By JustMarkets

By Monday’s close, the Dow Jones Index (US30) rose by 0.44%. The S&P 500 Index (US500) gained 1.55%. The Nasdaq (US100) closed higher at 2.69%. Markets were supported by comments from Federal Reserve officials. New York Fed President John Williams pointed to the possibility of rate cuts in the near term, while Fed Governor Christopher Waller noted that recent labor market weakness increases the likelihood of a December cut. According to CME FedWatch, the probability of a 25 bps cut at the December 9-10 meeting is estimated at about 79%.

The technology sector led the rally. Broadcom surged 11.1% amid renewed interest in AI infrastructure. Alphabet gained more than 6% after news related to Gemini 3 lifted its market capitalization above Microsoft. Tesla rose by 6.8% following Elon Musk’s statements about progress in developing next‑generation AI chips.

European stocks recovered and ended Monday with modest gains, recouping part of last week’s losses. Germany’s DAX (DE40) rose by 0.64%, France’s CAC 40 (FR40) closed down 0.29%, Spain’s IBEX 35 (ES35) gained 0.92%, and the UK’s FTSE 100 (UK100) closed negative 0.05%. The technology sector was a clear leader, following the positive momentum from US markets. ASML shares rose by 3%, Infineon gained 3.5%, while Siemens and Schneider Electric also closed higher.

On Tuesday, silver climbed above $51 per ounce, reaching a weekly high amid heightened expectations of imminent US rate cuts. Dovish comments from Fed officials supported the metal’s rise: Governor Christopher Waller expressed readiness to back a December cut, citing growing labor market risks, echoing recent remarks from San Francisco Fed President Mary Daly and New York Fed President John Williams.

WTI crude oil prices rose Monday to $59 per barrel, partially recovering after last week’s 3.4% drop, as markets assessed the likelihood of a peace agreement between Russia and Ukraine. The US‑brokered talks reportedly made some progress, though key disagreements remain. A potential deal could have major implications for the oil market. If sanctions are eased, Russian oil could return to the global market, increasing the expected supply surplus in 2026.

The US natural gas prices fell to $4.53/MMBtu, as the market remains well supplied thanks to near‑record production and high inventories. Output growth has kept stocks about 4% above seasonal norms. However, recent cold weather triggered the first drawdown of the winter. Rising exports partly offset high production, but the market balance remains comfortable.

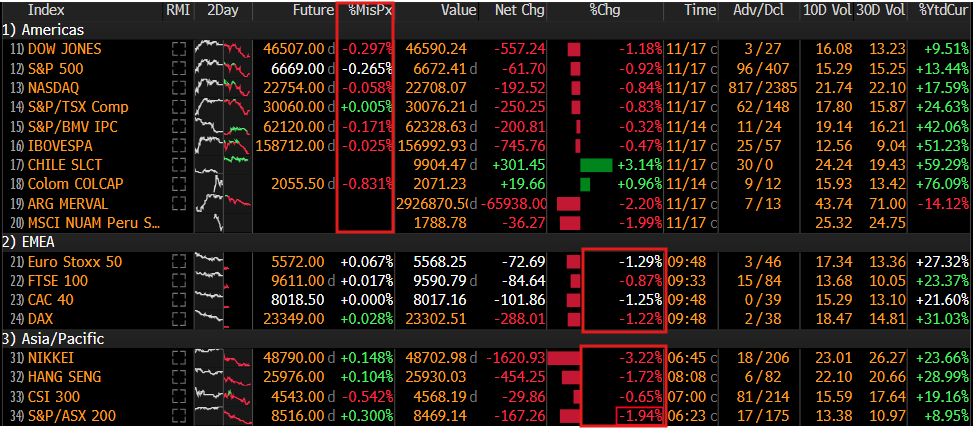

Asian markets traded mixed yesterday. Japan’s Nikkei 225 (JP225) fell by 2.40%, China’s FTSE China A50 (CHA50) dropped 2.57%, Hong Kong’s Hang Seng (HK50) gained 1.97%, and Australia’s ASX 200 (AU200) closed positive 1.29%. The Hang Seng broke a six‑day losing streak, supported by gains in US indices. Technology once again showed the strongest momentum: the Tech Index rose by 2.7% amid reports that the Trump administration may allow Nvidia to sell H200 chips to China. Additional support came from expectations of potential stimulus measures ahead of the Central Economic Work Conference in Beijing next month.

S&P 500 (US500) 6,705.12 +102.13 (+1.55%)

Dow Jones (US30) 46,448.27 +202.86 (+0.44%)

DAX (DE40) 23,239.18 +147.31 (+0.64%)

FTSE 100 (UK100) 9,534.91 −4.80 (−0.05%)

USD Index 100.18 +0.00% (+0.00%)

News feed for: 2025.11.25

- US Producer Price Index (m/m) at 15:30 (GMT+2); – USD (HIGH)

- US Retail Sales (m/m) at 15:30 (GMT+2); – USD (MED)

- US Pending Home Sales (m/m) at 17:00 (GMT+2). – USD (MED)

By JustMarkets

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.