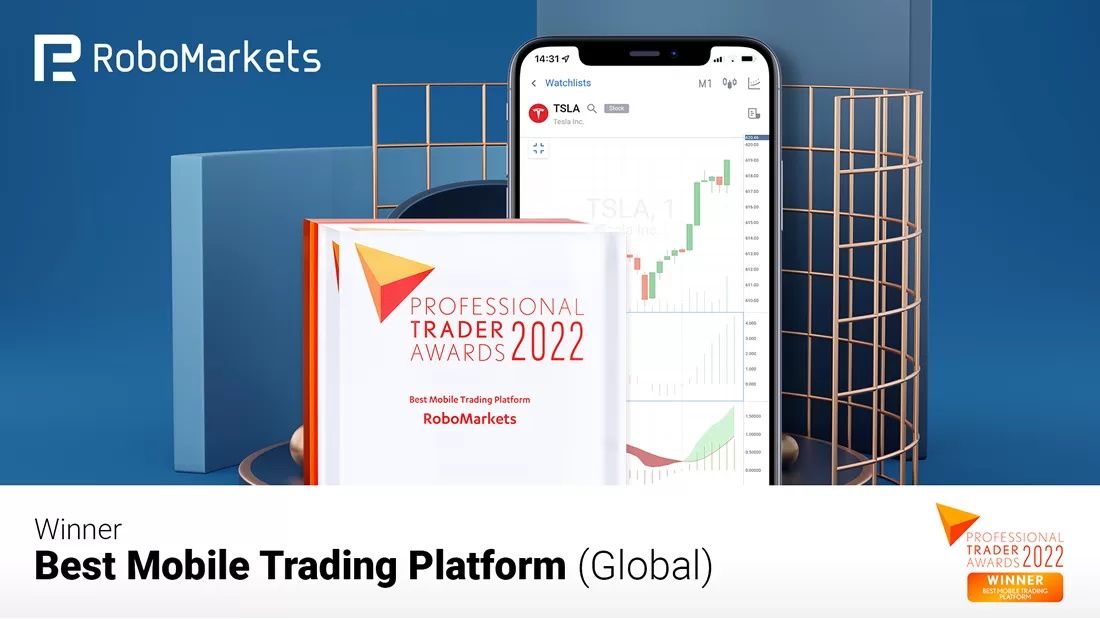

RoboMarkets, a European financial broker and developer of the R StocksTrader platform, proudly announces that its efforts have been acknowledged at the Professional Trader Awards event. The R StocksTrader mobile app was voted “Best Mobile Trading Platform-2022” globally. The winners were selected by the professional traders’ community.

The award winners companies were announced at a reception on 8 December 2022 in London. RoboMarkets has proudly earned the “Best Mobile Trading Platform” accolade for three consecutive years. This award is granted to the company that offers a top-tier mobile product to the market of professional trading accounts.

R StocksTrader is a brand-new trading platform, a powerful software for trading stocks and other financial instruments, featuring many added functions. The terminal makes available more than 12,000 trading instruments, allows for creating automated strategies, and more:

Access to the global markets from one platform

Minimal deposit of 100 USD

Leverage up to 1:20

3,000 stocks and 8,000 CFDs to choose from

Denis Golomedov, Chief Marketing Officer at RoboMarkets, comments: “We are extremely excited to receive this award, and would like to thank everyone who voted for us. Since the very start, we have focused on providing cutting-edge services to our clients, and this award reflects the result of our efforts. Our R StocksTrader mobile app offers direct access to the global financial markets from your mobile gadget from anywhere in the world. The app contains over 12,000 trading instruments, handy watchlists, a built-in corporate events calendar, analytics, and more. We constantly update the app, implementing solutions that enhance the trading functions of the platform, and improve risk control. Our team is truly engaged in providing users with an unhindered, cutting-edge trading experience.”

The winners of the Professional Trader Awards were selected after a three-stage process. Firstly, in the four weeks from 5 through 30 September, applications were filed to the organising committee by the brokers themselves, nominating their companies for the chosen award. Next, the organisers polled professional traders, who voted for their preferred nominees. Lastly, the winners of the Professional Trader Awards 2022 were announced after the final calculation of the votes.

About RoboMarkets

RoboMarkets is an investment company, operating under CySEC licence No. 191/13. RoboMarkets offers investment services in European countries by providing access to its proprietary trading platforms to traders who work on financial markets. Find out more about the Company’s products and activities on www.robomarkets.com.

Clinical-stage Algernon Pharmaceuticals’ multiple pipelines include testing a psychedelic for the treatment of stroke, and testing other drugs for idiopathic pulmonary fibrosis and chronic kidney disease.

Clinical-stage drug development company Algernon Pharmaceuticals Inc. (AGN:CSE; AGNPF:OTCQB; AGN0:XFRA) has multiple drugs in its pipeline and has garnered the support of AlphaNorth Asset Management, which now holds approximately 13% of the firm’s shares.

Why has the firm taken such a large position? AlphaNorth President and CEO Steve Palmer explained in a recent episode of Streetwise Live!: “We like it primarily because of the valuation. It’s quite cheap. Currently, the value of the whole company is CA$6–7 million. We also like it because they have multiple programs; I like companies like have multiple shots on goal, so to speak. And the trials that they are conducting are also lower risk than the typical biotech because they are using drugs that are already known to be safe.”

Analyst Andre Uddin with Research Capital Corporation follows the company and notes that Algernon has an “in-depth pipeline based on its novel repurposing drug development strategy.” He has calculated a CA$10.25/share target price on the company, an implied fourfold return based on the current share price of CA$2.78.

Multiple Pipelines

Algernon is about to begin testing the psychedelic compound DMT (N, N-dimethyltryptamine) for ischemic stroke, the type of stroke caused by blood clots blocking the flow of blood in the brain. The current treatment, tPA, must be administered within about three hours of the start of symptoms to be effective, a threshold that a large proportion of stroke victims don’t meet.

“The trials that they are conducting are also lower risk than the typical biotech,” said Steve Palmer of AlphaNorth Asset Management

The company has commenced screening subjects for the Phase 1 clinical study that will be conducted at the Centre for Human Drug Research in The Netherlands and expects to dose the first subject soon. Up to 60 healthy volunteers are expected to participate.

Algernon notes that the purpose of the study is to identify the “safety, tolerability, and pharmacokinetics of DMT when administered as an intravenous bolus followed by a prolonged infusion, for durations which have never been studied clinically. In addition, several pharmacodynamic measures believed to be associated with neuroplasticity, including both measurements of biochemical markers and electroencephalographic readings, will be recorded.”

“The potential of a stroke treatment drug is enormous,” Christopher Moreau, CEO of Algernon, stated. “On the human side, for approximately 85% of ischemic stroke patients, there is no treatment except to watch and hope. And on the market side, it is estimated to become a US$15 billion market by 2027, and so it’s truly global in scale and would have a huge impact on patients who suffer from this terrible injury.”

The company noted that its decision to investigate DMT and move it into human trials for stroke is “based on multiple independent, positive preclinical studies demonstrating that DMT, at a sub-psychedelic dose, helps promote structural and functional neuroplasticity. These are key factors involved in the brain’s ability to form and reorganize synaptic connections, which are needed for healing following a brain injury.”

Research Capital Corp. analyst Andre Uddin noted, “We believe AGN’s best asset is ifenprodil.”

“The preclinical data shows that DMT promotes the production of brain-derived neurotrophic factor, which is an important part of the brain’s recovery process after an injury like a stroke,” Moreau stated.

Because other Phase 1 studies have been completed on DMT, the company is not expecting any serious adverse events.

Algernon is also looking into DMT for additional indications. In late October, the company announced that it has entered into a clinical trial agreement with Yale University School of Medicine, New Haven, Conn., for the use of DMT in a Phase 2 depression study. “Although the treatment of psychiatric disorders with DMT [is] not the company’s current focus, we have patents pending on novel forms of DMT which could potentially be used across a broad range of diseases,” stated Moreau. “In addition, we believe the data generated from this study may help inform Algernon’s stroke research program.”

Orphan Drug Status for Ifenprodil for IPF

Algernon has received from the U.S. Food and Drug Administration Orphan Drug designation for Ifenprodil for the treatment of idiopathic pulmonary fibrosis (IPF). Orphan drug status is conferred on diseases that affect fewer than 200,000 patients in the U.S. and provides tax credits for trials and an exemption from user fees. If the drug receives FDA approval, seven years of market exclusivity are granted.

“We appreciate the U.S. FDA’s decision to grant ODD status to Ifenprodil for IPF, a disease for which prognosis remains dismal, with 50% mortality expected within three to four years,” said Moreau. “This regulatory milestone comes at an important time in the development of Ifenprodil as a potential new therapy for IPF as we plan the next steps for our clinical program.”

Technical analyst Clive Maund of CliveMaund.com recently charted Algernon’s stock and rated the stock a Buy.

Algernon’s Phase 2a study of Ifenprodil in patients recently concluded and met its co-primary endpoint “with patients receiving Ifenprodil experiencing no worsening of their lung function, and significant improvements were seen in the frequency of their IPF-associated cough as well. In addition, improvements in patient-reported measures of cough severity and quality of life were observed. Ifenprodil was also confirmed to be safe and well-tolerated in the study.”

Research Capital Corp. analyst Andre Uddin noted, “We believe AGN’s best asset is ifenprodil for treating refractory chronic cough (RCC) in idiopathic fibrosis (IPF)/IPF patients. . . Based on the positive Phase 2a data, we expect management to advance its 3x per day formulation of ifenprodil and initiate a Phase 2b trial in chronic cough H2 CY2023. A data set from a Phase 2b chronic cough trial would potentially be a large value-creating inflection point.”

Catalyst: Company Will Begin Testing For Chronic Kidney Disease Drug

The company plans to begin testing repirinast, a drug sold for 25 years in Japan for asthma, for chronic kidney disease. Analyst Uddin noted that Algernon “expects to begin conducting a Phase 1 study using repirinast to treat CKD in calendar year Q2 2023.”

Analysts and Expert Coverage

Technical analyst Clive Maund of CliveMaund.com recently charted Algernon’s stock and rated the stock a Buy. He wrote in October that “those interested should aim to buy it as soon as possible.”

Chris Temple of The National Investor also commented on the stock in a September post, saying that he considered the company an Immediate Buy.

The stock is also covered by analyst Dr. André Uddin of Research Capital Corp. and newsletter writers Gerard Adams of The National Inflation Association, Bob Moriarty of 321gold.com, and Penny Queen of Pennyqueen.com.

Click “See More Live Data” in the data box above to read more of what they are saying.

Ownership and Share Structure

AlphaNorth Asset Management is Algernon’s largest shareholder owning 13.46% of Algernon’s shares.

Algernon has approximately 2.3 million shares outstanding and 3.6 million fully diluted. It trades on the Canadian Securities Exchange under the ticker AGN and under the ticker AGNPF on the U.S. OTCQB platform.

Disclosures: 1) Patrice Fusillo wrote this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Algernon Pharmaceuticals Inc. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Algernon Pharmaceuticals Inc. Please click here for more information.

3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Algernon Pharmaceuticals Inc., a company mentioned in this article.

6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Research Capital Corporation disclosures:

1. This Issuer has generated investment banking revenue for RCC.

Analyst Certification I, Andre Uddin, Ph.D., certify the views expressed in this report were formed by my review of relevant company data and industry investigation, and accurately reflect my opinion about the investment merits of the securities mentioned in the report. I also certify that my compensation is not related to specific recommendations or views expressed in this report. Research Capital Corporation publishes research and investment recommendations for the use of its clients. Information regarding our categories of recommendations, quarterly summaries of the percentage of our recommendations which fall into each category and our policies regarding the release of our research reports is available at www.researchcapital.com or may be requested by contacting the analyst. Each analyst of Research Capital Corporation whose name appears in this report hereby certifies that (i) the recommendations and opinions expressed in this research report accurately reflect the analyst’s personal views and (ii) no part of the research analyst’s compensation was or will be directly or indirectly related to the specific conclusions or recommendations expressed in this research report.

CliveMaund.com disclosures:

Clive Maund has not been paid by the company and does not own shares of Algernon.

With the need for counterdrone technologies rising, Australian and U.S.-based DroneShield Ltd. has released a lot of news. Read more to learn about the company’s myriad of orders, the DOD recommendation, and the recent million-dollar placement.

Australian and U.S.-based tech company DroneShield Ltd. (DRO:ASX; DRSHF:OTC) has been making many moves lately. Along with an influx of orders over the past two months, the company has also secured a recommendation from the Depart of Defense (DOD) and a AU$3.7 million placement.

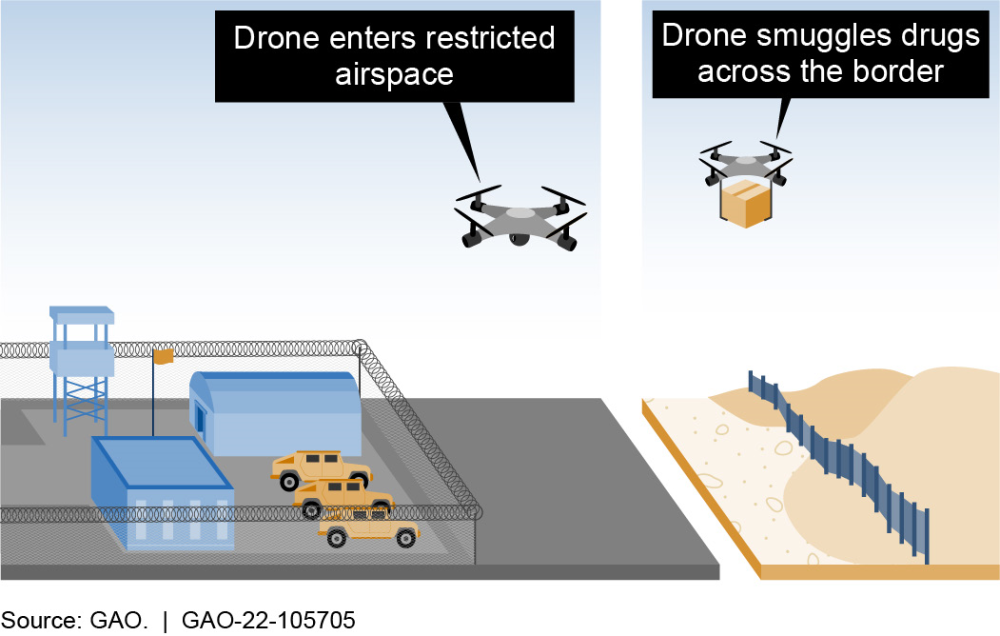

DroneShield offers what is known as counterdrone systems, which can interfere with or disable remote-controlled ground surveillance drones during operation and while in flight.

Due to the practical application of drones in modern warfare, the counterdrone technology marketed by DroneShield has attracted the attention of major military electronic warfare organizations, such as the ISREW branch of the Australian Joint Systems Division, The United States Department of Defense, and the Department of Homeland Security.

Why Is Counterdrone Technology Taking Off?

While drones can be extremely useful, they can also pose serious threats. They can be used for drug smuggling, interfere with planes if they are used in airspace near airports, or uncover secure data that should not be released. Because of this, it is imperative we have the technology to counter them by jamming their signal or taking them down completely, and this has become more important now than ever.

Figure 2. In this example, a critical site detects an unauthorized UAS nearby. An interference signal jams the connection between the UAS and its operator to reroute the UAS away from the site.

National Defense Business and Technology Magazine reported that Meni Deutsch, the regional director for Europe at Skylock Anti-Drone Technologies, said, “We have been witnessing the growing demand for anti-drone systems and technologies.”

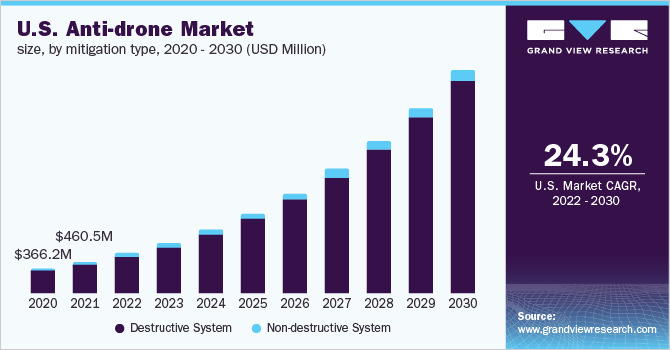

This demand has led to massive projected growth. The counterdrone market was already at “US$1.1 billion in 2021 and is anticipated to register a CAGR [compound annual growth rate] of 28.3% from 2022 to 2030,” which could provide ample opportunity to investors.

As for DroneShield, the company “differentiates itself from the rest of the market by offering an end-to-end counterdrone solution with largely in-house technology,” Daniel Laing of Bell Potter Securities wrote in a September report.

A Plethora of Orders

DroneShield has also identified critical markets for its counterdrone technology in correctional facilities, government offices, and airport security.

Laing of Bell Potter identified “the deployment of its technology at U.S. military bases following the U.S. DOD recommendation” as a “key catalyst for DroneShield’s projected growth.”

Airports have been on the watch for technology to counter drones. That need was amplified after several incidents, one being the 2018 Gatwick affair, where one of the U.K.’s most popular airports had to suspend all travel after multiple drones were sighted along its airfield.

Since then, “stakeholders at airports all over the world have called for a solution that can identify unauthorized drones — while complying with laws that generally prohibit interference with aircraft,” reported DroneLife.

This led to DroneShield’s August 2022 announcement of its first permanent deployment of DroneSentry at a U.S. airport. You can see a video demonstration of how the Sentry works here.

Then on October 25, 2022, the company received a AU$900,000 order contract for portable counterdrone systems for an undisclosed Asian country. This led to the company trading 2.56% higher on the announcement day.

Last month, DroneShield also announced it would receive AU$1 million from an unnamed international government agency. In this order, the company would provide several of its DroneSentry-X units. DroneSentry-X is vehicle compatible counterdrone device. You can read more details about it here and see a video demonstration of the product through this link.

Payment and shipment are expected before the end of the quarter. The company reported that “for this customer, it is an initial purchase that follows trials, and is expected to follow up with a number of additional systems, to be acquired in 2023.”

First Catalyst: U.S. DOD Recommendation

As the need for countdown technology intensifies, the department of defense has decided to spend at least US$668 million on counterdrone research and development and at least US$78 million on the acquisition by the 2023 fiscal year.

Technical Analyst Clive Maund rated the company an Immediate Buy and said, “with the outlook for orders and earnings improving dramatically, it is clear that there is everything to go for here.”

Along with this, the DroneShield happily unveiled it had been recommended by the U.S. DoD’s Joint Counter-small Unmanned Aircraft Systems Office (JCO) as part of the Science Applications International Corporation (SAIC) joint solution for Counter-UAS as a Service (CaaS).

CEO and managing director Oleg Vornik told Streetwise Reports that DroneShield is proud to have this recommendation and that they “look forward to installations next year as now [the] recommendation has been made to implement the rollout of counter drone systems across the U.S.”

Laing of Bell Potter identified “the deployment of its technology at U.S. military bases following the U.S. DOD recommendation” as a key catalyst for DroneShield’s projected growth.”

These inroads maintained with major government organizations have established the “validation of the sales pipeline through consistent contract wins,” which Laing claims to be an additional, concurrent catalyst for DroneShield’s sustained growth in other sectors.

Second Catalyst: Placement With Epirus

DroneShield also unveiled the organization of a placement of 18.5 million shares with technology investment firm Epirus Inc.

Epirus Inc., named after the unending arrows of the Greek hero Theseus, is a technology company that creates software-defined directed energy systems, which are used to counter electronics from various ranges.

Gavegan of Peloton Capital projects that the funding received from Epirus will contribute toward “the scaling up of engineering and operations in support of current momentum.”

Vornik spoke with Streetwise Reports about the deal, saying that DroneShield and Epirus have been working together for a while now. This is due to their complementary technologies, as DroneShield focuses on drone detection while Eprius focused on defeating drones through high-powered microwave weapons systems.

According to Peloton Capital, the market volume saturation resulting from this deal “represents a discount of 2.4% to the last closing price of AU$0.21 per share.”

At around AU$0.20 per share, Epirus’s placement has provided DroneShield an additional AU$3.7 million in operating capital. Peloton reports that this deal grants Epirus a 4.1% shareholder stake in the upstart Australian counterdrone company.

Shane Gavegan of Peloton Capital noted that DroneShield plans to direct this incoming investment capital toward “the scaling up of ready inventory and long lead items to rapidly fulfill anticipated orders.”

Analysts and Newsletter Commentary

DroneShield is covered by a surfeit of analysts, including Finola Burke of RaaS Advisory Pty Ltd., and previously mentioned Daniel Laing of Bell Potter Securities Ltd., and Shane Gavegan of Peloton Capital.

Laing suggested an estimated “AU$50 million worth of projects for 2022 and about AU$180 million worth for next year and further out” to be fulfilled by DroneShield — a matter of bolstering its supply to meet steady demand. The company, according to Laing, is well positioned to “capitalize on favorable macroeconomic conditions accelerating structural growth in the market.”

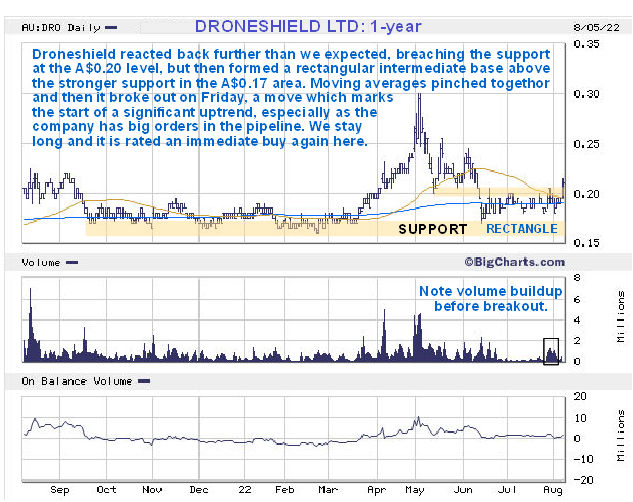

Charts courtesy of bigcharts.com

There is also evidence to suggest that this demand for DroneShield’s military technology will grow considerably in the coming quarters, where Gavegan projects that the funding received from Epirus will contribute toward “the scaling up of engineering and operations in support of current momentum.”

This momentum is echoed in the words of Peloton analyst Darren Odell, who noted that the counterdrone company is “currently selling its systems in the Five Eyes countries, the Middle East, and Ukraine.”

Technical analysts Clive Maund also commented on the stock in an August 9, 2022, post.

There Maund said, “the fundamentals of the company have continued to improve at an ever more rapid rate.”

He rated the company an Immediate Buy and said, “with the outlook for orders and earnings improving dramatically, it is clear that there is everything to go for here.”

Both Peloton and Bell Potter also maintain their Buy recommendations on DroneShield.

Click “See More Live Data” in the data box above to view more of what they are saying.

Ownership and Share Structure

Approximately 11% of DroneShield’s stock is owned by management, with CEO Oleg Vornik claiming 15.3 million shares at a majority stake of 3.39%. Other internal stakes are maintained by CFO Carla Balanco at 3.2 million shares, as well as board member Peter James with 9.3 million.

Without any institutional shareholders, the remaining 89% of DroneShield’s outstanding shares are retail.

By the end of the September quarter, the company had a cash balance of AU$7.5 million, along with the AU$3.7 million from Epirus. They ended the quarter slightly cash flow positive and expect to either break even or be cash flow positive this quarter.

A micro-cap, DroneShield currently boasts an approximate AU$90 million market cap on 432 million outstanding shares spread across more than 8,000 investors. Approximately 378 million shares are free-floating. In addition, as noted by analyst Daniel Laing of Bell Potter Securities, DroneShield operates without bank debt and has an estimated AU$7 million in cash available as capital expenditure.

It currently has 451.04 million shares outstanding and trades in the 52-week range between AU$0.188 and AU$0.20.

Disclosures: 1) Katherine DeGilio and Tom Griffin wrote this article for Streetwise Reports LLC and Tom Griffin provides services to Streetwise Reports as an independent contractor. They members of their household own securities of the following companies mentioned in the article: None. They or members of their household are paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with DroneShield Ltd. Please click here for more information.

3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of DroneShield Ltd., a company mentioned in this article.

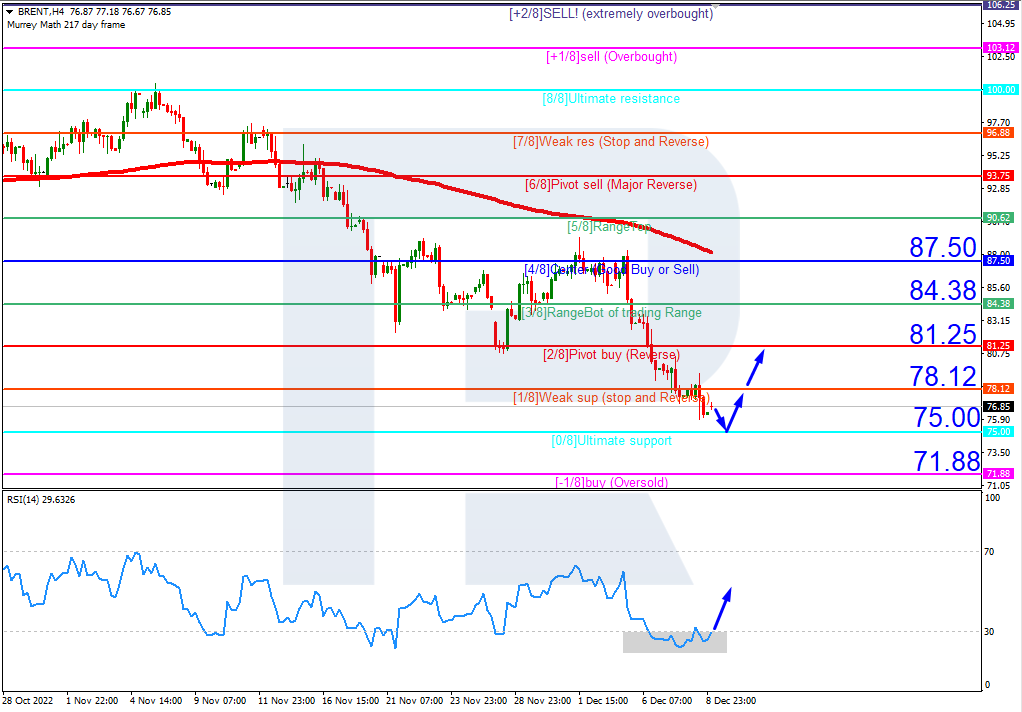

On H4, the quotes of Brent oil are below the 200-day Moving Average, which indicates the prevalence of a downtrend. However, the RSI is already in the oversold area. A test of 0/8 (75.00) should be expected, followed by a bounce off it and growth to the resistance level of 2/8 (81.25). The scenario can be cancelled by a downward breakaway of the support level of 0/8 (75.00). In the case, the quotes may fall to -1/8 (71.88).

On M15, the upper line of VoltyChannel is too far away from the current price, which means growth of the quotes will be initiated by a bounce off 0/8 on H4.

S&P 500

On H4, the S&P 500 quotes have dropped under the 200-day Moving Average again, indicating a downtrend. The RSI is testing the resistance line. In the end, a downward breakaway of the support level of 1/8 (3906.2) should be expected, followed by falling to 0/8 (3750.0). The scenario can be cancelled by rising over the resistance level of 2/8 (4062.5). This might lead to a trend reversal and growth of the quotes to 3/8 (4218.8).

On M15, an additional signal confirming the decline will be a bounce off the lower line of VoltyChannel.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

Prometheus Biosciences Inc. shares traded 170% higher to a new 52-week intraday high after the company reported positive results from two separate Phase 2 clinical studies for its PRA023, an anti-TL1A mAb used to treat inflammatory bowel disease. The company is actively planning to advance PRA023 into Phase 3 trials as a prospective treatment for ulcerative colitis and Crohn’s disease in FY/23.

Clinical-stage biotech company Prometheus Biosciences Inc. (RXDX:NASDAQ), which is engaged in the discovery, development, and commercialization of medicines for use in the treatment of immune-mediated diseases such as inflammatory bowel disease (IBD), today announced “results from its ARTEMIS-UC Phase 2 and APOLLO-CD Phase 2a studies of PRA023 demonstrating strong efficacy and favorable safety results in both studies.”

The firm advised that based upon the data collected during both of these independent Phase 2 trials, it plans to initiate discussions with regulators to move forward with two additional Phase 3 studies of PRA023 in FY/23 for the treatment of Crohn’s disease (CD) and ulcerative colitis (UC).

Prometheus advised that in its Phase 2 ARTEMIS-UC trial, “PRA023 met the primary and all ranked secondary endpoints including clinical, endoscopic, histologic, and patient-reported outcome measures in the initial cohort (Cohort 1) of the trial.”

In the double-blind, randomized ARTEMIS-UC trial, 135 patients with moderate-to-severely active UC who did not respond to prior therapies were treated over a period of 12 weeks with either PRA023 or placebo. The topline data showed that 26.5% of patients on PRA023 successfully achieved the predetermined primary endpoint of clinical remission versus just 1.5% in the control group. Additionally, 36.8% of the patients who receive PRA023 met the key secondary endpoint of endoscopic improvement, compared to 6.0% for those who were administered a placebo.

RXDX shares opened almost 200% higher today at US$105.07 (+US$69.01, +191.38%) over yesterday’s US$36.06 closing price and reached a new 52-week high price this morning of US$111.99.

The firm also reported positive findings in its Phase 2a APOLLO-CD trial, which enrolled a total of 55 patients diagnosed with a moderate-to-severely active CD with endoscopically active disease who also had failed other standard treatment regimens.

Results from the APOLLO-CD study demonstrated that 26.0% of patients who received PRA023 achieved endoscopic response versus the historical average placebo rate of 12%. In addition, 49.1% of trial participants’ patients administered PRA023 achieved clinical remission, compared to the historical placebo group rate of 16%.

Prometheus Biosciences’ Chairman and CEO Mark McKenna commented, “We are beyond enthusiastic with these study results and what they could mean for patients suffering from IBD. The performance of PRA023 in both UC and Crohn’s patients has surpassed our expectations . . . We believe PRA023 and our precision medicine approach [have] the potential to change the paradigm of IBD treatment, and we look forward to discussions with regulatory agencies as we prepare to advance into Phase 3 studies in Ulcerative Colitis and Crohn’s Disease.”

The company’s Chief Medical Officer Allison Luo, M.D. remarked, “PRA023 has clearly demonstrated clinical proof-of-concept in CD and remarkable efficacy for the treatment of UC . . . We look forward to further evaluating PRA023 in Phase 3 studies with the goal of bringing this promising candidate to the market.”

The firm explained that “PRA023 is an IgG1 humanized monoclonal antibody that has been shown to block tumor necrosis factor (TNF)-like ligand 1A (TL1A).” The company indicated that PRA023 shows the potential to substantially improve outcomes for patients with moderate-to-severe IBD in those persons predisposed to increased TL1A expression. In addition to prospective uses in the treatment of UC and CD, Prometheus is also investigating and developing PRA023 for use in treating systemic sclerosis-associated interstitial lung disease (SSc-ILD).

Prometheus Biosciences is a clinical-stage biotechnology firm based in San Diego, Calif., that is focused on discovering, developing, and commercializing novel therapeutics to treat immune-mediated diseases. The firm has created a precision medicine platform called Prometheus360™, which utilizes machine learning technology to query gastrointestinal bioinformatics databases to identify potential new therapeutic targets. The firm’s activities were initially focused mostly on gastrointestinal (GI) diseases such as IBD, but it is now expanding its efforts to target other autoimmune diseases.

Prometheus Biosciences started off the day with a market cap of around US$1.51 billion, with approximately 41.94 million shares outstanding and a short interest of about 11.6%. RXDX shares opened almost 200% higher today at US$105.07 (+US$69.01, +191.38%) over yesterday’s US$36.06 closing price and reached a new 52-week high price this morning of US$111.99. The stock has traded today between US$95.50 and US$111.99 per share and is currently trading at US$97.82 (+US$61.76, +171.27%).

Disclosures:

1) Stephen Hytha wrote this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees.

3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

So much for the conventional wisdom of the “balanced portfolio”

By Elliott Wave International

In his February 2022 book, Last Chance to Conquer the Crash, Robert Prechter said:

Countless advisors have counseled “diversification,” a “balanced portfolio” and other end-all solutions to the problem of allocating your investments. These approaches are delusional. … No investment strategy will provide stability forever.

That certainly has applied to the classic 60% stocks / 40% bonds portfolio this year.

On Oct. 14, a Reuters headline said:

’60/40′ Portfolios Are Facing Worst Returns in 100 Years: BofA

Of course, everyone knows that stocks are risky, but many investors expect bonds to provide a cushion in case equities slide into a downtrend. And, indeed, the stock market has been trending lower since January.

But bond prices have taken a hit, too. A BIG one. As you probably know, bonds prices decline when yields rise and that’s what’s taken place.

You may find it hard to believe, but Elliott wave patterns and sentiment readings in the bond markets warned of this. For example, the July 2021 Elliott Wave Theorist, a monthly publication (since 1979) which analyzes financial markets and major cultural trends, showed this chart and said:

U.S. Treasury bill rates have edged closer and closer to zero for over a year. The complacency about the nonexistent T-bill yield in the face of unprecedented inflating by the government and the Fed is truly amazing. … The Fed’s cavalier inflating is borne of optimism. … When optimism and complacency finally melt like popsicles in the sun, the lines in [the chart] will turn up.

During that same month / year (July 2021), The New York Times ran this headline:

Federal Reserve Officials Project Rate Increases in 2023 [emphasis added]

This next chart of the 6-month U.S. Treasury bill yield, which published in the Nov. 18, 2022 Elliott Wave Theorist, shows what we all know: Rates began to turn up more than a year before 2023 and then soared higher.

The question now is: What’s next?

Elliott wave analysis answered this question before, and it can help you answer it now.

You can read more about what Elliott Wave Theorist editor, and EWI Founder, Robert Prechter expects next in the Special Report: Preparing for Difficult Times. The report is free — for a limited time — inside their “12 Days of Elliott” event. You need only join Club EWI to read it, along with 11 other fascinating resources, December 1-12.

You can join Club EWI without any cost or obligation. All the while, you’ll enjoy complimentary access to an abundance of Elliott wave resources on financial markets and investing.

Get started by following the link: 12 Days of Elliott — get free and instant access.

This article was syndicated by Elliott Wave International and was originally published under the headline 60% stocks, 40% bonds? Ha!. EWI is the world’s largest market forecasting firm. Its staff of full-time analysts led by Chartered Market Technician Robert Prechter provides 24-hour-a-day market analysis to institutional and private investors around the world.

Summit Therapeutics Inc. shares traded 194% higher yesterday after the company reported it entered into an in-license agreement with Akeso Inc. for its breakthrough bispecific antibody ivonescimab, which combines a blockade of PD-1 with an anti-VEGF into a single molecule designed to target cancer. Summit has agreed to pay Akeso an upfront payment of US$500 million, which it plans to finance via an equity rights issuance.

Biopharmaceutical companySummit Therapeutics Inc. (SMMT:NASDAQ; SUMM:LON), which is engaged in the discovery, development of, and commercialization of medicines for infectious diseases, cancer, and other unmet medical needs, yesterday announced that it entered into a definitive partnership agreement with Akeso Inc. (9926.HK) to in-license its breakthrough bispecific antibody, ivonescimab.

Summit Therapeutics explained that ivonescimab, known as AK112 in China and Australia and SMT112 in the U.S, Canada, Europe, and Japan, is “a novel, potential first-in-class bispecific antibody combining the power of immunotherapy via a blockade of PD-1 with the anti-angiogenesis benefits of an anti-VEGF into a single molecule.”

The report indicated that ivonescimab is believed to be the most advanced PD-1 / VEGF bispecific antibody advanced in clinical studies, though to date, neither the U.S Food and Drug Administration (FDA) nor the European Medicines Agency (EMA) have granted approval for any PD-1- based bispecific antibodies. Summit mentioned that ivonescimab has received Breakthrough Therapy Designation status in China from The National Medical Products Administration (NMPA) for three separate indications relating to non-small cell lung cancer (NSCLC).

The agreement will provide Summit with the rights to advance, market, and commercialize SMT112 (ivonescimab) in the U.S, Canada, Japan, and Europe, with Akeso retaining the rights to develop and sell ivonescimab in China, Australia, and all other areas except for those assigned to Summit. The report stated that Akeso is considered to be a pioneer and source originator in creating and developing novel antibodies and that the in-license arrangement with Summit will allow it to advance its goals of becoming a global biopharma firm.

For its part, Summit will make an upfront payment in the amount of US$500 million to Akeso. Akeso will be eligible to receive up to an additional US$4.5 billion if certain regulatory and commercial milestones are achieved, along with low double-digit royalties on net sales.

The offering is expected to provide the company with gross proceeds of up to US$500 million, which it plans to utilize to pay its upfront payment to Akeso, support clinical development and regulatory approval for SMT112, and expand its drug pipeline.

Summit Therapeutics’ Chairman and CEO Robert W. Duggan commented, “The partnership between Summit Therapeutics and Akeso is a strategically compelling opportunity . . . We are extremely encouraged by ivonescimab and the potential for improving the quality and duration of patients’ lives based on clinical data to support this point.”

Akeso’s Co-founder, Chairwoman, CEO, and President, Dr. Michelle Xia, stated, “Ivonescimab has demonstrated the potential to deliver superior clinical benefit for patients and tremendous value for investors . . . The Akeso team has been dedicated to the development of ivonescimab for the past eight years and proudly advanced the molecule to the clinical Phase 3 stage. The global value of ivonescimab awaits great work from a great team to realize.”

“We look forward to the swift execution of the clinical development and commercial plan in a global setting for ivonescimab,” Xia added.

Summit Therapeutics advised that in a Phase 2 NSCLC trial that included patients with failed EGFR-TKI’s, those treated with ivonescimab demonstrated “an overall response rate (ORR) of 68.4% and a median Progression-Free Survival (mPFS) time period of 8.2 months when combined with combination chemotherapy (pemetrexed and carboplatin) as compared to historical mPFS of 4.3 months in patients treated with combination chemotherapy (pemetrexed and platinum-based chemotherapy) alone.”

Ivonescimab is now being developed in China and Australia for use in treating multiple solid tumors and is currently being evaluated in a Phase 3 clinical trial in patients with NSCLC that is positive for an epidermal growth factor receptor (EGFR) mutation and whose disease has progressed after treatment with an EGFR tyrosine-kinase inhibitor (TKI).

Co-CEO, President, and Summit Board Member Maky Zanganeh remarked, “We have found the ideal partnership with the potential to change the paradigm for treating patients facing difficult odds with devastating diagnoses . . . 10 years ago, metastatic lung cancer patients rarely survived for more than ten to twelve months from diagnosis. Today, survival can be measured in years.”

Summit advised that it intends to finance its obligations under the agreement by the issuance of a rights offering that will allow its common shareholders of record to purchase non-transferable subscription rights to buy common shares at the lesser of US$1.05 per share or the five-day volume weighted-average price of its shares prior to the date of the transaction. The offering is expected to provide the company with gross proceeds of up to US$500 million, which it plans to utilize to pay its upfront payment to Akeso, support clinical development and regulatory approval for SMT112, and expand its drug pipeline.

Summit Therapeutics is a biopharmaceutical firm headquartered in Menlo Park, Calif. The company is engaged in discovering, developing, and commercializing medicines to treat cancer, infectious and other diseases with high unmet needs. The firm is highly focused on developing SMT112 (ivonescimab), which was engineered to combine two well-established oncology-targeted mechanisms of action. Initially, the company’s SMT112 development efforts at being directed at treating NSCLC. Summit plans to begin treating patients in clinical studies by Q2/23.

Akeso is a biopharma company engaged in the discovery, development, manufacturing, and marketing of medicines designed to address high unmet medical needs worldwide. The company’s pipeline includes more than 30 assets that are being developed to treat cancer, autoimmune disease, inflammation, metabolic disease, and other therapeutic areas. To date, 17 of these product candidates have been advanced into clinical trials. Akeso’s Kaitanni (cadonilimab) received approval from China’s NMPA in June 2022 for use in the treatment of relapsed or metastatic cervical cancer in patients who progressed on or after platinum-based chemotherapy making it the first commercialized PD-1-based bispecific drug globally.

Summit Therapeutics started off the day yesterday with a market cap of around US$158.0 million with approximately 201.3 million shares outstanding. SMMT shares opened 68% higher yesterday at US$1.32 (+US$0.535, +68.15%) over the previous day’s US$0.785 closing price. The stock traded yesterday between US$1.19 and US$1.59 per share and closed for trading at US$1.54 (+US$0.755, +96.18%).

Disclosures:

1) Stephen Hytha wrote this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees.

3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

To achieve this end, the board of trustees is currently weighing various options, noted an Echelon Capital Markets report.

The Firm Capital Apartment REIT (FCA.U:TSX.V) posted a year-over-year AFFO/unit, or adjusted funds from operation per unit, gain in Q3/22 and during the quarter, commenced a strategic review, reported Echelon Capital Markets analyst David Chrystal in a Nov. 15 research note. Firm Capital invests in U.S. multifamily properties, owns assets and interests in joint venture investments, and provides debt financing.

The Canada-based real estate investment trust’s Q3/22 AFFO/unit was US$0.09, a 7% increase over Q3/21, Chrystal relayed. The figure beat Echelon’s estimate of US$0.06 due to a foreign exchange gain.

Target Price Decreased

However, Echelon reduced its target price on the REIT to US$7 per share from US$7.50, following the release of its Q3/22 results, to reflect writedowns carried out during the quarter on certain investments. The trust’s current share price is about US$4.67.

“Given the current capital market environment, a significant NAV discount is likely to persist under the trust’s current structure,” wrote Chrystal.

The target price could be raised in the future, Chrystal noted, if First Capital were to divest certain assets at an international financial reporting standards net asset value (NAV) of US$8.44 per unit.

This is because Echelon predicts near-term “incremental impairment of certain assets in the trust’s Northeast markets, where operations remain challenged due to regulatory issues delaying evictions and collections.”

Strategic Review Underway

The REIT’s board of trustees, in fact, may decide, during its strategic review, to dispose of some assets. The objective of the review is to “identify, evaluate and pursue potential strategic alternatives aimed at maximizing unitholder value,” Chrystal relayed.

Other options under consideration include effecting some type of merger or acquisition, privatizing, and changing the business to a real estate merchant bank or value-add model.

“Given the current capital market environment, a significant NAV discount is likely to persist under the trust’s current structure,” wrote Chrystal.

Distributions Paused

The analyst pointed out that while the review, in progress, is taking place, distributions by the REIT are and will remain on hold.

“A quarterly review will determine if the trust will allocate capital to unitholder distributions, unit repurchases, or reinvestment,” Chrystal added.

Echelon maintained its Buy rating on the First Capital Apartment REIT.

Disclosures: 1) Doresa Banning wrote this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures For Echelon Wealth Partners Inc., Firm Capital Apartment REIT, November 15, 2022

Echelon Wealth Partners Inc. is a member of IIROC and CIPF. The documents on this website have been prepared for the viewer only as an example of strategy consistent with our recommendations; it is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any particular investing strategy. Any opinions or recommendations expressed herein do not necessarily reflect those of Echelon Wealth Partners Inc. Echelon Wealth Partners Inc. cannot accept any trading instructions via e-mail as the timely receipt of e-mail messages, or their integrity over the Internet, cannot be guaranteed. Dividend yields change as stock prices change, and companies may change or cancel dividend payments in the future. All securities involve varying amounts of risk, and their values will fluctuate, and the fluctuation of foreign currency exchange rates will also impact your investment returns if measured in Canadian Dollars. Past performance does not guarantee future returns, investments may increase or decrease in value and you may lose money. Data from various sources were used in the preparation of these documents; the information is believed but in no way warranted to be reliable, accurate and appropriate. Echelon Wealth Partners Inc. employees may buy and sell shares of the companies that are recommended for their own accounts and for the accounts of other clients.

Echelon Wealth Partners compensates its Research Analysts from a variety of sources. The Research Department is a cost centre and is funded by the business activities of Echelon Wealth Partners including, Institutional Equity Sales and Trading, Retail Sales and Corporate and Investment Banking.

U.S. Disclosures: This research report was prepared by Echelon Wealth Partners Inc., a member of the Investment Industry Regulatory Organization of Canada and the Canadian Investor Protection Fund. This report does not constitute an offer to sell or the solicitation of an offer to buy any of the securities discussed herein. Echelon Wealth Partners Inc. is not registered as a broker-dealer in the United States and is not be subject to U.S. rules regarding the preparation of research reports and the independence of research analysts. Any resulting transactions should be effected through a U.S. broker-dealer.

ANALYST CERTIFICATION

Company: Firm Capital Apartment REIT | FCA.U-TSXV

I, David Chrystal, hereby certify that the views expressed in this report accurately reflect my personal views about the subject securities or issuers. I also certify that I have not, am not, and will not receive, directly or indirectly, compensation in exchange for expressing the specific recommendations or views in this report.

Expert Clive Maund reviews the 1-year chart for Reliq Health Technologies to tell you why he believes it is in another buy spot.

We caught a perfect buy spot when we went for Reliq Health Technologies Inc. (RHT:TSX.V; RQHTF:OTCQB; A2AJTB:WKN) at the start of the month (it was recommended in a Market Notebook update), as right after it proceeded to break out of a quite large Head-and-Shoulders bottom to rise quite steeply, resulting in good percentage gains for us in a short space of time.

The purpose of this update is to point out that it still looks good here.

It is, in fact, at another buy spot as it is starting to break out of a completing bull Flag that has formed over the past couple of weeks, as we can see on its latest 1-year chart below.

November 21, 2022, would have been the perfect time to buy, of course, because it ended up adding CA$0.04 by the end of the day, but it still looks good here as a breakout from the Flag should lead to a rally of similar magnitude to the one preceding the Flag.

We, therefore, stay long and this is a good point to add to positions or make fresh purchases. Reliq trades in reasonable volumes on the US OTC market.

Reliq Health Tech closed for trading at CA$0.71, $0.54 on November 21, 2022. It is currently trading at CA$0.69.

CliveMaund.com Disclosures

The above represents the opinion and analysis of Mr. Maund, based on data available to him, at the time of writing. Mr. Maund’s opinions are his own, and are not a recommendation or an offer to buy or sell securities. Mr. Maund is an independent analyst who receives no compensation of any kind from any groups, individuals or corporations mentioned in his reports. As trading and investing in any financial markets may involve serious risk of loss, Mr. Maund recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction and do your own due diligence and research when making any kind of a transaction with financial ramifications. Although a qualified and experienced stock market analyst, Clive Maund is not a Registered Securities Advisor. Therefore Mr. Maund’s opinions on the market and stocks can only be construed as a solicitation to buy and sell securities when they are subject to the prior approval and endorsement of a Registered Securities Advisor operating in accordance with the appropriate regulations in your area of jurisdiction.

Disclosures: 1) Clive Maund: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: None. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Reliq Health Technologies Inc. Click here for important disclosures about sponsor fees.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Reliq Health Technologies Inc., a company mentioned in this article.

Shares of Titan Machinery Inc. traded 26% higher yesterday to a new 52-week high after the company reported Q3/23 financial results, highlighting a 47.3% YoY increase in revenue. The firm additionally raised its full-year revenue and earnings estimates.

Titan Machinery Inc. (TITN:NASDA), which owns and operates more than 100 full-service stores in the U.S. and Europe, yesterday announced financial results for the third quarter of 2023, which ended October 31, 2022.

The company’s Chairman and CEO, David Meyer, led off the report by stating, “We delivered another consecutive quarter of record financial results, with third-quarter earnings per share of US$1.82. The ongoing strength of the agriculture sector combined with our customer-centric focus drove consolidated revenue growth of 47%, which was supported by strong contributions across each of our revenue streams – equipment, parts, and service . . . Given these strong third-quarter results, coupled with our expectations for the solid market fundamentals continuing through the fourth quarter, we are increasing our earnings per share modeling assumption for the fiscal year 2023 to a midpoint of US$4.70 per share.”

Gross profit in Q3/23 rose to US$139.6 million (20.9%), up from US$92.5 million (20.4%) in Q3/22. The company indicated that the increases were due mostly to stronger margins from equipment sales.

The firm reported that total revenue during Q3/23 increased by 47.3% to US$668.8 million, compared to US$454.0 million in Q3/22.

Revenues across almost all business segments increased versus the same period in the prior year and consisted of US$509.0 million from Equipment sales, US$108.7 million from parts sales, US$39.0 from Service, and US$12.1 million from rental and other sales.

Gross profit in Q3/23 rose to US$139.6 million (20.9%), up from US$92.5 million (20.4%) in Q3/22. The company indicated that the increases were due mostly to stronger margins from equipment sales.

Titan Machinery reported that for Q3/23, it recorded a net income of US$41.3 million, or US$1.83 per diluted share, versus a net income of US$21.8 million, or US$0.97 per share in Q3/22.

The firm added that during Q3/23, adjusted EBITDA increased by 80% to US$63.5 million, compared to US$35.3 million in Q3/22.

The company advised that in Q3/23, agriculture segment revenues grew to US$493.3 million, compared to US$281.5 million in Q3/22. The firm said the gains were the result of a combination of positive organic growth and contributions from three separate company acquisitions.

Titan added that during Q3/23, construction segment revenues increased to US$86.4 million, up from US$79.7 million in Q3/22, driven by increased demand for equipment, and listed that it posted revenues of US$89.0 million in its international segment.

CEO Meyer commented further that “The momentum in our business continues to be visible across all aspects of Titan Machinery, as favorable industry conditions combine with several years of operational improvements and solid growth through accretive and strategic acquisitions . . . Looking ahead, we are very well positioned to serve the strong industries that we operate in with our robust balance sheet and powerful operational performance.”

The company offered some upward adjusted forward guidance and stated that for FY/23, it expects that agriculture revenue will be up 55-60% year-over-year, compared to its prior estimates of 50-55%. The firm stated that construction revenue is expected to decrease by 0-5% y-o-y, and international segment revenue is also projected to be down by 0-5% y-o-y. Titan Machinery added that for FY/23, it now expects it will have diluted earnings per share (EPS) of US$4.55-4.85. Prior estimates called for diluted EPS of US$3.70-4.00.

Titan Machinery owns and operates full-service agricultural and construction equipment dealer locations in North America and Europe. The company is based in West Fargo, N.D., and offers products and services to farmers, ranchers, and other commercial customers from its network of over 100 dealer locations in Europe and 13 U.S. midwestern and western states.

The firm’s international stores are located in Bulgaria, Germany, Romania, and Ukraine. Titan noted that each of its store locations represents one or more of CNH Industrial N.V.’s (CNHI:NYSE; CNHI:MI) equipment brands, including Case Construction, Case IH, CNH Capital, New Holland Agriculture, and New Holland Construction.

Titan Machinery started the day with a market cap of around US$787.17 million yesterday with approximately 22.57 million shares outstanding. TITN shares opened 15% higher yesterday at US$40.20 (+US$5.32, +15.25%) over the previous day’s US$34.88 closing price and reached a new 52-week high price yesterday afternoon of US$44.29. The stock traded yesterday between US$38.31 and US$44.29 per share and closed for trading at US$44.03 (+US$9.15, +26.23%).

Disclosures:

1) Stephen Hytha wrote this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees.

3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.