By ForexTime

- Iran war keeps world on edge

- Prediction markets put odds of a ceasefire by end of April ↓ 50%

- New launched gold index/futures offset CFD risk

- Geopolitics + NFP = fresh volatility

- Technical levels – $4600 and $4300

Market sentiment remains fragile as the Iran war keeps the world on edge.

Mixed signals, ongoing conflict and disruptions around the Strait of Hormuz have sparked extreme levels of volatility. Washington talks up peace deals, but Tehran rejects repeatedly.

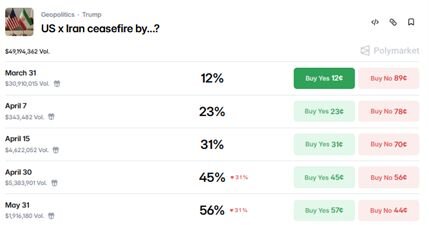

Prediction markets are putting the odds of a US-Iran ceasefire by end-April below 50%.

Given the growing uncertainty, this could spell more volatility in the week ahead already packed with high-impact data:

Monday, 30th March

- JPY: Retail Sales (Feb)

- EUR: Eurozone Economic Confidence

- GER40: German Inflation Rate (March)

- GOLDInd: Dallas Fed Manufacturing Index, New York Fed President John Williams speech

Tuesday, 31st March

- CNH: China manufacturing PMI, non-manufacturing PMI

- AUD: RBA Meeting Minutes

- EUR: Inflation Rates Flash (March)

- JPY: Japan Tokyo CPI, unemployment, industrial production, retail sales

- GOLDInd: US Conference Board consumer confidence

Wednesday, 1st April

- CNH: RatingDog Manufacturing PMI (March)

- CAD: S&P Global Manufacturing PMI (March)

- OIL: EIA Crude Oil Stocks

- GBP: UK S&P Global Manufacturing PMI

- GOLDJ6: US Retail Sales, ADP Employment, ISM Manufacturing PMI

Thursday, 2nd April

- CHF: Switzerland CPI

- GOLDInd: Initial Jobless Claims

Friday, 3rd April

- CNY: RatingDog Services PMI

- GOLDInd: US NFP (March), ISM Service PMI

Last week, gold saw its biggest weekly loss since 1983 despite the deepening conflict.

The culprits were a broadly stronger dollar and fears around conflict-induced inflation resulting in higher US interest rates.

Considering how volatility may remain a key theme, FXTM’s newly launched Gold Index and Futures may be ideal for offsetting spot CFD risk.

FXTM’s GOLDJ6 future

FXTM’s GOLDJ6 is 100% pegged to CME Group Futures price for absolute price clarity, charging traders zero swap when holding overnight positions.

This asset is a gift for active and long-term traders who want full price transparency without financing drag of holding positions over extended periods.

FXTM’s GOLDInd

FXTM’s GOLDInd tracks the spot/future price with fixed swap and spreads.

This asset is ideal for traders who want to hold the position over an extended period at a fixed cost, avoiding surprise overnight charges or widening spreads sparked by volatility.

With all the above said, here are 3 key factors that may influence Gold Futures & Indices.

1) Ongoing Iran conflict

In the latest twist to the Iran war, Trump has extended his deadline for Iran to strike a deal with the US by 10 days.

This development comes after Iran rejected the US ceasefire proposal and responded with its own negotiation plans.

It’s still unclear who the US is engaging in talks with the Strait of Hormuz still effectively closed amid the ongoing conflict.

- If the conflict deepens with both sides attacking key energy infrastructure, gold futures/index may dip as surging oil prices fuel inflation fears.

- Any signs of easing tensions and re-opening of the Straight of Hormuz to the US may weaken gold as inflation concerns cool.

2) US March NFP

The March US jobs report on Friday 3rd April will act as a key gauge over the health of the labour markets.

Here’s what economists predict for this closely-watched jobs report:

- Headline NFP figure: 51,000 (new jobs added to US labour market)

If so, this would be a sharp rebound from February’s -92,000 headline NFP figure.

- Unemployment rate: 4.4%

If so, this would match February’s unemployment rate

- Average hourly earnings month-on-month (March 2026 vs. Feb 2026): 0.3%

If so, this would be lower than February’s figure.

Note: Other key data in the week including the retail sales, ADP and ISM Manufacturing figures may offer key insight into the health of the US economy.

- A stronger-than-expected US jobs data may boost bets around the Fed hiking rates.

- A weaker-than-expected figure could cool bets around Fed hikes.

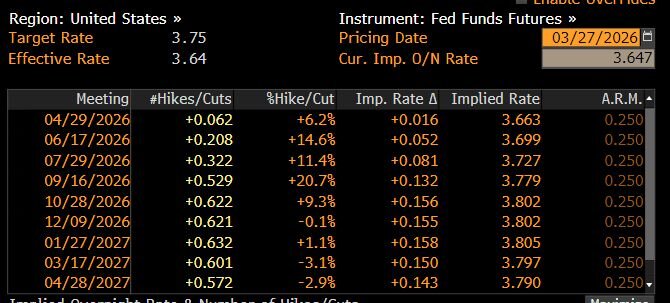

Note: Traders are currently pricing a 22% chance that the Fed will hike rates by June 2026.

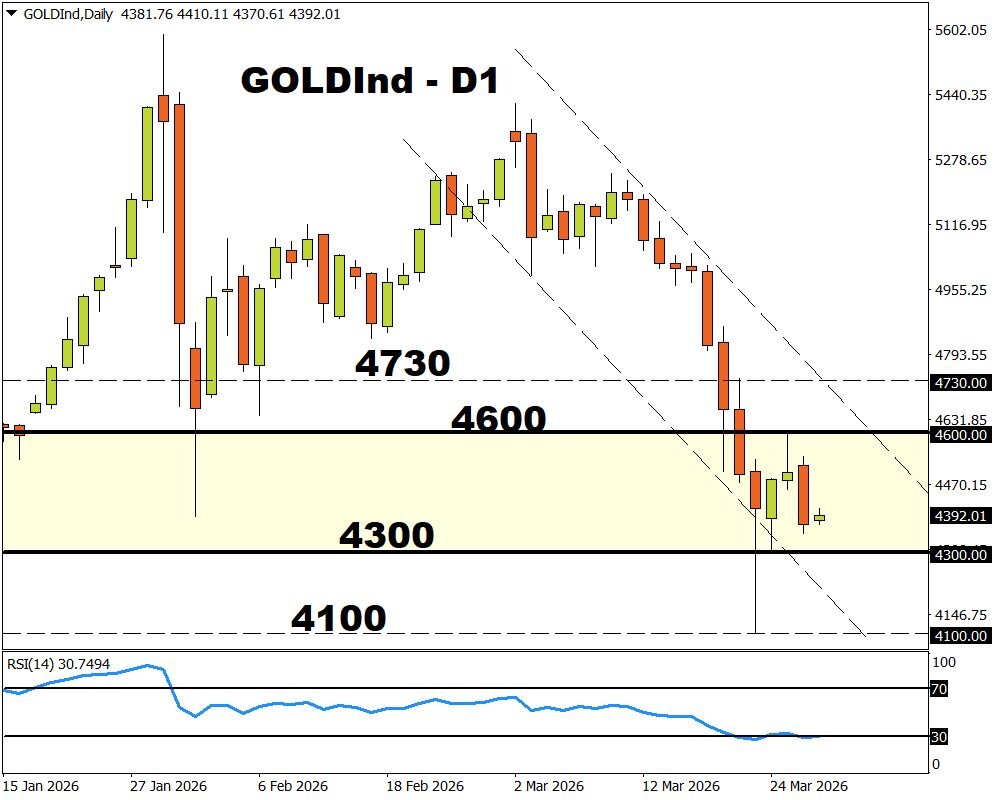

3) Technical forces

Prices remain in a bearish channel on the daily charts but have been consolidating over the past few days. Fundamentals point so further downside but technicals suggest that prices are heavily oversold.

- Should $4300 prove reliable support, prices may rebound back toward $4600 and higher.

- Weakness below $4300 could take prices toward $4100.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com