Last week’s ECB and FOMC minutes made investors across the globe realise that the end of an unprecedented era is now definitely over. Much will no doubt be written about the past decade and longer, when interest rates were cut and remained at levels previously seen decades and even centuries ago.

But now, markets are looking warily at major central banks, and certainly the world’s most powerful one, which is set to front-load interest rate hikes in order to tame the inflation genie that has been let out of the bottle to try and get rates quickly back to neutral.

The widely watched US 10-year Treasury yield has hit new cycle highs above 2.83% this morning. Interestingly, the move was still more or less equally driven by higher real yields and inflation expectations. The latter suggests that the market still sees room for the Fed to further step up the pace of tightening.

Red hot US inflation incoming

Today’s March US CPI release takes centre stage.

Free Reports:

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

The headline print is expected to accelerate to 1.2% m/m and 8.4% y/y. The core measure, which excludes the volatile food and energy sectors, is also set to rise to 0.5% m/m and 6.6% y/y. All these readings will be new multi-decade highs with the persistent high pace in the monthly price rises justifying the Fed’s red alert inflation mode.

This means a major correction in the current uptrend in yields is not expected any time soon. Even European bonds have cratered with yields breaking key levels recently ahead of the ECB meeting on Thursday. The major German government bond hit its highest yield since 2015 yesterday with the 10-year at 0.78%. This was still negative as of early March which shows the seismic recent moves in bond markets.

USD in pole position, stocks suffering

The sharp rise in rates, combined with ongoing geopolitical tensions and rising doubts on growth triggered more risk-off in equity markets.

The tech-heavy Nasdaq lost over 2% and futures are pointing to further losses today.

The US earnings season kicks off in earnest this week with several major US banks reporting. Analysts are forecasting overall revenues at the banks to fall around 10% with a 26% drop in investment banking fees.

Meanwhile, King Dollar is enjoying its safe haven status amid rising rates. The DXY has topped the 100 barrier earlier today, with the euro failing to maintain its gains after the first round of voting in the French presidential election.

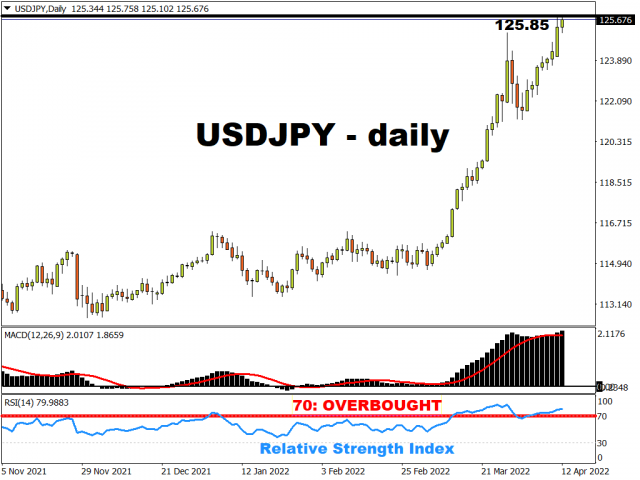

But the FX pair most affected by the long-end adjustment in bonds has been USD/JPY. Even rare jawboning from the Japanese authorities this morning has not stopped the enduring bids in this major.

Most seasoned traders don’t expect any proper intervention to start before 130, with the June 2015 peak at 125.85 the next resistance level to be toppled.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- COT Metals Charts: Weekly Speculator Bets led by Copper & Steel Jul 18, 2026

- COT Bonds Charts: Weekly Speculator Bets led by 2-Year, SOFR 3M & 5-Year Bonds Jul 18, 2026

- COT Energy Charts: Weekly Speculator Bets led by Brent Oil & Heating Oil Jul 18, 2026

- COT Soft Commodities Charts: Weekly Speculator Bets led by Wheat, Corn & Soybean Meal Jul 18, 2026

- The Bank of Canada kept its interest rate unchanged. Platinum prices reached a three‑week high Jul 16, 2026

- Stock indices rose after the release of US inflation data. China’s GDP slowed sharply Jul 15, 2026

- GBP/USD Awaits Political News: What Will Happen Next Jul 15, 2026

- USD/JPY Holds at Highs: Pressure Lingers on Yen Jul 14, 2026

- Oil prices jumped 4% amid a new wave of escalation between the US and Iran Jul 13, 2026

- EUR/USD: US Inflation Will Determine Everything Jul 13, 2026