You might not know it from the headlines, but there is some good news about the global fight against climate change.

A decade ago, the cheapest way to meet growing demand for electricity was to build more coal or natural gas power plants. Not anymore. Solar and wind power aren’t just better for the climate; they’re also less expensive today than fossil fuels at utility scale, and they’re less harmful to people’s health.

Yet renewable energy projects face headwinds, including in the world’s fast-growing developing countries. I study energy and climate solutions and their impact on society, and I see ways to overcome those challenges and expand renewable energy – but it will require international cooperation.

Falling clean energy prices

As their technologies have matured, solar power and wind power have become cheaper than coal and natural gas for utility-scale electricity generation in most areas, in large part because the fuel is free. The total global power generation from renewable sources saved US$467 billion in avoided fuel costs in 2024 alone.

As a result of falling prices, over 90% of all electricity-generating capacity added worldwide in 2024 came from clean energy sources, according to data from the International Renewable Energy Agency.

Burning coal, oil and natural gas releases tiny particles into the air along with toxic gases; these pollutants can make people sick. A recent study found air pollution from fossil fuels causes an estimated 5 million deaths worldwide a year, based on 2019 data.

Fossil fuels are also the leading sources of climate-warming greenhouse gases. When they’re burned to generate electricity or run factories, vehicles and appliances, they release carbon dioxide and other gases that accumulate in the atmosphere and trap heat near the Earth’s surface. That accumulation has been raising global temperatures and causing more heat stress, respiratory illnesses and the spread of disease.

Electrifying buildings, cars and appliances, and powering them with renewable energy, reduces these air pollutants while slowing climate change.

So what’s the problem?

In spite of the demonstrated economic and health benefits of transitioning to renewable energy, regulatory inertia, political gridlock and a lack of investment are holding back renewable energy deployment in much of the world.

The 2024 Energy Permitting Reform Act introduced by Sens. Joe Manchin, a Democrat from West Virginia, and John Barrasso, a Republican from Wyoming, to speed approvals failed to pass. Manchin called it “just another example of politics getting in the way of doing what’s best for the country.”

These countries need to meet soaring energy demand. The International Energy Agency expects emerging economies to account for 85% of added electricity demand from 2025 through 2027. Yet renewable energy development lags in most of them. The main reason is the high price of financing renewable energy construction.

Most of the cost of a renewable energy project is incurred up front in construction. Savings occur over its lifetime because it has no fuel costs. As a result, the levelized cost of energy (LCOE) for those projects varies depending on the cost of financing to build them. The chart shows what happens when borrowing costs are higher in developed countries. It illustrates the share of financing in each project’s levelized cost of energy in 2024 versus the weighted average cost of capital (WACC). The yellow dots are solar projects; black and gray are offshore and onshore wind. Adapted from IRENA, 2025, CC BY

In many developing countries, wind and solar projects cost more to finance than coal or gas. Fossil projects have a longer history, and financial and policy mechanisms have been developed over decades to lower lender risk for those projects. These include government payment guarantees, stable fuel contracts and long-term revenue deals that help guarantee the lender will be repaid.

Both lenders and governments have less experience with renewable energy projects. As a result, these projects often come with weaker government guarantees. This raises the risk to lenders, so they charge higher interest rates, making renewable projects more expensive upfront, even if the projects have lower lifetime costs.

To lower borrowing costs, governments and international development banks can take steps to make renewable projects a safer bet for investors. For example, they can keep energy policies stable and use public funds or insurance to cover part of the lenders’ investment risk.

Without international cooperation to lower finance costs, developing economies could miss out on the renewable-energy revolution and lock in decades of growing greenhouse gas emissions from fossil fuels, making climate change worse.

Achieving this goal won’t be easy, but it is significantly less difficult now that renewable energy is more affordable over the long run than fossil fuels.

Switching the world’s power supply to renewable energy and electrifying buildings and local transportation would cut about half of today’s greenhouse-gas emissions. The other half comes from sectors where it is harder to cut emissions — steel, cement and chemical production, aviation and shipping, and agriculture and land use. Solutions are being developed but need time to mature. Good governance, political support and accessible finance will be critical for these sectors as well.

The transition to renewable energy offers big economic and health benefits alongside lower climate risks — if countries can overcome political obstacles at home and cooperate to expand financing for developing economies.

Some major oil companies such as Shell and BP that once were touted as leading the way in clean energy investments are now pulling back from those projects to refocus on oil and gas production. Others, such as Exxon Mobil and Chevron, have concentrated on oil and gas but announced recent investments in carbon capture projects, as well as in lithium and graphite production for electric vehicle batteries.

Despite the relatively modest scale of investment in clean energy by oil and gas companies so far, there are several business reasons oil companies would increase their investments in clean energy over time.

The oil and gas industry has provided energy that has helped create much of modern society and technology, though those advances have also come with significant environmental and social costs. My own experience in the oil industry gave me insight into how at least some of these companies try to reconcile this tension and to make strategic portfolio decisions regarding what “green” technologies to invest in. Now the managing director and a professor of the practice at the Ray C. Anderson Center for Sustainable Business at Georgia Tech, I seek ways to eliminate the boundaries and identify mutually reinforcing innovations among business interests and environmental concerns.

Diversification and financial drivers

Just like financial advisers tell you to diversify your 401(k) investments, companies do so to weather different kinds of volatility, from commodity prices to political instability. Oil and gas markets are notoriously cyclical, so investments in clean energy can hedge against these shifts for companies and investors alike.

Clean energy can also provide opportunities for new revenue. Many customers want to buy clean energy, and oil companies want to be positioned to cash in as this transition occurs. By developing employees’ expertise and investing in emerging technologies, they can be ready for commercial opportunities in biofuels, renewable natural gas, hydrogen and other pathways that may overlap with their existing, core business competencies.

Fossil fuel companies have also found what other companies have: Clean energy can reduce costs. Some oil companies not only invest in energy efficiency for their buildings but use solar or wind to power their wells. And adding renewable energy to their activities can also lower the cost of investing in these companies.

Some companies, such as BP and Equinor, have previously even gone so far as rebranding themselves and acquiring clean energy businesses. But those efforts have also been criticized as “greenwashing,” taking actions for public relations value rather than real results.

How far can this go?

It is even possible for a fossil fuel company to reinvent itself as a clean energy operation. Denmark’s Orsted – formerly known as Danish Oil and Natural Gas – transitioned from fossil fuels to become a global leader in offshore wind. The company, whose majority owner is the Danish government, made the shift, however, with the help of significant public and political support.

To show students in my sustainability classes how companies’ choices affect both the environment and the industry as a whole, I use the MIT Fishbanks simulation. Students run fictional fishing companies competing for profit. Even when they know the fish population is finite, they overfish, leading to the collapse of the fishery and its businesses. Short-term profits cause long-term disaster for the fishery and the businesses that depend on it.

Yet students in a recent class showed me that a more collective way of thinking may be possible. Teams voluntarily reduced their fishing levels to preserve long-term business and environmental sustainability, and they even cooperated with their competitors. They did so without in-game regulatory threats, shareholder or customer complaints, or lawsuits.

Their shared understanding that the future of their own fishing companies was at stake makes me hopeful that this type of leadership may take hold in real companies and the energy system as a whole. But the question remains about how fast that change can happen, amid the accelerating global demand for more energy along with the increasing urgency and severity of climate change and its effects.

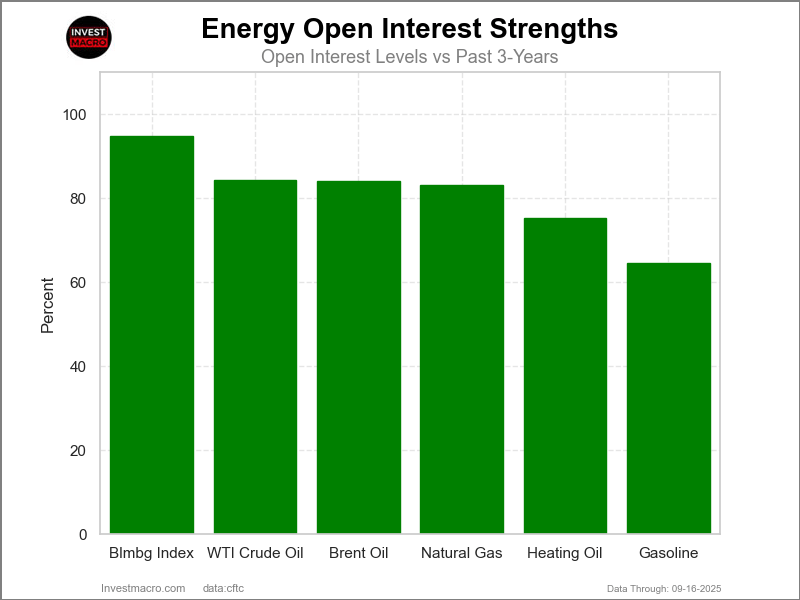

Open Interest Strength Levels vs Past 3-Years (Where are Traders putting positions in?)

Here are the latest charts and statistics for the Commitment of Traders (COT) data published by the Commodities Futures Trading Commission (CFTC).

The latest COT data is updated through Tuesday September 16th and shows a quick view of how large traders (for-profit speculators and commercial entities) were positioned in the futures markets.

Weekly Speculator Changes led by WTI Crude Oil

The COT energy market speculator bets were overall higher this week as four out of the six energy markets we cover had higher positioning while the other two markets had lower speculator contracts.

Leading the gains for the energy markets was WTI Crude Oil (16,865 contracts) with Gasoline (2,538 contracts), Brent Oil (1,496 contracts) and the Bloomberg Commodity Index (30 contracts) also having positive weeks.

The markets with declines in speculator bets for the week were Natural Gas (-16,397 contracts) and with Heating Oil (-474 contracts) also seeing slightly lower bets on the week.

Natural Gas leads Energy Price Changes

The energy markets price changes were mixed this week. Natural Gas was the highest mover with a muted 0.37% gain over the past 5 days. Natural Gas has been down -7.12% over the past 30 days while dropping a sharp -31.52% over the past 90 days.

Next up, Heating Oil was higher by 0.25% this week. Heating Oil is up 2.65% over the past 30 days while seeing a gain of 10.57% over the past 90 days.

WTI Crude Oil edged higher this week by 0.22% and has been up 8.73% over the past 90 days.

Brent Crude Oil was modestly lower by -0.38% over the past week. Brent Crude Oil has been up by approximately 1.5% in the past 30 days and is higher by 9% in the past 90 days.

The Bloomberg Commodity Index was the next lowest with a -0.43% return on the week while Gasoline saw the highest decline on the week with a -0.81% dip. Gasoline has been higher by 3.5% over the past 30 days and is up by approximately 6% over the past 90 days.

Energy Data:

Legend: Weekly Speculators Change | Speculators Current Net Position | Speculators Strength Score compared to last 3-Years (0-100 range)

Strength Scores led by Heating Oil & Natural Gas

COT Strength Scores (a normalized measure of Speculator positions over a 3-Year range, from 0 to 100 where above 80 is Extreme-Bullish and below 20 is Extreme-Bearish) showed that Heating Oil (68.5 percent) and Natural Gas (53.7 percent) led the energy markets this week.

On the downside, WTI Crude (6.3 percent) comes in at the lowest strength level and is the only market currently in Extreme-Bearish territory (below 20 percent).

Strength Statistics: WTI Crude Oil (6.3 percent) vs WTI Crude Oil previous week (0.0 percent) Brent Crude Oil (45.9 percent) vs Brent Crude Oil previous week (43.8 percent) Natural Gas (53.7 percent) vs Natural Gas previous week (66.3 percent) Gasoline (44.5 percent) vs Gasoline previous week (40.9 percent) Heating Oil (68.5 percent) vs Heating Oil previous week (69.1 percent) Bloomberg Commodity Index (44.8 percent) vs Bloomberg Commodity Index previous week (44.7 percent)

Gasoline tops the 6-Week Strength Trends

COT Strength Score Trends (or move index, calculates the 6-week changes in strength scores) showed that Gasoline (13.2 percent) leads the past six weeks trends for the energy markets. Heating Oil (0.9 percent) is the next highest positive mover in the latest trends data.

WTI Crude (-16.1 percent), Natural Gas (-13.2 percent) and the Bloomberg Index (-9.8 percent) lead the downside trend scores currently.

Move Statistics: WTI Crude Oil (-16.1 percent) vs WTI Crude Oil previous week (-27.7 percent) Brent Crude Oil (-3.6 percent) vs Brent Crude Oil previous week (-5.8 percent) Natural Gas (-13.2 percent) vs Natural Gas previous week (-6.8 percent) Gasoline (13.2 percent) vs Gasoline previous week (-1.7 percent) Heating Oil (0.9 percent) vs Heating Oil previous week (-6.7 percent) Bloomberg Commodity Index (-9.8 percent) vs Bloomberg Commodity Index previous week (-10.4 percent)

Individual COT Market Charts:

WTI Crude Oil Futures:

The WTI Crude Oil Futures large speculator standing this week came in at a net position of 98,709 contracts in the data reported through Tuesday. This was a weekly rise of 16,865 contracts from the previous week which had a total of 81,844 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 6.3 percent. The commercials are Bullish-Extreme with a score of 95.5 percent and the small traders (not shown in chart) are Bearish with a score of 34.1 percent.

Price Trend-Following Model: Weak Uptrend

Our weekly trend-following model classifies the current market price position as: Weak Uptrend.

WTI Crude Oil Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

14.2

41.8

3.3

– Percent of Open Interest Shorts:

9.1

47.7

2.5

– Net Position:

98,709

-114,749

16,040

– Gross Longs:

278,276

820,579

64,779

– Gross Shorts:

179,567

935,328

48,739

– Long to Short Ratio:

1.5 to 1

0.9 to 1

1.3 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

6.3

95.5

34.1

– Strength Index Reading (3 Year Range):

Bearish-Extreme

Bullish-Extreme

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-16.1

19.9

-26.2

Brent Crude Oil Futures:

The Brent Crude Oil Futures large speculator standing this week came in at a net position of -24,699 contracts in the data reported through Tuesday. This was a weekly rise of 1,496 contracts from the previous week which had a total of -26,195 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 45.9 percent. The commercials are Bullish with a score of 54.4 percent and the small traders (not shown in chart) are Bullish with a score of 54.7 percent.

Price Trend-Following Model: Weak Uptrend

Our weekly trend-following model classifies the current market price position as: Weak Uptrend.

Brent Crude Oil Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

19.8

43.2

4.1

– Percent of Open Interest Shorts:

31.8

32.0

3.3

– Net Position:

-24,699

23,024

1,675

– Gross Longs:

40,627

88,732

8,347

– Gross Shorts:

65,326

65,708

6,672

– Long to Short Ratio:

0.6 to 1

1.4 to 1

1.3 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

45.9

54.4

54.7

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-3.6

3.5

3.3

Natural Gas Futures:

The Natural Gas Futures large speculator standing this week came in at a net position of -110,944 contracts in the data reported through Tuesday. This was a weekly fall of -16,397 contracts from the previous week which had a total of -94,547 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 53.7 percent. The commercials are Bullish with a score of 54.8 percent and the small traders (not shown in chart) are Bearish-Extreme with a score of 19.4 percent.

Price Trend-Following Model: Downtrend

Our weekly trend-following model classifies the current market price position as: Downtrend.

Natural Gas Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

17.3

31.8

3.2

– Percent of Open Interest Shorts:

24.1

25.4

2.8

– Net Position:

-110,944

104,419

6,525

– Gross Longs:

283,441

520,328

52,273

– Gross Shorts:

394,385

415,909

45,748

– Long to Short Ratio:

0.7 to 1

1.3 to 1

1.1 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

53.7

54.8

19.4

– Strength Index Reading (3 Year Range):

Bullish

Bullish

Bearish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-13.2

22.3

-29.1

Gasoline Blendstock Futures:

The Gasoline Blendstock Futures large speculator standing this week came in at a net position of 43,659 contracts in the data reported through Tuesday. This was a weekly boost of 2,538 contracts from the previous week which had a total of 41,121 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 44.5 percent. The commercials are Bearish with a score of 49.3 percent and the small traders (not shown in chart) are Bullish-Extreme with a score of 86.2 percent.

Price Trend-Following Model: Uptrend

Our weekly trend-following model classifies the current market price position as: Uptrend.

Nasdaq Mini Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

23.3

49.5

7.3

– Percent of Open Interest Shorts:

11.5

64.3

4.3

– Net Position:

43,659

-54,863

11,204

– Gross Longs:

86,260

183,418

27,051

– Gross Shorts:

42,601

238,281

15,847

– Long to Short Ratio:

2.0 to 1

0.8 to 1

1.7 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

44.5

49.3

86.2

– Strength Index Reading (3 Year Range):

Bearish

Bearish

Bullish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

13.2

-17.7

31.1

#2 Heating Oil NY-Harbor Futures:

The #2 Heating Oil NY-Harbor Futures large speculator standing this week came in at a net position of 18,983 contracts in the data reported through Tuesday. This was a weekly fall of -474 contracts from the previous week which had a total of 19,457 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 68.5 percent. The commercials are Bearish with a score of 23.0 percent and the small traders (not shown in chart) are Bullish-Extreme with a score of 94.6 percent.

Price Trend-Following Model: Uptrend

Our weekly trend-following model classifies the current market price position as: Uptrend.

Heating Oil Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

14.3

44.5

14.1

– Percent of Open Interest Shorts:

9.5

56.1

7.4

– Net Position:

18,983

-45,749

26,766

– Gross Longs:

56,751

176,526

56,062

– Gross Shorts:

37,768

222,275

29,296

– Long to Short Ratio:

1.5 to 1

0.8 to 1

1.9 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

68.5

23.0

94.6

– Strength Index Reading (3 Year Range):

Bullish

Bearish

Bullish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

0.9

-8.2

22.2

Bloomberg Commodity Index Futures:

The Bloomberg Commodity Index Futures large speculator standing this week came in at a net position of -13,749 contracts in the data reported through Tuesday. This was a weekly advance of 30 contracts from the previous week which had a total of -13,779 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 44.8 percent. The commercials are Bullish with a score of 54.8 percent and the small traders (not shown in chart) are Bullish with a score of 64.2 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

Bloomberg Index Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

15.2

73.2

3.8

– Percent of Open Interest Shorts:

21.3

67.1

3.7

– Net Position:

-13,749

13,449

300

– Gross Longs:

33,754

162,851

8,485

– Gross Shorts:

47,503

149,402

8,185

– Long to Short Ratio:

0.7 to 1

1.1 to 1

1.0 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

44.8

54.8

64.2

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-9.8

9.5

1.4

Article By InvestMacro – Receive our weekly COT Newsletter

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators) as well as their open interest (contracts open in the market at time of reporting). See CFTC criteria here.

Here are the latest charts and statistics for the Commitment of Traders (COT) data published by the Commodities Futures Trading Commission (CFTC).

The latest COT data is updated through Tuesday September 9th and shows a quick view of how large traders (for-profit speculators and commercial entities) were positioned in the futures markets.

Weekly Speculator Changes led by Natural Gas & Brent Oil

The COT energy market speculator bets were overall lower this week as just two out of the six energy markets we cover had higher positioning while the other four markets had lower speculator contracts.

Leading the gains for the energy markets was Natural Gas (8,229 contracts) with Brent Oil (2,447 contracts) also having a positive week.

The markets with declines in speculator bets for the week were WTI Crude (-20,584 contracts), Heating Oil (-10,789 contracts), the Bloomberg Index (-522 contracts) and Gasoline (-185 contracts) also seeing lower bets on the week.

Brent Crude Oil Leads Weekly Price Performance

Brent Oil led the energy markets in price gains this week with a 1.83% rise for the last five days. Brent Crude has been down by over -5% in the last 30 days, but is up by 18% over the past 90 days.

The Bloomberg Commodity Index was the next highest gainer with a 1.4% increase over the past five days. Heating Oil rose by 1.33% this week and has been up by almost 20% over the last 90 days.

WTI Crude Oil rose by 0.97%. WTI has been down by about -8% over the past 30 days, while also being higher by 17.58% over the past 90 days. Gasoline was the next highest mover with a 0.92% increase for the week.

Natural Gas was the only decliner on the week with a -3.25% decrease. Natural Gas has been down by approximately -8% over the past 30 days, and over the past 90 days, Natural Gas has been down by over -30%.

Energy Data:

Legend: Weekly Speculators Change | Speculators Current Net Position | Speculators Strength Score compared to last 3-Years (0-100 range)

Strength Scores led by Heating Oil & Natural Gas

COT Strength Scores (a normalized measure of Speculator positions over a 3-Year range, from 0 to 100 where above 80 is Extreme-Bullish and below 20 is Extreme-Bearish) showed that Heating Oil (69 percent) and Natural Gas (66 percent) lead the energy markets this week.

On the downside, WTI Crude (0 percent) comes in at the lowest strength level currently and is in Extreme-Bearish territory (below 20 percent).

Strength Statistics: WTI Crude Oil (0.0 percent) vs WTI Crude Oil previous week (7.7 percent) Brent Crude Oil (43.8 percent) vs Brent Crude Oil previous week (40.3 percent) Natural Gas (66.3 percent) vs Natural Gas previous week (60.0 percent) Gasoline (40.9 percent) vs Gasoline previous week (41.2 percent) Heating Oil (69.1 percent) vs Heating Oil previous week (83.3 percent) Bloomberg Commodity Index (44.7 percent) vs Bloomberg Commodity Index previous week (47.0 percent)

Gasoline & Brent Oil top the 6-Week Strength Trends

COT Strength Score Trends (or move index, calculates the 6-week changes in strength scores) showed that all the energy markets have negative trend scores at the current time.

Gasoline (-1.7 percent) and Brent Oil (-5.8 percent) have the least negative scores while WTI Crude (-27.7 percent) and the Bloomberg Index (-10.4 percent) have the most negative scores in the latest trends data.

Move Statistics: WTI Crude Oil (-27.7 percent) vs WTI Crude Oil previous week (-19.0 percent) Brent Crude Oil (-5.8 percent) vs Brent Crude Oil previous week (-16.8 percent) Natural Gas (-6.8 percent) vs Natural Gas previous week (-19.3 percent) Gasoline (-1.7 percent) vs Gasoline previous week (9.2 percent) Heating Oil (-6.7 percent) vs Heating Oil previous week (11.6 percent) Bloomberg Commodity Index (-10.4 percent) vs Bloomberg Commodity Index previous week (-8.2 percent)

Individual COT Market Charts:

WTI Crude Oil Futures:

The WTI Crude Oil Futures large speculator standing this week equaled a net position of 81,844 contracts in the data reported through Tuesday. This was a weekly reduction of -20,584 contracts from the previous week which had a total of 102,428 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 0.0 percent. The commercials are Bullish-Extreme with a score of 100.0 percent and the small traders (not shown in chart) are Bearish with a score of 42.9 percent.

Price Trend-Following Model: Uptrend

Our weekly trend-following model classifies the current market price position as: Uptrend.

WTI Crude Oil Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

14.0

41.8

3.5

– Percent of Open Interest Shorts:

9.8

47.1

2.5

– Net Position:

81,844

-102,155

20,311

– Gross Longs:

274,256

818,832

69,296

– Gross Shorts:

192,412

920,987

48,985

– Long to Short Ratio:

1.4 to 1

0.9 to 1

1.4 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

0.0

100.0

42.9

– Strength Index Reading (3 Year Range):

Bearish-Extreme

Bullish-Extreme

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-27.7

27.7

-6.7

Brent Crude Oil Futures:

The Brent Crude Oil Futures large speculator standing this week equaled a net position of -26,195 contracts in the data reported through Tuesday. This was a weekly boost of 2,447 contracts from the previous week which had a total of -28,642 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 43.8 percent. The commercials are Bullish with a score of 58.0 percent and the small traders (not shown in chart) are Bearish with a score of 45.1 percent.

Price Trend-Following Model: Uptrend

Our weekly trend-following model classifies the current market price position as: Uptrend.

Brent Crude Oil Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

18.1

44.5

3.5

– Percent of Open Interest Shorts:

30.7

32.3

3.0

– Net Position:

-26,195

25,347

848

– Gross Longs:

37,678

92,625

7,193

– Gross Shorts:

63,873

67,278

6,345

– Long to Short Ratio:

0.6 to 1

1.4 to 1

1.1 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

43.8

58.0

45.1

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-5.8

5.3

7.0

Natural Gas Futures:

The Natural Gas Futures large speculator standing this week equaled a net position of -94,547 contracts in the data reported through Tuesday. This was a weekly lift of 8,229 contracts from the previous week which had a total of -102,776 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 66.3 percent. The commercials are Bearish with a score of 38.5 percent and the small traders (not shown in chart) are Bearish with a score of 31.1 percent.

Price Trend-Following Model: Downtrend

Our weekly trend-following model classifies the current market price position as: Downtrend.

Natural Gas Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

17.4

30.8

3.5

– Percent of Open Interest Shorts:

23.1

25.7

2.8

– Net Position:

-94,547

83,316

11,231

– Gross Longs:

282,995

502,932

56,670

– Gross Shorts:

377,542

419,616

45,439

– Long to Short Ratio:

0.7 to 1

1.2 to 1

1.2 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

66.3

38.5

31.1

– Strength Index Reading (3 Year Range):

Bullish

Bearish

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-6.8

11.8

-16.3

Gasoline Blendstock Futures:

The Gasoline Blendstock Futures large speculator standing this week equaled a net position of 41,121 contracts in the data reported through Tuesday. This was a weekly fall of -185 contracts from the previous week which had a total of 41,306 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 40.9 percent. The commercials are Bullish with a score of 52.2 percent and the small traders (not shown in chart) are Bullish-Extreme with a score of 86.7 percent.

Price Trend-Following Model: Uptrend

Our weekly trend-following model classifies the current market price position as: Uptrend.

Nasdaq Mini Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

23.9

48.7

7.9

– Percent of Open Interest Shorts:

11.8

64.1

4.6

– Net Position:

41,121

-52,405

11,284

– Gross Longs:

81,040

164,911

26,762

– Gross Shorts:

39,919

217,316

15,478

– Long to Short Ratio:

2.0 to 1

0.8 to 1

1.7 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

40.9

52.2

86.7

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bullish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-1.7

-5.2

32.5

#2 Heating Oil NY-Harbor Futures:

The #2 Heating Oil NY-Harbor Futures large speculator standing this week equaled a net position of 19,457 contracts in the data reported through Tuesday. This was a weekly fall of -10,789 contracts from the previous week which had a total of 30,246 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 69.1 percent. The commercials are Bearish with a score of 23.5 percent and the small traders (not shown in chart) are Bullish-Extreme with a score of 91.9 percent.

Price Trend-Following Model: Uptrend

Our weekly trend-following model classifies the current market price position as: Uptrend.

Heating Oil Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

14.8

43.9

13.9

– Percent of Open Interest Shorts:

9.7

55.7

7.2

– Net Position:

19,457

-45,269

25,812

– Gross Longs:

56,751

168,677

53,529

– Gross Shorts:

37,294

213,946

27,717

– Long to Short Ratio:

1.5 to 1

0.8 to 1

1.9 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

69.1

23.5

91.9

– Strength Index Reading (3 Year Range):

Bullish

Bearish

Bullish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-6.7

5.6

-2.3

Bloomberg Commodity Index Futures:

The Bloomberg Commodity Index Futures large speculator standing this week equaled a net position of -13,779 contracts in the data reported through Tuesday. This was a weekly reduction of -522 contracts from the previous week which had a total of -13,257 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 44.7 percent. The commercials are Bullish with a score of 54.9 percent and the small traders (not shown in chart) are Bullish with a score of 64.5 percent.

Price Trend-Following Model: Strong Uptrend

Our weekly trend-following model classifies the current market price position as: Strong Uptrend.

Bloomberg Index Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

16.9

80.8

0.2

– Percent of Open Interest Shorts:

23.7

74.1

0.1

– Net Position:

-13,779

13,468

311

– Gross Longs:

33,670

161,484

425

– Gross Shorts:

47,449

148,016

114

– Long to Short Ratio:

0.7 to 1

1.1 to 1

3.7 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

44.7

54.9

64.5

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-10.4

10.3

0.8

Article By InvestMacro – Receive our weekly COT Newsletter

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators) as well as their open interest (contracts open in the market at time of reporting). See CFTC criteria here.

Artificial intelligence is growing fast, and so are the number of computers that power it. Behind the scenes, this rapid growth is putting a huge strain on the data centers that run AI models. These facilities are using more energy than ever.

AI models are getting larger and more complex. Today’s most advanced systems have billions of parameters, the numerical values derived from training data, and run across thousands of computer chips. To keep up, companies have responded by adding more hardware, more chips, more memory and more powerful networks. This brute force approach has helped AI make big leaps, but it’s also created a new challenge: Data centers are becoming energy-hungry giants.

I’m a computer engineer and a professor at Georgia Tech who specializes in high-performance computing. I see another path to curbing AI’s energy appetite: Make data centers more resource aware and efficient.

Energy and heat

Modern AI data centers can use as much electricity as a small city. And it’s not just the computing that eats up power. Memory and cooling systems are major contributors, too. As AI models grow, they need more storage and faster access to data, which generates more heat. Also, as the chips become more powerful, removing heat becomes a central challenge.

Cooling isn’t just a technical detail; it’s a major part of the energy bill. Traditional cooling is done with specialized air conditioning systems that remove heat from server racks. New methods like liquid cooling are helping, but they also require careful planning and water management. Without smarter solutions, the energy requirements and costs of AI could become unsustainable.

Even with all this advanced equipment, many data centers aren’t running efficiently. That’s because different parts of the system don’t always talk to each other. For example, scheduling software might not know that a chip is overheating or that a network connection is clogged. As a result, some servers sit idle while others struggle to keep up. This lack of coordination can lead to wasted energy and underused resources.

A smarter way forward

Addressing this challenge requires rethinking how to design and manage the systems that support AI. That means moving away from brute-force scaling and toward smarter, more specialized infrastructure.

Here are three key ideas:

Address variability in hardware. Not all chips are the same. Even within the same generation, chips vary in how fast they operate and how much heat they can tolerate, leading to heterogeneity in both performance and energy efficiency. Computer systems in data centers should recognize differences among chips in performance, heat tolerance and energy use, and adjust accordingly.

Adapt to changing conditions. AI workloads vary over time. For instance, thermal hotspots on chips can trigger the chips to slow down, fluctuating grid supply can cap the peak power that centers can draw, and bursts of data between chips can create congestion in the network that connects them. Systems should be designed to respond in real time to things like temperature, power availability and data traffic.

How data center cooling works.

Break down silos. Engineers who design chips, software and data centers should work together. When these teams collaborate, they can find new ways to save energy and improve performance. To that end, my colleagues, students and I at Georgia Tech’s AI Makerspace, a high-performance AI data center, are exploring these challenges hands-on. We’re working across disciplines, from hardware to software to energy systems, to build and test AI systems that are efficient, scalable and sustainable.

Scaling with intelligence

AI has the potential to transform science, medicine, education and more, but risks hitting limits on performance, energy and cost. The future of AI depends not only on better models, but also on better infrastructure.

To keep AI growing in a way that benefits society, I believe it’s important to shift from scaling by force to scaling with intelligence.

In 2025, 1 in 4 new automotive vehicle sales globally are expected to be an electric vehicle – either fully electric or a plug-in hybrid.

That is a significant rise from just five years ago, when EV sales amounted to fewer than 1 in 20 new car sales, according to the International Energy Agency, an intergovernmental organization examining energy use around the world.

The International Energy Agency has reported that two-thirds of fully electric cars in China are now cheaper to buy than their gasoline equivalents. With operating and maintenance costs already cheaper than gasoline models, EVs are attractive purchases.

Most EVs purchased in China are made there as well, by a range of different companies. NIO, Xpeng, Xiaomi, Zeekr, Geely, Chery, Great Wall Motor, Leapmotor and especially BYD are household names in China. As someone who has followed and published on the topic of EVs for over 15 years, I expect they will soon become as widely known in the rest of the world.

What kinds of EVs is China producing?

China’s automakers are producing a full range of electric vehicles, from the subcompact, like the BYD Seagull, to full-size SUVs, like the Xpeng G9, and luxury cars, like the Zeekr 009.

A Wall Street Journal video explores a Chinese ‘dark factory’ – one so automated that it doesn’t need lights inside.

What’s behind Chinese EV success?

There are several factors behind Chinese companies’ success in producing and selling EVs. To be sure, relatively low labor costs are part of the explanation. So are generous government subsidies, as EVs were one of several advanced technologies selected by the Chinese government to propel the nation’s global technological profile.

But Chinese EV makers are also making other advances. They make significant use of industrial robotics, even to the point of building so-called “dark factories” that can operate with minimal human intervention. For passengers, they have reimagined vehicles’ interiors, with large touchscreens for information and entertainment, and even added a refrigerator, bed or karaoke system.

Competition among Chinese EV makers is fierce, which drives additional innovation. BYD is the largest seller of EVs, both domestically and globally. Yet the company says it employs over 100,000 scientists and engineers seeking continual improvement.

From initial concept models to actual rollout of factory-made cars, BYD takes 18 months – half as long as U.S. and other global automakers take for their product development processes, Reuters reported.

The real test of how well Chinese vehicles appeal to consumers will come from export sales. Chinese EV manufacturers are eager to sell abroad because their factories can produce far more than the 25 million vehicles they can sell within China each year – perhaps twice as much.

The largest market where Chinese vehicles, whether gasoline or electric, are not being sold is North America. Both the U.S. and Canadian governments have created what some have called a “tariff fortress” protecting their domestic automakers, by imposing tariffs of 100% on the import of Chinese EVs – literally doubling their cost to consumers.

Customers’ budgets matter too. The average price of a new electric vehicle in the U.S. is approximately $55,000. Less expensive vehicles make up part of this average, but without tax credits, which the Trump administration is eliminating after September 2025, nothing gets close to $25,000. By contrast, Chinese companies produce several sub-$25,000 EVs, including the Xpeng M03, the BYD Dolphin and the MG4 without tax credits. If sold in America, however, the 100% tariffs would remove the price advantage.

Tesla, Ford and General Motors all claim they are working on inexpensive EVs. More expensive vehicles, however, generate higher profits, and with the protection of the “tariff fortress,” their incentive to develop cheaper EVs is not as high as it might be.

In the 1970s and 1980s, there was considerable U.S. opposition to importing Japanese vehicles. But ultimately, a combination of consumer sentiment and the willingness of Japanese companies to open factories in the U.S. overcame that opposition, and Japanese brands like Toyota, Honda and Nissan are common on North American roads. The same process may play out for Chinese automakers, though it’s not clear how long that might take.

Here are the latest charts and statistics for the Commitment of Traders (COT) data published by the Commodities Futures Trading Commission (CFTC).

The latest COT data is updated through Tuesday September 2nd and shows a quick view of how large traders (for-profit speculators and commercial entities) were positioned in the futures markets.

Weekly Speculator Changes led by Heating Oil & Brent Oil

The COT energy market speculator bets were overall higher this week as four out of the six energy markets we cover had higher positioning while the other two markets had lower speculator contracts.

Leading the gains for the energy markets was Heating Oil (6,479 contracts) with Brent Oil (6,278 contracts), Gasoline (1,964 contracts) and Natural Gas (1,170 contracts) also having positive weeks.

The markets with declines in speculator bets for the week were WTI Crude (-7,044 contracts) and the Bloomberg Index (-288 contracts) which saw lower bets on the week.

Natural Gas led Energy Price Performance

Energy market performance this week was led by Natural Gas, which saw a 2.94% gain on the week. Despite that, Natural Gas is down by -6.64% over the last 30 days and is lower by -22.14% over the last 90 days.

The Bloomberg Commodity Index was the next highest mover with a 0.64% gain on the week. Heating Oil also saw a tiny gain this week with a 0.04% increase. Heating Oil has been up by 13.75% over the last 90 days.

On the downside, Gasoline fell by -0.58% this week. Gasoline has been higher by 3.44% over the last 30 days and up by 7.92% over the last 90 days. Brent Oil fell by -2.92% over the last five days. Brent Oil has been higher by almost 8% over the last 90 days.

And finally, WTI Crude Oil was down by -3.47% this week, but has been up by 7.19% over the last 90 days.

Energy Data:

Legend: Weekly Speculators Change | Speculators Current Net Position | Speculators Strength Score compared to last 3-Years (0-100 range)

Strength Scores led by Heating Oil & Natural Gas

COT Strength Scores (a normalized measure of Speculator positions over a 3-Year range, from 0 to 100 where above 80 is Extreme-Bullish and below 20 is Extreme-Bearish) showed that Heating Oil (83 percent) and Natural Gas (60 percent) lead the energy markets this week.

On the downside, WTI Crude (0 percent) comes in at the lowest strength level currently and is in Extreme-Bearish territory (below 20 percent).

Strength Statistics: WTI Crude Oil (0.0 percent) vs WTI Crude Oil previous week (2.8 percent) Brent Crude Oil (40.3 percent) vs Brent Crude Oil previous week (31.4 percent) Natural Gas (60.0 percent) vs Natural Gas previous week (59.1 percent) Gasoline (41.2 percent) vs Gasoline previous week (38.5 percent) Heating Oil (83.3 percent) vs Heating Oil previous week (74.8 percent) Bloomberg Commodity Index (47.0 percent) vs Bloomberg Commodity Index previous week (48.3 percent)

Heating Oil & Gasoline top the 6-Week Strength Trends

COT Strength Score Trends (or move index, calculates the 6-week changes in strength scores) showed that Heating Oil (12 percent) and Gasoline (9 percent) lead the past six weeks trends for the energy markets.

WTI Crude Oil (-21 percent), Natural Gas (-19 percent) and Brent Oil (-17 percent) leads the downside trend scores currently.

Move Statistics: WTI Crude Oil (-20.6 percent) vs WTI Crude Oil previous week (-21.4 percent) Brent Crude Oil (-16.8 percent) vs Brent Crude Oil previous week (-38.6 percent) Natural Gas (-19.3 percent) vs Natural Gas previous week (-23.0 percent) Gasoline (9.2 percent) vs Gasoline previous week (-6.9 percent) Heating Oil (11.6 percent) vs Heating Oil previous week (3.1 percent) Bloomberg Commodity Index (-8.2 percent) vs Bloomberg Commodity Index previous week (-6.4 percent)

Individual COT Market Charts:

WTI Crude Oil Futures:

WTI Crude vs Oil ETF

The WTI Crude Oil Futures large speculator standing this week was a net position of 102,428 contracts in the data reported through Tuesday. This was a weekly decrease of -7,044 contracts from the previous week which had a total of 109,472 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish-Extreme with a score of 0.0 percent. The commercials are Bullish-Extreme with a score of 100.0 percent and the small traders (not shown in chart) are Bearish with a score of 40.2 percent.

Price Trend-Following Model: Weak Uptrend

Our weekly trend-following model classifies the current market price position as: Weak Uptrend.

WTI Crude Oil Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

14.7

41.2

3.4

– Percent of Open Interest Shorts:

9.6

47.3

2.5

– Net Position:

102,428

-121,395

18,967

– Gross Longs:

293,055

819,102

67,712

– Gross Shorts:

190,627

940,497

48,745

– Long to Short Ratio:

1.5 to 1

0.9 to 1

1.4 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

0.0

100.0

40.2

– Strength Index Reading (3 Year Range):

Bearish-Extreme

Bullish-Extreme

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-20.6

23.2

-19.8

Brent Crude Oil Futures:

Brent vs Oil ETF

The Brent Crude Oil Futures large speculator standing this week was a net position of -28,642 contracts in the data reported through Tuesday. This was a weekly boost of 6,278 contracts from the previous week which had a total of -34,920 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 40.3 percent. The commercials are Bullish with a score of 62.5 percent and the small traders (not shown in chart) are Bearish with a score of 39.2 percent.

Price Trend-Following Model: Uptrend

Our weekly trend-following model classifies the current market price position as: Uptrend.

Brent Crude Oil Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

19.0

45.6

3.4

– Percent of Open Interest Shorts:

33.1

31.6

3.2

– Net Position:

-28,642

28,295

347

– Gross Longs:

38,506

92,395

6,853

– Gross Shorts:

67,148

64,100

6,506

– Long to Short Ratio:

0.6 to 1

1.4 to 1

1.1 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

40.3

62.5

39.2

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-16.8

18.6

-4.4

Natural Gas Futures:

Natural Gas vs ETF

The Natural Gas Futures large speculator standing this week was a net position of -102,776 contracts in the data reported through Tuesday. This was a weekly rise of 1,170 contracts from the previous week which had a total of -103,946 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish with a score of 60.0 percent. The commercials are Bearish with a score of 43.1 percent and the small traders (not shown in chart) are Bearish with a score of 37.0 percent.

Price Trend-Following Model: Downtrend

Our weekly trend-following model classifies the current market price position as: Downtrend.

Natural Gas Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

17.4

30.9

3.4

– Percent of Open Interest Shorts:

23.7

25.4

2.5

– Net Position:

-102,776

89,212

13,564

– Gross Longs:

284,272

504,792

55,175

– Gross Shorts:

387,048

415,580

41,611

– Long to Short Ratio:

0.7 to 1

1.2 to 1

1.3 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

60.0

43.1

37.0

– Strength Index Reading (3 Year Range):

Bullish

Bearish

Bearish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-19.3

23.5

-13.1

Gasoline Blendstock Futures:

Gasoline vs ETF

The Gasoline Blendstock Futures large speculator standing this week was a net position of 41,306 contracts in the data reported through Tuesday. This was a weekly lift of 1,964 contracts from the previous week which had a total of 39,342 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 41.2 percent. The commercials are Bullish with a score of 56.3 percent and the small traders (not shown in chart) are Bullish with a score of 66.0 percent.

Price Trend-Following Model: Uptrend

Our weekly trend-following model classifies the current market price position as: Uptrend.

Nasdaq Mini Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

26.1

49.1

7.5

– Percent of Open Interest Shorts:

13.2

64.4

5.1

– Net Position:

41,306

-48,980

7,674

– Gross Longs:

83,524

157,003

24,129

– Gross Shorts:

42,218

205,983

16,455

– Long to Short Ratio:

2.0 to 1

0.8 to 1

1.5 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

41.2

56.3

66.0

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

9.2

-10.7

13.9

#2 Heating Oil NY-Harbor Futures:

Heating Oil vs ETF

The #2 Heating Oil NY-Harbor Futures large speculator standing this week was a net position of 30,246 contracts in the data reported through Tuesday. This was a weekly boost of 6,479 contracts from the previous week which had a total of 23,767 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bullish-Extreme with a score of 83.3 percent. The commercials are Bearish-Extreme with a score of 15.6 percent and the small traders (not shown in chart) are Bullish-Extreme with a score of 84.7 percent.

Price Trend-Following Model: Uptrend

Our weekly trend-following model classifies the current market price position as: Uptrend.

Heating Oil Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

17.7

40.9

14.0

– Percent of Open Interest Shorts:

9.4

55.5

7.6

– Net Position:

30,246

-53,510

23,264

– Gross Longs:

64,603

149,076

51,122

– Gross Shorts:

34,357

202,586

27,858

– Long to Short Ratio:

1.9 to 1

0.7 to 1

1.8 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

83.3

15.6

84.7

– Strength Index Reading (3 Year Range):

Bullish-Extreme

Bearish-Extreme

Bullish-Extreme

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

11.6

-5.6

-8.3

Bloomberg Commodity Index Futures:

Bloomberg Commodity Index vs ETF

The Bloomberg Commodity Index Futures large speculator standing this week was a net position of -13,257 contracts in the data reported through Tuesday. This was a weekly decline of -288 contracts from the previous week which had a total of -12,969 net contracts.

This week’s current strength score (the trader positioning range over the past three years, measured from 0 to 100) shows the speculators are currently Bearish with a score of 47.0 percent. The commercials are Bullish with a score of 52.7 percent and the small traders (not shown in chart) are Bullish with a score of 64.0 percent.

Price Trend-Following Model: Uptrend

Our weekly trend-following model classifies the current market price position as: Uptrend.

Bloomberg Index Futures Statistics

SPECULATORS

COMMERCIALS

SMALL TRADERS

– Percent of Open Interest Longs:

13.6

81.7

0.2

– Percent of Open Interest Shorts:

20.3

75.1

0.1

– Net Position:

-13,257

12,966

291

– Gross Longs:

26,750

160,982

406

– Gross Shorts:

40,007

148,016

115

– Long to Short Ratio:

0.7 to 1

1.1 to 1

3.5 to 1

NET POSITION TREND:

– Strength Index Score (3 Year Range Pct):

47.0

52.7

64.0

– Strength Index Reading (3 Year Range):

Bearish

Bullish

Bullish

NET POSITION MOVEMENT INDEX:

– 6-Week Change in Strength Index:

-8.2

8.1

0.5

Article By InvestMacro – Receive our weekly COT Newsletter

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators) as well as their open interest (contracts open in the market at time of reporting). See CFTC criteria here.

Stephen McBride of The Rational Optimist shares his thoughts on how nuclear energy can be reshaped.

A tiny uranium pellet the size of a gummy bear holds energy matching 140 oil barrels. It’s humanity’s most environmentally friendly, secure power resource.

Every legitimate expert acknowledges this fact.

So what’s preventing universal nuclear implementation?

In brief: We smothered brilliance with bureaucracy. Since the 70s, constructing new facilities has practically been prohibited in America. It demanded $30 billion plus 15+ years battling regulatory obstacles.

I’ve got exciting updates. During my recent visits to Austin and Detroit, I connected with top-tier nuclear innovators. I’ve known these innovators for some time and consider many friends. They unanimously shared something unprecedented:

“Regulation is finally becoming a solved problem.”

One entrepreneur mentioned his microreactor (a small nuclear reactor or “SMR”) could become operational within a year.

This represents massive progress! We’re developing an extensive analysis about SMRs and approximately twelve startups racing to launch one. More information coming soon.

Today, let’s examine remaining nuclear “challenges.” What about waste management? And fuel acquisition? We’ll explore entrepreneurs tackling both issues.

First, a quick overview of major regulatory shifts.

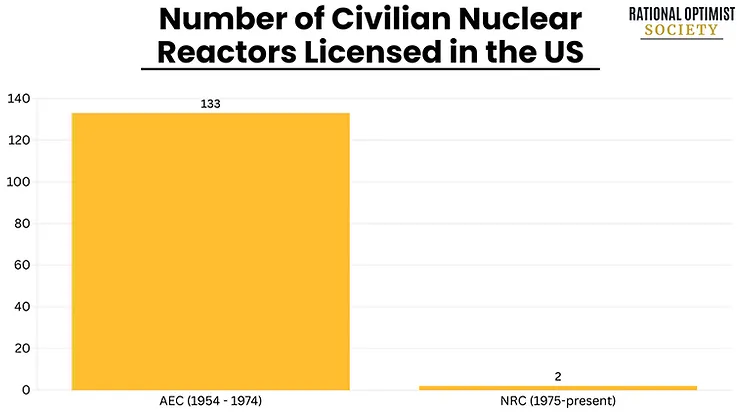

In 1974, a bureaucratic entity called the Nuclear Regulatory Commission (NRC) emerged. Guess how many innovative reactor designs it’s approved since inception?

None!

Just two reactors have begun commercial operations during the NRC’s existence, compared to 133 beforehand.

We’re finally addressing this imbalance. The President has authorized four executive directives to accelerate nuclear development. These orders initiate five significant changes:

Change 1: They establish a target of expanding America’s nuclear capacity fourfold by 2050.

Change 2: They accelerate “advanced nuclear” development (specifically small modular reactors or “SMRs”) through test programs and expedited environmental assessments. They mandate the NRC to authorize new reactors within 18 months.

Change 3: They instruct the Department of Energy (DoE) to sanction at least three reactors before mid-2026. Essentially, Trump wants three SMRs functioning for America’s 250th anniversary.

Change 4: They classify nuclear facilities powering AI operations as “defense-critical infrastructure.” Constructing nuclear-powered computing centers on military installations creates a brilliant workaround. It potentially enables projects to bypass lengthy NRC evaluations.

Change 5: Most crucially in my assessment: They request the NRC to reconsider its “As Low as Reasonably Achievable” (ALARA) regulation. You experience more radiation consuming a single banana than living beside a nuclear plant for twelve months. Yet under ALARA guidelines, even that isn’t considered sufficiently safe!

This “zero banana rule” has effectively prohibited nuclear construction in America. I believe the President should have commanded the NRC to eliminate this rule completely. Nevertheless, this represents advancement.

Nuclear entrepreneurs have anticipated this opportunity throughout their careers.

As Matt Loszak, founder of Aalo Atomics said, “We just have to wait for the executive orders to be implemented and we’re off to the races.”

In Detroit, Valar Atomics founder Isaiah Taylor said. . .

“The problem is no longer in the policy side. It’s now in the engineering side.”

One engineering challenge involves fuel acquisition.

Stephen with Valar Atomics founder Isaiah Taylor

Fuel access concerned many entrepreneurs I encountered. Even if prepared to activate their microreactors immediately, many would face obstacles. They lack necessary fuel.

Converting uranium from extraction to reactor-ready involves four fundamental stages:

Mining. Organizations like Cameco Corp. (CCO:TSX; CCJ:NYSE) (Canada) mine uranium in locations including Canada, Kazakhstan, Australia, Namibia, Niger, and Russia. These six nations produce over 85% of global uranium. Raw materials undergo processing into a substance called yellowcake.

Conversion. Yellowcake undergoes milling and conversion into uranium hexafluoride (UF6) enabling gasification for enrichment. Orano (France) and Rosatom (Russia) dominate over 50% of this market.

Enrichment. Nuclear “gas” undergoes enrichment through centrifugal spinning. Three corporations, Urenco (European consortium), Orano, and Rosatom control the enrichment market.

Fuel creation. Companies including Westinghouse (U.S.) and Framatome (France) compress and heat enriched uranium powder into solid ceramic pieces.

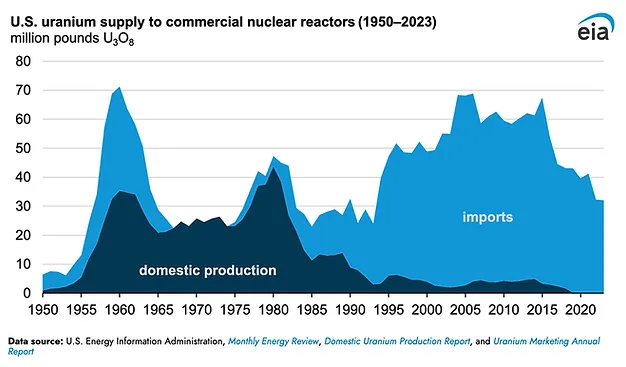

America possesses abundant underground uranium reserves. However, excessive regulation has minimized processing capabilities.

By 2023, 99% of fuel utilized in U.S. reactors was imported— with substantial quantities from Russia.

Meet innovators addressing this crisis . . .

Scott Nolan, partner at Peter Thiel’s investment firm Founders Fund, was among earliest backers of Radiant Nuclear, a venture developing portable microreactors. But Radiant encountered a major obstacle: fuel scarcity.

Specifically, limited access to high-assay low-enriched uranium (HALEU), premium uranium ideal for powering most microreactors.

Only Russia and China manufacture HALEU at scale. However, the U.S. plans to prohibit Russian uranium imports starting 2028. Leaving China — an unpredictable trade partner.

Accessing HALEU in America resembles Soviet-era bread queues. The DoE maintains limited reserves. Entrepreneurs must complete paperwork, endure months-long waits, and hope for allocations – merely to test prototypes. “Please sir, can I have some more?”

Scott Nolan established General Matter to produce HALEU fuel and revitalize America’s enrichment industry.

Meeting Scott at Detroit’s Reindustrialize summit, he shared “I spent over a year at Founders Fund searching for an American enrichment company to invest in, only to find there wasn’t one. So, we built our own.”

General Matter assembled elite professionals from organizations including SpaceX, Tesla, Anduril, and several American national nuclear laboratories. It was among four companies selected by the DoE to initiate American HALEU production.

If General Matter succeeds, it will achieve for uranium enrichment what SpaceX accomplished for rocketry: restore American competitiveness.

J.D. Rockefeller amassed historic wealth through Standard Oil.

Not through oil drilling. But by controlling the supply chain’s most valuable component: crude refinement.

Standard Nuclear aims to replicate this for nuclear energy. Its mission: become a scalable, affordable, entirely American nuclear fuel provider — the nuclear industry’s Standard Oil.

HALEU, optimal fuel for next-generation reactors, often comes encased in ceramic protection called TRISO, maintaining fuel density and safety.

TRISO appears as indestructible billiard ball-sized spheres. Each contains sufficient energy to power thousands of households.

Source: Kairos Power

TRISO resists melting. It prevents leakage. It contains radioactivity internally, even during extreme accidents. That’s why the DoE designates it Earth’s most robust nuclear fuel. Even the NRC acknowledges it as ‘functional containment.’

One entrepreneur described TRISO’s remarkable properties: “You know those giant concrete containment domes that surround old reactors in case something goes wrong? With TRISO, we’ve basically engineered the dome into every single fuel particle.”

TRISO provides microreactors with clean, compact, uninterrupted power, eliminating meltdown risks and massive containment structures.

China recently conducted safety testing by deactivating a nuclear reactor’s cooling system. The TRISO-powered reactor absorbed heat. The core cooled naturally. No alternative nuclear fuel demonstrates this capability.

Predictably, China remains the sole nation producing significant TRISO quantities.

Standard Nuclear will help America catch up.

Standard Nuclear represents genuine innovation. The company emerged following another company’s bankruptcy after its primary investor died. The team was commercializing TRISO, previously produced exclusively in America’s national laboratories.

Following the investor’s death, their commitment remained so strong that over 40 employees continued working approximately eight months without compensation. Some sold homes or downsized to maintain operations.

Their perseverance succeeded. In 2024, the organization reemerged as Standard Nuclear with $42 million in funding.

Standard Nuclear operates from Oak Ridge, Tennessee, formerly known as “Atomic City,” where Manhattan Project uranium enrichment occurred. It currently represents the largest TRISO manufacturing facility outside China.

Standard Nuclear recently secured $5 million in contracts and established offtake agreements exceeding $100 million with microreactor ventures including Radiant, Antares, and

NANO Nuclear Energy Inc. (NNE:NASDAQ).

“ROS never addresses the problem of nuclear waste storage.”

ROS Member John D highlighted this omission. Let me correct this.

Imagining radioactive material seeping from corroded containers seems frightening. Reality shows nuclear waste represents a resolved challenge. Innovators are transforming it into another opportunity.

Fundamentals: All nuclear waste ever generated throughout America — spanning 60 years — would occupy a single football field, stacked under 20 feet high.

Atomic byproducts have never harmed any American. Spent materials remain securely stored in sealed containers across 60+ locations throughout 34 states.

Why merely store it? SMR startups are creating reactors utilizing waste.

Oklo Inc.’s (OKLO:NYSE) Aurora microreactor, compact enough for a spacious living room, converts used fuel into fresh energy. Like automobiles running on exhaust fumes!

The most frustrating aspect regarding nuclear waste “problems” involves ignoring existing solutions for 60 years. Argonne National Laboratory constructed reactors capable of recycling nuclear waste into fuel during the 1960s!

Why isn’t fuel recycling standard practice? Blame political decisions. President Carter suspended reprocessing during the 1970s. Reagan reversed the prohibition, but companies had already pivoted elsewhere.

Consider Deep Isolation. I recently spoke with CEO Rod Baltzer. His company developed a methodology for permanently securing nuclear waste underground, utilizing directional drilling technology and their Universal Canister System.

Deep Isolation drills tunnels approximately pizza-box width into solid rock formations, reaching three miles beneath surface level. The tunnel’s bottom curves, creating an L-shaped pathway. They then insert sealed, corrosion-resistant containers filled with nuclear waste, designed for millennial timeframes.

Deep Isolation ensures waste disappears safely, permanently, and economically.

The genuine threat isn’t nuclear waste. It’s unrealized nuclear facilities, leaving us dependent on dirtier energy alternatives. Innovators are transforming perceived problems into productive power solutions.

Envision July 4, 2026. . .

We’re celebrating America’s 250th anniversary. The initial three microreactors operate on American soil. These engineered marvels generate clean, safe, “constantly available” energy.

After meeting numerous nuclear entrepreneurs, I recognize their determination toward this objective. Teams sleep in production facilities. Engineers work 18-hour shifts. Founders dedicate their lives toward achieving that July 2026 milestone.

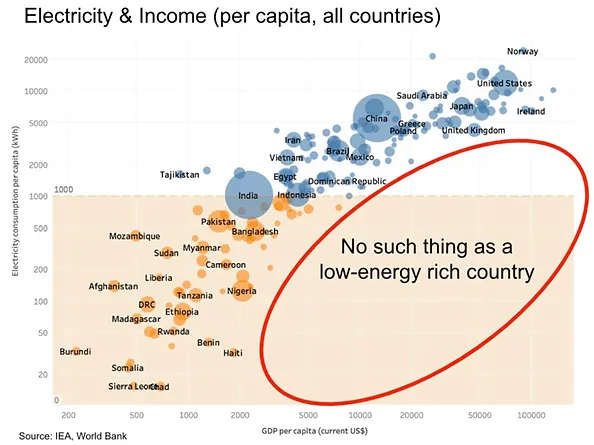

America’s prosperous future requires expanded energy access, not reduction. Remember: Rich, low-energy nations don’t exist.

In 1973 President Nixon proposed establishing 1,000 nuclear power plants before 2000. Better delayed than abandoned.

With 1,000 microreactors distributed across America, we could desalinate seawater and transform arid deserts into fertile land. Following hurricanes, mobile reactors could deploy, powering medical facilities and water systems within hours.

Building this future depends on communities nationwide embracing nuclear technology.

That’s where your role begins. Demonstrate to friends and relatives that nuclear represents our cleanest, safest energy resource. Challenge misinformed opposition.

Address questions resembling this inquiry: “What might terrorists accomplish capturing a microreactor?” Simple answer: they’d have years of clean energy, but concerns about weaponization are unfounded.

Perhaps most importantly, share nuclear innovation stories with younger generations! The Second Nuclear Age will create talent shortages. It requires engineers, technicians, machinists, and policy advocates.

The primary career aspiration among children today is… social media influencer. Disappointing. Let’s transform that to nuclear engineer!

At the Rational Optimist Society, we’re embracing nuclear technology and much more. We help our members understand, appreciate, and take advantage of the innovations revolutionizing our world for the better, so they can confidently flourish as change continues to accelerate.

As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Cameco Corp.

Stephen McBride: I, or members of my immediate household or family, own securities of: None. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

Imagine that you own a small, 20-acre farm in California’s Central Valley. You and your family have cultivated this land for decades, but drought, increasing costs and decreasing water availability are making each year more difficult.

Now imagine that a solar-electricity developer approaches you and presents three options:

You can lease the developer 10 acres of otherwise productive cropland, on which the developer will build an array of solar panels and sell electricity to the local power company.

You can select 1 or 2 acres of your land on which to build and operate your own solar array, using some electricity for your farm and selling the rest to the utility.

Or you can keep going as you have been, hoping your farm can somehow survive.

Thousands of farmers across the country, including in the Central Valley, are choosing one of the first two options. A 2022 survey by the U.S. Department of Agriculture found that roughly 117,000 U.S. farm operations have some type of solar device. Our own work has identified over 6,500 solar arrays currently located on U.S. farmland.

Our study of nearly 1,000 solar arrays built on 10,000 acres of the Central Valley over the past two decades found that solar power and farming are complementing each other in farmers’ business operations. As a result, farmers are making and saving more money while using less water – helping them keep their land and livelihood.

A hotter, drier and more built-up future

Perhaps nowhere in the U.S. is farmland more valuable or more productive than California’s Central Valley. The region grows a vast array of crops, including nearly all of the nation’s production of almonds, olives and sweet rice. Using less than 1% of all farmland in the country, the Central Valley supplies a quarter of the nation’s food, including 40% of its fruits, nuts and other fresh foods.

The food, fuel and fiber that these farms produce are a bedrock of the nation’s economy, food system and way of life.

But decades of intense cultivation, urban development and climate change are squeezing farmers. Water is limited, and getting more so: A state law passed in 2014 requires farmers to further reduce their water usage by the mid-2040s.

The trade-offs of installing solar on agricultural land

When the solar arrays we studied were installed, California state solar energy policy and incentives gave farm landowners new ways to diversify their income by either leasing their land for solar arrays or building their own.