By JustMarkets

On Friday, trading on the US stock market ended with a decline. The Dow Jones (US30) fell by 0.26% (-0.75% for the week). The S&P 500 (US500) dropped 0.61% (-0.30% for the week). The tech-heavy NASDAQ (US100) closed lower by 0.93% (-0.15% for the week). The US stock market ended the second week of March 2026 in the red, recording its third consecutive week of losses due to a sharp escalation of the military conflict with Iran. Secretary of Defense Pete Hegseth’s decision to launch massive strikes on Iranian facilities in response to attacks in the Persian Gulf effectively confirmed the war’s transition into a protracted phase, triggering a flight of capital toward the dollar and safe-haven assets. The situation is exacerbated by the unresolved blockade of the Strait of Hormuz, which forces investors to price in a global stagflation scenario in which high energy prices coincide with slowing economic growth. The most painful blow fell on the technology sector and companies with high debt loads, sensitive to rising bond yields. Adobe shares plummeted 7.6% following a disappointing prognosis and the sudden resignation of its CEO, which served as a catalyst for a sell-off in the software industry, affecting even market favorites like Palantir and Meta.

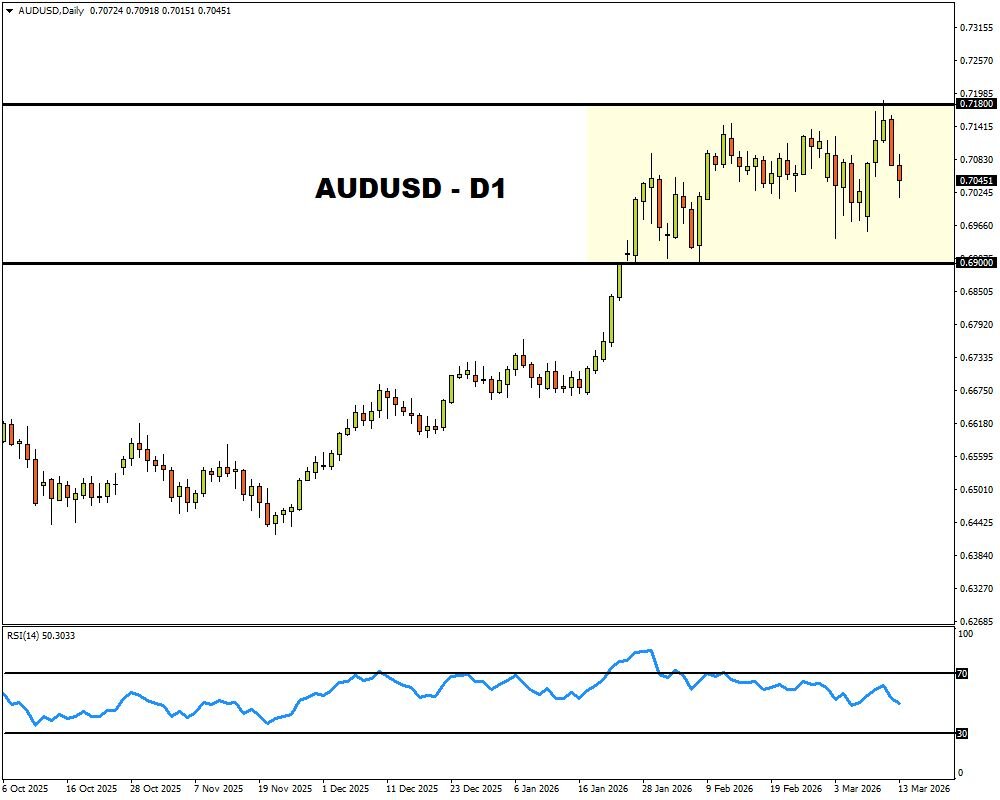

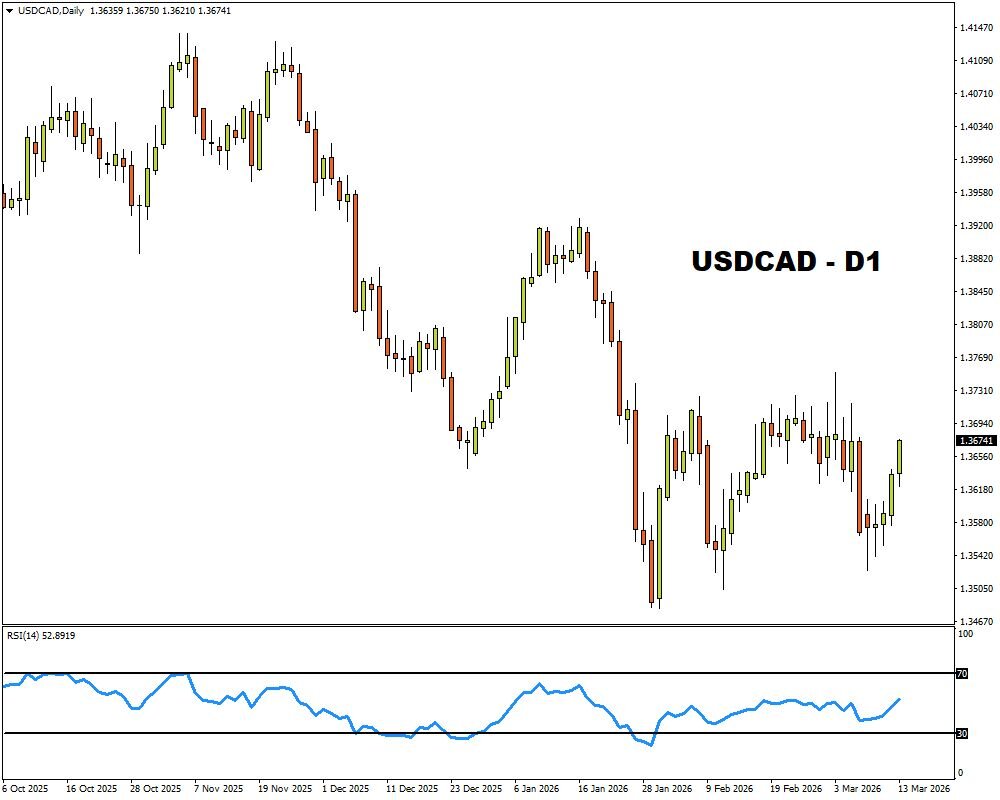

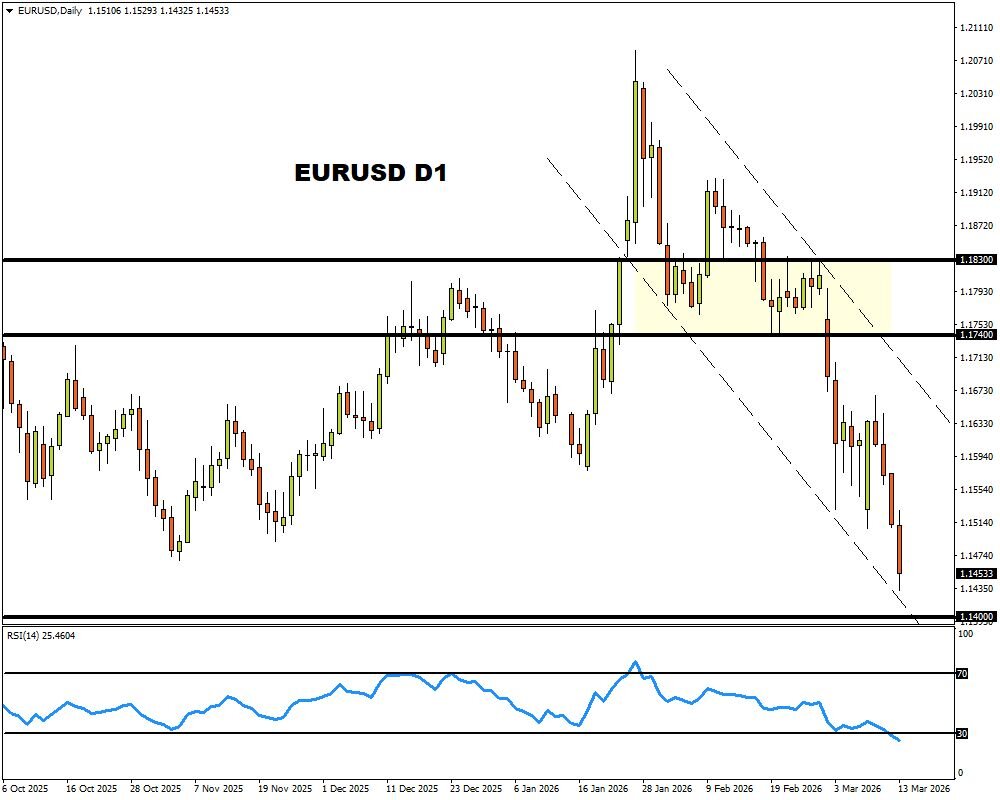

The Canadian dollar (CAD) is showing notable weakness, consolidating at the 1.381 level against the US dollar. This decline is driven by a combination of deeply disappointing domestic data and the global dominance of the US currency. The fresh February labor market report for Canada shocked investors: the economy lost 84,000 jobs, and the unemployment rate jumped to 6.7%. The situation was aggravated by a slump in the manufacturing sector, where January sales crashed by 3% (to C$68.7 billion) – the worst result in nine months, confirming a serious cooling of the economy. While the Bank of Canada is expected to maintain its rate at 2.25% at its March 18 meeting to contain inflation, the widening yield gap with US treasuries continues to pull the Canadian currency down.

On Friday, European stock markets closed in the red, recording bond yield growth to their highest levels in 15 years amid the prolonged energy crisis. The German DAX (DE40) fell by 0.60% (+2.00% for the week), the French CAC 40 (FR40) closed up 1.04% (+1.16% for the week), the Spanish IBEX 35 (ES35) dropped 0.47% (+2.95% for the week), and the British FTSE 100 (UK100) closed down 1.24% (-5.33% for the week). Investors have begun pricing in a scenario of prolonged stagflation: the blockade of the Strait of Hormuz and the war with Iran continue to drive up energy prices, forcing the ECB to consider the possibility of further rate hikes. The European banking sector also found itself at the center of the sell-off, losing a significant portion of its capitalization due to private credit risks and deteriorating divination for net interest margins. The week’s laggards included Deutsche Bank, which collapsed to a nine-month low, and UniCredit, whose quotes reached levels last seen in late 2024.

On Monday, Platinum quotes (XPT) strengthened at the $2,100 per ounce level, showing resilience amid volatility in the precious metals sector. This positive trend is supported by a chronic supply deficit, which the WPIC predicts will persist for the fourth consecutive year. Although the deficit is expected to narrow slightly to 240,000 ounces in 2026, total above-ground stocks continue to deplete and could fall to critical levels by the end of the year.

WTI crude oil prices consolidated above $99 per barrel, briefly peaking at $102.40. The market is reeling as the conflict enters its third week: after US forces launched massive strikes on military targets on Kharg Island during Operation “Epic Fury,” traders are seriously concerned about the safety of the region’s energy infrastructure. Although the recent strikes targeted only mine and missile warehouses, President Donald Trump explicitly warned that the island’s oil terminals, through which 90% of Iranian exports pass, will be the next target if Tehran does not end the blockade of the Strait of Hormuz.

By mid-March 2026, a turning point emerged in the US gas market: Henry Hub natural gas prices fell below $3.15 per MMBtu, losing about 3% of their value. Despite the ongoing blockade of the Strait of Hormuz and disruptions in Qatari LNG supplies, domestic factors took precedence – expectations of warm spring weather sharply reduced heating demand, and the weekly EIA report showed a storage withdrawal of only 38 billion cubic feet, significantly lower than expected. Fundamental pressure on prices is also exerted by record domestic production, which reached a historic high of 118.5 billion cubic feet per day, allowing the US to compensate for the global market deficit without compromising its own reserves.

Asian markets also partially recovered last week. The Japanese Nikkei 225 (JP225) rose by 3.04% over the trading week, the FTSE China A50 (CHA50) jumped at 2.64%, the Hong Kong Hang Seng (HK50) climbed up 1.82%, and the Australian ASX 200 (AU200) showed a positive result of 0.20% over 5 days.

On Monday, the offshore yuan (CNY) showed a weak attempt at stabilization, rising to the 6.901 mark against the US dollar. This slight increase broke last week’s prolonged decline and was the market’s reaction to an unexpectedly strong block of macroeconomic data from the PRC for January-February. Faster-than-prediction growth in industrial production and retail sales, along with a 1.8% rise in fixed-asset investment, created a short-term foundation for the national currency, confirming the resilience of China’s manufacturing sector against external shocks.

S&P 500 (US500) 6,632.19 −40.43 (−0.61%)

Dow Jones (US30) 46,558.47 −119.38 (−0.26%)

DAX (DE40) 23,447.29 −142.36 (−0.60%)

FTSE 100 (UK100) 10,261.15 −44.00 (−0.43%)

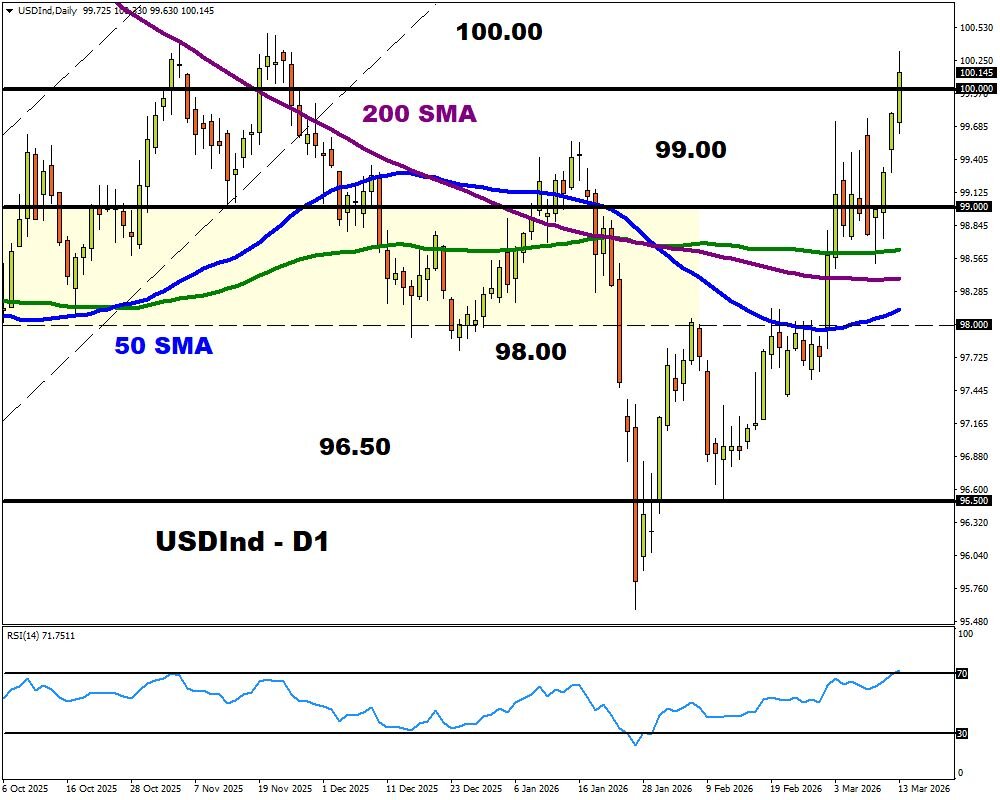

USD Index 100.50 +0.76% (+0.76%)

News feed for: 2026.03.16

- China Industrial Production (m/m) at 04:00 (GMT+2); – CHA50, HK50 (MED)

- China Retail Sales (m/m) at 04:00 (GMT+2); – CHA50, HK50 (MED)

- China Unemployment Rate (m/m) at 04:00 (GMT+2); – CHA50, HK50 (MED)

- Canada Consumer Price Index (m/m) at 14:30 (GMT+2); – CAD (HIGH)

- US Industrial Production (m/m) at 15:15 (GMT+2). – USD (MED)

By JustMarkets

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

A mechanical claw holds a polymetallic nodule, one of several seafloor sources of critical minerals.

A mechanical claw holds a polymetallic nodule, one of several seafloor sources of critical minerals.

{kind=link}