By RoboForex Analytical Department

On Tuesday, the price of Gold surged to an unprecedented 3,013 USD per troy ounce, marking a new all-time high. This milestone follows a prolonged upward trend, driven by heightened investor demand for safe-haven assets ahead of the US Federal Reserve’s decision on interest rates.

Key Drivers Behind Gold’s Rally

The Federal Reserve’s two-day meeting, which began today and concludes Wednesday evening, is the focal point for investors. While the base scenario suggests the Fed will maintain current interest rates, market participants are closely watching for updated economic forecasts and insights from Chair Jerome Powell’s press conference. His remarks could explain future monetary policy, particularly amid ongoing trade tensions and tariff disputes.

Geopolitical uncertainties are also fuelling Gold’s ascent. On Monday, US President Donald Trump issued a stern warning to Iran, holding it directly accountable for any further attacks by Yemen’s Houthi rebels. The group has threatened to target foreign vessels in the Red Sea, including those of the US.

Additionally, Trump announced plans to hold talks with the Russian president on Tuesday morning to discuss a potential ceasefire, further adding to the global uncertainty driving investors toward Gold.

Technical Analysis of XAU/USD

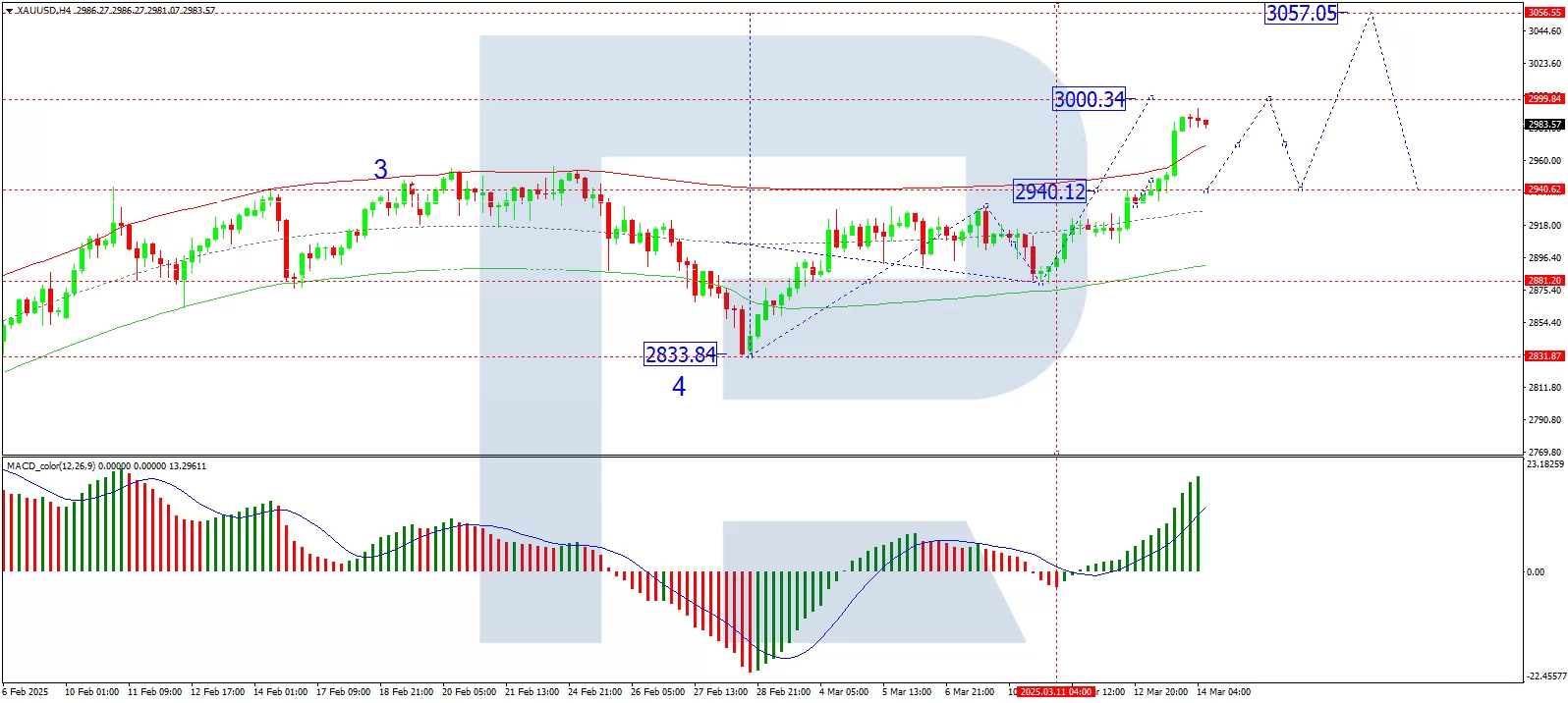

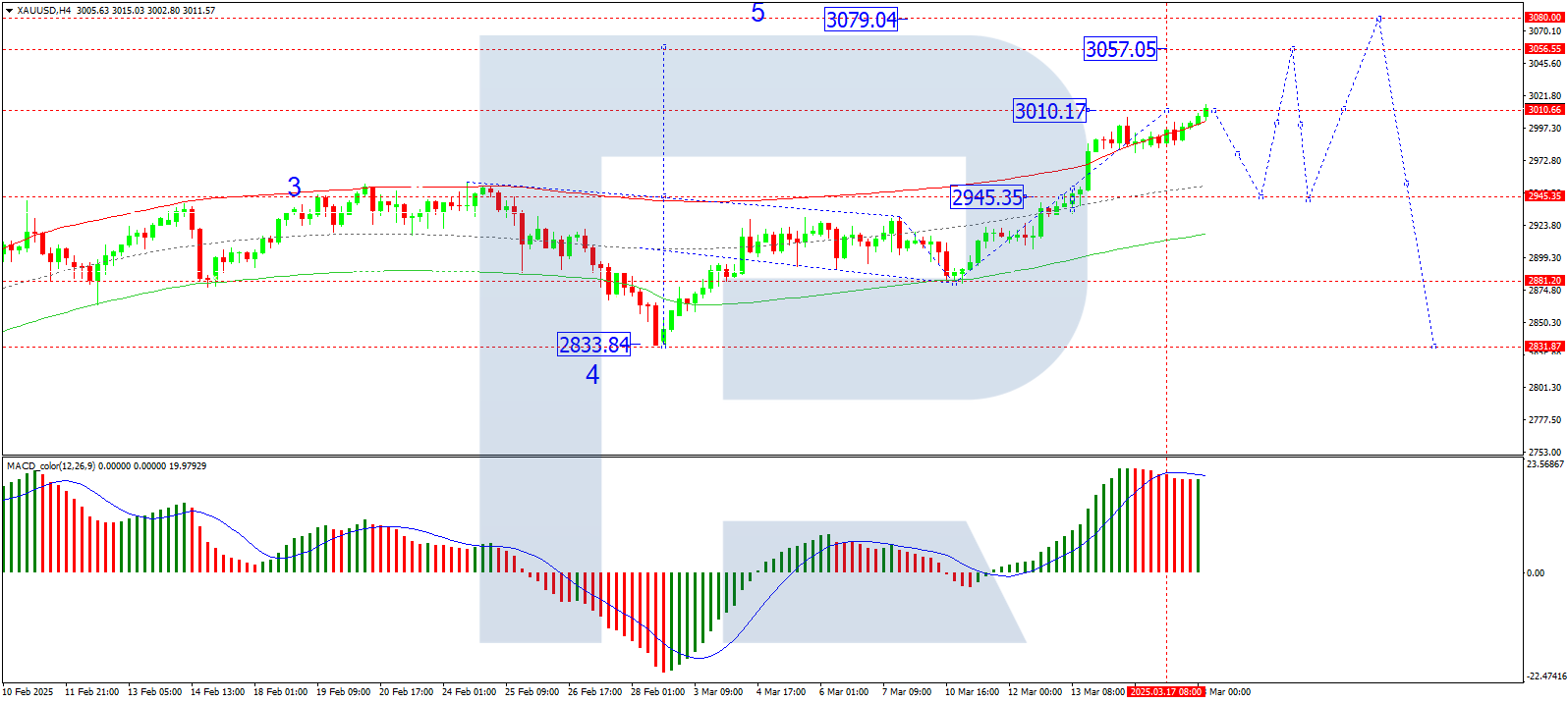

On the H4 chart, XAU/USD has formed a tight consolidation range around the 2,945 level, signalling the continuation of an upward growth wave. Today, we anticipate the price to test the 3,010 level, which serves as a local target. Following this, a corrective pullback toward 2,945 (testing from above) is possible. Once this correction concludes, we expect a new growth wave targeting the 3,057 level. This scenario is technically supported by the MACD indicator. The signal line has exited the histogram zone and is pointing sharply downward, indicating potential for upward momentum after the correction.

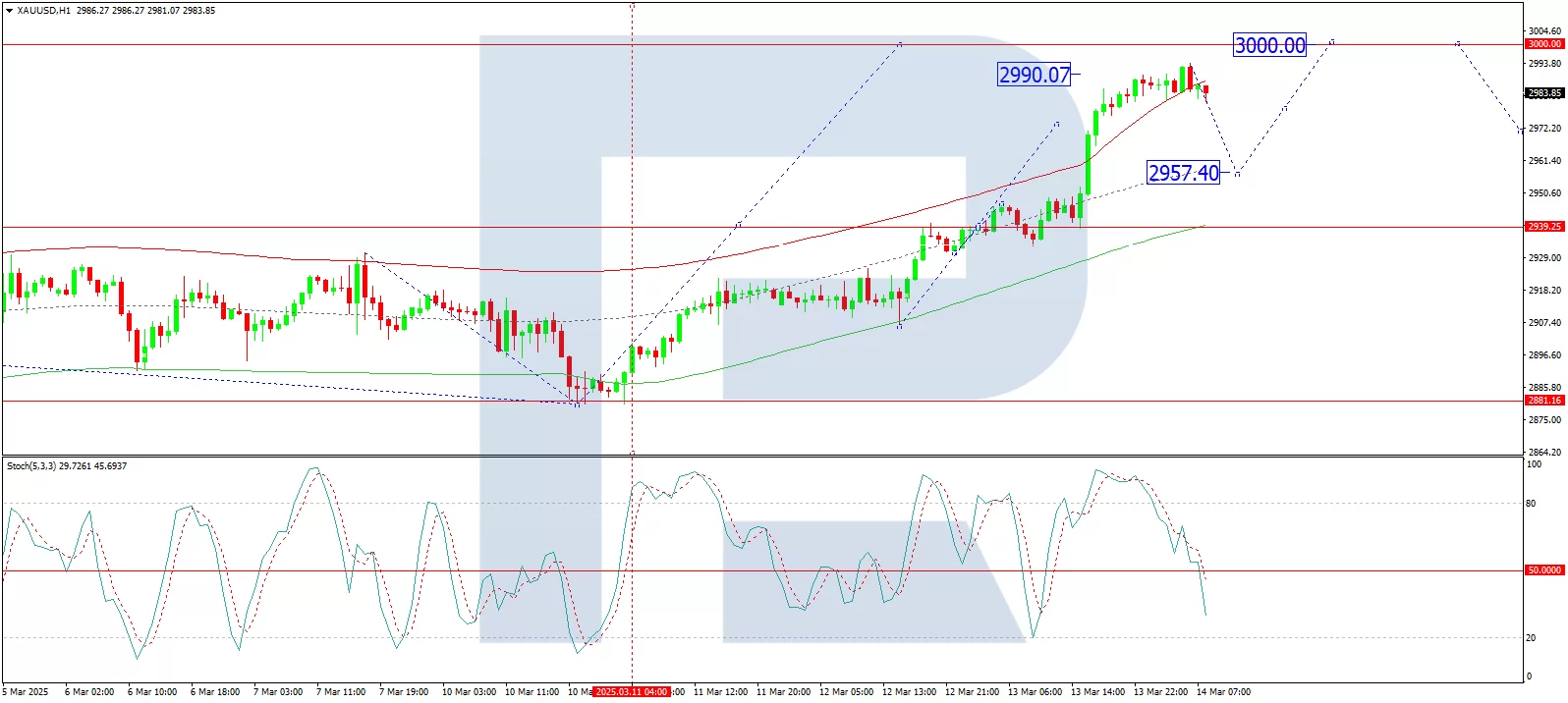

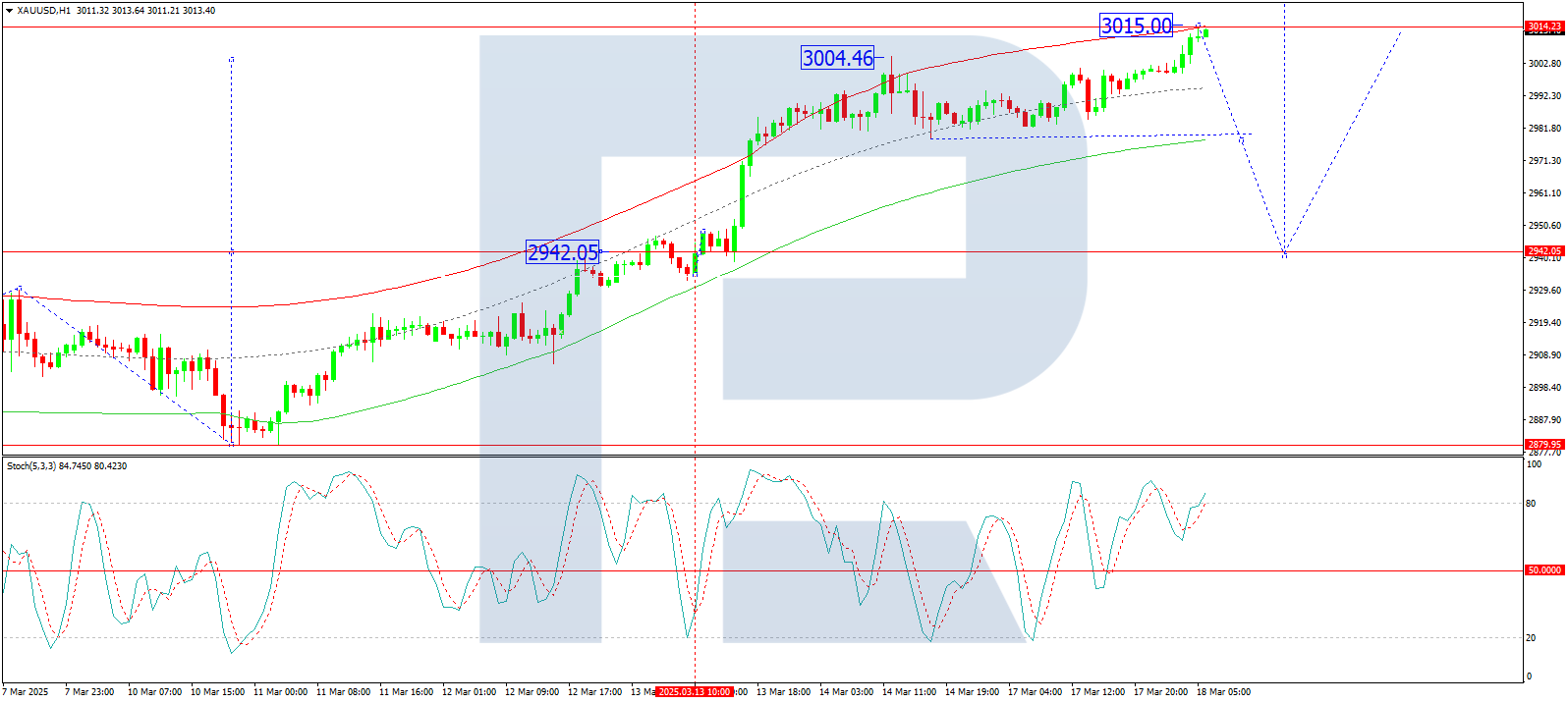

On the H1 chart, XAU/USD has completed the structure of the growth wave, reaching the 3,015 level. We now expect the start of a corrective move toward 2,945. After this correction, the price will likely resume its upward trajectory, targeting the 3,057 level. Upon reaching this target, we will assess the possibility of a more significant correction towards the 2,900 level. This outlook is further confirmed by the Stochastic oscillator. Its signal line is currently below the 80 level and trending downwards towards 20, suggesting a high probability of a corrective phase.

Conclusion

Gold’s record-breaking rally reflects a combination of macroeconomic uncertainty, geopolitical tensions, and technical momentum. With the Federal Reserve’s decision and global developments in focus, the precious metal remains a key asset for investors seeking stability. As the market navigates these dynamics, further milestones for Gold prices appear increasingly likely.

Disclaimer

Any forecasts contained herein are based on the author’s particular opinion. This analysis may not be treated as trading advice. RoboForex bears no responsibility for trading results based on trading recommendations and reviews contained herein.