By JustMarkets

On Wednesday, the US stock indices closed in the red. By the end of the day, the Dow Jones Index (US30) fell by 1.63%. The S&P 500 Index (US500) declined by 1.36%. The Technology Index NASDAQ (US100) closed lower by 1.46%. The FOMC’s decision to keep interest rates in the 3.5-3.75% range was accompanied by a “hawkish” comment about serious pro‑inflationary risks caused by the war in Iran and the threat of new tariffs. The regulator’s concerns were confirmed by the aggressively high industrial inflation (PPI) figure published earlier the same day, which led most committee members to rule out the possibility of rate cuts this year. Investors reacted by pushing Treasury yields higher, which put pressure on all market sectors. The worst performance came from the financial sector and consumer staples: payment system giants Visa and Mastercard plunged 3.1% and 3.7%, respectively, while retailers Walmart and B&G lost more than 2.5% amid fears of declining consumer purchasing power due to high energy costs.

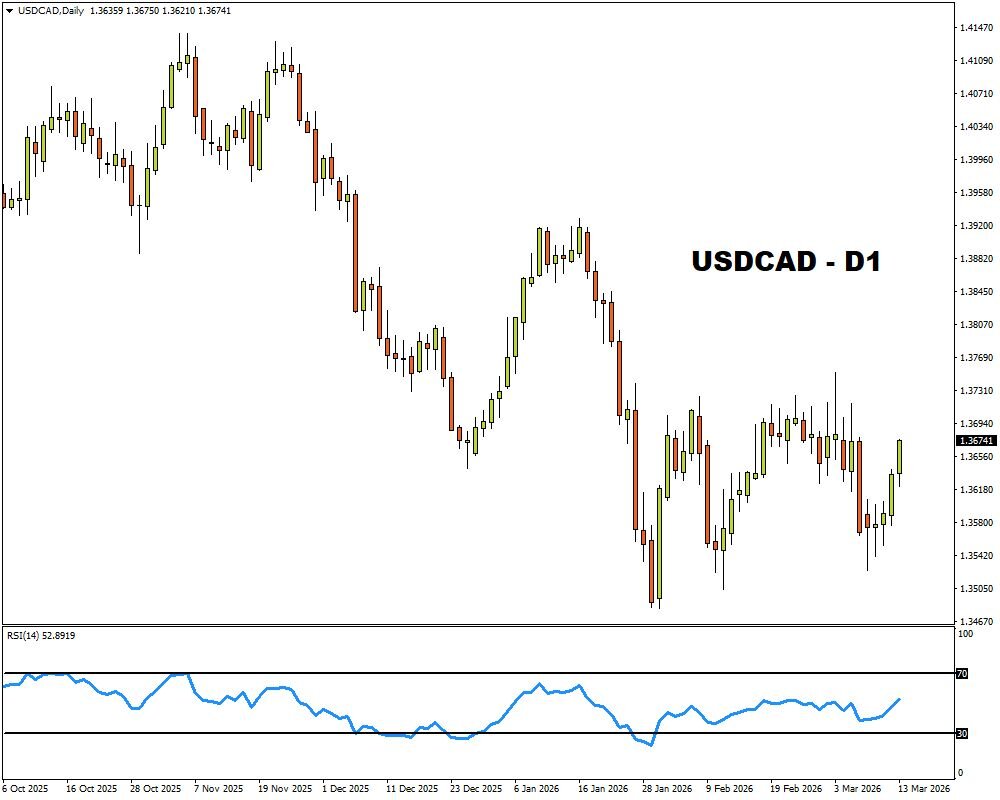

The Canadian dollar (CAD) fell to 1.37 per US dollar, reaching its lowest level in the past two months. In March, the BoC predictably kept its key rate unchanged, synchronizing its actions with the US Fed’s “hawkish pause.” The regulator emphasized that the war with Iran creates two‑sided risks: on one hand, it triggers an inflationary shock through fuel prices; on the other, it threatens to slow global economic growth. With the Strait of Hormuz paralyzed, the Canadian dollar remains in a unique “safe haven” position among commodity currencies, but its further recovery toward 1.35 will depend directly on whether the commodity factor outweighs Washington’s tight monetary policy in the coming weeks.

European markets showed a decline. Germany’s DAX (DE40) fell by 0.96%, France’s CAC 40 (FR40) closed slightly higher at 0.06%, Spain’s IBEX 35 (ES35) rose by 0.29%, and the UK’s FTSE 100 (UK100) closed down 0.94%. The main pressure factor was another spike in natural gas prices caused by the escalation in the Persian Gulf. Given that the Fed has already confirmed its “hawkish” stance, tomorrow’s meetings of European regulators will be a moment of truth: will they acknowledge the inevitability of a prolonged period of high rates due to the energy crisis, or will they attempt to soften their rhetoric to support fading economic growth?

Silver prices (XAG) fell to $76.9 per ounce, pressured by the Fed’s updated expectations. The FOMC’s decision to keep rates unchanged and project only one rate cut this year sharply increased the alternative cost of holding the metal. Investors were particularly alarmed by the upward revision of the core PCE inflation prediction: the regulator made it clear that it is prepared to stick to a “higher for longer” policy to contain the consequences of the structural energy shock caused by the blockade of the Strait of Hormuz and strikes on Iranian oil fields.

WTI crude oil showed a sharp intraday reversal, rising above $97.3 per barrel amid a critical escalation in the Persian Gulf. Reports of strikes on Iran’s gas giant South Pars and the death of Iran’s intelligence minister Esmail Khatib outweighed all attempts by Washington to stabilize the market, including the temporary suspension of the Jones Act and a 6.2‑million‑barrel increase in US commercial crude inventories. Even the Fed’s “hawkish” decision to keep rates in the 3.5-3.75% range only briefly cooled the bulls, as the effective blockade of the Strait of Hormuz created a structural deficit that cannot be quickly offset by strategic reserves or increased domestic refining.

Asian markets mostly rose yesterday. Japan’s Nikkei 225 (JP225) gained 2.87%, China’s FTSE China A50 (CHA50) jumped 0.14%, Hong Kong’s Hang Seng (HK50) rose by 0.61%, and Australia’s ASX 200 (AU200) posted a positive result of 0.31%.

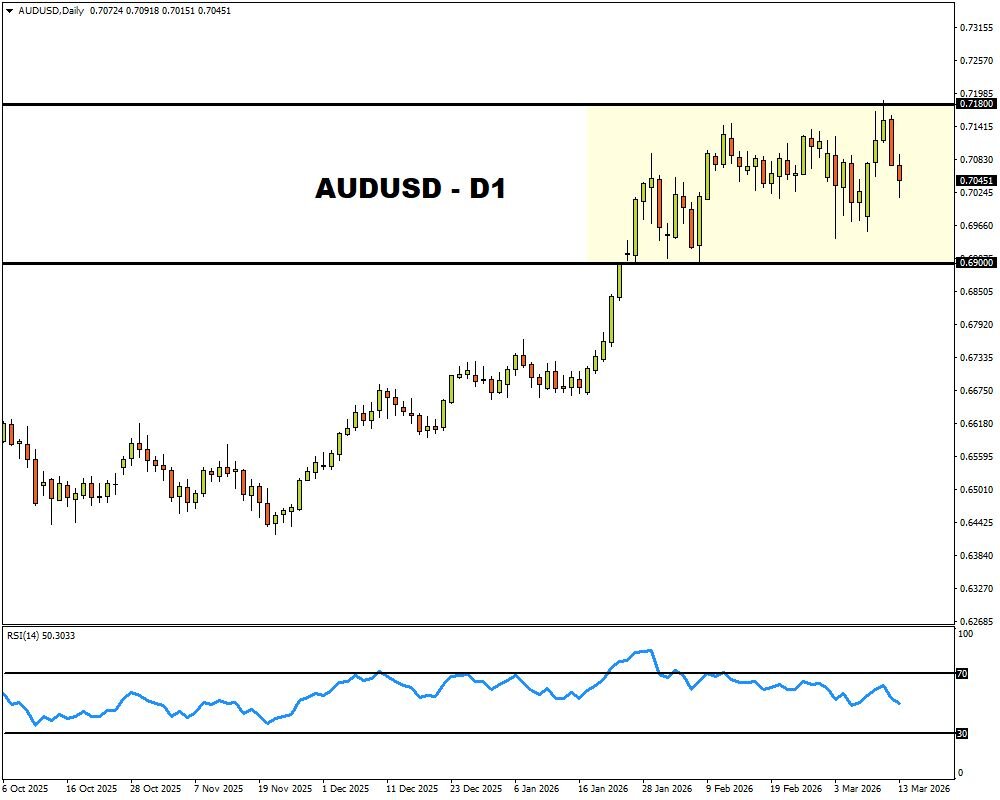

On Thursday, the Australian dollar (AUD) showed a corrective rise to 0.704 per US dollar, recovering part of its losses after yesterday’s decline. The fresh labor market report presented investors with a mixed but generally constructive picture: an explosive increase in employment by 48,900 (vs. the prognosis of 20,000) confirmed the economy’s strong resilience, but an unexpected rise in the unemployment rate to 4.3% slightly cooled the hawks’ enthusiasm. Nevertheless, the RBA still considers the labor market historically strong, leaving the door open for further policy tightening.

The New Zealand dollar (NZD) exhibited volatility. Investors faced conflicting signals: extremely weak GDP data for the December quarter (growth of only 0.2% vs. the expected 0.4%) point to economic fragility, while inflationary risks due to the war in Iran are forcing the market to revise rate anticipation. Although annual GDP growth reached 1.3%, it fell short of the target 1.7%, confirming that domestic consumption in New Zealand remains subdued.

S&P 500 (US500) 6,624.70 −91.39 (−1.36%)

Dow Jones (US30) 46,225.15 −768.11 (−1.63%)

DAX (DE40) 23,502.25 −228.67 (−0.96%)

FTSE 100 (UK100) 10,305.29 −98.31 (−0.94%)

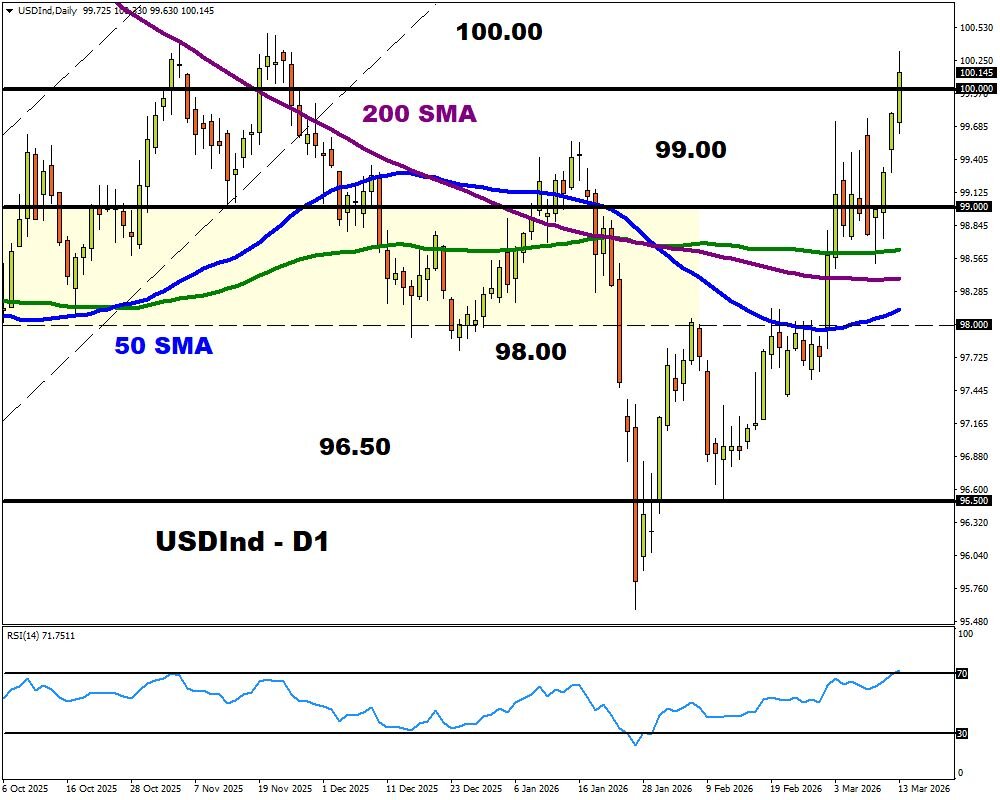

USD Index 100.26 +0.68% (+0.68%)

News feed for: 2026.03.19

- Australia Unemployment Rate (m/m) at 02:30 (GMT+2); – AUD (MED)

- Japan BoJ Policy Rate at 05:00 (GMT+2); – JPY (HIGH)

- Japan BoJ Press Conference at 06:30 (GMT+2); – JPY (HIGH)

- Switzerland Trade Balance (m/m) at 09:00 (GMT+2); – CHF (LOW)

- UK Claimant Count Change (m/m) at 09:00 (GMT+2); – GBP (MED)

- UK Average Earnings Index (m/m) at 09:00 (GMT+2); – GBP (MED)

- UK Unemployment Rate (m/m) at 09:00 (GMT+2); – GBP (MED)

- Sweden Riksbank Rate Decision at 10:30 (GMT+2); – SEK (HIGH)

- Switzerland SNB Policy Rate at 10:30 (GMT+2); – CHF (HIGH)

- Switzerland SNB Press Conference at 11:00 (GMT+2); – CHF (HIGH)

- UK BoE Official Bank Rate at 14:00 (GMT+2); – GBP (HIGH)

- UK BoE Press Conference at 14:30 (GMT+2); – GBP (HIGH)

- US Initial Jobless Claims (w/w) at 14:30 (GMT+2); – USD (MED)

- Eurozone ECB Interest Rate Decision at 15:15 (GMT+2); – EUR (HIGH)

- Eurozone ECB Press Conference at 15:45 (GMT+2); – EUR (HIGH)

- US New Home Sales (m/m) at 16:00 (GMT+2); – USD (MED)

- US Natural Gas Reserves (w/w) at 16:30 (GMT+2); – XNG (HIGH)

- New Zealand Trade Balance (q/q) at 23:45 (GMT+2). – NZD (MED)

By JustMarkets

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

A mechanical claw holds a polymetallic nodule, one of several seafloor sources of critical minerals.

A mechanical claw holds a polymetallic nodule, one of several seafloor sources of critical minerals.

{kind=link}