It was an intense week defined by speeches from numerous central bankers’, including testimonies from both Federal Reserve Chair Jerome Powell and Treasury secretary Janet Yellen.

Monday kicked off on a cautious note as Evergrande’s silence over a missed interest rate payment left investors on edge. Fears over further waves of coronavirus outbreaks in Asia compounded to the negative mood, leaving little room for equity bulls to stomp their feet. In the currency markets, the Euro weakened against most majors after European Central Bank (ECB) President Christine Lagarde struck a dovish tone during her speech.

Our trade of the week was none other than Brent crude which jumped to a new year-to-date high. Oil bulls drew ample strength from the global energy crunch while disruptions to crude production from Hurricane Ida last month complemented upside gains.

Free Reports:

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

On Tuesday, it was all about the movements in the bond markets. 10-year treasury yields hit their highest level since June, sparked by fears over rising inflation while the shorter end five-year yield touched levels not seen since February 2020.

Stock markets were beaten black and blue on Tuesday, with equities suffering their biggest fall since May thanks to a spike in US Treasury yields. The S&P500 collapsed like a house of cards, breaking below its 50-day simple moving average for the second time in September.

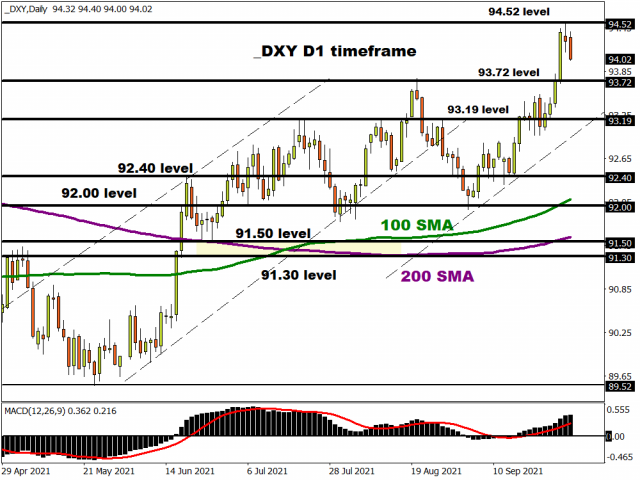

In the currency markets, the mighty dollar pushed higher – helped by rising yields with the Dollar Index (DXY) striking a fresh year-to-date high beyond 93.72. As the week progressesd, prices jumped as high as 94.52 before later pulling back.

Fed Chairman Jerome Powell and Treasury Secretary Janet Yellen testified before the Senate on Tuesday evening. On the data front, US consumer confidence unexpectedly fell to a seven-month low as the surge in coronavirus cases intensified fears about the economy’s near-term outlook.

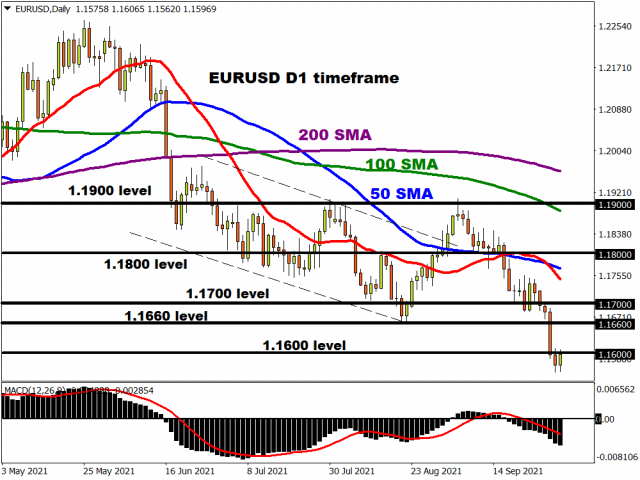

Mid-week, our technical outlook focused on the movers & shakers with the dollar, pound, natural gas among many other assets under the spotlight. Interestingly, we were heavily bearish on the EURUSD with 1.16 acting as the first level of interest for bears. After dipping as low as 1.1562, the currency pair is lingering around 1.16 as of writing.

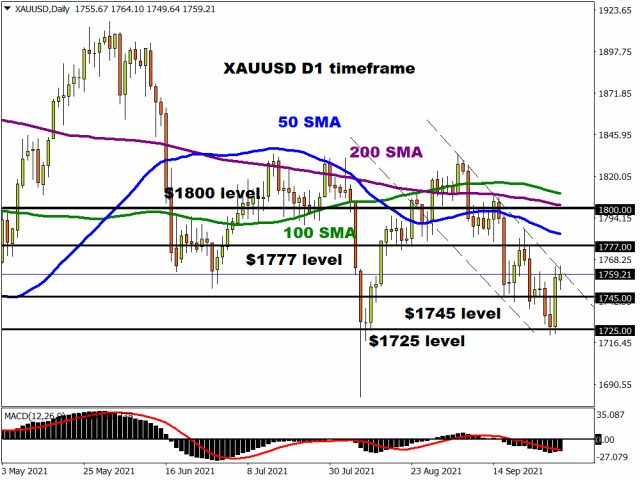

A sense of calm returned to financial markets on Thursday following the heavy selloff witnessed earlier in the week. One of the biggest takeaways from rout in the bond and equity space was how sensitive markets remained to rate hike expectations and inflation. In the currency space, the dollar index hit a fresh one-year while gold fought back after falling victim to rising treasury yields, taper expectations and prospects of higher interest rates.

On the political front, President Joe Biden signed a stopgap bill passed earlier by Congress to avert a government shutdown. Despite this encouraging development, the mood across markets was negative on Friday amid fears of high inflation, slowing global growth and rising interest rates. Although European stocks tumbled to a two-month low, stocks were mostly higher on Wallstreet.

In other news, the PCE index climbed 4.3% year-over-year in August, its highest level since 1991. The core PCE which is the Fed’s favoured measure of inflation remained unchanged at 3.6%. The strong figures may reinforce expectations over the Federal Reserve winding down its emergency economic stimulus.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- COT Metals Charts: Weekly Speculator Bets led by Copper & Steel Jul 18, 2026

- COT Bonds Charts: Weekly Speculator Bets led by 2-Year, SOFR 3M & 5-Year Bonds Jul 18, 2026

- COT Energy Charts: Weekly Speculator Bets led by Brent Oil & Heating Oil Jul 18, 2026

- COT Soft Commodities Charts: Weekly Speculator Bets led by Wheat, Corn & Soybean Meal Jul 18, 2026

- The Bank of Canada kept its interest rate unchanged. Platinum prices reached a three‑week high Jul 16, 2026

- Stock indices rose after the release of US inflation data. China’s GDP slowed sharply Jul 15, 2026

- GBP/USD Awaits Political News: What Will Happen Next Jul 15, 2026

- USD/JPY Holds at Highs: Pressure Lingers on Yen Jul 14, 2026

- Oil prices jumped 4% amid a new wave of escalation between the US and Iran Jul 13, 2026

- EUR/USD: US Inflation Will Determine Everything Jul 13, 2026