The S&P 500 was in a downtrend until a lower bottom formed on 13 October. Bulls found the price attractive at those levels and the momentum in the market started shifting.

A closer look at the Momentum Oscillator reveals positive divergence between points “a” and “b” when comparing the bottoms at 3559.0 and 3492.4. This could have alerted technical traders that the current trend might be losing steam.

After the lower bottom at 3492.4, the price of the S&P 500 broke through the weekly resistance level at 3661.5, and the bullish activity was further confirmed when the 15 and 34 Simple Moving Averages and the Momentum Oscillator broke through the 100 base-line into bullish territory.

Since then the market has made four impulse waves in the uptrend before a lower top formed on 24 November and the market seemed to begin to lose some bullish momentum. The bears tried to pull the market lower but the bulls found new backing near the weekly support level at 3920.0 and a new impulse wave started on 30 November.

As long as the bulls can sustain the upward momentum, the outlook for the S&P 500 on the D1 time frame will remain bullish.

Volatus Aerospace Corp. could be a company to watch in the fast-growing drone aviation market.

Volatus Aerospace Corp. (VOL:TSX; VLTTF:OTCQB) is a small, little-known player that could make a big impact in the burgeoning but rapidly growing multi-billion dollar commercial drone market.

Volatus is one of several players looking to carve a piece out of the global drone market expected to approach US$50 billion in annual revenues in the next seven years.

Earlier this month, the Canadian-based company, which serves the commercial and defense markets with integrated drone solutions, reported record revenue of CA$11.12 million, up 68% over the previous quarter and a 238% jump from the same period a year ago.

Building Revenue

Volatus is building revenue from sales of drone equipment, drones-as-a-service, training services, and crewed aircraft sales and services. The recent jump in revenue was driven by organic growth, scale in drone activities, and an increase in aviation revenue.

Global revenue from drones was valued at US$6.51 billion last year, expected to reach US$8.15 billion this year and jump to US$47.38 billion by 2029, according to a report by Fortune Business Insights.

The war in Ukraine has created a need for drones that will continue long after the conflict has ended, said Volatus Chief Executive Officer Glen Lynch during a conference call about the company’s earnings results earlier this month.

“Drones will have a major role to play in the reconstruction . . . of the country,” Lynch said. “The conflict in Ukraine literally changed the way countries around the world are looking at the use of drones and modern warfare. So, we’re responding to numerous opportunities right now for sales in NATO countries that are not currently engaged in fighting directly in the conflict in Ukraine; we’re looking at a fairly robust future for drones in the defense sector.”

Volatus provides the commercial and defense markets with integrated drone solutions. It uses a network of more than 1,200 contract pilots across the Americas, providing imaging and security, equipment sales, and support and training.

The company is also providing aerial surveillance and monitoring of oil and gas pipelines, a market Volatus executives believe is valued at US$58.4 billion.

Catalyst: Two New Acquisitions

Volatus may have taken another step toward cornering the market for monitoring the oil and gas pipeline market with its recent acquisition of Synergy Aviation. The company believes Synergy, based in Edmonton, Alberta, will strengthen its position to provide green drone technologies for oil and gas infrastructure monitoring as an alternative to less environmentally friendly helicopters and airplanes.

Volatus also completed an acquisition of iRed Remote Sensing of Emsworth, England, to reinforce the company’s ability in infrared inspection while expanding its presence in the UK and Europe.

Today, November 28, 2022, Volatus announced another acquisition, signing to annex Syracuse-based Empire Drone Company LLC. This company is known as one of North America’s burgeoning distributors and integrators for unmanned aerial systems. Empire Drone’s projected 2022 revenue is CA$2.5M with a 6% EBITDA margin.

With this acquisition, Volatus will purchase 100% of the company for a cash consideration of US$300,000, and equity of US$350,000 with a minimum floor price of $0.65. This includes, according to the company, “an earn-out of US$350,000 paid in equity after one year anniversary based on the 30-day volume weighted average price (VWAP) with a minimum floor price of US$0.65 per share and assume the long-term debt of US$225,000.”

Volatus Taking Off With Drone Sector

Global revenue from drones was valued at US$6.51 billion last year, expected to reach US$8.15 billion this year and jump to US$47.38 billion by 2029, according to a report by Fortune Business Insights.

While the report says drones will likely have several commercial applications, including medical emergency transportation, and filming and photography, it also concluded that a “rise in demand for unmanned systems in the oil and gas, energy, and power generation sector is likely to fuel market growth in the upcoming years.”

“I believe it’s only a matter of time before it eventually hits US$5.00,” Volatus Investor Edward Vranic wrote.

In addition to its third-quarter record revenue growth, Volatus also reported a gross profit of CA$3.3 million, up from CA$2.6 million in the year-ago period. The company also reported a gross margin of 30%, an increase of 127 basis points over its second quarter of this year.

Volatus says its recent acquisitions of Synergy and iRed provide approximately US$7.5 million in proforma revenue and US$1 million in proforma EBITDA for the first nine months, boosting the company’s revenue to US$30 million with a proforma EBITDA of US$1.63 million for the same three quarters.

Volatus is also working to improve Beyond Visual Line of Sight (BVLOS), a technology that helps drone operators avoid collisions with other aircraft when their drones are out of visual range. Volatus is currently trading at US$0.30. But the company’s stock could see a dramatic rise as it continues to grow aggressively in multiple areas in the drone sector, wrote Edward Vranic, a Volatus investor, in his Canadian small-cap investment blog on Oct. 31.

“I believe it’s only a matter of time before it eventually hits US$5.00,” he wrote. “With that stock price increase coming from a mix of continued revenue growth, an ability to achieve cash flow positive operations within two years, and improved market sentiment leading to more aggressive valuation multiples. VOL is a thinly traded stock, and it won’t take much to send it into rocket ship emoji mode.”

Ownership and Share Structure

Top shareholders in the company include CEO Lynch with 26.62% or 38.46 million shares and Chairman of The Board of Directors and Hauge Court advisory member Ian Alexander McDougall with 27% or 39 million shares, according to the company.

It has a market cap of CA$36.18 million with 113.9 million shares outstanding, 36 million of them free-floating. It trades in a 52-week range of CA$0.89 and CA$0.23.

Disclosures: 1) Pete Barlas wrote this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Volatus Aerospace Corp. Please click herefor more information.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Volatus Aerospace Corp., a company mentioned in this article.

Shares of Axsome Therapeutics Inc. traded to a new 52-week high after the company reported its AXS-05 successfully met both the primary and key secondary endpoints in the Phase 3 ACCORD Alzheimer’s disease agitation trial.

Biopharmaceutical company Axsome Therapeutics Inc. (AXSM:NASDAQ), which is focused on developing new medicines for use in the treatment of central nervous system (CNS) disorders, today announced that “AXS-05, a novel, oral, investigational NMDA receptor antagonist with multimodal activity, met the primary and key secondary endpoints in the ACCORD (Assessing Clinical Outcomes in Alzheimer’s Disease Agitation) Phase 3 trial, by substantially and statistically significantly delaying the time to relapse and preventing relapse of agitation in patients with Alzheimer’s disease, as compared to placebo.”

The company advised that the multi-center, randomized Phase 3 ACCORD study included a total of 178 patients in the U.S. who were diagnosed with Alzheimer’s disease agitation. The firm indicated that those who had received open-label treatment with AXS-05 demonstrated “rapid, substantial, and statistically significant improvement compared to baseline in agitation symptoms.” These patients who had experienced a sustained clinical response after open-label treatment with AXS-05 were then randomized to receive continued treatment with AXS-05 or a placebo.

Axsome Therapeutics noted that in the ACCORD study, AXS-05 met the primary objective defined as a substantial and statistically significant delay in the time elapsed to relapse of agitation symptoms compared to placebo. In the study, AXS-05 also met a key secondary endpoint which was listed as the prevention of relapses.

The company highlighted using the modified Alzheimer’s Disease Cooperative Study-CGIC (clinicians) scale, AXS-05 was shown to lessen Alzheimer’s disease agitation in 66% of patients after two weeks and by 86% of patients after five weeks. Similarly, utilizing the PGI-C assessment (caregivers) scale, 68% of patients showed improvement in agitation at two weeks, and 89% registered improvement at five weeks.

Dr. Cummings continued, “The results of the ACCORD trial demonstrate convincing clinical activity for AXS-05 on agitation associated with Alzheimer’s disease based on both a significant delay in symptom relapse as well as a reduction of relapse compared to placebo.”

Jeffrey Cummings, M.D., D.Sc., Director Emeritus of the Cleveland Clinic Lou Ruvo Center for Brain Health, and Chambers Professor of Brain Science at the University of Nevada Las Vegas, noted that “Agitation is one of the most troubling and consequential aspects of Alzheimer’s disease for patients and their caregivers as it is associated with early nursing home placement, accelerated cognitive decline, and increased mortality.”

Dr. Cummings continued, “The results of the ACCORD trial demonstrate convincing clinical activity for AXS-05 on agitation associated with Alzheimer’s disease based on both a significant delay in symptom relapse as well as a reduction of relapse compared to placebo. Treatment with AXS-05 during the open-label period in a large cohort of patients resulted in rapid and clinically meaningful improvements in Alzheimer’s disease agitation.”

The company’s CEO, Herriot Tabuteau, M.D., stated, “With the positive results from ACCORD, AXS-05 has now demonstrated efficacy in the treatment of Alzheimer’s disease agitation in two well-controlled trials. In addition to the strong results versus placebo in the double-blind period, results from the open-label period evidenced rapid, substantial, and significant improvements in Alzheimer’s disease agitation versus baseline with AXS-05 treatment.”

“We intend to discuss these findings with the FDA in the context of the ongoing clinical development of AXS-05 in this indication, with the goal of providing a much-needed treatment to the millions of patients living with Alzheimer’s disease agitation and their caregivers,” Dr. Tabuteau added.

The company stated that “Alzheimer’s disease (AD) is a progressive neurodegenerative disorder characterized by cognitive decline and behavioral and psychological symptoms including agitation.” AD affects around six million people in the U.S. and is the most frequently occurring type of dementia. Agitation, which includes aggressive behavior, disinhibition, disruptive irritability, and emotional distress, is reported in about 70% of patients diagnosed with AD. Currently, there are no U.S. Food and Drug Administration (FDA) approved therapies to treat agitation in AD patients.

The firm explained that “AXS-05 (dextromethorphan-bupropion) is a novel, oral, patent protected, investigational N-methyl-D-aspartate (NMDA) receptor antagonist with multimodal activity under development for the treatment of Alzheimer’s disease (AD) agitation and other central nervous system (CNS) disorders.” The company uses its metabolic inhibition technology to modulate the delivery of AXS-05’s patented formulation of dextromethorphan and bupropion. The report listed that supported by the positive results collected during the ADVANCE-1 trial, AXS-05 was awarded Breakthrough Therapy designation by the FDA in June 2020 for the treatment of Alzheimer’s disease agitation.

Axsome Therapeutics is a biopharmaceutical firm headquartered in New York, NY that is working to develop novel therapies for treating central nervous system (CNS) conditions. Axsome’s ongoing product development pipeline includes potential treatments for agitation associated with Alzheimer’s disease, acute migraine, fibromyalgia, smoking cessation, cataplexy in narcolepsy, and attention deficit hyperactivity disorder.

Axsome Therapeutics started the day with a market cap of around US$2.47 billion, with approximately 43.43 million shares outstanding and a short interest of about 15.6%. AXSM shares opened 25% higher today at US$71.035 (+US$14.215, +25.02%) over Friday’s US$56.82 closing price and reached a new 52-week high price this morning of US$79.68. The stock traded today between US$68.12 and US$79.68 per share and closed for trading at US$74.68 (+US$17.92, +31.54%).

Disclosures:

1) Stephen Hytha wrote this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees.

3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

This company serving the oil and gas industry grew revenue 14% over the last 12 months and is expected to continue the trend, noted an Echelon Capital Markets report.

Computer Modelling Group Ltd. (CMG:TSX; CMDXF:OTC), which develops and licenses simulation software for the oil and gas industry, posted Q2 FY23 results that beat Echelon Capital Markets and the Street’s projections, reported analyst Amr Ezzat in a November 10, 2022 research note.

After the Canadian tech firm released its quarterly results, Echelon increased some of its FY23 and FY24 estimates on the company to reflect the stronger growth in the annuity/maintenance (A&M) software licenses segment.

These changes boosted Echelon’s target price on Computer Modelling to CA$6.25 per share, up from CA$5.50. In comparison, the software firm’s current price is about CA$5.35 per share.

“The high-quality beat is characterized by recurring revenues growing at 14% year over year (YOY),” Echelon’s Ezzat highlighted. “The strong pick-up in growth is not a one-off.”

Ezzat pointed out that two factors should help Computer Modelling maintain its current growth momentum. One is new CEO Pramod Jain, likely requiring a more concerted effort going forward to increase revenues organically and organically.

The second is “the strong macroeconomic backdrop with higher oil prices.” Echelon rates the software firm Buy.

“The high-quality beat is characterized by recurring revenues growing at 14% year over year (YOY),” Echelon’s Ezzat highlighted. “The strong pick-up in growth is not a one-off.”

Proof of Growth

Computer Modelling’s A&M sales in all geographic locales accounted for about 80% of its total sales during Q2 FY23. At US$14.8 million (US$14.8M), A&M sales exceeded Echelon’s US$13.8M forecast and were 12% higher YOY. Standout regions were the U.S., where sales during the quarter increased by 20%, and the Eastern Hemisphere, where they grew by 15%.

Computer Modelling’s total Q2 FY23 sales were US$18.1M, a 13.4% increase over last year’s. The amount also surpassed Echelon and the Street’s forecasts of US$16.4M and US$16.6M, respectively.

Perpetual license sales amounted to $0.8M, better than Echelon’s US$0.4M estimate but worse YOY, by 7.8%. The professional services segment fared better, with US$2.5M in sales, up 32.9% YOY and better than Echelon’s US$2.2M projection.

Deferred revenues increased 13.8% YOY to US$24.2M and 4.1% quarter over quarter.

Adjusted Q2 FY23 EBITDA was US$8.8M (for a 48.8% margin), beating Echelon and the Street’s estimates of US$7M and US$7.3M, respectively. EBITDA included US$2.3M in charges for restructuring, but most of those changes should be done now, Ezzat noted. Total operating expenses were US$10.2M, 5.5% higher than last year’s US$9.7M.

Earnings per share were US$0.05, between Echelon’s US$0.04 and consensus’ US$0.06 forecasts.

Free cash flow was US$5.7M, up from Q2 FY22’s US$2.1M. The last 12 months of free cash flow amounted to US$25.9M, which exceeds the company’s US$16.1M dividend outlay.

At Q2 FY23’s end, Computer Modelling had US$56.9M in cash and no debt.

Disclosures: 1) Doresa Banning wrote this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures For Echelon Wealth Partners Inc., Computer Modelling Group, November 10, 2022

Echelon Wealth Partners Inc. is a member of IIROC and CIPF. The documents on this website have been prepared for the viewer only as an example of strategy consistent with our recommendations; it is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any particular investing strategy. Any opinions or recommendations expressed herein do not necessarily reflect those of Echelon Wealth Partners Inc.

Echelon Wealth Partners Inc. cannot accept any trading instructions via e-mail as the timely receipt of e-mail messages, or their integrity over the Internet, cannot be guaranteed.

Dividend yields change as stock prices change, and companies may change or cancel dividend payments in the future. All securities involve varying amounts of risk, and their values will fluctuate, and the fluctuation of foreign currency exchange rates will also impact your investment returns if measured in Canadian Dollars. Past performance does not guarantee future returns, investments may increase or decrease in value and you may lose money. Data from various sources were used in the preparation of these documents; the information is believed but in no way warranted to be reliable, accurate and appropriate. Echelon Wealth Partners Inc. employees may buy and sell shares of the companies that are recommended for their own accounts and for the accounts of other clients. Echelon Wealth Partners compensates its Research Analysts from a variety of sources. The Research Department is a cost centre and is funded by the business activities of Echelon Wealth Partners including, Institutional Equity Sales and Trading, Retail Sales and Corporate and Investment Banking.

U.S. Disclosures: This research report was prepared by Echelon Wealth Partners Inc., a member of the Investment Industry Regulatory Organization of Canada and the Canadian Investor Protection Fund. This report does not constitute an offer to sell or the solicitation of an offer to buy any of the securities discussed herein. Echelon Wealth Partners Inc. is not registered as a broker-dealer in the United States and is not be subject to U.S. rules regarding the preparation of research reports and the independence of research analysts. Any resulting transactions should be effected through a U.S. broker-dealer.

ANALYST CERTIFICATION

Company: Computer Modelling Group| CMG:TSX

I, Amr Ezzat, hereby certify that the views expressed in this report accurately reflect my personal views about the subject securities or issuers. I also certify that I have not, am not, and will not receive, directly or indirectly, compensation in exchange for expressing the specific recommendations or views in this report.

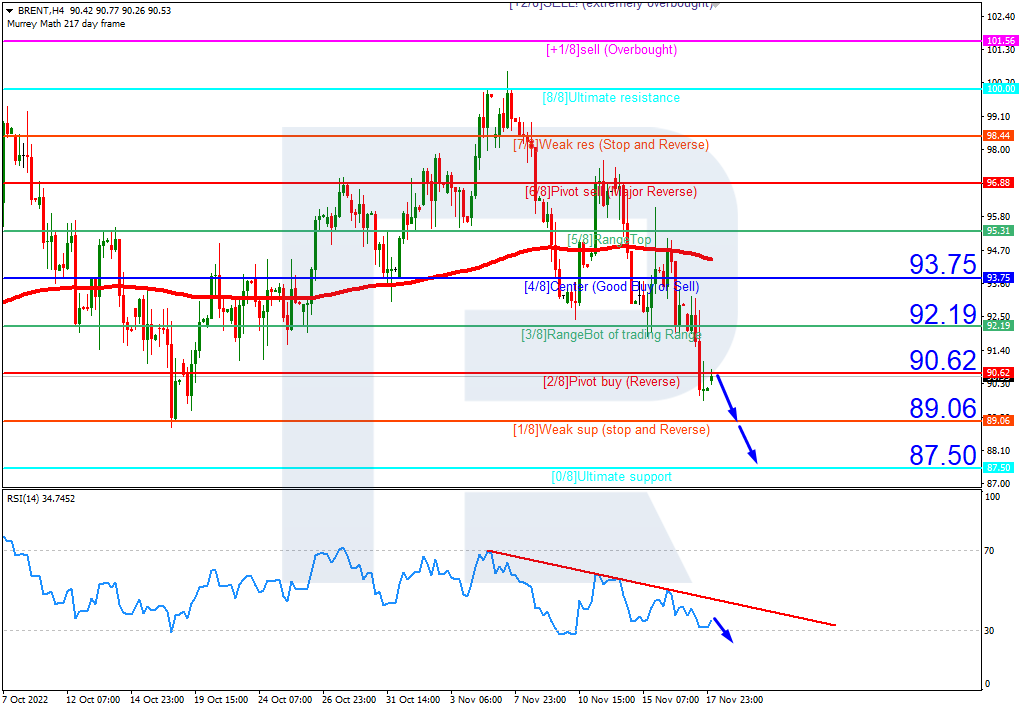

On H4, the quotes are under the 200-day Moving Average, which indicates prevalence of the downtrend. The RSI is nearing the oversold area. Currently, we should expect a test of 1/8 (89.06), a breakaway of it, and falling to the support level of 0/8 (87.50). The scenario can be cancelled by rising over the resistance level of 2/8 (90.62). In this case, the quotes might rise to 3/8 (92.19).

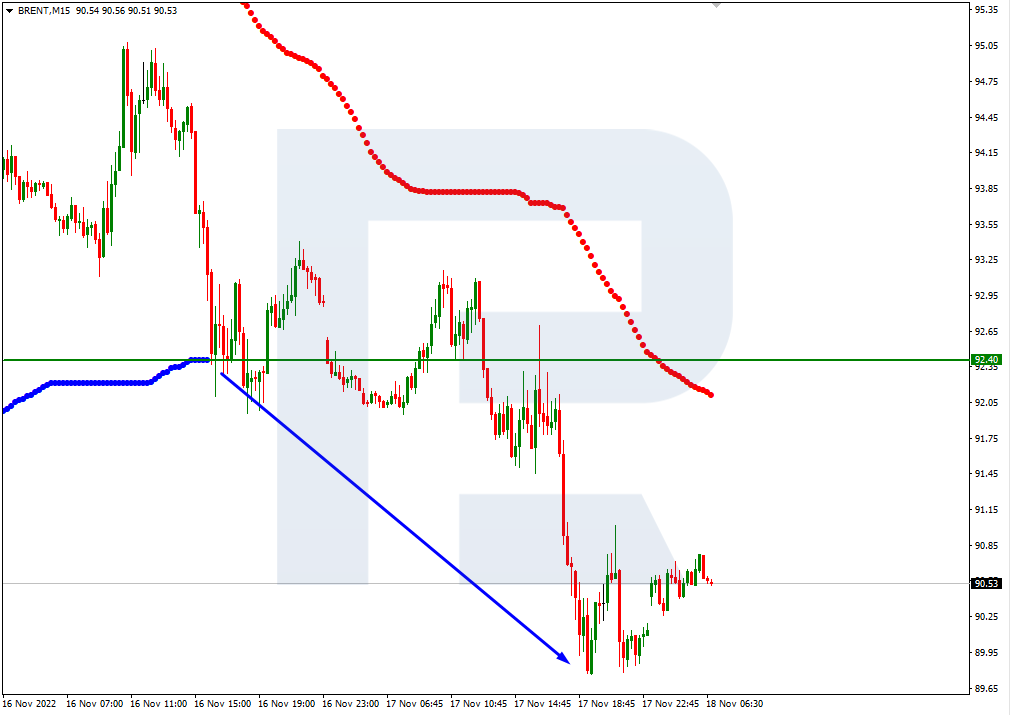

On M15, the lower line of VoltyChannel is broken away, which confirms the downtrend and a high probability of further price falling.

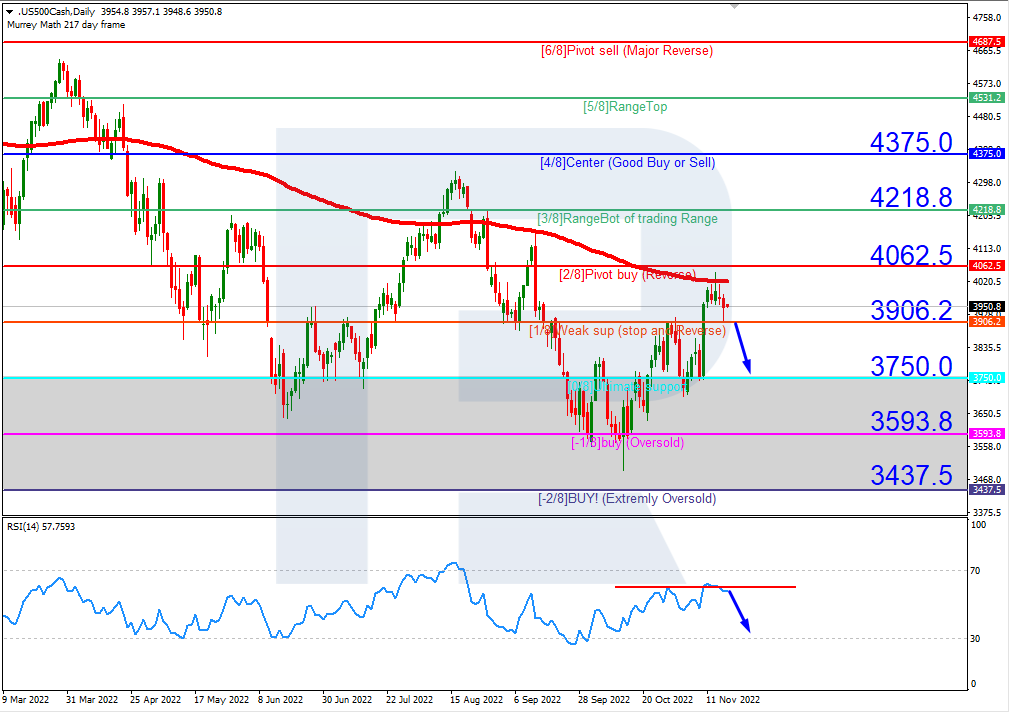

S&P 500

On H4, the quotes have bounced off the 200-day Moving Average and are now beneath it, which indicates the prevalence of a downtrend. The RSI is testing the resistance line. Currently, we expect the price to break through the support level of 1/8 (3906.2) downwards and fall to 0/8 (3750.0). The scenario can be cancelled by rising over the resistance level of 2/8 (4062.5). This might lead to a trend reversal and growth of the index quotes to 3/8 (4218.8).

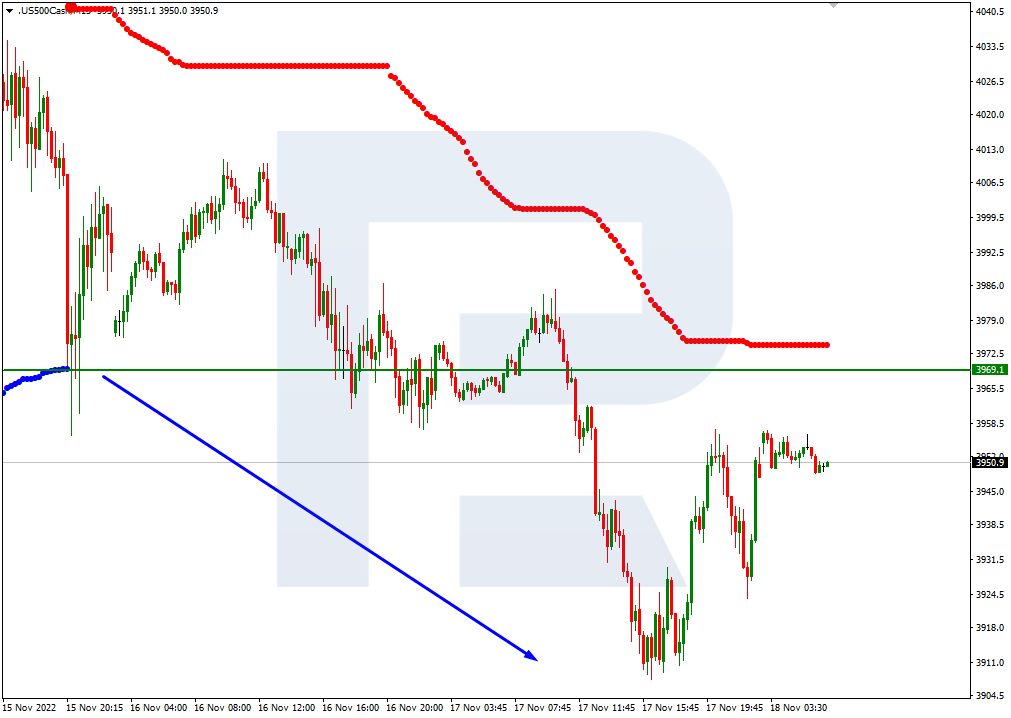

On M15, the lower line of VoltyChannel is broken away, which increases the probability of further falling.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

The company’s stock has been “nudging higher toward an upside breakout,” technical analyst Clive Maund of CliveMaund.com wrote.

Its gross profit was up 15.8%, its net income rose 175.8%, and EDITDA rose 25.7% over that time, the company said.

Over the nine months that ended Sept. 30, revenue was up 15.1%, gross profit was up 17.1%, net income was up 201%, and EDITDA was up 34.2% compared to 2021.

CliveMaund.com

The company’s stock has been “nudging higher toward an upside breakout,” technical analyst Clive Maund of CliveMaund.com wrote.

“With volume indicators overall positive, momentum-swinging positive again, and moving averages in quite strongly bullish alignment, it is in a position to break into another upleg imminently,” he wrote shortly before its stock went up CA$0.04 this week.

Debt was also lowered by 26.2% or CA$8.9 million to CA$25.1 million, the company said.

The Catalyst

This is not the first time the company has reported impressive growth. It continues to gain momentum after COVID and posted a 23.4% increase in revenue for the second quarter of 2022 compared to Q2 2021, results which analyst Noel Atkinson of Clarus Securities called “monster.”

“DCM achieved a spectacular quarter, driven by strong customer demand and the ability to start passing through some input cost increases to clients,” he wrote in an August update note.

Atkinson reiterated his Buy rating for the stock then and raised his target from CA$2.50 to CA$3.

“We have now delivered three sequential quarters of year over year growth, bringing our revenue up just over 15%,” DCM President and Chief Executive Officer Richard Kellam said. “This growth has been driven by a combination of expansion revenue with existing clients and new business wins of over CA$30 million through the year.”

The Digital Journey

In 2021, the company launched its digital asset management (DAM) cloud solution, ASMBL, to manage corporate media files and other content. The technology has the potential to become a substantial contributor to DCM’s income as it is deployed to the company’s 2,500 corporate clients.

“We continue to make positive progress on our digital journey,” Kellam said. “Substantially, all our new business wins are tech-enabled, and our digitally enabled subscription service and fees are pacing nicely ahead of last year.”

On the print side, the company also noted that it has reforested nearly 470,000 trees, “offsetting 100% of our clients’ paper use.”

DCM has been in business for 60 years. It helps companies with branding, communications, and logistics and provides customer loyalty programs, data and content management, location-specific marketing, labels and asset tracking, multimedia campaign management, and workflow management. Its clients are in many industries, including financial services, health care, emerging markets, retail, non-profits, energy, hospitality, and transportation.

Ownership, Coverage, and Share Structure

DCM Directors and officers hold 31.1% of the company, and employees own close to 4 percent through an employee share program.

The company is covered by Noel Atkinson of Clarus Securities and Chris Thompson of PI Financial. Newsletter writer Clive Maund also covers the stock. Click “See More Live Data” in the data box above to read more from them.

It has a market cap of CA$62.13 million with 44.06 million shares outstanding, with 27.3 million shares free-floating. It trades in the 52-week range of CA$1.46 and CA$1.01.

Disclosures:

1) Steve Sobek wrote this article for Streetwise Reports LLC. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Data Communications Management Corp. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

With late-stage drug candidates and major near-term catalysts, undervalued Aldeyra Therapeutics warrants a Buy to Outperform rating and consideration by potential investors, according to various analysts.

For a biopharma with one new drug candidate on the verge of potential approval in the U.S. and a second close behind, Aldeyra Therapeutics Inc.(ALDX:NASDAQ) is currently undervalued and represents an attractive, derisked investment opportunity, experts said.

The Massachusetts-based firm develops treatments for immune-mediated diseases, which regulate entire immunological systems rather than alter a single protein. The therapeutic candidates are designed to optimize numerous pathways while limiting toxicity, and the biopharma is currently advancing three such products.

A Trio of Potential New Therapies

1) Reproxalap: This RASP, or reactive aldehyde species, inhibiting 0.25% ophthalmic solution for dry eye disease is Aldeyra’s lead drug candidate, for which the company is on schedule to file a new drug application (NDA) with the U.S. Food and Drug Administration (FDA) by year-end.

Approval “could lead to a meaningful lift for the shares,” purported Oppenheimer analyst Justin Kim.

In clinical trials, reproxalap was shown to be efficacious and safe. It “demonstrated robust and consistent dry eye disease benefit,” wrote H.C. Wainwright & Co. analyst Matthew Caufield in a July 13 research note. “We view RASP inhibition as presenting a viable novel pathway in addressing current dry eye disease therapeutic limitations.”

Caulfield noted that approved dry eye disease treatments on the market could take months to have an appreciable effect, have inconsistent responses among patients, and can be uncomfortable, often causing patients to stop using them. RASP is different as it is said to provide immediate relief, unlike previous therapies.

“From an FDA perspective, reproxalap is very safe, passes the Schirmer test with high significance, and has a novel mechanism of action in a field with underserved patients. We think that will be enough for approval,” said BTIG’s Thomas Shrader.

Laidlaw & Co. analyst Dr. Yale Jen stated, “Although ALDX could launch reproxalap by themselves, we believe this is a highly desirable product for large pharma companies, especially those that could leverage their existing or start an ophthalmology sales force.”

BTIG’s Thomas Shrader is one of several analysts who remain bullish on reproxalap’s chances of approval for dry eye disease. In a June 8, 2022 research report, he wrote, “From an FDA perspective, reproxalap is very safe, passes the Schirmer test with high significance, and has a novel mechanism of action in a field with underserved patients. We think that will be enough for approval.”

Newsletter writer Clive Maund said, in a November 1st posting, “Action since this candle looks like a tiny bull Flag suggesting renewed advance soon. Buyers here should place a stop below US$5.00.”

Reproxalap is also being evaluated for allergic conjunctivitis and is now in Phase 3.

2) ADX-2191: This intravitreal methotrexate injection is a Phase 2 developmental treatment for retinitis pigmentosa and primary vitreoretinal lymphoma. For the latter, Aldeyra has a pre-NDA meeting scheduled with the FDA this quarter.

Aldeyra intends for ADX-2191 to also prevent proliferative vitreoretinopathy (in Phase 3). Topline Phase 3 GUARD trial results suggest ADX-2191 treatment could be safer and more effective in this indication than compounded methotrexate, wrote Dr. Yale Jen, a Laidlaw & Co. analyst, in an Oct. 6, 2022 research note.

Jen also noted the current clinical package for ADX-2191 in proliferative vitreoretinopathy is “strong” and likely to support an NDA. To delineate the regulatory pathway forward for this, Aldeyra is scheduling a Type C meeting with the FDA for H1/23.

3) ADX-629. This orally administered RASP modulator is in Phase 2 clinical testing for the treatment of four immune-mediated diseases: ethanol toxicity, chronic cough, Sjögren-Larsson Syndrome, and minimal change disease.

Implications of Near-Term Catalysts

Because dry eye disease is a large, currently underserved market, FDA approval of reproxalap as a treatment for it would be a significant development for Aldeyra, BTIG analyst Shrader wrote.

Approval “could lead to a meaningful lift for the shares,” purported analyst Justin Kim in a Sept. 15 research report. His firm Oppenheimer rates Aldeyra Outperform.

Were reproxalap approved, Aldeyra could reach commercialization in 2023.

As for Aldeyra’s shares, they are currently “underexposed and undervalued,” according to Laidlaw‘s Dr. Yale Jen.

With respect to ADX-2191, positive GUARD trial results, and the pre-NDA meeting on primary vitreoretinal lymphoma, Kim noted, “could catalyze a nontrivial revenue opportunity relative to current share levels.”

As for Aldeyra’s shares, they are currently “underexposed and undervalued,” according to analyst Jen. Today Aldeyra’s share price is US$5.32, and it has been trading in the US$5 range since Sept. 20, 2022.

In comparison, Jen’s firm, Laidlaw & Co., has a US$30 per share target price on the biopharma; this represents a significant jump and return on investment from its share price today.

While Aldeyra’s cash position declined in the latest quarter, Jen noted in a November 11 research note that “ALDX ended 3Q22 with ~US$185M cash, enough to support its operations throughout 2023.” In the report, Laidlaw & Co. reiterated its Buy rating and said, “ALDX shares remain underexposed and under-valued.”

Institutions Dominate Ownership

Institutions held 68.43% of Aldeyra’s shares, the Top 3 being Perceptive Advisors LLC (16.98%), The Vanguard Group Inc. (4.18%), and Citadel Advisors LLC (3.97%). The No. 1 mutual fund holder was the Vanguard Total Stock Market Index Fund at 2.74%.

Aldeyra insiders, including Chief Executive Officer Dr. Todd Brady, Chief Development Officer Dr. Stephen Machatha, Chairman of the Board Dr. Richard Douglas, and several directors, together owned 2.36% of the company’s shares.

The Aldeyra investment opportunity is one that numerous biotech research analysts view favorably. As of them, Kim wrote, “Aldeyra’s late-stage ophthalmology pipeline in allergic conjunctivitis and dry eye diseases offers a favorable risk-reward to current share levels, coupled with long-term pipeline optionality from ADX-2191 in proliferative vitreoretinopathy and systemic RASP applications.”

Coverage and Share Structure

Aldeyra is followed by numerous analysts, including Wainwright & Co. analyst Matthew Caufield, BTIG’s Thomas Shrader, Dr. Yale Jen of Laidlaw & Co., and Justin Kim of Oppenheimer. Newsletter writer Clive Maund also follows the stock. Click “See More Live Data” in the data box above to read their reports.

Aldeyra Therapeutics’ market cap is US$320.78M. The company has 58.32 million shares outstanding, and it trades in a 52-week range of US$2.36 and US$9.06.

Disclosures: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with None. Please click here for more information.

3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Aldeyra Therapeutics Inc., a company mentioned in this article.

6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Nova Scotia-based nanotech company Meta Materials Inc. reports a major revenue increase just as it signs an agreement to help reduce the cost and weight of batteries for electric vehicles, extend their range, and improve their safety.

Analyst MacMurray Whale of Cormark Securities maintained a Buy rating on the stock.

Total revenue grew YOY in Q3 by 329% to US$2.5 million and 388% to US$8.8 million over the first nine months versus the same period in 2021.

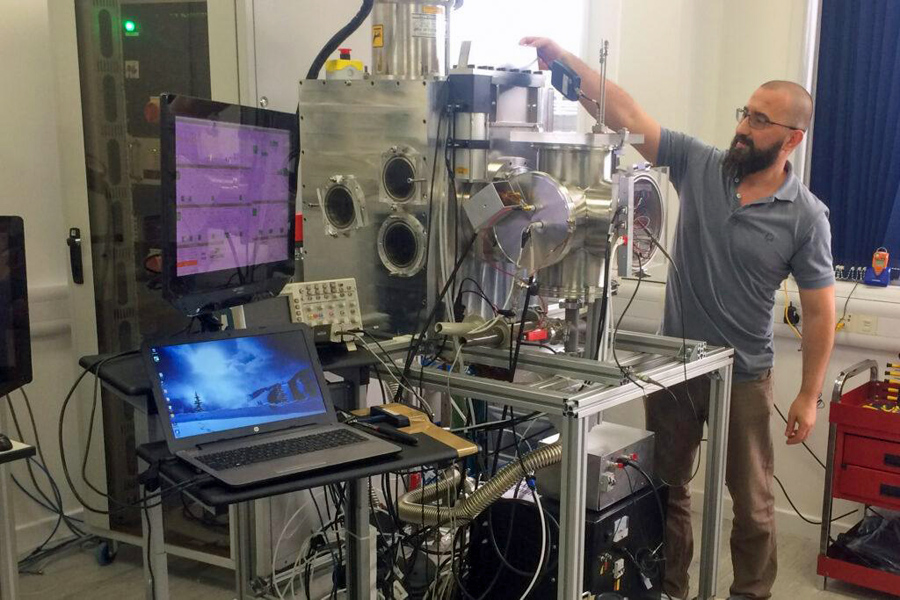

PLASMAfusion lab-scale tool. Source: Meta Materials Inc.

Analyst MacMurray Whale of Cormark Securities wrote in an updated note on Friday that the revenue increase was less than the US$3.4 million Cormark had predicted. However, he maintained a Buy rating on the stock, lowering the target to US$3.50 from US$5.

“We had expected indications of a more rapid ramp in volumes than we previously modeled but recognize the difficulty to model given the rapid changes in the EV space,” Whale wrote. “With the cash balance having declined to (US$31 million), the current quarterly spend gives a shorter runway than we had expected exiting the year.”

The company’s Q3 net loss increased to US$24.5 million, or 7 cents per share, on 362.2 million weighted average shares, compared to US$11.4 million, or 4 cents per share, on 280 million weighted average shares in Q3 2021.

But operating expenses also doubled YOY to US$23.9 million following several important acquisitions, the analyst pointed out.

“MMAT has many early-stage projects across a number of different verticals, most of which have not entered into commercial-scale production,” Whale stated.

The Catalyst

The largest part of the revenue increase was US$1.9 million from a deal with a confidential G10 central bank customer to develop anti-counterfeiting measures for currency, Whale said.

It’s part of an agreement with the bank for a maximum of US$41.5 million in development work over up to five years.

Metamaterials were first developed in the 1960s but only came into their own in the 2000s, when design and manufacturing capabilities caught up to the technology. The company is using them to develop nanotechnology products like self-deicing and defogging car and truck headlights and windows, see-through antennas, augmented reality glasses that look like regular glasses, and special eyewear that protects pilots’ eyes from laser strikes.

META is applying its futuristic technology to the communications, health and wellness, aerospace, automotive, and clean energy sectors.

The company has 472 active patent documents, of which 292 patents have been granted across all its technologies.

Big Strides in EV Battery Tech

Earlier this month, META announced it had entered a memo of understanding with DuPont Teijin Films and Mitsubishi Electric Europe to use Meta’s PLASMAfusion to scale a high-volume manufacturing system for film-based, coated copper current collectors.

The process reduces the amount of the red metal needed for EV batteries at a time when an upcoming copper shortage is threatening the transition to green energy, the company said.

“There has to be a better way,” META President, Chief Executive Officer, and founder George Palikaras said. “What we’re proposing here, and that’s part of the disruption, is that we have not only invented a way to make current collectors more efficient by reducing the copper content, but we have made an actual machine which we call PLASMAfusion.”

The agreement is focused on developing battery materials, such as coated copper current collectors and solid-state battery electrodes, META said. It will start with a pilot program and evolve into an industrial-scale mass production line.

META will provide the PLASMAfusion technology, DuPont Teijin Films will develop and supply polyester substrates, and Mitsubishi Electric Europe will contribute automation technology, expertise, and interface with machine builders.

“What’s very important here (is that) PLASMAfusion is very versatile,” Palikaras said. “It’s a platform technology with which we expect to increase productivity not only for batteries but also for nanoweb and other applications.”

Security Tech Set to Launch

The award from the G10 bank is part of an ongoing contract; META could not identify the bank for security reasons. But the company did say it was to work on the currency.

In addition to the US$4.3 million just announced, the bank already awarded the company a total of US$9.2 million.

The company said it is currently testing its anti-counterfeiting technology KolourOptik® Stripe and expects to launch it as early as the first quarter of 2023.

A blog on META’s site describes some of the security measures available through the technology, including images with omnidirectional movement, 3D depth, or holographic security patterns.

Those effects are “the exact visual triggers that millions of years of evolution have optimized human visual receptors to detect and respond to,” the company said. “Our toolkit of innovative nano-optic based visual effects to combat counterfeiting is available to brands and designers that are looking to build . . . extremely secure, custom solutions that (work) well with their brand.”

META also offers the technology for use on documents, smart packaging, and gift cards. The technology can also help prevent loss of life due to counterfeit medication.

Ownership, Coverage, and Share Structure

META had cash and cash equivalents of US$32.2 million in the third quarter and a burn rate of about US$6.5 million per month.

Major shareholders include Thomas Gordon Welch, with 6.64% or 24 million shares; Anne Barber Lambert, with 6.39% or 23.14 million shares; Lamda Guard Technologies Ltd., with 6.35% or 22.98 million shares; and State Street Global Advisors, with 3.54% or 12.82 million shares, according to Reuters. About 14% of META is held institutionally held.

The stock is covered by numerous analysts, including SingularResearch’s Christopher J. Sakai, ROTH Capital Partners’ Gerry Sweeney, as well as Cormark Securities’MacMurray Whale, and newsletter writer Clive Maund of Clivemaund.com. Click “See More Live Data” in the data box above to review more.

The company has a market cap of $473.6 million with 361.9 million shares outstanding, 267 million of them free-floating. It trades in a 52-week range of US$5.42 and US$0.63.

Disclosures: 1) Steve Sobek wrote this article for Streetwise Reports LLC. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. His/her company has a financial relationship with the following companies referred to in this article: None.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Meta Materials Inc. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

4) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Meta Materials Inc., a company mentioned in this article.

The company said the increase was driven by organic growth, scale in drone services activities, and increased aviation revenue.

Company officials said that the market for drones has remained strong as the war in Ukraine continues unabated and will continue to expand when it is over.

“Drones will have a major role to play in the reconstruction . . . of the country,” Volatus Chief Executive Officer Glen Lynch said during a conference call about the results on Monday. “The conflict in Ukraine literally changed the way countries around the world are looking at the use of drones and modern warfare. So, we’re responding to numerous opportunities right now for sales in NATO countries that are not currently engaged in fighting directly in the conflict in Ukraine. While I’m hopeful for peace and would be grateful if that was to happen overnight, we’re not seeing that happen anytime soon. And even if it does, we’re really looking at a fairly robust future for drones in the defense sector.”

Its target market is worth as much as US$58.4 billion, the company said.

Gross profit for the third quarter was CA$3.3 million, an increase of CA$2.6 million YOY, and the company has experienced a gross margin of 30%, an increase of 127 basis points over the second quarter of 2022.

Volatus serves the commercial and defense markets with integrated drone solutions using a network of more than 1,200 contract pilots across the Americas, providing imaging and security, equipment sales and support, and training.

It also offers aerial surveillance and monitoring of oil and gas pipelines. Its target market is worth as much as US$58.4 billion, the company said.

The company stated some of its accomplishments for the quarter include introducing a financing program for rapid drone adoption, demonstrating the remote operation of a drone from more than 3,000 kilometers away, entering into a strategic partnership with a radar company, and launching its Environmental Social Governance (ESG) program.

The company said the cash it had on hand as of Sept. 30 was about CA$6 million but raised an additional CA$4.2 million from an oversubscribed prospectus and private placement that closed on Oct. 6.

Ownership and Share Structure

Top shareholders in the company include the CEO Lynch with 26.62% or 38.46 million shares and Ian Alexander McDougall with 27% or 39 million shares, according to the company.

It has a market cap of CA$36.18 million with 113.9 million shares outstanding, 36 million of them free-floating. It trades in a 52-week range of CA$0.89 and CA$0.27.

Disclosures:

1) Steve Sobek compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports. They or members of their household own securities of the following companies mentioned in the article: None. His company has a financial relationship with the following companies referred to in this article: None.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Volatus Aerospace Corp. Please click here for more information.

3) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of the information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services, or securities of any company mentioned on Streetwise Reports.

4) From time to time, Streetwise Reports LLC and its directors, officers, employees, or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in the securities mentioned. Directors, officers, employees, or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Volatus Aerospace Corp., a company mentioned in this article.

Expert Clive Maund reviews the 6-month charts of nine companies he believes are worth keeping an eye on.

Aldeyra Therapeutics

After hitting a cyclical low back in February Aldeyra Therapeutics Inc. (ALDX:NASDAQ) rallied strongly to break clear above its 200-day moving average, which has now turned up.

After becoming very overbought early in August, it has reacted back in a normal manner towards this average above, which what looks like a base pattern has formed over the past six weeks.

With its volume pattern and volume indicators positive, it is in position to begin an uptrend, and the largish white candle about a week ago may mark the start of it.

Action since this candle looks like a tiny bull Flag suggesting renewed advance soon. Buyers here should place a stop below US$5.00.

Its volume pattern is positive, and its Accumulation line is strongly positive, with momentum (MACD) now swinging positive.

The initial target for an advance will be this year’s highs in the US$4.70 area, which is the upper boundary of the large trading range that has formed since last Spring.

Danavation Tech Corp.

A large Head-and-Shoulders bottom appears to be completing in Danavation Technologies Corp. (DVN:CSE; DVNCF:OTCQB), with the price having reacted back since August to what is believed to be the Right Shoulder low.

If so, it is at a great entry point here. The Accumulation line is very strong and making new highs despite the dip and with its MACD indicator below the zero line, it has plenty of upside potential from here.

It should start higher soon.

Buyers should place a stop at CA$0.244.

Data Communications Management Corp.

After a sharp rally early in August, Data Communications Management Corp. (DCM:TSX; DCMDF:OTCQX) has been moving sideways, consolidating in a pattern that resembles a bullish Rising Triangle that has allowed the 50-day moving average to catch up to the price which it is now nudging higher toward an upside breakout.

With volume indicators overall positive, momentum-swinging positive again, and moving averages in quite strongly bullish alignment, it is in a position to break into another upleg imminently.

Phenom Resources Corp.

Phenom Resources Corp. (PHNM:TSX.V; PHNMF:OTCQX; 1PY:FSE) has continued to strengthen since it was recommended on the site in the Market Notebook article of the 16th October, and a week ago, it advanced again on very strong volume that this time drove its Accumulation line sharply higher with its On-balance Volume line trending higher for months despite the price being in a downtrend.

The persistent heavy volume of the past month suggests that it is building up to something possibly big.

So we stay long and it remains a buy here and especially on any minor dips.

It attempted to break higher on an increased volume about a week ago, but with its 200-day moving average still dropping toward the price overhead, it was not quite ready. With the dip of recent days presenting us with a better entry point, this looks like a good time to buy.

There is a clear line of support at CA$0.50, so a good point to place stops would be at about CA$0.485.

Silver Hammer Mining Corp.

Silver Hammer Mining Corp. (HAMR:CSE; HAMRF:OTCQB) has been trundling sideways since June, marking out what is believed to be a low Pan base, especially given the now positive outlook for silver.

Whilst it could break lower from this pattern, this is only likely if a market crash forces the sector temporarily lower.

Otherwise, it looks set to break higher.

However, we should note that it may take some more time to do so, given that the falling 200-day moving average is still some way above the price. Positives are that the Accumulation line has held up quite well on the decline from the peak last April, and downside momentum (MACD) has dropped out.

Thought best for new buyers to wait to see if the price can hold in this area until the 200-day moving average has dropped down closer to the price, watching out for an influx of upside volume as a sign that it is ready to advance.

Slave Lake Zinc Corp.

Slave Lake Zinc Corp. (SLZ:CSE) popped higher on strong volume yesterday on good news out of the company that it deems it worthwhile to proceed with prospecting at O’Connor Lake.

With the company looking set to move forward, the move yesterday looks like the beginning of a new uptrend following the tedious downtrend from the highs of last April, and it is viewed as a speculative buy here and especially on any near-term dips.

Wealth Minerals

October saw a strong advance by Wealth Minerals Ltd. (WML:TSX.V; WMLLF:OTCQB) from a low at about CA$0.165 early in the month to touch CA$0.335 two weeks later. This impressive move was accompanied by persistent heavy upside volume, which is bullish.

Not surprisingly, this advance “hit the wall” when it became very overbought at a zone of quite strong resistance near a still falling 200-day moving average, so after several days of churning, it has dropped back over the past couple of days.

However, the volume pattern and volume indicators remain strongly positive, with volume dying right back as it has reacted, which suggests that it will soon turn higher again, so it is rated an immediate buy here.

CliveMaund.com Disclosures

The above represents the opinion and analysis of Mr. Maund, based on data available to him, at the time of writing. Mr. Maund’s opinions are his own, and are not a recommendation or an offer to buy or sell securities. Mr. Maund is an independent analyst who receives no compensation of any kind from any groups, individuals or corporations mentioned in his reports. As trading and investing in any financial markets may involve serious risk of loss, Mr. Maund recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction and do your own due diligence and research when making any kind of a transaction with financial ramifications. Although a qualified and experienced stock market analyst, Clive Maund is not a Registered Securities Advisor. Therefore Mr. Maund’s opinions on the market and stocks can only be construed as a solicitation to buy and sell securities when they are subject to the prior approval and endorsement of a Registered Securities Advisor operating in accordance with the appropriate regulations in your area of jurisdiction.

Disclosures: 1) Clive Maund: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: None. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Dakota Gold Corp., Danavation Technologies Corp., Data Communications Management Corp., Reliq Health Technologies Inc., and Wealth Minerals Ltd. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Danavation Technologies Corp. and Slave Lake Zinc Corp. Please click here for more information.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Aldeyra Therapeutics Inc., Dakota Gold Corp., Phenom Resources Corp., and Silver Hammer Mining Corp., companies mentioned in this article.

6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.