By ForexTime

The Canadian Dollar is the second-best performer against the US dollar so far in June, gaining 1% thanks to higher oil prices and increased expectations around a BoC rate hike.

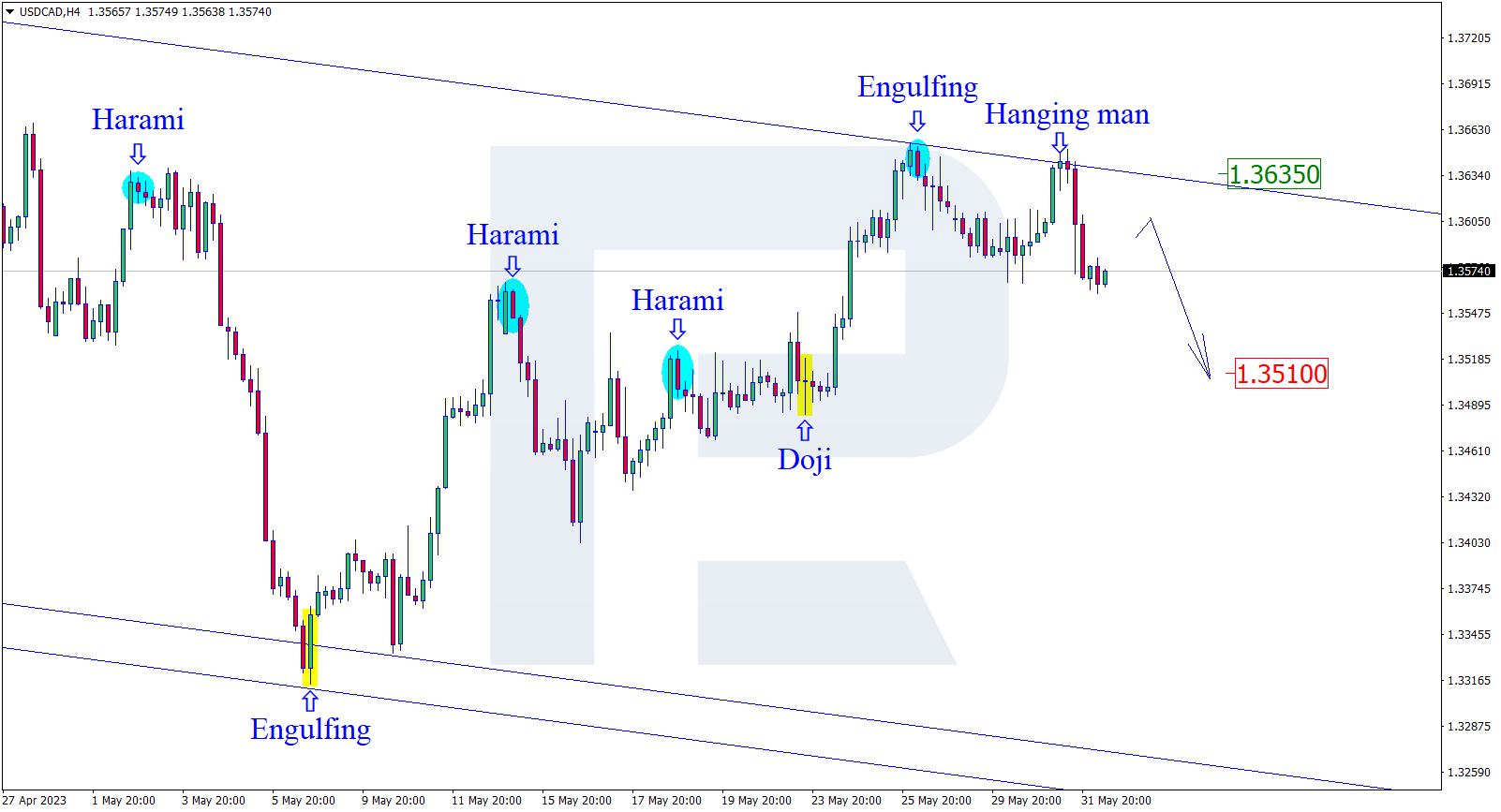

This could be another volatile week for the USDCAD as investors digest last Friday’s sizzling US jobs report and Saudi Arabia’s latest pledge to make an extra 1 million barrel-a-day supply cut in July. Taking a brief look at the technical picture, prices remain trapped within a wide range on the weekly charts with support found at 1.3250 and resistance at 1.3850.

A major breakout could be on the horizon for the USDCAD and here are 4 reasons why:

- Bank of Canada rate decision

On Wednesday, June 7th, the Bank of Canada (BoC) will announce its rate decision.

The recent better than expected economic data including GDP and employment figures have supported expectations around the BoC raising rates at least one final time before 2023 concludes. Traders are currently pricing in a 41% probability of a 25-basis point rate hike on Wednesday with this jumping to 90% by July’s meeting. Should the BoC surprise markets with a rate hike in June, CAD bulls could be injected with renewed confidence.

It may be worth keeping a close eye on the unemployment rate published on Friday, June 9th which could provide fresh insight into the health of the Canadian labour force. A solid report could fuel speculation around the BoC hiking rates further – ultimately dragging the USDCAD lower as the Canadian Dollar appreciates.

- Volatile oil prices

Oil prices jumped almost 5% early on Monday morning before giving back some gains after Saudi Arabia said it will cut oil production by an extra 1 million barrels per day in July.

This development has certainly added more spice to oil markets with expectations around tightening supplies potentially fuelling upside gains. Should oil bulls remain in the driving seat, this will be welcomed by the CAD which is a commodity-linked currency. However, if ongoing concerns around weak global demand cap upside gains and result in renewed weakness for oil, the CAD may be one of the first casualties.

- Dollar performance

The Dollar seems to have regained its mojo after last Friday’s stronger-than-expected US jobs report supported expectations around the Fed leaving rates higher for longer.

Non-farm payrolls soared 339,000 in May, surpassing April’s 294,000 and smashing the median estimates of 195,000. However, the unemployment rate leaped to 3.7% while annual growth cooled, slowing to 4.3%. Given how we have entered the blackout period for Fed speakers, the barrage of key US data releases on Monday could dictate the dollar’s near-term outlook. If dollar strength is a key theme this week, this could push the USDCAD higher. Alternatively, a weaker dollar may drag the currency pair lower.

- Technical forces

The USDCAD has found itself trapped within a very wide range over the past few months with the first layers of monthly support at 1.3250 and resistance at 1.3850.

Zooming into the daily timeframe prices are bouncing within a narrower range with resistance at 1.3650 and support at 1.3300. Bears seem to be in control after the heavy selloff that took prices below the 50, 100, and 200-day SMA. A solid breakdown and daily close below 1.3400 could encourage a decline toward 1.3300. Should prices push back above 1.3500, we could see 1.3560 and 1.3650, respectively.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com