader Awards 2021 selected?

During the first stage, which lasts for four weeks, the organising committee receives applications from brokers that nominate themselves in the different chosen categories. In the next stage, the committee conducts a survey among the trader community, whereby traders with professional trading accounts are asked to vote for a particular broker from the nominees list. This describes how the trader community has selected the winners of the Professional Trader Awards also in 2021.

In 2021, the organising committee presented awards for 17 nominations. The “Professional Trader Awards” are given in recognition of excellence to the brokers that offer exclusive services for professional trading accounts. Among the winners are the providers of financial services that equally prioritise the quality of their services, their cutting-edge technologies, and their clients’ needs and satisfaction.

Denis Golomedov, Chief Marketing Officer at RoboMarkets, says: “It’s a great honour for us to receive the best mobile platform award for the second time in a row. This means that the professional trader community highly appreciates the products for mobile trading offered by RoboMarkets. Our clients want to be able to exercise control over their accounts, and trade around the clock from any part of the world where there is internet access. We understand these needs, and therefore put a lot of effort and ingenuity into continuously developing our proprietary mobile trading solutions. R StocksTrader enables our clients to trade in 6 markets in over 12,000 trading instruments. The innovative app also offers analytical market data, excellent charts, and a handy corporate actions calendar – all made available free of charge (with no monthly fees). The trading features and the information sharing on the app, along with RoboMarkets support, help our clients invest confidently. All the above make R StocksTrader stand out from its market competitors, as evidenced by the choice of professional traders. We thank everyone who voted for RoboMarkets and helped us win this award!”

About RoboMarkets

RoboMarkets is an investment company, operating under CySEC licence No. 191/13. RoboMarkets offers investment services in European countries by providing access to its proprietary trading platforms to traders who work on financial markets. Find out more about the Company’s products and activities on www.robomarkets.com.

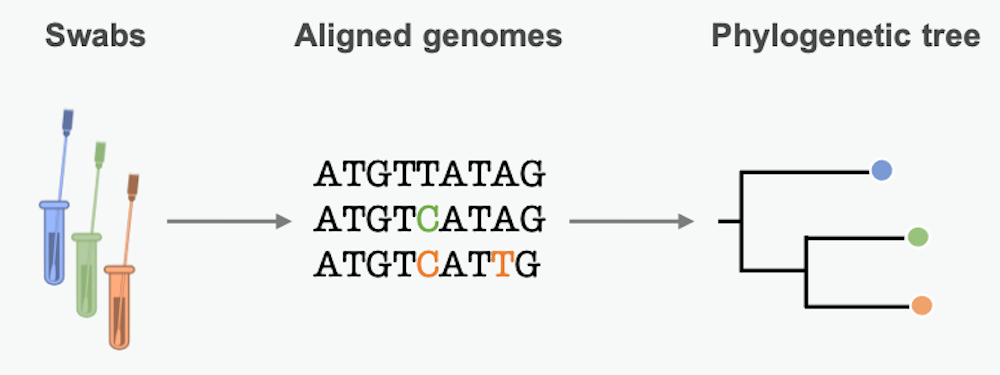

More than 250 million people worldwide have tested positive for SARS-CoV-2, usually after a diagnostic nose swab. Those swabs aren’t trash once they’ve delivered their positive result, though. For scientistslikeus they carry additional valuable information about the coronavirus. Leftover material from swabs can help us uncover hidden aspects of the COVID-19 pandemic.

Pathogens, just like people, each have a genome. This is RNA or DNA that contains an organism’s genetic code – its instructions for life and the information necessary for reproduction.

By lining up genetic sequences obtained from different patients, scientists can see which positions in the sequence differ. These differences represent mutations, small errors incorporated into the genome when the pathogen copies itself. We can use these mutational differences as clues to reconstruct chains of transmission and learn about epidemic dynamics along the way.

Phylodynamics: Piecing together genetic clues

Phylodynamic methods provide a way to describe how mutational differences relate to epidemic dynamics. These approaches allow researchers to get from the raw data about where mutations have occurred in the viral or bacterial genome to understanding all the implications. It might sound complicated, but it’s actually pretty easy to give an intuitive idea of how it works.

Mutations in the pathogen genome get passed from person to person in a transmission chain. Many pathogens acquire lots of mutations over the course of an epidemic. Scientists can summarize these mutational similarities and differences using what’s essentially a family tree for the pathogen. Biologists call it a phylogenetic tree. Each branching point represents a transmission event, when the pathogen moved from one person to another.

A phylogenetic tree is an approximation of the past transmission chain, based on variations in the pathogen’s genetic sequence. Guinat, Windels, Nadeau, CC BY-ND

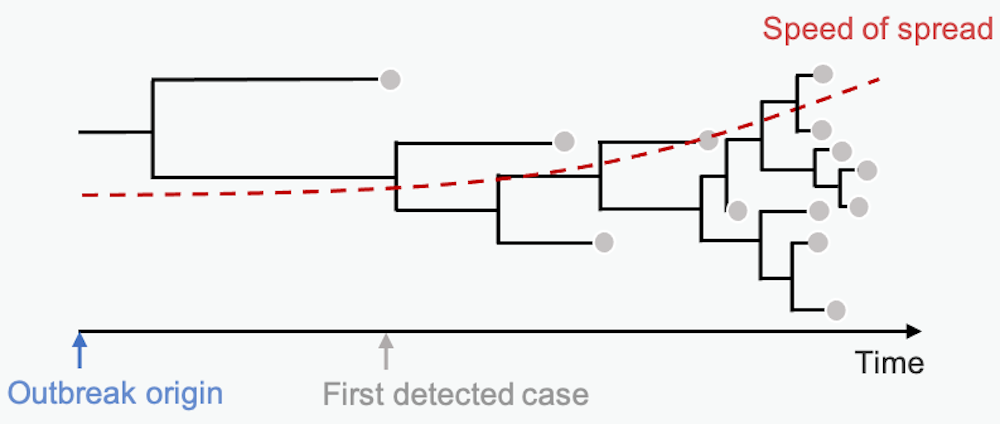

The branch lengths are proportional to the number of differences between sequenced samples. Short branches mean little time between branching points – fast transmission from person to person. Studying the length of branches on this tree can tell us about pathogen spread in the past – maybe even before we knew an epidemic was on the horizon.

Pathogen genome sequences can be used to construct phylogenetic trees and estimate hidden epidemic dynamics. Shorter branches stand for quicker transmission. Guinat, Windels, Nadeau, CC BY-ND

Mathematical models of disease dynamics

Models in general are simplifications of reality. They try to describe core real-life processes with mathematical equations. In phylodynamics, these equations describe the relationship between epidemic processes and the phylogenetic tree.

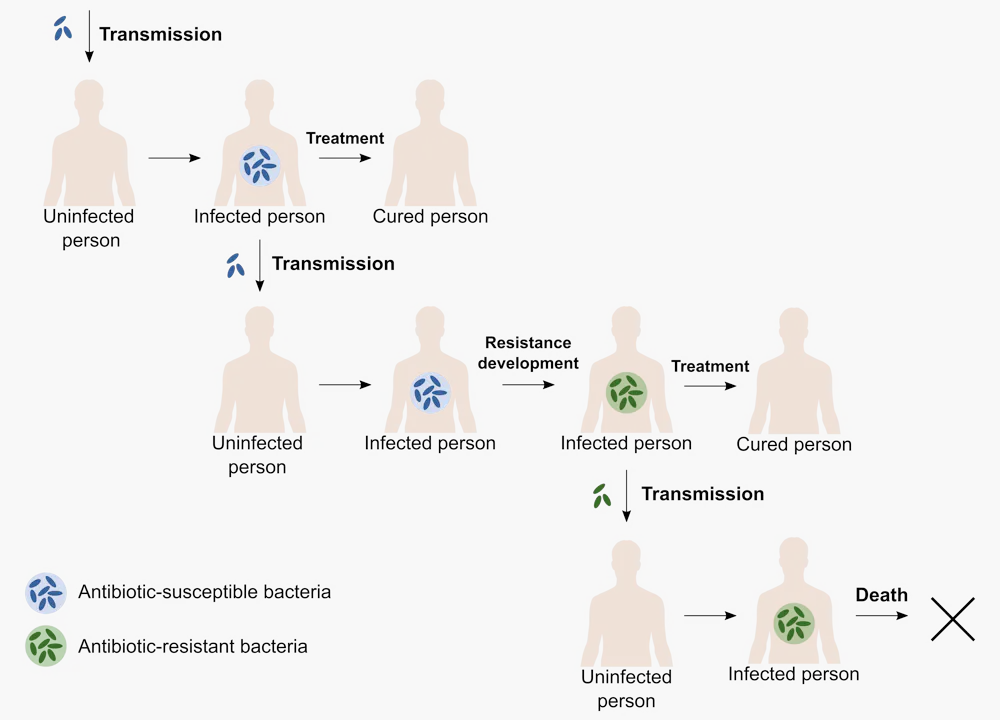

Take, for example, tuberculosis. It’s the deadliest bacterial infection in the world, and it is getting even more threatening because of the widespread evolution of antibiotic resistance. If you catch an antibiotic-resistant version of the tuberculosis bacterium, treatment can take years.

To predict the future burden of resistant tuberculosis, we want to estimate how fast it spreads.

Epidemiologists work to track infections as the pathogen moves through a population. Guinat, Windels, Nadeau, CC BY-ND

To do this, we need a model that captures two important processes. First, there’s the course of infection, and second, there’s the development of antibiotic resistance. In real life, infected people can infect others, get treatment and, in the end, either be cured or, in the worst case, die from the infection. On top of this, the pathogen can develop resistance.

Phylodynamic models capture real-life epidemiological processes into mathematical equations and parameters. Guinat, Windels, Nadeau, CC BY-ND

We can translate these epidemiological processes into a mathematical model with two groups of patients – one group infected with normal tuberculosis and one with antibiotic-resistant tuberculosis. The important processes – transmission, recovery and death – can happen at different rates for each group. Finally, patients whose infection develops antibiotic resistance move from the first group to the second.

This model does ignore some aspects of tuberculosis outbreaks, such as asymptomatic infections or relapses after treatment. Even so, when applied to a set of tuberculosis genomes, this model helps us estimate how fast resistant tuberculosis spreads.

Capturing hidden aspects of epidemics

Uniquely, phylodynamic approaches can help researchers answer questions in situations where diagnosed cases do not give the full picture. For example, what about the number of undetected cases or the source of a new epidemic?

But were poultry farms or wild birds the real driver of spread? Obviously we cannot ask the birds themselves. Instead, phylodynamic modeling based on H5N8 genomes sampled from poultry farms and wild birds helped us get an answer. It turns out that in some countries the pathogen mainly spread from farm to farm, while in others it spread from wild birds to farms.

Phylodynamic models can estimate the number of avian influenza virus transmissions between wild birds and poultry. C. LeGall, CC BY-NC-ND

More recently, phylodynamic analyses helped evaluate the impact of control strategies for SARS-CoV-2, including the first border closures and strict early lockdowns. A big advantage of phylodynamic modeling is that it can account for undetected cases. The models can even describe early stages of the outbreak in the absence of samples from that time period.

Phylodynamic models are under intensive development, continuously expanding the field to new applications and larger datasets. However, there are still challenges in extending genome sequencing efforts to undersampled species and regions and upholding rapid public data sharing. Ultimately, these data and models will help everyone gain new insights on epidemics and how to control them.

Interest rates were remarkably stable in ancient societies. It has been argued that this was because they reflected the local system of numerical fractions. Classical Greece had a “normal” interest rate of 10% per annum to reflect its smallest fractional unit, dekate, for instance, whereas classical Rome’s was 8.33% per annum to reflect its smallest fractional unit of 1/12th, uncia.

This saved ancient policymakers from the trouble of making interest rate decisions based on the economic outlook. It also spared them from being dubbed “unreliable boyfriends” by commentators for wrongfooting financial markets with their interest-rate decisions – unlike former Bank of England Governor Mark Carney and his successor, Andrew Bailey.

Bailey was most recently criticised in November when the Bank of England’s Monetary Policy Committee (MPC) voted to keep the policy rate of interest on hold at 0.1% despite signalling that it would be raising it to ward off inflation. The MPC’s job is to use interest rates to keep consumer price index (CPI) inflation within its 2% target over the next two years, but it is currently expected to remain above that until at least the first quarter of 2024.

The bank’s policymakers decided against raising rates because a majority believe that the current inflationary pressures are, to some extent, temporary. But is that so? US Treasury Secretary Janet Yellen believes inflation will remain high until COVID is under control, since the surge in prices is closely linked to problems in the global supply chain which have meant that there is too little supply to meet demand.

In Yellen’s view this means stubbornly high inflation well into 2022, which raises the question of what temporary means – particularly now that the omicron COVID variant will potentially see supply-chain disruption going on even longer.

Yet the markets’ bigger concern about omicron is that it is going to hamper economic growth. Economic growth is another (more positive) cause of inflation, so the new variant will potentially reduce the price pressure. For that reason, market expectations of imminent interest-rate rises have markedly weakened since omicron emerged. Paradoxically, however, delayed interest-rate action will arguably make it more likely that higher inflation (from prolonged supply-chain problems) will ultimately last longer.

To further raise the pressure on the MPC, the annual rate of inflation has just risen to 5.1% (up from 4.2% a month ago). The bank’s deputy governor, Ben Broadbent, had predicted recently that the UK wouldn’t hit this rate until the spring.

In this context, the MPC is currently meeting to make its latest decision on interest rates. So what should it do?

The interest rates predictor

To help determine this, there is a model called the “monetary policy rule”, originally devised by economist John Taylor at Stanford in the 1990s, which takes several important variables into account. The first is the central bank’s two-year inflation forecast – in other words, the most likely outcome based on market expectations of interest rates – relative to the official inflation target.

The second variable is UK economic growth relative to its long-run equilibrium level – that is, the Office for Budget Responsibility (OBR) “output gap” measure of “excess demand” in the economy. According to the OBR, UK output is currently 0.7% above equilibrium.

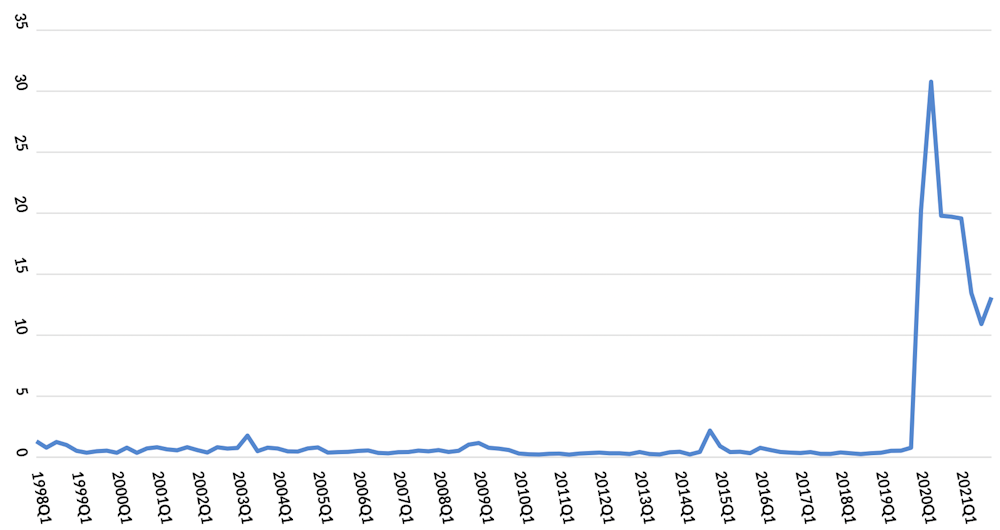

To improve the accuracy of the monetary rule during the pandemic, I have incorporated a third variable, an “infectious disease equity market volatility tracker”. This is an index constructed and updated daily by a team of US economists. It is based on approximately 3,000 US newspaper articles that contain economic terms such as “economy” and “financial”; stock market terms; volatility terms such as “uncertainty” and “risk”; and infectious disease terms such as “epidemic”, “pandemic”, “virus”, “flu” and “coronavirus”. The tracker is not just focused on COVID, and has over 20 years of historical data.

Infectious disease tracker, 1998-2021

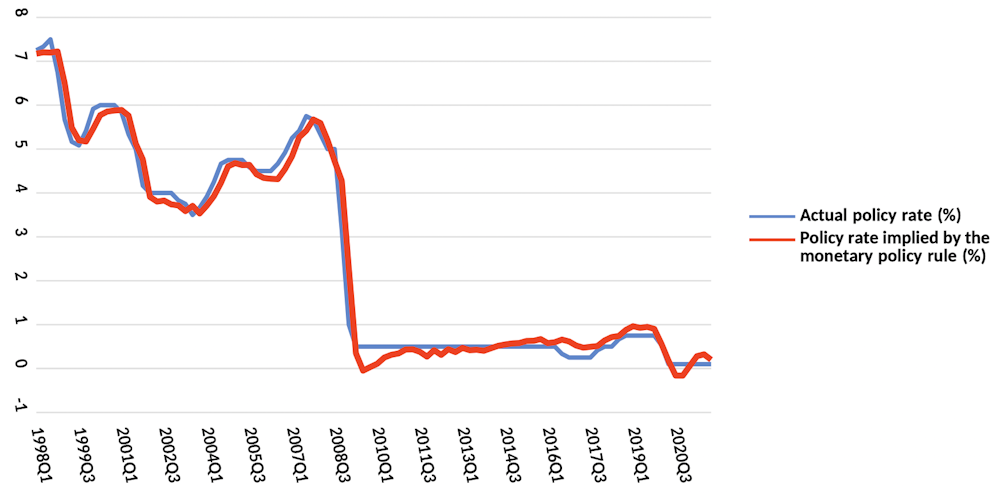

So how well does this model predict interest-rate decisions? The next chart shows Bank of England interest-rate decisions going back to 1998, alongside what the model would have predicted. As you can see, it does a pretty decent job in explaining the MPC’s interest rate decisions. (Since the disease tracker was at such low levels until the COVID pandemic, its influence on interest rates would have been very small until recently).

UK policy rate decisions vs model predictions

One interesting thing to point out about this model is that it prescribed a negative policy rate of -0.15% for the end of 2020, when the UK was pushed into yet another COVID lockdown. At that time, the MPC decided against a negative interest rate, although it was certainly an option at the time as a way of encouraging as much lending as possible. Other central banks such as the European Central Bank had already been experimenting with negative rates for some time.

As for the MPC’s upcoming decision, the model is “recommending” a policy rate of 0.2% – in other words, a slight increase from today’s 0.1% rate. Without the disease tracker built in, the model would instead be calling for a 0.5% rate, so it shows how growth fears are weighing on its advice. Of course, if market expectations are correct and the MPC leaves rates unchanged, we will conclude that these fears were weighing on them even more.

The danger with such an approach is that growth fears are potentially being overdone right now. There is evidence that the UK economy has managed to adapt to past COVID restrictions. And the latest annual inflation reading of 5.1% will make it more likely that inflation in two years’ time will be higher than the current 2.2% prediction – putting additional pressure on the MPC to act.

Then again, with the speed at which omicron is moving through the population, the infectious disease tracker could well soon jump back to 2020 levels. Were that to happen, the model would recommend that interest rates remain at 0.1%. It all serves to highlight why it is a very difficult time for the MPC to make a decision, and why, particularly during the pandemic era, it is useful to look at the monetary rule for guidance.