By JustMarkets

At the end of Tuesday, the Dow Jones Index (US30) rose by 0.91%. The S&P 500 Index (US500) fell by 0.11%. The Nasdaq (US100) Tech Index closed down 0.82%. The US stocks closed mixed on Tuesday after the Senate passed President Trump’s massive budget bill, while investors also kept an eye on trade developments. Enthusiasm about potential economic stimulus was tempered by concerns about the bill’s multi-trillion-dollar cost. The bill is projected to increase the national debt by $3.3 trillion. Tesla fell by 5.3% after Trump escalated his feud with Elon Musk, threatening to strip him of federal subsidies. Fed Chairman Jerome Powell maintained a cautious tone on rate cuts, noting tariff-related inflation risks and emphasizing the need for additional data.

European stock markets were mostly lower on Tuesday. Germany’s DAX (DE40) fell by 0.99%, France’s CAC 40 (FR40) closed down 0.04%, the Spanish IBEX35 (ES35) Index fell by 0.03%, and the British FTSE 100 (UK100) closed positive 0.28%. European stocks fell on Tuesday amid trade uncertainty and doubts that the ECB will continue to cut interest rates. According to reports, the EU is open to a deal that would impose a 10% universal tariff on many types of exports, but is demanding concessions from the US in key sectors such as pharmaceuticals, alcohol, semiconductors, and commercial aircraft. The head of the EU trade department is expected to lead a delegation to Washington this week to try to advance the negotiations. On the data front, preliminary figures showed the Eurozone inflation at 2%, as expected, and in line with the ECB’s target. Meanwhile, ECB chief economist Philip Lane said the recent cycle of Central Bank policy tightening was over.

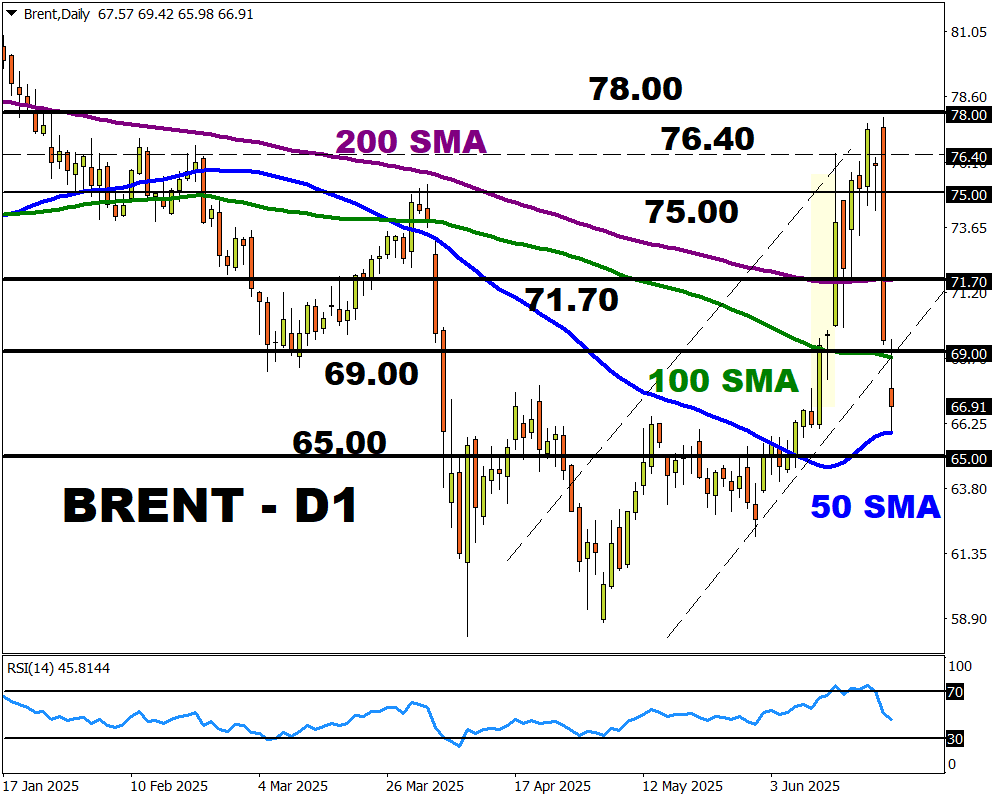

WTI oil prices are holding steady at around $65 per barrel on Wednesday after rising in the previous session, as investors remain cautious ahead of OPEC+’s production decision. The group intends to increase production by 411,000 barrels per day in August, resulting in a total increase in production in 2025 of 1.78 million barrels per day — more than 1.5% of global demand. This move is seen both as a punishment for overproducers and as an attempt by Saudi Arabia to win market share from US shale fields and other countries.

Asian markets were mostly down yesterday. Japan’s Nikkei 225 (JP225) fell by 1.24%, China’s FTSE China A50 (CHA50) rose by 0.25%, Hong Kong’s Hang Seng (HK50) did not trade yesterday, and Australia’s ASX 200 (AU200) showed a negative result of 0.01%.

The Nikkei 225 (JP225) Index fell by 1.1% on Wednesday, marking the second consecutive day of losses for Japanese stocks. The decline came after US President Donald Trump threatened to impose 35% tariffs on Japanese imports in an attempt to pressure Tokyo into making trade concessions. Trump called negotiations with Japan “very tough,” repeating his criticism of the country’s unwillingness to accept American-made cars and rice. His comments heightened investor concerns, especially after Federal Reserve Chairman Jerome Powell said the Fed would have already cut interest rates if not for the inflationary impact of Trump’s tariffs.

On Wednesday, the New Zealand dollar traded around US$0.609, close to its highest level in more than eight months, helped by the general weakening of the US dollar. Meanwhile, investors are closely watching trade developments as many countries try to reach an agreement with the US before the July 9 deadline. In the domestic market, the Reserve Bank of New Zealand is expected to keep rates at 3.25% next week, with market prices indicating only a small chance of a 25 basis point cut.

The Australian dollar weakened to $0.656 on Wednesday, retreating from the previous session as weaker-than-expected domestic data dampened investor sentiment. The Australian Bureau of Statistics reported that retail sales rose 0.2% in May, higher than the revised April figure but below market expectations of 0.4% growth. The data reinforced expectations that the Reserve Bank of Australia will cut rates by 25 basis points to 3.60%, with markets increasingly pricing in the possibility of further easing in the second half of the year, which could see rates fall to 3.10% or even 2.85%.

S&P 500 (US500) 6,198.01 −6.94 (−0.11%)

Dow Jones (US30) 44,494.94 +400.17 (+0.91%)

DAX (DE40) 23,673.29 −236.32 (−0.99%)

FTSE 100 (UK100) 8,785.33 +24.37 (+0.28%)

USD Index 96.66 −0.21 (−0.22%)

News feed for: 2025.07.02

- Australia Retail Sales (m/m) at 04:30 (GMT+3);

- Eurozone Unemployment Rate (m/m) at 12:00 (GMT+3);

- US ADP Nonfarm Employment Change (m/m) at 15:15 (GMT+3);

- Canada Manufacturing PMI (m/m) at 16:30 (GMT+3);

- Eurozone ECB President Lagarde Speaks at 17:15 (GMT+3);

- US Crude Oil Reserves (w/w) at 17:30 (GMT+3).

By JustMarkets

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.