The US stocks concluded the first session of the year with gains following volatile trading. At the close of Friday, the Dow Jones (US30) rose by 0.66% (-0.68% for the week). The S&P 500 (US500) gained 0.19% (-1.12% for the week). The technology-heavy Nasdaq (US100) closed lower by 0.17% (-1.89% for the week). The market was supported by a sharp rise in chipmakers following positive corporate news: Nvidia shares rose 2%, Micron gained 10%, and Intel added 7%. Additional drivers included news of the planned IPO of Baidu’s chip division in Hong Kong and rating upgrades for ASML by several asset managers. At the same time, shares of major AI software developers came under pressure: Microsoft, Meta, Amazon, and Palantir declined by 2–5%, reflecting concerns over the return on investment in AI. Tesla lost 2.5% after failing to meet its delivery targets for the fourth quarter.

Equity markets in Europe mostly rose on Friday. The German DAX (DE40) rose by 0.20% (+1.02% for the week), the French CAC 40 (FR40) closed with an increase of 0.56% (+1.06% for the week), the Spanish IBEX 35 (ES35) gained 1.07% (+2.02% for the week), and the British FTSE 100 (UK100) closed up 0.20% (+0.63% for the week).

On Monday, silver appreciated by nearly 4%, rising to around $76 per ounce and continuing the growth of the previous session. The increase in quotes followed the US strikes on Venezuela and the arrest of President Nicolas Maduro over the weekend, which sharply heightened geopolitical risks and triggered a surge in demand for safe-haven assets. President Donald Trump stated on Saturday that the US would “manage” Venezuela until a proper political transition occurs. WTI crude oil prices dropped below $57 per barrel as investors assessed the consequences of the US strike on Venezuela and the capture of President Nicolas Maduro. Market attention is centered on the potential impact of these events on regional oil supplies, given that Venezuela possesses the world’s largest proven hydrocarbon reserves. At the same time, a number of analysts believe that short-term disruptions will be limited, as Venezuela’s current production is less than 1 million barrels per day – less than 1% of global production.

The US natural gas prices declined by more than 3%, falling to around $3.48 per MMBtu and hitting new lows since late October. Pressure on quotes was exerted by weather prognoses indicating abnormally warm weather in the coming weeks.

Asian markets traded mixed last week. The Japanese Nikkei 225 (JP225) fell by 0.27%, the Chinese FTSE China A50 (CHA50) dropped 0.94%, the Hong Kong Hang Seng (HK50) gained 2.17%, and the Australian ASX 200 (AU200) showed a negative result of 0.64% over the 5-day period. The New Zealand dollar weakened to the $0.576 area, remaining near a two-week low amid a reassessment of the Reserve Bank of New Zealand’s (RBNZ) monetary policy outlook. The regulator signaled that the easing cycle, in which rates were cut by a total of 225 bps, has likely concluded, while simultaneously cooling expectations for an imminent policy tightening. Comments from RBNZ Governor Anne Breman reinforced this signal, indicating that in the absence of unexpected economic shocks, rates could remain unchanged for an extended period.

On Monday, the Australian dollar fell below the $0.668 level, continuing the decline that began last week amid deteriorating global sentiment due to renewed geopolitical tensions. The currency, sensitive to commodity market dynamics and widely used as an indicator of global risk appetite, came under pressure following the US capture of Venezuelan President Nicolas Maduro.

The offshore yuan weakened slightly below the 6.98 mark per dollar but remained near its highest levels since May 2023 as investors analyzed fresh PMI data for signals on the state of China’s economy. A private survey showed that the composite PMI remained in the growth zone for the seventh consecutive month, although the expansion rate in the services sector slowed to a six-month low. Meanwhile, official statistics published earlier indicated an improvement in the overall picture: the composite PMI rose to a six-month high, manufacturing activity unexpectedly returned to growth, and the services index reached a four-month peak.

S&P 500 (US500) 6,858.47 +12.97 (+0.19%)

Dow Jones (US30) 48,382.39 +319.10 (+0.66%)

DAX (DE40) 24,539.34 +48.93 (+0.20%)

FTSE 100 (UK100 9,951.14 +19.76 (+0.20%)

USD Index 98.43 +0.11% (+0.11%)

News feed for: 2026.01.05

Japan Manufacturing PMI (m/m) at 02:30 (GMT+2); – JPY (MED)

China RatingDog Services PMI (m/m) at 03:45 (GMT+2); – CHA50, HK50 (MED)

Switzerland Retail Sales (m/m) at 08:30 (GMT+2); – CHF (MED)

US ISM Manufacturing PMI (m/m) at 17:00 (GMT+2). – USD (MED)

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

As the weather grows cold this winter, you may be one of the many Americans pulling their winter jackets out of the closet. Not only can this extra layer keep you warm on a chilly day, but modern winter jackets are also a testament to centuries-old physics and cutting-edge materials science.

Winter jackets keep you warm by managing heat through the three classical modes of heat transfer – conduction, convection and radiation – all while remaining breathable so sweat can escape.

In a fireplace, heat transfer occurs by all three methods: conduction, convection and radiation. Radiation is responsible for most of the heat transferred into the room. Heat transfer also occurs through conduction into the room’s floor, but at a much slower rate. Heat transfer by convection also occurs through cold air entering the room around windows and hot air leaving the room by rising up the chimney. Douglas College Physics 1207, CC BY

The physics has been around for centuries, yet modern material innovations represent a leap forward that let those principles shine.

Old science with a new glow

Physicists like us who study heat transfer sometimes see thermal science as “settled.” Isaac Newton first described convective cooling, the heat loss driven by fluid motion that sweeps thermal energy away from a surface, in the early 18th century. Joseph Fourier’s 1822 analytical theory of heat then put conduction – the transfer of thermal energy through direct physical contact – on mathematical footing.

Late-19th-century work by Josef Stefan and Ludwig Boltzmann, followed by the work of Max Planck at the dawn of the 20th century, made thermal radiation – the transfer of heat through electromagnetic waves – a pillar of modern physics.

All these principles inform modern materials design. Yet what feels new today are not the equations but the textiles. Over the last two decades, engineers have developed extremely thin synthetic fibers that trap heat more efficiently and treatments that make natural down repel water instead of soaking it up. They’ve designed breathable membranes full of tiny pores that let sweat escape, thin reflective layers that bounce your body heat back toward you, coatings that store and release heat as the temperature changes, and ultralight materials.

Together, these innovations give designers far more control over warmth, breathability and comfort than ever before. That’s why jackets now feel warmer, lighter and drier than anything Newton or Fourier could have imagined.

Trap still air, slow the leak

Conduction is the direct flow of heat from your warm body into your colder surroundings. In winter, all that heat escaping your body makes you feel cold. Insulation fights conduction by trapping air in a web of tiny pockets, slowing the heat’s escape. It keeps the air still and lengthens the path heat must take to get out.

High-loft down makes up the expansive, fluffy clusters of feathers that create the volume inside a puffer jacket. Combined with modern synthetic fibers, the down immobilizes warm air and slows its escape. New types of fabrics infused with highly porous, ultralight materials called aerogels pack even more insulation into surprisingly slim layers.

Tame the wind, protect the boundary layer

A good winter jacket also needs to withstand wind, which can strip away the thin boundary layer of warm air that naturally forms around you. A jacket with a good outer shell blocks the wind’s pumping action with tightly woven fabric that keeps heat in. Some jackets also have an outer layer of lamination that keeps water and cold air out, and a woven pattern that seals any paths heat might leak through around the cuffs, hems, flaps and collars.

The outer membrane layer on many jacket shells is both waterproof and breathable. It stops rain and snow from getting in, and it also lets your sweat escape as water vapor. This feature is key because insulation, such as down, stops working if it gets wet. It loses its fluff and can’t trap air, meaning you cool quickly.

How modern jackets manage heat: Left, a typical insulated shell; right, layers that trap air, block wind, and reflect infrared heat without adding bulk. Wan Xiong and Longji Cui

These shells also block wind, which protects the bubble of warm air your body creates. By stopping wind and water, the shell creates a calm, dry space for the insulation to do its job and keep you warm.

New tricks to reflect infrared heat

Even in still air, your body sheds heat by emitting invisible waves of heat energy. Modern jackets address this by using new types of cloth and technology that make the jacket’s inner surface reflect your body’s heat back toward you. This type of surface has a subtle space blanket effect that adds noticeable warmth without adding any bulk.

However, how jacket manufacturers apply that reflective material matters. Coating the entire material in metallic film would reflect lots of heat, but it wouldn’t allow sweat to escape, and you might overheat.

Some liners use a micro-dot pattern: The reflective dots bounce heat back while the gaps between them keep the material breathable and allow sweat to escape.

Another approach moves this technology to the outside of the garment. Some designs add a pattern of reflective material to the outer shell to keep heat from radiating out into the cold air.

When those exterior dots are a dark color, they can also absorb a touch of warmth from the sun. This effect is similar to window coatings that keep heat inside while taking advantage of sunlight to add more heat.

Warmth only matters if you stay dry. Sweat that can’t escape wets a jacket’s layer of insulation and accelerates heat loss. That’s why the best winter systems combine moisture-wicking inner fabrics with venting options and membranes whose pores let water vapor escape while keeping liquid water out.

What’s coming

Describing where heat travels throughout textiles remains challenging because, unlike light or electricity, heat diffuses through nearly everything. But new types of unique materials and surfaces with ultra-fine patterns are allowing scientists to better control how heat travels throughout textiles.

Managing warmth in clothing is part of a broader heat-management challenge in engineering that spans microchips, data centers, spacecraft and life-support systems. There’s still no universal winter jacket for all conditions; most garments are passive, meaning they don’t adapt to their environment. We dress for the day we think we’ll face.

But some engineering researchers are working on environmentally adaptive textiles. Imagine fabrics that open microscopic vents as the humidity rises, then close them again in dry, bitter air. Picture linings that reflect more heat under blazing sun and less in the dark. Or loft that puffs up when you’re outside in the cold and relaxes when you step indoors. It’s like a science fiction costume made practical: Clothing that senses, decides and subtly reconfigures itself without you ever touching a zipper.

Today’s jackets don’t need a new law of thermodynamics to work – they couple basic physics with the use of precisely engineered materials and thermal fabrics specifically made to keep heat locked in. That marriage is why today’s winter wear feels like a leap forward.

In artificial intelligence, 2025 marked a decisive shift. Systems once confined to research labs and prototypes began to appear as everyday tools. At the center of this transition was the rise of AI agents – AI systems that can use other software tools and act on their own.

While researchers have studied AI for more than 60 years, and the term “agent” has long been part of the field’s vocabulary, 2025 was the year the concept became concrete for developers and consumers alike.

AI agents moved from theory to infrastructure, reshaping how people interact with large language models, the systems that power chatbots like ChatGPT.

In 2025, the definition of AI agent shifted from the academic framing of systems that perceive, reason and act to AI company Anthropic’s description of large language models that are capable of using software tools and taking autonomous action. While large language models have long excelled at text-based responses, the recent change is their expanding capacity to act, using tools, calling APIs, coordinating with other systems and completing tasks independently.

This shift did not happen overnight. A key inflection point came in late 2024, when Anthropic released the Model Context Protocol. The protocol allowed developers to connect large language models to external tools in a standardized way, effectively giving models the ability to act beyond generating text. With that, the stage was set for 2025 to become the year of AI agents.

AI agents are a whole new ballgame compared with generative AI.

The milestones that defined 2025

The momentum accelerated quickly. In January, the release of Chinese model DeepSeek-R1 as an open-weight model disrupted assumptions about who could build high-performing large language models, briefly rattling markets and intensifying global competition. An open-weight model is an AI model whose training, reflected in values called weights, is publicly available. Throughout 2025, major U.S. labs such as OpenAI, Anthropic, Google and xAI released larger, high-performance models, while Chinese tech companies including Alibaba, Tencent, and DeepSeek expanded the open-model ecosystem to the point where the Chinese models have been downloaded more than American models.

Another turning point came in April, when Google introduced its Agent2Agent protocol. While Anthropic’s Model Context Protocol focused on how agents use tools, Agent2Agent addressed how agents communicate with each other. Crucially, the two protocols were designed to work together. Later in the year, both Anthropic and Google donated their protocols to the open-source software nonprofit Linux Foundation, cementing them as open standards rather than proprietary experiments.

At the same time, workflow builders like n8n and Google’s Antigravity lowered the technical barrier for creating custom agent systems beyond what has already happened with coding agents like Cursor and GitHub Copilot.

New power, new risks

As agents became more capable, their risks became harder to ignore. In November, Anthropic disclosed how its Claude Code agent had been misused to automate parts of a cyberattack. The incident illustrated a broader concern: By automating repetitive, technical work, AI agents can also lower the barrier for malicious activity.

This tension defined much of 2025. AI agents expanded what individuals and organizations could do, but they also amplified existing vulnerabilities. Systems that were once isolated text generators became interconnected, tool-using actors operating with little human oversight.

The business community is gearing up for multiagent systems.

What to watch for in 2026

Looking ahead, several open questions are likely to shape the next phase of AI agents.

One is benchmarks. Traditional benchmarks, which are like a structured exam with a series of questions and standardized scoring, work well for single models, but agents are composite systems made up of models, tools, memory and decision logic. Researchers increasingly want to evaluate not just outcomes, but processes. This would be like asking students to show their work, not just provide an answer.

Progress here will be critical for improving reliability and trust, and ensuring that an AI agent will perform the task at hand. One method is establishing clear definitions around AI agents and AI workflows. Organizations will need to map out exactly where AI will integrate into workflows or introduce new ones.

Another development to watch is governance. In late 2025, the Linux Foundation announced the creation of the Agentic AI Foundation, signaling an effort to establish shared standards and best practices. If successful, it could play a role like the World Wide Web Consortium in shaping an open, interoperable agent ecosystem.

There is also a growing debate over model size. While large, general-purpose models dominate headlines, smaller and more specialized models are often better suited to specific tasks. As agents become configurable consumer and business tools, whether through browsers or workflow management software, the power to choose the right model increasingly shifts to users rather than labs or corporations.

The challenges ahead

Despite the optimism, significant socio-technical challenges remain. Expanding data center infrastructure strains energy grids and affects local communities. In workplaces, agents raise concerns about automation, job displacement and surveillance.

From a security perspective, connecting models to tools and stacking agents together multiplies risks that are already unresolved in standalone large language models. Specifically, AI practitioners are addressing the dangers of indirect prompt injections, where prompts are hidden in open web spaces that are readable by AI agents and result in harmful or unintended actions.

Regulation is another unresolved issue. Compared with Europe and China, the United States has relatively limited oversight of algorithmic systems. As AI agents become embedded across digital life, questions about access, accountability and limits remain largely unanswered.

Meeting these challenges will require more than technical breakthroughs. It demands rigorous engineering practices, careful design and clear documentation of how systems work and fail. Only by treating AI agents as socio-technical systems rather than mere software components, I believe, can we build an AI ecosystem that is both innovative and safe.

Still, other households are stretched, even as gas prices fall. This contributes to a continuing “vibecession,” a term popularized by Kyla Scanlon to describe the disconnect between strong aggregate economic data and weaker lived experiences amid economic growth. As lower-income households feel the pinch of tariffs, wealthier households continue to drive consumer spending.

For the Fed, that’s the puzzle: solid top-line numbers, growing pockets of stress and noisier data – all at once. With this unevenness and weakness in some sectors, the next big question is what could tip the balance toward a slowdown or another year of growth. And increasingly, all eyes are on AI.

Comparisons are always imperfect, so we won’t linger on the differences between this time and two decades ago when the dot-com bubble burst. Let’s instead focus on what we know about bubbles.

Economists often categorize bubbles into two types. Inflection bubbles are driven by genuine technological breakthroughs and ultimately transform the economy, even if they involve excess along the way. Think the internet or transcontinental railroad. Mean-reversion bubbles, by contrast, are fads that inflate and collapse without transforming the underlying industry. Some examples include the subprime mortgage crisis of 2008 and The South Sea Company collapse of 1720.

In some cases, housing costs have doubled as a share of income over the past decade, forcing households to delay purchases, take more risk or even give up on hopes of homeownership entirely. That pressure matters not only for housing itself, but for sentiment and consumption more broadly.

Looking beyond the housing market, inflation has fallen considerably since 2021, but certain types of services, such as insurance, remain sticky. Immigration policy also plays an important role here, and changes to labor supply could influence wage pressures and inflation dynamics going forward.

Encouragingly, greater clarity on taxes, tariffs, regulation and monetary policy may arrive in the coming year. When it does, it could help unlock delayed business investment across multiple sectors, an outcome the Federal Reserve itself appears to be anticipating.

If there is one lesson worth emphasizing, it’s this: Uncertainty is always greater than anyone expects. As the oft-quoted baseball sage Yogi Berra memorably put it, “It’s tough to make predictions, especially about the future.”

Everyone – politicians and the public – is talking about energy costs. In particular, they’re talking about data centers that drive artificial intelligence systems and their increasing energy demand, electricity costs and strain on the nation’s already overloaded energy grid.

As a former state energy official and utility executive, I know that many of the underlying questions involving energy affordability are very complex and have been festering for decades, in part because of how many groups are involved. Energy projects are expensive and take a long time to build. Where to build them is often also a difficult, even controversial, question. Consumers, regulators, utilities and developers all value energy reliability but have different interests, cost sensitivities and time frames in mind.

By 2030, energy analysts expect U.S. electricity demand to rise about 25%, and McKinsey estimates that data centers’ energy use could nearly triple from current levels by that year, using as much as 11.7% of all electricity in the U.S. – more than double their current share.

The nation’s current electricity grid is not ready to supply all that energy. And even if the electricity could be generated, transmission lines are aging and not up to carrying all that power. Their capacity would need to be expanded by about 60% by 2050.

That multiyear effort is just one example of how the vast web of companies that generate power, transmit it from power plants to communities, and distribute it to homes and businesses complicates attempts to make changes to the power grid.

State and federal government agencies have roles in these processes. States’ public utilities commissions oversee the utility companies that distribute power to customers. The Federal Energy Regulatory Commission oversees connections of power generators to the grid and the transmission lines that move electricity across state lines.

Often, those efforts aren’t aligned with each other, leading to delays over jurisdiction and decision-making.

For instance, as new generators prepare to operate, whether they are solar farms or gas-fired power plants, they need permission from FERC to connect to the transmission grid. The commission typically requests technical engineering studies to determine how the project would affect the existing system. Delays in this process increase the timeline and cost of development and postpone adding new capacity to the grid.

In some states, efforts have begun to address public concern about electricity bills. In November 2025, two utility commissioners in Georgia, who had consistently approved electricity rate hikes over the previous two years, were voted out of office in a landslide.

In New York, Gov. Kathy Hochul has paused implementation of state law, driven by environmental concerns, requiring that all new buildings over seven stories tall only use electricity and not natural gas or other energy sources. Hochul has said that requirement would increase electricity demand too much, raising prices and making the grid less stable.

In Massachusetts, Gov. Maura Healey has filed legislation seeking to provide energy affordability, including eliminating some charges from utility bills, capping bill increases and barring utility companies from charging customers for advertisement costs.

Generating more power – from wind, nuclear or other sources – is only part of the potential solution.

The solutions

Clearly, there are no quick fixes or easy solutions to this complex situation.

However, innovation in regulation, combined with new technologies and even AI itself, may enable creative regulatory and technical solutions. For instance, devices that can be programmed to use energy efficiently, time-sensitive pricing and demand monitoring to smooth out peaks and valleys in electricity use can potentially ease both grid load and customers’ bills. But those solutions will work only if all the players are willing to cooperate.

There are a lot of ideas about how to lower the public’s burden of paying for data centers’ power. New ideas like this need careful scrutiny and possible revisions to ensure they are effective at lowering costs and increasing reliability.

As the country grapples with the effort to upgrade the grid, perform long-deferred maintenance and build new power plants, consumers’ costs are likely to continue to rise, further increasing pressure on Americans. Existing regulations and government oversight may no longer lower electricity costs immediately or help people plan for the rising costs over the long term.

Dominic Frisby of The Flying Frisby shares how you can profit from December’s forced selling and why you need to be out by March.

In Canada and the U.S., the tax year ends on December 31. This creates a flurry of selling as the year draws to a close. Why? Investors want to realise losses which they can then offset against gains elsewhere and so reduce their tax bill.

This creates considerable selling pressure, especially amongst small-cap stocks, and they can become quite oversold. The selling can be quite indiscriminate in the last few days before Christmas, but it abates as soon as the year ends, and the stocks often rally — particularly if there is a reason for them to rally (such as them being cheap or, better, some positive newsflow or generally better market conditions for the sector in which that company operates: eg Bitcoin rallies a bit, so all Bitcoin related companies rally).

Some years this works better than others, some picks work better than others. But manage your risk — don’t take on position sizes which are too large, be prepared to sell if the trade goes against you, etc. — and the trade can work well.

You want to be exiting your positions by February-March, so the trade has a nice structured timescale around it.

Note: Companies often do badly because they are not very good companies, so that means you are often buying not-very-good companies. Be under no illusions.

The trade seems to work particularly well with small-cap Canadian resource stocks, so you will need a broker who deals in such things. I use Interactive Investor. If you want to open an account, use this affiliate link (I get a fee, and you get a year’s free trading.)

Anatomy of a tax loss candidate

The ideal candidate wants to have spiked at some point in the last couple of years so that it sucked in a lot of buyers at higher prices. It wants to have been flat or declining for some time, so that buyers will now hate it and want it out of their portfolio, happy to sell at any price just to get rid of the wretched thing.

It wants to be really oversold so there is room for a rebound.

Ideally, they want to have some cash so they are not coming to market for capital in the New Year and thereby killing any rally with a raise.

It’s better if the company has genuine assets and is a genuine business, not some lifestyle company. That lowers risk and betters chances of positive, real newsflow in the New Year.

Take a look at this chart of Company Unknown. You can see that three times this year it spiked above $10. Now it is trading at 84c. How many people have lost money, I dread to think. It has been a proverbial clusterfook.

If you bought anywhere above $2 or $3 — and especially up near $10 or $13 – you will HATE this company.

Meanwhile, there is a huge potential loss for you to realise. So you sell it and take the loss.

But look also at the volume — that has been quite high since the sell off (short sellers covering, increased stock coming to market as it became free trading, but also capitulation). There is a story there, too. Note also the volumes when the stock went from 80c to $1.80 in October.

It’s tailing off again.

This stock could easily rise 50% — and that would only take it to $1.25, which is nothing in the context of the greater volatility.

I’ve read the chatboards. Investors hate this stock. It is not a good company. It’s even been associated with scams.

But all we are looking for is a New Year bounce.

Imagine owning Company Unknown 2, meanwhile. It’s been falling for five years!

It was a $7 stock, now it’s 60c. Investors have had five years of relentless grind lower. It’s a copper company with resources in the Southwestern U.S. That should be a golden ticket in current markets.

Investors will be furious. No surprise they’re selling.

But it’s got capital. There’s some newsflow coming early next year. It looks like it has made a low around 50c. Could this be a dollar stock by March? Why not? The world needs copper. This company has lots of it.

You get the point.

Selling in my view will climax this Friday, December 19, and Monday, December 22, but you have until New Year’s Eve to buy. (Most will have left their desks by Tuesday of next week I’d say).

The timeframe for the exit is February to March.

With all that in mind, here are 10 tax loss selling ideas for 2025-2-26:

I have been on a 2-day marathon scanning charts. Here are the best ten I could find.

This has been a hard year to find candidates, I must say, largely because resource stocks have had such a good time of it.

Crypto Treasury Companies, on the other hand, have had a terrible year, so — with a bit of help from Bitcoin (it needs to rebound) — they could enjoy a nice bounce.

I’ll tell you my ideas and then at the end of today’s piece, tell you the ones I am going for.

Tech

(NB $ = USD, unless otherwise stated).

1. Strategy Inc. (MSTR:NASDAQ)

Billionaire genius Michael Saylor’s Strategy has had a rotten time of it lately. Once trading at a premium to its Bitcoins, it’s now trading at a slight discount to them. If you want a long-term position in this company, now might not be a bad time to acquire it.

Trading at or near its lows for the year, it has properly puked.

It will only rally if Bitcoin rallies — and that particular engine has run out of steam — but it’s a prime candidate for a rebound.

2. SOL Strategies Inc. (HODL:CSE; STKE:NASDAQ).

To think I was CEO of this company once upon a time, in its earlier incarnation as a privacy company, Cypherpunk Holdings. The company changed focus a year or two ago and is now a Sol staking company.

Basically, it sinks or swims with Solana.

Earlier this year, it got to $34. Now it’s under $2. A proper puke job. One to sell and realise a loss. And so one for us to buy.

Like Strategy and Bitcoin, we will need some help from Solana. If it doesn’t rally, this remains dead in the water. But if it does, it makes a lovely flip.

This could quite easily go above $5.

3. Strive (ASST:NASDAQ) is the third of my crypto treasury ideas.

That’s the one with the chart above — Unnamed Company. I stress this trade is not about quality. It is unfortunately merging with Semler Scientific, which other readers and I hold (Semler is another tax loss candidate by the way, but there are better ones).

Again, with some help from Bitcoin, it could be a nice flip.

Here’s another tech-related idea for you.

4. Healwell AI (AIDX:TSX)

Three years ago, this was a CA$3 stock. Now it’s 85c. But it’s now a top pick of Canadian broker, Haywood Securities, which has put a target of $4.50, now that it has cleaned up its balance sheet and refocused its activities on AI.

We don’t need it to get that high. Pick it up in the low 80s and aim to flip at 1.20 is what I am looking to do.

Oil and Gas

I was looking for names in the oil and gas space as I think oil could prove a winner next year, but while oil itself has been weak, the stocks themselves have not been the disaster I have been looking for.

5. Vermilion Energy Corp. (VET:TSX; VET:NYSE) is not a bad option.

It looks like it made its low in April at CA$7. It was a CA$35 stock in 2022, so there are losers over that time frame, and this year it’s “only down” about 15% which means it is not a mega tax loss candidate. But if oil and gas rally, so will this.

I see it as quite a low-risk bet, although I don’t see mega gains either

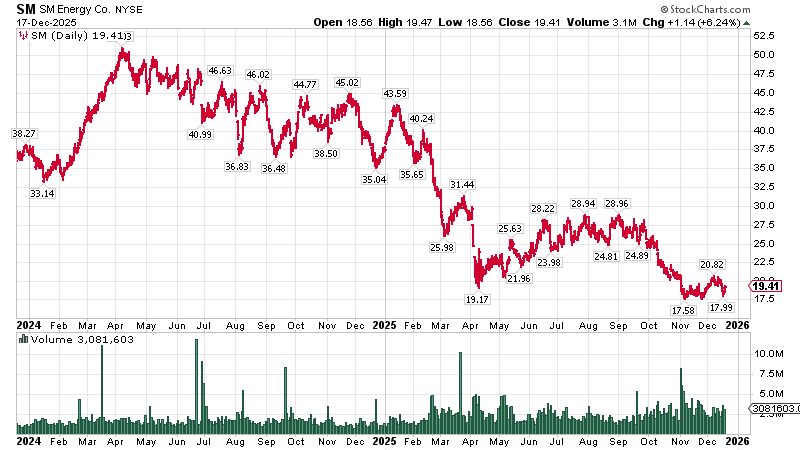

6. SM Energy Co. (SM:NYSE)

This $2 billion market company is perhaps a bit larger than ideal, but its chart — going from $50 to $17 — fits the bill.

The reason for the declines is largely lower oil prices. Its production has increased, though its margins have been compressed, so profitability is in doubt. There are also doubts about its reserves.

Such things need not bother us. We are here for a good time, not a long time.

Just as the treasury companies sink or swim with Bitcoin (and Solana), these will need some help from oil and gas prices, but oil to me looks like it’s making a long-term low at $55.

A rally early next year will give this the filip it needs. A decline, though, won’t.

Uranium

7. Lightbridge Fuels (LTBR:NASDAQ) has been a big winner for readers.

I think we first wrote it up at $3 or thereabouts, and it was a great tax loss trade last year, too.

This uranium fuel tech company, with a market cap $420 million, is up and down like the proverbial, and it has just had one of its down phases, hence my adding it to this list.

Really, the chart doesn’t quite fit the bill, but it sort of does and it keeps on giving, so I include it here, if you can get it in the $12 range, here’s hoping in 2026 it will do its thang.

Mining

8. As mentioned, we have a shortage of good mining candidates, butArizona Metals Corp. (AMC:TSX.V; AZMCF:OTCQX) is a beauty — Company Unknown 2 above.

This CA$80 million cap copper development play has been a right dog, and it has a lot of disgruntled shareholders, but it has some news flow to come early next year in the form of PEA plus about CA$15 million in cash. The chart to me looks like it has bottomed at 50c, which would make an ideal buy point.

I would have expected it to reach there, but it spiked a bit yesterday for some reason, so maybe it won’t go back there before year’s end.

9. NexMetals Mining Corp. (NEXM:TSX.V; NEXM; NASDAQ)Can’t really tell you much about this Botswana critical metals miner, except to say that it was a $50 stock 4 years ago and now it’s a $5. No surprise it’s now looking for a new CEO.

The declines have been relentless and inexorable, and now it’s near its lows. But this CA$180 million market cap company has some $90 million in cash, and some heavyweight promoters, including Frank Giustra, behind the scenes, so it fits our bill well.

Here’s the four-year chart of grimness.

10. I really shouldn’t be giving airtime to companies like this. It’s too small and too illiquid. But South Star Battery Metals Corp. (STS:TSX.V; STSBF:OTCBB)has a humdinger of a chart and plenty of cash — this CA$14 million market company just completed a highly dilutive, full warrants and all, raise CA$6.7 million.

That stock comes free trading in February 2026, so you don’t want to be around for that. Exit this one earlier than the others. But at 13c, it’s tempting.

What will be the trigger for this graphite miner? Lord knows, but the company could start by updating its presentation, which hasn’t been touched since February. What a joke.

Phew. That was some work. I need to go and get some fresh air.

Summary

So there are ten ideas here. Obviously, you can’t go for all of them. Maybe pick three or four — one from each category.

The risk with the treasury companies is that Bitcoin itself continues its declines, and we are unfortunately in crypto winter again, so that is not unlikely. Strategy is the safer option; Sol and Strive will see the bigger gains but also the bigger losses if they don’t work.

Healwell AI is tempting me too.

Oil-wise, I lean towards SM Energy.

And as for the miners, they all have their allure, but probably avoid South Star unless you are feeling really reckless.

A reminder. Don’t chase these things. Leave a stink bid under the market and let the price come to you. You have between now and New Year’s Eve to get your limit order filled.

The usual disclaimers all apply, but I should say this. If you are not an experienced trader, you might be better off not playing this game.

As always, watch your position sizes and manage your risk.

Good luck!

If you’d like to read more from Dominic, you can sign up for The Flying Frisby here.

Important Disclosures:

As of the date of this article, officers, contractors, shareholders, and/or employees of Streetwise Reports LLC (including members of their household) own securities of NexMetals Mining Corp.

Dominic Frisby: I, or members of my immediate household or family, own securities of: Strategy Inc., Sol Strategies, Healwell AI, Vermilion Energy Corp., SM Energy Co., NexMetals Mining Corp., and South Star Battery Metals Corp. . My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

Dr. John Wolstencroft: I, or members of my immediate household or family, own securities of: ishares US treasury 1-3 year ETF, Volta, Aberdeen Diversified, Black Rock World Mining, Van Eck global mining ETF, Aberdeen Asian Income..My company has a financial relationship with:None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

Dominic Frisby Disclosures: This letter is not regulated by the FCA or any other body as a financial advisor, so anything you read above does not constitute regulated financial advice. It is an expression of opinion only. Please do your own due diligence and if in any doubt consult with a financial advisor. Markets go down as well as up, especially junior resource stocks. We do not know your personal financial circumstances, only you do. Never speculate with money you can’t afford to lose.

As another busy year in the financial markets comes to an end our Senior Market Analyst Lukman Otunuga talks a look at the major stories from 2025.

This review covers the major themes, key movers, the year’s biggest shocks, our forecast scorecard, and the lessons worth taking into 2026.

All performance figures referenced are year-to-date as of 16th December 2025 unless otherwise stated.

Key takeaways

USD’s grip slips on FX throne, down 9% year-to-date

Oil ends 2025 with double-digit losses

EU50 catches up to pack, hitting fresh all-time highs

Read on as we reveal the FXTM Awards: Best performing assets of 2025!

What happened to markets in 2025?

2025 was defined by uncertainty as investors navigated Trump’s trade war, monetary policy shifts, geopolitical risk and the AI bet.

These themes sparked monstrous levels of volatility, sending tremors across the board. World stocks were placed on a rollercoaster ride in the face of Trump’s trade war before surging due to the AI bet. Nvidia, feeding off this momentum, became the first company ever to reach a market cap of $5 trillion.

The Cboe volatility index saw its biggest ever one-day spike amid the tariff chaos. A shaky dollar offered relief to G10 currencies, while oil prices were mostly pressured by oversupply fears and signs of tepid demand. In the crypto space, bitcoin bulls failed to deliver due to massive ETF outflows and growing sensitivity to macroeconomic forces. Precious metals welcomed the chaos, with one even ending the year with triple-digit gains!

Amid all these developments, there were some standout market shockers:

“Liberation Day” tariffs in April

On 2nd April 2025, the Trump administration announced a universal 10% tariff on all imported goods that would take effect on 15th April. This sent shockwaves across world markets as global growth fears sparked a risk-off stampede. The S&P500 lost more than 10% in the two days after the announcement.

Bitcoin flash crash during October

Bitcoin experienced a sudden flash crash on 10th October, wiping $12,000 from its value in a matter of minutes – resulting in an unprecedented $19 billion worth of liquidations. This brutal selloff was sparked by Trump’s threat to impose an additional 100% tariff on Chinese goods.

Longest US government shutdown in history

The US government shutdown on 1st October and didn’t reopen until 13th November.

Such an event created widespread disruptions, raised fears around the US economic outlook and threw everyone into the dark. Markets are still suffering the consequences with the October US jobs report never to be released.

How did our 2025 predictions play out?

Despite all the chaos and surprises, some of our market predictions came true.

12 months ago, we picked 3 assets that could serve up major opportunities for traders and investors this year.

Here’s how they performed:

1) Dollar loosens grip on FX throne

What we discussed in the 2025 Outlook

Our dollar outlook was firmly bullish due to Trump’s “America First” policies resulting in slower Fed rate cuts, US exceptionalism and safe-haven demand.

How things played out

The USDInd did not see its best year in a decade. Instead prices weakened as Trump’s tariffs sparked concerns over the US economic outlook.

After peaking in January, it was a slippery decline amid growing bets around the Fed cutting interest rates in the face of slowing growth.

Concerns over the Fed’s independence, political uncertainty and risk appetite favouring other currencies fuelled the USD’s decline. The longest US government shutdown in history rubbed salt into the wound.

At the start of the year, markets were only expecting the Fed to cut rates twice in 2025. We saw three rate cuts instead with further cuts expected in 2026.

Technical review

In our 2025 Outlook, we suggested “should prices slip under 105.50, bears may target the 50-week SMA at 103.90, 102.70 and 100.00.”

All bearish price targets were reached.

USD Index down 9% YTD

2) Oil lingers near 2025 lows

What we discussed in the 2025 Outlook

Our outlook on oil was heavily bearish thanks to Trump’s tariffs, global oversupply, OPEC+ output hikes, rising US shale production and still-elevated Fed rates.

How things played out

Oil prices ended 2025 roughly 15% lower but nowhere near the levels seen during the Covid-19 pandemic.

Prices were hit by demand-side fears and oversupply concerns as OPEC kept pumping production to reclaim lost market share.

In 2025, the cartel implemented a series of monthly production increases starting in April. These were part of a plan to gradually reverse previous voluntary output cuts totaling 2.2 million barrels per day (bpd). Rising non-OPEC supply and higher inventories contributed to the downside.

If not for mounting geopolitical risk in the Middle East and sanctions against Russia, oil prices may have extended loss – trading closer to Covid-19 levels.

Technical review

We suggested that “a solid weekly close below $70 may open a path toward $62, $50 and $37.”

Prices hit our first bearish price targets before bottoming out around $63.

Brent Oil down 16% YTD

3) EU plays catchup to hit all-time highs

What we discussed in the 2025 Outlook

We were firmly bullish on the EU50 due to expectations around the ECB cutting rates and easing geopolitical risk in the region.

How things played out

FXTM’s EU50 surged in 2025, gaining over 15% year-to-date.

These gains were powered by lower rates in Europe, robust earnings and a historic change to German government spending which saw hundreds of billions of euros on defense/infrastructure spending.

With more government spending for Europe’s largest economy, this boosted sentiment over the Eurozone’s economic outlook – supporting equities in the region.

Technical review

We stated that “a solid weekly close above 5110 may open a path toward 5250 and the all-time high at 5522. Beyond this point, prices may venture toward 5632.”

The EU50 peaked at 5831 in 2025, fulfilling all our bullish price targets.

EU50 up 17% YTD

FXTM Awards: Best performing assets of 2025

Looking across the FXTM universe, these were the best performing assets we offered in 2025!

Crypto: Bitcoin Cash ↑ 25% YTD

Stock Index: SPN35 ↑ 46% YTD

Metal: XAGUSD (Silver) ↑ 120% YTD

G10 currency: SEK (Swedish Krona) ↑ 20% YTD

Disclaimer: Data correct as of 16th December 2025.

What lessons can traders learn from 2025?

Volatility offers opportunity regardless of market direction was one of the biggest lessons of 2025.

We went into the year with a Trump-centric focus, bracing for his trade war to throw global markets into chaos.

Trump certainly didn’t disappoint with the knock-on effects impacting commodities, currencies, indices and cryptos.

But markets proved resilient with equities across the globe hitting records and on track for double-digit gains in 2025.

Metals also found their champion in silver, which gained 100% year-to-date amid supply constraints and rate cut bets. Interestingly bitcoin suffered from heavy institutional selling and could be on track for its first negative year since 2022.

We saw the AI bet and expectations around lower interest rates support global stocks this year, but the question is for how long?

What’s the outlook for 2026?

With concerns still lingering around an AI bubble, tariffs starting to bite and geopolitical risk present, things could spice up in 2026.

And this means one thing: more volatility.

Get the inside story on what to expect from markets next year with our 2026 Outlook, which is set to be published early January 2026.

In a Nov. 24, 2025, filing by representatives of more than 300 victims and family members, Binance and its former CEO – recently pardoned Changpeng Zhao – were accused of willfully ignoring anti-money-laundering and so-called “know your customer” controls that require financial institutions to identify who is engaging in transactions.

In so doing, the suit alleged that Binance and Zhao – who in 2023 pleaded guilty to money laundering violations – allowed U.S.-designated terrorist entities such as Hamas and Hezbollah to launder US$1 billion. Binance has declined to comment on the case but issued a statement saying it complies “fully with internationally recognized sanctions laws.”

As an expert in countering the proliferation of weapons technology, I believe the Binance-Hamas allegations could represent the tip of the iceberg in how cryptocurrency is being leveraged to undermine global security and, in some instances, U.S. national security.

Cryptocurrency is aiding countries such as North Korea, Iran and Russia, and various terror- and drug-related groups in funding and purchasing billions of dollars worth of technology for illicit weapons programs.

Though some enforcement actions continue, I believe the Trump administration’s embrace of cryptocurrency might compromise the U.S.’s ability to counter the illicit financing of military technology.

For the past 13 years, the Project on International Security, Commerce, and Economic Statecraft, where I serve as a research fellow, has conducted research and led industry and government outreach to help countries counter the proliferation of dangerous weapons technology, including the use of cryptocurrency in weapons fundraising and money laundering.

Over that time, we have seen an increase in cryptocurrency being used to launder and raise funds for weapons programs and as an innovative tool to evade sanctions.

Efforts by state actors in Iran, North Korea and Russia rely on enforcement gaps, loopholes and the nebulous nature of cryptocurrency to launder and raise money for purchasing weapons technology. For example, in 2024 it was thought that around 50% of North Korea’s foreign currency came from crypto raised in cyberattacks.

A digital bank heist

In February 2025, North Korea stole over $1.5 billion worth of cryptocurrency from Bybit, a cryptocurrency exchange based in the United Arab Emirates. Such attacks can be thought of as a form of digital bank heist. Bybit was executing regular transfers of cryptocurrency from cold offline wallets – like a safe in your home – to “warm wallets” that are online but require human verification for transactions.

North Korean agents duped a developer working at a service used by Bybit to install malware that granted them access to bypass the multifactor authentication. This allowed North Korea to reroute the crypto transfers to itself. The funds were moved to North Korean-controlled wallets but then washed repeatedly through mixers and multiple other crypto currencies and wallets that serve to hide the origin and end location of the funds.

Cryptocurrency is attractive because of the ease with which it can be acquired and transferred between accounts and various digital and government-issued currencies, with little to no requirements to identify oneself.

And as countries such as Russia, Iran and North Korea have become constricted by international sanctions, they have turned to cryptocurrency to both raise funds and purchase materials for weapons programs.

Even stablecoins, promoted by the Trump administration as safer and backed by hard currency such as the U.S. dollar, suffer from extensive misuse linked to funding illicit weapons programs and other activities.

But recent analysis shows that despite enforcement efforts, the cryptocurrency industry continues to lag behind when it comes to enforcing anti-money-laundering safeguards. In at least some cases this is willful, as some crypto firms may attempt to circumvent controls for profit motives, ideological reasons or policy disputes over whether platforms can be held accountable for the actions of individual users.

It isn’t only the raising of these funds by rogue nations and terrorist groups that poses a threat, though that is often what makes headlines. A more pressing concern is the ability to quietly launder funds between front companies. This helps actors avoid the scrutiny of traditional financial networks as they seek to move funds from other fundraising efforts or firms they use to purchase equipment and technology.

The incredible number of crypto transactions, the large number of centralized and decentralized exchanges and brokers, and limited regulatory efforts have made crypto incredibly useful for laundering funds for weapons programs.

This process benefits from a lack of safeguards and “know your customer” controls that banks are required to follow to prevent financial crimes. These should, I believe, and often do apply to entities large and small that help move, store or transfer cryptocurrency known as virtual asset service providers, or VASPs. However, enforcement has proven difficult as there are an incredibly large number of VASPs across numerous jurisdictions. And jurisdictions have fluctuating capacity or willingness to implement controls.

The rewards for rogue nations and organizations such as North Korea can be great.

Ever the savvy sanctions evader, North Korea has benefited the most from its early vision on the promise of crypto. The reclusive country has established an extensive cyber program to evade sanctions that relies heavily on cryptocurrency. It is not known how much money North Korea has raised or laundered in total for its weapons program using crypto, but in the past 21 months it has stolen at least $2.8 billion in crypto.

Iran has also begun relying on cryptocurrency to aid in the sale of oil linked to weapons programs – both for itself and proxy forces such as the Houthis and Hezbollah. These efforts are fueled in part by Iran’s own crypto exchange, Nobitex.

Russia has been documented going beyond the use of crypto as a fundraising and laundering tool and has begun using its own crypto to purchase weapons material and technology that fuel its war against Ukraine.

A threat to national security

Despite these serious and escalating risks, the U.S. government is pulling back enforcement.

The controversial pardon of Binance founder Changpeng Zhao raised eyebrows for the signal it sends regarding U.S. commitment to enforcing sanctions related to the cryptocurrency industry. Other actions such as deregulating the banking industry’s use of crypto and shuttering the Department of Justice’s crypto fraud unit have done serious damage to the U.S.’s ability to interdict and prevent efforts to utilize cryptocurrencies to fund weapons programs.

These actions, I believe, send the wrong message. At this very moment, cryptocurrency is being illicitly used to fund weapons programs that threaten American security. It’s a real problem that deserves to be taken seriously.

And while some enforcement actions do continue, failing to implement and enforce safeguards up front means that crypto will continue to be used to fund weapons programs. Cryptocurrency has legitimate uses, but ignoring the laundering and sanctions-evasion risks will damage American national interests and global security.

As Americans gather for holiday celebrations, many will quietly thank the health care workers who keep their families and friends well: the ICU nurse who stabilized a grandparent, the doctor who adjusted a tricky prescription, the home health aide who ensures an aging relative can bathe and eat safely.

As an economist who studies how immigration influences economies, including health care systems, I see a consistent picture: Immigrants are a vital part of the health care workforce, especially in roles facing staffing shortages.

America’s health care system is entering an unprecedented period of strain. An aging population, coupled with rising rates of chronic conditions, is driving demand for care to new heights.

State-level data reveals just how deeply immigrants are embedded in the health care system. Consider California, where immigrants account for 1 in 3 physicians, 36% of registered nurses and 42% of health aides. On the other side of the country, immigrants make up 35% of hospital staff in New York state. In New York City, they are the majority of health care workers, representing 57% of the health care workforce.

Even in states with smaller immigrant populations, their impact is outsized.

These patterns transcend geography and partisan divides. From urban hospitals to rural clinics, immigrants keep facilities operational. Policies that reduce their numbers – through higher visa fees, stricter eligibility requirements or increased deportations – have ripple effects, closed hospital beds.

While health care demand soars, the pipeline for new health care workers could struggle to keep pace under current rules. Medical schools and nursing programs face capacity limits, and the time required to train new professionals – often a decade for doctors – means that there aren’t any quick fixes.

Immigrants have long bridged this gap – not just in clinical roles but in research and innovation. International students, who often pursue STEM and health-related fields at U.S. universities, are a key part of this pipeline. Yet recent surveys from the Council of Graduate Schools show a sharp decline in new international student enrollment for the 2025-26 academic year, driven partly by visa uncertainties and global talent competition.

If this trend holds, the smaller cohorts arriving today will mean fewer physicians, nurses, biostatisticians and medical researchers in the coming decade – precisely when demand peaks. Although no major research organization has yet modeled the full impact that stricter immigration policies could have on the health care workforce, experts warn that tighter visa rules, higher application fees and stepped-up enforcement are likely to intensify shortages, not ease them.

These policies make it harder to hire foreign-born workers and create uncertainty for those already here. In turn, that complicates efforts to staff hospitals, clinics and long-term care facilities at a moment when the system can least afford additional strain.

The hidden toll: Delayed care, rising risks

Patients don’t feel staffing gaps as statistics – they feel them physically.

A specialist appointment delayed by months can mean worsening pain. Older adults without home care aides face higher risks of falls, malnutrition and medication errors. An understaffed nursing home turning away patients leaves families scrambling. These aren’t hypotheticals – they’re already happening in pockets of the country where shortages are acute.

The costs of restrictive immigration policies won’t appear in federal budgets but in human tolls: months spent with untreated depression, discomfort awaiting procedures, or preventable hospitalizations. Rural communities, often served by immigrant physicians, and urban nursing homes, reliant on immigrant aides, will feel this most acutely.

Most Americans won’t read a visa bulletin or a labor market forecast over holiday dinners. But they will notice when it becomes harder to get care for a child, a partner or an aging parent.

Aligning immigration policy with the realities of the health care system will not, by itself, fix every problem in U.S. health care. But tightening the rules in the face of rising demand and known shortages almost guarantees more disruption. If policymakers connect immigration policy to workforce realities, and adjust it accordingly, they can help ensure that when Americans reach out for care, someone is there to answer.

Michael Ballanger of GGM Advisory Inc. shares some words of wisdom and his 2026 outlook.

Originating in Greek mythology as a challenge to divine order, the term “hubris” remains a significant theme in literature and life, representing a dangerous belief in one’s own invincibility or superiority. Strictly defined, it is “excessive pride, arrogance, or overconfidence that leads to a person’s downfall, often by causing them to overstep limits, defy gods, or ignore warnings.”

Mark Twain had a different definition that we as humans know all too well. Twain once wrote, “It ain’t what you don’t know that gits ya into trouble. It’s what you know for sure that ain’t exactly so.”

I had a teacher who reminded me at a very young age that making blind assumptions without checking one’s facts is a recipe for disaster and, worse still, embarrassment. “You know what you do when you ‘ASSUME’ something? You make an “ASS” of “U” and “ME.”

In the practice of writing newsletters, one tends to get elevated to the undeserved role of “authority,” as in, “he/she is an authority on gold and silver.” Sometimes, authors of financial newsletters are assigned designations like “guru” or “pundit” or “expert” but the reality of this pastime (as opposed to profession) is that most of us are simply common folks that for some unworldly reason have the intestinal fortitude and rhinoceros-like skin to put their opinions, expert or not, out there in full view for all the world to judge and rejoice or judge and condemn. The rejoicing comes after a particularly good guess (as opposed to calculation) at the future direction and amplitude of a particular stock or commodity. The condemnation occurs when one’s stab at the future direction and amplitude of a particular stock or commodity winds up in the trash bin. Reward or punishment for well-executed speculations is either more or fewer followers, and depending on whether one is paid as a “content provider” or under the subscriber model, loss or gain of people that grew accustomed to one’s accurate (or inaccurate) guesses.

As a young boy, I used to sell papers in the wee hours of weekend mornings at Woodbine Racetrack in northwest Toronto where the industry professionals such as trainers and grooms and jockeys would all arrive as the sun was rising and pay a dime for the “Daily Racing Form” which had all the races and the horses listed along with a list of their last three heats on either the turf (grass) or mud (dirt). One section of the paper featured the section where the handicappers wrote a column with their “touts” for the day’s races, which is where the term “tout sheet” was first derived. There was “Peter’s Picks,” “The Trackman,” and “The OddsMaker” all picking winners, placers, and showers for the expressed benefit of the amateur handicapper or weekend gambler who would lay down their minimum $2 bets with absolute certainty after reading through the hieroglyphics contained in the form.

One day, I decided to keep track of all the picks made by the “expert” race appraisers, so for the next few months of the summer, I wrote down the names of all the horses and where they finished each race. At the same time, I would pick three horses to win, place, and show in the same races, all based on their “colours” which were bay, chestnut, black, brown, or gray. At the end of the season, I tallied up all the results, and to no one’s particular surprise (except mine), a 12-year-old boy picking horses based on the colour of their coats outperformed the “experts” all equipped with 30-odd years of bookmaking and handicapping under their belts.

That is eerily similar to the late 1970s when newsletter guru and former E.F. Hutton Senior Technical Analyst Joe Granville would ask chimpanzees (dressed up as Wall Street bankers) to throw darts at the stock pages of the Wall Street Journal and then compare their track records to those of the “bank trust officers” that are today’s “market strategists.”

The results were all the same. Sometimes the monkeys would be on top of the pack (usually in down markets), and sometimes they would be in the middle of the pack, but rarely did they trail the pack, once again proving that “A Random Walk down Wall Street” author Burton G. Malkiel was more than just a theorist but more of a statistician.

Over the years, I have found that investment success was more common in areas in which I was familiar, such as the junior mining space. I think the reason that my career evolved around commodities and mining was my fascination with those horses at Woodbine. You could look at two dozen horses under two dozen different jockeys, and only in the manner in which both horse and rider displayed a certain “swagger” could one recognize the importance of “presence” in the sport of kings. In a similar manner, CEO’s of successful mining and or exploration companies would emit a similar “swagger” when they entered a boardroom.

The firmness of a handshake or the directness of focus when being introduced seemed to accompany the great ones. However, at the end of the day, even the great ones (like Friedland, Beattie, or Netolitzky) would be the first to admit that really great geologists need an ample serving of good fortune in order to amass enviable track records. Luck does play a big part in any discovery because even the most sophisticated technology in geophysics or geochemistry cannot prevent Mother Nature and Lady Luck from playing a cruel trick with ruthless regularity and tempestuous timing.

Technical analysts would have us believe that all those squiggly lines on a graph are infinitely more predictive than the soggy leaves at the bottom of a teacup or a wishbone-shaped piece of driftwood in locating subsurface water. However, despite finding personal success in using the tool called “technical analysis” (“TA”) in improving returns, I learned a valuable lesson this past week. About a month ago, with gold prices approaching $4,400, I used TA to identify a series of extreme readings that, in past eras, have led to trend reversals.

As a result, on October 17, I sent out an email alert calling for a top in gold, which resulted in an outside key reversal day followed by a retest the following Monday that also failed. As a result, my call for the near-term top in gold was then and remains today as a solid one, with February gold still $213 below the top of $4,433 seen the prior Friday.

Inflated with inner peace and burgeoning with the pride one feels when a particular call goes well, I waited with the patience of a lion-hunter for another popular metal to display characteristics similar to that of gold. I lurked silently in the bushes until late November, and with all the hubris and swagger of a Secretariat or Northern Dancer approaching the starting gate, I elected to make the call that I now regret, and that call was “Sell silver.” The price was around $57.00 per ounce basis March.

During the week immediately following that call, I began to sense that there had been a kind of shift, as in “there’s been a shift in the force, Luke” from Star Wars fame, as silver spat in the face of GGMA “expertise” and drove northward through $59. On Monday, March silver gapped through $60, and by Thursday, it hit $65.

What changed?

As I sat in my office overlooking the lovely and now-frozen Scugog Swamp listening intently to Fed Chairman Jerome Powell, I decided to write the following to my subscribers:

“In keeping with the Fed’s dual mandates of “price stability” and “maximum full employment,” their clandestine third mandate “protecting Wall Street” was delivered wonderfully today by Fed Chairman Jerome Powell as he walked the world through the 2:30 presser with nary a thought about inflation but ample comments about the “weakening jobs market.” Wall Street took that as a “dovish” tilt and took the DJIA to a 600-point gain and the S&P 500 to a 55-point gain. Traders also took the U.S. dollar down with the DXY down .568 to 98.632, and gold from down $30 to up $27, and silver from down $0.27 to up $1.36.

With this kind of cheerleading, the Fed has given traders an early Christmas gift, so my speculation of a weaker, 2018-style close to 2025 must be shuttered. Also, the hedges on gold and silver being used in the GGMA 2025 Trading Account have to be re-examined as the dovish Fed has now thrown the U.S. dollar overboard in favour of easier money. The Fed has also reintroduced a mild form of quantitative easing, or as the commentators called it, “soft QE.” In a scenario of Fed purchases of $40 billion of T-bills every month, we are back to a stimulative environment, which, from where I sit, is patently absurd given the S&P within a chip shot of record highs. Any time the Fed engineers a “risk on” policy move, stocks and the metals always move higher, so to be hedged against a stimulative Fed is at once dangerous and stupid.

I look for traders to now have a free rein to take stocks and the metals higher into year-end. While I will not move to add to any new long positions in the gold or silver space, I now expect February gold to re-test the high of October 19th at $4,433. Gold traders cannot ignore the breathtaking breakout in silver, so I suspect that there will be a lot of short-covering by the end of the month. I will be looking at the RSI and the HUI:US to see if we get a confirmed new high for gold. If we get one, I will open new speculative positions in the leveraged ETFs and in options.”

This week, the HUI:US broke out above the October 15 high of 693.10 and moved to a new record high of 715.70. All that is required for there to be a confirmed new “leg” of the precious metals bull is for February gold to close above $4,433. At Friday’s high, it was $4,387.80, so we are banging on the proverbial door.

I used a phrase in this Thursday’s alert that should be recalled and recited, and that is this: “It is not a sin to be wrong, but it IS a sin to STAY wrong.”

May we never forget the wisdom of that adage.

2026

Moving into 2026 is going to be a very interesting endeavour as I am now forced to begin to formulate the GGMA 2026 Forecast Issue, which seems to be getting more difficult each and every year. The newsletter I write focuses on a given theme each year, after starting off in 2020 with the idea that escalating debt levels in the West would eventually require collateralization of sovereign debt with gold reserves, and whether it was pandemics or regional bank problems, each crisis was met with monetization.

Debt has remained a dominant theme and rationale for gold and silver ownership every year since the service was founded, but in the past two years, the electrification movement and the macroeconomic outlook for copper sent me scurrying for senior and junior opportunities in the northern and southern hemispheres. I used my beloved Freeport-McMoRan Inc. (FCX:NYSE)as a proxy for not only copper but also gold, as the globe’s premier producer of the red metal is also a significant member of the gold club, thanks largely to its part-ownership of the mighty Grasberg Mine in Indonesia.

With great trepidation and fear verging upon abject guilt, I exited FCX in early July based largely on my concern that the huge gap between London Metals Exchange copper (at $4.40/lb.) was too much of a discount to CME (U.S.) copper, which had been “tariffed” into a $1.50 premium over London due solely to political posturing. A seminal event occurred in July when the Trump Administration elected to remove tariffs on imports of “raw copper,” causing a cataclysmic crash in U.S. copper prices to align perfectly with London prices. I bought back my position in July at sub-$40 and then exited again in September when copper prices had rebounded into overbought conditions.

Then the news hit of the Grasberg “mud rush” accident that caused a halt in operations in that portion of the mine complex, after which the stock cratered to just above $35. I fully expected that overvalued equity markets would weaken during the seasonally soft August-October period, but resilient equities and a stubbornly strong copper price prevented the target price of “sub-$30” from ever being achieved. So, here I sit, with 13 trading sessions left in 2025, and I am bereft of my beloved FCX as it steams northward at $47.38 after hitting $49 earlier today. Every single time I exit FCX, karma bites me in the backside, shaking its skeletal finger while shrieking “Sacrilege!”

The good news is that I have been blessed with a couple of junior copper deals that caught my attention in 2025. One is not new in that I have been an investor in Australian Campbell Smyth’s

Fitzroy Minerals Inc. (FTZ:TSX.V; FTZFF:OTCQB) since 2019, when he launched Norseman Silver into what we both thought could be a rip-roaring silver market in 2020. The company went through growing pains in 2020-2022 and then went “dark” in 2023 before finding a new team of managers and projects in U.K.-based CEO Merlin Marr-Johnson and Santiago-based COO Gilberto Schubert and after bottoming in late 2023 at $.035, the shares responded favourably to the management change and since then have not had time to even glance into the rear-view mirror.

Smyth has put together one superb team of highly-skilled professionals and is now backed by Crux Investor founder Matt Gordon as a major shareholder as well as Technical Advisor Craig Perry in their quest for copper stardom in the Atacama Region of the Chilean Andes. Searching for copper in Chile is like looking for seashells in the Bahamas in that, despite declining grade and reserves in some of the legendary state-run Codelco operations, it is the prime locale for copper discoveries. Blessed with a wonderfully hospitable mining environment, only the province of Quebec in Canada is friendlier to people with money looking to find metals while employing people, a notion that the Canadian provinces of Ontario and B.C. might consider. Smyth and friends have raised over CA$20 million since the lows of 2023 and have since come up with a brand new copper-gold-molybdenum discovery in their Caballos project that serves as a wonderful complement to their oxide copper deposit at Buen Retiro.

However, the seriously underpromoted and underemphasized component of that property is what may or may not be lurking under that massive oxide copper-bearing cap. Management has been quite “coy” about revealing anything about drilling intentions until their press release of December 2, where they reported: “Hole 43, 150 metres north of hole 42, is currently underway. Crucially, the core photographs look very similar to the style of mineralization from within the resource zone at Candelaria. These holes are the first time that Fitzroy has seen consistent sulphide mineralization of this nature, which further enhances the exploration model at this project.

Followers of this publication are quite familiar with my contention that Buen Retiro is one of those projects where management has — most appropriately — de-risked the project by drilling of the easily fundable oxide cap, where CAPEX requirements are relatively low, while carefully and very much under the cloak of darkness, valiantly trying to unlock the secrets of the deeper regions of Andean geology. All I can say is that it is exciting to be a shareholder, and we will leave it at that.

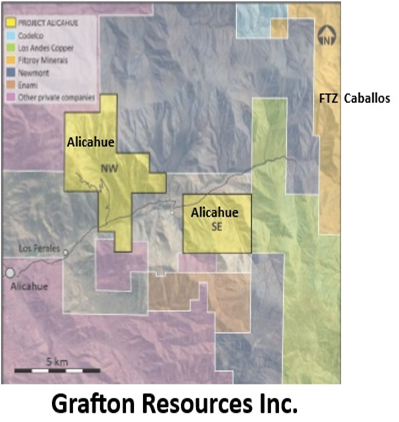

The other Chilean project is Grafton Resources Inc. (GFT:CSE; PMSXF:OTC), where essentially the same management group as Fitzroy has attempted to firewall the two main projects (Buen Retiro and Caballos) from further dilution by way of the creation of this new company.

New prospects that come across Schubert’s desk are funnelled into Grafton while the team focuses 100% on near-term production for Fitzroy, which is somewhat akin to one car driving in the middle lane of the Autobahn while the other is in the outside lane with full throttle, taking the moniker of “aggressive exploration.”

With a capital structure time-warped from the 1980s, GFT has only 25 million shares issued, $4m in the bank, and a project (Alicahue) approved for drilling in January. All that needs to be completed is an airborne MMT survey to be completed in the very early New Year, and then it is “Game on.”

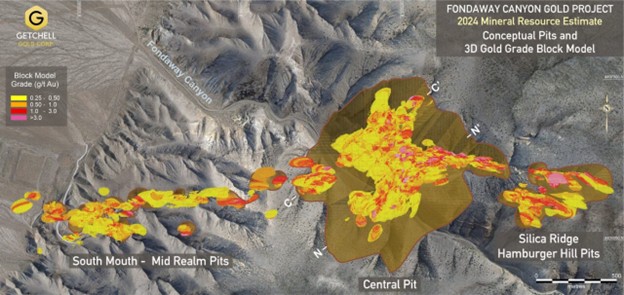

Many of the people who follow me are asking questions about Getchell Gold Corp. (GTCH:CSE; GGLDF:OTCQB) and the dismal lack of performance in this latest move in the mining stocks, as evidenced by the HUI:US move to 715 this week.

As a starter, the promotions of the last few years are not exactly at new highs. Let’s start with the greatest promotion in eastern Canada since the Hibernia oil discoveries in the late 1970s —

New Found Gold Corp. (NFG:TSX.V; NFGC:NYSE.American) — a highly publicized holding of billionaire Eric Sprott, who loves to have his name on private placements in order to attract institutional accompaniment.

The stock topped in 2021 at CA$13.50 per share, only to go through a series of disappointing resource calculations and board-level resignations. The stock is now at $3.93 despite an advance in gold from $1,700 in the month it topped in 2021 to the current level of $4,329.

Those who bought shares in NFG in 2021 as a proxy for a) gold and b) Eric Sprott’s brain have been squarely left in the camp of the “Bagholder Blues.” Let us take another look at the famous gold promotions of the past few years.

How about Novo Resources Corp. (NVO:TSX.V; NSRPF:OTCQX).

This company is touted by both Eric Sprott and legendary geoscientist Quentin Hennigh.

It topped at over $8.00 in 2017 and now resides at $0.12.

I would ask you all: Is it any wonder why a company staffed with solid management and loyal shareholders, developing an economically-viable project in an infinitely-promotable jurisdiction (Nevada), cannot cop a bid from the Sprotts or Rules of this world? Why does it take years to attract the favor of really well-intentioned and seasoned influencers?