Last week, the U.S. introduced new initiatives aimed at forming a preferential trade bloc for critical minerals like uranium, including coordinated price floors, as part of efforts to counter China’s dominance in this essential market for technology and defense, according to a CNBC report on February 5 by Dylan Butts.

These plans were discussed at a “Critical Minerals Ministerial” in Washington, which included representatives from 54 countries, the European Union, and senior Trump administration officials. Following the event, Washington announced that it had signed bilateral critical minerals agreements with 11 countries, building on 10 similar agreements made over the past five months. Negotiations were also completed with an additional 17 nations.

The Trump administration’s new minerals stockpile initiative, known as “Project Vault,” can encompass any materials identified as “critical” by the U.S. Geological Survey, a White House official told CNBC, according to another February 3 report by Pippa Stevens and Spencer Kimball for the website. The agency, which is part of the Interior Department, lists over 50 minerals as critical, including rare earths, lithium, uranium, and copper. These minerals are considered essential for national security, economic stability, and supply chain resilience. According to the USGS, these minerals are crucial because they “underpin key industries, drive technological innovation, and support critical infrastructure vital for a modern American economy.”

The objectives of these agreements are to tackle pricing challenges, encourage development, create fairer markets, and expand access to financing in the critical minerals sector. Secretary of State Marco Rubio, who hosted the Ministerial, also announced the creation of the “Forum on Resource Geostrategic Engagement (FORGE)” on Wednesday. This partnership aims to coordinate critical mineral policy and projects.

“We have a number of countries that have signed on to that, and many more that we hope will do so… the purpose of FORGE is to foster collaboration and to build a network of partners across the world,” Rubio said.

FORGE will complement an earlier initiative between the U.S. and nine partners, known as “Pax Silica.” While Pax Silica focuses on safeguarding AI-related supply chains, FORGE is designed as a broader platform to coordinate critical mineral policy, pricing, and project development. Rubio highlighted the risks associated with the concentration of critical minerals in “one country,” implicitly referring to China, including geopolitical leverage and potential disruptions from pandemics or instability.

AI, Data Centers Begin Impacting Power Grids

Uranium is becoming one of the most important of these minerals. Predictions of increased electricity consumption from data centers are beginning to materialize, raising concerns about the impact on the power grid and the environment, according to a report by Benjamin Storrow for E&E News/Politico on December 24, 2025.

Commercial electricity demand, which serves as a proxy for data center power usage, rose by 2% in the first nine months of 2025 compared to the same period last year, following a 3% increase in 2024. This marks a significant shift for the U.S. power sector, which had experienced flat electricity demand for much of the past two decades.

Demand is expected to climb even higher as the Trump administration and tech companies aim to outpace China in artificial intelligence development. The consulting firm Grid Strategies forecasts that peak electricity demand nationwide could rise by 166 gigawatts by 2030, equivalent to adding 15 New York Cities over the next five years.

“We’re now seeing in the data what we’ve all been talking about the last couple years,” said Rob Gramlich, CEO of Grid Strategies. He estimated that data centers would contribute to 55% of the growth in U.S. electricity demand over the next five years. The increasing power needs of data centers have become a political issue as electricity costs rise for consumers.

AI data centers and the electrification of various industries are driving a surge in power demand that exceeds global supply, prompting companies, policymakers, and investors to reconsider nuclear power, according to a research report by Morgan Stanley on August 28, 2025. Morgan Stanley Research projects 586 gigawatts (GW) of new global nuclear capacity by 2050, which is 53% higher than their previous forecast last year when analysts noted a “renaissance” in the industry. They now estimate that potential investments in the nuclear value chain could reach US$2.2 trillion by 2050, up from the initial US$1.5 trillion forecast. This increased momentum is expected to benefit several sectors, including uranium mining, nuclear power generation, and the construction of equipment and plants. “The nuclear renaissance has been building for some time already—with 22 nations pledging to triple nuclear capacity by 2050 at the COP28 summit in December 2023, plant life extensions in Europe, a strong pipeline in China, and Japan continuing to restart capacity,” says Tim Chan, Morgan Stanley’s Head of Asia Sustainability Research. “The dual imperatives of decarbonization and energy security are making the nuclear renaissance a truly global investment theme.”

While natural gas is currently the primary alternative to meet AI’s energy needs, technology companies are willing to pay a premium to transition to nuclear energy. “We believe natural gas will be the primary near-term solution for powering AI data centers due to its speed to market, reliability, and flexibility, while nuclear power represents a longer-term clean energy alternative that is likely to gradually increase in importance,” said Stephen Byrd, Morgan Stanley’s Global Head of Sustainability Research. “Gas and nuclear are likely to play complementary roles.”

Uranium Is Now a Critical Mineral

Last fall, the USGS released the final 2025 list of critical minerals deemed essential to mitigate potential risks from disrupted supply chains, reported Nick Mordowanec for Military.com on December 1, 2025. Ten new minerals were added, including uranium, bringing the total to 60.

“This is the most comprehensive, science-based assessment yet of the minerals our nation relies on,” said USGS Director Ned Mamula. “Critical minerals underpin industries worth trillions of dollars, and import dependence puts key sectors at risk. This work helps secure the materials needed for U.S. economic growth and technological leadership.”

Trump has called for a quadrupling of nuclear power by 2050, the article reported.

Christo Liebenberg, co-founder and president of the U.S.-based uranium enrichment company LIS Technologies, told Military.com that there is “huge market demand” for uranium to bolster a domestic electricity grid facing challenges from expanding AI data centers across the country.

He noted the significance of the critical list now including 60 minerals — more than half of the 118 elements on the periodic table.

“Being on that list, it’s clear that it triggers a whole set of advantages,” Liebenberg said. “That makes mining uranium in the U.S. a lot easier, faster, and more attractive to investors. It’s like flipping a switch that says, ‘OK, everybody, uranium is now important. Let’s make mining in the US easier, cheaper, faster, and more predictable.’ Of course, this is exactly what would stimulate production. But the thing is, it doesn’t stop just with mining. Being on that list actually has a ripple effect through the entire nuclear fuel supply chain.”

Key actions and impacts for uranium under the U.S. critical minerals framework include fast-tracked permitting, reduced foreign reliance, strategic stockpiling, improved support for the mining industry, and energy security.

Companies With Tangible Operational Progress in the Spotlight

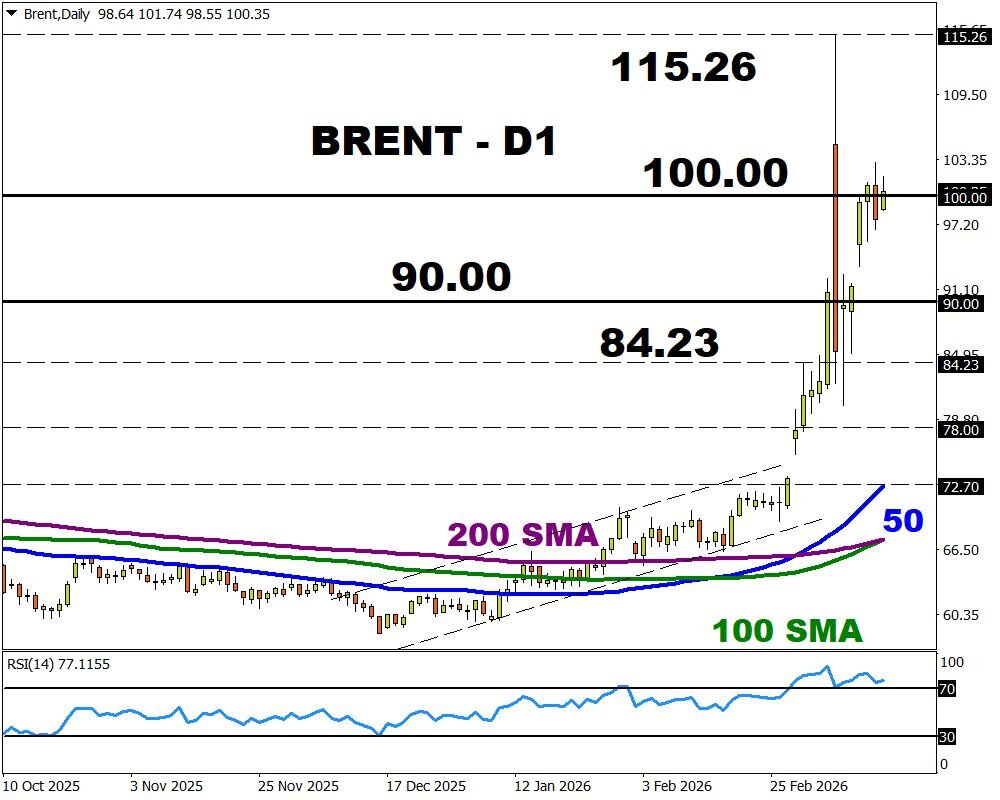

The uranium sector enters 2026 at a pivotal moment where operational execution increasingly distinguishes credible investment opportunities from speculative ventures, according to Henry Mann writing for Crux Investor on January 27. Spot uranium prices reached US$100 per pound in January 2026, marking 17-month highs. However, equity valuations across the sector reflect ongoing institutional caution about timing mismatches between nuclear buildouts and the upstream uranium supply response.

In this context of structural demand growth and supply fragility, companies demonstrating tangible operational progress — such as permitting momentum — are positioning themselves to attract capital as the gap between operational reality and equity pricing narrows, Mann wrote.

Chris Frostad, CEO of Purepoint Uranium, explains the demand fundamentals, according to Mann: “When a reactor begins operation, it creates a customer relationship lasting 40 years or more. Reactors operate under strict refueling schedules, and utilities know precisely how much fuel they will require annually for years into the future.” The growth in artificial intelligence infrastructure and data centers adds incremental demand considerations, though existing reactor fleets provide the foundation of predictable consumption.

In 2025, utilities contracted for approximately 82-85 million pounds of uranium, while replacement requirements approached 150-180 million pounds. However, utility contracting does not follow smooth patterns, as buyers may contract for 250 million pounds in a single year when conditions align with their strategies.

Laramide Resources Ltd.

One company uniquely positioned to take advantage of these events is Laramide Resources Ltd. (LAM:TSX; LMRXF:OTCQX: LAM:ASX), a uranium developer with both in-situ and hard-rock deposits located in the southwestern United States and Australia.

In June 2025, Laramide announced that its advanced-stage uranium projects, Crownpoint-Churchrock and La Jara Mesa in New Mexico, were designated as FAST-41 covered projects by the Federal Permitting Improvement Steering Council. This designation is part of the federal infrastructure permitting program established under Title 41 of the Fixing America’s Surface Transportation Act. It underscores the strategic importance of Laramide’s projects and streamlines the evaluation process.

The FAST-41 designation places these uranium projects among a select group of federally prioritized energy initiatives, receiving enhanced permitting coordination and transparency to support the Department of Energy’s domestic uranium reserve and the U.S. government’s broader energy-security goals.

“The project comprises two geographically distinct deposits: one at Crownpoint and the other at Churchrock,” the company said in a recent recap sent to Streetwise Reports. “They are unified under a single U.S. Nuclear Regulatory Commission (NRC) Source Material License. This regulatory status differentiates the project from many U.S. peers that remain at earlier permitting stages.”

Churchrock’s current NI 43-101 Inferred Mineral Resource is 50.8 million pounds U₃O₈ based on historic drilling consolidated into a modern database. Crownpoint adds an NI 43-101 Inferred Mineral Resource of 5.1 million pounds U₃O₈, also derived from historic datasets and interpreted for ISR-style mineralization geometry, the company said.

Laramide’s U.S. portfolio is “increasingly relevant against the backdrop of declining domestic uranium production and growing demand tied to nuclear energy, including life-extensions of existing reactors and new investments linked to data centers and advanced nuclear technologies,” Laramide said in the document. “With the majority of U.S. uranium supply currently imported, projects that are licensed, permitted, or moving visibly through federal processes have taken on heightened strategic importance.”

Analyst: Co. ‘Scans Very Well on Value’

Laramide is a uranium exploration and development company with projects in the western United States and Australia, according to Beacon Securities Analyst Michael Curran in an updated research note on November 3, 2025.

Crownpoint-Churchrock’s designation as a FAST-41 project is expected to streamline the permitting process as part of the U.S. government’s initiative to advance domestic critical mineral and metal projects toward production. This followed a similar designation for LAM’s La Jara Mesa project in early May, also in New Mexico.

“In mid-July, LAM’s Westmoreland project in Queensland, Australia, received a Mineral Development License (MDL), which allows Laramide to proceed with studies to advance the project towards a Mining Lease (ML) application,” the analyst wrote. “This work is likely to include metallurgical testing, environmental, engineering and design studies, as well as feasibility-related work.”

In July, Laramide raised gross proceeds of CA$12 million by issuing 20 million common shares at CA$0.60 each.

Beacon’s 12-month fair value increased from CA$1.45 to CA$1.50 per LAM share. As this still represents significant upside from current price levels, the firm maintained its BUY rating for Laramide Resources.

“In our view, Laramide represents an attractive investment for exposure to uranium developments in the top-tier mining jurisdictions,” Curran wrote. “Laramide’s assets are in areas of historical uranium mining, thus should have lower barriers to development than other jurisdictions.”

Curran said the firm’s preferred valuation for mining equities uses cash flow-based metrics such as P/CF and P/NAV, utilizing life-of-mine production forecasts and commodity price assumptions.

“However, for earlier-staged explorers where it is arguably too early to create a DCF model with much accuracy, we employ a more basic valuation metric of Adjusted Market Capitalization per total resource (AMC/lb) or Enterprise Value per resource pound (EV/lb),” the analyst wrote. For Laramide, he employed a hybrid model using DCF-based valuation for Churchrock and EV/lb valuation methods for the company’s other U.S. and Australian assets. Curran noted that Beacon currently did not attribute any value to the Kazakhstan assets.

Retail: 70%

Strategic Investors: 19%

Insiders and Management: 11%

*Share Structure as of 2/9/2026

Churchrock is recognized as a development-ready asset, as noted by SCP Equity Research analysts J. Chan, E. Magdzinski, and K. Kormpis in a June 3 research note. The company’s January 2024 PEA forecasts a 31-year operational lifespan, producing 31.2 million pounds at an all-in sustaining cost of US$34.83 per pound using ISR extraction methods.

With uranium valued at US$75 per pound, this results in a US$239 million after-tax NPV, strongly supporting Laramide’s evaluation. The plan involves accelerating wellfield development to increase output to 2-3 million pounds, thereby shortening the operational timeline while improving financial outcomes.

“We think Laramide scans very well on value, with two projects of reasonable size/scale in the U.S. and Australia (arguably two of the top three jurisdictions in today’s geopolitically bifurcating market),” the analysts remarked, giving the stock a Buy rating with a CA$1.35 per share target price.

Ownership and Share Structure1

Laramide reports that insiders and management hold about 11% of the company, with strategic corporate entity Boss Energy Ltd. owning 19%. The remainder is held by retail investors.

Other major shareholders include Alps Advisors with 9.4%, Henderson with 6.82%, Mirae Asset Global Investments LLC with 4.78%, and Vident Investment Advisory LLC with 1.1%. As of February 9, its market capitalization is CA$215.06 million, with 283.62 million shares outstanding. It trades within a 52-week range of CA$0.46 to CA$0.91.

Important Disclosures:

- Laramide Resources Ltd. is a billboard sponsor of Streetwise Reports and pays SWR a monthly sponsorship fee between US$3,000 and US$6,000.

- Steve Sobek wrote this article for Streetwise Reports LLC and provides services to Streetwise Reports as an employee.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

1. Ownership and Share Structure Information

The information listed above was updated on the date this article was published and was compiled from information from the company and various other data providers.

{kind=link}