By ForexTime

If you thought the last few days were explosive for gold prices, then wait until you see what factors could spark even more volatility next week!

The precious metal experienced a brutal selloff this week, shedding roughly 2.7% (at the time of writing) as the prospects of higher-for-longer interest rates boosted the dollar and Treasury yields.

Before we unpack what factors may further influence gold prices, here is a list of key economic reports and events to watch out for in the first week of Q4:

Sunday, October 1

- CNH: China Caixin manufacturing PMI, Caixin services PMI

- US Government shutdown if deadline missed

Monday, October 2

- AUD: Australia Melbourne Institute inflation

- JPY: BoJ September meeting minutes

- EUR: Eurozone/Germany S&P Global Manufacturing PMI

- GBP: UK S&P Global/CIPS Manufacturing PMI

- USD: US ISM Manufacturing, Fed Chair Jerome Powell, Philadelphia Fed President Patrick Harker, Cleveland Fed President Loretta Mester, New York Fed President John Williams speech

Tuesday, October 3

- AUD: RBA rate decision

- Bitcoin: Former FTX CEO set to go on trial

- USD: Atlanta Fed President Raphael Bostic speech

Wednesday, October 4

- NZD: RBNZ rate decision

- EUR: Eurozone S&P Global Services PMI, retail sales, PPI

- USD: US factory orders, ADP employment, Chicago Fed President Austan Goolsbee, Fed Governor Michelle Bowman speech

Thursday, October 5

- AUD: Australia trade

- USD: US trade, initial jobless claims, San Francisco Fed President Mary Daly, Cleveland Fed President Loretta Mester speech

Friday, October 6

- CAD: Canada unemployment

- EUR: Germany factory orders

- USD: US September nonfarm payrolls (NFP)

Now, here are 4 reasons why we’re keeping a close eye on gold:

Possible US Government shutdown

The US government will experience a partial shutdown from Sunday 1st October if US Congress fails to meet the September 30th midnight deadline to pass funding bills.

Such a negative development could be incredibly disruptive for the US economy. Many public employees will not receive their payslips while private companies who get paid by government contracts may see funds halted until the government re-opens.

But it does not end here. Key economic data such as the US NFP and inflation among other releases may be delayed at a critical time when investors are constantly seeking key insight on the health of the US economy and future monetary policy.

- Should an extended US government shutdown fuel fears of a US recession and cool bets around the Fed raising rates one more time in 2023, gold could shine.

Powell & Fed speakers in focus

A week jam-packed with speeches from numerous Fed officials, including Jerome Powell could place gold on a rollercoaster ride.

Most Fed speakers have struck a hawkish note recently, standing firm on their mission to tame inflation by pointing in the direction of more tightening. With the latest US CPI figures accelerating for a second month to 3.7% in August, policymakers may be keen to keep the beast under control. Traders are currently pricing in a 38% probability of a 25-basis point hike by the end of 2023, according to Fed fund futures. This figure may be influenced by the messaging of Fed speakers among over major factors.

- Another round of hawkish comments from Fed officials may drag gold prices lower as Fed hike bets rise.

- Gold bulls could fight back if Fed officials strike a cautious note with the impending government shutdown supporting upside gains.

US September nonfarm payrolls (NFP)

It is worth keeping in mind that the US September nonfarm payrolls report could be delayed if the US government experiences a partial shutdown from the 1st of October.

Markets expect the US economy to have created 170,000 jobs in September following August’s increase of 187,000. The unemployment rate is seen cooling to 3.7% from the 3.8% in the previous month.

- A strong-than-expected US jobs report may support the “higher for longer” expectations around US interest rates – dragging gold prices lower.

- However, further evidence of a cooling US jobs market may support the argument that the Fed is finished with hiking rates this year – providing support to gold.

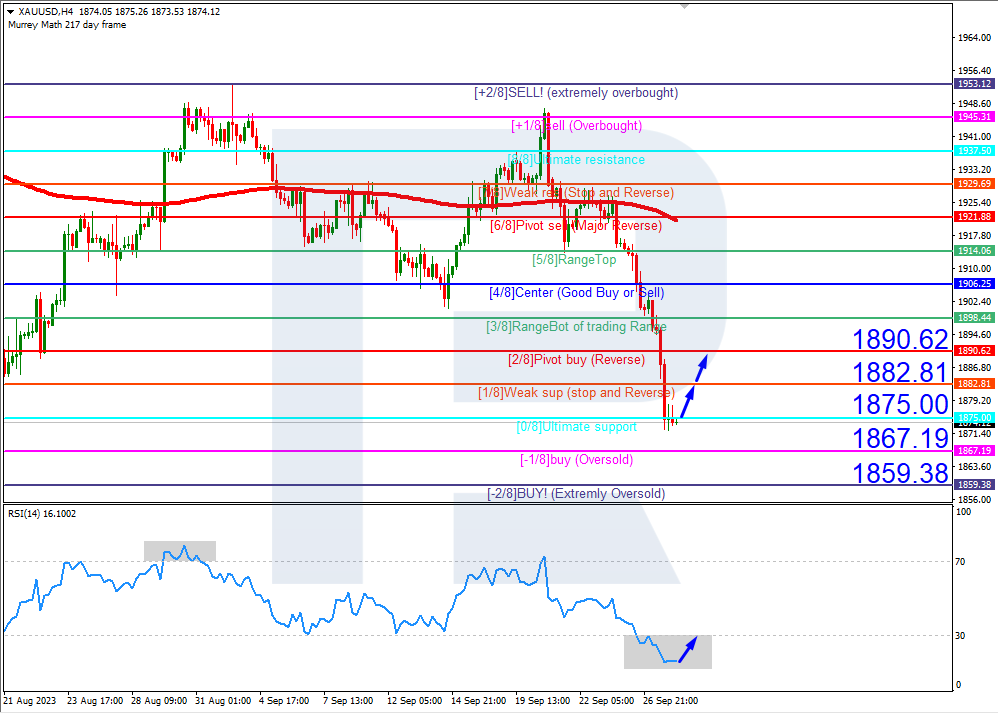

Bearish technical forces

Gold remains under intense pressure on the daily charts with prices well below the 50, 100, and 200-day SMA.

Although bears are in a position of power thanks to fundamental forces, the Relative Strength Index (RSI) is signaling heavily oversold conditions. A technical pullback could be on the horizon before prices extend the heavy decline toward the next key level of interest at $1810.

- A technical pullback towards the $1885 resistance level may encourage a decline back towards $1857.50, $1830, and $1810, respectively.

- Should prices break above $1885, this could encourage a move back towards $1900.

At the time of writing, Bloomberg’s FX model points to a 74% chance that Gold will trade within the $1843.46 – $1905.39 range over the next one-week period.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com