China will be a more attractive investment destination for global investors in 2024 despite the economic warning signs, predicts the CEO and founder of one of the world’s largest independent financial advisory, asset management and fintech organizations.

The bullish predictions from Nigel Green of deVere Group come as Beijing on Thursday confirmed additional financial support for China’s beleaguered property market and developers, including hard-hit Country Garden.

Shenzhen, China’s main industrial hub, has also unveiled new homebuying measures to further support the critical market.

It also comes as Reuters exclusively reports that government advisors are to recommend 2024 growth targets of 4.5-5.5%.

The deVere CEO says: “The marked slowdown of the world’s second-largest economy, home to 1.4 billion people, has been a huge international narrative for the last two years.

“China’s share of the global economy has dropped by 1.4% in this period – the largest drop since the 1960s.

“This matters for not only China but the rest of the world as it’s the largest trading partner of 140 countries and regions globally.”

Much of the focus has been on the downturn of the country’s property market, which makes up a considerable proportion of the economy, and the demographic and unemployment challenges that the economy faces.

But the economic red flags are beginning to flash less brightly say some experts and this will not go unnoticed by global investors.

“The property sector’s drag on China GDP has shrunk from 4% in 2022 to currently less than 2%,” says Nigel Green.

“In addition, Beijing’s further support of the market announced on Thursday shows it is committed to contributing to stability, boosting liquidity, preventing systemic risks, and avoiding contagion.

“Against this backdrop of the government’s increasingly proactive policies, such as stimulus measures and targeted reforms, it is likely that China will again become a more attractive destination for global investors.”

There are other ‘pull factors’ involved too which are expected to be zoomed in upon next year.

“Investors, including multinationals, have shunned the world’s second-largest economy in the last couple of years, but this could change again as the fundamentals come back into focus,” notes the deVere CEO.

“China is transitioning from an export economy to a consumption one that, ultimately, will be more sustainable. Indeed, the country’s burgeoning middle class could create the largest consumption market in the world in the next decade.

“As China moves up the value chain, it is directly acquiring more and more foreign brands, market networks and technologies that will further strengthen its position for global investors.”

He continues: “There’s still enormous potential for infrastructure growth, as its urbanization strategy is still in its infancy and the scope is massive.

“Plus, the reform of state-owned companies could blow apart monopolies and create major investment opportunities.”

The deVere Group chief executive also stresses that China is the world leader in sectors of “the fourth industrial revolution, including clean energy, electric vehicles and industrial robots.”

The Chinese government’s debt could also be noted as a positive. China’s debt to GDP ratio is about 110%, compared to the Japanese and US governments which are around 260% and 120%, respectively.

“China continues to face serious challenges, but the economic woes are starting to look less stark than they have over the last two years as Beijing appears to be becoming increasingly proactive on the essential property sector.

“This is likely to draw the attention of investors in 2024,” concludes Nigel Green.

About:

deVere Group is one of the world’s largest independent advisors of specialist global financial solutions to international, local mass affluent, and high-net-worth clients. It has a network of more than 70 offices across the world, over 80,000 clients and $12bn under advisement.

Stephane Foucaud at Auctus Advisors sees over 90% upside for Panoro Energy based on increased reserves, new exploration potential, and improving fundamentals.

Norway-based Panoro Energy ASA (PEN:OSE; 1PZ:FRA) provided an operational update highlighting increased reserves and new exploration upside across its African oil assets, noted Auctus Advisors in a November 17 research report.

Analyst Stephane Foucaud reiterated a Buy rating and NOK$50 price target on Panoro Energy.

Expanded Resource Estimates in Gabon

According to Foucaud, the operator of Panoro’s Dussafu permit offshore Gabon now estimates 10 million barrels of oil in place above initial expectations, adding 4-5 million barrels of recoverable resources.

This is in addition to the recent 6-7 million barrel discovery at Hibiscus South, both driving increased reserve potential.

New Exploration Prospects Identified

Panoro also plans to drill the 29 million barrel Bourdon exploration prospect on the Dussafu permit. The company sees further upside at its Ceiba field in Equatorial Guinea and added the Akeng Deep prospect.

The analyst believes these opportunities, along with expanded reserves, support his unchanged valuation.

Production Impacted by Temporary Issues

While Panoro produced 10,000 barrels per day in Q3, exceeding estimates, short-term electrical submersible pump (ESP) problems temporarily impacted the Dussafu wells.

This will defer some production to late 2023 and early 2024 before new wells boost output.

Significant Upside Based on Improving Fundamentals

Auctus’ NOK$50 price target implies over 90% upside potential for Panoro Energy. The firm’s valuation is based on increasing reserves, new exploration prospects, and attractive EV/DACF multiples.

In summary, the analyst sees the company’s expanded resources and lower leverage supporting significant share price appreciation.

Important Disclosures:

The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

Disclosures for Auctus Advisors, Panoro Energy ASA, November 17, 2023

Panoro Energy ASA (“Panoro” or the “Company”) is a corporate client of Auctus Advisors LLP (“Auctus”). Auctus receives, and has received in the past 12 months, compensation for providing corporate broking and/or investment banking services to the Company, including the publication and dissemination of marketing material from time to time.

MiFID II Disclosures This document, being paid for by a corporate issuer, is believed by Auctus to be an ‘acceptable minor non-monetary benefit’ as set out in Article 12 (3) of the Commission Delegated Act C(2016) 2031 which is part of UK law by virtue of the European Union (Withdrawal) Act 2018. It is produced solely in support of our corporate broking and corporate finance business. Auctus does not offer a secondary execution service in the UK. This note is a marketing communication and NOT independent research. As such, it has not been prepared in accordance with legal requirements designed to promote the independence of investment research and this note is NOT subject to the prohibition on dealing ahead of the dissemination of investment research.

Author The research analyst who prepared this research report was Stephane Foucaud, a partner of Auctus.

Not an offer to buy or sell Under no circumstances is this note to be construed to be an offer to buy or sell or deal in any security and/or derivative instruments. It is not an initiation or an inducement to engage in investment activity under section 21 of the Financial Services and Markets Act 2000.

Note prepared in good faith and in reliance on publicly available information Comments made in this note have been arrived at in good faith and are based, at least in part, on current public information that Auctus considers reliable, but which it does not represent to be accurate or complete, and it should not be relied on as such. The information, opinions, forecasts and estimates contained in this document are current as of the date of this document and are subject to change without prior notification. No representation or warranty either actual or implied is made as to the accuracy, precision, completeness or correctness of the statements, opinions and judgements contained in this document.

Auctus’ and related interests The persons who produced this note may be partners, employees and/or associates of Auctus. Auctus and/or its employees and/or partners and associates may or may not hold shares, warrants, options, other derivative instruments or other financial interests in the Company and reserve the right to acquire, hold or dispose of such positions in the future and without prior notification to the Company or any other person.

Information purposes only This document is intended to be for background information purposes only and should be treated as such. This note is furnished on the basis and understanding that Auctus is under no responsibility or liability whatsoever in respect thereof, whether to the Company or any other person.

Investment Risk Warning The value of any potential investment made in relation to companies mentioned in this document may rise or fall and sums realised may be less than those originally invested. Any reference to past performance should not be construed as being a guide to future performance. Investment in small companies, and especially upstream oil & gas companies, carries a high degree of risk and investment in the companies or commodities mentioned in this document may be affected by related currency variations. Changes in the pricing of related currencies and or commodities mentioned in this document may have an adverse effect on the value, price or income of the investment.

Distribution This document is directed at persons having professional experience in matters relating to investments to whom Article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (“FPO”) applies, or high net worth organisations to whom Article 49 of the FPO applies. The investment or investment activity to which this communication relates is available only to such persons and other persons to whom this communication may lawfully be made (“relevant persons”) and will be engaged in only with such persons. This Document must not be acted upon or relied upon by persons who are not relevant persons. Without limiting the foregoing, this note may not be distributed to any persons (or groups of persons), to whom such distribution would contravene the UK Financial Services and Markets Act 2000 or would constitute a contravention of the corresponding statute or statutory instrument in any other jurisdiction.

Disclaimer This note has been forwarded to you solely for information purposes only and should not be considered as an offer or solicitation of an offer to sell, buy or subscribe to any securities or any derivative instrument or any other rights pertaining thereto (“financial instruments”). This note is intended for use by professional and business investors only. This note may not be reproduced without the prior written consent of Auctus. The information and opinions expressed in this note have been compiled from sources believed to be reliable but, neither Auctus, nor any of its partners, officers, or employees accept liability from any loss arising from the use hereof or makes any representations as to its accuracy and completeness. Any opinions, forecasts or estimates herein constitute a judgement as at the date of this note. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or estimates. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied is made regarding future performance. This information is subject to change without notice, its accuracy is not guaranteed, it may be incomplete or condensed and it may not contain all material information concerning the company and its subsidiaries. Auctus is not agreeing to nor is it required to update the opinions, forecasts or estimates contained herein. The value of any securities or financial instruments mentioned in this note can fall as well as rise. Foreign currency denominated securities and financial instruments are subject to fluctuations in exchange rates that may have a positive or adverse effect on the value, price or income of such securities or financial instruments. Certain transactions, including those involving futures, options and other derivative instruments, can give rise to substantial risk and are not suitable for all investors. This note does not have regard to the specific instrument objectives, financial situation and the particular needs of any specific person who may receive this note. Auctus (or its partners, officers or employees) may, to the extent permitted by law, own or have a position in the securities or financial instruments (including derivative instruments or any other rights pertaining thereto) of the Company or any related or other company referred to herein, and may add to or dispose of any such position or may make a market or act as principle in any transaction in such securities or financial instruments. Partners of Auctus may also be directors of the Company or any other of the companies mentioned in this note. Auctus may, from time to time, provide or solicit investment banking or other financial services to, for or from the Company or any other company referred to herein. Auctus (or its partners, officers or employees) may, to the extent permitted by law, act upon or use the information or opinions presented herein, or research or analysis on which they are based prior to the material being published.

How can anyone decide on the best course of action in a world full of unknowns?

There are few better examples of this challenge than the COVID-19 pandemic, when officials fervently compared potential outcomes as they weighed options like whether to implement lockdowns or require masks in schools. The main tools they used to compare these futures were epidemic models.

But often, models included numerous unstated assumptions and considered only one scenario – for instance, that lockdowns would continue. Chosen scenarios were rarely consistent across models. All this variability made it difficult to compare models, because it’s unclear whether the differences between them were due to different starting assumptions or scientific disagreement.

In response, we came together with colleagues to found the U.S. COVID-19 Scenario Modeling Hub in December 2020. We provide real-time, long-term projections in the U.S. for use by federal agencies such as the Centers for Disease Control and Prevention, local health authorities and the public. We work directly with public health officials to identify which possible futures, or scenarios, would be most helpful to consider as they set policy, and we convene multiple independent modeling teams to make projections of public health outcomes for each scenario. Crucially, having multiple teams address the same question allows us to better envision what could possibly happen in the future.

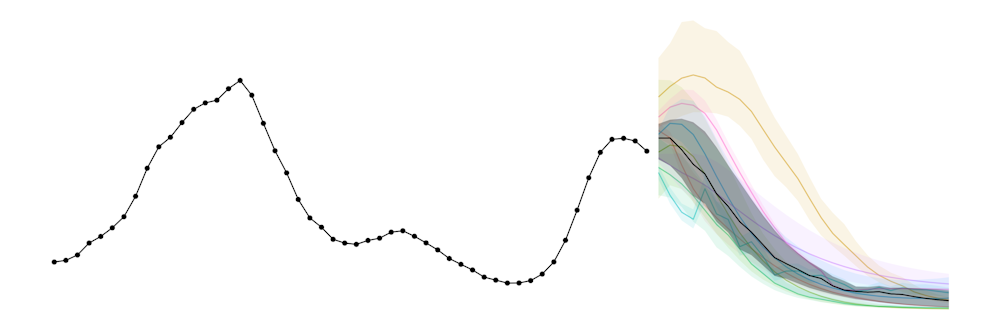

Since its inception, the Scenario Modeling Hub has generated 17 rounds of projections of COVID-19 cases, hospitalizations and deaths in the U.S. across varying stages of the pandemic. In a recent study published in the journal Nature Communications, we looked back at all these projections and evaluated how well they matched the reality that unfolded. This work provided insights about when and what kinds of model projections are most trustworthy – and most importantly supported our strategy of combining multiple models into one ensemble.

Collecting projections from multiple independent models provides a fuller picture of possible futures − as in this graph of potential hospitalizations − and allows researchers to generate an ensemble. COVID-19 Scenario Modeling Hub, CC BY-ND

Multiple models are better than just one

A founding principle of our Scenario Modeling Hub is that multiple models are more reliable than one.

From tomorrow’s temperature on your weather app to predictions of interest rates in the next few months, you likely use the combined results of multiple models all the time. Especially in times like the COVID-19 pandemic when uncertainty abounds, combining projections from multiple models into an ensemble provides a fuller picture of what could happen in the future. Ensembles have become ubiquitous in many fields, primarily because they work.

Our analysis of this approach with COVID-19 models resoundingly showed the strong performance of the Scenario Modeling Hub ensemble. Not only did the ensemble give us more accurate predictions of what could happen in the future overall, it was substantially more consistent than any individual model throughout the different stages of the pandemic. When one model failed, another performed well, and by taking into account results from all of these varying models, the ensemble emerged as more accurate and more reliable.

Researchers have previously shown performance benefits of ensembles for short-term forecasts of influenza, dengue and SARS-CoV-2. But our recent study is one of the first times researchers have tested this effect for long-term projections of alternative scenarios.

A ‘hub’ makes multimodel projections possible

While scientists know combining multiple models into an ensemble improves predictions, it can be tricky to put an ensemble together. For example, in order for an ensemble to be meaningful, model outputs and key assumptions need to be standardized. If one model assumes a new COVID-19 variant will gain steam and another model does not, they will come up with vastly different results. Likewise, a model that projects cases and one that projects hospitalizations would not provide comparable results.

Meeting frequently helps multiple modeling teams stay on the same page. Matteo Chinazzi, CC BY-ND

Many of these challenges are overcome by convening as a “hub.” Our modeling teams meet weekly to make sure we’re all on the same page about the scenarios we model. This way, any differences in what individual models project are the result of things researchers truly do not know. Retaining this scientific disagreement is essential; the success of the Scenario Modeling Hub ensemble arises because each modeling team takes a different approach.

At our hub we work together to design our scenarios strategically and in close collaboration with public health officials. By projecting outcomes under specific scenarios, we can estimate the impact of particular interventions, like vaccination.

For example, a scenario with higher vaccine uptake can be compared with a scenario with current vaccination rates to understand how many lives could potentially be saved. Our projections have informed recommendations of COVID-19 vaccines for children and bivalent boosters for all age groups, both in 2022 and 2023.

In other cases, we design scenarios to explore the effects of important unknowns, such as the impact of a new variant – known or hypothetical. These types of scenarios can help individuals and institutions know what they might be up against in the future and plan accordingly.

Although the hub process requires substantial time and resources, our results showed that the effort has clear payoffs: The information we generate together is more reliable than the information we could generate alone.

The sum is greater than the parts when researchers build an ensemble from multiple coordinated but independent models. Matteo Chinazzi, CC BY-ND

Past reliability, confidence for future

Because Scenario Modeling Hub projections can inform real public health decisions, it is essential that we provide the best possible information. Holding ourselves accountable in retrospective evaluations not only allows us to identify places where the models and the scenarios can be improved, but also helps us build trust with the people who rely on our projections.

Our hub has expanded to produce scenario projections for influenza, and we are introducing projections of respiratory syncytial virus, or RSV. And encouragingly, other groups abroad, particularly in the EU, are replicating our setup.

Scientists around the world can take the hub-based approach that we’ve shown improves reliability during the COVID-19 pandemic and use it to support a comprehensive public health response to important pathogen threats.

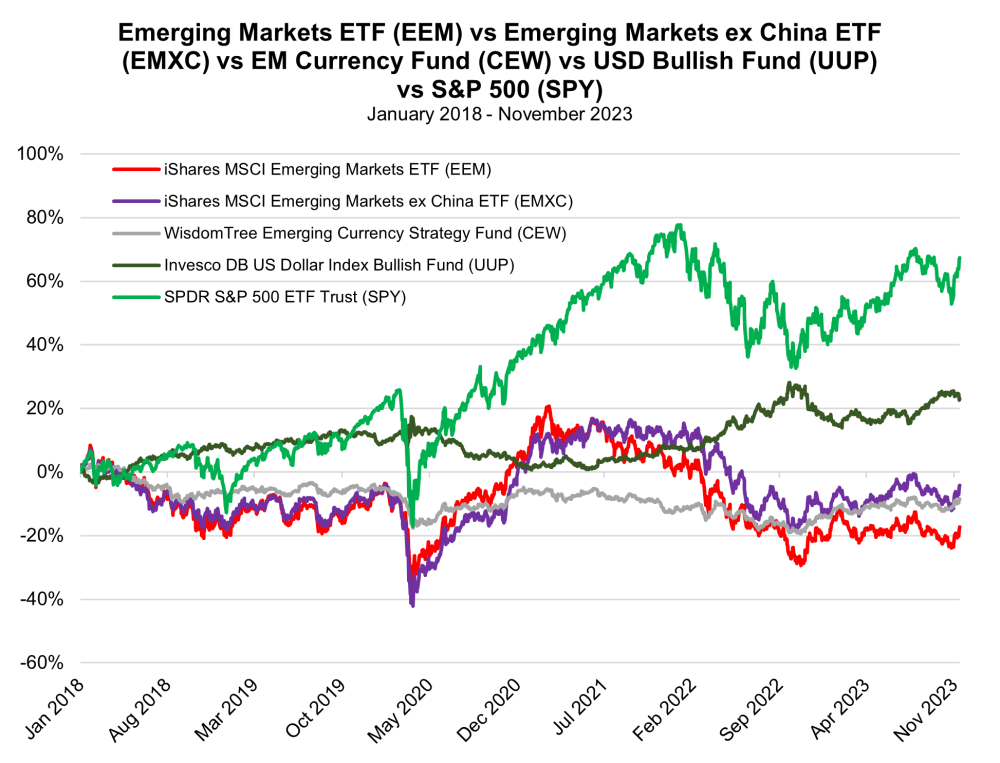

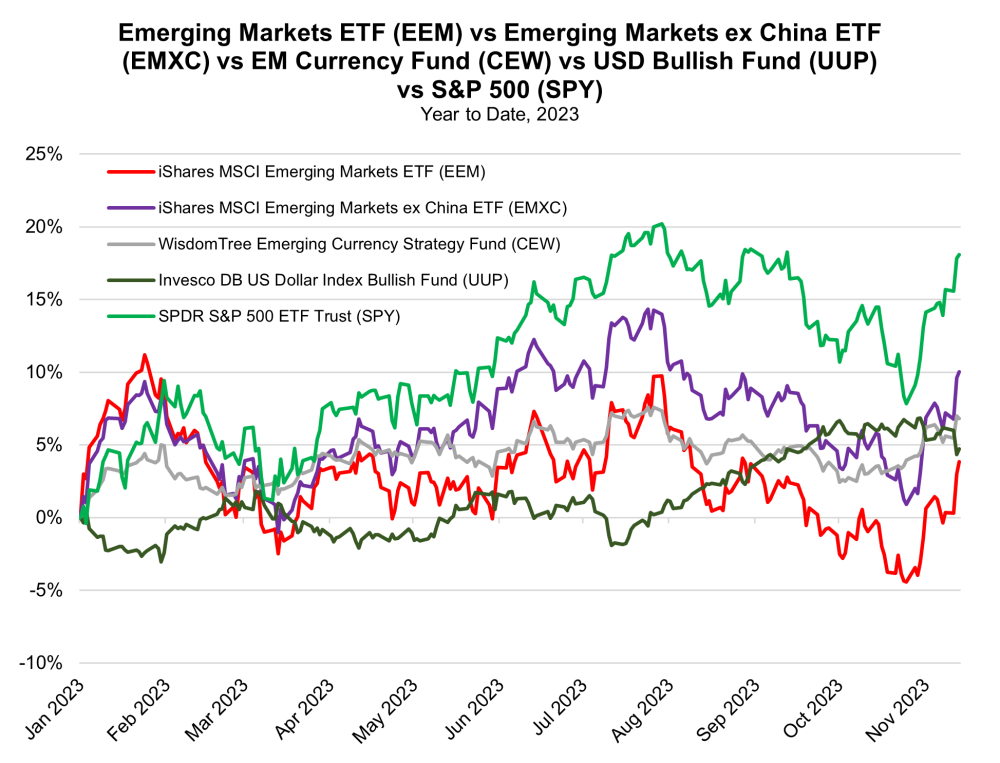

McAlinden Research shares thoughts on the current state of the U.S. dollar and how this may impact the market.

The U.S. Dollar Index (DXY) fell to a 2-month low earlier this week on consumer price inflation data that was softer than expected. A gradual pace of disinflation has taken hold and appears to indicate the Federal Reserve has wrangled inflation for the moment. The slowing pace of growth in the CPI was compounded by outright deflation in producer prices, as well as import and export price data.

These data points have increased the likelihood that the Fed has concluded its spate of rate hikes, reaching a terminal Fed Funds rate of 5.5%. If so, that would fall one hike short of what Fed policymakers projected for 2023 in September’s dot plot. Fed Funds futures contracts traded on the Chicago Mercantile Exchange (CME) indicate that traders see no further hikes going forward into 2024.

When interest rates rise in the U.S., the higher yields can attract investment capital from investors abroad who exchange assets in non-USD currencies for Dollar-denominated investments. This demand, in turn, raises the value of the Dollar compared to other currencies. In a similar way, if rates are to hold steady or even begin to fall, that can cut the appeal of the Dollar. CME’s FedWatch tool suggests a cut is actually more likely than any further hikes going forward — particularly from May 2024 and beyond.

It was all the way back in our August 2022 Viewpoint, The FX Timebomb , that MRP noted the Dollar was likely on the verge of a downturn, as the Fed was rapidly approaching what we termed “peak hawkishness;” the point at which rate hikes reached their maximum size and frequency. We wagered that, from that point on, the central bank’s rate hike regime would gradually reduce the size of rate hikes from 75bps at their largest to 50bps and then, eventually, just 25bps. Further, these hikes would become less frequent until they ceased altogether — likely the state of affairs we have now reached with just one hike in the past four FOMC meetings. The DXY hit a more than 20-year high north of 114.0 that September, prior to retreating. Though we did witness a rebound in the Dollar from lows under 100.00 earlier this year, it has not gotten anywhere near its 2022 high.

If Dollar strength is indeed set to subside further, that could provide a boon to emerging market (EM) economies. Per a 2023 IMF analysis, a 10.0% USD appreciation, linked to global financial market forces, decreases economic output in emerging economies by -1.9% after one year’s time, and this drag lingers for two and a half years. The international impact of material USD appreciation is felt disproportionately in EM economies, as growth in developed economies only experiences an immediate decline of -0.6% in the wake of 10.0% USD appreciation, and that dent dissipates in a year’s time.

The strong USD battered nearly all international currencies — particularly those in emerging markets — but subsiding rate pressure from the Fed is bolstering expectations for non-USD currencies in the year ahead. A majority of analysts in a November Reuters poll indicated that they expect the Dollar to trade lower by year-end. The rebound in EM currencies is expected to be gradual, but several EM currencies, like the Indian Rupee, Thai Baht, and South Korean Won, were projected to recoup recent losses sustained against the US Dollar by late 2024.

Shares of many publicly traded EM firms could be bolstered by a favorable currency translation effect if the Dollar continues to soften relative to local currencies. An October 2023 outlook report from Lazard Asset Management notes that current earnings growth forecasts show EM earnings growth of 19% in 2024, nearly doubling expectations for developed markets earnings growth at just 10%. Earnings in the U.S. are only expected to expand by 12%, signifying a 7% positive earnings growth spread in favor of EM over U.S. equities.

The most significant impact of a weakening Dollar on emerging markets may be the impact on their debt loads. As of 2019, about two-thirds of external debt in EM economies was denominated in USD. By October 2022, Bank for International Settlements (BIS) data showed that non-financial dollar-denominated debt in emerging economies stood at $4.2 trillion. When the Dollar appreciates in value compared to local currencies in emerging markets, the servicing of USD-denominated debt becomes more costly on a relative basis. However, the opposite case could now take place, with EM debt loads becoming more manageable.

Investors can gain exposure to emerging markets via the iShares MSCI Emerging Markets ETF (EEM), as well as EM currencies via the WisdomTree Emerging Currency Strategy Fund (CEW). Additionally, exposure to the U.S. Dollar can be gained with either the Invesco DB U.S. Dollar Index Bullish Fund (UUP) or Invesco’s DB U.S. Dollar Index Bearish Fund (UDN).

Charts

Important Disclosures:

Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

McAlinden Research Partners Disclosures This report has been prepared solely for informational purposes and is not an offer to buy/sell/endorse or a solicitation of an offer to buy/sell/endorse Interests or any other security or instrument or to participate in any trading or investment strategy. No representation or warranty (express or implied) is made or can be given with respect to the sequence, accuracy, completeness, or timeliness of the information in this Report. Unless otherwise noted, all information is sourced from public data. McAlinden Research Partners is a division of Catalpa Capital Advisors, LLC (CCA), a Registered Investment Advisor. References to specific securities, asset classes and financial markets discussed herein are for illustrative purposes only and should not be interpreted as recommendations to purchase or sell such securities. CCA, MRP, employees and direct affiliates of the firm may or may not own any of the securities mentioned in the report at the time of publication.

In December 2001, Argentina experienced one of the most dramatic moments in its history. The collapse of convertibility – the monetary stabilisation plan that established parity between the dollar and the peso – brought tens of thousands of people onto the streets to protest against the government’s confiscation of their money, the “corralito”.

Almost 22 years later, the Argentinian population seems to have finally found a figure who could effectively express the “let them all go” slogan that marked that December.

Javier Milei, a far-right economist and founder of the La Libertad Avanza (LLA) party, was elected president of Argentina by defeating Peronist Sergio Massa in the second round held last Sunday.

The more than ten-point lead between Milei and Massa once again called into question the credibility of the polling institutes, which had been predicting a tight race defined by narrow margins. However, there were signs this picture was wrong since the first round. In the first round of voting in October, the sum of the votes given to Milei and Patrícia Bullrich already exceeded Massa’s vote by around 15%.

Victory in 20 of the country’s 23 provinces

In the end, Milei managed to retain more than 80% of Bullrich’s votes and expanded his electoral base by more than 324,000 votes compared to the right-wing’s performance in the first round. The result was a resounding victory, with Milei beating Massa in 20 of the country’s 23 provinces, as well as the federal capital, Buenos Aires. In traditional anti-Peronist strongholds, such as Mendoza, the difference was over 40%, but Milei won in five of the eight provinces currently governed by Peronism.

Understanding the reasons behind this situation is an endeavour that will last for some years. In a preliminary analysis, the results can be read as the expected end of an atypical electoral cycle in which a society punished by a decade of economic stagnation and various failed stabilisation plans decided to punish the traditional political forces. In other words, faced with the rejection of known formulas, the unknown was embraced.

The striking fact is that this discontent has found its main representative in Javier Milei. Milei is an aggressive figure, visibly unprepared, without firm social foundations and who has become known more for idiosyncrasies than for the defence of a project or a track record in politics.

Extreme and rabid campaigning

Milei ran a campaign in his image and likeness: histrionic, extreme and angry, symbolised by the chainsaw with which he sought – metaphorically, one hopes – to destroy the “caste”, the expression by which he referred to the country’s politicians. To this, he added half a dozen slogans (“dollarisation”, “freedom”, “end the Central Bank”), about which little explanation was given, and built the successful campaign that took him to the Casa Rosada.

Understanding this phenomenon requires consideration of transformations underway in Argentine society, ranging from the changes wrought by communication in the internet age to the advance of job insecurity and the marginalisation of large parts of the population from markets and formal state protection networks.

In this sense, it must be recognised that Milei has shown a greater ability to read the current situation than his opponents. He understood that fatigue with the government would not be represented in gradual formulas, as proposed by the coalition Juntos por el Cambio, and made room for accepting a shock therapy proposal.

In this respect, the proposal to dollarise the economy proved a smart electoral move, as it won over younger voters, who have no memory of the collapse of the 1990s and feel the direct impact of a stagnant economy just as they enter the labour market.

Whilst it is necessary to broaden the effort to understand the roots of this result, it is also necessary to reflect on its implications moving forward.

‘Change needs to be drastic, with no middle ground’

Milei himself seems to be aware that his agenda is less feasible than he made it out to be during the campaign. During his victory speech, Milei made no reference to dollarisation or the abolition of the Central Bank, but he made it clear the path he intends to follow is one of shock therapy. He stated: “The changes we need are drastic. There is no room for gradualism, there is no room for middle ground.”

Implementing this shock agenda represents a politically very complex operation. Passing laws and projects that require a qualified majority will require agreements with sectors of Peronism, but the challenge doesn’t end there. The adoption of shock therapy tends to produce very costly effects in terms of employment and income, which could unleash waves of protests that could jeopardise the country’s already difficult governability.

In this context, Milei’s political sustainability will depend on building a network of support that goes beyond votes in the House and Senate and makes a name for itself on the streets.

Will Milei be restrained?

To what extent Milei will be able to make these articulations without losing his anti-system legitimacy is unknown.

Another open question, and a potentially more serious one, concerns the impact of Milei’s presidency on Argentina’s democratic institutions. At the moment, there seems to be an expectation in the country’s traditional circles that the president-elect will be moderate, restrained by the weight of the office, and that his virulent tone is more a candidate’s speech than an expression of temperament.

However, one of the lessons to be learned from the experiences of Donald Trump and Jair Bolsonaro in Brazil is that expectations of moderation are frustrated by far-right politicians. The notion that the Republican Party or the armed forces would contain Trump and Bolsonaro, respectively, was not only wrong, but what we saw was a radicalisation of these actors, who mostly adhered to the authoritarian projects of their leaders.

Authoritarian DNA

To deny the authoritarian DNA of Milei’s project, as the traditional Argentinian right has done, is to close one’s eyes to the obvious in order to avoid facing one’s own contradictions. In the campaign committee, posters with Milei’s face were accompanied by the phrase “the only solution”.

Now, if a figure claims to be the only solution to the country’s problems, all those who oppose that solution automatically become part of the problem.

How the new Argentine president intends to deal with this scenario is something we’ll soon find out, but the clues offered by Milei and Argentine history suggest that the vibrant capacity for mobilisation that distinguishes Argentine society may be more necessary than ever.

Quantum advantage is the milestone the field of quantum computing is fervently working toward, where a quantum computer can solve problems that are beyond the reach of the most powerful non-quantum, or classical, computers.

Quantum refers to the scale of atoms and molecules where the laws of physics as we experience them break down and a different, counterintuitive set of laws apply. Quantum computers take advantage of these strange behaviors to solve problems.

There are some types of problems that are impractical for classical computers to solve, such as cracking state-of-the-art encryption algorithms. Research in recent decades has shown that quantum computers have the potential to solve some of these problems. If a quantum computer can be built that actually does solve one of these problems, it will have demonstrated quantum advantage.

I am a physicist who studies quantum information processing and the control of quantum systems. I believe that this frontier of scientific and technological innovation not only promises groundbreaking advances in computation but also represents a broader surge in quantum technology, including significant advancements in quantum cryptography and quantum sensing.

The source of quantum computing’s power

Central to quantum computing is the quantum bit, or qubit. Unlike classical bits, which can only be in states of 0 or 1, a qubit can be in any state that is some combination of 0 and 1. This state of neither just 1 or just 0 is known as a quantum superposition. With every additional qubit, the number of states that can be represented by the qubits doubles.

This property is often mistaken for the source of the power of quantum computing. Instead, it comes down to an intricate interplay of superposition, interference and entanglement.

Interference involves manipulating qubits so that their states combine constructively during computations to amplify correct solutions and destructively to suppress the wrong answers. Constructive interference is what happens when the peaks of two waves – like sound waves or ocean waves – combine to create a higher peak. Destructive interference is what happens when a wave peak and a wave trough combine and cancel each other out. Quantum algorithms, which are few and difficult to devise, set up a sequence of interference patterns that yield the correct answer to a problem.

Entanglement establishes a uniquely quantum correlation between qubits: The state of one cannot be described independently of the others, no matter how far apart the qubits are. This is what Albert Einstein famously dismissed as “spooky action at a distance.” Entanglement’s collective behavior, orchestrated through a quantum computer, enables computational speed-ups that are beyond the reach of classical computers.

The ones and zeros – and everything in between – of quantum computing.

Applications of quantum computing

Quantum computing has a range of potential uses where it can outperform classical computers. In cryptography, quantum computers pose both an opportunity and a challenge. Most famously, they have the potential to decipher current encryption algorithms, such as the widely used RSA scheme.

One consequence of this is that today’s encryption protocols need to be reengineered to be resistant to future quantum attacks. This recognition has led to the burgeoning field of post-quantum cryptography. After a long process, the National Institute of Standards and Technology recently selected four quantum-resistant algorithms and has begun the process of readying them so that organizations around the world can use them in their encryption technology.

In addition, quantum computing can dramatically speed up quantum simulation: the ability to predict the outcome of experiments operating in the quantum realm. Famed physicist Richard Feynman envisioned this possibility more than 40 years ago. Quantum simulation offers the potential for considerable advancements in chemistry and materials science, aiding in areas such as the intricate modeling of molecular structures for drug discovery and enabling the discovery or creation of materials with novel properties.

Another use of quantum information technology is quantum sensing: detecting and measuring physical properties like electromagnetic energy, gravity, pressure and temperature with greater sensitivity and precision than non-quantum instruments. Quantum sensing has myriad applications in fields such as environmental monitoring, geological exploration, medical imaging and surveillance.

Initiatives such as the development of a quantum internet that interconnects quantum computers are crucial steps toward bridging the quantum and classical computing worlds. This network could be secured using quantum cryptographic protocols such as quantum key distribution, which enables ultra-secure communication channels that are protected against computational attacks – including those using quantum computers.

Despite a growing application suite for quantum computing, developing new algorithms that make full use of the quantum advantage – in particular in machine learning – remains a critical area of ongoing research.

A prototype quantum sensor developed by MIT researchers can detect any frequency of electromagnetic waves. Guoqing Wang, CC BY-NC-ND

Staying coherent and overcoming errors

The quantum computing field faces significant hurdles in hardware and software development. Quantum computers are highly sensitive to any unintentional interactions with their environments. This leads to the phenomenon of decoherence, where qubits rapidly degrade to the 0 or 1 states of classical bits.

Building large-scale quantum computing systems capable of delivering on the promise of quantum speed-ups requires overcoming decoherence. The key is developing effective methods of suppressing and correcting quantum errors, an area my own research is focused on.

In navigating these challenges, numerous quantum hardware and software startups have emerged alongside well-established technology industry players like Google and IBM. This industry interest, combined with significant investment from governments worldwide, underscores a collective recognition of quantum technology’s transformative potential. These initiatives foster a rich ecosystem where academia and industry collaborate, accelerating progress in the field.

On the other hand, there is a tangible risk of entering a “quantum winter,” a period of reduced investment if practical results fail to materialize in the near term.

While the technology industry is working to deliver quantum advantage in products and services in the near term, academic research remains focused on investigating the fundamental principles underpinning this new science and technology. This ongoing basic research, fueled by enthusiastic cadres of new and bright students of the type I encounter almost every day, ensures that the field will continue to progress.

Despite stockpiles of copper growing quickly, analysts polled at London Metal Exchange Week believe the red metal will bring good returns in the long run.

Stockpiles of copper registered with the London Metal Exchange (LME) more than doubled this summer and were at their highest level since May 2022 in September.

Despite that, just one month later, an informal poll of 800 people attending LME Week in London found that 53% believed the red metal needed for the green energy revolution would be the metal with the most upside price potential next year, according to Reuters.

Copper will be “THE bullish energy transition trade within commodities,” said Max Layton of Citi during an analysts’ debate, the report said.

Tin came in a distant second in the survey with 23%.

Copper will be “THE bullish energy transition trade within commodities,” said Max Layton of Citi during an analysts’ debate.

Analysts said several companies — including World Copper Ltd., Granite Creek Copper Ltd., and Fabled Copper Corp. — could be there to reap the benefits of that upside.

The International Copper Study Group met in Lisbon, Portugal, last month, and found that stockpiles are expected to grow, and 2024 could see a surplus of about 467,000 pounds of copper on the market as a consequence of higher supply from new or expanded mines.

“Although the global economic outlook is challenging, an expected improvement in manufacturing activity, the ongoing energy transition and the development of new semis production capacity in various countries should support higher growth in world refined usage in 2024,” the group wrote in a release.

The Catalyst: Deficits Will Grow

Copper (Cu) prices haven’t moved much since spiking earlier this year, but BMI analysts believe deficits could still grow at an extreme pace over the coming decade as the clean energy revolution takes hold, predicting prices of US$11,500 per ton by 2032. Copper’s price was US$8,030 per ton ” Friday morning.

“In the longer term, we expect the copper market to remain in deficit as the green transition accelerates along with the demand for ‘green’ metals, including copper,” BMI’s analysts said, according to Stockhead.

EVs use more than three times as much copper as gas-burning cars. New copper production — and investment in exploration — will be needed to fuel the supply of those vehicles long-term, analysts have said.

“In the longer term, we expect the copper market to remain in deficit as the green transition accelerates along with the demand for ‘green’ metals, including copper,” BMI’s analysts said, according to Stockhead.

“Based on industry-wide capital intensity data, we calculate that some US$196 billion of investment will be required,” a market analysis issued by RFC Ambrian said. “Of this, US$80 billion is for greenfield projects, and US$116 billion is for brownfield projects, of which US$71 billion is simply for replacement capacity. A further US$35 billion of investment will be required to close the supply gap.”

An S&P report called copper “one of the most underappreciated critical minerals.”

“Deeper electrification requires wires, and wires are primarily made from copper,” the report said.

Billionaire Robert Friedland, founder and executive co-chairman of Ivanhoe Mines Ltd., recently told Bloomberg that he fears copper prices could jump tenfold eventually.

“We’re heading for a train wreck here,” he said.

World Copper Ltd.

One company that could benefit from a future spike in copper prices is Vancouver-based World Copper Ltd. (WCU:TSX.V;WCUFF:OTCQX; 7LY0:FRA), which is focused on the exploration and development of its copper porphyry projects: Escalones and Cristal in Chile, and Zonia in Arizona.

Taylor Combaluzier of Red Cloud Securities has rated the stock a Buy with a target of CA$2.15. He said World Copper has “transformed from an explorer into a developer with a portfolio of high-quality copper projects in premiere copper mining jurisdictions.

“We believe Escalones shows compelling economics when compared to other copper development projects and that it offers lots of potential for resource expansion,” he wrote. “Additionally, we believe Zonia has lots of untapped potential, as it could either be rapidly developed for nearer-term production or potentially be expanded through exploration to increase the scale of the project.”

Zacks Small-Cap Research analyst Steven Ralston has a CA$0.59 per share target price on the junior mining company. Its share price on Friday, in comparison, was CA$0.065 per share, implying a potential return for investors of more than 800%.

Earlier this year, World Copper filed an updated mineral resource estimate (MRE) for Zonia. It increased total resources by about 90% to about 198 million tonnes from a 2017 estimate, with contained copper increasing by 55% to about 1.03 billion pounds.

Escalones is about 100 kilometers from Santiago. Its PEA (preliminary economic assessment) estimates an inferred resource of 426 million tonnes of 0.367% copper, containing 3,447 pounds of copper.

Coming catalysts include permitting for Escalones and a preliminary feasibility study (PFS) of Zonia’s main deposit.

Wealth Minerals Ltd. (WML:TSX.V; WMLLF:OTCQB) owns about 15.8% of World Copper or about 19.2 million shares. About 27% is owned by management and insiders, including Director Robert Kopple with 11.84% or 14.8 million shares and Board Chairman Hendrik van Alphen with 2.67% or 3.25 million shares. CEO Peterson said he holds about 700,000 shares. The rest is retail.

Its market cap is CA$8.13 million. It has 125 million shares outstanding, including 87.2 million of them free-floating. It trades in a 52-week range of CA$0.26 and CA$0.07.

Granite Creek Copper Ltd.

Another play for copper is Granite Creek Copper Ltd. (GCX:TSX.V; GCXXF:OTCQB), “a Canadian exploration company focused on the acquisition and development of highly prospective brownfields assets in top districts of favorable North American mining jurisdictions,” according to its website. It is a member of the Metallic Group of Companies, along with Metallic Minerals and Stillwater Critical Minerals.

Per a 2023 PEA, its Carmacks Project has the potential for significant additional cash flow from the processing of oxide tailings to increase total copper recovery.

The company has also identified additional near-mine exploration targets that have the potential to increase the resource from the current 36 million tonnes grading around 1.07% copper equivalent. The project currently has a mine life of nine years, at 7,000 tonnes per day (TPD), and any further expansion into the surrounding area could significantly extend that operational lifespan.

Recently, the company announced the preliminary results of a metallurgical study designed to increase the recovery of copper from oxide material at Carmacks, with up to 81% of the copper present in the test samples going into solution.

A Couloir Capital research report referred to Granite Creek Copper as a “promising base metals explorer with a near-term target of reaching a billion pounds of copper at its Carmacks Copper Project.”

Bob Moriarty of 321gold.com said Granite Greek was “a really easy call.”

“Green energy requires enormous quantities of copper, lithium, and graphite, far more than today,” Moriarty wrote. “Prices will have to go up. Granite Creek Copper is in the catbird’s seat, ready to move to production.”

Moriarty wrote that he’s “not a big expert on copper, but Granite has to be one of the lowest market cap copper stories with a real asset.”

Management and insiders own 5.71% of the company. Timothy Johnson owns 2.54% of the company with 4.08 million shares, Robert Sennott owns 1.84% with 2.96 million shares, Michael Victor Rowley owns 1.07% with 1.71 million shares, and John Charles Richard Cumming owns 0.26% with 0.42 million shares.

There are 160.77 million shares outstanding, with 151.59 million free-float traded shares. The company has a market cap of CA$5.63 million. It trades in the 52-week period between CA$0.03 and CA$0.105.

Fabled Copper Corp.

Fabled Copper Corp. (FABL:CSE) has continually seen high grades of copper in fieldwork results from its Muskwa Project in British Columbia.

One float sample taken at about 1,600 meters elevation contained massive sulfides and quartz veining with 60% chalcopyrite, 3% bornite, and 23.4% copper (Cu). Another sample at the western side of the occurrence found “a staggering” 29.3% Cu.

“We’re finding all this high-grade mineralization,” President and Chief Executive Officer Peter Hawley said. “So that’s a pretty good hint that, you know, we’re, we’re very close to the source . . . It’s not very often you see high-grade numbers like this.”

Muskwa is in northwestern British Columbia near the Yukon border. It consists of the Toro, Bronson, and Neil claim blocks. All three were explored in the early 1970s before rockslides and snowfields arrested further development. One vein was developed and partly mined — 498,000 tons were milled with a head grade of about 3% Cu.

On the same day as the 29.3% Cu sample, 11 other samples were collected over an altitude of 158 meters. Of the 12 collected, 11 assayed greater than 0.5% Cu, seven greater than 10% Cu, and four greater than 20% Cu.

Fabled has applied for 15 drill sites at the project, including four in the Eagle Vein area. Negotiations with First Nations continue.

According to Yahoo Finance, about 3% of the company is held by insiders. They include Director Luc Pelchat with 1.19% or 210,000 shares, David Smalley with 0.86% or 150,000 shares, and President and CEO Hawley with 0.65% or 110,000 shares, Reuters said.

The rest, 97%, is retail.

Fabled Copper’s market cap is CA$870,000, with 21.75 million shares outstanding, 21.28 million of them floating. It trades in a 52-week range of CA$0.105 and CA$0.03.

Important Disclosures:

World Copper Ltd., Granite Creek Copper Ltd., and Fabled Copper Corp. are billboard sponsors of Streetwise Reports and pays SWR a monthly sponsorship fee between US$4,000 and US$5,000. In addition, Fabled Copper Corp. has a consulting relationship with an affiliate of Streetwise Reports, and pays a monthly consulting fee between US$8,000 and US$20,000.

As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Fabled Copper Corp.

Steve Sobek wrote this article for Streetwise Reports LLC and provides services to Streetwise Reports as an employee.

The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

Some analysts say the stock of tech giant Apple Inc., the world’s most valuable company with a US$2.95 trillion market cap, still has room to grow.

Tech giant Apple Inc. (AAPL:NASDAQ), the world’s most valuable company with a US$2.95 trillion market cap, met some Wall Street expectations with its recent fourth-quarter results but missed others. However, some analysts agree there is still room to grow with the stock.

AAPL earlier this month posted revenue of US$89.5 billion for the fourth quarter ending Sept. 30, down 1% over the same quarter in 2022, and quarterly earnings per diluted share of US$1.46, up 13% YoY.

While Apple’s revenue has slipped in the last few quarters compared with 2022, its gross margins are expanding, Bernstein analyst Toni Sacconaghi wrote, according to Barrons.

“Fundamentally, it has been an improvement in product gross margins, which have grown an average of ~170 bps per year since 2020, vs. declining ~140 bps per year between 2015 and 2020,” wrote Sacconaghi about basis points, or hundredths of a percentage point.

The analyst has a Market Perform rating on Apple’s stock with a target of US$195 per share.

The company’s Q4 FY2023 iPhone revenue went up 3% to US$43.8 billion YoY, which is in line with Wall Street predictions.

The Catalyst: Services Growth Beats Estimates

While the revenue for some of Apple’s product categories declined — wearables were down 3%, iPad revenue was down 10%, and Mac revenue was down 33% — some analysts pointed to the strong performance of the company’s Services segment as a bright spot. The division includes the App Store, AppleCare, iCloud data storage, Apple Pay, Apple Music, and Apple TV+.

“Fundamentally, it has been an improvement in product gross margins, which have grown an average of ~170 bps per year since 2020, vs. declining ~140 bps per year between 2015 and 2020,” wrote Sacconaghi.

That segment was up 16% YoY to US$22.3 billion and beat analysts’ estimates.

“Underlying iPhone and Services growth looks relatively healthy in the holiday quarter and generally in line with whisper numbers,” wrote Wedbush analyst Dan Ives, according to Benzinga. Ives rated the stock Outperform with a price target of US$240 per share.

Goldman Sachs analyst Michael Ng, who has a Buy rating with a price target of US$227 per share on AAPL, agreed.

“iPhone installed base continues to compound, with the iPhone active installed base reaching a record F4Q23 and benefitting from a record number of switchers in F2023 driven in part by expansion into emerging markets and a growing installed base in Apple Watch, Mac, and iPad,” Ng said.

Personal Computer Pioneer

Apple started in 1976, and its Apple II became one of the first mass-produced microcomputers. Its Macintosh computer, released in 1984, pioneered a graphical-user interface that directly influenced how we use our computers even now.

Goldman Sachs analyst Michael Ng, who has a Buy rating with a price target of US$227 per share on AAPL, agreed.

The company’s software now provides a connected ecosystem across several platforms – Macs, iPhones, iPads, Apple Watches, and Apple TVs. In 2018, it became the first publicly traded U.S. company to be valued at more than US$1 trillion, and its market capitalization rose to over US$3 trillion earlier this year. Its other products include AirPods wireless headphones and HomePod Mini smart speakers.

This year, Apple introduced its much-anticipated new virtual reality headset, Vision Pro, which is scheduled for availability early next year at US$3,499.

“Apple is pleased to report a September quarter revenue record for iPhone and an all-time revenue record in Services,” Apple Chief Executive Office Tim Cook said on the release of the figures. “We now have our strongest lineup of products ever heading into the holiday season, including the iPhone 15 lineup and our first carbon-neutral Apple Watch models, a major milestone in our efforts to make all Apple products carbon neutral by 2030.”

China Fears ‘Overblown,’ Analysts Say

Some analysts also agreed that fears of Apple losing iPhone market share in China could be overstated. Oppenheimer analyst Martin Yang rates Apple Outperform with a US$200 per share price target.

“Fears of iPhone’s share loss in Mainland China to Huawei seem overblown when iPhone likely gained share in F4Q,” Yang wrote, according to Benzinga. “We expect investor concerns over China share loss to mostly dissolve heading into FY24.”

Yang said Apple’s financial results were solid given a “very tough macro backdrop,” Barrons reported.

Oppenheimer analyst Martin Yang rates Apple Outperform with a US$200 per share price target.

“We continue to favor its long-term growth potential and unchallenged market positioning,” Yang wrote.

Wedbush analyst Ives said iPhone 15 demand in China was a highlight of Apple’s results.

“While overall, China revenues missed the Street in the September quarter, this was due to softer Mac/iPad sales, which marks the underlying growth the Street is truly focused on,” Ives said.

Apple’s numbers should cause analysts to “breathe a sea of relief,” he said.

“Underlying iPhone and Services growth looks relatively healthy in the holiday quarter and generally in line with whisper numbers,” he said, adding that iPhone China demand concerns were “a great fictional story by the bears.”

Heading Into the Holiday Season

Bernstein’s Sacconaghi said, Apple’s “guided below consensus revenues for the December quarter, (are) largely driven by a weak iPhone cycle. The December quarter typically sets the tone for the year.”

The analyst said he sees the stock’s quality as holding, but encourages investors to “‘be like Buffett’ and buy on dips.”

Raymond James analyst Srini Pajjuri agreed with Sacconaghi that Apple is seeing higher margins, the China numbers were encouraging.

“iPhone was in line and more importantly, China was an area of strength, which should help allay recent slowdown concerns,” Pajjuri said.

Pajjuri rates APPL Outperform with a price target of US$200 to US$195.

Apple recently filled in its holiday lineup with the new iPhone 15 and Apple Watch Series 9 smartwatches, plus new MacBook Pro and iMac computers that run on the company’s new M3 family of chips, which are based on a smaller and more efficient 3-nanometer process.

“On Oct. 25, Apple raised prices for multiple subscription services, including Apple TV+ and its Apple One bundles,” Seitz wrote.

Investor’s Business Daily gave AAPL a Composite Rating of 90 out of 99. The rating combines “five separate proprietary ratings of fundamental and technical performance,” with the best growth stocks having a rating of 90 or better. It also gave the stock a Relative Strength Rating, looking at how the stock performs against others in the last year, of 90 out of 99.

“Wall Street sees the iPhone maker returning to growth in the December quarter,” Seitz wrote.

The company’s next earnings report is due in late January and could be a catalyst for the stock, he said.

Ownership and Share Structure

About 54% of Apple is owned by institutions and about 0.06% by insiders, according to Yahoo! Finance. The rest, about 46%, is in retail.

Top shareholders include The Vanguard Group Inc. with 8.32% or 1.32 billion shares, Berkshire Hathaway Inc. with 5.89% or 916 million shares, BlackRock Institutional Trust Co. with 4.32% or 672 million shares, State Street Global Advisors (US) with 3.66% or 569 million shares, and Geode Capital Management LLC with 1.9% or 296 million shares.

Top individual shareholders include Arthur D. Levinson with 0.03% or 4.59 million shares, CEO Cook with 0.02% or 3.28 million shares, Jeffrey E. Williams with 0% 560,000 shares, and former Vice President Al Gore with 0% or 470,000 shares.

Apple’s market cap is US$2.95 trillion, with 15.55 billion shares outstanding, 15.54 of them free-floating. It trades in a 52-week range of US$198.23 and US$124.17.

Important Disclosures:

As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Apple Inc.

Steve Sobek wrote this article for Streetwise Reports LLC and provides services to Streetwise Reports as an employee.

The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

Yanis Varoufakis grew up during the Greek dictatorship of 1967-1974. He later became an economics professor and was briefly Greek finance minister in 2015.

His late father, a chemical engineer in a steel plant, instilled in his son a critical appreciation of how technology drives social change. He also instilled him with a belief that capitalism and genuine freedom were antithetical – a leftist politics that made his father a political prisoner for several years during the “junta”, as they called it.

In 1993, when he first got the internet, Varoufakis’s father posed a “killer question” to his son: “now computers speak to each other, will this network make capitalism impossible to overthrow? Or might it finally reveal its Achilles heel?”

Varoufakis has been mulling it over ever since.

Though, sadly, it is now too late to explain to his father in person, Varoufakis’s new book Technofeudalism: What Killed Capitalism answers the question in the form of an extended reflection addressed to his father.

“Achilles heel” was on the right track. In his striking response, Varoufakis argues that we no longer live in a capitalist society; capitalism has morphed into a “technologically advanced form of feudalism”.

Review: Technofeudalism: What Killed Capitalism – Yanis Varoufakis (Bodley Head)

Rent over profit

Traditional capitalists are people who can use capital – defined as “anything that can be used to produce saleable goods” (such as factories, machinery, raw materials, money) – to coerce workers and generate income in the form of profits. Such capitalists are clearly still flourishing, but Varoufakis argues they are not driving the economy in the way they used to.

many feudal relations remained intact, but capitalist relations had begun to dominate. Today, capitalist relations remain intact, but techno-feudalist relations have begun to overtake them.

Traditional capitalists, he proposes, have become “vassal capitalists”. They are subordinate and dependent on a new breed of “lords” – the Big Tech companies – who generate enormous wealth via new digital platforms. A new form of algorithmic capital has evolved – what Varoufakis calls “cloud capital” – and it has displaced “capitalism’s two pillars: markets and profits”.

Markets have been “replaced by digital trading platforms which look like, but are not, markets”. The moment you enter amazon.com “you exit capitalism” and enter something that resembles a “feudal fief”: a digital world belonging to one man and his algorithm, which determines what products you will see and what products you won’t see.

If you are a seller, the platform will determine how you can sell and which customers you can approach. The terms in which you interact, share information and trade are dictated by an “algo” that “works for [Jeff Bezos’] bottom line”.

The capitalists who rely on this mode of selling are granted access to the digital estate by its virtual landowners, the Big Tech companies. And if “vassal capitalists” don’t abide by the laws of the estate, they are kicked out – removed from Apple’s App Store or Google’s search index – with disastrous consequences for their business.

Access to the “digital fief” comes at the cost of exorbitant rents. Varoufakis notes that many third-party developers on the Apple store, for example, pay 30% “on all their revenues”, while Amazon charges its sellers “35% of revenues”. This, he argues, is like a medieval feudal lord sending round the sheriff to collect a large chunk of his serfs’ produce because he owns the estate and everything within it.

This is not extracting profit through the production or provision of goods and services, as these platforms are not a “service” in the sense in which the term is used in economics. They are extracting rents in the form of the huge cuts they take from the capitalists on their platforms.

There is “no disinterested invisible hand of the market” here. The Big Tech platforms are exempted from free-market competition. Their owners – “cloudalists” – increase their wealth and power at a dizzying pace with each click, exploiting a new form of rent-seeking made possible by the new algorithmically structured digital platforms. Parasitic on capitalist production, they are now dominating it.

Cloud serfs

But something even more transformative has happened, Varoufakis argues.

Even though most of us are regularly interacting with capitalists and earning wages via our labour, now, for the first time in history, all of us contribute to “the wealth and power of the new ruling class” through our “unpaid labour”.

Every time we use our cloud-linked devices – smartphones, laptops, Alexa, Google Assistant, Siri – we replenish the capital of the Big Tech cloudalists. This in turn increases their capacity to generate more wealth. How? We train their algorithms, which train us, to train them, and so on, in a feedback loop whose goal is to shape our desires and behaviour. They are “selling things to us while selling our attention to others”.

This interaction, Varoufakis insists, is not taking place as any kind of market exchange, such as wages being paid by a capitalist to a group of workers. In this interaction, we are all high-tech “cloud serfs”.

The new advertising men of the postwar world, portrayed in the series Mad Men (Yanis is clearly a fan), thought television was amazing because of its power to deliver audiences to advertisers. They could innovate “attention-grabbing” ways of “manufacturing” consumer desires – and it was delivered free-to-air!

But, Varoufakis emphasises, the ad men of the previous century could never have imagined the development of something like Amazon’s Alexa: a digital network learning “at lightning speed”, via the input of millions of people, how to train us. It is shaping our desires and behaviours in a process of perpetual reinforcement. Our experience and reality are increasingly algorithmically curated. And due to the incredible ease and utility, the information is all freely given.

So the “cloud capital” we are generating for them all the time increases their capacity to generate yet more wealth, and thus increases their power – something we have only begun to realise. Approximately 80% of the income of traditional capitalist conglomerates go to salaries and wages, according to Varoufakis, while Big Tech’s workers, in contrast, collect “less than 1% of their firms’ revenues”.

Quantitative easing

So how did this dystopian turn happen without us really noticing the change? Varoufakis’s story is detailed, but he emphasises two main drivers.

First, the “internet commons” of Web 1.0 transformed into Web 2.0, privatised by American and Chinese Big Tech.

Second, the colossal sums of central bank money that were supposed to refloat our economies in the aftermath of the 2008 Global Financial Crisis (GFC) – a process known as “quantitative easing” – were lent out to big business. Coupled with “austerity” economics for the many, this “murder[ed] investment” and led to what Varoufakis calls “gilded stagnation”.

Much of the central bank money, particularly following another round of quantitative easing during the COVID pandemic, made its way to the Big Tech companies. Their share prices soared to astronomical levels.

The “world of money” was decoupled from the “real economy” where most of us live and work. In an environment where profit became “optional”, loss-making Big Tech companies run by “intrepid and talented entrepreneurs” chose to build up their cloud capital.

So along with markets being steadily replaced by digital platforms, central bank money displaced private profits as the fuel that “fire[s] the global economy’s engine”. Intended by G7 central bankers and their presidents and prime ministers to “save capitalism”, it has unintentionally helped finance the emergence of a new form of capital (cloud capital) and a “new ruling class”.

The ‘world of finance’, argues Yanis Varoufakis, has decoupled from the ‘real economy’ Markus Spiske/Unsplash

GFC: the turning point

So why was the GFC such a pivotal point? Varoufakis has a lot to say. Here’s a brief sketch. (Bear with me!)

Crucial changes had taken place in our economies since the rise of large corporations in industry and banking, which grew ever bigger over the course of the 20th century, eventually becoming global in scale.

The Bretton Woods international financial system – designed to prevent the “greed-fuelled recklessness” that led to the 1929 crash, the Great Depression and a world war – was abolished in 1971. From the 1970s, economies were progressively deregulated and free-market policies were increasingly enthusiastically practised, leading to a new “financialised” version of capitalism.

This was facilitated by the suppression of workers’ wages and bargaining power. The weakened state was progressively captured by lobbyists for the interests of big business. And the hegemony of the US dollar in the global system led to a “tsunami” of dollars pouring back into US markets from Europe, Japan, and later China, “[enriching] America’s ruling class, despite its [large trade] deficit”.

By the new millennium, this had led to an orgy of speculation and, by 2007, the financiers, using “computer-generated complexity” to obscure the “gargantuan risks”, had “placed bets worth ten times more than humanity’s total income”.

The new version of capitalism was failing. But it had grown to such scale and in such a complex, integrated “globalised” way that the banks and insurance companies were “too big to fail”. Their collapse in 2008 would have taken down the US banking system, and the rest of the world with it. Their hubris was thus “rewarded with massive state bailouts”.

What could have happened, as in Sweden in the 1990s, was to “kick out” the bankers, nationalise the banks, appoint new directors and, years later, sell them to new owners – thus saving the banks, but not the bankers.

What happened instead was that bankers, handed large bailouts, did not direct the money to where it was most needed. Neither punished nor chastened, they sent it straight to Wall Street. And there it stayed. Combined with the profits sent to Wall Street from the rest of the world, it eventually caused an “everything rally” that went on for over a decade.

This ultimately helped fuel the development of the cloud capital that has overtaken capitalism. And every time we use our devices, we contribute to its value. The more we transact via platforms, the further we move away from an economic system primarily driven by markets and profits, and the more power concentrates “in the hands of even fewer individuals” – a “tiny band of multi-billionaires residing mostly in California or Shanghai”.

A tech-driven economic revolution

Varoufakis suggests his theory helps us better understand extreme wealth inequalities, the “atrophied democracies” and “poisoned politics” of the West, geopolitics (he interprets the United States and China as two rival “super cloud fiefs”), the stalling of the green energy revolution, and more.

For Varoufakis, we are not just living through a tech revolution, but a tech-driven economic revolution. He challenges us to come to terms with just what has happened to our economies – and our societies – in the era of Big Tech and Big Finance.

The first decades of the 21st century have brought challenges that we are still struggling to come to grips with. One thing is for sure – we have no hope of improving things without properly understanding our predicament.

This book is a welcome contribution towards that task. A technofeudalist age, Varoufakis argues, is not inevitable. Despite the difficulties we face, we have the agency to reject “techno dystopia” and structure our institutions in ways that more meaningfully embody freedom and democracy.

Towards the end of Technofeudalism, Varoufakis canvasses some proposals, drawn from his earlier book Another Now (2020), for how to address these issues. These include ending the cloudalists faux “free service” model and replacing it with a universal micro-payment model, instituting a Bill of Digital Rights, and using digital technology to “democratise companies” (with decisions being taken collectively by “employee-shareholders”).

Varoufakis also proposes to “democratise money”. This plan would involve central banks issuing digital wallets, a universal basic income, reconfiguring “the central bank’s ledger” in the direction of a “common payment and savings system”, and abolishing the current capacity of private banks to “create money”.

The proposals are pretty radical, but I think Varoukais would say they are as radical as the times require them to be.

As of November 2023, sports betting is legal in some form in 38 states and Washington, D.C. Further, 26 states allow sports betting online. Bills have been introduced – and some recently passed – in more states. These states include Vermont, Missouri and North Carolina. Thanks to technology, sports betting is now accessible beyond casinos. Anyone can access it online and on their smartphone.

Sports betting is also becoming more accessible on college campuses. A New York Times investigation found that sports betting companies and universities have essentially “Caesarized” college life. That is to say, they’ve made campuses resemble elements of the world famous casinos by introducing online gambling to students.

College betting scandals shine light on campus wagering.

These profits have driven increased advertising. Some estimate that total advertising through all media channels could approach $3 billion annually. This includes social media platforms like TikTok, where young adults are more likely to see ads for gambling. A study in the United Kingdom found that 72% of 18- to 24-year-olds have seen gambling ads through social media.

While advertisers reportedly focus on young adults of legal age, research suggests that children under 18 are also being exposed to advertising related to gambling. The intensity of advertising activity on social media has raised concerns and brought scrutiny. Earlier this year, for example, prosecutors in the Massachusetts attorney general’s office expressed concern that sports betting and other gambling might spread quickly through college campuses as a result of advertising.

Why college students are at greater risk of gambling addiction

Gambling addiction affects people from all backgrounds and across all ages, but it is an even bigger threat to college students. Adolescents of college age are uniquely likely to engage in impulsive or risky behaviors because of a variety of developmental factors, leaving them more susceptible to take bigger risks and experience adverse consequences.

It’s no secret that drinking alcohol is prevalent on college campuses, and this can increase the likelihood of other risk-taking behaviors such as gambling. Like other addictive behaviors, gambling can stimulate the reward centers of the brain, which makes it more difficult to stop even if someone is building up losses.

What colleges and universities can do to help

If you’re worried a student in your life might have a gambling problem, the Mayo Clinic describes signs to look for. These include restlessness or irritability when attempting to stop or reduce gambling, gambling more when feeling distressed, and lying to hide gambling or financial losses from it. Gamblers Anonymous provides a 20-question, self-diagnostic questionnaire to help people identify problems or compulsive gambling.

For more resources, organizations like the Gateway Foundation offer information and support to help someone with a gambling problem. Immediate help is available at the national problem gambling helpline, 1-800-GAMBLER. The National Council on Problem Gaming has lists of resources within each state that can provide more local support and assistance.