by JustForex

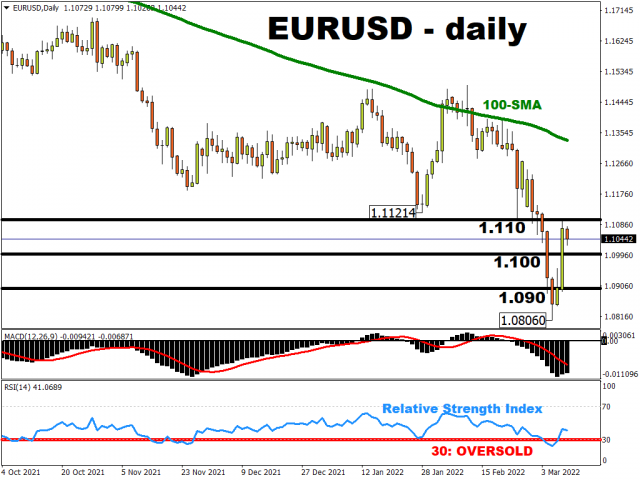

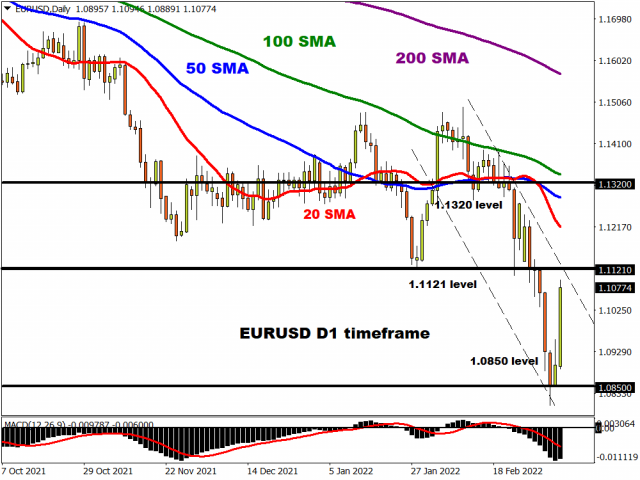

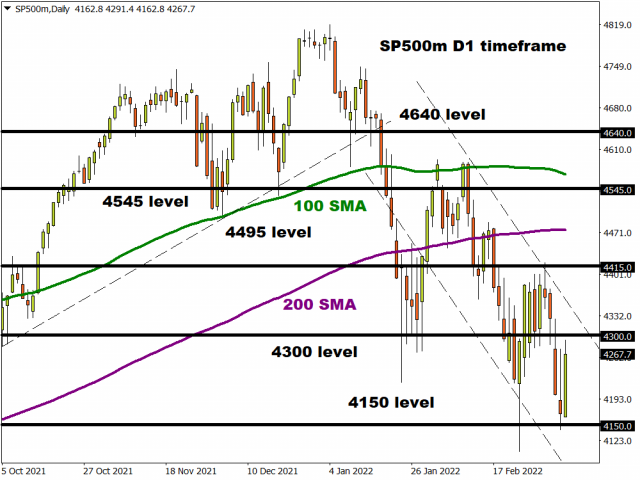

The EUR/USD currency pair

- Prev Open: 1.0896

- Prev Close: 1.1075

- % chg. over the last day: +1.64%

Yesterday, the European currency showed the sharpest daily jump in almost six years after it became known that the foreign ministers of Ukraine and Russia will hold negotiations in Turkey today. The ECB will hold a meeting on monetary policy and an interest rate decision. Analysts believe that amid the war in Ukraine, the ECB will not change anything in monetary policy.

- Support levels: 1.0993, 1.0930, 1.0823

- Resistance levels: 1.1065, 1.1144, 1.1291

From the technical point of view, the EUR/USD currency pair trend on the hourly time frame is bearish, but there are signs that the price may change a priority. The MACD indicator has become positive. The price has adopted the structure of sideways movement with a wide range. In such market conditions, it is better to look for sell trades on the intraday time frames from the resistance level of 1.1065. Buy trades can be looked at from the support of 1.0993 or 1.0930, but only with short targets since there is no fundamental reason for the Euro to strengthen right now.

Alternative scenario: if the price breaks out through the 1.1065 resistance level and fixes above, the mid-term uptrend will likely resume.

- – Eurozone ECB Monetary Policy Statement at 14:45 (GMT+2);

- – Eurozone ECB Interest Rate Decision at 14:45 (GMT+2);

- – Eurozone ECB Press Conference at 15:30 (GMT+2);

- – US Consumer Price Index (m/m) at 15:30 (GMT+2);

- – US Initial Jobless Claims (w/w) at 15:30 (GMT+2).

The GBP/USD currency pair

- Prev Open: 1.3099

- Prev Close: 1.3186

- % chg. over the last day: +0.66%

There are no major economic events related to the UK this week, so the British pound has remained stable in recent days. Today, the US publishes data on consumer inflation, which could significantly shake the dollar, as analysts expect another acceleration of inflation in the United States. If the actual value is worse than expected, the dollar index could strengthen sharply, and the next week’s Fed meeting is likely to decide on a more aggressive increase in interest rates. A rise in the dollar index will cause the GBP/USD to fall. If the real inflation value turns out to be better than expected, the opposite may happen – a decrease in the dollar index and an increase of GBP/USD.

- Support levels: 1.3127, 1.3091

- Resistance levels: 1.3274, 1.3315, 1.3418

On the hourly time frame, the trend on the GBP/USD currency pair is bearish. Volatility is high, sellers’ pressure has stopped, the price started trading in a sideways range. The MACD indicator has become positive. Under such market conditions, buy trades should be considered from the support level of 1.3127, but better with confirmation. For sell deals, there are no optimal entry points now.

Alternative scenario: if the price breaks out through the 1.3275 resistance level and fixes above, the mid-term uptrend will likely resume.

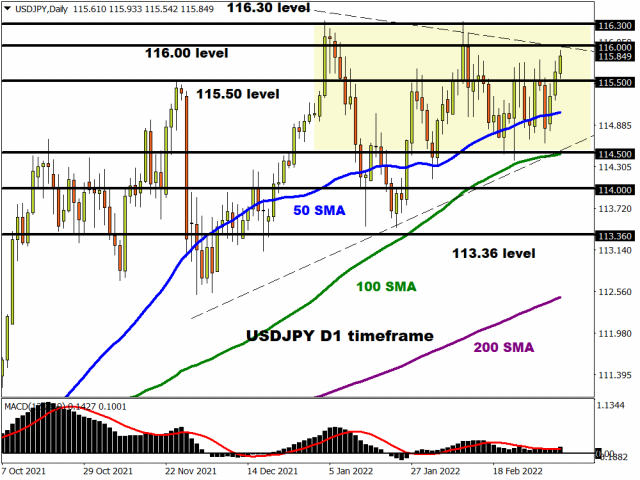

The USD/JPY currency pair

- Prev Open: 115.67

- Prev Close: 115.86

- % chg. over the last day: +0.16%

The monetary policy of the central bank of Japan is now aimed at making the Japanese yen cheaper (USD/JPY growth), and the US Federal Reserve will begin to tighten monetary policy this month. Therefore, investors often transfer their funds to the yen in case of any panic moods in the market.

- Support levels: 115.89, 115.41, 115.13, 114.71, 114.41

- Resistance levels: 116.32

The medium-term trend on the USD/JPY currency pair is bullish. The MACD indicator is in the positive zone, but there are signs of divergence. Under such market conditions, it is best to look for buy deals on the lower time frames from the support level of 115.89, but with additional confirmation. Sell deals may be considered from the resistance level of 116.32, but it is better to wait for the reaction of sellers.

Alternative scenario: if the price fixes below 115.41, the uptrend will likely be broken.

- – Japan Producer Price Index (m/m) at 01:50 (GMT+2).

The USD/CAD currency pair

- Prev Open: 1.2885

- Prev Close: 1.2805

- % chg. over the last day: -0.62%

The Canadian dollar is a commodity currency, so it is highly dependent not only on the monetary policy of the Bank of Canada but also on the dynamics of oil prices and the dollar index. The dollar index fell yesterday, while oil showed its biggest drop in almost two years after the United Arab Emirates, a member of the Organization of Petroleum Exporting Countries and their allies (OPEC+), said it would support increased production. This situation led to a sharp decline in USD/CAD quotes.

- Support levels: 1.2790, 1.2653, 1.2555, 1.2517

- Resistance levels: 1.2871, 1.2890

From a technical point of view, the USD/CAD currency pair trend is bullish. The price trades between the moving averages, indicating a more flat structure within a bullish trend. It is worth trading only with short targets, as both oil and the dollar index are still fundamentally inclined to rise. Under such market conditions, it is better to look for buy trades on lower time frames from the support level of 1.2790, but it is better with additional confirmation. For sell deals, it is better to consider the resistance level of 1.2871.

Alternative scenario: if the price breaks through and consolidates below 1.2726, the downtrend will likely resume.

by JustForex

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

{kind=link}