Forget waiting on the upcoming OPEC meeting later this week or US jobs report on Friday.

If you want market action now, then check out the Japanese Yen.

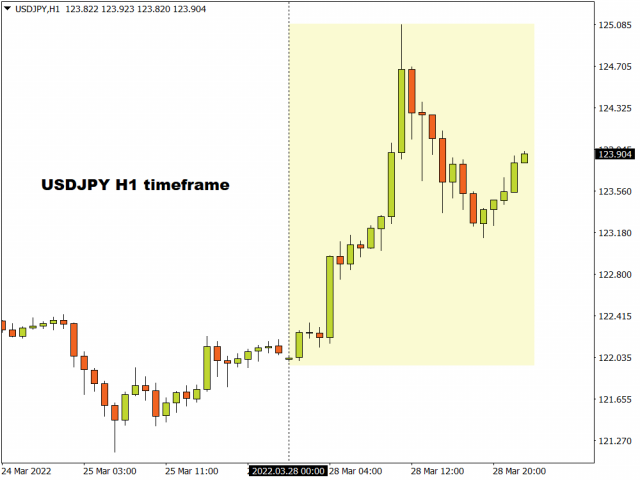

The currency was beaten black and blue on Monday, weakening to a seven-year low against the dollar.

It stood little chance against other G10 majors.

Free Reports:

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

In fact, since the start of March, the Yen has turned into a punching bag for its major counterparts.

There were a couple of factors behind the Yen’s painful selloff.

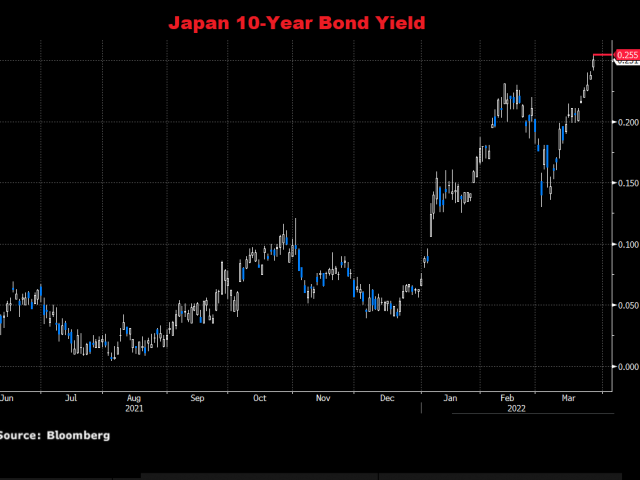

A key culprit was the Bank of Japan (BoJ) offering to buy an unlimited amount of 10-year Japanese Government Bonds (JGB) after yields rose to a fresh six-year high of 0.255%. Secondly, the widening monetary policy divergence between the BoJ and the Federal Reserve (Fed). While the Fed is willing to raise interest rates more aggressively in the face of soaring inflation, the BoJ continues to ease monetary policy aggressively.

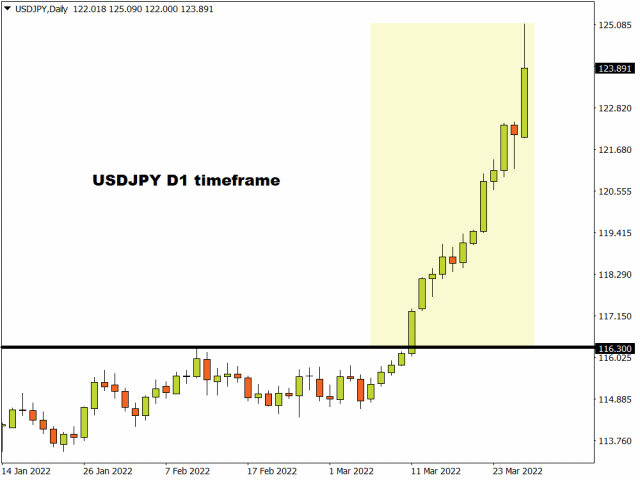

These fundamental forces have injected the USDJPY with vitality and direction. The currency pair remains heavily bullish on the daily charts with the path of least resistance north.

Why is the Yen getting no love?

One would think that the heightened levels of uncertainty, explosive volatility, and geopolitical risks would send investors rushing toward’s the Yen’s safe embrace. However, the numbers are saying a different story. Since the 24th of February 2022, when Russia began its invasion of Ukraine – the Yen has weakened against every single G10 currency.

This weakness could be based around:

- Divergence in monetary policy

Central banks across the world remain entangled in a fierce battle against soaring inflation. This month alone, the Fed raised rates for the first time since 2018, the Bank of England raised rates for the third consecutive meeting while the Bank of Canada raised interest rates. Even the ECB struck a hawkish tone.

The BoJ, in contrast has held tight to its dovish monetary policy.

- Yields differentials

As central banks across the world raise interest rates in the face of rising inflation, this has hammered bond markets – resulting in higher yields across the world.

-High inflation is bad for bonds.

-Bonds are inversely correlated to interest rates.

The 10-year Treasury yield punched above 2.5% on Monday with similar scenes witnessed across the world.

Even in Japan, the 10-year JGB yield crept up to a six-year high of 0.255% – prompting the BoJ to announce that it would buy unlimited amounts of 10-year JGB at a fixed rate of 0.25%. This move was to prevent yields from rising beyond the 0.25% policy target.

It is worth keeping in mind that the BoJ operates a policy of yield curve control.

The central bank will allow the 10-year treasury yield to move flexibly around its 0% target as long as it stays below the 0.25% upper limit – printing whatever money is needed to keep yields at that level. Given how bond prices are rising across the world amid higher interest rates, this has also impacted Japanese bonds. Ultimately, if you print cash to control yields this will hit the currency. This is what happened to the Yen.

But the key thing here is yield differentials. Japanese bonds yields are being capped at 0.25% by the BoJ, relative to other major market yields which have surged to multi-year highs. As the yield differentials widen, this could keep yen bears in the driving seat.

- An appreciating dollar

The dollar is likely to draw strength from rising Treasury yields, enforcing more pressure on the Japanese Yen. As highlighted earlier, the greenback has appreciated over 7% against the dollar since the start of 2022. With the mighty dollar still in a position of power and likely to appreciate as we explained here, this could push the USDJPY higher in the medium to longer term.

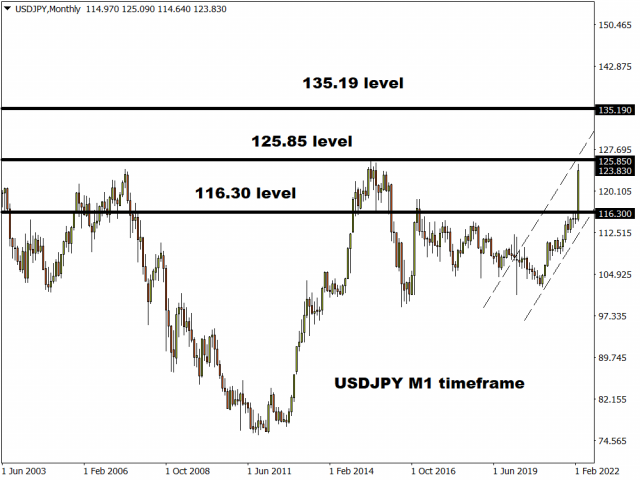

USDJPY eyes 2015 high

A weaker Yen propelled the USDJPY to a fresh 7 year high on Monday with prices trading around 123.72 as of writing. A solid daily close above 125.00 could open doors toward the June 2015 peak of 125.85. Beyond this level, prices could rally towards 129.00, a level not seen in almost 20 years.

If the upside momentum runs of out steam, the USDJPY could decline back towards 122.50 before experiencing a technical rebound or extending losses towards 121.00 and 119.40, respectively.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- COT Metals Charts: Weekly Speculator Bets led by Copper & Steel Jul 18, 2026

- COT Bonds Charts: Weekly Speculator Bets led by 2-Year, SOFR 3M & 5-Year Bonds Jul 18, 2026

- COT Energy Charts: Weekly Speculator Bets led by Brent Oil & Heating Oil Jul 18, 2026

- COT Soft Commodities Charts: Weekly Speculator Bets led by Wheat, Corn & Soybean Meal Jul 18, 2026

- The Bank of Canada kept its interest rate unchanged. Platinum prices reached a three‑week high Jul 16, 2026

- Stock indices rose after the release of US inflation data. China’s GDP slowed sharply Jul 15, 2026

- GBP/USD Awaits Political News: What Will Happen Next Jul 15, 2026

- USD/JPY Holds at Highs: Pressure Lingers on Yen Jul 14, 2026

- Oil prices jumped 4% amid a new wave of escalation between the US and Iran Jul 13, 2026

- EUR/USD: US Inflation Will Determine Everything Jul 13, 2026