By JustMarkets

The US stock market rose on Wednesday. By the end of the day, the Dow Jones (US30) increased by 0.49%. The S&P 500 (US500) gained 0.79%. The tech-heavy NASDAQ (US100) closed higher by 1.51%. The US stock market displayed a confident “bullish” sentiment, largely ignoring geopolitical tensions. The primary driver of optimism was a decline in WTI oil prices: the market reacted with relief to Treasury Secretary Scott Bessent’s plan to protect oil traffic in the Persian Gulf. Even the official confirmation of the 15% global tariffs taking effect this week failed to dampen risk appetite, as strong US macro data outweighed trade concerns. The February ADP report showed private sector employment growth of 185k (above the 145k prediction), while wage growth slowed. This created an ideal “soft landing” picture – a strong economy with cooling inflation in the services sector. The semiconductor sector led the rally: Micron and AMD shares jumped more than 5.5%, while Amazon rose 3.9%. Investors are betting that tech giants will remain resilient even under inflationary pressure.

The market was also stirred by a New York Times report stating that Iranian intelligence, through intermediaries, reached out to the CIA to discuss ceasefire terms. Despite this rare signal toward de-escalation, investor reaction remained cautious. US officials expressed doubt regarding Iran’s sincerity, viewing it as an attempt to buy time. Following the deaths of Iran’s top leadership, it remains unclear who possesses the authority to negotiate, which intensifies political chaos and sustains demand for safe-haven assets.

Bitcoin has consolidated above the psychological threshold of $72,000, holding near monthly highs as markets gradually stabilize following the escalation in the Middle East. Despite disruptions in global logistics through the Strait of Hormuz and the initial flight to safety, the digital coin demonstrated exceptional resilience. Notably, in recent days, the flagship of the digital assets market outperformed traditional gold in recovery pace: while the precious metal dipped by 2%, Bitcoin gained about 12%, effectively seizing the status of a priority haven amid geopolitical turbulence.

European markets showed a strong bullish reversal, almost completely recouping the losses of “Black Tuesday.” The German DAX (DE40) rose by 1.74%, the French CAC 40 (FR40) closed up 0.79%, the Spanish IBEX 35 (ES35) gained 2.49%, and the British FTSE 100 (UK100) closed up 0.80%. Despite the ongoing conflict in the Middle East, diplomatic signals from Washington and the stabilization of the energy market provided Europe with a necessary breathing spell.

The Swiss franc (CHF) held its position near 0.78 against the US dollar, remaining at historic highs amid a complex interplay of geopolitics and domestic economics. Investors continue to view the franc as a “safe harbor,” though further growth potential is limited by the hawkish rhetoric of the SNB. Internal conditions are complicated by fresh inflation data: in February, the CPI rose 0.6% for the month, but annual inflation stalled at 0.1%. This is a critically low figure, sitting at the very edge of the SNB’s target range (0-2%). SNB Vice Chairman Antoine Martin confirmed that the bank is ready for aggressive currency interventions, fearing that an overly strong franc will cheapen imports and push the economy into a deflationary spiral.

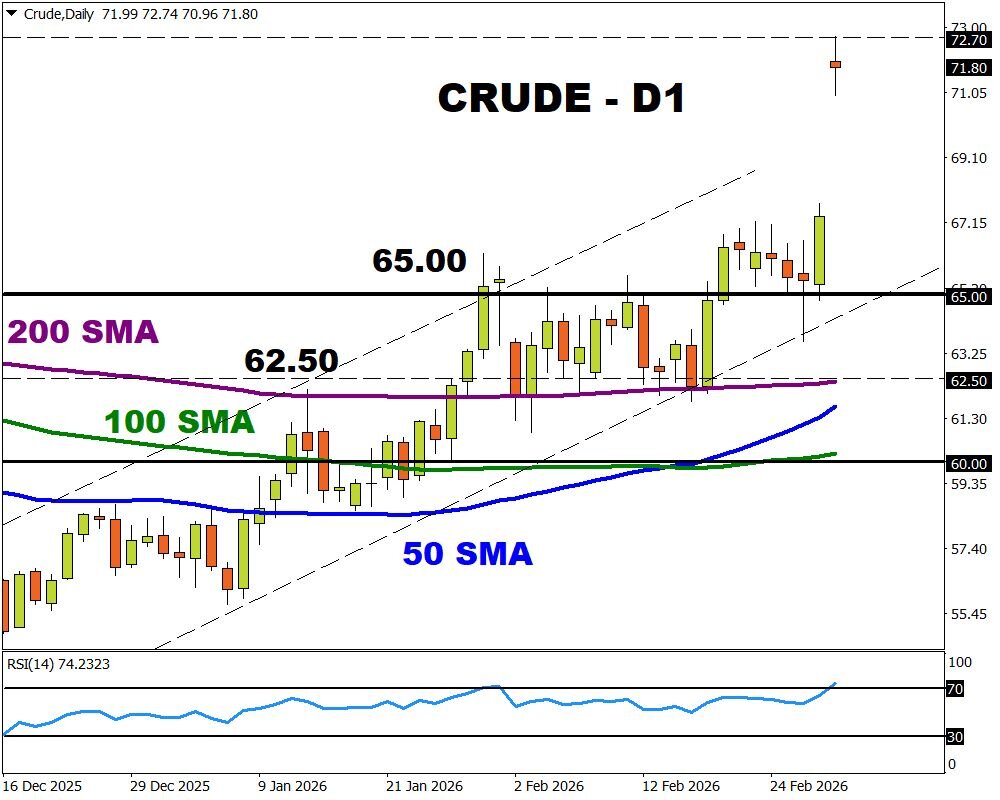

The oil market moved toward a fragile stabilization, with WTI crude futures declining to $74 per barrel. This marked the first drop in prices since the start of direct military confrontation between the US and Iran. The primary factor for the price decline was the decisive economic measures taken by the Donald Trump administration aimed at preventing a global energy collapse. Specifically, the President directed the International Development Finance Corporation (DFC) to implement a political risk insurance mechanism with affordable rates for vessels operating in the conflict zone. Despite verbal interventions by Scott Bessent and US promises of military escort for tankers, the physical situation in the Persian Gulf remains paralyzed. Commercial shipping through the Strait of Hormuz has effectively ceased following IRGC threats to attack any vessels. Most large tankers remain at anchor.

The US natural gas prices (XNG) broke a three-day rally on Wednesday, falling below $3 per MMBtu. The market reacted to the first signals of possible de-escalation in the Middle East: reports of Iran’s readiness for negotiations reduced fears of a global fuel shortage, leading to a price correction, following oil. Despite positive news regarding possible contacts between Tehran and Washington, the physical blockage of supplies from the Persian Gulf remains a reality. The Strait of Hormuz remains closed to most commercial traffic, and Qatar’s largest LNG plant has yet to resume operations.

Asian markets traded lower yesterday. The Japanese Nikkei 225 (JP225) fell by 3.61% during the session, the FTSE China A50 (CHA50) dropped 1.60%, the Hong Kong Hang Seng (HK50) fell 2.01%, and the Australian ASX 200 (AU200) showed a negative result of 1.91%. On Thursday, however, Chinese stock indices showed a confident rebound. The recovery was driven by improved global sentiment and the stabilization of inflation expectations, despite ongoing tensions between Washington and Tehran. Beijing intends to counter deflationary risks and external tariff pressure through aggressive subsidies for the high-tech sector, R&D, and support for domestic consumer demand.

S&P 500 (US500) 6,869.50 +52.87 (+0.78%)

Dow Jones (US30) 48,739.41 +238.14 +(0.49%)

DAX (DE40) 24,205.36 +414.71 (+1.74%)

FTSE 100 (UK100) 10,567.65 +83.52 (+0.80%)

USD Index 98.76 -0.28% (-0.29%)

News feed for: 2026.03.05

- Australia Trade Balance (m/m) at 02:30 (GMT+2); – AUD (MED)

- Switzerland Unemployment Rate (m/m) at 08:45 (GMT+2); – CHF (MED)

- Eurozone Retail Sales (m/m) at 12:00 (GMT+2); – EUR (MED)

- Eurozone ECB Monetary Policy Meeting Accounts at 14:30 (GMT+2); – EUR (LOW)

- US Initial Jobless Claims (w/w) at 15:30 (GMT+2); – USD (MED)

- US Natural Gas Storage (w/w) at 17:30 (GMT+2). – XNG (HIGH)

By JustMarkets

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.