By JustForex

The EUR/USD currency pair

- Prev Open: 1.0049

- Prev Close: 0.9943

- % chg. over the last day: -1.07 %

Important data will be released today on the US labor market. The Nonfarm Payroll report is expected to show an increase of 300,000 jobs after recording an increase of 528,000 in July. Another strong report is likely to further reinforce expectations that the Fed will continue its excessive rate hikes after three straight 75 basis point hikes. The US dollar hit a 20-year high yesterday as economic data supports the Fed’s aggressive stance.

- Support levels: 0.9900

- Resistance levels: 0.9973, 1.0024, 1.0112, 1.0146, 1.0230, 1.0286, 1.0365

From the technical point of view, the trend on the EUR/USD currency pair on the hourly time frame is bearish. Yesterday the EUR/USD quotes fell below parity again. Technically, a wide balance is being formed. The MACD indicator has become negative, and the selling pressure remains. Under such market conditions it is best to look for buy trades on intraday time frames from the support level of 0.9900, but only with a confirmation in the form of a false breakdown. Sell trades can be considered from resistance levels of 0.9973 or 1.0024, but only after the additional confirmation.

Alternative scenario: if the price breaks out of the 1.0146 resistance level and fixes above, the uptrend will likely resume.

- – Eurozone Producer Price Index (m/m) at 12:00 (GMT+3);

- – US Nonfarm Payrolls (m/m) at 15:30 (GMT+3);

- – US Unemployment Rate (m/m) at 15:30 (GMT+3).

The GBP/USD currency pair

- Prev Open: 1.1622

- Prev Close: 1.1544

- % chg. over the last day: -0.67 %

The UK Manufacturing Business Activity Index unexpectedly increased overr the last month from 46 to 47.3. This is a positive factor, but the value is still below the 50 levels, indicating a slowdown in the sector. If you look at the GBP/USD chart on higher time frames, traders can clearly see that the British pound has been declining against the US dollar since 2007. But the rate of decline has gained strength in recent months, as the energy crisis and lack of government continue to weigh on the national exchange rate.

- Support levels: 1.1500, 1.1400

- Resistance levels: 1.1586, 1.1670, 1.1817, 1.1838, 1.1901, 1.1994, 1.2035, 1.2167

From the technical point of view, the trend on the GBP/USD currency pair on the hourly time frame is bearish. The situation does not change. The British pound has been declining for 8 sessions in a row and breaking through all support levels. The price is trading below the moving levels, and the MACD indicator is in the negative zone, but the divergence is getting stronger. At the moment, it is best to look for sell trades on intraday time frames, the nearest resistance level is 1.1586. Buy trades can be considered from the support level of 1.1500, but only after an additional confirmation in the form of a reverse initiative.

Alternative scenario: if the price breaks out through the 1.1817 resistance level and fixes above, the uptrend will likely resume.

- – US Nonfarm Payrolls (m/m) at 15:30 (GMT+3);

- – US Unemployment Rate (m/m) at 15:30 (GMT+3).

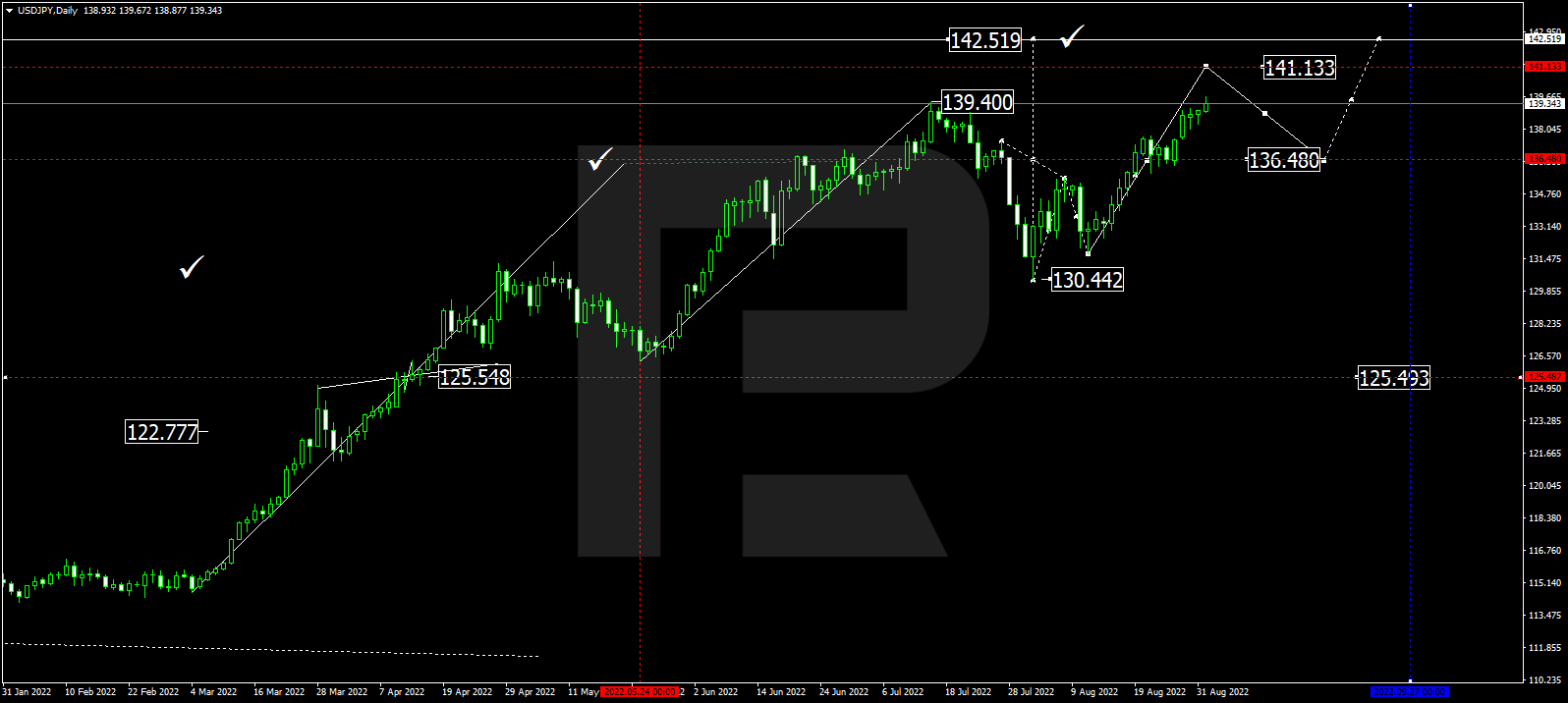

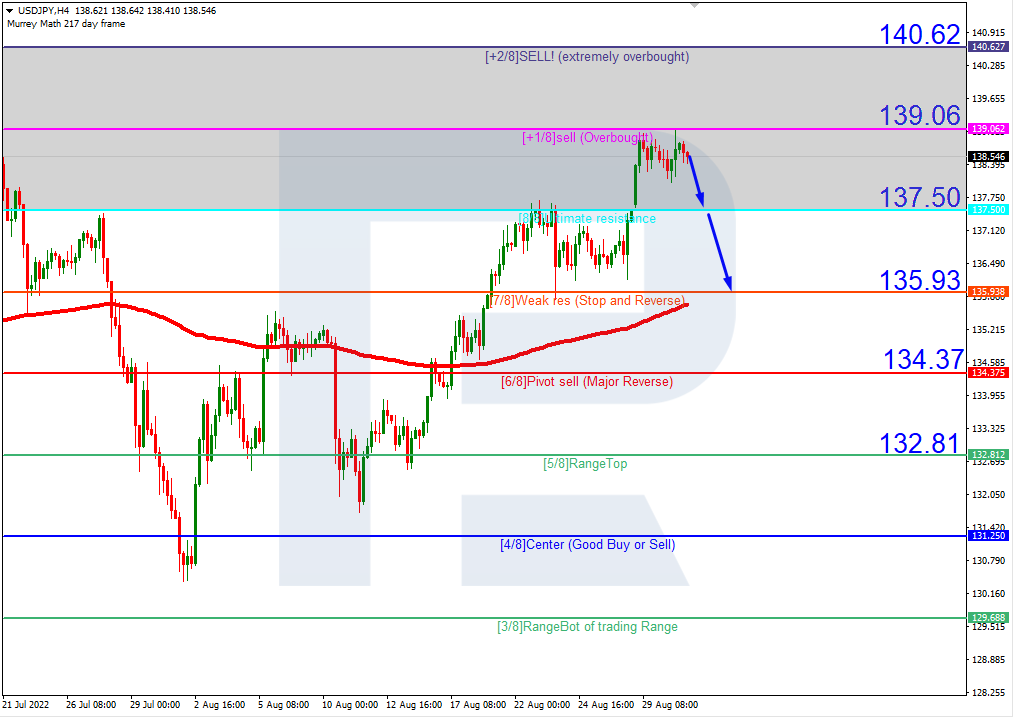

The USD/JPY currency pair

- Prev Open: 139.08

- Prev Close: 140.20

- % chg. over the last day: +0.81 %

The Japanese yen has fallen to 140.23 yen against the dollar, its lowest level since 1998. The continuing fall in the Japanese currency is putting pressure on the consensus between Japan’s Central Bank, which is trying to boost inflation, and Japan’s government, which is desperately trying to avoid a cost-of-living crisis. Some analysts say that fixing the price above the 140 level could trigger government intervention.

- Support levels: 139.61, 137.67, 136.85, 135.89, 135.35, 134.23, 133.47, 132.27

- Resistance levels: 141.00, 142.00

From the technical point of view, the medium-term trend on the currency pair USD/JPY is bullish. The price is trading above the moving average lines again, and the buyers’ pressure remains. The MACD indicator remains positive, but there are signs of divergence, which means that a technical correction will take place soon. Under such market conditions, buy trades can be sought from the support level of 139.61, but with additional confirmation. For sell deals, it is possible to consider the psychological resistance levels of 141 and 142, but only with additional confirmation, as fundamentally, USD/JPY quotes are inclined to grow.

Alternative scenario: If the price fixes below 137.67, the downtrend will likely resume.

- – US Nonfarm Payrolls (m/m) at 15:30 (GMT+3);

- – US Unemployment Rate (m/m) at 15:30 (GMT+3).

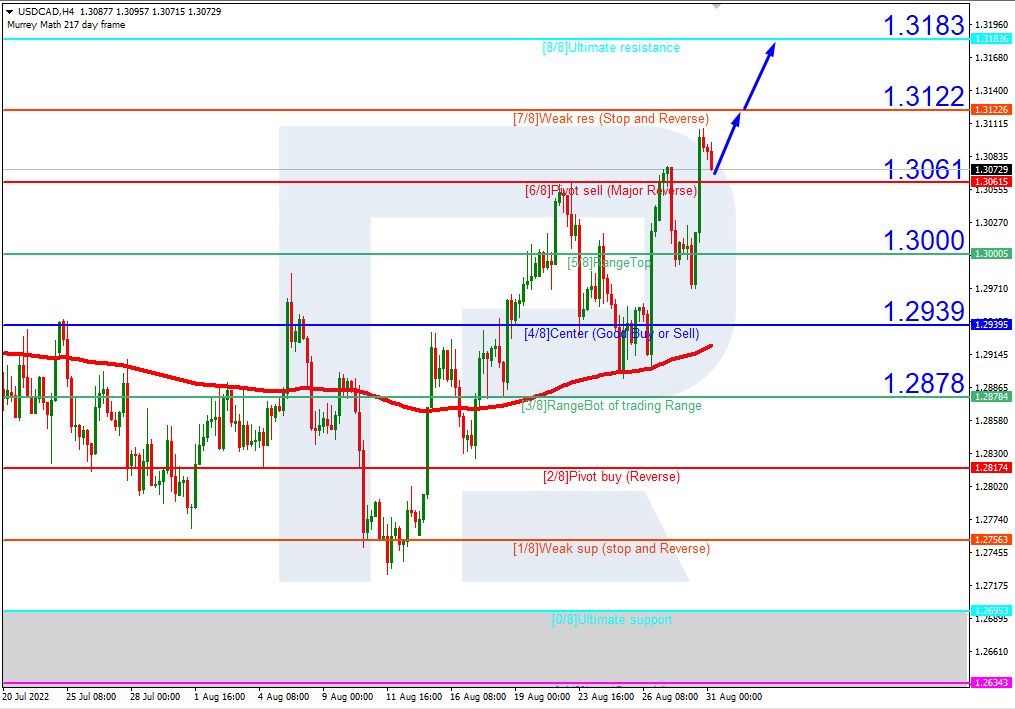

The USD/CAD currency pair

- Prev Open: 1.3125

- Prev Close: 1.3153

- % chg. over the last day: +0.21 %

The Canadian dollar is a commodity currency and depends not only on the monetary policy of the Bank of Canada, but also on the dynamics of the dollar index and oil prices. The deteriorating economic outlook in China and Europe, along with geopolitical concerns related to soaring gas prices and the ongoing war in Ukraine have bolstered the dollar in recent weeks. At the same time, an oil sell-off due to a new coronavirus outbreak in China could push a barrel below $85. As a result, the Canadian dollar has been under pressure from a rising dollar index and falling oil prices recently.

- Support levels: 1.3103, 1.3026, 1.2992, 1.2958, 1.2940, 1.2900, 1.2858, 1.2809, 1.2761

- Resistance levels: 1.3220

From the point of view of technical analysis, the trend on the USD/CAD currency pair is bullish. The price is now trading above the moving averages. The MACD indicator is in the positive zone, but there are signs of divergence. Under such market conditions, buy trades should be considered on the lower time frames from the support levels of 1.3103 or 1.3026, but only with confirmation. For sell deals, it is better to consider the resistance level of 1.3220, but only after additional confirmation, as the level has already been tested.

Alternative scenario: if the price breaks down and consolidates below the 1.2992 support level, the downtrend will likely resume.

- – US Nonfarm Payrolls (m/m) at 15:30 (GMT+3);

- – US Unemployment Rate (m/m) at 15:30 (GMT+3).

By JustForex

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.