By Jean-Philippe Serbera, Sheffield Hallam University

– Cryptocurrencies have had an exceptional year, reaching a combined value of more than US$3 trillion (£2.2 trillion) for the first time in November. The market seems to have benefited from the public having time on their hands during pandemic lockdowns. Also, large investment funds and banks have stepped in, not least with the recent launch of the first bitcoin-backed ETF – a listed fund that makes it easier for more investors to get exposure to this asset class.

Alongside this has been an explosive rise in the value of stablecoins like tether, USDC and Binance USD. Like other cryptocurrencies, stablecoins move around on the same online ledger technology known as blockchains. The difference is that their value is pegged 1:1 to a financial asset outside the world of crypto, usually the US dollar.

Stablecoins enable investors to keep money in their digital wallets that is less volatile than bitcoin, giving them one less reason to need a bank account. For a whole movement that is about a declaration of independence from banks and other centralised financial providers, stablecoins help to facilitate that. And since the rest of crypto tends to go up and down together, investors can protect themselves better in a falling market by moving money into stablecoins than, say, selling their ether for bitcoin.

A substantial proportion of buying and selling of crypto is done using stablecoins. They are particularly useful for trading on exchanges like Uniswap where there is no single company in control and no option to use fiat currencies. The total dollar value of stablecoins has shot up from the low US$20 billions a year ago to US$139 billion today. In one sense this is a sign that the cryptocurrency market is maturing, but it also has regulators worried about the risks that stablecoins could pose to the financial system. So what’s the problem and what can be done about it?

Initially introduced in the mid-2010s, stablecoins are centralised operations – in other words, someone is in control of them. Tether is ultimately controlled by the owners of the crypto exchange Bitfinex, which is based in the British Virgin Islands. USDC is owned by an American consortium consisting of payments provider Circle, bitcoin miner Bitmain and crypto exchange Coinbase. Binance USD is owned by Binance, another crypto exchange, which is headquartered in the Cayman Islands.

Free Reports:

There is a philosophical contradiction between the decentralised ideal of cryptocurrencies and the fact that such an important part of the market is centralised. But also, there are serious questions about whether these organisations hold enough financial reserves to be able to maintain the 1:1 fiat ratios of their stablecoins in the event of a crisis.

These 1:1 ratios are not automatic. They depend on stablecoin providers having reserves of financial assets equivalent to the value of their stablecoins in circulation, which adjust with supply and demand from investors. The providers promise they have reserves worth 100% of the value of their stablecoins, but that’s not quite accurate – as can be seen in the charts below.

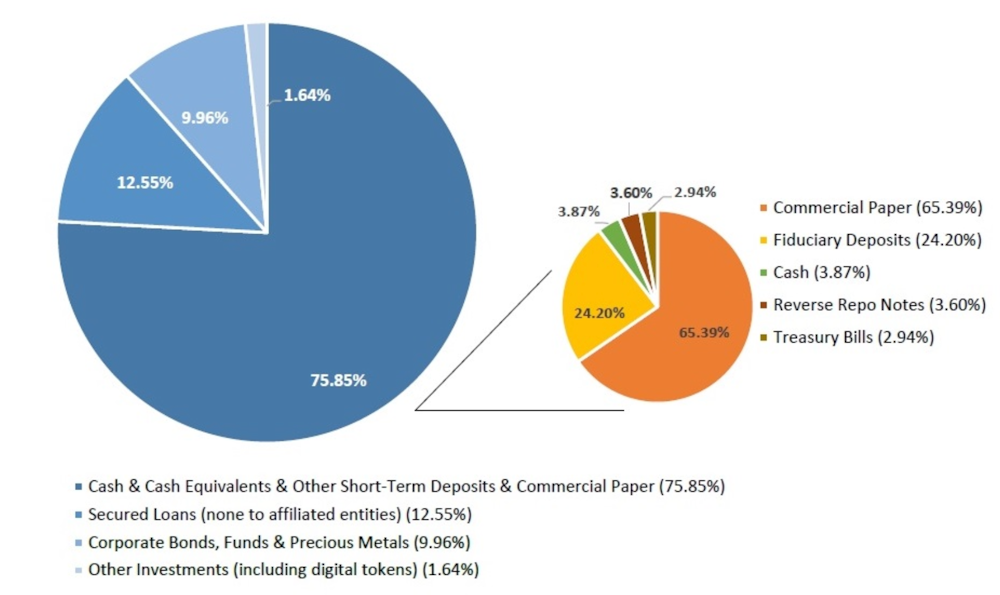

Tether reserves

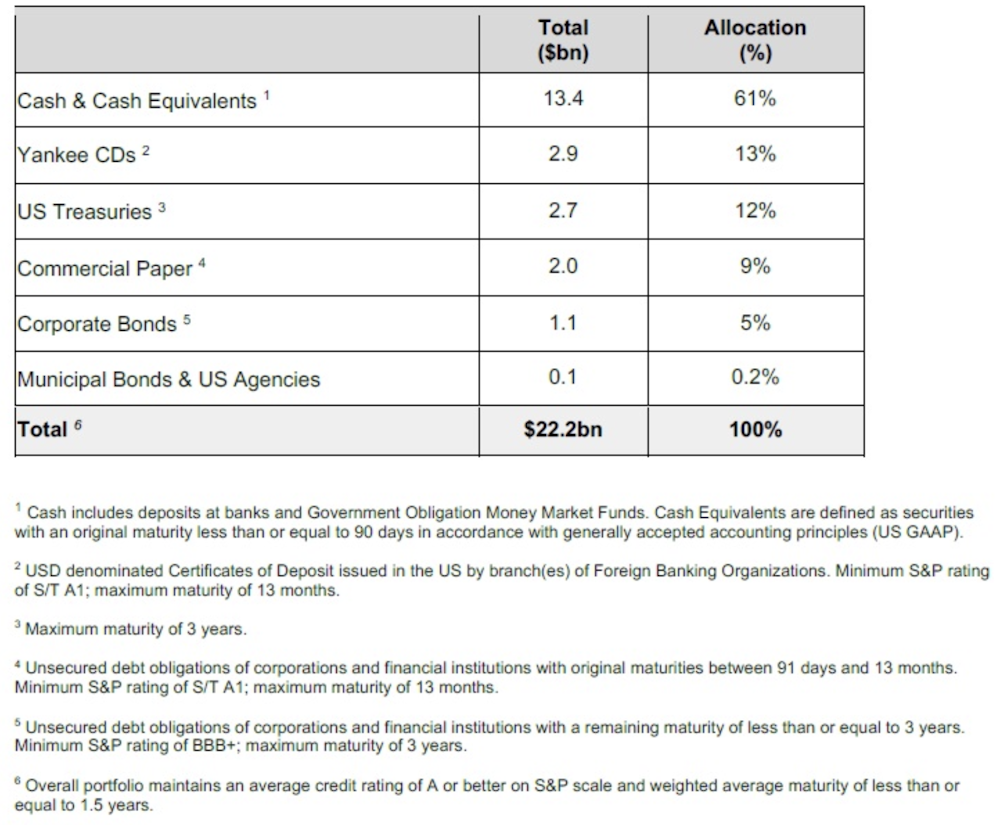

USDC reserves

Tether holds 75% of its reserves in cash and equivalents as of March 2021. USDC has 61% as at May 2021, so both are some way short of 100%. A large part of the assets of both operations are based on commercial paper, which is a form of short-term company debt. This is not cash equivalent and poses a solvency risk in the event of a sudden collapse in the value of these assets.

So what could derail the machine? Currently there is almost unlimited money in circulation, interest rates are still at record lows and with the US government having just voted to accept another economic stimulus package worth US$1.2 trillion, the supply of money is not likely to be reduced significantly any time soon. The only element that could challenge this abundance of money is inflation.

There are several possible inflation scenarios, but the market currently still considers the “goldilocks” scenario to be the most likely, with inflation and growth rising together at high but manageable levels. In this case, central banks can let inflation run at 3%-4% levels.

But if the economy overheats, it could lead to an explosive situation of high inflation and economic recession. Lots of money would be moved out of risky assets and bonds into safer havens like the US dollar. The value of those riskier assets, including commercial paper, would fall off a cliff.

This would seriously damage the value of the reserves of stablecoin providers. Many investors with their money in stablecoins might panic and try and convert their money into, say, US dollars, and the stablecoin providers might be unable to give everyone their money back at a 1:1 ratio. This could drag down the crypto market and potentially the financial system as a whole.

Regulators are certainly worried about the stability of stablecoins. A US report published a few days ago by the President’s Working Group on Financial Markets said that they potentially pose a systemic risk, not to mention the danger that a huge amount of economic power could end up concentrated in the hands of one provider.

In October, the US Commodity Futures Trading Commission fined Tether US$41 million for claiming to be 100%-backed by fiat currency between 2016 and 2019. Bank of England Governor Andrew Bailey said in June that the bank was still deciding how to regulate stablecoins but that they had some “difficult questions” to answer.

Overall, however, it seems that the response from the regulators is still tentative. The President’s Working Group report recommended stablecoin providers be forced to become banks, but delegated any decisions to Congress. With several big providers and such a burgeoning international market, my worry is that stablecoins may already effectively be too big and disparate to control.

It is possible that the risks will reduce as more stablecoins arrive on the market. Facebook/Meta has well publicised plans for a stablecoin called diem, for instance. Meanwhile, central bank digital currencies (CBDCs) will put fiat currencies on the blockchain if and when they arrive. The Bank of England is to consult on a digital pound, for example, while the EU and especially China are also moving ahead here. Perhaps the systemic risks of stablecoins will be reduced in a more diversified market.

For now, we wait and see. The speed at which this unnerving risk has emerged is certainly a concern. Unless governments and central banks move up a gear on regulation, a 2008-style crisis in digital assets cannot be ruled out.

About the Author:

Jean-Philippe Serbera, Senior Lecturer, Sheffield Hallam University

This article is republished from The Conversation under a Creative Commons license. Read the original article.

By ForexTime FXTM’s USDInd ↑ 2% MTD Dollar best performing G10 currency MTD Geopolitical risk…

By JustMarkets The US stock market concluded Thursday’s session in the red as the escalating…

By Analytical Department RoboForex EUR/USD is holding near 1.1620 on Friday, with the US dollar…

By JustMarkets The US stock market rose on Wednesday. By the end of the day,…

By Daniele D'Alvia, Queen Mary University of London When a conflict escalates, financial markets respond…

By Analytical Department RoboForex GBP/USD contracted to 1.3350 on Thursday, with the pound remaining under…

This website uses cookies.

{kind=link}

{kind=link}