By RoboForex Analytical Department

The EUR/USD pair rose to 1.1418 before pausing, as bearish sentiment towards the US dollar intensified following the release of disappointing US macroeconomic data and escalating trade tensions.

The dollar is under pressure from weak data and trade uncertainty

The dollar came under renewed pressure after the release of weaker-than-expected US manufacturing activity data for May, which pointed to a deeper-than-anticipated slowdown. These figures indicate that economic risks remain elevated, particularly amid continued trade policy uncertainty under President Donald Trump.

Trump’s recent decision to raise steel import tariffs to 50% sparked fresh concerns and drew sharp criticism from major trading partners, further heightening investor unease.

Tensions with China have also escalated, with Beijing rejecting Trump’s accusations of violating the interim trade deal and vowing retaliatory measures to defend its interests.

Looking ahead, markets will closely monitor a series of US macroeconomic releases due on Tuesday, including job openings, durable goods orders, and factory orders – all of which will help assess the health of the US economy.

The eurozone is also set to publish preliminary inflation data for May, which may influence euro sentiment. However, for now, investors remain optimistic about EUR/USD. Barring any surprises, the pair appears well-supported.

Technical analysis of EUR/USD

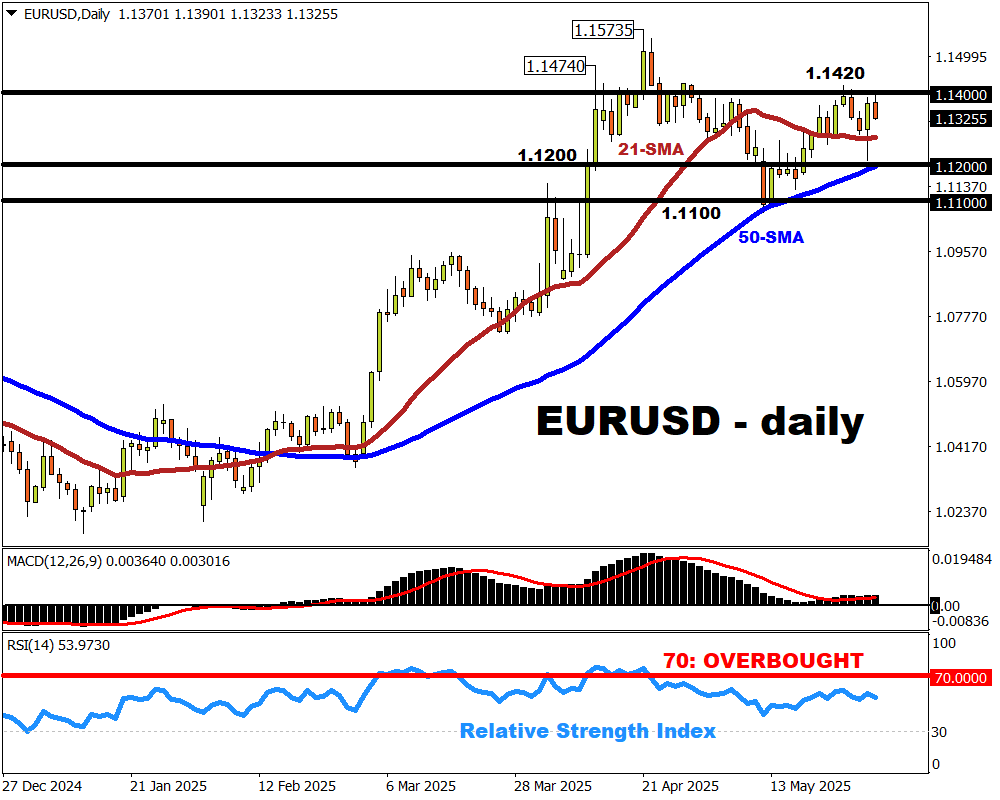

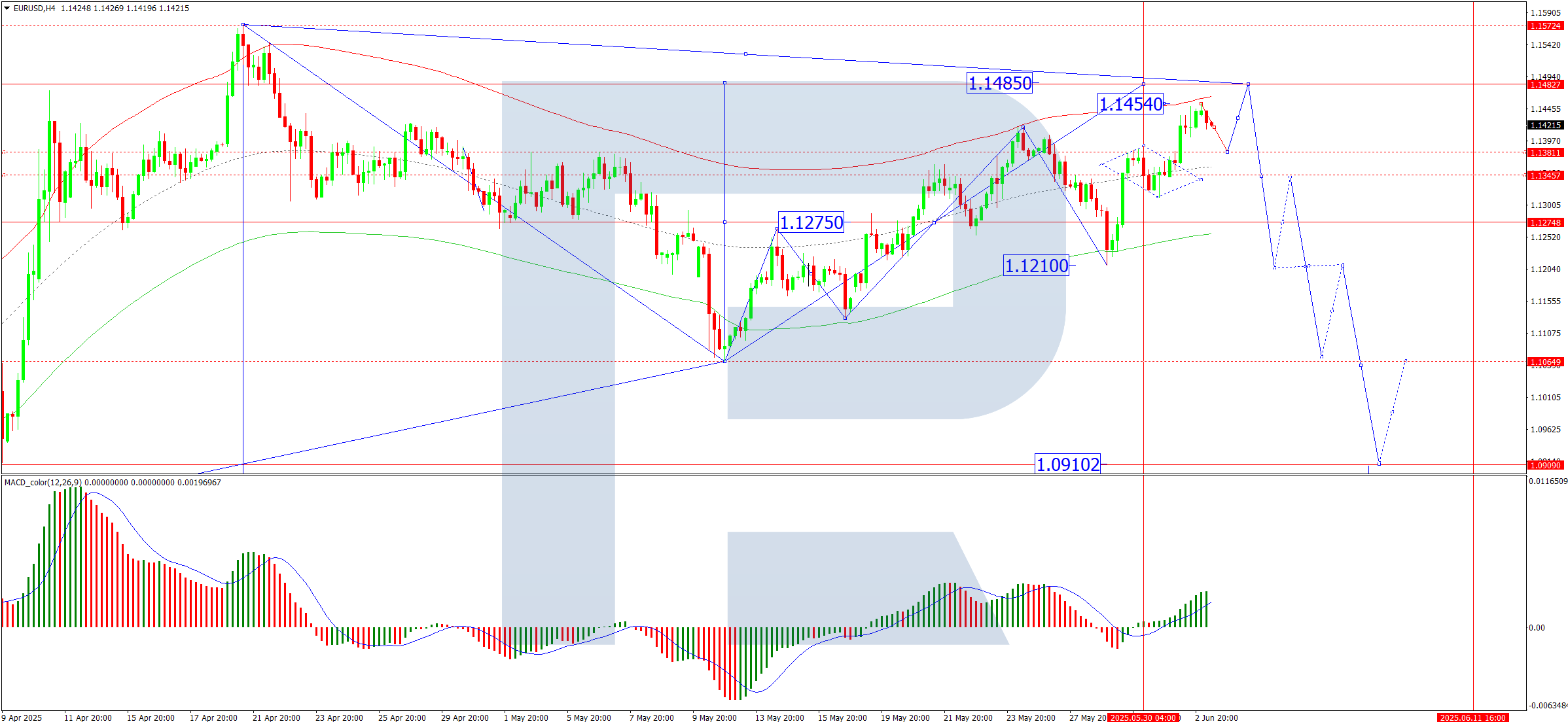

On the H4 chart, EUR/USD is extending the fifth wave of growth towards 1.1485. The market has already met the local target at 1.1450, and a short-term correction to 1.1380 is expected next. Once this pullback concludes, a final push towards 1.1485 is likely, marking the end of the current growth wave. From there, a new downward phase may begin, with a target at 1.1210. The MACD indicator supports this scenario, with its signal line above zero and pointing sharply upwards, indicating continued bullish momentum.

On the H1 chart, EUR/USD formed a consolidation range around 1.1350, broke to the upside, and completed the growth structure, reaching a local target of 1.1450 within the fifth wave. A correction to 1.1380 is anticipated, followed by another growth wave towards 1.1485. The Stochastic oscillator confirms this outlook, with its signal line below 20 and preparing to rise towards 80, signalling a potential bullish continuation after the correction.

Conclusion

EUR/USD remains well-positioned for further gains amid mounting US economic concerns and renewed trade tensions. The pair has short-term support at 1.1380 and faces resistance at 1.1485. A reversal could occur once the current growth wave is exhausted, with 1.1210 as a longer-term downside target. For now, technical indicators and market sentiment continue to point to further upside, particularly if upcoming US data confirms a weakening economic outlook.

Disclaimer

Any forecasts contained herein are based on the author’s particular opinion. This analysis may not be treated as trading advice. RoboForex bears no responsibility for trading results based on trading recommendations and reviews contained herein.