By InvestMacro

Here are the latest charts and statistics for the Commitment of Traders (COT) data published by the Commodities Futures Trading Commission (CFTC).

The latest COT data is updated through Tuesday September 24th and shows a quick view of how large market participants (for-profit speculators and commercial traders) were positioned in the futures markets. All currency positions are in direct relation to the US dollar where, for example, a bet for the euro is a bet that the euro will rise versus the dollar while a bet against the euro will be a bet that the euro will decline versus the dollar.

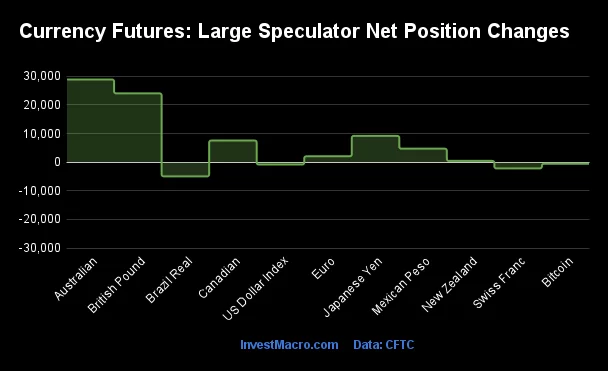

Weekly Speculator Changes led by Australian Dollar & British Pound

The COT currency market speculator bets were higher this week as seven out of the eleven currency markets we cover had higher positioning while the other four markets had lower speculator contracts.

Leading the gains for the currency markets was the Australian Dollar (28,874 contracts) with the British Pound (24,013 contracts), the Japanese Yen (9,171 contracts), the Canadian Dollar (7,561 contracts), the Mexican Peso (4,703 contracts), the EuroFX (2,052 contracts) and the New Zealand Dollar (432 contracts) recording positive weeks.

The currencies seeing declines in speculator bets on the week were the Brazilian Real (-4,956 contracts), the Swiss Franc (-2,182 contracts), the US Dollar Index (-839 contracts) and with Bitcoin (-573 contracts) round out the lower bets on the week.

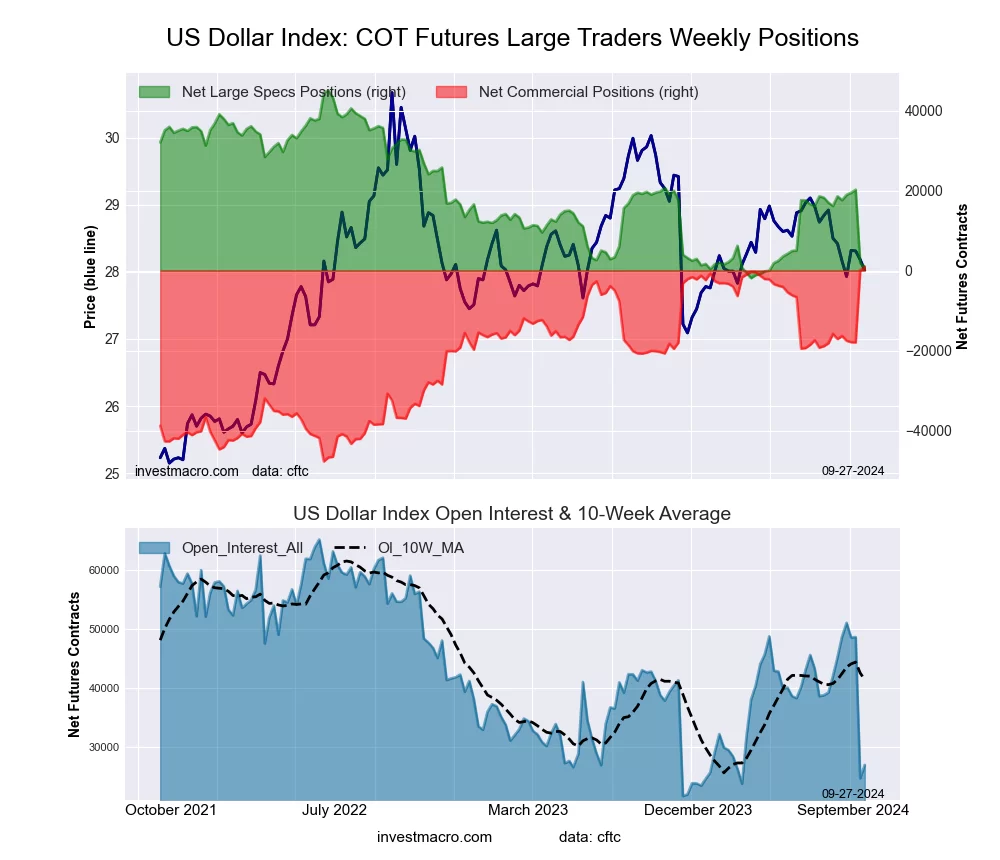

US Dollar Index Speculator bets drop for 2nd week to lowest since April

Highlighting the COT currency’s data this week is the decline of the speculator’s positioning in the US Dollar Index. The large speculative US Dollar Index positions declined for a second straight week and for sixth time out of the past ten weeks this week. This recent weakness has brought the US Dollar Index speculator net position (currently at just a total of +959 contracts) to the lowest level since April 30th, a span of 21 weeks.

The Dollar Index has been under pressure with the US Federal Reserve reducing interest rates by 50 basis points at the last central bank meeting to bring the current rate to a range of 4.75-5.00 percent. The CME Fedwatch tool shows at the current time, there is a 53.3 percent probability outlook that the Fed will cut the rate by another 50 basis points at the November 7th meeting while there is a 46.7 percent probability outlook of a 25 basis point reduction.

The US Dollar Index is currently at significant price levels and closed this week at 100.11. The 100.00 level has been a major support and resistance level in the past and also coincides with the 200-week moving average which is currently right around the 100.40 level. The Dollar Index has not traded consistently below the 200-week MA since 2021. A break below the 100.00 would see the 99.00 level come immediately into play which is also where the 61.8 Fibonacci retracement support level resides (from the January 2021 bottom to September 2022 high). Needless to say, these will likely be some important weeks coming for the USD and its future direction.

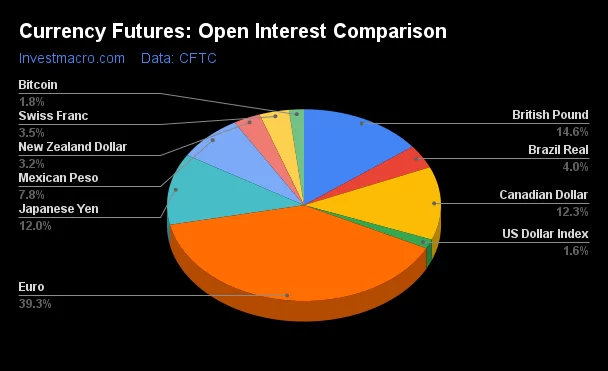

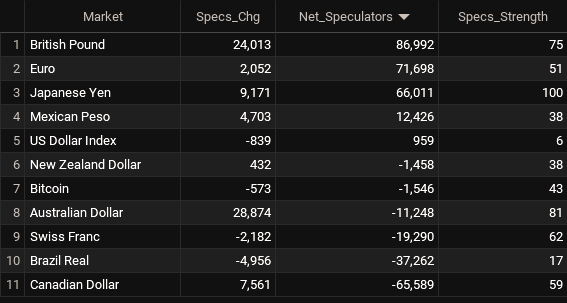

Currencies Net Speculators Leaderboard

Legend: Weekly Speculators Change | Speculators Current Net Position | Speculators Strength Score compared to last 3-Years (0-100 range)

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large speculators) and nonreportable traders (usually small traders/speculators) as well as their open interest (contracts open in the market at time of reporting). CFTC criteria here.

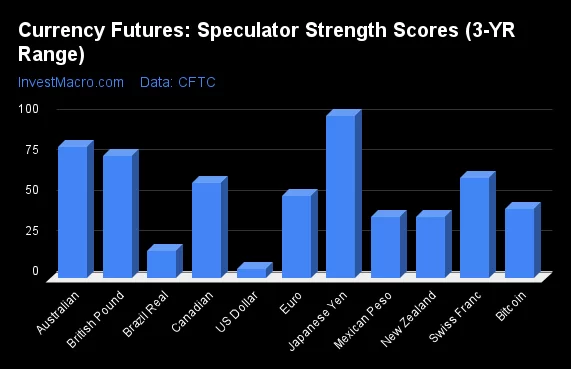

Strength Scores led by Japanese Yen & Australian Dollar

COT Strength Scores (a normalized measure of Speculator positions over a 3-Year range, from 0 to 100 where above 80 is Extreme-Bullish and below 20 is Extreme-Bearish) showed that the Japanese Yen (100 percent) and the Australian Dollar (81 percent) lead the currency markets this week. The British Pound (75 percent), Swiss Franc (62 percent) and the Canadian Dollar (59 percent) come in as the next highest in the 3-Year strength scores.

On the downside, the US Dollar Index (6 percent) and the Brazilian Real (17 percent) come in at the lowest strength levels currently and are in Extreme-Bearish territory (below 20 percent). The next lowest strength scores are the Mexican Peso (38 percent) and the New Zealand Dollar (38 percent).

3-Year Strength Statistics:

US Dollar Index (6.1 percent) vs US Dollar Index previous week (7.9 percent)

EuroFX (50.8 percent) vs EuroFX previous week (50.0 percent)

British Pound Sterling (75.2 percent) vs British Pound Sterling previous week (64.4 percent)

Japanese Yen (100.0 percent) vs Japanese Yen previous week (96.3 percent)

Swiss Franc (61.8 percent) vs Swiss Franc previous week (66.2 percent)

Canadian Dollar (58.6 percent) vs Canadian Dollar previous week (55.2 percent)

Australian Dollar (81.2 percent) vs Australian Dollar previous week (56.8 percent)

New Zealand Dollar (38.1 percent) vs New Zealand Dollar previous week (37.3 percent)

Mexican Peso (37.6 percent) vs Mexican Peso previous week (35.3 percent)

Brazilian Real (16.7 percent) vs Brazilian Real previous week (21.4 percent)

Bitcoin (43.1 percent) vs Bitcoin previous week (51.8 percent)

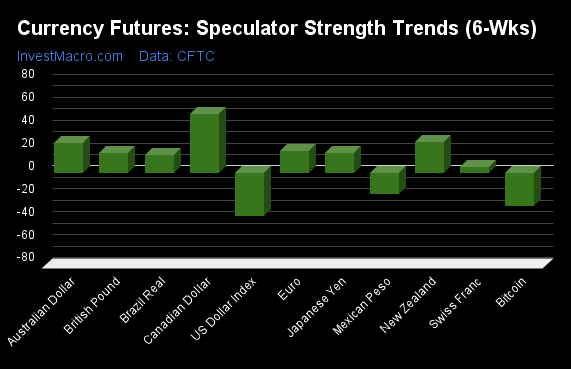

Canadian Dollar & New Zealand Dollar top the 6-Week Strength Trends

COT Strength Score Trends (or move index, calculates the 6-week changes in strength scores) showed that the Canadian Dollar (51 percent) and the New Zealand Dollar (27 percent) lead the past six weeks trends for the currencies. The Australian Dollar (26 percent), the EuroFX (19 percent) and the British Pound (18 percent) are the next highest positive movers in the latest trends data.

The US Dollar Index (-37 percent) leads the downside trend scores currently with Bitcoin (-29 percent) and the Mexican Peso (-18 percent) following next with lower trend scores.

3-Year Strength Trends:

US Dollar Index (-37.5 percent) vs US Dollar Index previous week (-30.6 percent)

EuroFX (19.0 percent) vs EuroFX previous week (15.4 percent)

British Pound Sterling (17.6 percent) vs British Pound Sterling previous week (-5.1 percent)

Japanese Yen (17.1 percent) vs Japanese Yen previous week (27.3 percent)

Swiss Franc (4.8 percent) vs Swiss Franc previous week (10.1 percent)

Canadian Dollar (51.1 percent) vs Canadian Dollar previous week (48.6 percent)

Australian Dollar (26.4 percent) vs Australian Dollar previous week (0.1 percent)

New Zealand Dollar (27.2 percent) vs New Zealand Dollar previous week (28.6 percent)

Mexican Peso (-18.5 percent) vs Mexican Peso previous week (-28.3 percent)

Brazilian Real (15.7 percent) vs Brazilian Real previous week (21.4 percent)

Bitcoin (-29.2 percent) vs Bitcoin previous week (-22.7 percent)

Individual COT Forex Markets:

US Dollar Index Futures:

The US Dollar Index large speculator standing this week resulted in a net position of 959 contracts in the data reported through Tuesday. This was a weekly lowering of -839 contracts from the previous week which had a total of 1,798 net contracts.

The US Dollar Index large speculator standing this week resulted in a net position of 959 contracts in the data reported through Tuesday. This was a weekly lowering of -839 contracts from the previous week which had a total of 1,798 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 6.1 percent. The commercials are Bullish-Extreme with a score of 100.0 percent and the small traders (not shown in chart) are Bearish-Extreme with a score of 3.8 percent.

Price Trend-Following Model: Strong Downtrend

Our weekly trend-following model classifies the current market price position as: Strong Downtrend.

| US DOLLAR INDEX Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 61.1 | 25.5 | 7.8 |

| – Percent of Open Interest Shorts: | 57.6 | 22.1 | 14.6 |

| – Net Position: | 959 | 899 | -1,858 |

| – Gross Longs: | 16,524 | 6,885 | 2,097 |

| – Gross Shorts: | 15,565 | 5,986 | 3,955 |

| – Long to Short Ratio: | 1.1 to 1 | 1.2 to 1 | 0.5 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 6.1 | 100.0 | 3.8 |

| – Strength Index Reading (3 Year Range): | Bearish-Extreme | Bullish-Extreme | Bearish-Extreme |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -37.5 | 37.0 | -4.5 |

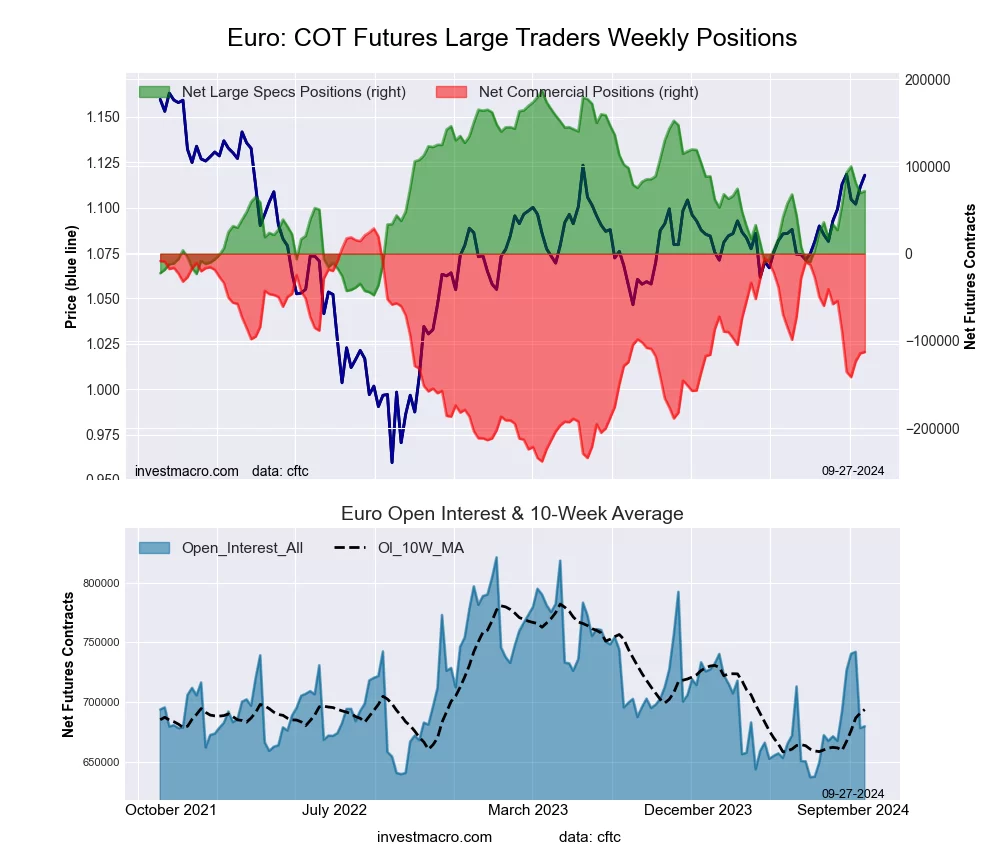

Euro Currency Futures:

The Euro Currency large speculator standing this week resulted in a net position of 71,698 contracts in the data reported through Tuesday. This was a weekly gain of 2,052 contracts from the previous week which had a total of 69,646 net contracts.

The Euro Currency large speculator standing this week resulted in a net position of 71,698 contracts in the data reported through Tuesday. This was a weekly gain of 2,052 contracts from the previous week which had a total of 69,646 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 50.8 percent. The commercials are Bearish with a score of 47.0 percent and the small traders (not shown in chart) are Bullish with a score of 63.7 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| EURO Currency Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 27.6 | 55.9 | 12.8 |

| – Percent of Open Interest Shorts: | 17.1 | 72.5 | 6.8 |

| – Net Position: | 71,698 | -112,828 | 41,130 |

| – Gross Longs: | 187,795 | 379,577 | 87,312 |

| – Gross Shorts: | 116,097 | 492,405 | 46,182 |

| – Long to Short Ratio: | 1.6 to 1 | 0.8 to 1 | 1.9 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 50.8 | 47.0 | 63.7 |

| – Strength Index Reading (3 Year Range): | Bullish | Bearish | Bullish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 19.0 | -22.0 | 32.1 |

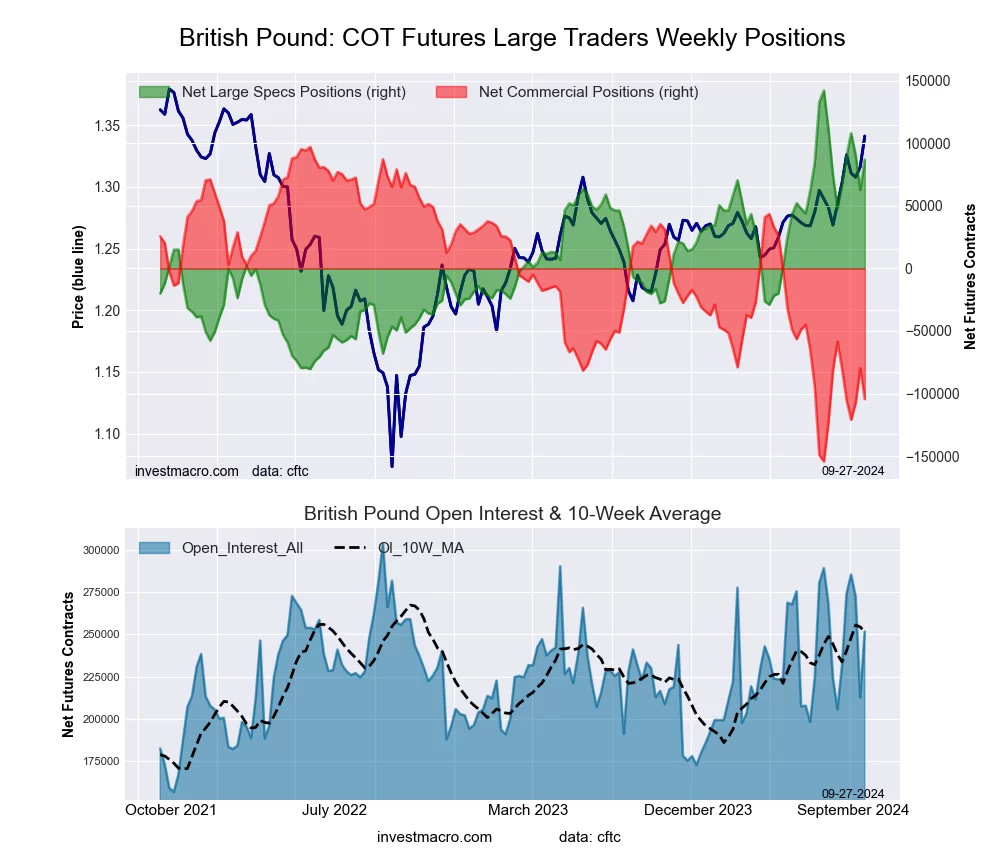

British Pound Sterling Futures:

The British Pound Sterling large speculator standing this week resulted in a net position of 86,992 contracts in the data reported through Tuesday. This was a weekly gain of 24,013 contracts from the previous week which had a total of 62,979 net contracts.

The British Pound Sterling large speculator standing this week resulted in a net position of 86,992 contracts in the data reported through Tuesday. This was a weekly gain of 24,013 contracts from the previous week which had a total of 62,979 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 75.2 percent. The commercials are Bearish-Extreme with a score of 19.9 percent and the small traders (not shown in chart) are Bullish-Extreme with a score of 98.7 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| BRITISH POUND Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 61.7 | 20.8 | 16.3 |

| – Percent of Open Interest Shorts: | 27.2 | 62.3 | 9.4 |

| – Net Position: | 86,992 | -104,383 | 17,391 |

| – Gross Longs: | 155,325 | 52,374 | 40,935 |

| – Gross Shorts: | 68,333 | 156,757 | 23,544 |

| – Long to Short Ratio: | 2.3 to 1 | 0.3 to 1 | 1.7 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 75.2 | 19.9 | 98.7 |

| – Strength Index Reading (3 Year Range): | Bullish | Bearish-Extreme | Bullish-Extreme |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 17.6 | -18.3 | 14.4 |

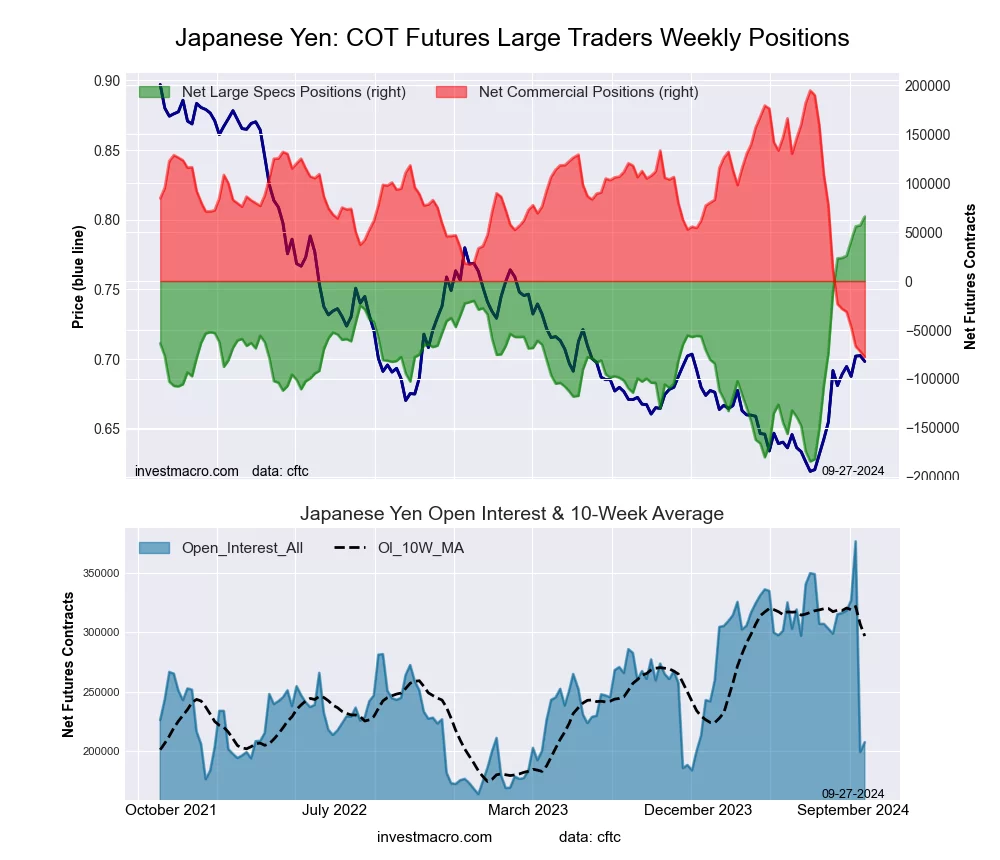

Japanese Yen Futures:

The Japanese Yen large speculator standing this week resulted in a net position of 66,011 contracts in the data reported through Tuesday. This was a weekly gain of 9,171 contracts from the previous week which had a total of 56,840 net contracts.

The Japanese Yen large speculator standing this week resulted in a net position of 66,011 contracts in the data reported through Tuesday. This was a weekly gain of 9,171 contracts from the previous week which had a total of 56,840 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 100.0 percent. The commercials are Bearish-Extreme with a score of 0.0 percent and the small traders (not shown in chart) are Bullish-Extreme with a score of 91.5 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| JAPANESE YEN Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 50.4 | 28.2 | 19.7 |

| – Percent of Open Interest Shorts: | 18.6 | 65.5 | 14.2 |

| – Net Position: | 66,011 | -77,508 | 11,497 |

| – Gross Longs: | 104,690 | 58,606 | 40,901 |

| – Gross Shorts: | 38,679 | 136,114 | 29,404 |

| – Long to Short Ratio: | 2.7 to 1 | 0.4 to 1 | 1.4 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 100.0 | 0.0 | 91.5 |

| – Strength Index Reading (3 Year Range): | Bullish-Extreme | Bearish-Extreme | Bullish-Extreme |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 17.1 | -19.8 | 26.8 |

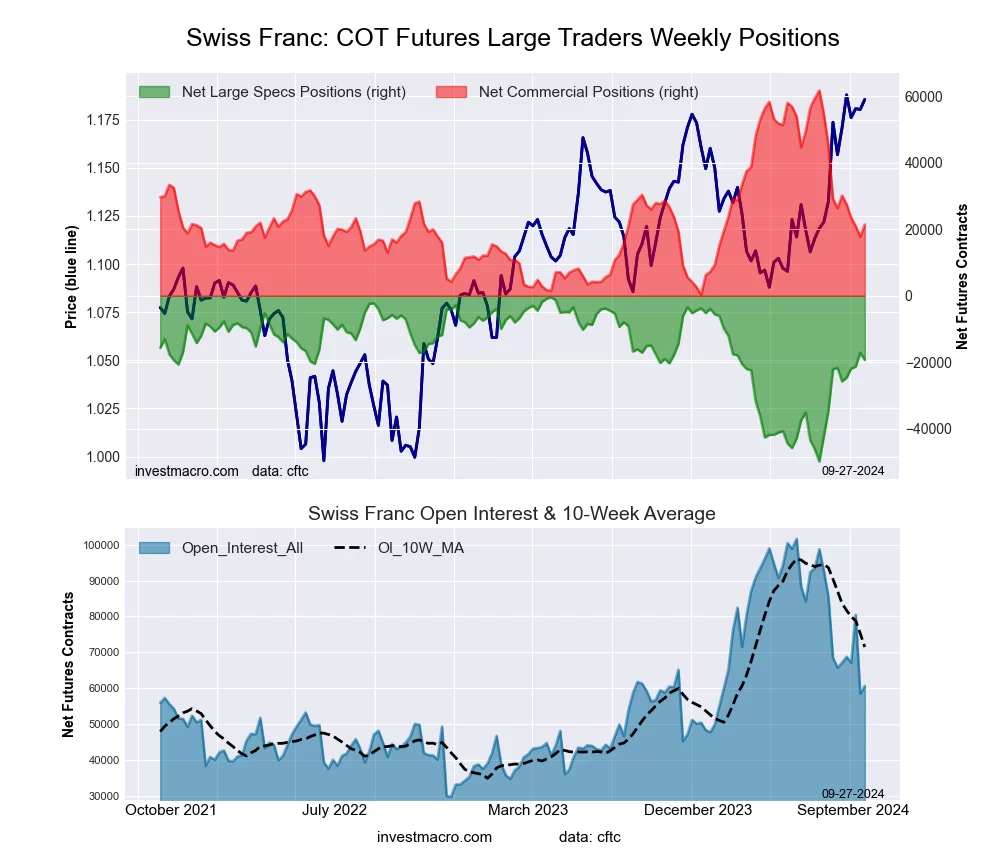

Swiss Franc Futures:

The Swiss Franc large speculator standing this week resulted in a net position of -19,290 contracts in the data reported through Tuesday. This was a weekly fall of -2,182 contracts from the previous week which had a total of -17,108 net contracts.

The Swiss Franc large speculator standing this week resulted in a net position of -19,290 contracts in the data reported through Tuesday. This was a weekly fall of -2,182 contracts from the previous week which had a total of -17,108 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 61.8 percent. The commercials are Bearish with a score of 34.4 percent and the small traders (not shown in chart) are Bullish with a score of 67.7 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| SWISS FRANC Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 12.4 | 64.1 | 22.4 |

| – Percent of Open Interest Shorts: | 44.1 | 28.8 | 25.9 |

| – Net Position: | -19,290 | 21,396 | -2,106 |

| – Gross Longs: | 7,501 | 38,884 | 13,588 |

| – Gross Shorts: | 26,791 | 17,488 | 15,694 |

| – Long to Short Ratio: | 0.3 to 1 | 2.2 to 1 | 0.9 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 61.8 | 34.4 | 67.7 |

| – Strength Index Reading (3 Year Range): | Bullish | Bearish | Bullish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 4.8 | -8.0 | 11.5 |

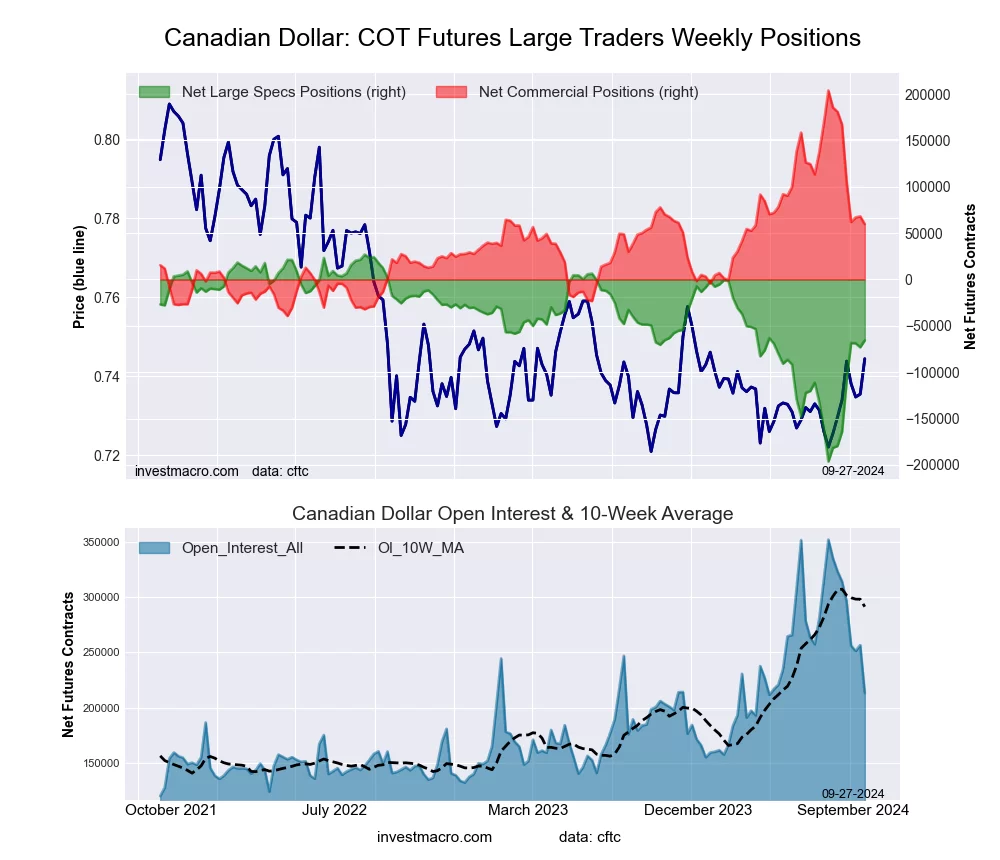

Canadian Dollar Futures:

The Canadian Dollar large speculator standing this week resulted in a net position of -65,589 contracts in the data reported through Tuesday. This was a weekly rise of 7,561 contracts from the previous week which had a total of -73,150 net contracts.

The Canadian Dollar large speculator standing this week resulted in a net position of -65,589 contracts in the data reported through Tuesday. This was a weekly rise of 7,561 contracts from the previous week which had a total of -73,150 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 58.6 percent. The commercials are Bearish with a score of 40.8 percent and the small traders (not shown in chart) are Bearish with a score of 48.0 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| CANADIAN DOLLAR Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 11.9 | 71.8 | 14.7 |

| – Percent of Open Interest Shorts: | 42.6 | 43.8 | 12.0 |

| – Net Position: | -65,589 | 59,746 | 5,843 |

| – Gross Longs: | 25,305 | 153,065 | 31,425 |

| – Gross Shorts: | 90,894 | 93,319 | 25,582 |

| – Long to Short Ratio: | 0.3 to 1 | 1.6 to 1 | 1.2 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 58.6 | 40.8 | 48.0 |

| – Strength Index Reading (3 Year Range): | Bullish | Bearish | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 51.1 | -49.9 | 21.2 |

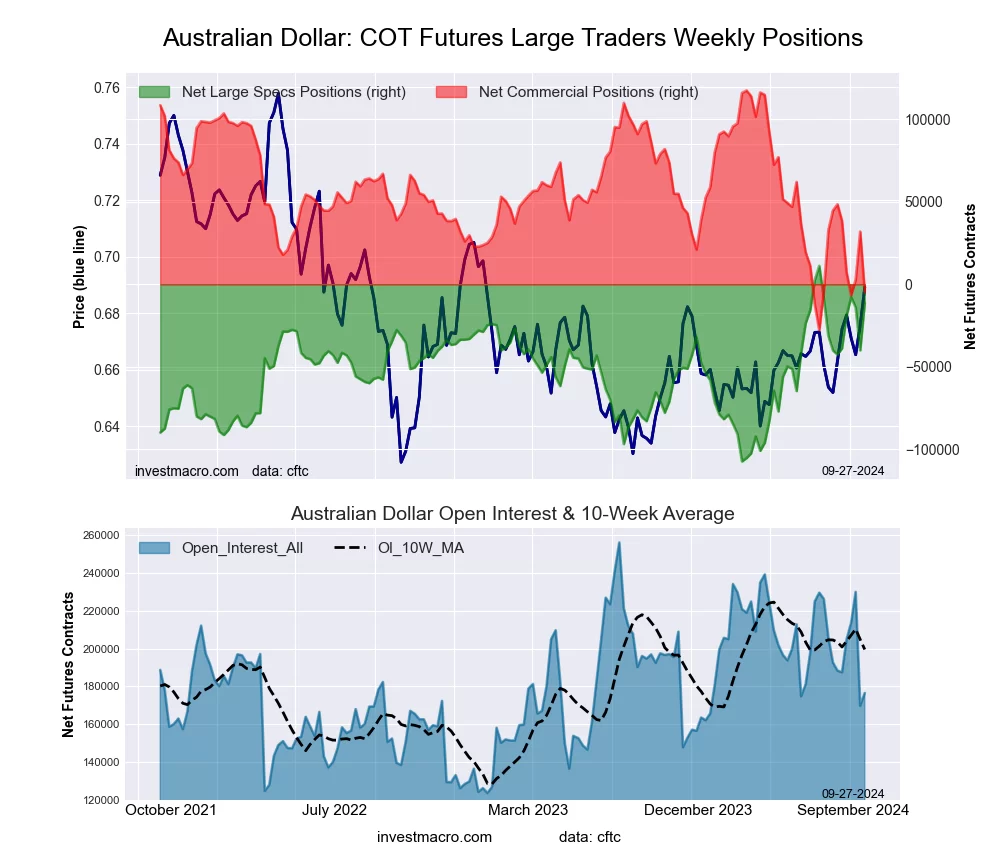

Australian Dollar Futures:

The Australian Dollar large speculator standing this week resulted in a net position of -11,248 contracts in the data reported through Tuesday. This was a weekly gain of 28,874 contracts from the previous week which had a total of -40,122 net contracts.

The Australian Dollar large speculator standing this week resulted in a net position of -11,248 contracts in the data reported through Tuesday. This was a weekly gain of 28,874 contracts from the previous week which had a total of -40,122 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 81.2 percent. The commercials are Bearish-Extreme with a score of 16.0 percent and the small traders (not shown in chart) are Bullish-Extreme with a score of 97.6 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| AUSTRALIAN DOLLAR Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 46.4 | 33.1 | 19.9 |

| – Percent of Open Interest Shorts: | 52.8 | 35.8 | 10.9 |

| – Net Position: | -11,248 | -4,644 | 15,892 |

| – Gross Longs: | 81,924 | 58,488 | 35,139 |

| – Gross Shorts: | 93,172 | 63,132 | 19,247 |

| – Long to Short Ratio: | 0.9 to 1 | 0.9 to 1 | 1.8 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 81.2 | 16.0 | 97.6 |

| – Strength Index Reading (3 Year Range): | Bullish-Extreme | Bearish-Extreme | Bullish-Extreme |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 26.4 | -36.5 | 60.0 |

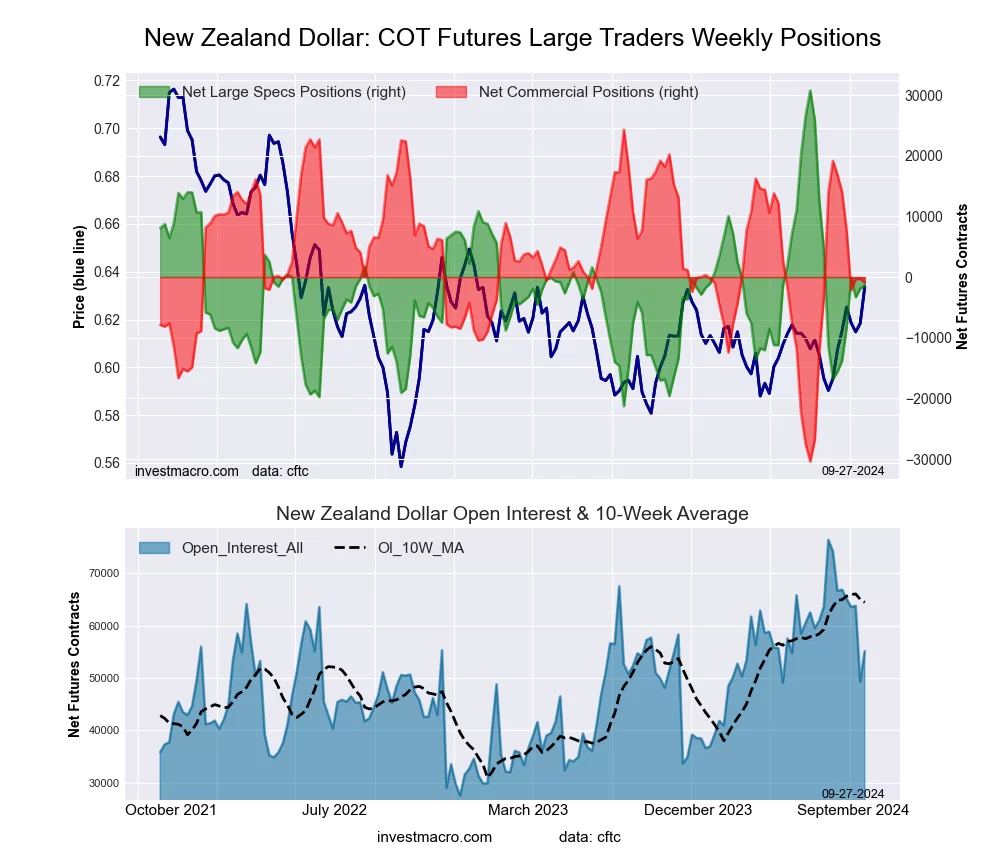

New Zealand Dollar Futures:

The New Zealand Dollar large speculator standing this week resulted in a net position of -1,458 contracts in the data reported through Tuesday. This was a weekly increase of 432 contracts from the previous week which had a total of -1,890 net contracts.

The New Zealand Dollar large speculator standing this week resulted in a net position of -1,458 contracts in the data reported through Tuesday. This was a weekly increase of 432 contracts from the previous week which had a total of -1,890 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 38.1 percent. The commercials are Bullish with a score of 53.9 percent and the small traders (not shown in chart) are Bullish-Extreme with a score of 83.8 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

| NEW ZEALAND DOLLAR Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 48.0 | 41.4 | 10.5 |

| – Percent of Open Interest Shorts: | 50.7 | 43.1 | 6.2 |

| – Net Position: | -1,458 | -928 | 2,386 |

| – Gross Longs: | 26,475 | 22,853 | 5,792 |

| – Gross Shorts: | 27,933 | 23,781 | 3,406 |

| – Long to Short Ratio: | 0.9 to 1 | 1.0 to 1 | 1.7 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 38.1 | 53.9 | 83.8 |

| – Strength Index Reading (3 Year Range): | Bearish | Bullish | Bullish-Extreme |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 27.2 | -32.4 | 45.4 |

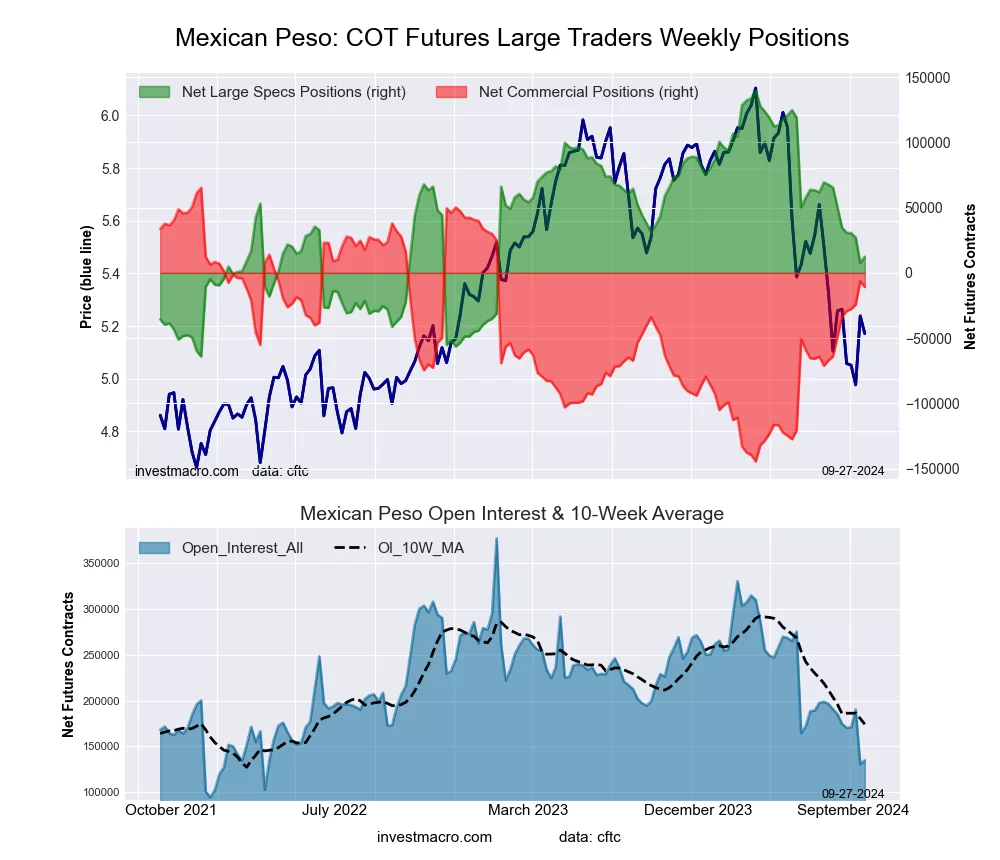

Mexican Peso Futures:

The Mexican Peso large speculator standing this week resulted in a net position of 12,426 contracts in the data reported through Tuesday. This was a weekly increase of 4,703 contracts from the previous week which had a total of 7,723 net contracts.

The Mexican Peso large speculator standing this week resulted in a net position of 12,426 contracts in the data reported through Tuesday. This was a weekly increase of 4,703 contracts from the previous week which had a total of 7,723 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 37.6 percent. The commercials are Bullish with a score of 63.7 percent and the small traders (not shown in chart) are Bearish-Extreme with a score of 7.4 percent.

Price Trend-Following Model: Downtrend

Our weekly trend-following model classifies the current market price position as: Downtrend.

| MEXICAN PESO Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 38.1 | 56.9 | 3.1 |

| – Percent of Open Interest Shorts: | 28.9 | 65.0 | 4.2 |

| – Net Position: | 12,426 | -10,852 | -1,574 |

| – Gross Longs: | 51,480 | 76,816 | 4,127 |

| – Gross Shorts: | 39,054 | 87,668 | 5,701 |

| – Long to Short Ratio: | 1.3 to 1 | 0.9 to 1 | 0.7 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 37.6 | 63.7 | 7.4 |

| – Strength Index Reading (3 Year Range): | Bearish | Bullish | Bearish-Extreme |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -18.5 | 18.1 | -1.1 |

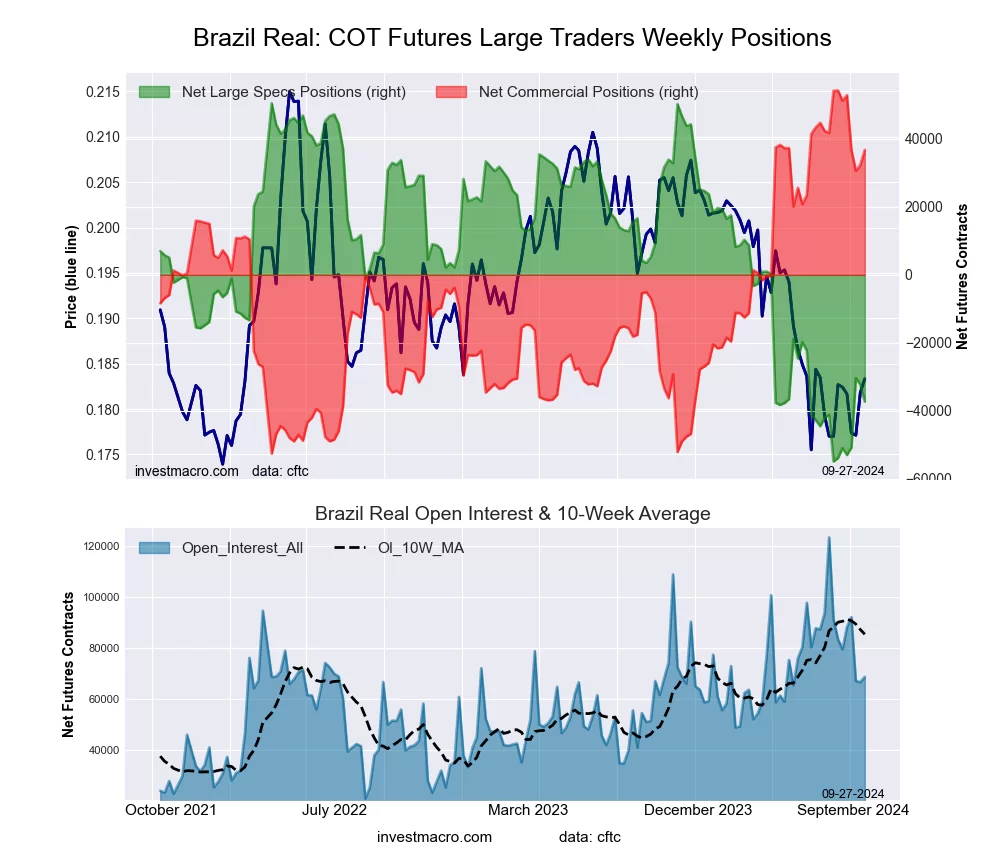

Brazilian Real Futures:

The Brazilian Real large speculator standing this week resulted in a net position of -37,262 contracts in the data reported through Tuesday. This was a weekly decrease of -4,956 contracts from the previous week which had a total of -32,306 net contracts.

The Brazilian Real large speculator standing this week resulted in a net position of -37,262 contracts in the data reported through Tuesday. This was a weekly decrease of -4,956 contracts from the previous week which had a total of -32,306 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 16.7 percent. The commercials are Bullish-Extreme with a score of 83.7 percent and the small traders (not shown in chart) are Bearish with a score of 23.6 percent.

Price Trend-Following Model: Weak Downtrend

Our weekly trend-following model classifies the current market price position as: Weak Downtrend.

| BRAZIL REAL Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 20.1 | 73.4 | 4.2 |

| – Percent of Open Interest Shorts: | 74.4 | 19.8 | 3.5 |

| – Net Position: | -37,262 | 36,777 | 485 |

| – Gross Longs: | 13,840 | 50,396 | 2,883 |

| – Gross Shorts: | 51,102 | 13,619 | 2,398 |

| – Long to Short Ratio: | 0.3 to 1 | 3.7 to 1 | 1.2 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 16.7 | 83.7 | 23.6 |

| – Strength Index Reading (3 Year Range): | Bearish-Extreme | Bullish-Extreme | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | 15.7 | -16.3 | 4.9 |

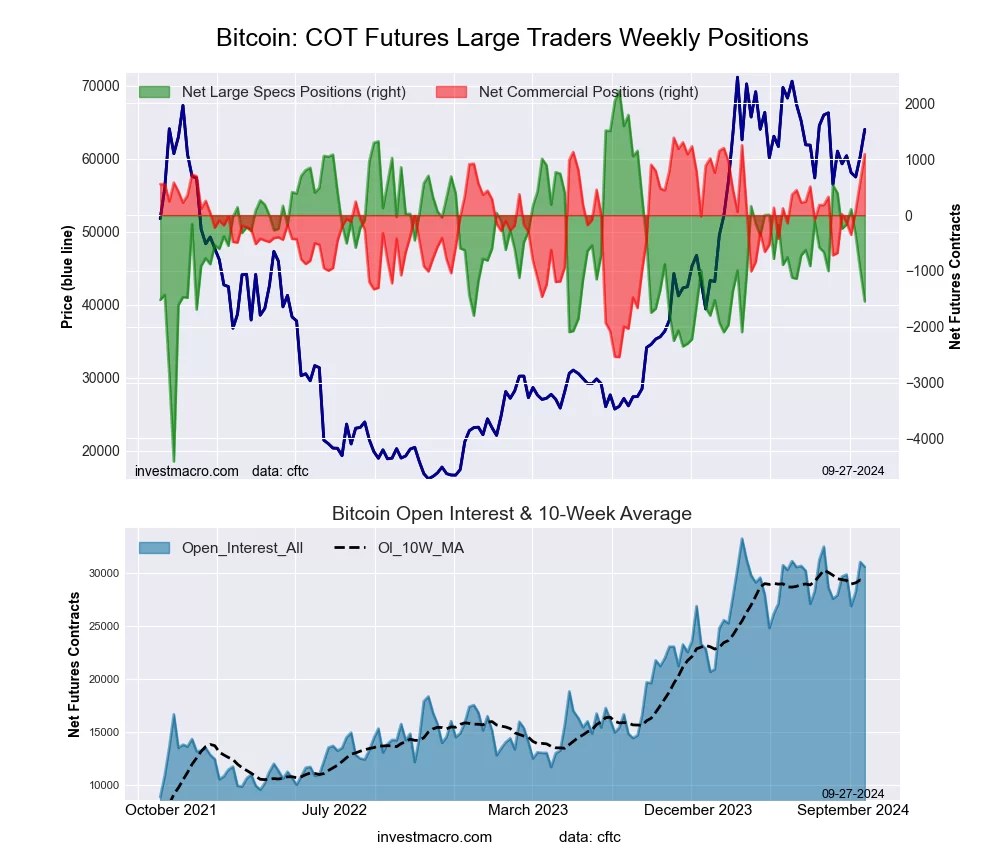

Bitcoin Futures:

The Bitcoin large speculator standing this week resulted in a net position of -1,546 contracts in the data reported through Tuesday. This was a weekly reduction of -573 contracts from the previous week which had a total of -973 net contracts.

The Bitcoin large speculator standing this week resulted in a net position of -1,546 contracts in the data reported through Tuesday. This was a weekly reduction of -573 contracts from the previous week which had a total of -973 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 43.1 percent. The commercials are Bullish-Extreme with a score of 92.5 percent and the small traders (not shown in chart) are Bearish with a score of 23.2 percent.

Price Trend-Following Model: Weak Downtrend

Our weekly trend-following model classifies the current market price position as: Weak Downtrend.

| BITCOIN Statistics | SPECULATORS | COMMERCIALS | SMALL TRADERS |

| – Percent of Open Interest Longs: | 78.1 | 6.7 | 4.7 |

| – Percent of Open Interest Shorts: | 83.2 | 3.1 | 3.2 |

| – Net Position: | -1,546 | 1,093 | 453 |

| – Gross Longs: | 23,856 | 2,033 | 1,433 |

| – Gross Shorts: | 25,402 | 940 | 980 |

| – Long to Short Ratio: | 0.9 to 1 | 2.2 to 1 | 1.5 to 1 |

| NET POSITION TREND: | | | |

| – Strength Index Score (3 Year Range Pct): | 43.1 | 92.5 | 23.2 |

| – Strength Index Reading (3 Year Range): | Bearish | Bullish-Extreme | Bearish |

| NET POSITION MOVEMENT INDEX: | | | |

| – 6-Week Change in Strength Index: | -29.2 | 45.0 | 3.9 |

Article By InvestMacro – Receive our weekly COT Newsletter