By Iordanis Kalaitzoglou, Audencia

In a bid to play catch up with technology companies and younger generations of consumers, central banks are finally starting to take digital currencies seriously. Countries such as Sweden, China, and India have establish pilot digital currencies – respectively, the e-krona, e-yuan and e-rupee – via their central banks. In the finance sector, these are known as central bank digital currencies (CBDCs).

The purpose, scale and status of such efforts vary considerably. In Sweden, the goal is to investigate the potential transition from banknotes to a digital currency, and the e-krona remains in the starting blocks. In China, the “digital renminbi” started to roll out in 2020, and its goal is to allow the state to better control the retail economy. India launched an e-rupee pilot in 2022 and its purpose is to facilitate a broad range of transactions. Meanwhile, the United States is exploring the potential repercussions of establishing its own digital currency.

Along the same lines, the European Union is currently toying with the idea of launching its own digital currency, the e-euro. As the European Central Bank (ECB) explains, it would provide a digital alternative to existing payment methods with the goal of increasing the security and stability of the EU’s monetary system. The e-euro would be held in digital wallets, with transactions facilitated by the use of blockchain.

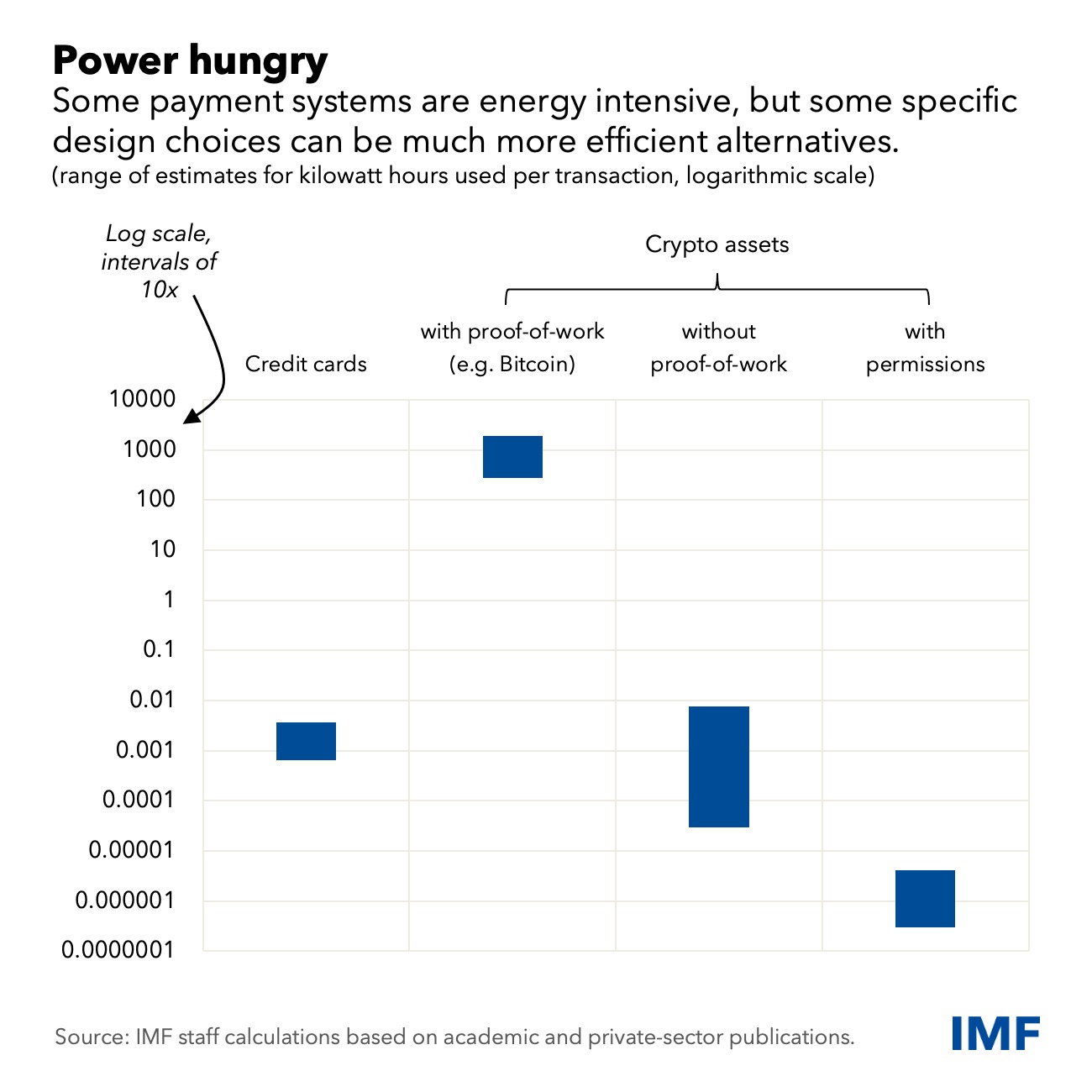

A crucial difference between the e-euro (a CBDC) and cryptocurrencies is that its overall quantity – the number in circulation – would not be capped. Because bitcoins and other cryptocurrencies aren’t issued by central banks, the number in circulation is limited by the fact that creating new ones requires “mining”, an energy-intensive process that involves solving extremely complicated math problems. Not the case with the e-euro, as it would be regulated by the European Central Bank and be linked directly to the euro itself – there will be no exchange rate, it would simply be the euro in another format.

While there is a superficial similarity between the e-euro and “stablecoins” – cryptocurrencies whose value is pegged to a major currency – the e-euro would be issued and controlled from a public entity. This will ensure stability in valuations and regulation.

Free Reports:

Christian Dubovan/Unsplash

The 1 million euro question is why is the ECB would consider a digital currency. While we all have a centuries-long familiarity with physical currencies, digital ones have some advantages:

Given the potential advantages of central bank digital currencies, what is holding countries back? Everything depends on how CBDCs are be designed and implemented, and some challenges that might overshadow any potential.

So is the e-euro something that we need or want? This depends on how it will be designed and regulated. For this particular venture, given the complexity of EU regulation, the devil is in the details.

About the Author:

Iordanis Kalaitzoglou, Ascociate Professor in Finance, Audencia

This article is republished from The Conversation under a Creative Commons license. Read the original article.

By ForexTime FXTM’s USDInd ↑ 2% MTD Dollar best performing G10 currency MTD Geopolitical risk…

By JustMarkets The US stock market concluded Thursday’s session in the red as the escalating…

By Analytical Department RoboForex EUR/USD is holding near 1.1620 on Friday, with the US dollar…

By JustMarkets The US stock market rose on Wednesday. By the end of the day,…

By Daniele D'Alvia, Queen Mary University of London When a conflict escalates, financial markets respond…

By Analytical Department RoboForex GBP/USD contracted to 1.3350 on Thursday, with the pound remaining under…

This website uses cookies.

{kind=link}